Transcatheter Aortic Valve Replacement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

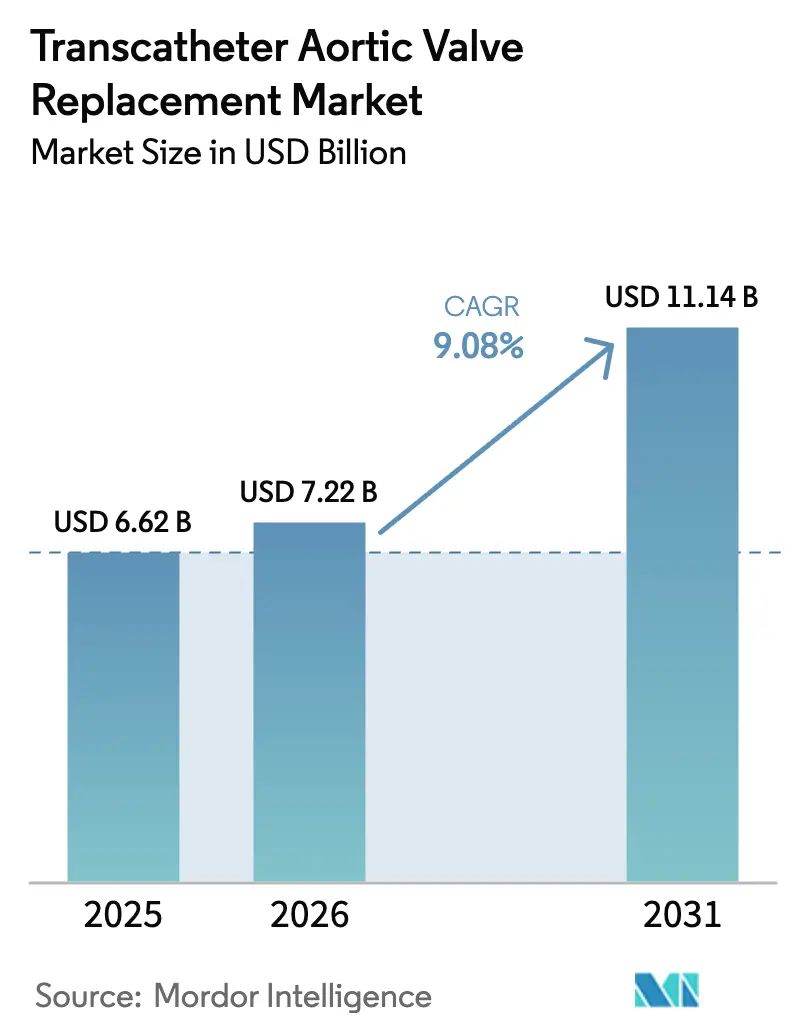

| Market Size (2026) | USD 7.22 Billion |

| Market Size (2031) | USD 11.14 Billion |

| Growth Rate (2026 - 2031) | 9.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transcatheter Aortic Valve Replacement Market Analysis by Mordor Intelligence

The transcatheter aortic valve replacement market size was valued at USD 6.62 billion in 2025 and estimated to grow from USD 7.22 billion in 2026 to reach USD 11.14 billion by 2031, at a CAGR of 9.08% during the forecast period (2026-2031). Strong growth comes from broader clinical indications, device miniaturization, and expanding global access pathways that position TAVR as the default therapy for severe aortic stenosis rather than only a high-risk alternative to open surgery. The FDA’s 2025 approval of SAPIEN 3 for asymptomatic disease effectively doubled the treatable population and triggered rapid adoption momentum in North America. Valve-in-valve procedures are emerging as a second growth vector by offering less invasive solutions for failed surgical bioprostheses. On the supply side, polymer-based leaflets and AI-guided delivery systems improve durability and precision, allowing physicians to consider TAVR for younger, lower-risk cohorts. Regional expansion, particularly in Asia-Pacific, intensifies competition as local manufacturers secure domestic approvals and lower price points.

Key Report Takeaways

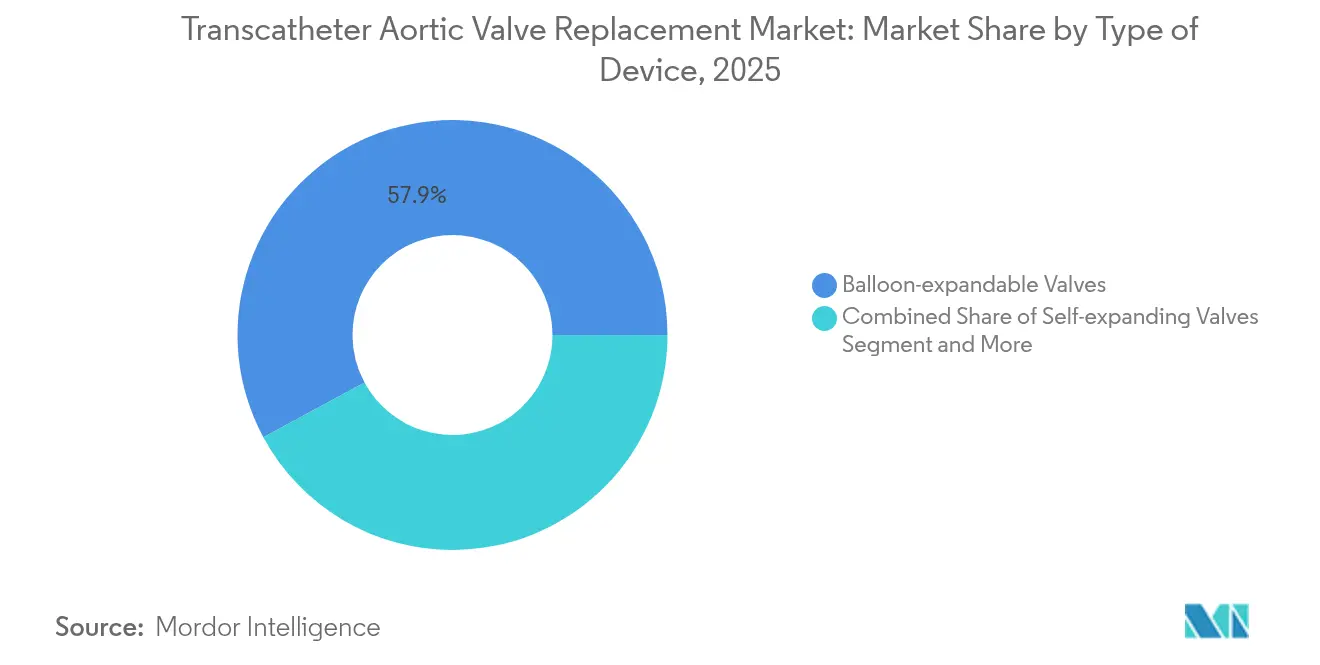

- By type of device, balloon-expandable valves led with 57.88% of transcatheter aortic valve replacement market share in 2025, while mechanically and hybrid expandable valves are projected to grow at 14.38% CAGR through 2031.

- By procedure, transfemoral access accounted for 89.10% of the transcatheter aortic valve replacement market size in 2025; transaortic access is poised to expand at 12.11% CAGR to 2031.

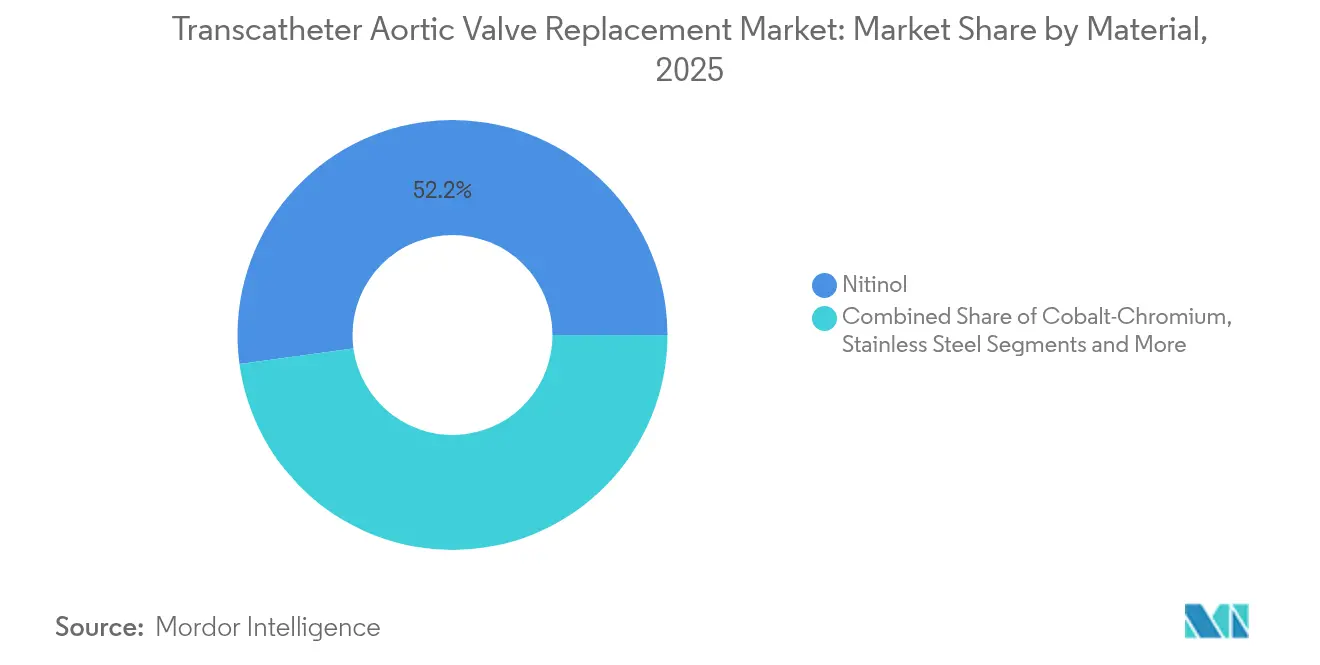

- By material, nitinol frames captured 52.15% share of the transcatheter aortic valve replacement market size in 2025, whereas polymer composites are advancing at a 12.96% CAGR.

- By end user, hospitals retained 69.05% revenue share in 2025, but ambulatory surgical centers are set to register a 11.74% CAGR through 2031 within the transcatheter aortic valve replacement market.

- By geography, North America commanded 43.20% share in 2025; the Asia-Pacific region is forecast to grow at 11.88% CAGR, making it the fastest-expanding cluster in the transcatheter aortic valve replacement market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Transcatheter Aortic Valve Replacement Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of aortic stenosis in ageing populations | +2.1% | North America & Europe, rising in APAC | Long term (≥ 4 years) |

| Demand shift toward minimally invasive cardiac therapies | +1.8% | Global, led by developed markets | Medium term (2-4 years) |

| Expanding indications into low-to-moderate surgical-risk cohorts | +2.3% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Next-gen leaflet durability and embolic-protection innovations | +1.4% | Global | Long term (≥ 4 years) |

| Valve-in-valve usage for failed surgical bioprostheses | +0.9% | North America & Europe | Short term (≤ 2 years) |

| Bundled-payment models boosting hospital adoption in OECD | +0.7% | OECD nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Aortic Stenosis In Ageing Populations

Severe aortic stenosis affects an estimated 9% of Americans older than 65, yet screening initiatives reveal substantial underdiagnosis. The 2025 FDA label expansion that allows TAVR in asymptomatic severe disease instantly broadened the treatable cohort and prompted hospital systems to invest in imaging programs and workforce training to handle rising procedure volumes[1]Abbott, “Abbott Announces First Step Toward Its Software-Guided Balloon-Expandable TAVI System to Treat Aortic Stenosis,” abbott.com. Enhanced echocardiography workflows and AI-supported triage tools shorten diagnostic timelines, further fueling the transcatheter aortic valve replacement market.

Demand Shift Toward Minimally-Invasive Cardiac Therapies

Median hospital stay after TAVR is now less than three days and in-hospital mortality is under 1% in experienced centers, making it competitive with and often superior to surgery[2]Cardiovascular Business, “Boston Scientific pulls plug on TAVR devices after failing to gain FDA approval,” cardiovascularbusiness.com. Bundled payment models show 20-30% lower total episode costs, encouraging payers and providers to favor TAVR over sternotomy. Same-day discharge protocols executed in ambulatory surgical centers cut costs another 40-50%, expanding addressable out-of-hospital volumes in the transcatheter aortic valve replacement market.

Expanding Indications Into Low-To-Moderate Surgical-Risk Cohorts

Outcomes from the PARTNER 3 and Evolut Low-Risk trials demonstrated non-inferiority and sometimes superiority of TAVR versus surgery in younger, healthier patients, prompting clinical guidelines to recommend TAVR for individuals aged 65-80 regardless of operative risk. Device companies now focus on long-term leaflet durability and ease of future valve-in-valve interventions, ensuring sustained trust among this demographic and pushing new demand into the transcatheter aortic valve replacement market.

Next-Gen Leaflet Durability & Embolic-Protection Innovations

Polymer composite leaflets show higher calcification resistance and potential performance longevity, addressing a core durability concern that historically limited uptake in younger patients. Simultaneously, advanced cerebral protection systems are selectively deployed in high-risk strokes, strengthening operator confidence. These advancements facilitate wider adoption and reinforce value propositions in the transcatheter aortic valve replacement industry.

Restraints Impact Analysis of Transcatheter Aortic Valve Replacement Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & procedure cost burden on payers | -1.6% | Emerging markets global | Medium term (2-4 years) |

| Stroke, conduction disturbances & PV-leak complications | -1.2% | Global, higher in low-volume centers | Short term (≤ 2 years) |

| Inconsistent reimbursement in EMs & some APAC countries | -0.8% | Latin America & parts of APAC | Long term (≥ 4 years) |

| Nitinol supply-chain bottlenecks | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device & Procedure Cost Burden On Payers

Device pricing sits near USD 30,000 per valve, consuming 60-70% of direct procedural spend, a hurdle for systems managing growing volumes after indication expansion. Bundled payments shift part of the risk to providers, compelling negotiations with manufacturers and driving exploration of domestic alternatives in Asia to temper costs across the transcatheter aortic valve replacement market.

Stroke, Conduction Disturbances & PV-Leak Complications

Despite lower rates than early eras, 2-4% stroke incidence, 10-20% pacemaker implantation, and 5-10% moderate PV-leak still deter low-risk candidates. Hospitals answer with operator credentialing, imaging-guided sizing, and selective cerebral protection to uphold quality metrics crucial for confidence in the transcatheter aortic valve replacement market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Transcatheter Aortic Valve Replacement Market Segment Analysis

By Type of Device:

Balloon-Expandable Dominance Faces Innovation ChallengeBalloon-expandable valves generated the largest revenue share at 57.88% in 2025, reinforcing their status as the benchmark platform within the transcatheter aortic valve replacement market. This position stems from predictable deployment and long-term data that comfort physicians managing complex comorbidities. The transcatheter aortic valve replacement market size for mechanically and hybrid expandable valves is projected to post a 14.38% CAGR through 2031, aided by repositioning capabilities that better address non-circular annuli and previously implanted surgical valves.

Mechanical-hybrid innovations borrow from both balloon and self-expanding designs, giving operators retrieval flexibility absent in earlier irreversible deployments. Major manufacturers are investing in polymer leaflets, low-profile sheaths, and AI-navigation to reduce complication rates and extend durability—critical factors as indications broaden to patients under 70 years. This competitive evolution is anticipated to redistribute revenue share but not immediately dethrone balloon-expandable devices, which still accumulate broad procedural familiarity and outcome data.

By Procedure:

Transfemoral Access Consolidates While Alternative Routes EvolveTransfemoral access reached 89.10% utilization in 2025, reflecting advances in delivery profiles, vascular closure, and operator proficiency that removed many anatomic exclusions. The transcatheter aortic valve replacement market now sees alternative transaortic routes growing at 12.11% CAGR, especially for heavily calcified or small femoral arteries.

Cardiac teams employ 3-D CT reconstruction to map optimal insertion angles, minimizing trauma and boosting one-year survival metrics. Transapical access continues to decline as less invasive alternatives mature, yet remains an option in select redo thoracotomy patients. Training emphasis has shifted to procedural versatility, ensuring a comprehensive access toolkit supportive of ever-more diverse patient anatomies.

By Material:

Nitinol Leadership Challenged by Polymer InnovationNitinol’s 52.15% share derived from its shape-memory properties suits self-expanding valves, anchoring its dominance in the transcatheter aortic valve replacement market. However, polymer composites are gaining interest; the segment is expected to expand at 12.96% CAGR through 2031. Developers highlight better calcification resistance, thromboresistance, and extended hemodynamic stability versus animal pericardium.

Supply concerns surface as nitinol sourcing concentrates in limited geographies. Consequently, manufacturers diversify raw-material procurement and invest in polymer R&D to lower exposure. Stainless-steel and cobalt-chromium frames maintain niche relevance in balloon-expandable systems demanding rigid radial force.

By End User:

Hospital Dominance Shifts Toward Outpatient ModelsHospitals represented 69.05% of global revenue in 2025, but ambulatory surgical centers show the fastest 11.74% CAGR, evidencing payers’ preference for lower-cost settings. US ASC procedure volumes rose 2.8% year-on-year in 2024, with cardiology leading gains.

ASC expansion pushes device makers to generate real-world evidence supporting same-day discharge safety, while operators refine fast-track recovery pathways. Hybrid cardiac centers located near tertiary hospitals ensure emergency backup, providing confidence for complex cases transitioning out of inpatient suites.

Geography Analysis

North America Transcatheter Aortic Valve Replacement Market

North America contributed 43.20% of global revenue in 2025, reflecting mature reimbursement, early technology adoption, and the largest installed base of certified TAVR programs. Growth here moderates as penetration nears structural ceilings, but procedure volume still climbs due to the asymptomatic indication expansion and robust valve-in-valve demand. CMS reimbursement updates continue to shape utilization but rarely curtail momentum in the transcatheter aortic valve replacement market.

APAC, EMEA and LATAM Transcatheter Aortic Valve Replacement Market

Asia-Pacific is forecast to register a 11.88% CAGR, the quickest worldwide. China exemplifies this arc: domestic manufacturers such as MicroPort gained NMPA clearance for third-generation systems in 2025, lowering costs and increasing access among a rapidly ageing population. Japan, with national coverage, posts one of the world’s highest per-capita procedure rates, whereas India advances more slowly given out-of-pocket pay models. Europe maintains steady volumes with reimbursement stability in Germany, France, and the Nordics. Ongoing guideline endorsements and registry-based quality tracking encourage physicians to steer eligible patients toward minimally invasive solutions. Latin America and the Middle East show gradual growth tied to economic cycles and private insurance uptake. Market entry strategies hinge on distributor alliances and tailored training programs to overcome workforce constraints.

Competitive Landscape

The transcatheter aortic valve replacement market remains concentrated, with Edwards Lifesciences and Medtronic anchoring share through broad portfolios and extensive clinical evidence. Boston Scientific’s 2025 withdrawal, after consecutive FDA setbacks, underscores high regulatory hurdles and reinforces incumbents’ positions.

Manufacturers increasingly compete on durability claims, frame flexibility, and leaflet technology rather than price. AI-integrated delivery catheters and real-time hemodynamic monitoring differentiate offerings while amplifying procedural safety. Geographic expansion strategies involve partnering with regional value analysis committees and fostering local manufacturing, as seen with MicroPort’s supply chain localization in China. Intellectual-property disputes, such as Meril vs Edwards in Europe, indicate sustained patent significance.

Second-tier challengers focus on niche anatomies, including purely transcatheter solutions for pure aortic regurgitation and ultra-low profile devices suitable for small annuli prevalent in Asian populations. Suppliers of adjunctive technologies—imaging, embolic protection, and closure devices—forge ecosystem alliances, boosting cross-selling and procedure standardization throughout the transcatheter aortic valve replacement industry.

Transcatheter Aortic Valve Replacement Industry Leaders

Bracco SpA

Medtronic plc

Abbott Laboratories

Boston Scientific Corp.

Edwards Lifesciences Corp.

- *Disclaimer: Major Players sorted in no particular order

Transcatheter Aortic Valve Replacement Market Companies Covered in this Report

- Edwards Lifesciences Corp.

- Medtronic

- Boston Scientific

- Abbott Laboratories

- Meril Life Science

- JenaValve Technology Inc.

- Artivion Inc. (ex-CryoLife)

- Lepu Medical Technology Co.

- Venus Medtech

- MicroPort Scientific Corp.

- Transcatheter Technologies GmbH

- Bracco

- Peijia Medical Ltd.

- Balanced Medical Solutions LLC

- Xeltis BV

- NaviGate Cardiac Structures Inc.

- HighLife SAS

- Colibri Heart Valve

- FoldaValve Ltd.

Read Analysis of Transcatheter Aortic Valve Replacement Companies

Recent Industry Developments in Transcatheter Aortic Valve Replacement Market

- January 2025: MicroPort CardioFlow received NMPA approval in China for the VitaFlow Liberty Flex TAVI system, intensifying domestic competition.

- December 2024: Abbott completed first-in-human use of its AI-guided balloon-expandable TAVI platform, introducing software-driven precision deployment.

Transcatheter Aortic Valve Replacement Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the transcatheter aortic valve replacement (TAVR) market as all commercially marketed catheter-delivered prosthetic aortic valves, their dedicated delivery systems, and associated implantation accessories that enable minimally invasive replacement of native stenotic valves in adults who are judged high, intermediate, or low surgical risk. Devices intended exclusively for pre-clinical research or non-aortic transcatheter valve therapies fall outside this scope.

Scope exclusion: surgical aortic valve replacement devices and repair accessories are not counted.

Segments Covered in This Report

- By Type of Device

- Self-expanding Valves

- Balloon-expandable Valves

- Mechanically & Hybrid Expandable Valves

- By Procedure

- Transfemoral

- Transapical

- Transaortic

- By Material

- Nitinol

- Cobalt-Chromium

- Stainless Steel

- Polymer Composites

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Cardiovascular Centers

- Cath Labs & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed interventional cardiologists, structural-heart program directors, cath-lab managers, and reimbursement specialists across North America, Europe, and Asia-Pacific. These conversations clarified real-world patient selection thresholds, procedural mix shifts, negotiated ASP corridors, and likely timing of next-generation valve launches, enabling us to confirm assumptions and reconcile desk findings.

Desk Research

We began with procedure-volume and disease-burden datasets available from open repositories such as the WHO Global Health Estimates, OECD Health Statistics, the U.S. Centers for Medicare & Medicaid Services Part B claims files, and Eurostat hospital-discharge tables. Regulatory approval notices on FDA and EMA portals, patent families extracted through Questel, and peer-reviewed outcome studies in journals like JACC supplied technology uptake signals. Company 10-Ks, investor decks, and press releases were screened on Dow Jones Factiva for shipment trends and average selling price (ASP) commentary, which anchor the revenue side of our model. These sources illustrate, rather than exhaust, the secondary material we mined to establish the evidence base.

A second desk pass used trade-association briefs (Society for Cardiovascular Angiography and Interventions, European Association for Percutaneous Cardiovascular Interventions) plus customs dashboards such as Volza to refine the regional flow of finished valves and delivery kits, flagging anomalies for analyst review. The sources listed here are representative, and many additional public and proprietary references contributed to data collection and validation.

Market-Sizing & Forecasting

Our top-down model starts with treated-patient pools reconstructed from national procedure registries and payer claims; volumes are multiplied by regional ASP medians, then reconciled with sampled manufacturer revenue lines to catch under-coding or inventory timing effects. Bottom-up cross-checks, such as supplier roll-ups and cath-lab channel checks, help fine-tune totals. Key variables include the prevalence of severe aortic stenosis in 70+ cohorts, TAVR penetration rate among eligible patients, share of transfemoral access, mean device ASP trends, and reimbursement-policy shifts. A multivariate regression, incorporating aging-population curves, risk-stratification adoption, and valve-technology upgrade cycles, projects demand through 2030. Gaps in bottom-up evidence are bridged using conservative elasticity factors agreed upon during primary interviews.

Data Validation & Update Cycle

Outputs pass variance screens against independent procedure tallies; currency conversions are standardized quarterly, and any anomaly triggers a senior analyst review before final sign-off. Reports refresh yearly; interim updates are issued when regulatory, reimbursement, or competitive events materially alter volume or price baselines.

How Mordor Intelligence's Transcatheter Aortic Valve Replacement Market Size Compares to Other Published Estimates

Published TAVR estimates often diverge because firms choose different device mixes, patient-risk pools, and refresh cadences.

Key gap drivers include: some studies fold surgical valve revenue into totals; others apply flat ASP deflators that ignore premium-cohort pricing; several models extrapolate limited U.S. registry data globally without adjusting for delayed approvals and payer hurdles elsewhere. Mordor's scope, variable selection, and yearly refresh cycle minimize such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.62 bn (2025) | Mordor Intelligence | - |

| USD 6.83 bn (2024) | Global Consultancy A | Includes surgical valve kits; uses single-region ASP applied worldwide |

| USD 5.64 bn (2024) | Industry Journal B | Excludes low-risk patient cohort; relies on historical growth extrapolation |

| USD 7.22 bn (2025) | Regional Consultancy C | Uses list-price ASP without volume-weighted discounts |

These comparisons show that Mordor's disciplined triangulation and timely updates deliver a balanced, decision-ready baseline that clients can trace to transparent variables and reproducible steps.

Key Questions Answered in the Report

What is the current global value of the transcatheter aortic valve replacement market?

The market is valued at USD 7.22 billion in 2026 and is projected to hit USD 11.14 billion by 2031.

Which region shows the fastest growth in the transcatheter aortic valve replacement market?

Asia-Pacific leads with a 11.88% forecast CAGR through 2031, driven by ageing demographics and local manufacturing approvals.

Why are ambulatory surgical centers gaining share in TAVR procedures?

Same-day discharge protocols and bundled payments cut total costs up to 50%, making ASCs attractive for payers and patients.

Which device segment is expected to grow the quickest?

Mechanically and hybrid expandable valves are projected at a 14.38% CAGR due to repositioning features for complex anatomies.

How are polymer composite valves influencing future adoption?

Polymers promise improved durability and lower calcification, encouraging use in younger, low-risk patients who need long-lasting implants.

What key restraint could slow growth in emerging markets?

High device prices relative to healthcare budgets and uneven reimbursement policies limit procedure adoption outside developed economies.

Page last updated on: