Central Venous Catheter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.69 Billion |

| Market Size (2031) | USD 3.67 Billion |

| Growth Rate (2026 - 2031) | 6.40% CAGR |

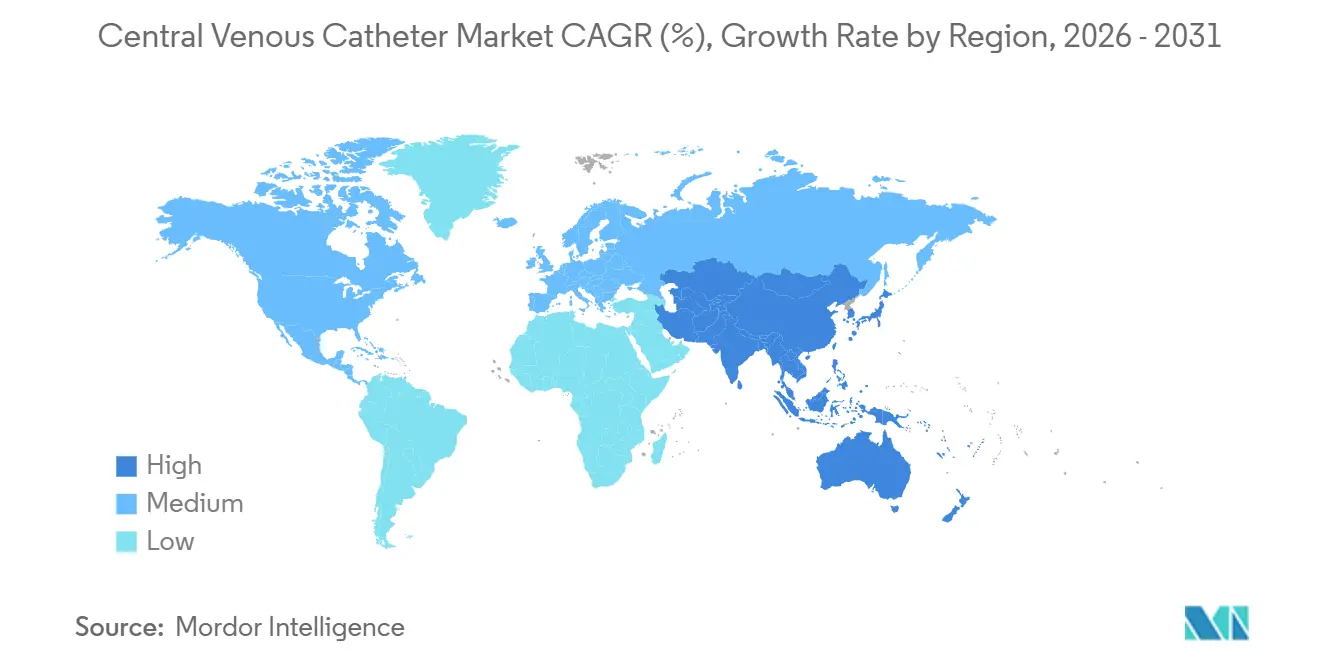

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

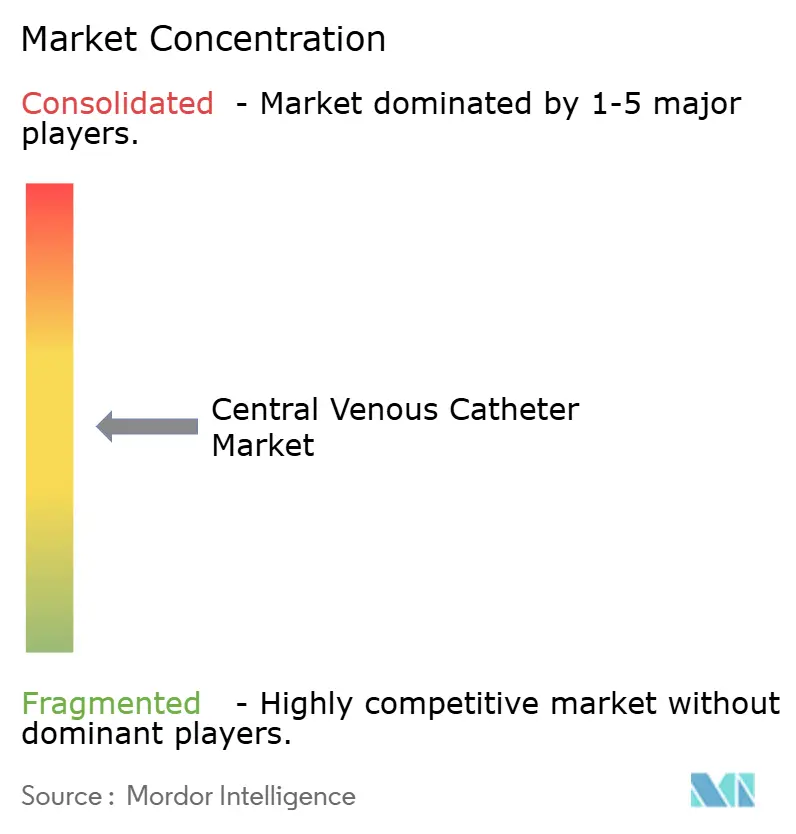

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central Venous Catheter Market Analysis by Mordor Intelligence

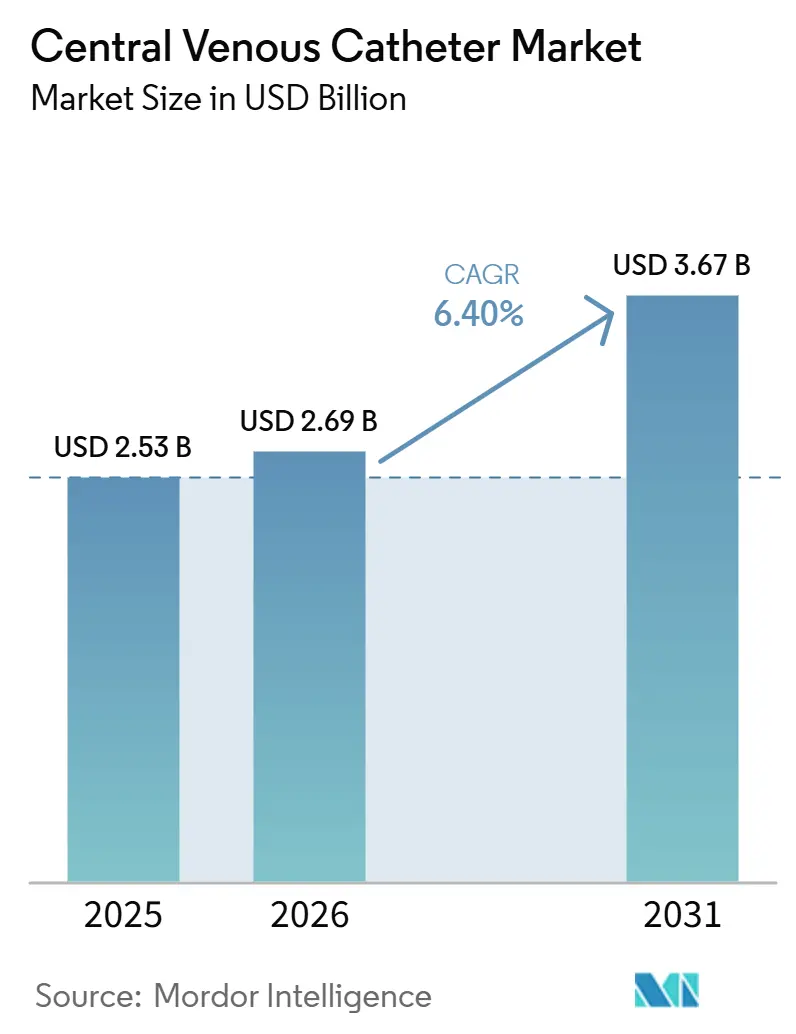

The Central Venous Catheter Market size is expected to grow from USD 2.53 billion in 2025 to USD 2.69 billion in 2026 and is forecast to reach USD 3.67 billion by 2031 at 6.40% CAGR over 2026-2031.

The central venous catheter market is supported by steady demand from oncology infusion, hemodialysis, critical care, and long-duration nutrition support, as these care settings rely on central access for drug delivery and monitoring. Rising use in dialysis and cancer care continues to sustain procedure volumes, while the shift toward home infusion and ambulatory settings is expanding adoption beyond hospitals. Product development is moving the central venous catheter market toward power-injectable, antimicrobial, and workflow-integrated systems that meet stricter clinical protocols and reduce insertion complexity. However, pricing pressure from tenders and value-based procurement limits broader price realization across regions, while leading suppliers maintain a competitive edge through broad portfolios, clinical evidence, and established hospital contracting channels.

Key Report Takeaways

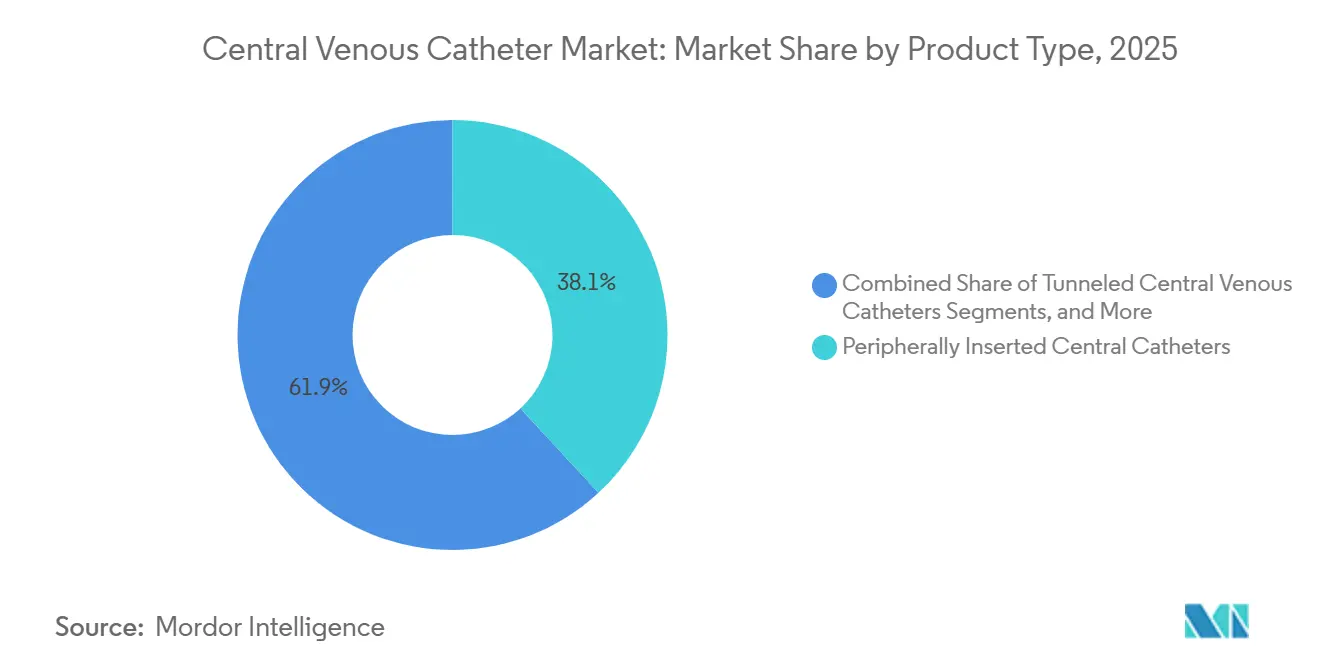

- By product type, peripherally inserted central catheters held 38.12% share in 2025, while implanted ports are forecast to expand at a 9.53% CAGR through 2031.

- By lumen type, double lumen catheters held 42.45% share in 2025, while multi-lumen catheters is projected to grow CAGR at 8.67% through 2031.

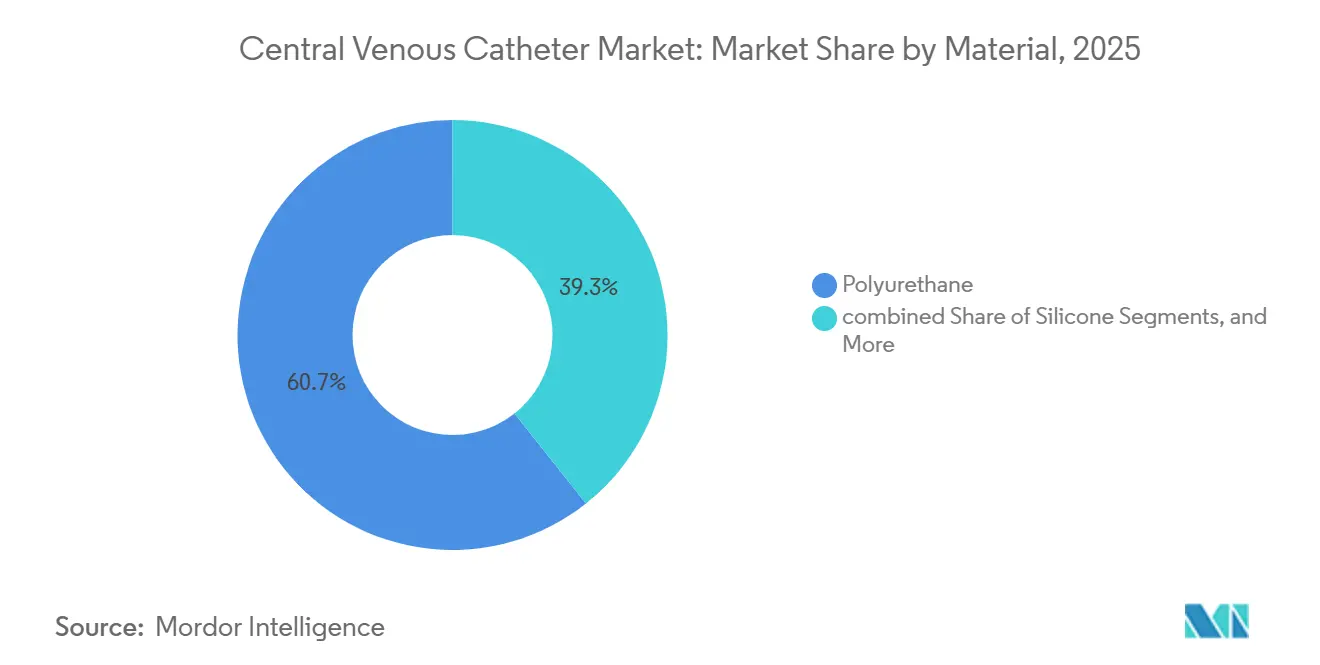

- By material, polyurethane accounted for 60.66% share in 2025, and are expected to grow at CAGR 7.35% through 2031.

- By application, drug administration accounted for 52.67% share of the central venous catheter market size in 2025, while fluid and nutrition administration is projected at a 9.67% CAGR through 2031.

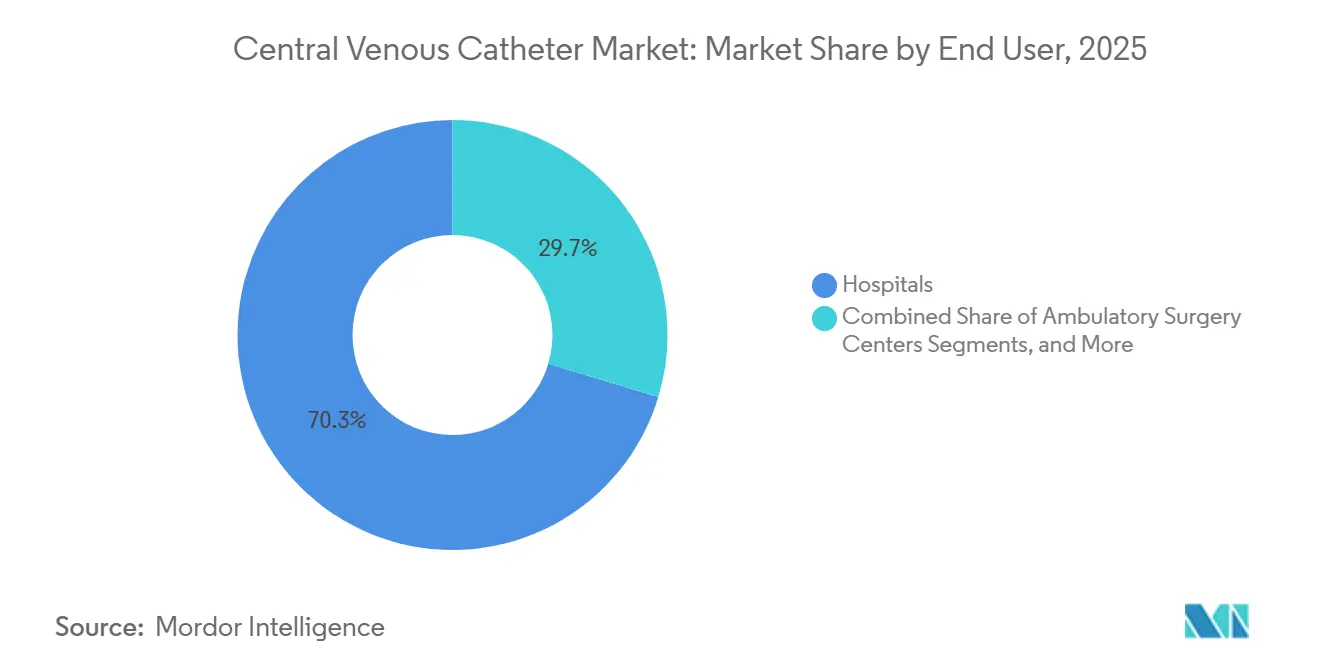

- By end user, hospitals held 70.34% share in 2025, while ambulatory surgery centers are forecast to grow at an 8.87% CAGR through 2031.

- By geography, North America held 41.56% of the central venous catheter market share in 2025, while Asia-Pacific is projected to grow at a 10.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Central Venous Catheter Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising cancer, dialysis, and critical-care demand | +1.8% | Global | Long term (≥ 4 years) |

| Increasing preference for power-injectable central venous catheters | +1.1% | North America & EU | Medium term (2-4 years) |

| Infection-prevention bundling and chlorhexidine adoption | +0.9% | Global | Medium term (2-4 years) |

| Expansion of interventional and ICU procedure volumes | +1.0% | APAC, Middle East | Medium term (2-4 years) |

| Longer dwell-time use in home infusion and ambulatory settings | +0.8% | North America, EU | Long term (≥ 4 years) |

| Smarter insertion, securement, and tip-verification workflows | +0.6% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cancer, Dialysis, and Critical-Care Demand

The central venous catheter market continues to gain from cancer, dialysis, and critical care cases that require repeated access, reliable infusion, and controlled administration over extended treatment periods. Dialysis remains a key demand driver, as healthcare providers use tunneled catheters as bridging access when fistulas are not ready. Critical care also supports market growth, as patients in intensive care settings often need vasoactive drugs, blood products, monitoring, and nutritional support through a single access route. The overlap between oncology and kidney disease increases catheter use per patient when individuals require both chemotherapy and dialysis support. Public program expansion in countries such as India shows how higher service capacity can increase catheter placements in real care settings.

Increasing Preference for Power-Injectable Central Venous Catheters

Hospitals are increasingly adopting power-injectable systems as contrast-enhanced imaging becomes routine in cancer diagnosis, staging, and follow-up care. When catheters cannot support high-pressure contrast injection, clinicians often need an additional access step, which increases workload and patient inconvenience. Protocol-driven hospitals now treat power-injectable peripherally inserted central catheters (PICCs) and ports as standard specifications rather than optional premium upgrades. This shift benefits suppliers that combine catheter performance, insertion safety, and simplified workflow design in a single platform. BD’s CentroVena One launch reflects this direction, with a focus on integrated insertion, fewer procedural steps, and use in high-acuity environments.

Infection-Prevention Bundling and Chlorhexidine Adoption

Infection control remains a major factor shaping product selection in the central venous catheter market. Hospitals now assess standard and antimicrobial catheters within broader infection-prevention bundles that include insertion practices, dressing selection, barrier precautions, and coated devices. This approach makes premium catheter use easier to justify when infection reduction can be measured against reporting requirements and avoidable treatment costs. Teleflex reported a 70.5% reduction in central line-associated bloodstream infection (CLABSI) incidence in a multinational intensive care unit (ICU) cohort using Arrow chlorhexidine-impregnated catheters. This evidence supports broader formulary substitution and strengthens adoption across larger healthcare systems.

Longer Dwell-Time Use in Home Infusion and Ambulatory Settings

The central venous catheter market is gaining support from the shift toward decentralized care delivery. Patients receiving long-term antibiotics, parenteral nutrition, and repeated infusions are spending more treatment time outside traditional inpatient settings. This trend broadens demand for peripherally inserted central catheters (PICCs) and tunneled catheters that can remain in place for weeks or months without frequent replacement. APIC’s 2025 implementation guide will be important, as it extends infection-control focus beyond hospital central lines to outpatient and home vascular access. As surveillance, training, and securement practices improve, longer-dwell devices become easier to support at scale.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Catheter-related bloodstream infection risk | -0.6% | Global | Short term (≤ 2 years) |

| Clinical preference shift toward piccs in select settings | -0.5% | North America & EU | Medium term (2-4 years) |

| Pricing pressure from value-based procurement and tenders | -0.5% | APAC, EU | Medium term (2-4 years) |

| Regulatory burden for antimicrobial, coated, and novel devices | -0.4% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Catheter-Related Bloodstream Infection Risk

Infection risk continues to affect confidence in central access, despite stronger prevention protocols. The WHO’s 2024 guidance states that bloodstream infections associated with intravascular catheters require strict procedural discipline and continuous oversight. Hospitals also face reporting pressure, reimbursement consequences, and internal reviews when central line-associated bloodstream infection (CLABSI) events occur, extending the burden beyond clinical harm. Thrombosis adds further concern, as it can interrupt therapy, require catheter removal, and increase treatment costs for already fragile patients. A 2026 retrospective cohort study in BMC Surgery confirmed that tunneled non-cuffed centrally inserted catheters in oncology patients still carry meaningful thrombosis risk despite optimized placement protocols.[1]International Society of Nephrology, “Global Variations in Funding and Use of Hemodialysis Accesses, An International Report Using the ISN Global Kidney Health Atlas,” BMC Nephrology, link.springer.com This restraint remains important for the central venous catheter market because safety concerns can slow adoption when buyers compare central access with less invasive options in selected cases.

Pricing Pressure from Value-Based Procurement and Tenders

Purchasing models that prioritize cost control and contract scale also restrain the central venous catheter market. In many regions, hospitals and public systems evaluate catheters through tenders, group purchasing organization (GPO) agreements, or multi-year contracting frameworks, which limit pricing flexibility for suppliers. These models make it harder for manufacturers to pass on the added costs of antimicrobial coatings, integrated insertion designs, or other premium features unless they clearly document outcome benefits. Teleflex’s 2025 Vizient contract illustrates how large contracting channels increasingly shape supplier access and favor vendors with established evidence and national reach. Smaller players may offer viable products, but they often lack the clinical documentation or contracting leverage needed to defend higher price points in large procurement systems. As a result, the central venous catheter market can grow in volume while still facing pressure on average selling prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Long-Term Oncology Needs Are Lifting Implanted Port Demand

Peripherally inserted central catheters (PICCs) are expected to account for 38.12% of the product type segment in 2025, maintaining the leading position across intermediate-duration therapies. Their use remains strong in antibiotic infusion, chemotherapy cycles, and treatments that require reliable access without immediate surgical implantation. Non-tunneled catheters support acute hospital needs, while tunneled devices remain important in dialysis and chronic oncology care. This mix keeps the central venous catheter market balanced between high-volume acute use and durable long-term access.

Implanted ports are projected to be the fastest-growing product category, registering a 9.53% compound annual growth rate (CAGR) from 2026 to 2031, driven by stronger demand in oncology and pediatric care. Their fully subcutaneous design improves patient comfort, lowers visibility, and supports extended treatment needs. Hybrid concepts, such as PICC-PORT designs, indicate a shift toward flexible access options for difficult anatomies. This category is gaining importance as suppliers pursue differentiation in high-value and long-dwell applications.

By Lumen Type: Procedure Complexity Is Supporting More Channels per Catheter

Double lumen catheters are expected to hold a 42.45% share in 2025, making them the leading lumen type across dialysis and multi-drug hospital protocols. Dialysis requires simultaneous withdrawal and return, while oncology and intensive care regimens benefit from separated channels. Single lumen devices support simpler therapies, and triple lumen configurations remain relevant in high-acuity care. Lumen selection in the central venous catheter market remains closely linked to treatment complexity.

Multi-lumen catheters are projected to be the fastest-growing lumen category, registering an 8.67% CAGR through 2031, as care pathways require more simultaneous infusions through fewer insertion sites. Fewer insertion points can reduce patient access burden and simplify complex hospital protocols. Innovation is also advancing lumen-level performance, including surfaces designed to reduce clot formation and support longer use. Suppliers that improve channel functionality without complicating insertion are likely to stay well positioned.

By Material: Polyurethane Continues to Set the Performance Standard

Polyurethane is expected to account for 60.66% of the material segment in 2025, making it the dominant choice across most mainstream device formats. Its performance profile supports kink resistance, pushability, in-body softening, and compatibility with power injection in many use cases. Silicone continues to add value in selected long-dwell and pediatric applications where softness and compliance matter. The market continues to favor materials that support procedural efficiency and patient tolerance.

Other materials, including newer polymer blends and coated formulations, remain innovation areas but have not matched polyurethane’s installed base or scale. Procurement trends continue to support polyurethane because it offers a familiar platform that can incorporate antimicrobial or surface-enhanced features without disrupting workflow. A 2024 retrospective real-world study reported a 99% success rate and a 0.8% adverse event rate for chlorhexidine-silver sulfadiazine-coated polyurethane central venous catheters in 384 patients. This evidence strengthens buyer confidence in polyurethane-based platforms.

By Application: Nutrition Support Is Expanding Faster Than the Base of Drug Delivery

Drug administration is expected to remain the largest application segment, with a 52.67% share in 2025, as chemotherapy, antibiotics, and biologics continue to depend on stable central access. Blood transfusion and diagnostics also generate steady demand, particularly in oncology-linked and critical care pathways. Medication delivery remains the most frequent and operationally important use case across settings. This large installed base gives suppliers a stable platform as faster-growing applications expand.

Fluid and nutrition administration is projected to be the fastest-growing application, registering a 9.67% CAGR through 2031, marking a shift in central venous catheter use. Home parenteral nutrition, intensive care unit (ICU) nutritional support, and discharge models that extend therapy beyond inpatient care are supporting growth. When patients leave hospitals with ongoing nutrition needs, demand shifts toward longer outpatient management. A 2026 prospective observational study reported that PICCs represented 43.5% of all central venous access device (CVAD) insertions in hospitalized patients and found higher appropriateness rates for CVADs than for peripheral devices.

By End User: Site-of-Care Change Is Widening the Demand Base

Hospitals are expected to hold a 70.34% share in 2025, keeping them as the leading end-user group in the central venous catheter market. Their dominance reflects the concentration of intensive care, oncology treatment, interventional radiology, and complex inpatient procedures in hospital settings. Hospitals also remain the main environment for first placement in acute and high-risk cases, giving them strong influence over initial device selection. Specialty clinics are gaining relevance as dialysis units and oncology infusion centers expand central-access capabilities.

Ambulatory surgery centers (ASCs) are projected to be the fastest-growing end-user segment, registering an 8.87% CAGR from 2026 to 2031, as reimbursement and workflow pressures move suitable procedures into lower-cost settings. This trend favors products that reduce procedural steps, accelerate placement, and standardize performance across frequent procedures. Home healthcare is also gaining visibility, although expansion depends on nursing capacity, training, and coverage conditions. Suppliers that serve hospitals, ASCs, and home-linked care with fewer procedural burdens should have a clearer path to share retention.

Geography Analysis

North America is expected to hold a 41.56% share in 2025, maintaining its position as the largest regional block in the central venous catheter market. Strong infection-control standards, established hospital accreditation requirements, and broad adoption of premium antimicrobial and power-injectable device types support the region’s leadership. The United States remains especially important, as clinical protocols, mature contracting channels, and strong demand for workflow-improving technologies support premium device adoption. Canada and Mexico contribute steady growth, while product differentiation is shifting toward insertion systems, securement, and integrated workflow design rather than basic catheter access alone.

Europe remains the second-largest geographic block in the central venous catheter market, supported by large oncology treatment programs and established dialysis networks in Germany, France, and the United Kingdom. Italy and Spain add incremental demand through aging demographics and expanding outpatient infusion capabilities. Regulatory expectations under the European Union Medical Device Regulation increase the burden for newer entrants, especially in coated and antimicrobial categories where sustained post-market clinical follow-up remains important. B. Braun’s 2025 results, expected to be published in 2026, are expected to show EUR 584 million in research and development spending, with an 11% year-on-year increase, underlining continued investment in connected infusion and vascular access capabilities.

Asia-Pacific is the fastest-growing region in the central venous catheter market, with a projected compound annual growth rate of 10.56% from 2026 to 2031. Hospital capacity expansion, a rising chronic disease burden, and stronger public investment in dialysis and cancer care infrastructure drive regional growth. India benefits from dialysis program expansion, which supports tunneled catheter placement where fistula-based access is not yet available. China is developing along two tracks, with multinational suppliers competing on premium performance in top-tier hospitals while domestic manufacturers remain active in cost-sensitive procurement channels.

Competitive Landscape

The central venous catheter market shows moderate concentration, with BD, Teleflex, B. Braun, ICU Medical, and Fresenius Medical Care forming the core group of recognized global suppliers. These companies benefit from broad portfolios, established procurement relationships, and the ability to support product claims with clinical or operational evidence. Competition remains stronger in premium categories, where antimicrobial coatings, power-injectable designs, and workflow-oriented insertion systems offer more differentiation than standard catheter formats. As a result, the market depends not only on manufacturing scale but also on trust, outcomes evidence, and clinical usability.

BD is expected to strengthen its position in 2026 with the commercial launch of CentroVena One, an integrated all-in-one insertion system designed to reduce steps and shorten procedure time. This move shifts competition toward the total insertion workflow rather than catheter choice alone. Teleflex is taking a different but equally strategic path by combining clinical evidence development for Arrow chlorhexidine-impregnated catheters with the July 2025 acquisition of BIOTRONIK’s vascular intervention business. Together, these actions are expected to expand product credibility and channel reach within the central venous catheter market.

A second theme is portfolio rationalization, as some companies are narrowing their focus rather than defending every catheter category simultaneously. The user-supplied draft cited AngioDynamics’ 2024 divestiture of its peripherally inserted central catheter (PICC) and Midline portfolios to Spectrum Vascular for up to USD 45 million, showing that specialized positioning can be more defensible than broad exposure in lower-margin lines. The market also leaves room for lower-cost regional suppliers in government-linked and tender-heavy environments, especially in parts of Asia. However, large global suppliers retain an advantage when hospitals want a single vendor that can support evidence, service, training, and procurement coverage across multiple product tiers.

Central Venous Catheter Industry Leaders

Teleflex Incorporated

B. Braun SE

Becton, Dickinson and Company

ICU Medical, Inc.

Edwards Lifesciences Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Vizient awarded BD’s CentroVena One Insertion System an Innovative Technology contract, citing its 30% fewer insertion steps and safety features addressing air embolism and needlestick risks.

- April 2026: Becton, Dickinson and Company launched the BD CentroVena One Insertion System in the United States, integrating key CVC insertion components and reducing insertion steps by 30% and maximum procedure time by 50%.

- July 2025: Teleflex Incorporated acquired substantially all of BIOTRONIK SE & Co. KG’s Vascular Intervention business, expanding its therapeutic vascular portfolio and strengthening its catheter-lab channel.

- June 2025: Teleflex published study findings showing a 70.5% reduction in CLABSI incidence among ICU patients using Arrow Chlorhexidine-Impregnated CVCs, Arrowg+ard Blue, and Arrowg+ard Blue Plus compared to non-impregnated catheters.

Global Central Venous Catheter Market Report Scope

As per the scope of the report, a central venous catheter (CVC), or "central line," is a long, flexible tube inserted into a large vein in the chest, neck, or arm. Its tip rests near the heart, allowing doctors to deliver medications, fluids, or nutrition directly into the bloodstream and draw blood samples.

The central venous catheter market is segmented by product type, lumen type, material, application, end user, and geography. By product type, the market includes non-tunneled central venous catheters, tunneled central venous catheters, peripherally inserted central catheters, and implanted ports. By lumen type, the market is segmented into single lumen, double lumen, triple lumen, and multi-lumen. By material, the market includes polyurethane, silicone, and other materials. By application, the market is segmented into drug administration, fluid and nutrition administration, blood transfusion, and diagnostics and testing. By end user, the market includes hospitals, ambulatory surgery centers, specialty clinics, and home healthcare settings. By geography, the market is analyzed across key regions globally. The report offers the market sizes and forecasts for the above segments.

| Non-Tunneled Central Venous Catheters |

| Tunneled Central Venous Catheters |

| Peripherally Inserted Central Catheters |

| Implanted Ports |

| Single Lumen |

| Double Lumen |

| Triple Lumen |

| Multi-Lumen |

| Polyurethane |

| Silicone |

| Other Materials |

| Drug Administration |

| Fluid and Nutrition Administration |

| Blood Transfusion |

| Diagnostics and Testing |

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty Clinics |

| Home Healthcare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Non-Tunneled Central Venous Catheters | |

| Tunneled Central Venous Catheters | ||

| Peripherally Inserted Central Catheters | ||

| Implanted Ports | ||

| By Lumen Type | Single Lumen | |

| Double Lumen | ||

| Triple Lumen | ||

| Multi-Lumen | ||

| By Material | Polyurethane | |

| Silicone | ||

| Other Materials | ||

| By Application | Drug Administration | |

| Fluid and Nutrition Administration | ||

| Blood Transfusion | ||

| Diagnostics and Testing | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Specialty Clinics | ||

| Home Healthcare Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for the central venous catheter market?

The central venous catheter market is valued at USD 2.69 billion in 2026 and is forecast to reach USD 3.67 billion by 2031 at a 6.40% CAGR. Growth is tied to oncology, dialysis, critical care, and longer-duration infusion use.

Which product type is leading central venous catheter demand?

PICCs led product demand with a 38.12% share in 2025. They remain widely used for intermediate-duration therapy across antibiotics, chemotherapy, and hospital-based infusion care.

Which product segment is growing the fastest through 2031?

Implanted ports are the fastest-growing product type, with a projected 9.53% CAGR through 2031. Their growth is linked to long-term oncology and pediatric use where patient comfort and lower external exposure matter.

Why is North America the largest regional revenue contributor?

North America held 41.56% share in 2025 because the region has mature infection-control protocols, strong premium device adoption, and hospital systems that value procedural safety and integrated workflow improvements.

Which application is expanding most quickly in this space?

Fluid and nutrition administration is the fastest-growing application, with a 9.67% CAGR through 2031. Home parenteral nutrition and ICU nutrition support are widening catheter use beyond drug delivery alone.

What is the main competitive theme among major suppliers?

Large suppliers are competing through premium features, clinical evidence, and workflow simplification. Recent examples include BD's CentroVena One launch and Teleflex's expansion through clinical studies and the BIOTRONIK vascular intervention acquisition.

Page last updated on: