Prosthetic Heart Valve Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

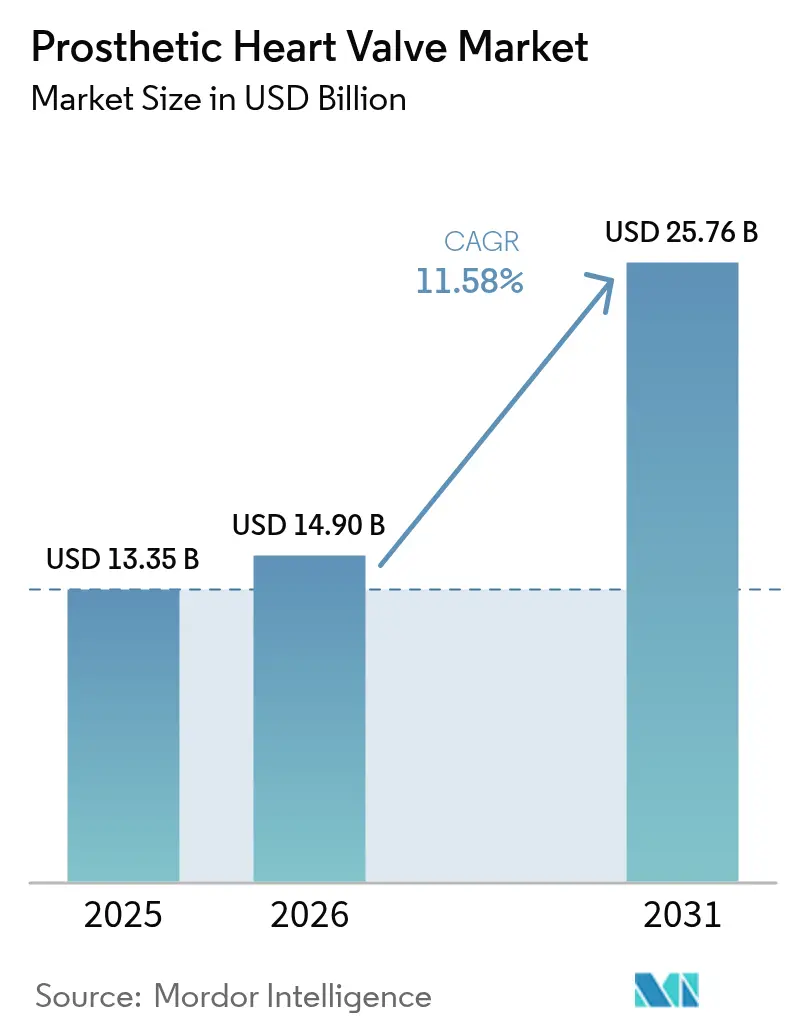

| Market Size (2026) | USD 14.9 Billion |

| Market Size (2031) | USD 25.76 Billion |

| Growth Rate (2026 - 2031) | 11.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prosthetic Heart Valve Market Analysis by Mordor Intelligence

prosthetic heart valve market size in 2026 is estimated at USD 14.9 billion, growing from 2025 value of USD 13.35 billion with 2031 projections showing USD 25.76 billion, growing at 11.58% CAGR over 2026-2031. Demographic ageing, expanded indications for transcatheter aortic valve replacement (TAVR), and faster regulatory reviews position transcatheter innovation as the primary growth engine of the prosthetic heart valve market. Edwards Lifesciences obtained United States Food and Drug Administration (FDA) approval in May 2025 for the SAPIEN 3 platform in asymptomatic severe aortic stenosis, enlarging the treatable population beyond symptomatic patients. Transcatheter heart valves held 45.55% of revenue in 2024, while tricuspid systems such as Edwards’ EVOQUE and Abbott’s TriClip have accelerated into double-digit growth after first-in-class clearances. Hospitals continue to dominate procedure volumes, yet ambulatory surgical centers (ASCs) are expanding fastest as same-day discharge protocols reduce inpatient reliance. North America generates the largest share, but Asia-Pacific is the high-growth frontier thanks to local approvals like MicroPort’s VitaFlow Liberty Flex in China. Portfolio consolidation—exemplified by Edwards’ USD 300 million Innovalve purchase and Johnson & Johnson’s USD 1.7 billion V-Wave deal—further intensifies competition.

Key Report Takeaways

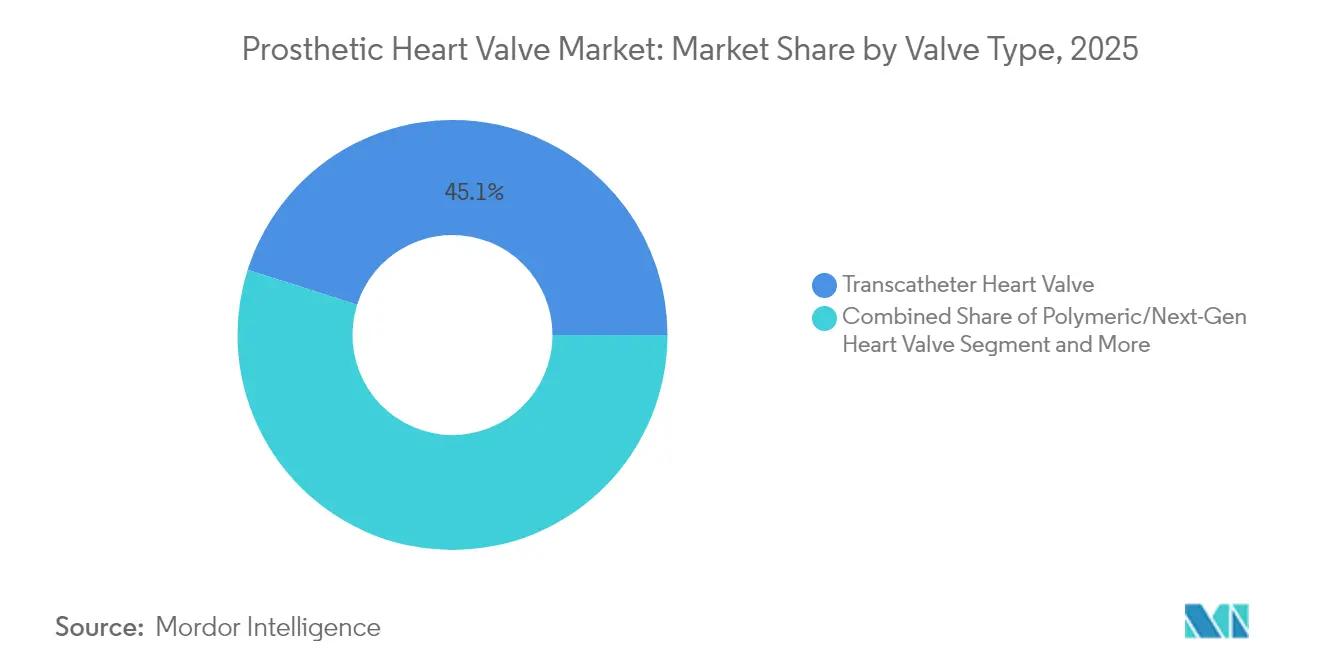

- By valve type, transcatheter heart valves led with 45.10% revenue share in 2025; polymeric valves are forecast to expand at an 17.74% CAGR through 2031.

- By position, aortic procedures accounted for 56.02% of the prosthetic heart valve market share in 2025, while tricuspid interventions register the highest projected CAGR at 14.92% to 2031.

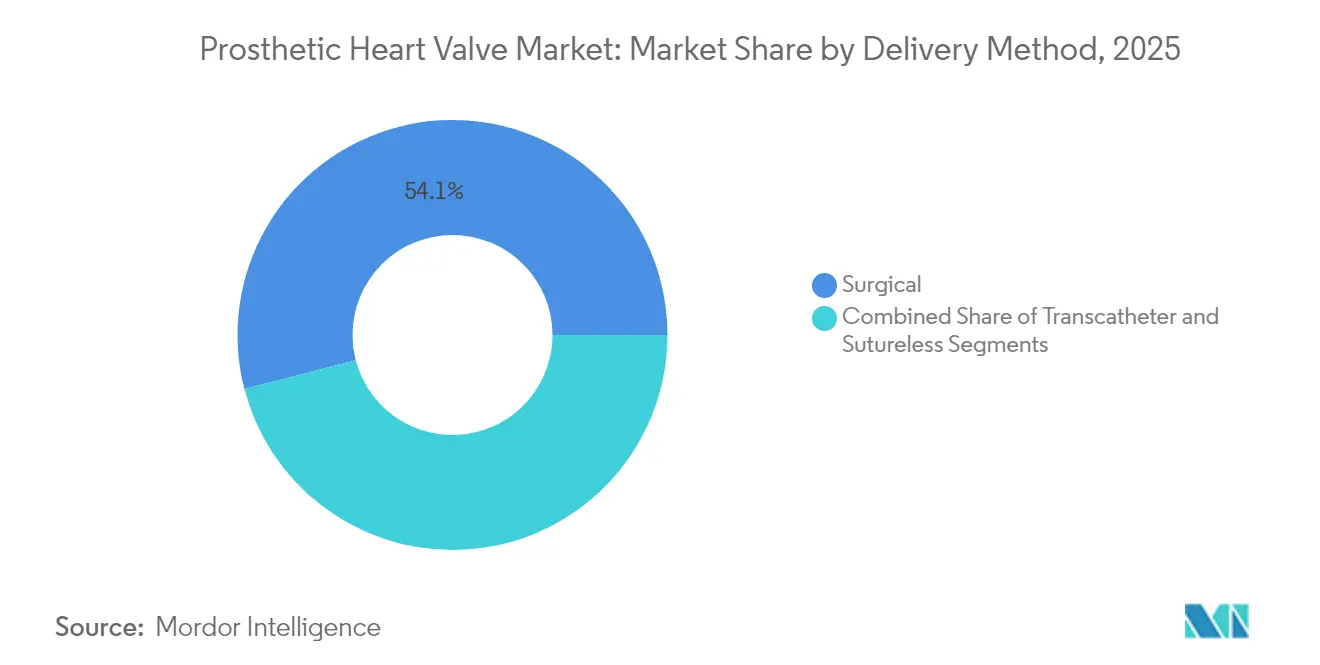

- By delivery method, surgical approaches retained 54.05% share in 2025, yet sutureless/rapid-deployment solutions are expected to grow at 13.31% CAGR to 2031.

- By end-user, tertiary-care hospitals held 45.20% of prosthetic heart valve market size in 2025, whereas ASCs are advancing at a 13.98% CAGR through 2031.

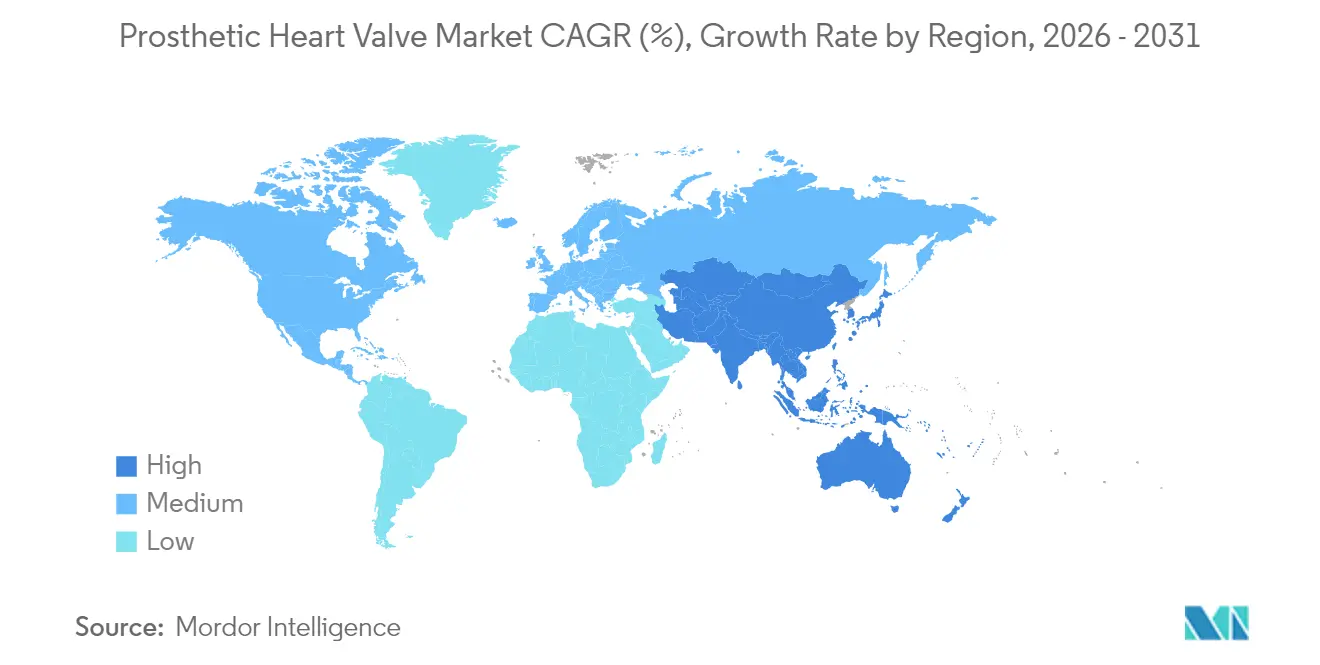

- By geography, North America commanded 42.10% revenue in 2025, but Asia-Pacific is projected to post the fastest 13.90% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Prosthetic Heart Valve Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Rising VHD Prevalence | +2.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Expanding Indications For TAVR/TAVI | +3.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Regulatory Fast-Tracks & Breakthrough Designations | +1.9% | North America & Europe | Short term (≤ 2 years) |

| Reimbursement Expansion In Middle-Income Countries | +1.5% | APAC, Latin America, Middle East | Medium term (2-4 years) |

| Polymeric Valve R&D Breakthroughs | +1.8% | Global, led by North America & Europe | Long term (≥ 4 years) |

| AI-Guided Patient Selection & Sizing Tools | +0.8% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Indications for TAVR/TAVI

The May 2025 FDA approval of Edwards’ SAPIEN 3 platform for asymptomatic severe aortic stenosis removes the “watchful waiting” mindset, allowing clinicians to intervene before symptom onset. EARLY TAVR data showed 26.8% adverse events with early treatment versus 45.3% under surveillance during 3.8-year follow-up, validating proactive therapy and effectively doubling the addressable pool. Edwards forecasts TAVR sales of USD 4.1–4.4 billion in 2025, and rivals such as Abbott have launched the ENVISION trial to capture lower-risk patients. Centers for Medicare & Medicaid Services (CMS) coverage decisions will shape adoption because private payers typically mirror Medicare precedent. As coverage broadens, procedure volumes rise, reinforcing the prosthetic heart valve market’s shift toward transcatheter dominance.

Regulatory Fast-Tracks & Breakthrough Designations

Breakthrough device designations hit a record 1,041 by September 2024; 128 authorized products demonstrate how the pathway compresses approvals from 3-5 years to around 18–24 months[1]U.S. Food and Drug Administration, “Breakthrough Devices Program,” fda.gov. Edwards’ EVOQUE tricuspid valve capitalized on breakthrough status to secure February 2024 clearance, while 4C Medical’s polymer AltaValve holds two breakthrough labels. Europe parallels this urgency, granting the world’s first transfemoral mitral CE mark to SAPIEN M3 in April 2025. Companies that lock in early designations gain speed-to-market advantages, boosting revenue and brand positioning within the prosthetic heart valve market.

Polymeric Valve R&D Breakthroughs

Polymeric technology combines durability with hemocompatibility, addressing a key limitation of bioprosthetic devices that typically require replacement after 10–15 years. Foldax’s TRIA valve reported favorable 2024 outcomes without the need for lifelong anticoagulation. Peijia Medical and dsm-firmenich are tailoring polymers to resist calcification, while Georgia Tech’s 3D-printed bioresorbable valve fosters native tissue regeneration. Institutional investors such as the British Heart Foundation have funded block co-polymer platforms to reduce long-term failure rates[2]British Heart Foundation, “New Artificial Heart Valve,” bhf.org.uk. As data accrue, polymeric designs could re-set durability benchmarks and widen the prosthetic heart valve market.

AI-Guided Patient Selection & Sizing Tools

Machine-learning models achieved 82.2% sensitivity and 98.1% specificity in detecting severe aortic stenosis across Medicare cohorts. Early identification shortens time to therapy and improves outcomes. During procedures, AI-based sizing cuts paravalvular leak and conduction disturbance risk, which is critical for transcatheter approaches. Edwards and Medtronic embed algorithms in pre-operative platforms, evidencing convergence between software and hardware. Predictive analytics also flag structural valve deterioration, allowing proactive follow-up. Facilities using AI achieve smoother workflows that lift success rates, fostering wider adoption and fueling prosthetic heart valve market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TAVR Device & Procedure Costs | -2.1% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Durability Concerns In Younger Cohorts | -1.8% | Global, particularly North America & Europe | Long term (≥ 4 years) |

| Limited Cath-Lab Capacity Outside Tier-1 Cities | -1.3% | APAC, Latin America, Africa | Medium term (2-4 years) |

| Surge In Valve-In-Valve Re-Interventions | -0.9% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High TAVR Device & Procedure Costs

Commercial US payers reimburse a median USD 71,312 for TAVR, versus Medicare’s USD 37,865; Aetna tops at USD 84,190, and prices vary two-fold between New England and Pacific regions. Europe and North America together spend over USD 2 billion annually on TAVR, pressuring budgets. Emerging markets face larger hurdles, as devices can exceed annual per-capita healthcare outlays. Spain’s incremental cost-effectiveness ratio of EUR 6,952 per QALY is below threshold, but payer constraints limit immediate uptake. Manufacturers are exploring value-based contracts, yet high prices remain a brake on the prosthetic heart valve market.

Durability Concerns in Younger Cohorts

Transcatheter structural deterioration data remain immature for patients under 60. Surgical bioprostheses in individuals ≤50 show 41.9% freedom from failure at 15 years, raising caution. TAVR valves may deteriorate faster, and redo valve-in-valve procedures carry hemodynamic penalties. Edwards’ RESILIA tissue offers 99.3% eight-year durability, yet clinicians await decade-plus outcomes before widely extending indications to younger, low-risk cohorts. Until long-term confidence builds, skepticism may temper the prosthetic heart valve market’s expansion into younger demographics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Type: Transcatheter Momentum Drives Portfolio Shifts

Transcatheter heart valves accounted for 45.10% of 2025 revenue, underlining their rapid shift from salvage therapy to first-line option across risk profiles. This segment anchors the prosthetic heart valve market through streamlined procedures that shorten hospital stays and widen eligibility. Polymeric valves represent the fastest-growing niche, delivering an 17.74% CAGR through 2031 because materials resist calcification without anticoagulation, appealing to active patients. Tissue valves retain relevance for conventional surgery, while mechanical devices remain the choice for select younger users who accept lifelong anticoagulation in exchange for durability. Regulatory wins, such as Edwards’ SAPIEN 3 for asymptomatic patients and the EVOQUE tricuspid system, keep transcatheter solutions at the forefront. Polymeric innovators Foldax and 4C Medical are reshaping durability expectations, catalyzing competitive differentiation. Clinical acceptance broadens as device platforms address multiple positions, reinforcing the prosthetic heart valve market’s direction toward catheter-based therapy.

Sutureless platforms blur the line between open surgery and catheter techniques by offering shorter cross-clamp times and facilitating future valve-in-valve interventions. This hybrid evolution attracts surgeons who seek faster procedures without relinquishing operative control. Rapid-deployment valves, such as LivaNova’s Perceval Plus, appeal to institutions balancing throughput and outcomes, prompting incremental share gains within the broader prosthetic heart valve market.

By Position: Aortic Dominance Meets Tricuspid Upswing

Aortic valves represented 56.02% of revenue in 2025, buttressed by a mature evidence base and streamlined reimbursement pathways. Patient demand remains strong because aortic stenosis prevalence rises with age, yet growth moderates as penetration in high-income markets stabilizes. Tricuspid interventions recorded a 14.92% forecast CAGR, the fastest among all positions, buoyed by Edwards’ EVOQUE approval and trial success for Abbott’s TriClip. Mitral programs gain momentum as the SAPIEN M3 CE mark unlocks the transfemoral approach. Specialized firms address pulmonary needs with devices such as the Venus P-valve for enlarged outflow tracts.

The prosthetic heart valve market share for aortic products is expected to narrow modestly as tricuspid and mitral growth outpaces traditional volumes. CMS coverage under Evidence Development for transcatheter tricuspid procedures will accelerate US uptake. Simultaneously, Asia-Pacific companies craft position-specific devices suited to local anatomies, such as Venus Medtech’s mitral platform, diversifying competitive dynamics. As position specialization deepens, manufacturers secure regulatory timelines and clinical trials tailored to anatomical nuance, anchoring durable growth within the prosthetic heart valve market.

By Delivery Method: Open Surgery Retains Relevance Within Hybrid Pathways

Surgical deliveries still generated 54.05% of 2025 sales, demonstrating that open procedures remain important for complex anatomies and younger patients requiring extended durability. The prosthetic heart valve market size for surgical implants is projected to expand at 7.08% CAGR thanks to sutureless and rapid-deployment innovations that compress operative times. Hospitals appreciate predictable outcomes and the ability to accommodate future valve-in-valve options through designs like Edwards’ INSPIRIS RESILIA with VFit. Transcatheter deliveries, meanwhile, grow faster as improved catheter designs allow alternate accesses, including transaxillary and transcaval routes for complex vascular profiles.

Rapid-deployment solutions clock a 13.31% CAGR by blending minimally invasive surgical access with reduced cross-clamp duration, satisfying surgeon preference while lowering resource utilization. Robotic-assisted mitral valve replacement trials underscore the convergence of surgical precision with catheter efficiency, further segmenting the delivery landscape. As institutions evaluate cost, throughput, and workforce constraints, treatment algorithms will integrate multiple delivery methods instead of a binary surgical-versus-catheter choice, helping stabilise market expansion within the prosthetic heart valve market.

By End-user: Outpatient Transition Reshapes Care Pathways

Tertiary centers held 45.20% of 2025 procedures because high-risk cases demand extensive imaging, perfusion support, and multidisciplinary teams. Yet ASCs are registering a 13.98% CAGR as same-day TAVR protocols cut inpatient stays, aligning with payer cost-containment goals. Cardiac specialty hospitals sit between these endpoints, providing focused expertise at lower overheads than large academic sites. Workforce training remains pivotal; individualized cath-lab education programs have improved retention and procedural quality, mitigating looming cardiologist shortages.

Infrastructure gaps outside tier-1 urban areas limit cath-lab capacity, constraining adoption in emerging economies. Health-system investments, such as Highmark’s USD 1 billion Allegheny expansion and Emory’s USD 87.7 million facility upgrade, illustrate concerted responses to capacity bottlenecks. As procedures migrate toward outpatient settings, payers demand outcome-linked reimbursement, reinforcing the trend toward value-based models within the prosthetic heart valve market.

Geography Analysis

North America accounted for 42.10% of 2025 revenue, cementing its leadership through established reimbursement, robust clinical infrastructure, and early adopter mindsets. CMS coverage expansions drive procedure growth, and private insurers generally mirror Medicare’s stance, ensuring broad access. The United States faces a looming 8,650-cardiologist shortfall by 2037, a constraint that may dampen procedure growth if training pipelines do not accelerate. Canada benefits from integrated provincial health systems and rising TAVR volumes. Mexico’s modernizing private sector and cross-border medical tourism represent niche growth contributors.

Asia-Pacific delivers the fastest 13.90% CAGR through 2031, propelled by infrastructure investment, regulatory harmonization, and domestic innovation. China’s National Medical Products Administration (NMPA) approval of MicroPort’s VitaFlow Liberty Flex expands home-grown transcatheter options. Japan and South Korea leverage ageing populations and universal coverage to accelerate uptake. India exhibits long-term potential as cardiac programmes expand beyond metro hubs. Anatomical differences, notably smaller aortic annuli in East Asian patients, necessitate region-specific valve sizing and reinforce local R&D. Australia functions as a clinical trial nucleus, supporting regional skill transfer and evidence generation.

Europe sustains a balanced growth outlook, underpinned by coordinated regulation and strong clinician networks. Germany, United Kingdom, France, Italy, and Spain anchor procedural volumes, supported by long-standing TAVR programmes and standardized curricula. Edwards’ SAPIEN M3 CE mark emphasises Europe’s role as a launch pad for transfemoral mitral solutions. Eastern Europe lags but offers catch-up potential as economies converge. Meanwhile, the Middle East, Africa, and South America grow from a small base; selective investments in centres of excellence create regional hubs that train physicians and demonstrate outcomes, progressively widening access to the prosthetic heart valve market.

Competitive Landscape

Moderate concentration defines the prosthetic heart valve market, with established multinationals expanding portfolios while nimble entrants target white-space positions. Edwards Lifesciences leads through comprehensive TAVR and transcatheter mitral and tricuspid therapies, reinforced by vertical moves including the USD 300 million Innovalve buyout. Medtronic maintains competitive breadth, whereas Abbott leverages structural heart breadth exemplified by Tendyne’s 2025 FDA clearance. Boston Scientific’s ACURATE neo2 studies add incremental valve options.

Start-ups thrive under breakthrough designations: 4C Medical’s AltaValve, Foldax’s TRIA, and JenaValve’s Trilogy system each advance distinct niches. Asian players, notably MicroPort and Venus Medtech, gain share in domestic markets through NMPA approvals and anatomical customisation. Private-equity consolidation of interventional practices—approaching 50% penetration—shifts purchasing power toward integrated networks able to negotiate bundled deals across portfolios. Competitive focus increasingly revolves around polymer durability, AI-enabled planning, and flexible delivery frames such as the collapsible systems in Edwards’ latest patent. As established and emerging companies compete across risk categories and valve positions, differentiation hinges on clinical evidence, regulatory speed, and ecosystem partnerships, sustaining dynamic rivalry within the prosthetic heart valve market.

Prosthetic Heart Valve Industry Leaders

Edwards Lifesciences

Medtronic plc

Boston Scientific Corp.

Abbott Laboratories

LivaNova PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Edwards Lifesciences secured FDA approval for SAPIEN 3, SAPIEN 3 Ultra, and SAPIEN 3 Ultra RESILIA transcatheter heart valves in asymptomatic severe aortic stenosis.

- May 2025: Abbott received FDA clearance for the Tendyne transcatheter mitral valve replacement, designed for severe mitral annular calcification.

- April 2025: Edwards SAPIEN M3 gained CE mark, becoming the first transfemoral mitral replacement system for commercial use in Europe.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the prosthetic heart valve market as the total revenue generated from newly implanted mechanical, tissue-based (bioprosthetic), transcatheter, and next-generation polymeric heart valves that permanently replace diseased native valves in hospitals and ambulatory surgical centers worldwide.

Scope exclusion: Repair devices such as annuloplasty rings, valved conduits, and temporary circulatory support systems are not counted in this valuation.

Segmentation Overview

- By Valve Type

- Mechanical Heart Valve

- Tissue/Bioprosthetic Heart Valve

- Transcatheter Heart Valve (TAVR/TMVR/TTVR/TPVR)

- Polymeric/Next-Gen Heart Valve

- By Position

- Aortic

- Mitral

- Tricuspid

- Pulmonary

- By Delivery Method

- Surgical (SAVR/SMVR)

- Transcatheter

- Sutureless/Rapid-deployment

- By End-user

- Tertiary-care Hospitals

- Cardiac Specialty Centers

- Ambulatory Surgical Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed interventional cardiologists, cardiothoracic surgeons, catheter-lab managers, and regional distributors across North America, Europe, Asia-Pacific, and Latin America. Short online surveys with payers and biomedical engineers helped us verify average selling prices, durability-linked replacement cycles, and early adoption rates for polymeric valves.

Desk Research

We mapped prevalence, incidence, and replacement volumes using open datasets such as the WHO Global Health Observatory, Eurostat hospital-discharge files, the American Heart Association annual statistics, United Nations population forecasts, and the US FDA Premarket Approval database that tracks newly cleared valves. Company 10-Ks, CMS Medicare claims, peer-reviewed journals, and clinical-trial registries enriched regional implant ratios and pricing clues. Paid resources, including D&B Hoovers for company revenue splits and Dow Jones Factiva for shipment commentary, supplied further granularity. The sources listed illustrate our approach; numerous additional public and proprietary references supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down model converts annual valve-replacement procedure counts into monetary value through region-specific penetration rates and weighted ASPs. Results are corroborated with selective bottom-up checks such as disclosed valve revenues and sampled supplier invoices. Key variables include severe aortic stenosis prevalence in 65-plus cohorts, transcatheter share of total replacements, biological versus mechanical mix, regulatory approval cadence, and inflation-adjusted device pricing. Multivariate regression, anchored to population aging, healthcare spend per capita, and technology diffusion indices, projects demand through 2030, while scenario analysis stress tests high-impact reimbursement or safety events. Proxy ratios from comparable health systems fill any remaining geographic data gaps.

Data Validation & Update Cycle

Our team runs variance flags on every output, revisits interviewees when anomalies appear, and secures a second analyst audit before sign-off. We refresh models once a year. Interim updates are issued whenever major approvals, product recalls, or reimbursement shifts materially change the baseline.

Why Mordor's Prosthetic Heart Valve Baseline Commands Reliability

Published estimates often diverge because firms adopt different scope boundaries, input sources, and currency treatments. Some bundle repair rings or structural-heart ancillaries, while others freeze 2023 price points or omit emerging geographies.

According to Mordor Intelligence, the principal gap drivers are scope breadth, procedure-count derivation, ASP progression logic, and refresh cadence. Our numbers reflect only replacement valves, apply hospital billing data current to 2025, and convert revenues using IMF average exchange rates, delivering a clear and up-to-date picture.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.35 Bn (2025) | Mordor Intelligence | - |

| USD 10.60 Bn (2025) | Global Consultancy A | Omits polymeric and sutureless valves, relies on 2023 ASPs, excludes Latin America and MENA |

| USD 14.76 Bn (2025) | Industry Association B | Includes repair rings and conduits, uses implant counts rather than valve units, unclear FX conversion year |

These comparisons highlight that our disciplined scope selection, fresh 2025 pricing, and transparent variable mapping give decision-makers a balanced, reproducible baseline they can trust for planning and investment.

Key Questions Answered in the Report

What is the current size of the prosthetic heart valve market?

The prosthetic heart valve market size reached USD 14.9 billion in 2026 and is projected to hit USD 25.76 billion by 2031.

Which valve type leads global sales?

Transcatheter heart valves led with 45.10% of 2025 revenue, reflecting their shift to first-line therapy across risk categories.

Why are polymeric valves attracting attention?

Polymeric valves deliver an 17.74% forecast CAGR because they combine mechanical-like durability with bioprosthetic-level hemocompatibility, potentially eliminating calcification and lifelong anticoagulation.

Which region will grow fastest through 2031?

Asia-Pacific is forecast to expand at a 13.90% CAGR, powered by infrastructure build-outs, regulatory reform, and domestic device approvals such as MicroPort’s VitaFlow Liberty Flex in China.

How are costs influencing market adoption?

High device and procedure prices—commercial US median of USD 71,312 versus Medicare’s USD 37,865—limit penetration in lower-income settings, prompting value-based contracting and cost-effectiveness scrutiny.

Page last updated on: