Hemostasis Valve Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

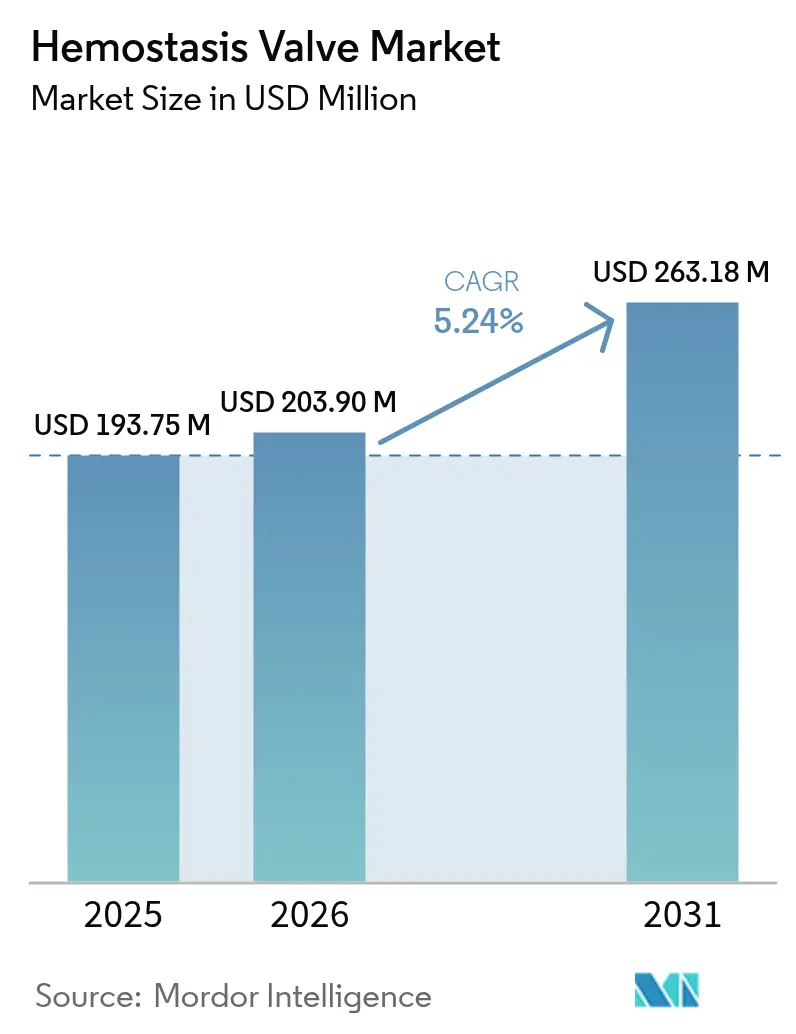

| Market Size (2026) | USD 203.9 Million |

| Market Size (2031) | USD 263.18 Million |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemostasis Valve Market Analysis by Mordor Intelligence

The hemostasis valve market size is expected to grow from USD 193.75 million in 2025 to USD 203.9 million in 2026 and is forecast to reach USD 263.18 million by 2031 at 5.24% CAGR over 2026-2031. Growth accompanies a 20.9% jump in interventional cardiology procedure volumes reported by Boston Scientific in Q1 2025, underscoring robust device utilization. The continuing transition from femoral to radial access drives demand for low-profile valves that maintain seal integrity with smaller French sizes. Product innovation now centers on single-handed operation and pressure-responsive “smart” valves able to relay real-time intraluminal pressure. Regulatory costs tied to EU-MDR re-certification and raw-material shortages of medical-grade silicone pose cost pressures, yet rising adoption of same-day discharge protocols in ambulatory settings offsets these hurdles through higher procedural throughput.

Key Report Takeaways

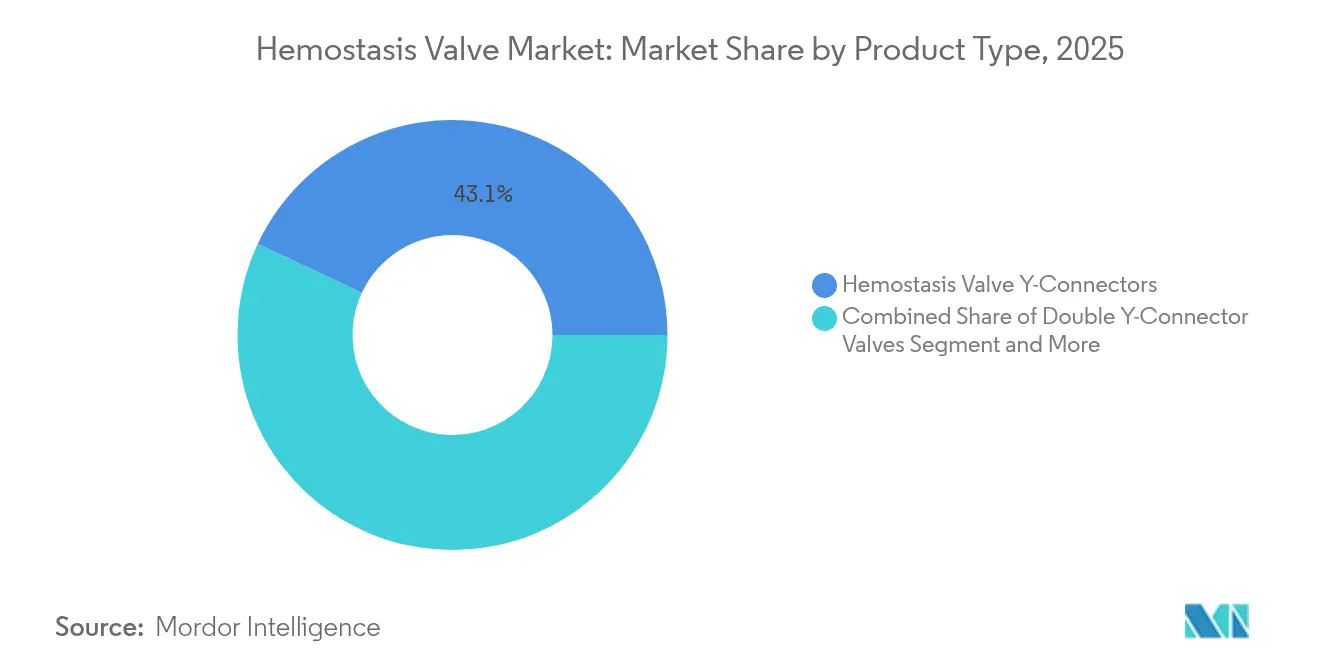

- By product type, hemostasis Valve Y-Connectors led with 43.05% of hemostasis valve market share in 2025; One-Handed Hemostasis Valves are forecast to expand at a 9.10% CAGR through 2031.

- By application, angiography captured 39.13% revenue share in 2025, while neuro-interventional procedures are advancing at a 10.56% CAGR to 2031.

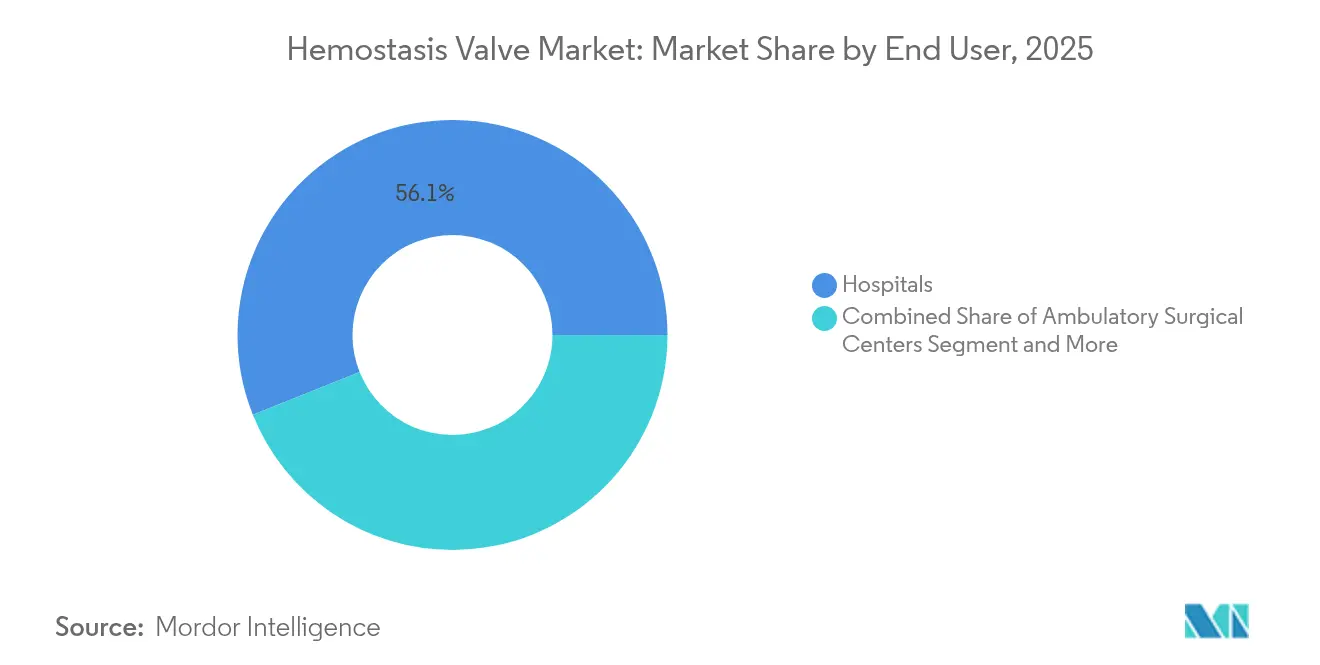

- By end user, hospitals held 56.05% of the hemostasis valve market size in 2025; ambulatory surgical centers record the fastest growth at 8.38% CAGR through 2031.

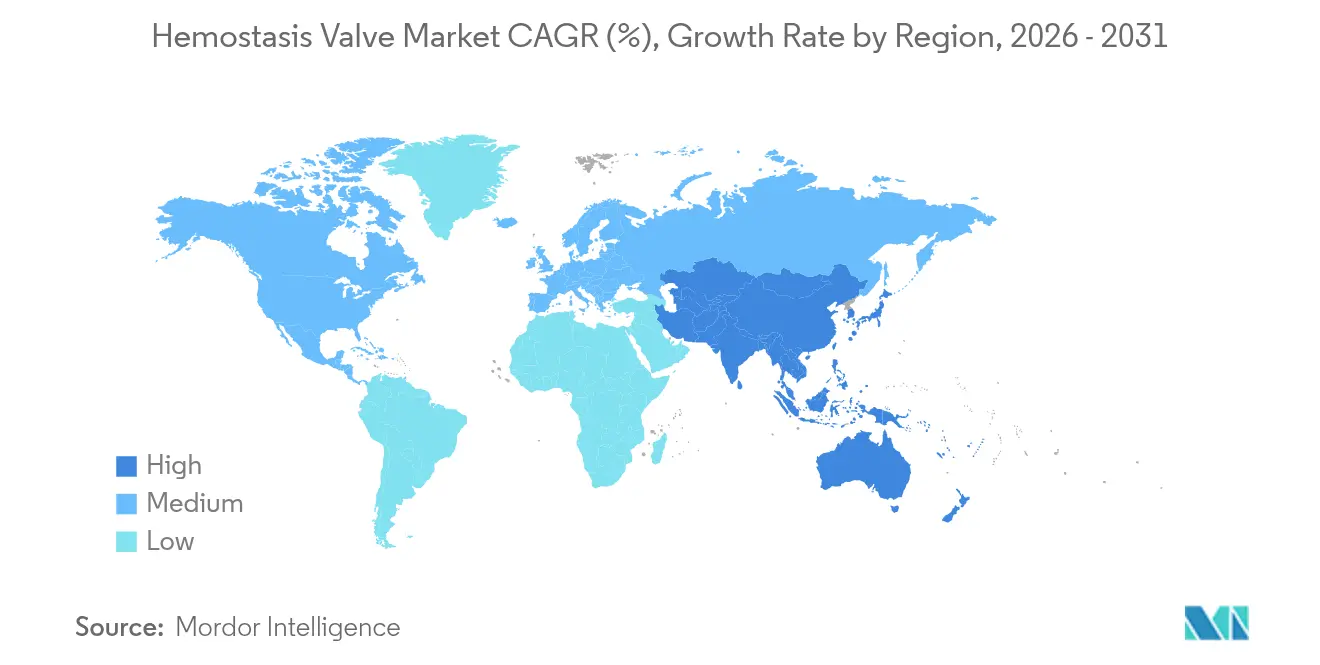

- By geography, North America accounted for 37.55% revenue share in 2025, yet Asia-Pacific is set to rise at an 8.18% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hemostasis Valve Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging volume of interventional cardiology & radiology procedures | +1.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Rising global burden of cardiovascular & chronic metabolic diseases | +1.2% | Global, highest in Asia-Pacific & emerging markets | Long term (≥ 4 years) |

| Growing adoption of minimally-invasive endovascular surgeries | +1.0% | North America & EU leading, Asia-Pacific following | Medium term (2-4 years) |

| Rapid shift to radial access & lower-French devices | +0.8% | Global, accelerated in developed markets | Short term (≤ 2 years) |

| Proliferation of day-case cath-labs in emerging economies | +0.6% | Asia-Pacific core, spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Commercialization of pressure-responsive “smart” valves | +0.4% | North America & EU early adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Volume of Interventional Cardiology & Radiology Procedures

Q1 2025 results showed a 20.9% year-over-year sales rise for Boston Scientific attributable to higher catheterization activity[1]Boston Scientific, “Boston Scientific Announces Results for First Quarter 2025,” news.bostonscientific.com. Complex procedures require multiple device exchanges, elevating the need for reliable hemostasis valves that minimize blood loss. Operators now favor premium seals for high-risk neuro-interventions, where middle meningeal artery embolization volumes could hit 79,483 cases by 2029. Increased procedure counts translate directly into recurring demand for disposable valves. In addition, supportive reimbursement schemes in the United States continue to reward radial access, sustaining device utilization. These factors collectively add 1.8 percentage points to the anticipated CAGR.

Rising Global Burden of Cardiovascular & Chronic Metabolic Diseases

Age-standardized ischemic heart disease prevalence remains high even as mortality declines, leading to more repeat interventions over a patient’s lifetime. Asia already records 722.45 heart-failure cases per 100,000 population, intensifying catheter-based therapy needs. A growing hypertensive population further drives electrophysiology volumes, pushing adoption of specialized hemostasis solutions. Procedure repetitions for chronic disease monitoring secure a durable growth runway. Lower-cost disposable kits aimed at emerging markets broaden access. The combined effect raises the growth trajectory by 1.2 percentage points.

Growing Adoption of Minimally-Invasive Endovascular Surgeries

Endovascular aneurysm repair now surpasses open surgery across many vascular centers, reducing recovery times yet increasing annual procedure counts per facility. Same-day discharge after transradial PCI saved up to USD 1,480 per patient in Trinidad and Tobago, illustrating the economic incentive for higher turnover. Robot-assisted vascular platforms add precision to these minimally invasive techniques, though capital cost slows adoption. Valves that maintain seal integrity during extended dwell times underpin this surgical shift. Broader procedural eligibility expands the addressable patient base, supporting a 1.0 percentage-point positive CAGR contribution.

Rapid Shift to Radial Access & Lower-French Devices

Radial access complications are minimal at 0.58%, compared with 3.71% for femoral approaches. The American Heart Association now endorses radial access for peripheral interventions, boosting operator confidence[2]American Heart Association, “Radial Access Approach to Peripheral Vascular Interventions,” ahajournals.org. However, radial artery occlusion remains a concern, prompting demand for valves compatible with lower French sizes that limit vessel trauma. Neuro-intervention’s fast embrace of distal radial routes reinforces this trend. The resulting preference for compact seals accelerates product substitution, adding 0.8 percentage points to CAGR expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operational complexity & supervision challenges in high-throughput cath-labs | -0.7% | Global, acute in high-volume centers | Short term (≤ 2 years) |

| Availability of alternative vascular closure technologies | -0.5% | North America & EU leading adoption | Medium term (2-4 years) |

| Volatile supply of medical-grade silicone & polycarbonate resins | -0.4% | Global manufacturing impact | Short term (≤ 2 years) |

| Cost escalation linked to EU-MDR Class IIb/III re-certification | -0.3% | EU primary impact, global compliance costs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Operational Complexity & Supervision Challenges in High-Throughput Cath-Labs

Physicians now execute more than 100 procedures each year, but case complexity climbs, raising staff fatigue and radiation exposure concerns. Workforce shortages oblige tailored education programs to sustain competencies. Real-time perception systems promise automation yet remain experimental. Maintaining diverse valve inventories for varied sheath sizes complicates logistics and can delay procedures. Collectively, these operational hurdles shave 0.7 percentage points off expected CAGR growth.

Availability of Alternative Vascular Closure Technologies

Devices such as MYNX CONTROL achieved 100% procedural success with hemostasis in 2.1 minutes, challenging manual compression and traditional valves for large-bore venous access[3]Cordis, “Cordis Receives FDA Approval for MYNX CONTROL™ Venous Vascular Closure Device,” cordis.com. Abbott’s StarClose SE likewise offers rapid arterial closure without major vascular complications. Bioabsorbable technology eliminates foreign material retention, appealing to health systems concerned about late complications. The expanding closure toolkit diverts purchasing budgets, subtracting 0.5 percentage points from growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: One-Handed Innovation Drives Market Evolution

Hemostasis Valve Y-Connectors retained a 43.05% hemostasis valve market share in 2025, confirming their entrenched role in dual-port access for diagnostic angiography. The segment’s stability underpins a sizable installed base that ensures repeat purchases. Operator feedback, however, increasingly favors single-handed manipulation to cut exchange times, triggering rapid adoption of One-Handed Hemostasis Valves that post a 9.10% CAGR through 2031. The shift influences procurement policies at teaching hospitals where efficiency metrics are closely tracked.

One-Handed valves incorporate cross-slit seals that maintain integrity at elevated pressures, exemplified by the WATCHDOG system. Double Y-Connectors target niche procedures needing simultaneous guidewire and microcatheter access, whereas Integrated Extension-Line valves gain momentum for chronic total occlusion work. Push-Pull designs survive in legacy setups but face cannibalization. Material advances, including high-durometer silicone, reduce valve fatigue during lengthy rotational atherectomy, further boosting adoption among high-volume centers keen on workflow streamlining.

By Application: Neuro-Interventional Surge Reshapes Market Dynamics

Angiography remained the backbone application with 39.13% revenue share in 2025, driven by its role in both diagnostic and therapeutic settings. Repeat coronary angiographies for chronic coronary syndrome patients sustain base demand, anchoring the hemostasis valve market. Parallel growth in complex percutaneous coronary interventions reinforces the need for robust Y-Connector valves capable of multiple device exchanges.

Neuro-interventional procedures register the fastest growth at 10.56% CAGR, propelled by marked expansion in middle meningeal artery embolization for chronic subdural hematoma management. Radial adoption within neuro-intervention fosters demand for ultra-low-profile seals compatible with 4F and 5F sheath sizes. Peripheral vascular interventions also witness higher uptake as endovascular aneurysm repair captures larger aneurysm-repair volumes, creating incremental opportunities. Electrophysiology benefits from atrial fibrillation prevalence, but venous access requires valves tailored for larger bore sizes, adding complexity to product portfolios.

By End User: Ambulatory Centers Drive Efficiency Revolution

Hospitals dominated revenue with 56.05% in 2025, reflecting their capacity for complex multi-disciplinary interventions and intensive care backup. Purchasing committees within large academic centers typically negotiate multi-year contracts favoring vendors offering integrated valve portfolios. Despite this dominance, ambulatory surgical centers lead growth at 8.38% CAGR amid healthcare cost-containment reforms. Same-day discharge studies validate economic savings and patient satisfaction, incentivizing payers to steer suitable cases to these facilities.

Catheterization laboratories embedded within tertiary hospitals focus on throughput optimization, often adopting reusable seals to manage consumable budgets. Specialty clinics target electrophysiology and peripheral procedures, demanding valves compatible with dedicated mapping or atherectomy systems. Mobile cath-lab pilots in rural China trial low-profile valve kits designed for rapid deployment. Across end users, suppliers that harmonize product codes and training programs gain competitive advantage.

Geography Analysis

North America captured 37.55% of the hemostasis valve market in 2025, bolstered by high procedural volumes and advanced reimbursement structures. Extensive radial adoption combined with an aging population maintains steady unit demand. Europe follows with consistent spending, although EU-MDR compliance introduces cost headwinds that may temper near-term growth.

Asia-Pacific is the standout, poised for an 8.18% CAGR as domestic manufacturers scale production of cost-effective valves aligned with regional price sensitivities. Government-funded cath-lab rollouts in Indonesia and the Philippines emphasize day-case capacity, creating demand for durable valves that tolerate sterilization cycles. Japan and South Korea continue to set quality benchmarks, spurring local suppliers to adopt high-precision molding technologies. The hemostasis valve market size for Asia-Pacific is therefore projected to close the decade at roughly USD 88.6 million, representing meaningful share gains.

The Middle East and Africa show latent potential, hinged on national cardiac-center programs emerging in Saudi Arabia and the United Arab Emirates. South America gradually advances as Brazil lifts capital-equipment import barriers, yet currency volatility moderates momentum. Collectively, these regions provide diversification opportunities for multinationals hedging against saturated developed markets.

Competitive Landscape

The hemostasis valve market features moderate fragmentation, with the top five firms controlling significant global revenue. Boston Scientific leverages broad cardiovascular portfolios and the 2024 acquisition of Silk Road Medical to widen neurovascular access. Teleflex agreed to purchase BIOTRONIK’s vascular intervention unit for EUR 760 million, instantly adding drug-coated balloons and scaffolds that complement its valve line. Merit Medical continues to grow share through incremental innovations in low-profile seals optimized for radial access.

Terumo capitalizes on Asia-Pacific growth by co-developing reusable valves with regional distributors, focusing on sterilization durability. Nordson’s USD 800 million acquisition of Atrion signals a push into integrated infusion and cardiovascular components. Smaller innovators focus on smart valves with embedded pressure sensors, aiming to license technology to incumbents rather than compete on scale.

Competitive factors now revolve around seal reliability, ergonomic design, and supply-chain resilience. Vendors offering training modules on radial access and sustainability claim differentiation in procurement bids. The proliferation of alternative vascular closure devices forces traditional valve suppliers to underline cost-effectiveness in multi-device cycles rather than single-use economics. Firms adept at bundling valves with guidewires or sheath kits secure higher average selling prices.

Hemostasis Valve Industry Leaders

Boston Scientific Corporation

Merit Medical Systems

Teleflex Incorporated

Terumo Corporation

Freudenberg Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex announced an agreement to acquire BIOTRONIK's Vascular Intervention business for approximately EUR 760 million, broadening its interventional cardiology portfolio.

- October 2024: Boston Scientific released ACURATE neo2 data at TCT 2024; discussions with the FDA continue regarding the U.S. regulatory pathway.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hemostasis valve market as the worldwide sales revenue generated from stand-alone mechanical or polymeric valves, such as Y-connectors, double Y-connectors, and single-handed rotating units, that are fitted on guiding catheters and sheaths to maintain a blood-free field during angiography, angioplasty, and other endovascular procedures.

Scope exclusion: disposable vascular closure plugs and active flow-control introducers are not counted.

Segmentation Overview

- By Product Type

- Hemostasis Valve Y-Connectors

- Double Y-Connector Valves

- One-Handed Hemostasis Valves

- Integrated Extension-Line Valves

- Push-Pull Hemostasis Valves

- Others

- By Application

- Angiography

- Angioplasty

- Electrophysiology Procedures

- Neuro-interventional Procedures

- Peripheral Vascular Interventions

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Catheterization Laboratories

- Specialty Clinics

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with cath-lab managers in North America, purchasing directors in high-volume European hospitals, and product engineers at valve OEMs across Asia-Pacific. These discussions validated radial-access penetration, average selling price progression, and supply back-orders, closing data gaps left by public sources.

Desk Research

We began with core public datasets, interventional cardiology procedure volumes from the American College of Cardiology, EU-27 hospital discharge files, and Japan's MHLW cath-lab statistics, which anchored regional demand patterns. Device import-export codes (HS 9018.39) gathered from UN Comtrade, plus 10-K shipment disclosures, helped us approximate traded unit flow. Complementary signals came from clinical-trial registries that disclose trial counts for low-profile valves and from peer-reviewed journals tracking the shift to radial access. To enrich company positioning, we extracted product ASP cues from U.S. SEC filings and voluntary UDI submissions. Proprietary look-ups on D&B Hoovers and Dow Jones Factiva gave us baseline revenue splits by geography. The secondary source list is indicative, not exhaustive.

Market-Sizing & Forecasting

A top-down construct starts with yearly interventional procedure counts, adjusted by the observed ratio of procedures per valve and further refined through country-level radial adoption rates. Results are cross-checked through selective bottom-up roll-ups of leading supplier revenues and sampled ASP × units gleaned from distributor interviews. Key variables driving the model include:

1. Annual PCI and peripheral intervention volumes,

2. Radial versus femoral access mix,

3. Average valve ASP by hospital type,

4. Cath-lab installation growth,

5. Regulatory recertification costs influencing pricing.

Five-year forecasts are produced with a multivariate regression that links valve demand to procedure growth and ASP inflation scenarios, and then stress-tested by scenario analysis for elective-procedure deferrals.

Data Validation & Update Cycle

Outputs pass a three-layer review, analyst, senior peer, and research manager, where anomalies versus external trade data and supplier filings trigger re-checks. We refresh each model annually and issue interim revisions when material recalls, pricing shocks, or guideline changes occur.

Why Mordor's Hemostasis Valve Baseline Commands Dependability

Published market values often diverge because firms vary scope definitions, cut-off years, and refresh rhythms.

According to Mordor Intelligence, our disciplined scoping around valve-only revenue and our yearly refresh cadence narrow such gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 193.8 M (2025) | Mordor Intelligence | - |

| USD 184.6 M (2024) | Global Consultancy A | Excludes Asia-Pacific low-volume cath-labs, uses static 2024 ASPs |

| USD 180.2 M (2024) | Industry Association B | Bundles introducer sheaths with valves, partial hospital sampling |

| USD 161.3 M (2022) | Regional Consultancy C | Historic base year, no adjustment for post-pandemic elective rebound |

In summary, the Mordor approach, grounded in current procedure data, selective bottom-up validation, and timely refreshes, delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current value of the hemostasis valve market?

The hemostasis valve market generated USD 203.9 million in 2026 and is forecast to reach USD 263.18 million by 2031.

Which product type leads revenue in the hemostasis valve market?

Hemostasis Valve Y-Connectors led with 43.05% market share in 2025.

Why are ambulatory surgical centers growing faster than hospitals?

Same-day discharge protocols and cost advantages drive an 8.38% CAGR for ambulatory surgical centers, outpacing hospital growth.

Which region is expected to experience the highest growth?

Asia-Pacific is projected to grow at an 8.18% CAGR through 2031 due to expanding day-case catheterization laboratories.

How do smart hemostasis valves differ from traditional models?

Smart valves incorporate pressure sensors that provide real-time feedback, improving seal management and potentially enhancing patient safety.

Page last updated on: