Bovine Pericardial Valve Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

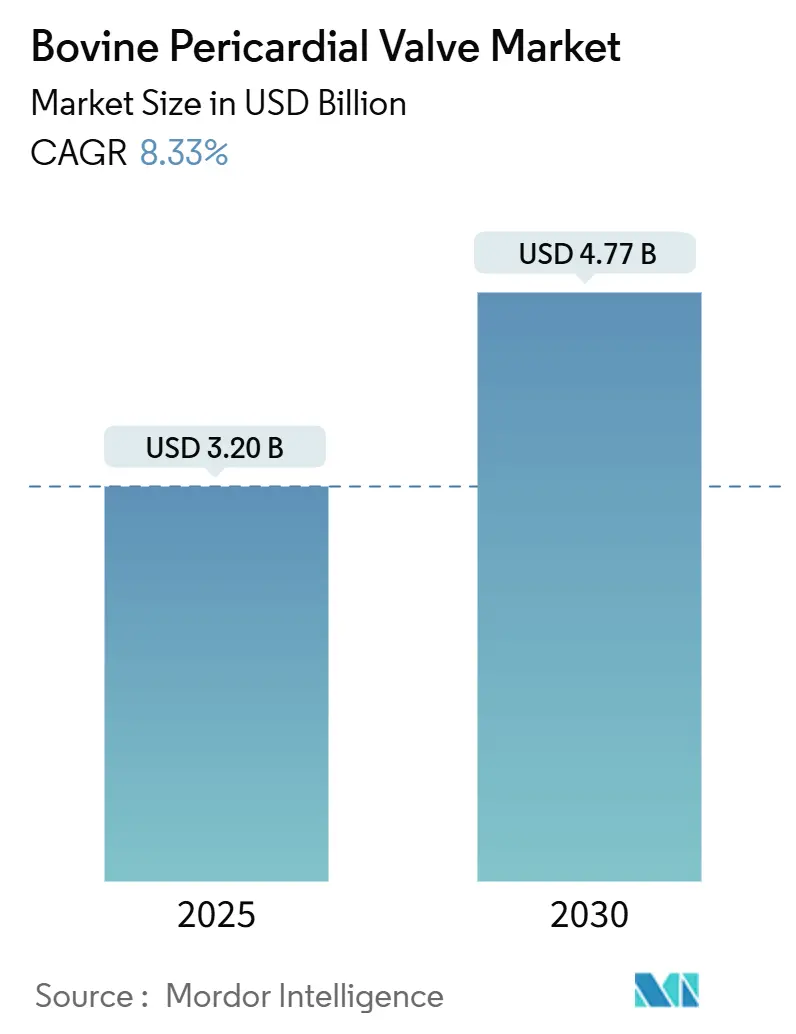

| Market Size (2025) | USD 3.20 Billion |

| Market Size (2030) | USD 4.77 Billion |

| Growth Rate (2025 - 2030) | 8.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bovine Pericardial Valve Market Analysis by Mordor Intelligence

The Bovine Pericardial Valve Market size is estimated at USD 3.20 billion in 2025, and is expected to reach USD 4.77 billion by 2030, at a CAGR of 8.33% during the forecast period (2025-2030).

Continuous demographic aging, earlier‐stage transcatheter indications, and anti-calcification tissue innovations are expanding the eligible patient pool and lengthening device life cycles. Hospitals are shifting valve replacement volumes toward cardiac catheterization suites that favor conscious sedation, shortening stays and improving throughput. Competitive momentum is intensifying as emerging Asian and European manufacturers introduce intermediate and extra-large sizes that reduce leaflet overexpansion and paravalvular leak. Regulatory bodies in North America, Europe, and Asia-Pacific now tie premium reimbursement to registry-based outcomes, rewarding devices that show durable hemodynamics beyond five years.

Key Report Takeaways

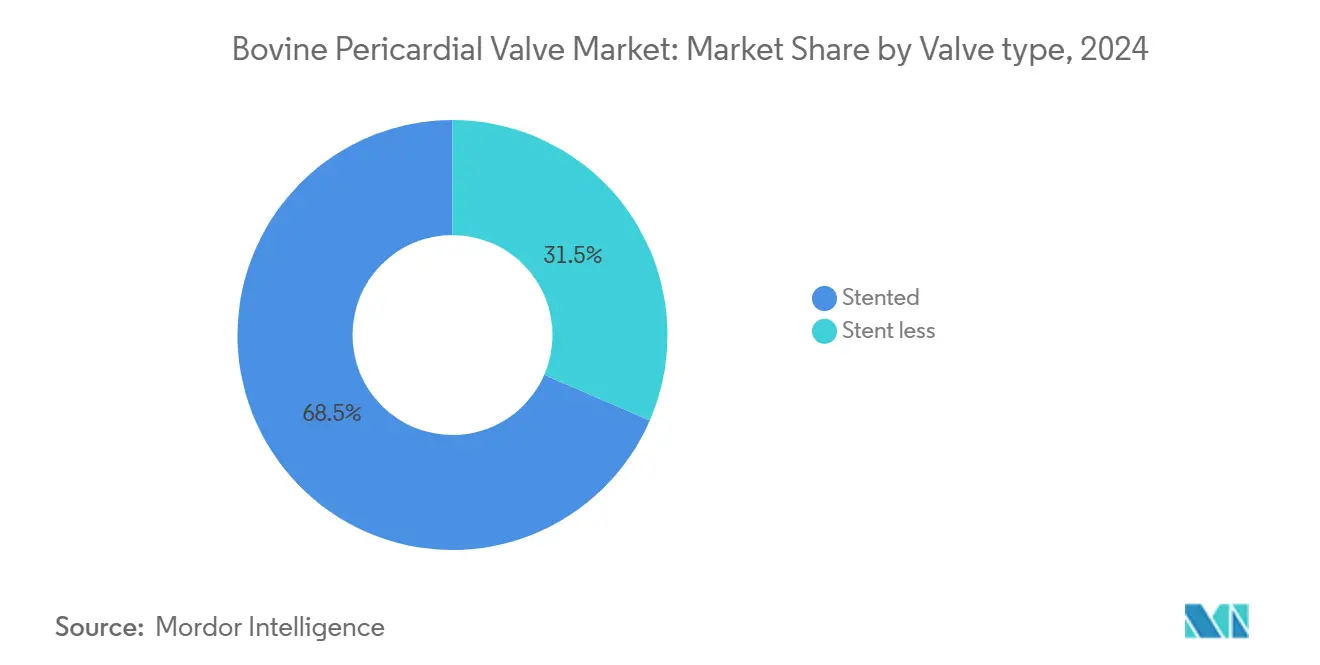

- By Valve Type, Stented valves captured 68.5% of bovine pericardial valve market share in 2024 and will remain the revenue leader through 2030. Stentless valves are forecast to grow at an 11.4% CAGR between 2025 and 2030, the fastest rate among valve types.

- By Delivery Method, Transcatheter delivery accounted for the highest growth trajectory at 14.8% CAGR, while surgical implantation retained the largest volume base in 2024.

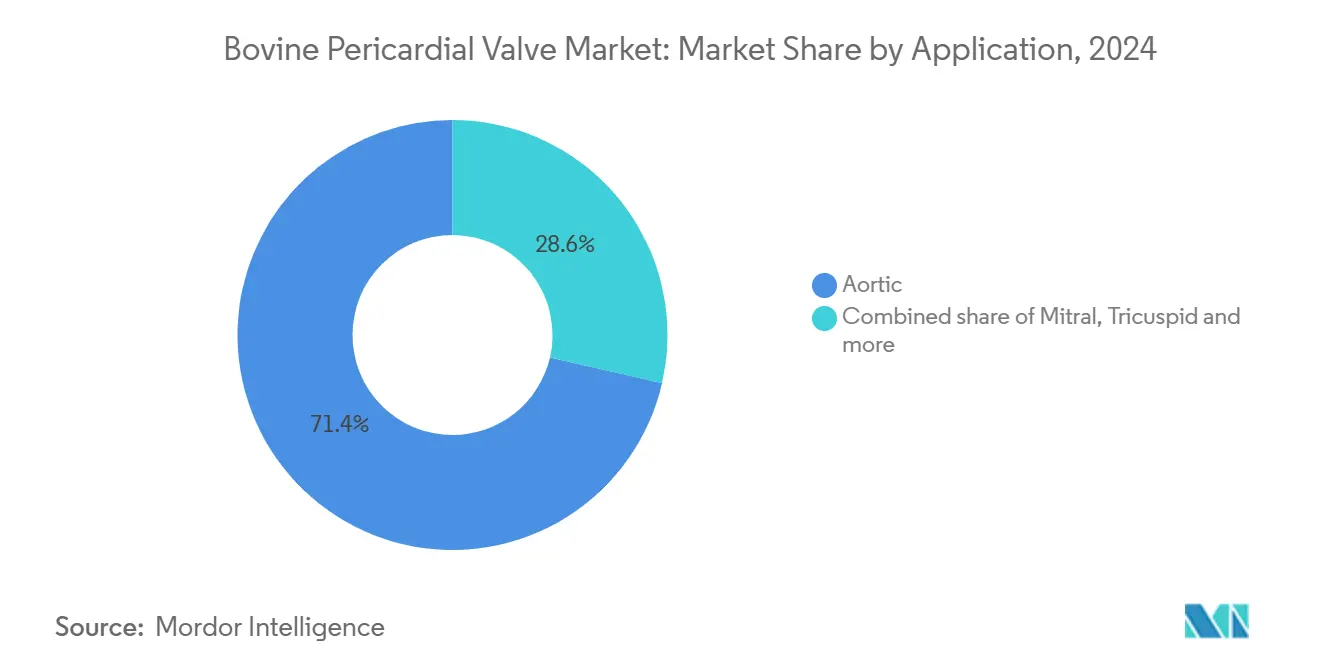

- By Application, Aortic procedures dominated with 71.4% revenue in 2024; tricuspid interventions are set to post a 12.9% CAGR to 2030.

- By Alloy / Frame Material, Cobalt-chrome frames held 44.2% of 2024 sales, yet titanium frames lead growth at 13.5% CAGR on imaging and sealing advantages.

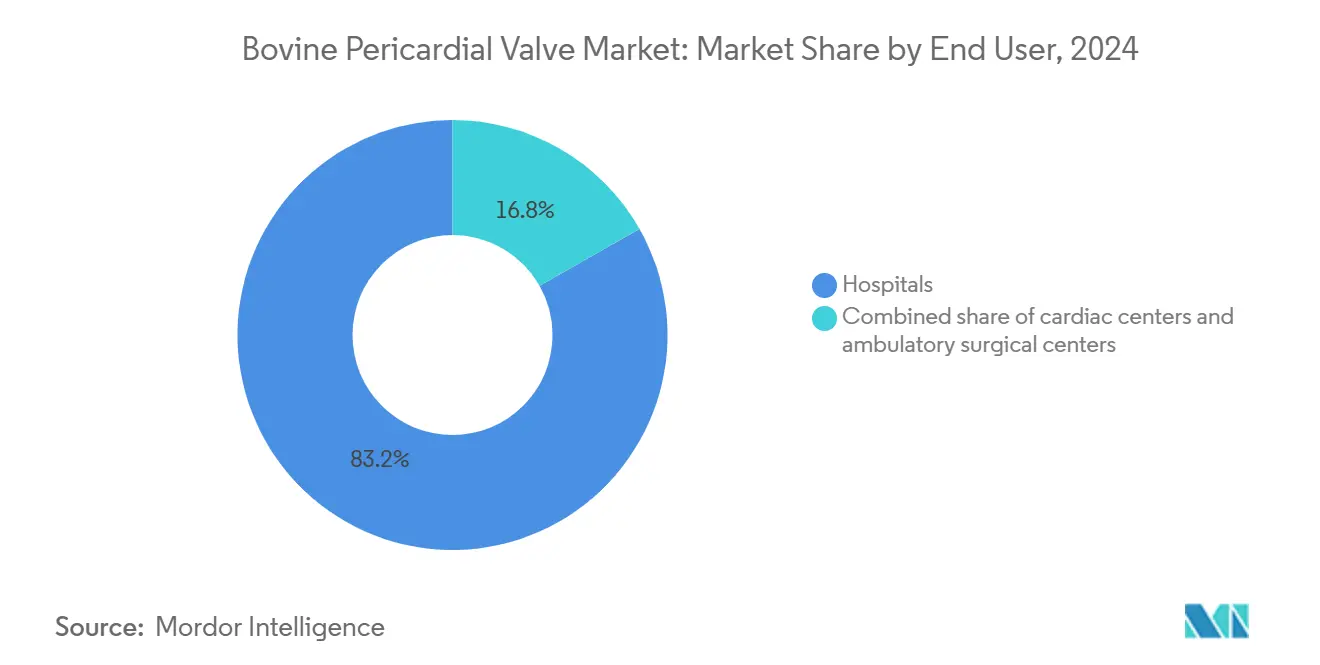

- By End User, Hospitals and diagnostic laboratories performed 83.2% of 2024 procedures, but cardiac centers are expanding fastest at 12.4% CAGR.

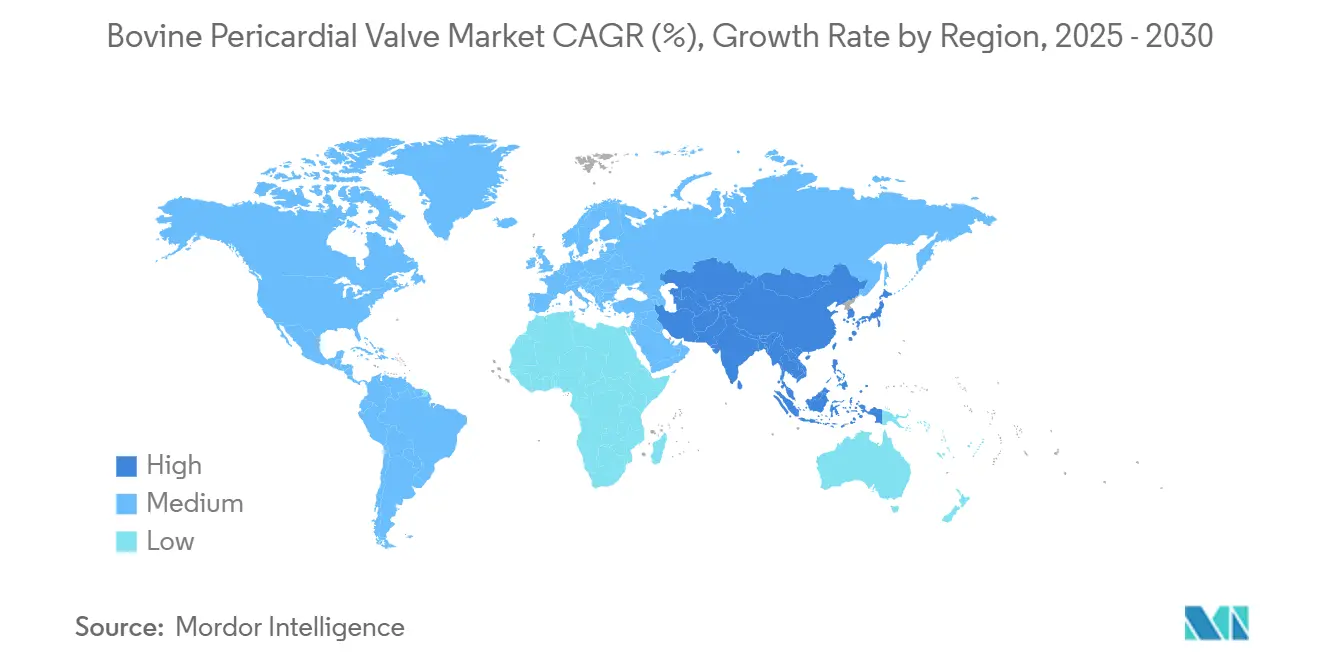

- By Geography, North America remained the largest region with 40.5% revenue in 2024, while Asia-Pacific will be the most dynamic, advancing at 11.7% CAGR through 2030.

Global Bovine Pericardial Valve Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of valvular heart diseases in aging population | +2.1% | Japan, Germany, Italy, North America | Long term (≥ 4 years) |

| Growing adoption of minimally-invasive transcatheter procedures | +2.8% | North America, Europe, China, Japan, India | Medium term (2-4 years) |

| Advancements in anti-calcification and durability treatments | +1.6% | North America, Europe | Long term (≥ 4 years) |

| Favorable reimbursement for bioprosthetic valve replacements | +1.4% | United States, Germany, France, Japan | Short term (≤ 2 years) |

| Expansion of intermediate and XL-sized THVs for large annuli | +1.2% | North America, Europe | Medium term (2-4 years) |

| Surge in valve-in-valve reoperations of legacy tissue valves | +0.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Valvular Heart Diseases in Aging Population

Adults aged ≥65 will exceed 20% of the population in Japan, Italy, and Germany by 2030, accelerating demand for aortic stenosis interventions in cohorts with multiple comorbidities. Five-year data from SOLVE-TAVI showed 41.5% mortality with conscious sedation versus 54.3% with general anesthesia, highlighting the benefit of less invasive care in frail patients. China’s regulator cleared Venus Medtech’s VenusP-Valve and encouraged domestic platforms priced 40–50% below imports, broadening access. These factors collectively push operators to favor transcatheter approaches and enlarge the bovine pericardial valve market.

Growing Adoption of Minimally-Invasive Transcatheter Procedures

Transcatheter volumes are rising in cardiac catheterization centers that achieve shorter door-to-deployment times and same-day discharge protocols. The LANDMARK trial (768 patients) confirmed Myval’s non-inferiority to SAPIEN and Evolut with fewer post-dilatations. Edwards introduced SAPIEN 3 Ultra with RESILIA tissue, lowering moderate-to-severe paravalvular leak in European real-world use. Boston Scientific’s ACURATE Prime gained CE Mark with frame refinements that equalize radial force and protect coronary access. Procedure migration toward lower-acuity sites is therefore accelerating bovine pericardial valve market expansion.

Advancements in Anti-Calcification & Durability Treatments

Residual aldehydes from glutaraldehyde fixation catalyze leaflet calcification, but detoxification chemistries such as RESILIA and ADAPT neutralize these moieties. Seven-year COMMENCE results for RESILIA showed durable gradients and freedom from structural degeneration. Anteris’ single-piece DurAVR restored mean gradients to 13.76 mmHg in valve-in-valve cases, matching immediate post-surgical results despite prior degeneration. Although long-term human data are still emerging, these findings strengthen confidence in bovine pericardial valve longevity.

Favorable Reimbursement for Bioprosthetic Valve Replacements

In 2025, the FDA cleared SAPIEN for asymptomatic severe aortic stenosis, and CMS aligned coverage to support earlier intervention [1]U.S. Food and Drug Administration, “Premarket Approval Supplement,” CMS also placed EVOQUE tricuspid therapy under Coverage with Evidence Development, shifting financial risk away from hospitals while real-world data accrue [2]Centers for Medicare & Medicaid Services, “Coverage with Evidence Development,”. Germany reimburses certified centers 15–20% above surgical rates, incentivizing high-volume practice consolidation. Japan approved multiple platforms in 2024, albeit at reimbursement 30–40% below U.S. levels, spurring cost-optimized local manufacturing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural valve deterioration triggering reoperations | -1.3% | Global, higher in younger cohorts | Long term (≥ 4 years) |

| High device and procedure cost in emerging markets | -1.1% | Latin America, Middle East & Africa, South Asia | Medium term (2-4 years) |

| Elevated long-term endocarditis risk versus porcine valves | -0.4% | Global, immunocompromised groups | Long term (≥ 4 years) |

| Competitive threat from next-generation polymer heart valves | -0.6% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Structural Valve Deterioration Triggering Reoperations

Carpentier-Edwards Perimount showed 6.3% structural degeneration at a 112-month mean follow-up, with 2.5% reintervention. Residual aldehydes accelerate calcification, and PARTNER 3 logged 2.5% thrombosis in SAPIEN 3 recipients at five years. Although decellularization and alternative crosslinkers reduce calcification in models, long-term human durability remains unproven, tempering uptake in younger patients.

High Device & Procedure Cost in Emerging Markets

A full transcatheter kit can exceed USD 25,000, far above per-capita health spending in Latin America or Sub-Saharan Africa. Public payers in Brazil and Argentina limit coverage to prohibitive-risk cases, creating a two-tier treatment landscape. Domestic Indian and Chinese suppliers offer valves priced up to 50% lower than Western imports, but quality perception gaps and sparse durability data restrain broader bovine pericardial valve market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Type: Stent less Designs Gain Traction in Younger Cohorts

Stented valves accounted for 68.5% of the bovine pericardial valve market in 2024, underpinned by the ease of anchoring rigid frames in calcified annuli. Stentless alternatives will, however, post an 11.4% CAGR through 2030, reflecting demand from younger patients who benefit from larger effective orifice areas and easier future valve-in-valve access. Evidence from a 2,500-patient Perceval registry showed shorter bypass times but higher pacemaker rates, illustrating both the advantage and trade-offs of suture less technology.

Surgeons at high-volume centers now favor supra-annular hemodynamics for recipients expected to undergo multiple reinterventions over their lifetime. This approach reduces patient-prosthesis mismatch, a driver of late heart failure symptoms, and thereby enlarges the bovine pericardial valve market by improving long-term quality of life.

By Delivery Method: Transcatheter Approaches Reshape Procedural Volumes

Surgical implantation still delivered 56.3% of 2024 unit sales, yet transcatheter cases are climbing at a 14.8% CAGR. Conscious-sedation protocols lowered five-year mortality by 12.8 percentage points in SOLVE-TAVI, cementing operator preference for catheter-based therapy. The bovine pericardial valve market size for transcatheter platforms is therefore expanding rapidly within outpatient centers.

Regulatory clearance for asymptomatic aortic stenosis further tilts volume toward catheter-based approaches, while surgical procedures remain critical for bicuspid anatomy or combined coronary bypass cases.

By Application: Tricuspid Interventions Surge as Reimbursement Pathways Clarify

Aortic disease held 71.4% of 2024 revenue, yet tricuspid therapy will grow fastest at 12.9% CAGR through 2030 on the back of EVOQUE’s CMS registry pathway. Mitral indications lag due to complex anatomy and coronary proximity. As data accumulate, the bovine pericardial valve market size for tricuspid repair is poised to rise, attracting new entrants focused on right-sided pathology.

Operators now treat severe tricuspid regurgitation once deemed inoperable, expanding the candidate pool and creating fresh commercial headroom.

By Alloy/Frame Material: Titanium Gains Share on Imaging and Compliance Advantages

Cobalt-chrome frames delivered 44.2% of 2024 revenue, but titanium is projected to grow at 13.5% CAGR owing to radiolucency and lower elastic modulus. Improved visualization reduces follow-up imaging artifact, and a more compliant frame lowers paravalvular leak when the device is oversized. These benefits have heightened clinician demand and will gradually re-mix material share inside the bovine pericardial valve market.

Nitinol retains superiority in self-expanding systems, although nickel sensitivity and supply-chain risks prompt diversification, as evidenced by Abbott’s multi-source tubing approval.

By End User: Cardiac Centers Consolidate Expertise and Negotiate Bundled Payments

Hospitals and diagnostic labs performed 83.2% of all interventions in 2024, but specialist cardiac centers are growing at 12.4% CAGR by leveraging volume-based procurement and bundled payer contracts. High-volume operators have documented lower 30-day mortality, and payers now channel patients to centers executing ≥50 transcatheter cases annually. This shift concentrates purchasing power, shaping competitive dynamics inside the bovine pericardial valve market.

Ambulatory surgery centers may capture selective low-risk cases once reimbursement codes mature, suggesting further venue redistribution by the decade’s end.

Geography Analysis

North America generated 40.5% of 2024 revenue, supported by CMS expansion into low-risk and asymptomatic cohorts, and by registry-linked reimbursement that rewards durable outcomes. FDA approval for asymptomatic treatment in 2025 further enlarges the bovine pericardial valve market. Canada follows similar protocols but faces provincial budget ceilings that trim per-capita procedure penetration.

Europe benefits from mature structural heart programs in Germany, France, and the United Kingdom. CE Mark approvals for ACURATE Prime and SAPIEN 3 Ultra widened device choice and contained pacemaker and leak rates. Certified centers receive up to 20% higher reimbursement than surgical replacement, reinforcing procedural migration.

Asia-Pacific is the fastest-growing region at an 11.7% CAGR. China’s NMPA supports domestic developers such as Venus Medtech, while Japan’s super-aged demographic and limited surgical capacity accelerate transcatheter uptake. India remains cost-sensitive, prompting localization initiatives that could add volume once quality perceptions improve.

Competitive Landscape

Edwards Lifesciences and Medtronic together hold a majority share, yet new entrants are eroding this lead through design innovation and granular sizing. Edwards purchased J-Valve in 2024 to strengthen its Chinese position and diversify into mitral therapy [3]Edwards Lifesciences, “Investor Conference 2024,” . Meril’s LANDMARK study verified non-inferiority to incumbents with fewer post-dilatations, supporting global roll-out in price-sensitive markets.

Boston Scientific’s ACURATE Prime adds an extra valve size and optimizes radial force, aiming to match SAPIEN’s hemodynamics while preserving coronary access. Anteris Technologies advances single-piece biomimetic tissue that mimics native valve flow and facilitates commissural alignment. Domestic Chinese firms leverage cost advantages and local approval pathways to capture regional share, while polymer valve developers threaten long-term with calcification-free leaflets.

Bovine Pericardial Valve Industry Leaders

Edwards Lifesciences Corporation

Medtronic plc

Abbott Laboratories

Boston Scientific Corporation

MERIL LIFE SCIENCES INDIA PRIVATE LIMITED

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Edwards Lifesciences received FDA approval to use SAPIEN in asymptomatic severe aortic stenosis, broadening the eligible population.

- November 2024: Meril Life Sciences launched Myval Octapro, lowering moderate-to-severe paravalvular regurgitation to 2.8% in core-lab analysis.

- October 2024: MicroPort’s 4C Medical began the ATLAS pivotal trial for AltaValve in severe mitral and tricuspid regurgitation.

- October 2024: Abbott gained approval for an alternative nitinol supplier for the 35 mm Navitor Titan valve

- August 2024: Boston Scientific secured CE Mark for ACURATE Prime, extending its annular range

Global Bovine Pericardial Valve Market Report Scope

As per the scope of the report, the bovine pericardial valve is a bioprosthetic heart valve made from the pericardium of cow. It is widely used to replace diseased heart valves offering a more natural blood flow pattern than mechanical valves and avoiding lifelong anticoagulation in most cases.

The bovine pericardial valve market is segmented by valve type, delivery method, application, alloy/frame material end user, and geography. By valve type, the market is categorized into stented, and stentless. By delivery method, it is segmented into surgical implantation, and transcatheter (TAVR / TMVR / TPVR). By application the market is divided into aortic, mitral, tricuspid, and pulmonary. By alloy/ frame material the market is segmented into cobalt-chrome, titanium, nickel-molybdenum, and others (stainless steel, nitinol and more). By end user, the segmentation includes hospitals, cardiac centres, and ambulatory surgery centers. Geographically, the market is analyzed across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Stented |

| Stentless |

| Surgical Implantation |

| Transcatheter (TAVR / TMVR / TPVR) |

| Aortic |

| Mitral |

| Tricuspid |

| Pulmonary |

| Cobalt-Chrome |

| Titanium |

| Nickel-Molybdenum |

| Others (Stainless Steel, Nitinol and more) |

| Hospitals |

| Cardiac Centres |

| Ambulatory Surgery Centres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Valve Type | Stented | |

| Stentless | ||

| By Delivery Method | Surgical Implantation | |

| Transcatheter (TAVR / TMVR / TPVR) | ||

| By Application (Valve Position) | Aortic | |

| Mitral | ||

| Tricuspid | ||

| Pulmonary | ||

| By Alloy / Frame Material | Cobalt-Chrome | |

| Titanium | ||

| Nickel-Molybdenum | ||

| Others (Stainless Steel, Nitinol and more) | ||

| By End User | Hospitals | |

| Cardiac Centres | ||

| Ambulatory Surgery Centres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the bovine pericardial valve market in 2025?

The bovine pericardial valve market size is USD 3.2 billion in 2025 and is projected to reach USD 4.77 billion by 2030

Which delivery approach is growing fastest?

Transcatheter implantation is expanding at a 14.8% CAGR through 2030 as centers adopt conscious-sedation protocols and earlier-stage indications.

What segment leads future growth by valve type?

Stent less valves will post the highest growth, advancing at an 11.4% CAGR due to better hemodynamics and valve-in-valve compatibility

Why are titanium frames gaining traction?

Titanium’s radiolucency eases imaging follow-up and its lower elastic modulus reduces paravalvular leak, driving a 13.5% CAGR through 2030.

Page last updated on: