Global Angiographic Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

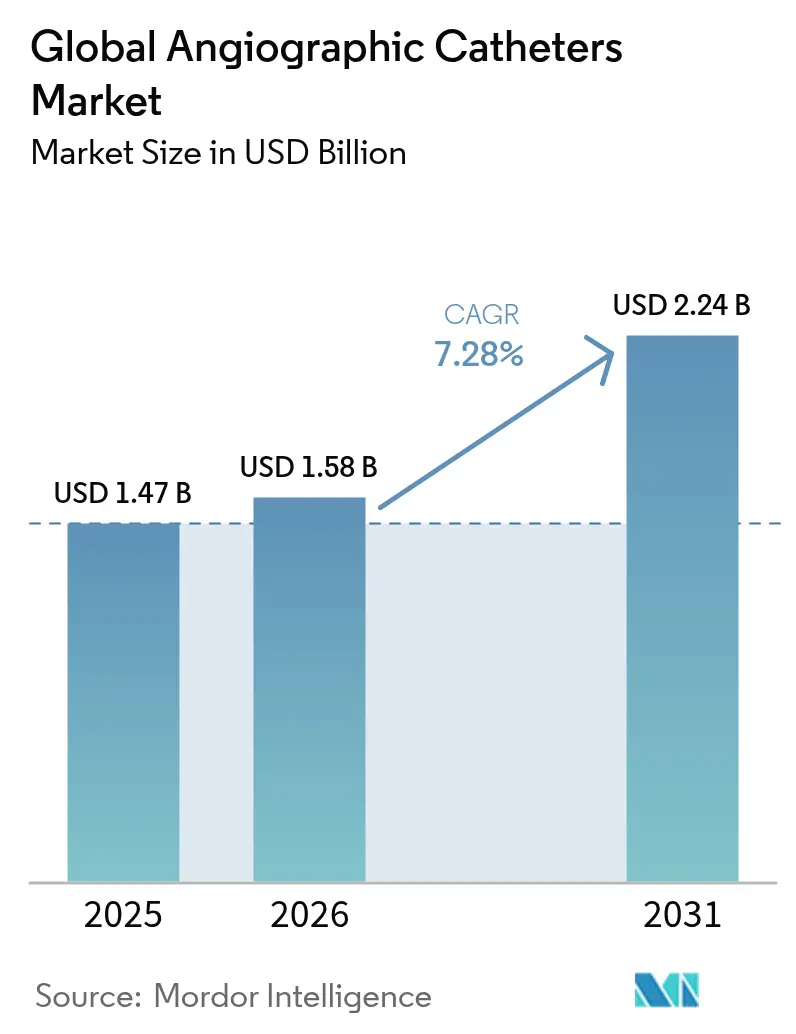

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Angiographic Catheters Market Analysis by Mordor Intelligence

The angiographic catheter market size was valued at USD 1.47 billion in 2025 and estimated to grow from USD 1.58 billion in 2026 to reach USD 2.24 billion by 2031, at a CAGR of 7.28% during the forecast period (2026-2031). This growth reflects rising cardiovascular disease (CVD) prevalence, rapid device innovation, and the continued migration of percutaneous procedures to outpatient settings. An aging population with complex comorbidities drives steady procedural volume, while reimbursement reforms encourage hospitals and ambulatory sites to adopt minimally invasive solutions that shorten stays and lower overall costs. Material science breakthroughs—particularly Nylon & Pebax blends—improve torque control and kink resistance, enabling complex interventions through smaller access points. Strategic acquisitions such as Boston Scientific’s purchase of Silk Road Medical and Teleflex’s buyout of BIOTRONIK’s vascular unit signal that scale and technological breadth remain decisive competitive levers. Conversely, expanding use of intravascular imaging is beginning to reduce purely angiography-guided runs, creating a long-term usage headwind for basic catheters.

Key Report Takeaways

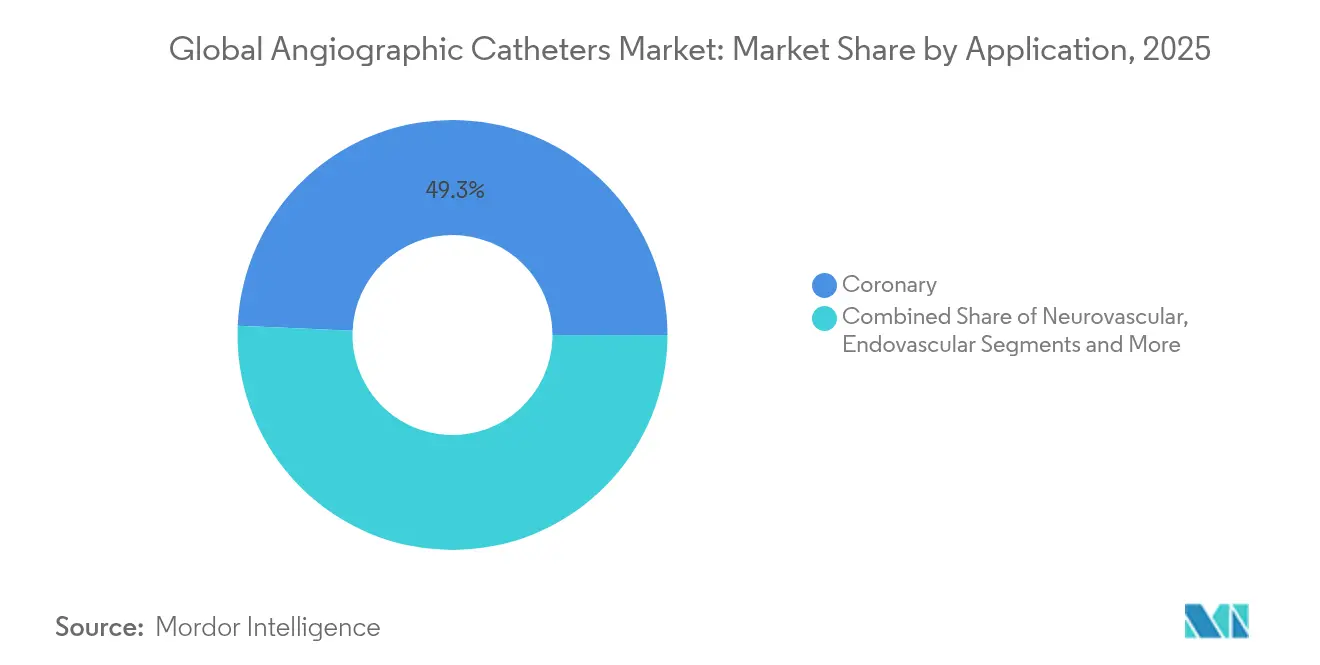

- By application, coronary procedures held 49.32% of angiographic catheter market share in 2025; neurovascular applications are projected to expand at a 7.96% CAGR through 2031.

- By end-user, hospitals accounted for 64.78% of the angiographic catheter market size in 2025, whereas ambulatory surgical centers (ASCs) are poised for the fastest growth at an 8.15% CAGR to 2031.

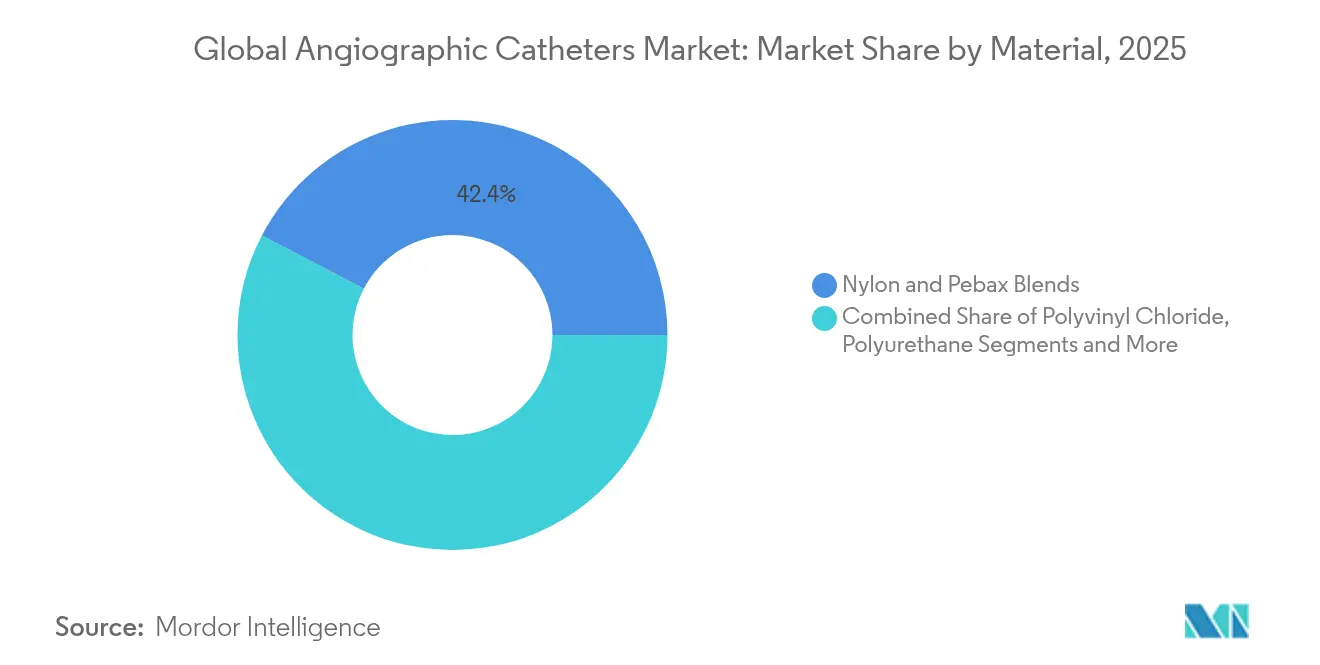

- By material, Nylon & Pebax blends dominated with a 42.35% share of the angiographic catheter market in 2025; polyurethane lines are forecast to rise at a 7.74% CAGR.

- By coating type, non-coated products retained 54.62% revenue share in 2025, while hydrophilic-coated lines are advancing at an 8.33% CAGR through 2031.

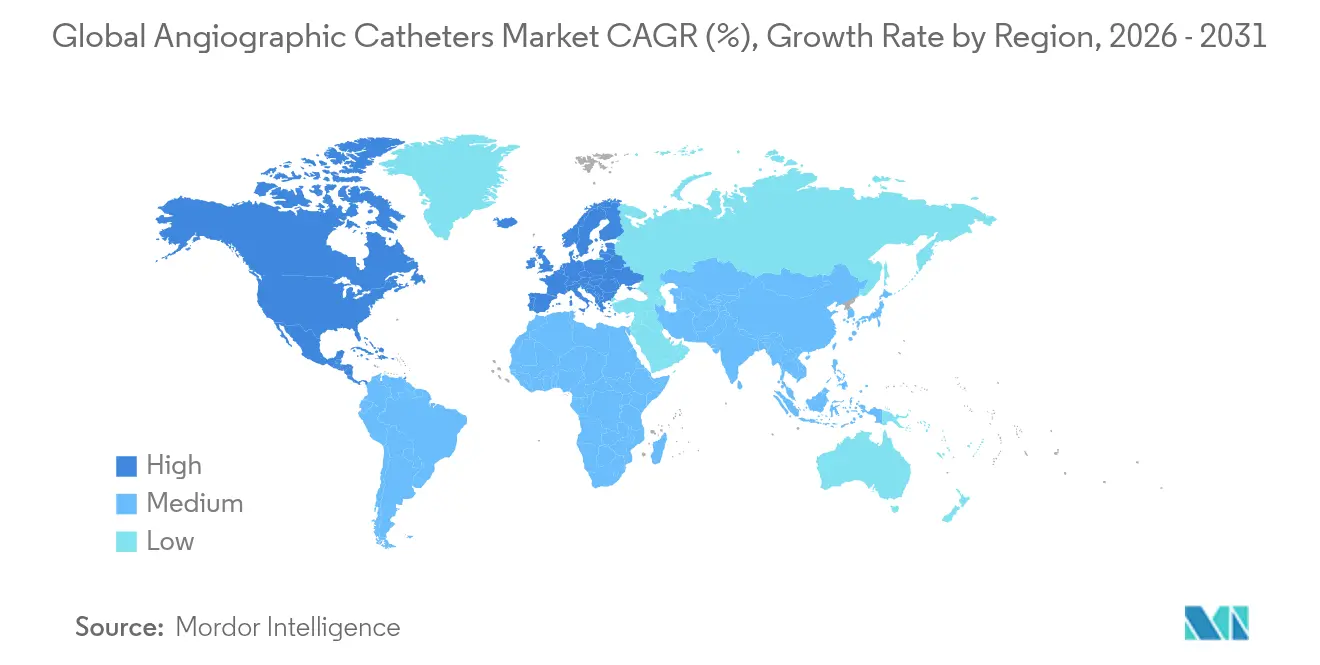

- By geography, North America commanded 42.18% of 2025 revenue; Asia-Pacific is the fastest-growing region at an 8.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Angiographic Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of cardiovascular diseases | +1.8% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Growing geriatric population prone to CVD | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Demand for minimally invasive procedures | +1.5% | Global, led by North America & Asia-Pacific | Medium term (2-4 years) |

| Expansion of ambulatory cath-labs in EMS | +1.0% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| AI-enabled 3-D road-mapping integration | +0.8% | North America & Europe, selective Asia-Pacific adoption | Short term (≤ 2 years) |

| Ultra-low-profile polymer blends for radial access | +0.5% | Global, fastest adoption in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Of Cardiovascular Diseases

Ischemic heart disease remained the leading cause of CVD deaths in 2024, claiming 20.5 million lives and shifting therapeutic focus toward earlier diagnosis and less-invasive care [1]Global Heart Journal, “Global Burden of Ischemic Heart Disease,” globalheartjournal.com. Emerging economies experience the steepest climb as dietary and lifestyle risk factors converge with urbanization. Procedural volumes therefore rise in tandem, especially where governments invest in catheterization capacity. Private-equity groups viewed this demand as durable, acquiring 41 cardiology practices comprising 342 sites between 2021 and 2023 to build regional networks that capture steady referral streams. These trends collectively sustain healthy growth in the angiographic catheter market.

Growing Geriatric Population Prone To CVD

Older adults present higher rates of multivessel stenosis, calcified lesions, and frailty, each necessitating specialized catheter platforms that balance pushability with vessel safety. Vascular stiffening complicates device navigation, prompting manufacturers to refine shaft stiffness gradients and tip flexibility. Minimally invasive access translates to shorter recovery times—an outcome prized by physicians managing elderly patients with multiple comorbidities. Global cardiac surgery benchmarking suggests an unmet need of 61.6 catheter-based or surgical cardiac procedures per 100,000 population in low- and middle-income countries, implying vast room for catheter expansion as life expectancy rises [2]Annals of Thoracic Surgery, “Global Cardiac Surgery Volume Benchmarks,” annalsthoracicsurgery.org.

Demand For Minimally-Invasive Procedures

Radial access has reduced major bleeding by more than 70% versus femoral techniques, making wrist-based entry the new default for uncomplicated PCI. Hospitals increasingly discharge same day, lowering costs and freeing beds. Continuous AI integration, such as automated FFR estimation, provides real-time hemodynamic insights through standard angiograms, further streamlining workflows. The ECLIPSE trial reported a 26% reduction in target-vessel failure when intravascular imaging guided stent placement, reinforcing precision benefits over conventional angiography. Together these factors accelerate adoption of sophisticated catheters capable of delivering complex therapies through ever-smaller lumens.

Expansion Of Ambulatory Cath-Labs In EMS

Medicare’s 2020 policy to cover basic PCI in ASCs spurred facility growth; ASC sites billing for PCI climbed from 30 in 2019 to 65 in 2023. Yet ASCs still handle only 1.8% of outpatient PCI volume, signaling substantial headroom for shift from hospitals. Dedicated cath-lab workflows allow higher daily case throughput, while new ASC-only reimbursement codes add up to USD 2,321 per peripheral vascular case, strengthening their economic rationale. As social-vulnerability mapping shows, many new centers locate in underserved U.S. counties, broadening geographic access and sustaining the angiographic catheter market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of angiographic procedures | -0.9% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Catheter-related complications & recalls | -0.6% | Global, regulatory scrutiny highest in developed markets | Short term (≤ 2 years) |

| Reimbursement uncertainties in emerging markets | -0.8% | Latin America, Middle East, Africa, parts of Asia-Pacific | Long term (≥ 4 years) |

| Intravascular imaging reducing stand-alone angiography | -1.2% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost Of Angiographic Procedures

Device prices, facility fees, and post-acute care combine to make angiography among the costliest routine hospital procedures, a reality magnified in cash-pay and publicly funded systems. The USD 156 billion U.S. device market demonstrates that navigating complex reimbursement channels remains resource-intensive for manufacturers [3]National Institutes of Health, “Medical Device Market Statistics,” nih.gov. Cost-effectiveness studies increasingly favor pharmacologic or preventive options for borderline lesions, potentially dampening catheter usage when payers tighten thresholds. Utilization-management programs that mandate prior authorization now span most U.S. insurers, adding administrative lag that can defer non-urgent cases.

Intravascular Imaging Reducing Stand-Alone Angiography Usage

Meta-analyses show intravascular ultrasound lowers mortality (HR 0.59) and stent thrombosis (HR 0.58) relative to angiography-only guidance. As IVUS and OCT systems gain reimbursement, operators reduce contrast injections and radiation exposure by substituting image-based lesion sizing. While up-front imaging capital costs are high, procedural efficiency gains increasingly justify purchase. Hybrid catheters that combine imaging and delivery lumens represent an adaptive play for incumbents, preserving relevance within a changing diagnostic landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Coronary Dominance Drives Innovation

The coronary segment accounted for 49.32% of the angiographic catheter market share in 2025 and remains the bedrock of vendor revenue. Despite mature protocols, ongoing material and coating enhancements keep demand steady, with the angiographic catheter market size for coronary work projected to rise in parallel with stable 7%-plus CAGR. Neurovascular catheters, by contrast, show an 7.96% CAGR as mechanical thrombectomy becomes front-line for large-vessel stroke. Ultra-trackable distal access catheters and aspiration platforms such as SOFIA Flow 88 optimize clot retrieval success rates, pushing neurovascular penetration higher.

Endovascular and peripheral interventions form a sizable mid-tier, where devices like intravascular lithotripsy catheters treat heavily calcified lesions. The “Others” category, renal denervation, structural heart, and hybrid platforms, remains small yet lucrative. Medtronic’s Symplicity Spyral won transitional pass-through status in 2025, unlocking incremental reimbursement and placing hypertension therapy firmly within the angiographic catheter market.

By End-User: Hospital Dominance Faces ASC Challenge

Hospitals retained 64.78% of 2025 revenue, largely because they manage complex and emergent cases requiring surgical back-up or ICU care. The angiographic catheter market size attributable to hospitals should still climb but at a slower rate than ASCs. Outpatient centers enjoy lean staffing models and dedicated rooms, translating to shorter turnaround and improved patient throughput. Growth momentum is further reinforced by private-equity consolidation of cardiology groups that establish in-house ASCs to capture downstream device margins.

Specialty clinics and office-based labs occupy a niche for diagnostic angiography and simple interventions, relying on shared staff with nearby hospitals. Their appeal lies in lower facility fees and community proximity, though capital requirements limit expansion pace. Mobile cath-lab units and hybrid ORs round out the landscape, offering flexible solutions for underserved regions or combined surgical-interventional cases.

By Material: Advanced Polymers Lead Innovation

Nylon & Pebax blends represented 42.35% of 2025 revenue because they deliver the optimal trio of pushability, torque control, and kink resistance necessary for tight lesion navigation. Polyurethane lines, advancing at a 7.74% CAGR, capitalize on new biocompatible additives that lower thrombogenicity and support drug-eluting applications. PVC remains the workhorse for cost-sensitive markets; surface engineering such as hyperbranched polylysine coatings dramatically improves hydrophilicity without changing base resin economics.

Regulators increasingly scrutinize coating integrity. China’s YY/T 1898-2024 standard for hydrophilic layer adhesion forces manufacturers to validate durability under simulated use. Global suppliers respond with long-life heparin-network coatings that preserve anti-thrombotic performance up to 30 days. Smart polymers incorporating shape-memory nitinol and bio-resorbable backbones also enter limited use, foreshadowing next-generation hybrid constructs.

By Coating Type: Hydrophilic Growth Accelerates

Uncoated catheters maintained 54.62% revenue in 2025, driven by lower price points and established clinician comfort. Nevertheless, hydrophilic-coated products are gaining fastest at 8.33% CAGR because they diminish insertion force and improve trackability across tortuous vasculature. University-developed technologies extend surface wetness duration, mitigating “dry-out” risks during lengthy neurovascular procedures. Coatings are also becoming multifunctional: Terumo funded antimicrobial layers that release silver ions slowly, targeting infection control without compromising lubricity.

Regulatory agencies now demand quantitative friction and durability metrics, compelling suppliers to adopt robust test protocols. Over the forecast period, suppliers are expected to launch smart coatings capable of on-demand drug release or pH-responsive swelling, enhancing therapeutic value beyond mechanical delivery.

Geography Analysis

North America captured 42.18% revenue in 2025, underpinned by broad insurance coverage, national clinical guidelines, and high procedural density. Transitional pass-through payments for break-through devices shorten payback cycles, incentivizing hospitals to upgrade inventories. The U.S. alone holds 40% of global device sales and exerts outsized influence on material and coating standards. Consolidation among cardiology practices has accelerated, bringing ASC development to both urban and underserved rural counties, thereby preserving volume growth in the angiographic catheter market.

Asia-Pacific logs the highest CAGR at 8.62%. China streamlined device reviews, approving 12,213 new registrations in 2023, including 61 classified as innovative, which sharply cuts time-to-market. Government push under Healthy China 2030 and rising CVD incidence create dual demand and policy tailwinds. Japan and South Korea contribute through export-oriented manufacturing, while India’s 2025 marketing code elevates ethical promotion standards, giving multinational brands clearer compliance guidance.

Europe offers steady but slower gains. The Medical Device Regulation unifies market entry, and Germany’s updated OPS coding ensures reimbursement alignment for novel procedures. France’s 2025 add-on payment policy widens access to specialty catheters once superiority is proven. Post-Brexit, the UK maintains a distinct yet harmonized pathway that still recognizes much of the Continental clinical evidence file, limiting duplicative trials.

The Middle East & Africa and South America collectively present high-single-digit growth potential but face structural hurdles. In North Africa, ischemic heart disease ranks among leading DALY drivers, yet public funding gaps and brain drain hinder cath-lab expansion. Opportunities lie in public-private partnerships and regional manufacturing of base-grade catheters. In Latin America, Brazil spearheads adoption through hybrid cardiac centers in tertiary hospitals, while Argentina and Colombia steadily update reimbursement lists, albeit with currency volatility risks.

Competitive Landscape

Global leadership rests with diversified multinationals holding broad, technologically differentiated portfolios. Boston Scientific’s USD 1.26 billion Silk Road Medical acquisition broadens its stroke-prevention suite and complements lithotripsy know-how acquired via Bolt Medical, enabling cross-segment synergies. Teleflex’s EUR 760 million purchase of BIOTRONIK’s vascular division similarly boosts access to drug-coated balloons and scaffold technologies, creating a one-stop shop for peripheral interventions.

Medium-tier players pursue focused innovation: Shockwave Medical’s intravascular lithotripsy catheters open heavily calcified lesions while preserving vessel integrity, making the firm a takeover candidate. Penumbra expands neurovascular reach with aspiration platforms that integrate AI-based clot characterization software. Start-ups rise in robotics and autonomous navigation, using machine-learning algorithms to compute optimal catheter paths in real time.

Quality, however, remains a market gatekeeper. Boston Scientific recalled over 1 million units in 2024 after identifying potential separation at proximal hubs, exemplifying the reputational and financial risks of manufacturing lapses. Providers increasingly demand supplier uptime guarantees, spurring investment in inline vision inspection and predictive maintenance. Collectively these dynamics yield a moderately consolidated environment in which the top five vendors hold about 55% share, while regional specialists fill high-growth niches.

Global Angiographic Catheters Industry Leaders

AngioDynamics

Cook Medical

Medtronic

Merit Medical Systems, Inc.

Terumo Interventional Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cook Medical initiated a Class I recall of Beacon Tip 5.0 Fr angiographic catheters due to incidents of tip separation during use.

- June 2025: Terumo partnered with MedHub AI to market the AutocathFFR™ coronary physiology platform in Japan, with commercial launch set for October.

- June 2025: Terumo Neuro commenced EMEA distribution of the SOFIA™ Flow 88 aspiration catheter to enhance large-vessel stroke reperfusion capabilities.

Global Angiographic Catheters Market Report Scope

As per the scope of the report, an angiographic catheter or diagnostic catheter is a tubular device that can be inserted into the anatomical cavity or blood vessels to allow the passage of fluid from or into a body cavity or blood vessel. Such catheters facilitate selective locating (as in a renal or coronary vessel) from a remote entry site. The Angiographic Catheters Market is segmented by Application (Coronary, Endovascular, Others), End-User (Hospital, Ambulatory Surgical Centers, Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Coronary |

| Endovascular / Peripheral |

| Neurovascular |

| Others |

| Hospitals |

| Ambulatory Surgical Centres |

| Specialty Clinics |

| Others |

| Polyurethane |

| Polyvinyl Chloride |

| Nylon & Pebax Blends |

| Others |

| Hydrophilic |

| Non-coated |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Coronary | |

| Endovascular / Peripheral | ||

| Neurovascular | ||

| Others | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centres | ||

| Specialty Clinics | ||

| Others | ||

| By Material | Polyurethane | |

| Polyvinyl Chloride | ||

| Nylon & Pebax Blends | ||

| Others | ||

| By Coating Type | Hydrophilic | |

| Non-coated | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Global Angiographic Catheters Market size?

The angiographic catheter market was worth USD 1.58 billion in 2026 and is set to reach USD 2.24 billion by 2031.

Which application segment leads the angiographic catheter market?

Coronary procedures lead, commanding 49.32% market share in 2025, supported by well-established clinical protocols.

Which is the fastest growing region in Global Angiographic Catheters Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which material occupies the largest share of catheter construction?

Nylon & Pebax blends hold 42.35% share because they combine torque strength with flexibility critical for complex anatomy.

Page last updated on: