Transcatheter Pulmonary Valve Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

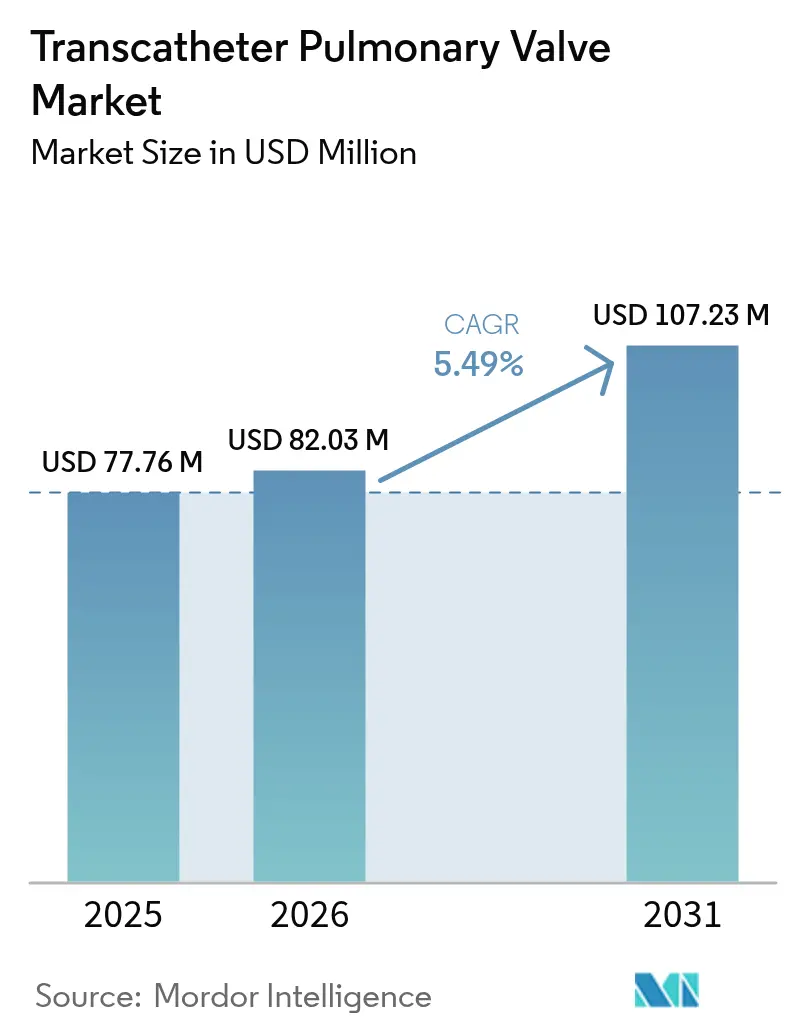

| Market Size (2026) | USD 82.03 Million |

| Market Size (2031) | USD 107.23 Million |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transcatheter Pulmonary Valve Market Analysis by Mordor Intelligence

The global transcatheter pulmonary valve market size was valued at USD 77.76 million in 2025 and estimated to grow from USD 82.03 million in 2026 to reach USD 107.23 million by 2031, at a CAGR of 5.49% during the forecast period (2026-2031). An expanding cohort of adult survivors of congenital heart disease (CHD), rapid device approvals, and supportive reimbursement updates are sustaining demand. Self-expanding platforms are doubling the addressable patient pool by treating large native right ventricular outflow tracts (RVOT), while balloon-expandable valves remain indispensable for conduit-based anatomies. Payer policies increasingly reward outpatient cath-lab procedures, accelerating the shift from tertiary surgical centers to ambulatory facilities. Regulatory vigilance around durability and endocarditis continues to temper near-term adoption but also drives sustained R&D investment in advanced tissue processing and anti-calcification technologies.

Key Report Takeaways

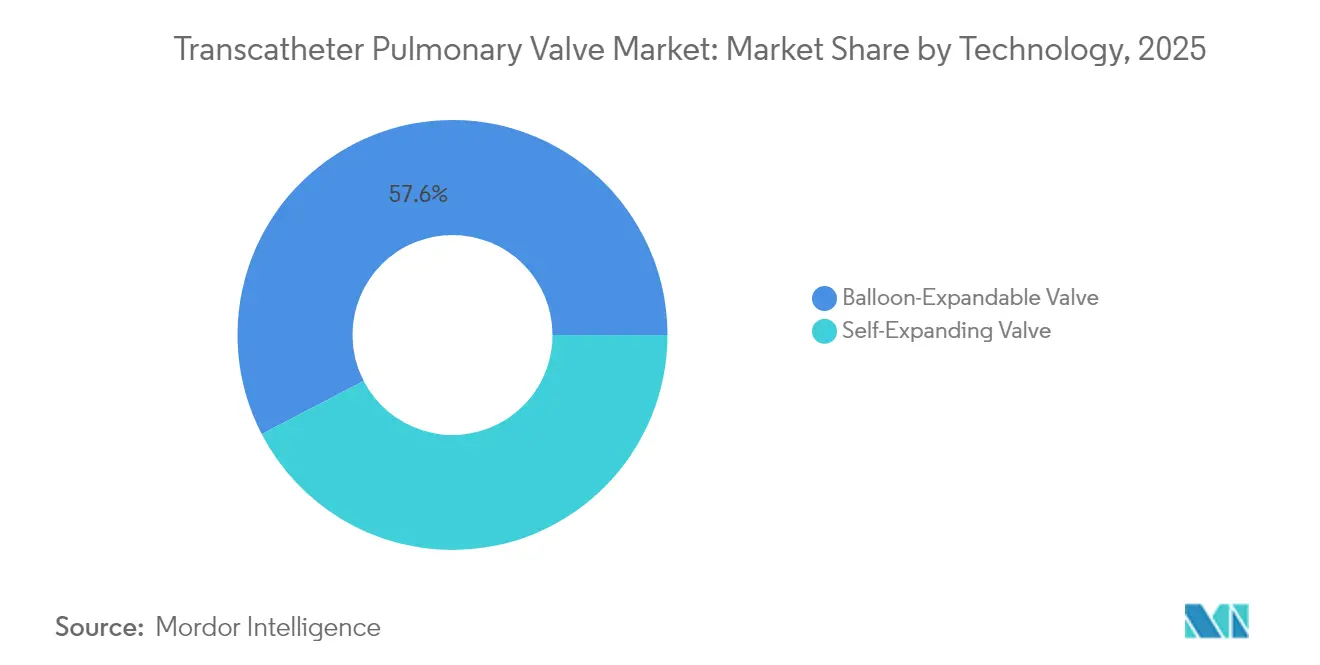

- By technology, balloon-expandable valves led with 57.62% of the transcatheter pulmonary valve market share in 2025, whereas self-expanding devices are forecast to register the fastest 11.92% CAGR through 2031.

- By application, pulmonary regurgitation accounted for 45.02% share of the transcatheter pulmonary valve market size in 2025; pulmonary stenosis procedures are set to advance at a 10.67% CAGR to 2031.

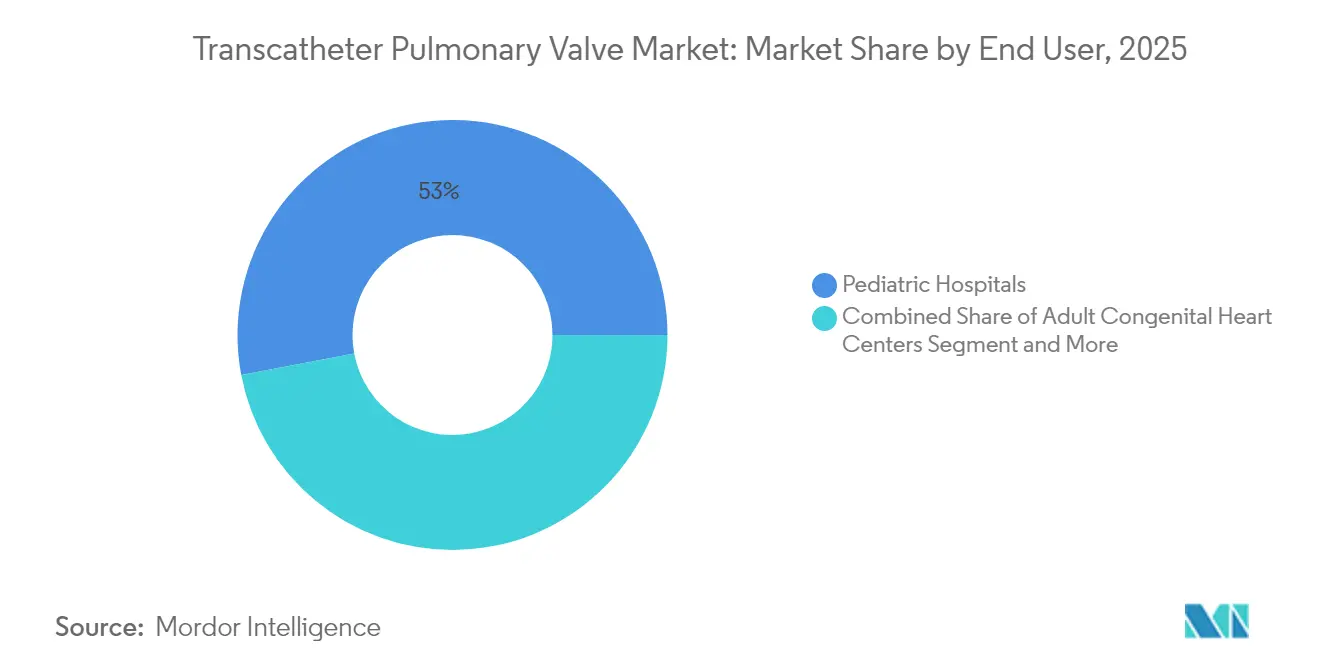

- By end user, pediatric hospitals held 52.98% of 2025 revenue, yet ambulatory surgical centers are expanding at 12.15% CAGR, the quickest across settings.

- By RVOT anatomy, conduit-based interventions represented 58.95% of global volume in 2025, while native/enlarged RVOT treatments are growing at an 11.03% CAGR.

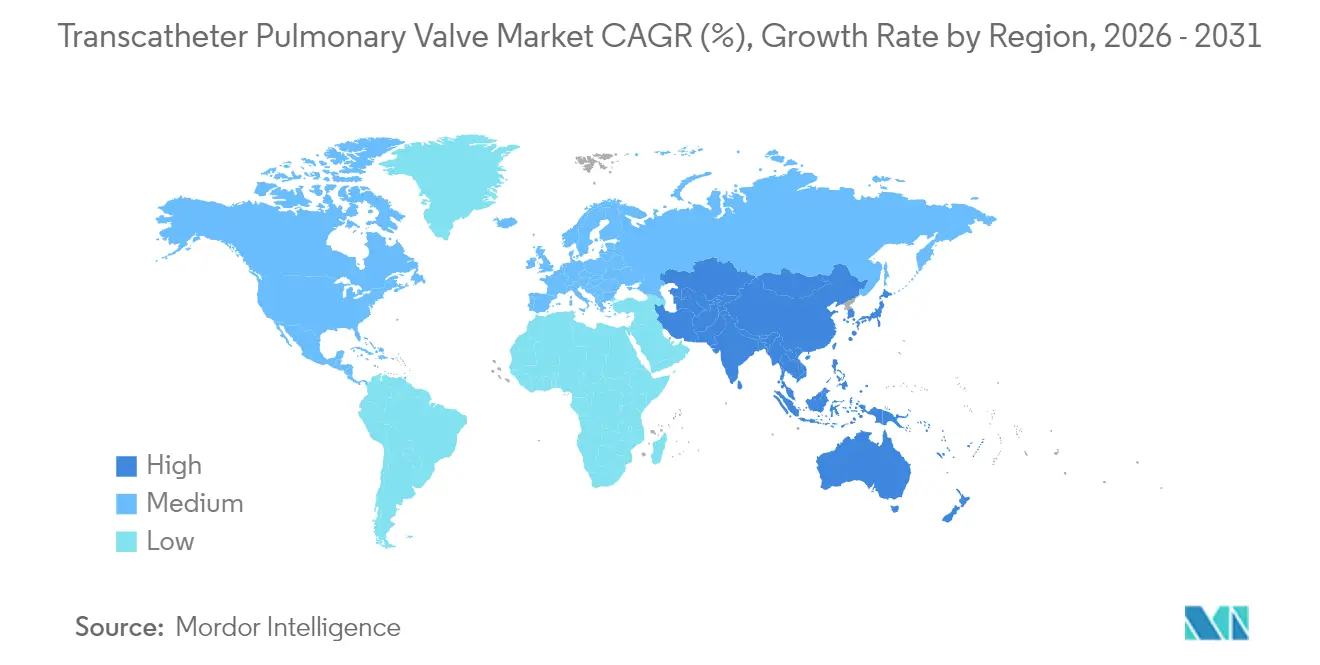

- By geography, North America contributed 38.30% of revenue in 2025; Asia-Pacific is expected to grow the quickest at 10.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transcatheter Pulmonary Valve Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adult-Survivor CHD Population | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Rapid Approvals Of Self-Expanding TPV Platforms | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Patient & Clinician Shift To Minimally-Invasive Therapies | +1.0% | Global | Medium term (2-4 years) |

| Investment Surge From Leading Med-Tech Strategics | +0.8% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Expansion Of Outpatient Cath-Lab Reimbursement Codes | +0.7% | North America, with EU adoption following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adult-Survivor CHD Population

Adults living with congenital heart defects now exceed 1 million in the United States, 20% of whom require complex cardiac re-interventions. Hospitalizations are 91% higher and average USD 81,332 per stay versus USD 49,000 for non-congenital heart failure, incentivizing payers to endorse less invasive options. Strong long-term tissue durability—99.3% freedom from structural deterioration over eight years—supports device longevity expectations[1]Edwards Lifesciences, “Eight-Year Data Confirm Long-Term Durability of Edwards' RESILIA Tissue,” ir.edwards.com. The demographic trajectory ensures persistent case flow across developed markets.

Rapid Approvals of Self-Expanding TPV Platforms

Multicenter registry data covering 243 U.S. patients recorded 98% acceptable hemodynamics and 99% freedom from major composite events at one-year follow-up[2]Doff B. McElhinney, “Early Outcomes From a Multicenter Transcatheter Self-Expanding Pulmonary Valve Replacement Registry,” jacc.org. UK regulators granted exceptional approval for the Venus P-valve despite a pending CE mark, signaling readiness to fast-track solutions addressing unmet needs. Ability to land securely in large native RVOT anatomies effectively doubles the clinical universe.

Patient and Clinician Shift to Minimally Invasive Therapies

The American Heart Association’s 2024 statement positions transcatheter replacement as preferred care for conduit longevity. Thirty-day functional status improved in 83.9% of recipients, and procedural success reached 95% with only 2.4% major adverse events. Spanish cost-utility analyses placed incremental cost-effectiveness at EUR 6,952 per QALY, well below national willingness-to-pay thresholds.

Investment Surge from Leading Med-Tech Strategics

Edwards Lifesciences targets USD 4.1–4.4 billion in 2025 transcatheter aortic revenue and continues to fund pulmonary innovations, including SAPIEN 3 Ultra RESILIA. Venus Medtech secured FDA Breakthrough Device status for Cardiovalve, illustrating investor appetite for structural heart expansions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Durability & Strict Post-Market Surveillance | -1.5% | Global | Long term (≥ 4 years) |

| Surgical Alternatives (Ross, Homografts) Remain Viable | -0.8% | Europe & North America | Medium term (2-4 years) |

| Endocarditis Uptick Triggering Caution In Key Centers | -1.2% | Global, with higher impact in pediatric centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Durability and Strict Post-Market Surveillance

FDA registries logged 631 adverse events for Melody implants, including stent fragment embolization. Ten-year freedom from dysfunction sits at 53% in pediatric cohorts, driving regulatory calls for harmonized durability definitions. Although RESILIA tissue shows encouraging eight-year durability, pulmonary positioning evidence remains early stage.

Endocarditis Uptick Triggering Caution in Key Centers

Multicenter data reveal 9.5% cumulative endocarditis at five years and 16.9% at eight years, equivalent to 2.2 events per 100 patient-years. ESC guidelines now recommend valve-specific antimicrobial regimens. Institutions adopting stringent prophylaxis report declining incidence, but heightened vigilance persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Self-Expanding Platforms Reshape Treatment Paradigms

Global revenue remains anchored by balloon-expandable devices, which commanded 57.62% of the transcatheter pulmonary valve market share in 2025. Precise conduit sizing, immediate anchoring, and robust long-term data sustain clinician confidence. The Edwards SAPIEN 3 system achieved 98.1% device success and 100% freedom from surgical reintervention at one year. At the same time, self-expanding solutions are advancing at 11.92% CAGR through 2031, transforming therapeutic possibilities for enlarged native RVOT anatomies. One-year registry follow-up showed 96% freedom from composite events with acceptable hemodynamics in 98% of cases. The Venus P-valve and Harmony systems now anchor treatment algorithms in Asia and North America respectively, with CE certification further broadening access.

By Application: Stenosis Cases Fuel Growth Despite Regurgitation Dominance

Pulmonary regurgitation generated 45.02% of 2025 procedure volume, reflecting historical focus on volume-overload correction. Nonetheless, pulmonary stenosis indications are forecast to post a 10.67% CAGR, the strongest trajectory within the transcatheter pulmonary valve market. Earlier intervention strategies that aim to pre-empt right-ventricular compromise underpin this acceleration, especially for repaired Tetralogy of Fallot patients. Comparative trials such as COMPASS will clarify optimal timing and modality selection, potentially increasing stenosis-related volumes.

By End User: Ambulatory Centers Lead Transformation

Pediatric hospitals retained 52.98% revenue in 2025 but ambulatory surgical centers are registering a 12.15% CAGR, reshaping care delivery. CMS reimbursement revisions and strong safety data—95% procedural success with 2.4% major adverse events—support same-day discharge protocols. Adult congenital heart centers are expanding multidisciplinary programs to handle the growing adult CHD population, estimated to reach 510,000 U.S. patients by 2050.

By RVOT Anatomy: Native-Tract Technologies Expand Eligibility

Conduit-based interventions account for 58.95% of global cases, yet native/enlarged RVOT treatments will outpace at an 11.03% CAGR. Harmony earned FDA approval for native RVOTs, and early use demonstrates 98.2% procedural success with significant right-ventricular volume reductions. Screening perimeter plot analyses are refining candidate selection, even as false negatives highlight the need for iterative imaging protocols.

Geography Analysis

North America generated 38.30% of global revenue in 2025, buoyed by advanced centers, widespread payer support, and active clinical-trial pipelines. CMS’s 2.9% outpatient payment hike and new device categories accelerate catheter-lab uptake. Canada and Mexico are scaling specialist capabilities, supported by cross-border training and regional clinical studies.

Europe sustains mid-single-digit growth, underpinned by mature infrastructure and adaptable regulators willing to expedite devices with demonstrable need. Exceptional UK approval of Venus P-valve underscores demand-driven flexibility. Health-economic studies from Spain showed favorable EUR 6,952 per QALY, reinforcing payer confidence.

Asia-Pacific represents the fastest regional expansion at 10.44% CAGR. Domestic innovators such as Venus Medtech tailor self-expanding valves for prevalent anatomical features in Chinese and Indian populations. Japan’s registry exceeding 8,000 transcatheter aortic cases provides a procedural blueprint for pulmonary adoption. Government initiatives to expand cardiac catheterization labs in South Korea and Australia further catalyze uptake.

South America and the Middle East & Africa trail but show rising interest as referral pathways mature. Partnerships with global device makers and training exchanges with European centers are improving procedural readiness. Incremental gains in reimbursement coverage, especially for pediatric CHD, are expected to translate into a steady but smaller share of the transcatheter pulmonary valve market by 2030.

Competitive Landscape

The transcatheter pulmonary valve market remains moderately concentrated. Edwards Lifesciences’ balloon-expandable SAPIEN platform and Medtronic’s self-expanding Harmony system collectively accounted for over 70% of 2024 revenue. Edwards recorded USD 1 billion structural heart sales in Q3 2024, an 8% year-on-year rise, driven partly by pulmonic implants. Medtronic secured CE Mark for Harmony in January 2025, reinforcing its first-mover advantage in native RVOT therapy [news.medtronic.com].

Boston Scientific’s 2025 withdrawal of the Acurate TAVR line after unsuccessful FDA review illustrates high regulatory hurdles and has marginally eased competitive pressure. Meanwhile, Venus Medtech pursues Western approvals for its P-valve and Cardiovalve systems, aiming to disrupt incumbents in enlarged RVOT and tricuspid niches.

Strategic priorities revolve around durability, expanded size matrices, and simplified delivery systems. Intellectual-property extensions, such as the FDA-granted review period for SAPIEN 3 Ultra, highlight the importance of patent longevity. AI-guided imaging and valve-in-valve software modules are emerging differentiators as providers seek to minimize screening failures and enhance procedural planning.

Transcatheter Pulmonary Valve Industry Leaders

Boston Scientific Corporation

Braile Biomedica

Medtronic PLC

Edwards Lifesciences Corporation

Artivion, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Medtronic received CE Mark for the Harmony transcatheter pulmonary valve system, enabling minimally invasive care for patients with native or surgically repaired RVOT.

- September 2024: Edwards Lifesciences launched the SAPIEN 3 pulmonic system with Alterra adaptive prestent in Europe, broadening access to conduit and enlarged RVOT anatomies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the transcatheter pulmonary valve (TPV) market as revenue generated from new, catheter-delivered balloon-expanded or self-expanding valves that permanently replace a dysfunctional native or conduit-based pulmonary valve in pediatric and adult congenital-heart-disease patients worldwide.

Scope exclusion: Surgical pulmonary valve prostheses, repair kits, and delivery catheters sold separately are outside this assessment.

Segmentation Overview

- By Technology

- Balloon-Expandable Valve

- Self-Expanding Valve

- By Application

- Pulmonary Stenosis

- Pulmonary Regurgitation

- Tetralogy-of-Fallot Post-Repair

- Others

- By End-User

- Pediatric Hospitals

- Adult Congenital Heart Centers

- Ambulatory Surgical Centers

- By RVOT Anatomy

- Conduit-Based RVOT

- Native / Enlarged RVOT

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Rest of the World

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with interventional cardiologists, cath-lab managers, and payor specialists across North America, Europe, and Asia confirmed selling-price corridors, device-choice drivers, and adoption hurdles. These insights closed secondary gaps and allowed us to validate key assumptions before final modeling.

Desk Research

We began with public datasets such as FDA Premarket Approval files, EUDAMED summaries, CMS outpatient procedure counts, Eurostat surgical discharges, and congenital-heart registries to size annual TPV implant volumes by country. Investor presentations, 10-K filings, recall notices, and reimbursement code histories then anchored company shipment trajectories.

Further perspective came from journals including Circulation and JACC, trade bodies like the Society for Cardiovascular Angiography and Interventions, and customs data accessed through Volza. When reporting depth was thin, Mordor analysts turned to D&B Hoovers, Dow Jones Factiva, and Questel patent analytics to cross-verify pipeline maturity. The sources cited illustrate our approach and are not exhaustive.

Market-Sizing & Forecasting

A blended top-down and bottom-up framework underpins our model. Top-down, registry and claims-derived procedure counts were multiplied by region-specific average selling prices. Bottom-up checks used sampled hospital purchase data and supplier roll-ups to stress-test totals. Core drivers include live-birth CHD prevalence, adult-survivor growth, cath-lab density, reimbursement expansion, and ASP trends. Forecasts to 2030 employ exponential smoothing informed by multivariate regression on those variables. Where hospital reporting was missing, procedure-to-device utilization ratios validated during field calls filled the gaps.

Data Validation & Update Cycle

Outputs pass variance checks against historical approval volumes and registry trends, with anomalies escalated for senior review. Reports refresh annually, and material regulatory or clinical events trigger interim revisions. Just before release, an analyst re-runs the model so clients receive the latest view.

Why Our Transcatheter Pulmonary Valve Baseline Commands Reliability

Published TPV estimates often diverge because firms mix valve categories, apply differing ASP paths, or refresh on uneven timetables. According to Mordor Intelligence, we anchor every baseline to clearly defined device boundaries and current-year procedure evidence, which limits over- or under-statement.

Common gap drivers include scope creep into broader transcatheter heart valves, the inclusion of accessories, aggressive global ASP uplift factors, and infrequent data updates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 77.76 million (2025) | Mordor Intelligence | - |

| USD 73.1 million (2024) | Regional Consultancy A | Excludes Rest-of-World geographies and relies on historical ASPs |

| USD 1.20 billion (2024) | Global Consultancy B | Bundles aortic and mitral devices plus service revenues |

| USD 245 million (2024) | Trade Journal C | Counts delivery systems and surgical conduits alongside TPVs |

These contrasts show that when consistent scope, fresh procedure data, and transparent variables are applied, Mordor delivers a balanced, traceable baseline that decision-makers can reproduce with limited resources.

Key Questions Answered in the Report

What is the current size of the transcatheter pulmonary valve market?

The transcatheter pulmonary valve market is valued at USD 82.03 million in 2026 and is forecast to reach USD 107.23 million by 2031.

Which technology segment is growing fastest?

Self-expanding valves are expanding at a 11.92% CAGR through 2031 as they enable treatment of large native RVOT anatomies.

Why are ambulatory surgical centers gaining share?

CMS payment upgrades and strong safety data allow same-day discharge, prompting a 12.15% CAGR for procedures in ambulatory settings.

How significant is endocarditis risk after implantation?

Registry data show a cumulative 9.5% incidence at five years, driving enhanced prophylaxis protocols in high-volume centers.

Which regions will drive future growth?

Asia-Pacific will post the fastest 10.44% CAGR thanks to domestic innovation, expanding cath-lab infrastructure, and rising CHD awareness.

Page last updated on: