Transcatheter Heart Valve Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

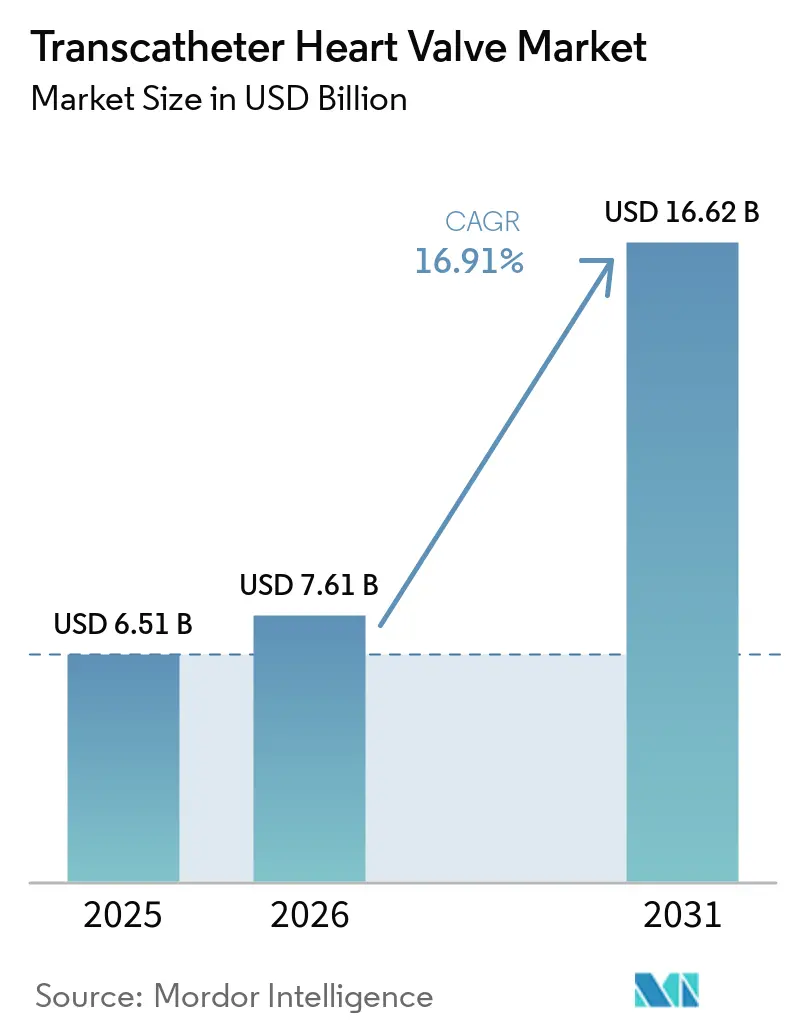

| Market Size (2026) | USD 7.61 Billion |

| Market Size (2031) | USD 16.62 Billion |

| Growth Rate (2026 - 2031) | 16.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transcatheter Heart Valve Market Analysis by Mordor Intelligence

The Transcatheter Heart Valve Market size was valued at USD 6.51 billion in 2025 and is estimated to grow from USD 7.61 billion in 2026 to reach USD 16.62 billion by 2031, at a CAGR of 16.91% during the forecast period (2026-2031).

Stronger long-term clinical evidence is driving the transcatheter heart valve market, particularly for less invasive valve replacements in severe aortic stenosis. Notably, 7-year low-risk data continues to support the transcatheter approach alongside traditional surgery. The market is also expanding with new approvals in mitral and tricuspid therapies, broadening treatment options for patient groups previously limited in alternatives. Product innovation remains critical, as durability, repositionability, and coronary re-access are key to building physician confidence, especially for younger and more complex patients. Recent advancements in valve platforms are addressing these priorities directly.

Key Report Takeaways

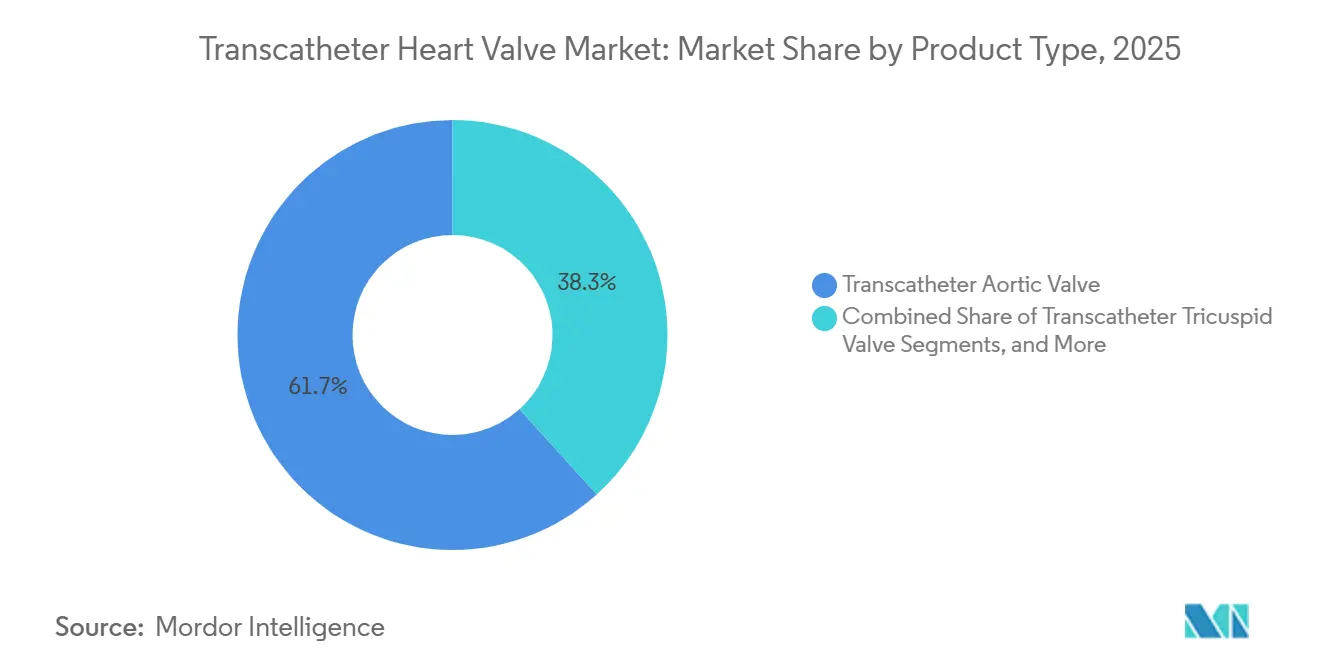

- By product type, transcatheter aortic valves led with 61.67% share in 2025, while transcatheter mitral valves are forecast to expand at an 18.90% CAGR through 2031.

- By valve technology, self-expandable valves held 63.91% share in 2025, while balloon-expandable valves recorded the highest projected CAGR at 19.25% through 2031.

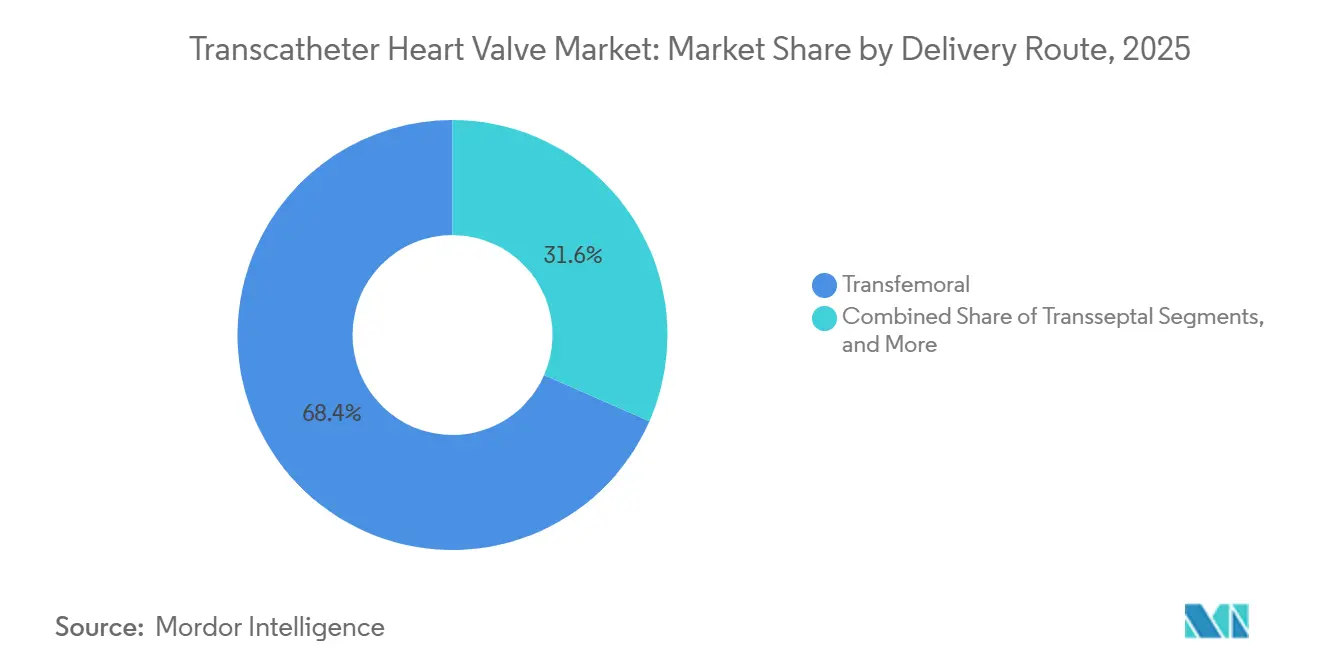

- By delivery route, transfemoral systems accounted for 68.45% share in 2025, while transseptal delivery is projected to grow at a 18.55% CAGR through 2031.

- By end user, hospitals captured 71.22% share in 2025, while ambulatory surgical centers are projected to grow at a 17.33% CAGR through 2031.

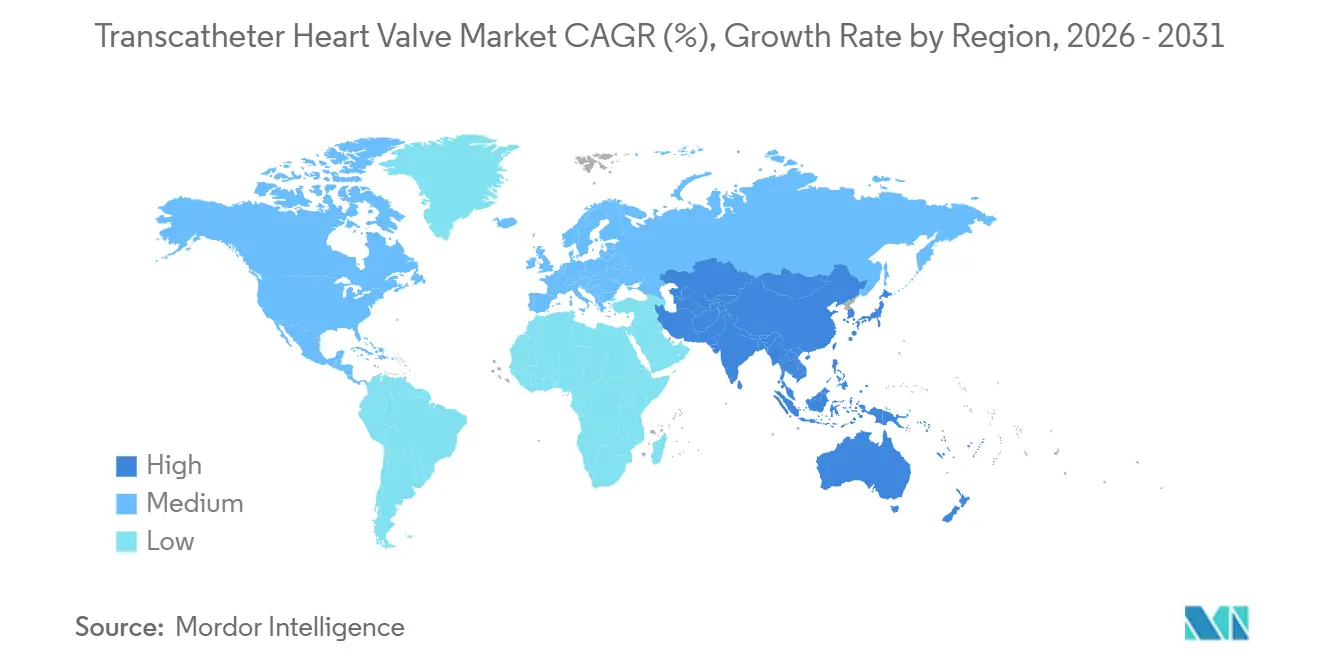

- By geography, North America held 42.55% share in 2025, while Asia-Pacific posted the highest projected CAGR at 19.22% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Transcatheter Heart Valve Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging population and rising severe aortic stenosis burden | +2.8% | Global, concentrated in North America, EU, Japan | Long term (≥ 4 years) |

| Expansion into lower-risk patient populations | +3.2% | North America, Western Europe, early gains in Australia and South Korea | Medium term (2-4 years) |

| One-step pathway from diagnosis to intervention through multidisciplinary heart teams | +1.5% | North America, Germany, United Kingdom, France | Medium term (2-4 years) |

| Next-generation valve durability, repositionability, and coronary access innovation | +2.0% | Global, with early gains in US and EU5 | Long term (≥ 4 years) |

| Earlier intervention enabled by trial evidence and label expansion | +2.5% | North America, Europe | Short term (≤ 2 years) |

| Hospital economics favoring shorter length of stay and reduced procedural costs | +1.3% | North America, APAC core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Severe Aortic Stenosis Burden

The transcatheter heart valve market benefits from the increasing prevalence of severe aortic stenosis in aging populations, as disease incidence rises sharply with age, driving procedural demand. Clinical discussions have progressed beyond safety, with findings from the 7-year PARTNER 3 follow-up showing no significant difference in all-cause mortality or disabling stroke between transcatheter and surgical valve replacements in low-risk patients. This supports earlier referrals, enhances physician confidence, and emphasizes timely treatment to prevent complex and costly conditions. National registry systems in countries with organized cardiac tracking further accelerate clinical adoption by providing hospitals and payers with clear outcome evidence. The market is thus supported by aging demographics and a more assured treatment pathway for severe valve diseases.

Expansion Into Lower-Risk Patient Populations

The transcatheter heart valve market is expanding as treatments extend to lower-risk groups beyond high-risk surgical candidates. A 2025 meta-analysis highlighted that younger, low-risk patients undergoing transcatheter aortic valve replacement (TAVR) achieved comparable outcomes in terms of death or disabling stroke compared to surgery, along with improvements in functional class and quality of life. The 5-year Evolut Low Risk results reported 15.5% all-cause mortality for TAVR and 16.4% for surgery, reducing resistance to broader TAVR use.[1]New England Journal of Medicine, “Transcatheter or Surgical Aortic-Valve Replacement in Low-Risk Patients at 7 Years,” New England Journal of Medicine, nejm.org This evidence not only shifts volume from surgery to catheter-based care but also broadens the patient pool, enabling earlier interventions and driving market growth.

Next-Generation Valve Durability, Repositionability, and Coronary Access Innovation

The transcatheter heart valve market is advancing as manufacturers address concerns like long-term durability and future intervention feasibility. Edwards Lifesciences presented 10-year data from the COMMENCE aortic trial in 2026, demonstrating durable performance of its RESILIA tissue platform across over 500,000 patients globally. Anteris Technologies advanced coronary re-access and lifetime valve management with FDA clearance for the IDE of the PARADIGM global pivotal trial in 2025, introducing a biomimetic balloon-expandable design. These innovations focus on improving long-term outcomes, reducing physician hesitation, and expanding treatment to younger demographics.

Earlier Intervention Enabled by Trial Evidence and Label Expansion

The transcatheter heart valve market is growing due to evidence supporting earlier treatment across more valve positions. ACC 2025 data showed minimal outcome differences between transcatheter therapy and surgery at 5 years for low-risk severe aortic stenosis, encouraging earlier consideration of catheter-based treatments.[2]Frontiers in Cardiovascular Medicine, “Outcomes of Transcatheter Aortic Valve Replacement in Younger Low-Risk Patients, A Comprehensive Meta-Analysis of Efficacy and Safety,” Frontiers in Cardiovascular Medicine, frontiersin.org The FDA approved Edwards Lifesciences’ SAPIEN M3 in 2025 for patients with moderate-to-severe mitral regurgitation unsuitable for surgery. Additionally, Edwards reported 2-year TRISCEND II data in 2026, highlighting sustained benefits and reduced mortality for the EVOQUE tricuspid valve replacement system. These developments enhance confidence in aortic, mitral, and tricuspid treatment pathways, driving market growth through broader labels, improved outcomes, and a larger patient base.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Lifetime management concerns in younger patients | -2.2% | North America, EU, Australia, South Korea | Long term (≥ 4 years) |

| Anatomical complexity in native aortic regurgitation, mitral, and tricuspid positions | -1.8% | Global, most acute in emerging markets with limited imaging infrastructure | Medium term (2-4 years) |

| Reimbursement and coverage variability across healthcare systems | -2.5% | APAC ex-Japan, MEA, South America | Medium term (2-4 years) |

| High capital, imaging, and structural heart program costs | -1.9% | APAC developing markets, MEA, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lifetime Management Concerns in Younger Patients

The transcatheter heart valve market faces limitations in younger patients due to unresolved lifetime management challenges after the initial implant. In 2025, the Society of Thoracic Surgeons recommended surgical aortic valve replacement as the preferred option for younger patients, especially when surgery ensures low morbidity and better planning for future interventions.[3]Society of Thoracic Surgeons, “Too Young for TAVI? Prioritizing Evidence Over Age,” Society of Thoracic Surgeons, sts.org This highlights concerns that patients in their mid-60s may outlive the current evidence available for many modern devices. Additionally, valve-in-valve procedures complicate coronary access and future reinterventions after the first prosthesis placement. Despite advancements, conservative heart teams are expected to prioritize age, anatomy, and long-term reintervention strategies, slowing the adoption of transcatheter heart valves among younger patients.

Reimbursement and Coverage Variability Across Healthcare Systems

The transcatheter heart valve market's growth is uneven globally due to the impact of coverage policies on procedure volumes. In the U.S., CMS ties TAVR reimbursement to specific coverage conditions and registry participation, restricting access to approved care settings and certified centers. In China, domestic approvals like MicroPort’s VitaFlow Liberty Flex enhance cost accessibility and local availability, but reimbursement adoption depends on payer and system-level acceptance after regulatory clearance. Emerging markets face additional challenges, as establishing hybrid operating rooms, imaging systems, and structural heart teams requires significant upfront investment. This delays market expansion in regions with high patient demand, as funding, training, and infrastructure development often lag. The market grows fastest where regulation, payment, and hospital capabilities align effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aortic Valve Dominance Meets a Mitral Inflection Point

In 2025, transcatheter aortic valves held 61.67% of the transcatheter heart valve market, reflecting their strong position driven by a robust clinical history, physician familiarity, and established TAVR protocols for severe aortic stenosis. The aortic segment benefits from intense competition among leading platforms, fostering innovation and procedural confidence in advanced cardiac centers. Pulmonary and tricuspid products, though smaller in revenue, address critical patient needs previously underserved by surgical options. Edwards strengthened the tricuspid segment in March 2026 with 2-year TRISCEND II data showing sustained patient benefits and reduced mortality for the EVOQUE system, supporting broader physician adoption.

Transcatheter mitral valves are projected to grow at an 18.90% CAGR through 2031, marking a significant growth area in the transcatheter heart valve market. Abbott’s FDA approval for Tendyne in May 2025 introduced a minimally invasive mitral replacement for patients lacking surgical options. Edwards followed with FDA approval for SAPIEN M3 in December 2025, offering a transseptal treatment for moderate-to-severe mitral regurgitation in non-surgical candidates.

By Valve Technology: Balloon-Expandable Platforms Challenge Self-Expandable Incumbency

Self-expandable valves led the market with a 63.91% share in 2025, driven by Medtronic’s Evolut platform and Abbott’s Navitor system. Their appeal lies in a lower crossing profile and adaptability to challenging anatomies, supported by years of operator experience. However, the focus is shifting toward long-term performance over initial convenience. Edwards reported a slight improvement in its global TAVR position in Q1 2026, partly due to discussions around Medtronic’s Evolut reintervention profile.

Balloon-expandable valves are expected to grow at a 19.25% CAGR through 2031, signaling a shift in market dynamics. This growth is fueled by Edwards’ SAPIEN franchise and next-generation designs mimicking native valve behavior. Anteris Technologies entered the market with DurAVR, and the FDA approved the PARADIGM global pivotal trial in November 2025. The platform addresses durability and hemodynamic concerns, driving physician preference. The market is evolving from platform familiarity to long-term valve performance and structural durability.

By Delivery Route: Transfemoral Maturity and Transseptal Emergence

The transfemoral route accounted for 68.45% of the market in 2025, maintaining its position as the standard access path. Its dominance is attributed to refined workflows, including minimalist TAVR protocols that reduce anesthesia reliance and recovery time. A 2025 study highlighted the safety and feasibility of direct ward returns post-TAVR, emphasizing operational efficiencies. Transapical and transjugular approaches remain relevant for patients with challenging femoral access but play a narrower role as femoral-first programs become standardized.

Transseptal delivery is the fastest-growing route, with an 18.55% CAGR projected through 2031, driven by the expansion of mitral therapy. Edwards’ CE Mark approval for SAPIEN M3 in April 2025 marked a milestone for transseptal access, which enables left-heart treatment via the femoral vein without thoracotomy. This approach is particularly valuable for patients unsuitable for open surgery. As centers integrate mitral programs with TAVR teams, they leverage existing expertise and resources, ensuring sustainable growth in structural heart services.

By End User: Hospitals Lead as Specialty Cardiac Centres Scale

Hospitals held a 71.22% market share in 2025, remaining the primary revenue source in the transcatheter heart valve market. CMS classifies TAVR as an inpatient procedure under its National Coverage Determination, reinforcing the role of large hospital systems in delivery and reimbursement. Hospitals also provide essential infrastructure, including imaging systems, hybrid rooms, and multidisciplinary teams, making them indispensable even as procedures become less invasive. Specialty cardiac centers within hospital networks are gaining prominence, offering standardized workflows and enhanced quality oversight.

Ambulatory surgical centers are projected to grow at a 17.33% CAGR through 2031, though their role in the market is currently more visible in adjacent cardiovascular care than in core TAVR. Policy constraints, such as CMS’s inpatient classification for TAVR, limit their immediate impact. However, investments in cardiovascular outpatient models are increasing. For instance, ChristianaCare and Atlas Healthcare Partners announced a joint venture in April 2026 to establish a cardiovascular ambulatory surgery center in Delaware. While hospitals remain dominant, these centers may gradually integrate into the broader referral and recovery ecosystem as simpler procedures shift outward.

Geography Analysis

In 2025, North America accounted for 42.55% of the transcatheter heart valve market, maintaining its position as the largest regional contributor. The region benefits from mature reimbursement systems, a strong interventional cardiology base, and an extensive network of advanced cardiac centers. The U.S. remains pivotal, with coverage and registry requirements concentrating treatments within highly capable hospital systems.

Europe continues to be a stable contributor to the transcatheter heart valve market, supported by consistent reimbursement policies in Germany, France, the U.K., Italy, and Spain, along with a solid base of structural heart programs. Years of physician expertise in TAVR have ensured mature and standardized procedural pathways. Larger manufacturers hold an advantage due to their ability to manage regulatory and compliance demands effectively, ensuring supply continuity and market coverage. Despite slower growth compared to newer adoption regions, Europe remains a reliable volume base.

Asia-Pacific is projected to grow at a 19.22% CAGR through 2031, marking the fastest expansion in the transcatheter heart valve market. China's improving domestic approvals are enhancing product availability and affordability for hospitals. MicroPort’s VitaFlow Liberty Flex received NMPA approval in January 2025, and Genesis MedTech’s J-VALVE TF, the first transfemoral TAVR system for aortic regurgitation in China, was approved in September 2025. Japan's national health insurance supports procedural access, while South Korea is expanding structural heart capacity through a broader network of centers.

Competitive Landscape

In the transcatheter heart valve market, aortic valve replacement sees moderate consolidation, predominantly influenced by Major players includes Edwards Lifesciences Corporation, Abbott Laboratories, JenaValve Technology, Inc., Boston Scientific Corporation, and Medtronic plc., who command a significant share of global procedural activities. In contrast, the landscape is more fragmented for mitral, tricuspid, and pulmonary therapies, where competitive benchmarks are still evolving, and no single entity dominates. Thus, the transcatheter heart valve market melds a robust core of incumbents with emerging niches where being a first-mover holds significant weight.

Leading firms in the transcatheter heart valve arena are broadening their portfolios, moving beyond merely defending individual product lines. Abbott, in May 2025, secured FDA approval for Tendyne, enabling a minimally invasive mitral replacement in a previously limited segment. Edwards followed with FDA approval for SAPIEN M3 in December 2025 and strengthened its tricuspid position with 2-year EVOQUE data in March 2026, signaling a concerted push across various valve positions, not just aortic therapy. Meanwhile, in China, MicroPort and Genesis MedTech are leveraging local approvals to enhance their domestic presence, particularly in response to pricing and disease pattern differences from Western markets. These moves highlight a market shift toward broader portfolios, local relevance, and clinical growth across multiple valve positions.

Emerging players are reshaping the transcatheter heart valve landscape, prioritizing long-term performance over short-term trends. Anteris Technologies, in November 2025, received FDA IDE approval for the PARADIGM trial, positioning DurAVR in direct competition with established valves and creating a significant clinical pathway. Similarly, TRiCares, in April 2026, gained FDA IDE approval for the TRICURE pivotal trial of the Topaz transcatheter tricuspid valve replacement system, spanning up to 75 investigative sites. This competitive dynamic underscores the market's focus on clinical validation, regulatory execution, and long-term valve management, particularly in areas lacking a standard care protocol.

Transcatheter Heart Valve Industry Leaders

Edwards Lifesciences Corporation

Abbott Laboratories

JenaValve Technology, Inc.

Boston Scientific Corporation

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Edwards Lifesciences presented 10-year data from the COMMENCE aortic trial at the AATS Annual Meeting, confirming the long-term durability of RESILIA tissue in over 500,000 patients and addressing valve degeneration concerns in younger TAVR patients.

- April 2026: TRiCares GmbH received FDA IDE approval for TRICURE, its pivotal trial evaluating the Topaz transcatheter tricuspid valve replacement system across 75 sites in the US, Canada, and Europe, entering the competitive tricuspid valve replacement trial market.

- March 2026: Edwards Lifesciences shared two-year TRISCEND II trial data for the EVOQUE tricuspid valve replacement system at ACC.26, demonstrating sustained patient benefits and reduced mortality compared to medical therapy.

- December 2025: Edwards Lifesciences received FDA approval for the SAPIEN M3 mitral valve replacement system, the first transcatheter therapy using a transseptal approach, with ENCIRCLE trial data showing 95.7% MR elimination in 299 patients.

- November 2025: Anteris Technologies received FDA IDE approval for the PARADIGM global pivotal trial, comparing DurAVR with SAPIEN and Evolut valves in severe calcific aortic stenosis, enabling the first randomized controlled trial for a biomimetic transcatheter aortic valve.

Global Transcatheter Heart Valve Market Report Scope

As per the scope of the report, a transcatheter heart valve is an artificial heart valve that doctors put into a patient using a small tube called a catheter. It treats a damaged heart valve without doing open-heart surgery.

The transcatheter heart valve market is segmented by product type, valve technology, delivery route, end-user, and geography. By product type, the market includes transcatheter aortic valve, transcatheter mitral valve, transcatheter tricuspid valve, and transcatheter pulmonary valve. By valve technology, the market is segmented into balloon-expandable valves, self-expandable valves, and others. By delivery route, the market is categorized into transfemoral, transapical, transseptal, and transjugular. By end-user, the market is segmented into hospitals, ambulatory surgical centers, specialty cardiac centers, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Transcatheter Aortic Valve |

| Transcatheter Mitral Valve |

| Transcatheter Tricuspid Valve |

| Transcatheter Pulmonary Valve |

| Balloon-Expandable Valves |

| Self-Expandable Valves |

| Others |

| Transfemoral |

| Transapical |

| Transseptal |

| Transjugular |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Cardiac Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Transcatheter Aortic Valve | |

| Transcatheter Mitral Valve | ||

| Transcatheter Tricuspid Valve | ||

| Transcatheter Pulmonary Valve | ||

| By Valve Technology | Balloon-Expandable Valves | |

| Self-Expandable Valves | ||

| Others | ||

| By Delivery Route | Transfemoral | |

| Transapical | ||

| Transseptal | ||

| Transjugular | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Cardiac Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the transcatheter heart valve space by 2031?

The transcatheter heart valve market is projected to reach USD 16.62 billion by 2031, up from USD 7.61 billion in 2026, at a CAGR of 16.91%.

Which product category leads current revenue generation?

Transcatheter aortic valves led the product mix with 61.67% share in 2025, supported by the long clinical maturity of TAVR.

Which segment is expanding the fastest over the forecast period?

Transcatheter mitral valves are projected to grow at 18.90% CAGR through 2031, helped by FDA approvals for Tendyne and SAPIEN M3.

Why does North America remain the largest regional contributor?

North America held 42.55% share in 2025 because of mature reimbursement, strong hospital infrastructure, and continued commercial momentum from leading structural heart companies.

What is driving uptake in Asia-Pacific?

Asia-Pacific is forecast to grow at 19.22% CAGR through 2031, supported by domestic regulatory approvals in China, improving cost access, and broader structural heart capacity in major markets.

What is the main challenge slowing broader adoption in younger patients?

The biggest challenge is lifetime valve management, since physicians still weigh durability, coronary re-access, and future reintervention planning carefully in younger patients.

Page last updated on: