Cardiac Catheters And Guidewires Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

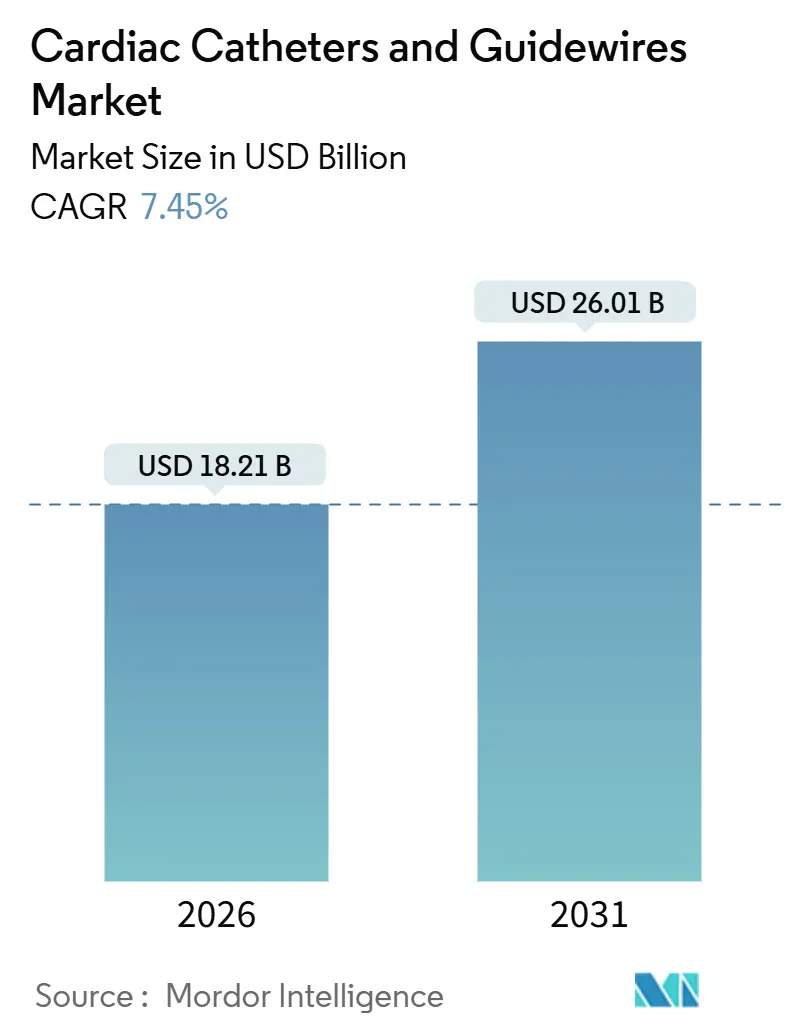

| Market Size (2026) | USD 18.21 Billion |

| Market Size (2031) | USD 26.01 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Catheters And Guidewires Market Analysis by Mordor Intelligence

The Cardiac Catheters And Guidewires Market size is estimated at USD 18.21 billion in 2026, and is expected to reach USD 26.01 billion by 2031, at a CAGR of 7.45% during the forecast period (2026-2031).

Growth rests on three structural shifts: first, minimally invasive techniques are replacing open surgery; second, same-day discharge protocols cut inpatient costs; and third, pulsed-field ablation systems approved in 2024 shorten electrophysiology procedure times by up to 40%.[1]World Health Organization, “Cardiovascular Diseases (CVDs),” WHO.INT Radial access gained a Class I recommendation under the 2025 ACC/AHA acute coronary syndrome guideline, accelerating demand for low-profile guidewires.[2]merican College of Cardiology, “Ten Points to Remember From the 2025 AHA/ACC Acute Coronary Syndrome Guideline,” ACC.ORGNew drug-coated balloon approvals are expanding therapeutic use cases, particularly in below-the-knee disease. FDA clearance of the Evolut FX+ valve system in 2024 widened transcatheter aortic valve replacement to lower-risk patients. Meanwhile, Asia-Pacific hospital build-outs and supply-constrained nitinol tubing continue to shape procurement strategies.

Key Report Takeaways

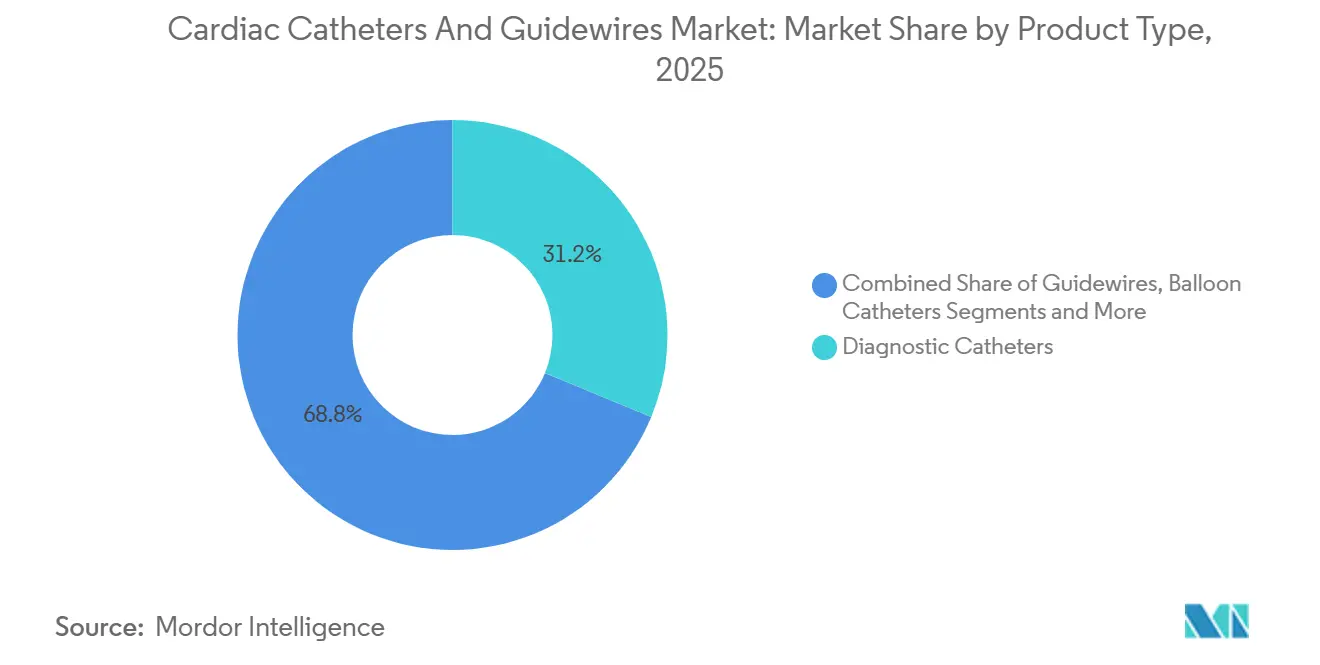

- By product type, diagnostic catheters led with 31.22% share in 2025 while balloon catheters are forecast to rise at an 11.44% CAGR through 2031.

- By application, coronary artery disease held 59.62% of revenue in 2025 and structural heart procedures are projected to grow at a 10.53% CAGR to 2031.

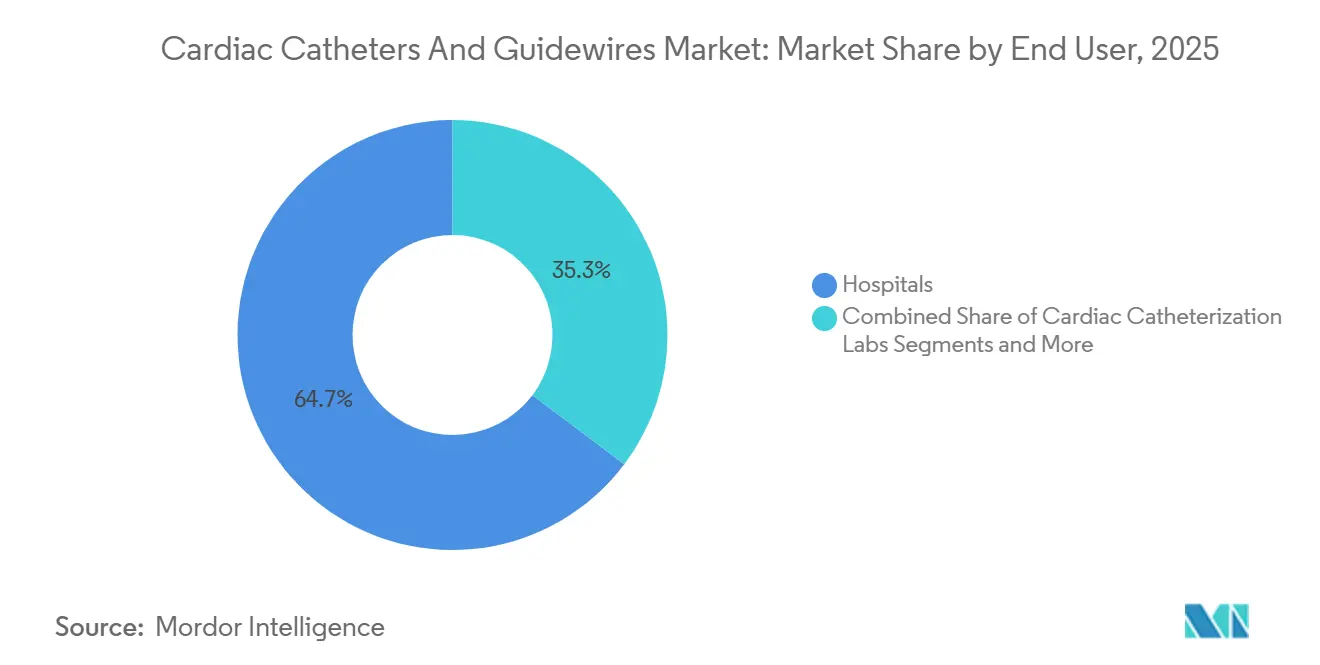

- By end user, hospitals controlled 64.73% in 2025, yet ambulatory surgical centers are advancing at a 9.24% CAGR.

- By material, nitinol captured 53.63% share in 2025 and hybrid alloys are expanding at an 11.56% CAGR.

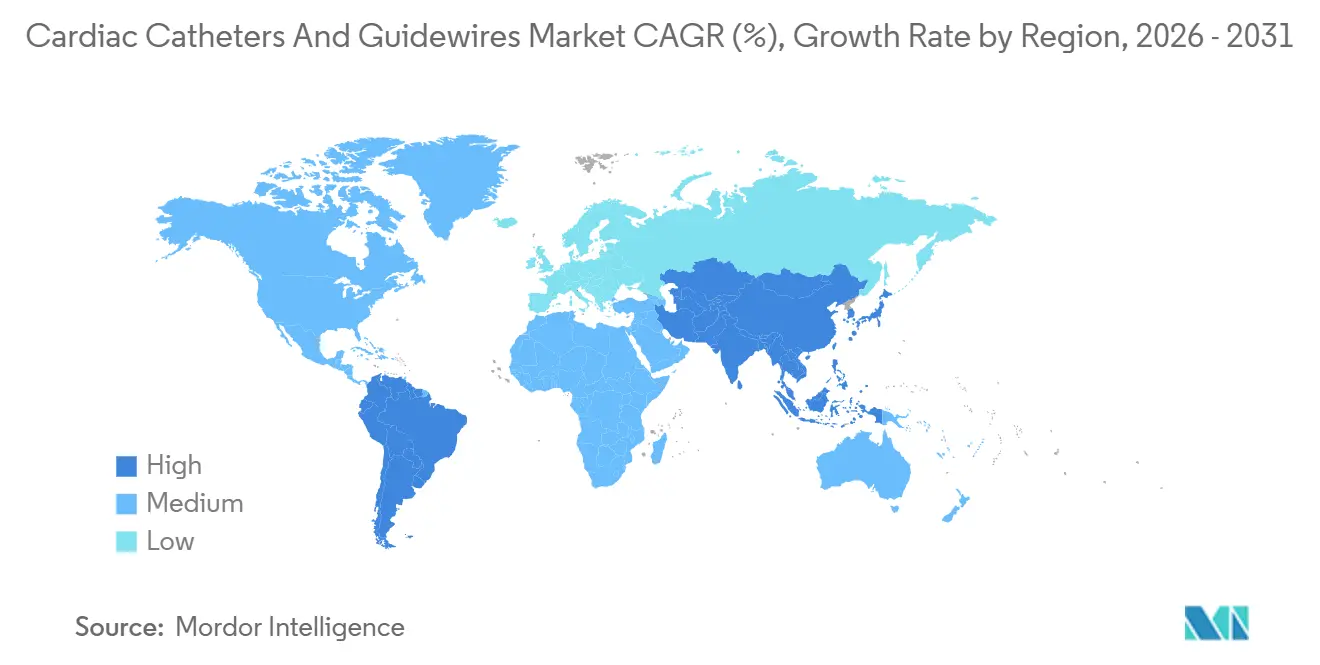

- Geographically, North America accounted for 41.42% revenue in 2025 while Asia-Pacific is growing at a 9.64% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cardiac Catheters And Guidewires Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular diseases | +1.2% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Rapid adoption of minimally invasive PCI & EP | +1.8% | North America, Western Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Advances in hydrophilic-coated guidewires | +0.9% | North America, Japan | Medium term (2–4 years) |

| Surging cath-lab build-out in emerging economies | +1.5% | China, India, Southeast Asia, Middle East & Africa | Long term (≥ 4 years) |

| Radial same-day discharge protocols | +1.0% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| AI-guided imaging adoption | +0.7% | North America, Western Europe, select Asia-Pacific centers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular Diseases

Cardiovascular disease caused 20.5 million deaths in 2021 and remains the chief mortality driver worldwide. Aging populations and metabolic risk factors are expanding the pool of patients eligible for catheter-based interventions. Updated guidelines recommend percutaneous coronary intervention once medical therapy fails, enlarging the treatable population. This clinical shift boosts baseline procedure volumes across both high-income and developing regions. Demographic inertia in Japan, South Korea, and Southern Europe will sustain demand through 2031, while urbanization in South Asia and Africa adds new cohorts. As prevention efforts mature, earlier intervention ensures sustained consumable use.

Rapid Adoption of Minimally Invasive PCI & EP Procedures

Percutaneous coronary intervention and pulsed-field ablation shorten recovery, cut infections, and lower costs. The ACC/AHA guideline raised radial access to Class I, citing MATRIX trial outcomes that reduced bleeding and mortality. FDA approvals of FARAPULSE, VARIPULSE, and PulseSelect in 2024 compress atrial fibrillation ablation times to 90 minutes.[3] U.S. Food and Drug Administration, “FDA Approves First Pulsed Field Ablation System to Treat Atrial Fibrillation,” FDA.GOV Cath-lab throughput rises, lifting wire and catheter consumption per facility. Hospital capital cycles now fund pulsed-field generators, spurring replacement of legacy radiofrequency systems. Medium-term momentum hinges on reimbursement, yet early adopters already report daily case-count gains.

Advances in Hydrophilic-Coated Guidewires & Microcatheters

Polyvinylpyrrolidone and hydrogel coatings slash friction and ease lesion crossing. Terumo’s Glidewire Advantage and Asahi Intecc’s SION series showcase low-force navigation. Lower trauma aligns with imaging-guided workflows that expose micro-dissections. Composite polymer-nitinol hybrids introduced in 2024 keep coatings intact through multiple device exchanges. Adoption is accelerating in complex PCI, where single wires must withstand multiple balloon and stent passes. Despite higher per-wire costs, total complication expenses fall.

Surging Cath-Lab Build-Out in Emerging Economies

China now hosts more than 5,000 catheterization laboratories, propelled by its 14th Five-Year Plan. India’s National Health Mission funds district labs, narrowing urban–rural gaps. Indonesia plans 50 new cardiac centers between 2024 and 2026. New facilities favor cost-effective single-use kits, reshaping vendor pricing. Infrastructure investments precede volume ramps by roughly two years, ensuring long-run growth for the cardiac catheters and guidewires market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price of next-gen devices | -0.8% | Emerging markets, public health systems | Medium term (2–4 years) |

| Lengthy global regulatory approval cycles | -0.6% | U.S., EU, Japan | Long term (≥ 4 years) |

| Complication risk and liability premiums | -0.5% | North America, Western Europe | Medium term (2–4 years) |

| Constrained nitinol tubing supply | -0.7% | Global, acute for niche guidewire producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Price of Next-Gen Catheters & Guidewires

Drug-coated balloons and pulsed-field ablation catheters list between USD 1,500 and USD 3,000 per unit, far above standard balloon prices. Abbott’s Esprit BTK drug-coated balloon lists at roughly USD 2,200 in Europe. Reimbursement bodies in Germany and the United Kingdom demand cost-effectiveness evidence, slowing adoption. Hospitals redirect savings from biosimilar stents toward premium devices, but uptake varies by procurement model. Price sensitivity remains acute across Africa and parts of Latin America, reducing near-term penetration of advanced products.

Lengthy Global Regulatory Approval Cycles

FDA premarket approvals average 12–24 months, and EU Medical Device Regulation reviews add six to 12 months. Boston Scientific’s AGENT balloon won FDA clearance in 2024 yet required extra European data, delaying launch. Smaller firms lack resources for parallel submissions, concentrating innovation among large players. Extended timelines inflate R&D costs and compress exclusivity windows, marginally dampening the cardiac catheters and guidewires market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutic Balloons Outpace Diagnostics

Balloon catheters are projected to grow at 11.44% through 2031, the fastest within the cardiac catheters and guidewires market, while diagnostic catheters retained 31.22% share in 2025. The premium shift stems from FDA-cleared drug-coated balloons like AGENT, which command four to five times the price of uncoated units. Interventional catheters and guidewires ride the same trend as complex cases require multiple device exchanges. The others segment, including fractional-flow-reserve wires, is rising under reimbursement mandates in Germany and Japan but remains smaller. ISO 10555 compliance costs are increasing, prompting large vendors to streamline portfolios to defend margin.

Diagnostic advances outside the cath-lab—CT angiography and cardiac MRI—reduce standalone diagnostic catheter demand, yet each therapeutic procedure still starts with a diagnostic pass. As imaging migrates upstream, therapeutic consumables capture rising revenue per case, keeping the cardiac catheters and guidewires market share concentrated in higher-margin products.

By Application: Structural Heart Leads Growth Momentum

Coronary artery disease contributed 59.62% of revenue in 2025, yet structural heart procedures are set to expand at a 10.53% CAGR through 2031. FDA approval of the Evolut FX+ valve for low-risk patients doubles the potential transcatheter aortic valve replacement population. Large-bore delivery catheters and stiff wires push per-procedure device spend to as high as USD 12,000. Peripheral vascular interventions benefit from drug-coated balloons targeting critical limb ischemia, adding incremental volumes. Electrophysiology adoption of pulsed-field ablation boosts consumable turnover as procedure times shrink.

Overall, while coronary interventions dominate absolute units, structural heart and electrophysiology segments add the most incremental value, reinforcing a premiumization arc in the cardiac catheters and guidewires market.

By End User: Ambulatory Centers Gain Share

Hospitals held 64.73% revenue in 2025, but ambulatory surgical centers are increasing at a 9.24% CAGR as payers favor outpatient settings. Medicare’s 2025 outpatient rules reduced payments for overnight PCI stays, pushing stable cases into day-surgery formats. Ambulatory centers prefer bundled kits that minimize inventory variation, whereas hospitals continue to demand customizable portfolios for complex cases.

Cardiac cath labs affiliated with hospitals retain hybrid capabilities, supporting both diagnostic and interventional work. Specialty clinics for electrophysiology and peripheral intervention are emerging but remain subscale. Vendor strategies now segment catalogs: standardized trays for cost-focused ambulatory sites, and modular systems for tertiary centers.

By Material: Composite Alloys Challenge Nitinol

Nitinol captured 53.63% revenue in 2025, yet hybrid alloys are forecast to climb 11.56% through 2031. Composite designs add radiopaque filaments without sacrificing flexibility, improving visibility under fluoroscopy. Stainless steel lingers in cost-sensitive markets and large-bore sheaths, but its share is sliding.

Prolonged nitinol lead times have pushed vendors to test cobalt-chromium substitutes and polymer-jacketed cores. ISO 5832-11 biocompatibility testing adds up to nine months, favoring incumbents that already possess validated supply chains. Material diversification mitigates supply risk and supports long-term resilience in the cardiac catheters and guidewires market.

Geography Analysis

North America generated 41.42% revenue in 2025, driven by 1,800 + cath-labs, routine imaging guidance, and rapid adoption of pulsed-field ablation. Reimbursement pressure, however, caps price growth and encourages same-day discharge, affecting device mix. Europe remains sizable, with Germany, France, and the United Kingdom at the forefront, yet EU Medical Device Regulation delays weigh on new launches, moderating growth.

Asia-Pacific is the fastest-growing region at a 9.64% CAGR through 2031, propelled by China’s 5,000 + labs and India’s district-level expansion programs. Emerging Southeast Asian economies are also scaling capacity, often preferring single-use kits over robotic systems to control costs. Aging populations in Japan and South Korea sustain volumes, though price caps restrain revenue per case.

South America and the Middle East & Africa remain smaller but show pockets of investment: Brazil updates public hospital cath-labs, and Gulf Cooperation Council countries deploy cardiac centers as part of broader diversification strategies. Currency volatility and tariffs introduce margin risk, yet rising disease incidence ensures steady baseline demand across these regions.

Competitive Landscape

Abbott, Boston Scientific, and Medtronic collectively command a sizable portion of the cardiac catheters and guidewires market, but niche players such as Asahi Intecc, Teleflex, and Merit Medical defend specialized positions. Boston Scientific’s 2022 Baylis Medical acquisition broadened its transseptal access offerings, and Abbott’s VARIPULSE launch in 2024 leveraged its EnSite mapping system for ecosystem lock-in. Emerging competitors include Robocath in robotic PCI and Abiomed in mechanical support, both extending interventional boundaries.

Technology integration is the central differentiator. Philips’ LumiGuide couples AI imaging with compatible wires to reduce procedure time and radiation. Patent activity now centers on composite materials and sensor-embedded catheters. Regulatory strategy also matters: 12 cardiac catheter technologies gained FDA Breakthrough Device Status in 2024, granting expedited review.

Procurement models are tilting toward value-based care, prompting vendors to pair devices with training, analytics, and reimbursement support. Players that deliver integrated solutions are poised to capture incremental share as hospitals aim to cut total episode costs.

Cardiac Catheters And Guidewires Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic plc

Terumo Corporation

Asahi Intecc Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Abbott received CE Mark for the TactiFlex Duo Ablation Catheter, enabling the first commercial European cases in atrial fibrillation therapy.

- January 2026: Stereotaxis secured FDA approval for the MAGiC Magnetic Interventional Ablation Catheter, advancing robotic navigation for complex arrhythmias.

- May 2025: Boston Scientific gained dual CE Mark and FDA approval for the NC Quantum Apex PTCA Dilatation Balloon Catheter, with launches scheduled for Europe and the United States.

- February 2025: Johnson & Johnson MedTech introduced the CEREGLIDE 92 Catheter System, designed for large distal neurovascular access in acute stroke interventions.

Global Cardiac Catheters And Guidewires Market Report Scope

A cardiac catheter is a thin, flexible, hollow tube inserted into blood vessels to diagnose or treat heart conditions, such as measuring pressure or delivering therapies. A guidewire is an ultra-thin, steerable, solid, or coiled wire used to navigate complex vasculature, acting as a rail for catheters to follow securely.

The Cardiac Catheters and Guidewires Market Report is segmented by Product Type, Application, End User, Material, and Geography. By Product Type, the market is segmented into Diagnostic Catheters, Interventional Catheters, Guidewires, Balloon Catheters, and Others. By Application, the market is segmented into Coronary Artery Disease, Peripheral Vascular, Electrophysiology & Ablation, and Structural Heart/TAVR. By End User, the market is segmented into Hospitals, Cardiac Cath Labs, ASCs, and Specialty Clinics. By Material, the market is segmented into Nitinol, Stainless Steel, Polymers, and Hybrid Alloys. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Diagnostic Catheters |

| Interventional Catheters |

| Guidewires |

| Balloon Catheters |

| Others (Pressure, FFR, Imaging Wires) |

| Coronary Artery Disease Interventions |

| Peripheral Vascular Interventions |

| Electrophysiology & Ablation |

| Structural Heart / TAVR & Valve Repair |

| Hospitals |

| Cardiac Catheterization Labs |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Nitinol |

| Stainless Steel |

| Polymers (PTFE, PU etc.) |

| Hybrid / Composite Alloys |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Diagnostic Catheters | |

| Interventional Catheters | ||

| Guidewires | ||

| Balloon Catheters | ||

| Others (Pressure, FFR, Imaging Wires) | ||

| By Application | Coronary Artery Disease Interventions | |

| Peripheral Vascular Interventions | ||

| Electrophysiology & Ablation | ||

| Structural Heart / TAVR & Valve Repair | ||

| By End User | Hospitals | |

| Cardiac Catheterization Labs | ||

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Material | Nitinol | |

| Stainless Steel | ||

| Polymers (PTFE, PU etc.) | ||

| Hybrid / Composite Alloys | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the cardiac catheters and guidewires market expected to grow through 2031?

The market is projected to rise from USD 18.21 billion in 2026 to USD 26.01 billion by 2031, posting a 7.45% CAGR.

Which product segment is expanding the quickest?

Balloon catheters, especially drug-coated balloons, are forecast to grow at 11.44% through 2031 thanks to recent FDA approvals.

Why are ambulatory surgical centers gaining share?

Medicare’s 2025 outpatient rules favor same-day discharge, pushing stable percutaneous coronary interventions to low-cost ambulatory centers growing at 9.24% CAGR.

What material trend is challenging nitinol’s dominance?

Hybrid composite alloys combining nitinol cores with polymer or radiopaque filaments are advancing at an 11.56% CAGR, offering better visibility and supply flexibility.

Which region will add the most incremental procedures?

Asia-Pacific, led by China and India, is expanding at 9.64% CAGR due to rapid cath-lab construction and rising cardiovascular disease prevalence.

Page last updated on: