Electrophysiology Catheter Ablation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 3.23 Billion |

| Growth Rate (2026 - 2031) | 8.92% CAGR |

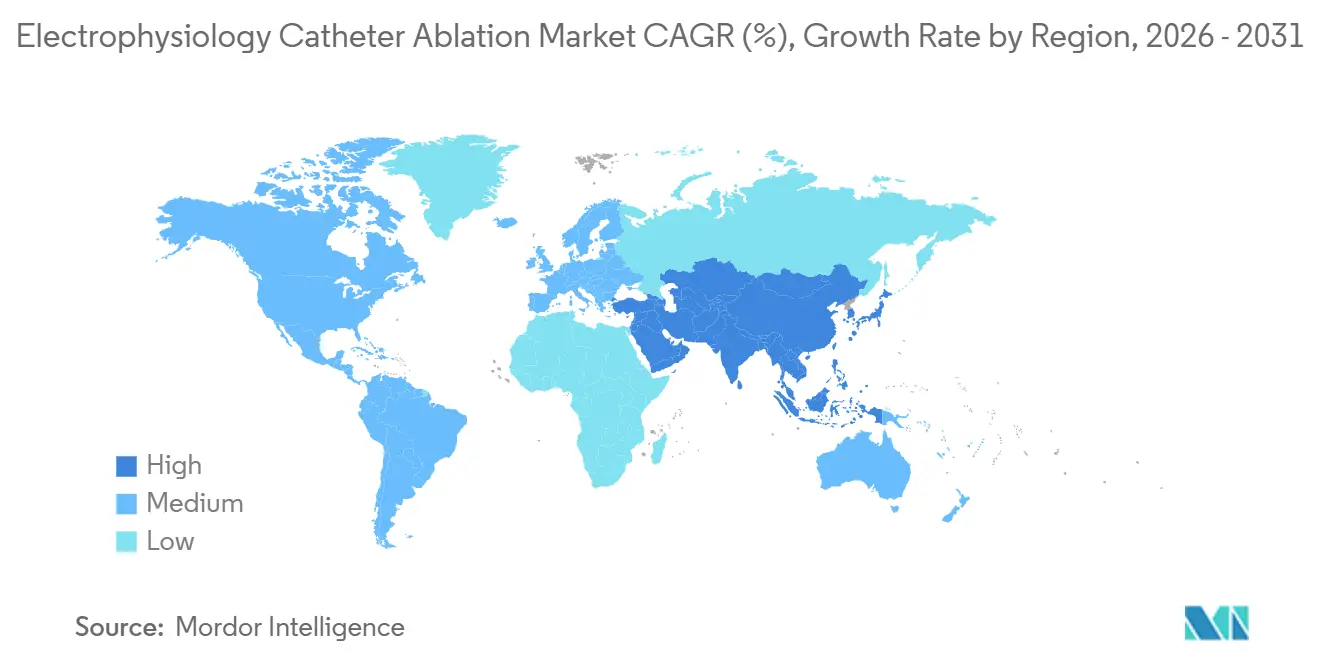

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

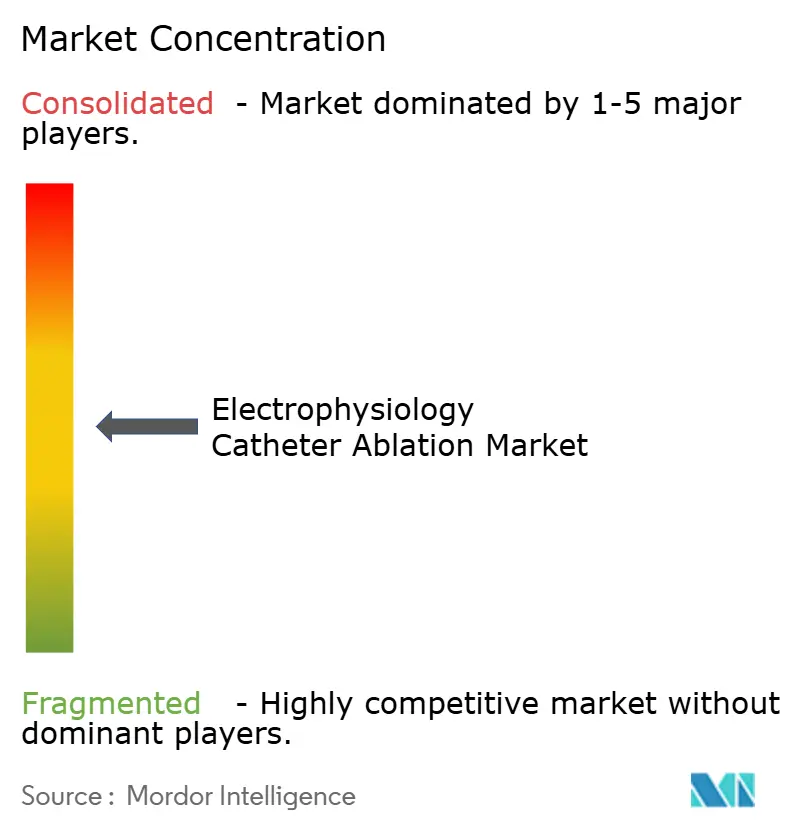

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electrophysiology Catheter Ablation Market Analysis by Mordor Intelligence

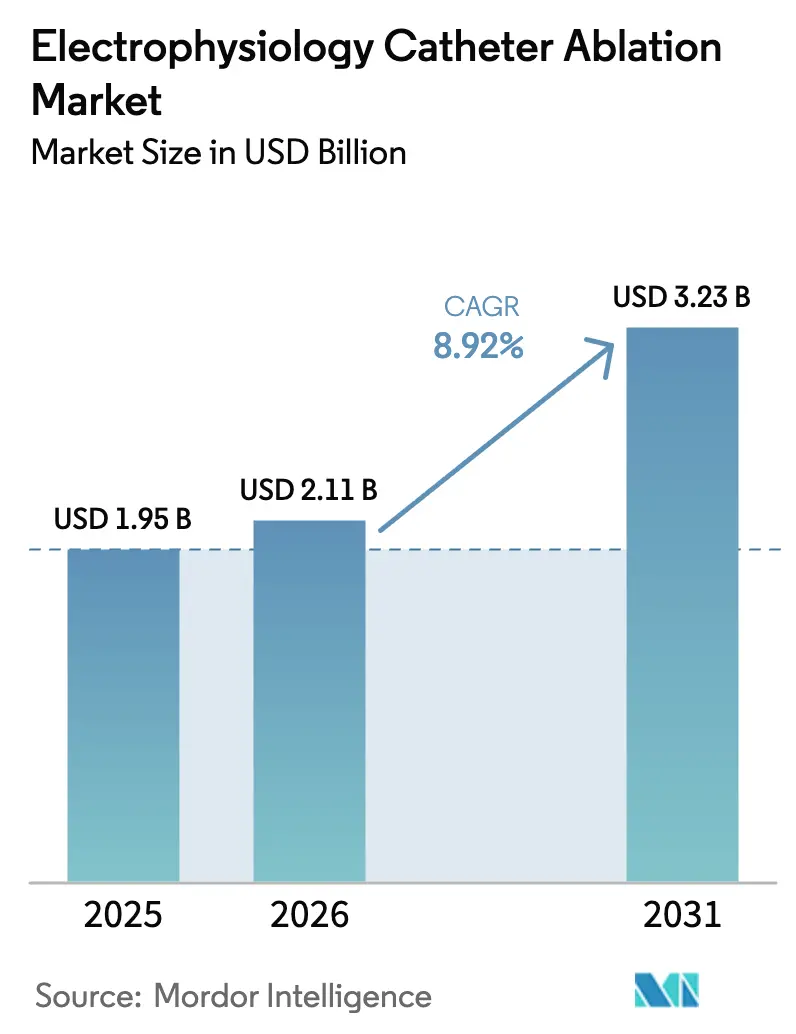

The Electrophysiology Catheter Ablation Market is expected to grow from USD 1.95 billion in 2025 to USD 2.11 billion in 2026 and is forecasted to reach USD 3.23 billion by 2031 at 8.92% CAGR over 2026-2031.

Growth is underpinned by a rapid rise in atrial fibrillation (AF) prevalence, accelerated regulatory approvals for pulsed-field ablation (PFA) systems, and payer policies that reward shorter, outpatient-eligible procedures. Boston Scientific’s FARAPULSE and Medtronic’s PulseSelect launches catalyzed an early-adopter wave, while Abbott and Johnson & Johnson added AI-guided navigation features that reduce procedure time and radiation exposure. Hospitals are scaling capacity through zero-fluoroscopy labs, and ambulatory surgical centers (ASCs) now qualify for Medicare payment parity, altering site-of-service economics in favor of same-day discharge workflows. Competitive differentiation is shifting toward disposable catheter innovation rather than legacy capital equipment, tightening the race among the top four vendors that already control about three-quarters of global revenue.

Key Report Takeaways

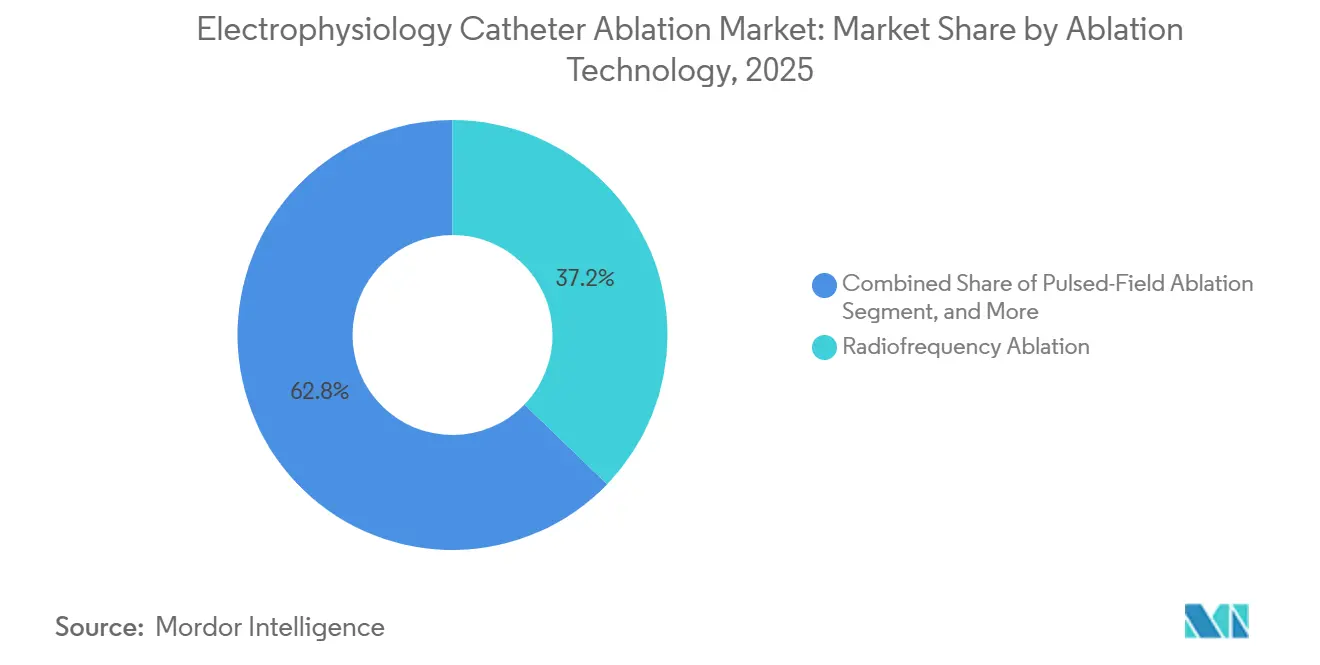

- By ablation technology, radiofrequency led with 56.01% of the electrophysiology catheter ablation market share in 2025; pulsed-field ablation is forecast to expand at a 9.59% CAGR through 2031.

- By procedure approach, point-by-point workflows accounted for 64.57% of the electrophysiology catheter ablation market in 2025, whereas single-shot devices are projected to grow at a 10.54% CAGR through 2031.

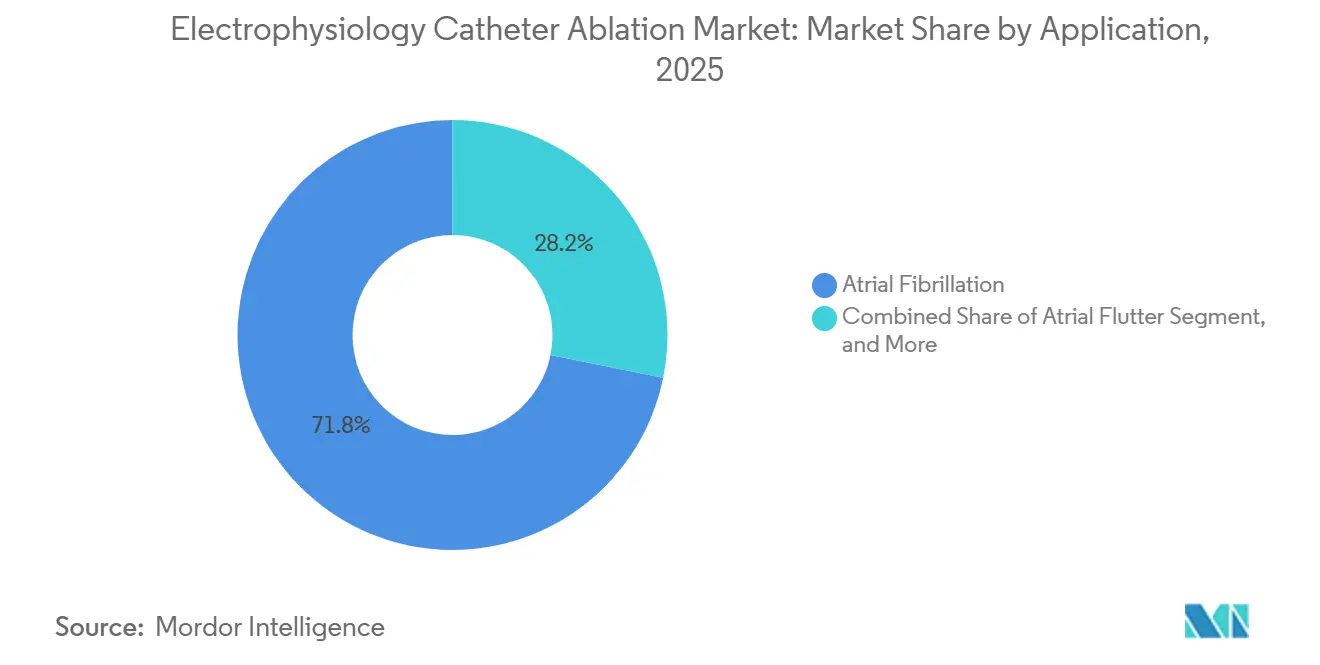

- By application, atrial fibrillation captured 71.82% share of the electrophysiology catheter ablation market size in 2025, and ventricular tachycardia is advancing at a 13.12% CAGR through 2031.

- By end user, hospitals held 58.03% of the electrophysiology catheter ablation market share in 2025, while ASCs are poised to post an 11.19% CAGR between 2026-2031.

- By geography, North America led with 38.83% revenue share in 2025; Asia-Pacific is forecast to post a 13.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electrophysiology Catheter Ablation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AF Prevalence Growth | +2.1% | Global, with acute pressure in North America, Europe, and aging Asia-Pacific markets | Long term (≥ 4 years) |

| Shift Toward Zero-Fluoroscopy Labs | +1.3% | North America & EU, early adoption in Australia and Japan | Medium term (2-4 years) |

| Integration of AI-Guided Navigation | +1.5% | North America, Western Europe, select Asia-Pacific tertiary centers | Medium term (2-4 years) |

| CMS Add-On Payments for Novel Catheters | +1.8% | United States, with spillover influence on private payers in Canada and select Latin American markets | Short term (≤ 2 years) |

| Pulsed-Field Ablation's Safety Profile | +2.3% | Global, led by US and EU regulatory clearances; China NMPA approvals accelerating adoption | Medium term (2-4 years) |

| Growing Preference for Minimally Invasive Catheter Procedures | +1.6% | Global, with strongest momentum in ambulatory surgical centers across North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid AF Prevalence Growth

U.S. atrial fibrillation diagnoses reached 10.55 million in 2024, a 23% jump over 2019 figures. Global prevalence is on track to top 60 million cases by 2030 as hypertension, diabetes, and obesity converge with longer life expectancy in Asia-Pacific countries. The American Heart Association’s 2024 guideline upgrade, which positions catheter ablation as a first-line therapy, expanded the eligible patient pool by about 40%.[1]Vivek Y. Reddy et al., “Pulsed Field Ablation for Paroxysmal Atrial Fibrillation,” Heart Rhythm, heartrhythmjournal.com Hospitals responded by ordering 19% more Abbott EnSite systems in 2024, particularly in community facilities that previously referred complex cases out. Together, these factors intensify procedure volume and sustain double-digit growth for the electrophysiology catheter ablation market.

Pulsed-Field Ablation’s Safety Profile

Boston Scientific’s FARAPULSE delivered zero esophageal fistulas in the 1,500-patient ADVENT trial, an outcome that persuaded U.S. Medicare to grant New Technology Add-on Payment status in 2024. Medtronic’s PulseSelect showed 66% arrhythmia-free survival at 12 months in the PULSED AF trial and obtained China NMPA clearance in early 2025, accelerating cross-border rollouts. PFA’s non-thermal, microsecond electric pulses circumvent the phrenic-nerve and esophageal-injury risks that limit the adoption of radiofrequency and cryoablation, improving both safety optics and litigation exposure for hospitals. Johnson & Johnson’s VARIPULSE, still under FDA review, targets sub-60-minute procedure times through variable-loop geometry, aligning with same-day discharge thresholds. These advances are central to the premium growth trajectory of the electrophysiology catheter ablation market.

Integration of AI-Guided Navigation

Abbott’s EnSite X embeds algorithms that predict lesion durability from contact force, impedance drop, and catheter stability, removing subjective operator interpretation in 87% of paroxysmal AF cases. Biosense Webster’s Carto 3 v8 flags lesion gaps larger than 6 mm, the reconnection threshold that doubles failure rates. Stereotaxis upgraded its Genesis robotic magnetic navigation system in 2025 to automate catheter advancement and cut operator radiation exposure by 94%. Collectively, AI features reduce average lab times by 20% in 20% of cases, previously exceeding 180 minutes, and free up capacity for additional cases, supporting sustained adoption across high-volume centers. The resulting efficiency lifts overall throughput in the electrophysiology catheter ablation market.

CMS Add-On Payments for Novel Catheters

The U.S. Centers for Medicare & Medicaid Services increased outpatient reimbursement by USD 3,200-4,500 per PFA procedure in its 2024 OPPS rule, closing the profitability gap with point-by-point radiofrequency workflows.[2]Centers for Medicare & Medicaid Services, “CY 2024 OPPS Final Rule,” cms.gov Separate billing for advanced mapping (CPT 93609) added another USD 800-1,200, incentivizing hospitals to deploy ultra-high-density systems for ventricular tachycardia. Private payers followed; Anthem and UnitedHealthcare removed prior authorization for PFA in 2025, slashing scheduling delays to under 10 days. Internationally, Japan lifted its catheter-ablation fee schedule by 12% in 2024 to reflect PFA device costs, improving margins for facilities treating an aging population. Aligning reimbursement policies accelerates growth in the electrophysiology catheter ablation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long Learning Curve for PFA Systems | -0.8% | Global, most acute in community hospitals and emerging markets with limited training infrastructure | Short term (≤ 2 years) |

| High Capital Cost of 3-D Mapping Suites | -1.4% | Global, with disproportionate impact on rural hospitals in North America, public hospitals in Europe, and Tier 2-3 cities in Asia-Pacific | Medium term (2-4 years) |

| Re-Do Procedures Due To Lesion Reconnection | -0.6% | Global, with higher rates in centers performing <50 procedures annually | Long term (≥ 4 years) |

| Shortage of Trained Electrophysiologists and EP Nurses | -1.2% | North America, Western Europe, and Australia; emerging in urban China and India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of 3-D Mapping Suites

Electroanatomic mapping systems cost USD 300,000-500,000, with annual service contracts of USD 40,000-70,000, making them challenging for facilities that perform fewer than 150 ablations a year. Disposable mapping catheters add USD 2,500-4,000 per case, straining margins after Medicare’s 2024 site-neutral payment cut for outpatient ablation. European public hospitals face similar pressures under DRG caps of EUR 8,000-12,000 per case, leaving little room for PFA catheter premiums, which run at EUR 3,500, compared with EUR 1,800 for radiofrequency devices. Leasing and per-procedure pricing models help low-volume centers but raise total cost for high-volume operators over time. Access to capital, therefore, moderates the expansion of the electrophysiology catheter ablation market.

Shortage of Trained Electrophysiologists and EP Nurses

The American College of Cardiology projects a 20% deficit in board-certified electrophysiologists by 2030, with 62% of U.S. counties lacking a single specialist.[3]American Hospital Association, “Rural Hospital Report 2024,” aha.org Procedural delays average 6-8 weeks for rural patients, and salaries for EP-qualified nurses run 25-30% above general cath-lab rates, widening labor gaps. In Europe, 40% of labs operate below optimal staffing levels, with Germany, the U.K., and Spain reporting vacancy rates above 15%. Simulation-based training and AI-supported navigation ease the burden but require multi-year scaling cycles. Workforce scarcity, therefore, tempers throughput in the electrophysiology catheter ablation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ablation Technology: PFA Disrupts RF Dominance

Radiofrequency ablation retained a 56.01% share of the electrophysiology catheter ablation market in 2025, reflecting 2 decades of clinical validation. However, PFA is growing 9.59% annually, buoyed by Boston Scientific’s FARAPULSE, which captured 12% of U.S. paroxysmal AF procedures within nine months of launch and prompted a USD 200 million capacity expansion. Cryoablation’s 22% share faces pressure as PFA matches its 60-75-minute procedure time while eliminating the risk of phrenic-nerve palsy. Laser and microwave modalities remain niche, constrained by reimbursement and limited approvals, while emerging ultrasound and electroporation variants sit 3-5 years from commercialization.

PFA’s rise is reshaping capital allocation. Abbott’s EnSite X and Biosense Webster’s Carto 3 v8 now feature PFA-specific algorithms that visualize lesion transmurality in real time, future-proofing system purchases. Hospitals seek multi-energy compatibility to hedge against obsolescence risk, steering toward vendors that can integrate PFA alongside radiofrequency and cryo workflows. The FDA’s 2024 guidance, which enables a streamlined 510(k) pathway for PFA variants, accelerates this shift, and the resulting buyer behavior underpins premium growth in the electrophysiology catheter ablation market.

By Procedure Approach: Single-Shot Gains on Efficiency

Point-by-point workflows held a 64.57% share of the electrophysiology catheter ablation market in 2025, favored for lesion-set customization across ventricular and supraventricular substrates. Single-shot devices are expanding at a 10.54% CAGR as hospitals prize 60-minute average lab times and shorter radiation exposure. Medtronic’s Arctic Front Advance Pro and Boston Scientific’s Pentaspline FARAPULSE achieve near-circumferential isolation in fewer applications, boosting daily case counts and enabling ASCs to schedule four or more ablations per lab per day.

Single-shot growth is AF-centric; ventricular tachycardia and atypical flutter still require point-by-point precision, which requires gathering 500-1,000 electrograms per case. Reimbursement neutrality between the two approaches sustains physician choice, but bundled private-payer contracts that reward throughput increasingly favor single-shot devices for paroxysmal AF. The diverging application mix keeps both modalities relevant, but the efficiency premium accelerates single-shot adoption in the electrophysiology catheter ablation market.

By Application: VT Ablation Outpaces AF Growth

Atrial fibrillation dominated 71.82% of the 2025 volume, yet ventricular tachycardia ablation is slated to grow 13.12% annually, the fastest among all arrhythmia types. The 2024 guideline elevation of substrate-based VT ablation to Class I status for ischemic cardiomyopathy doubled the U.S. addressable population to 120,000 annual procedures. Ultra-high-density mapping, exemplified by Rhythmia HDx’s 10,000-electrogram capacity, reduces VT procedure length to 180 minutes, making same-day discharge feasible for stable patients.

AF growth persists at 8.5% CAGR due to first-line ablation recommendations and expanded screening programs. Atrial flutter and supraventricular tachycardia grow at 7-8%, while PVC ablations lag under unfavorable bundling rules. Collectively, rising case complexity boosts demand for advanced mapping and sustains premium pricing in the electrophysiology catheter ablation market.

By End User: ASCs Capture Outpatient Shift

Hospitals retained a 58.03% share of the electrophysiology catheter ablation market in 2025, leveraging intensive care resources for complex ventricular work. ASCs, however, benefit from 2025 Medicare payment parity that removed a USD 3,500 facility-fee gap, propelling an 11.19% CAGR through 2031. Heart Rhythm Society registry data show a 0.8% rate of major adverse events within 30 days for same-day discharge AF cases, validating the outpatient model.

Physician-owned specialty centers and hybrid hospital-based ASCs now compete aggressively for routine AF cases, while high-acuity VT and redo procedures remain hospital-anchored. Investment from private equity, such as Ares Management’s 2024 USD 240 million acquisition of a 15-center EP network, signals confidence in outpatient scalability. The evolving site-of-care mix broadens access and underpins growth in the electrophysiology catheter ablation market.

Geography Analysis

North America generated 38.83% of global revenue in 2025, supported by Medicare coverage and a dense concentration of EP fellowship programs that train 60% of the world’s specialists. PFA catheters qualified for U.S. New Technology Add-on Payments in 2024, giving facilities a USD 3,200-4,500 margin lift per case and sustaining capital investment cycles. Canada’s single-payer system is evaluating similar add-on payments, suggesting regional convergence.

Europe's delay in implementing the Medical Device Regulation in 2024 delayed several PFA launches by up to 12 months. The U.K.’s National Health Service shortened AF ablation wait times from 18 to 6 months after extending coverage for PFA, increasing throughput in publicly funded labs.

Asia-Pacific is the growth engine, forecast to post a 13.92% CAGR through 2031. China’s February 2025 NMPA approval of PulseSelect opens a population where AF cases numbered 8 million in 2024 and could surpass 12 million by 2030. Domestic vendors such as Lepu Medical already undercut Western list prices by 40-50%, easing budget constraints for DRG-restricted hospitals. Japan’s 12% reimbursement uplift in 2024 offsets higher PFA catheter costs, and a senior population that reached 29.1% in 2024 magnifies demand.

Brazil’s August 2024 ANVISA approval of FARAPULSE widened private-payer coverage, whereas Argentina’s economic volatility curbed equipment purchases, relying on affluent self-pay patients for growth. Gulf Cooperation Council nations are recruiting Western-trained electrophysiologists through Vision 2030 programs and installing Carto 3 and EnSite X systems in flagship hospitals across Abu Dhabi and Riyadh.

Competitive Landscape

Abbott, Boston Scientific, Medtronic, and Johnson & Johnson controlled significant revenue in 2025, reflecting moderate concentration in the electrophysiology catheter ablation market. Boston Scientific’s USD 925 million Farapulse acquisition in 2024 was priced at 12× projected sales, underscoring the strategic premium on PFA assets. Abbott is progressing Volt PFA through pivotal trials, while Medtronic is adding focal PulseSelect variants for persistent AF and atrial flutter indications. Johnson & Johnson leans on Carto’s AI-driven lesion-assessment tools to protect its 40% share of the mapping system amid 8-10% pricing declines amid intense vendor competition.

Niche players fill whitespace. Stereotaxis offers USD 2 million robotic magnetic navigation systems that virtually eliminate radiation but confine adoption to high-volume academic centers. MicroPort and Lepu Medical are accelerating in China with lower-cost PFA catheters, pressuring Western incumbents on pricing and local-content rules. Pediatric EP and outpatient VT represent under-penetrated segments; the FDA’s 2024 Pediatric Device Consortia grants earmarked USD 12 million for child-sized PFA catheters, illustrating regulatory support for novel indications. Overall, rivalry is intensifying as PFA lowers technical barriers and shifts value to disposables, prompting aggressive R&D and pricing responses.

Electrophysiology Catheter Ablation Industry Leaders

-

AngioDynamics Inc.

-

Biotronik SE & Co. KG

-

Medtronic

-

Johnson & Johnson

-

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Boston Scientific reported continued EP sales growth driven by PFA despite an overall slowdown in company revenue.

- January 2026: Abbott received CE Mark for the TactiFlex Duo ablation catheter, and the first European cases were completed the same week.

- November 2025: MicroPort EP launched the PulseMagic TrueForce pressure-sensing PFA catheter upon China NMPA approval, broadening its non-thermal portfolio.

- October 2024: Medtronic gained U.S. FDA approval for the Affera Mapping and Ablation System with Sphere-9 catheter, integrating high-density mapping with dual-energy ablation.

Global Electrophysiology Catheter Ablation Market Report Scope

The Electrophysiology (EP) Catheter Ablation Market refers to the global industry for medical devices specifically catheters used in minimally invasive procedures to treat cardiac arrhythmias such as atrial fibrillation, atrial flutter, and ventricular tachycardia. These catheters deliver energy (radiofrequency, cryo, laser, or pulsed field) to targeted heart tissue to disrupt abnormal electrical pathways and restore normal rhythm.

The Electrophysiology Catheter Ablation Market Report is Segmented by Ablation Technology (Radiofrequency, Cryoablation, Laser, Microwave, Pulsed-Field, Other), Procedure Approach (Point-By-Point, Single-Shot), Application (AF, Flutter, SVT, VT, Other), End User (Hospitals, ASCs, Specialty Centers, Academic Institutes), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Value (USD).

| Radiofrequency Ablation |

| Cryoablation |

| Laser |

| Microwave |

| Pulsed-Field Ablation |

| Other Emerging Energy Sources |

| Point-By-Point Ablation |

| Single-Shot Devices |

| Atrial Fibrillation |

| Atrial Flutter |

| Supraventricular Tachycardia |

| Ventricular Tachycardia |

| Other Arrhythmias |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Cardiac Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Ablation Technology | Radiofrequency Ablation | |

| Cryoablation | ||

| Laser | ||

| Microwave | ||

| Pulsed-Field Ablation | ||

| Other Emerging Energy Sources | ||

| By Procedure Approach | Point-By-Point Ablation | |

| Single-Shot Devices | ||

| By Application | Atrial Fibrillation | |

| Atrial Flutter | ||

| Supraventricular Tachycardia | ||

| Ventricular Tachycardia | ||

| Other Arrhythmias | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Cardiac Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the electrophysiology catheter ablation market in 2026?

The electrophysiology catheter ablation market size is USD 2.11 billion in 2026 and is projected to reach USD 3.23 billion by 2031.

Which ablation technology is growing the fastest?

Pulsed-field ablation is advancing at a 9.59% CAGR through 2031, outpacing radiofrequency, cryo, and laser modalities.

Why are ambulatory surgical centers gaining share in catheter ablation?

Medicare payment parity introduced in 2025 eliminated a facility-fee disadvantage, and same-day discharge protocols have proven safe, supporting an 11.19% CAGR for ASCs.

Which region offers the highest growth potential?

Asia-Pacific is forecast to expand at a 13.92% CAGR, energized by China’s regulatory approvals and Japan’s aging population.

What is the main challenge restraining market growth?

High capital costs for 3-D mapping suites and a shortage of trained electrophysiologists constrain capacity expansion, especially in rural and lower-income markets.

Page last updated on: