United States Thoracic Catheter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

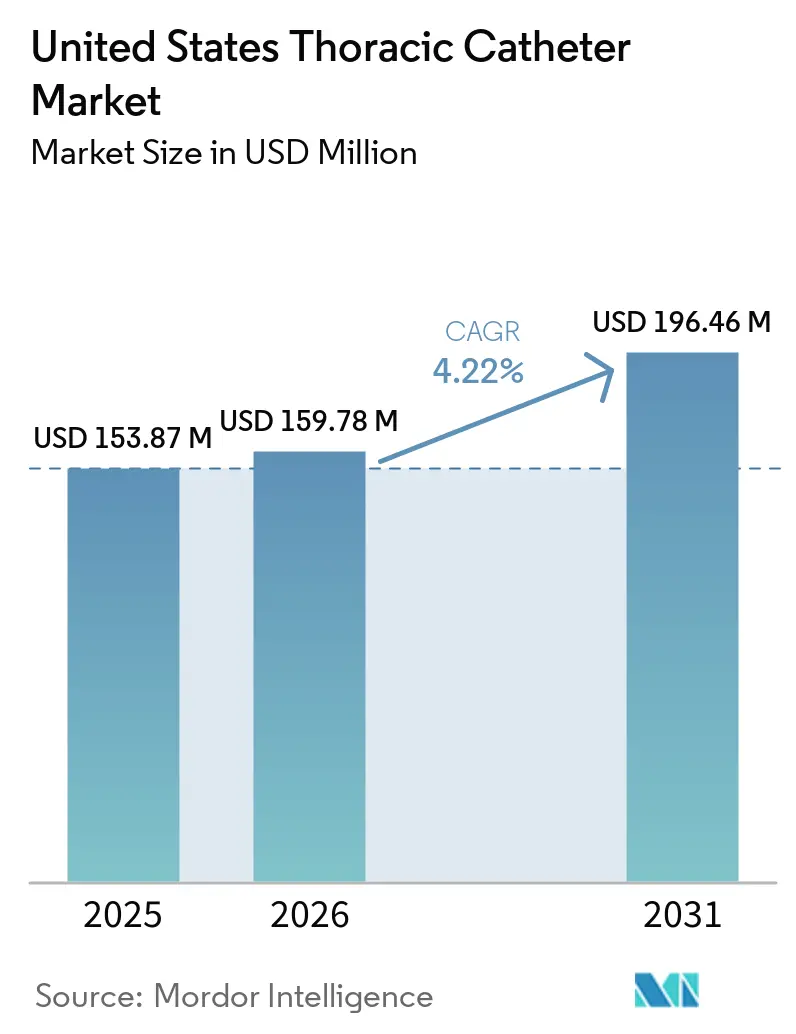

| Base Year Market Size (2025) | USD 153.87 Million |

| Market Size (2026) | USD 159.78 Million |

| Market Size (2031) | USD 196.46 Million |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Thoracic Catheter Market Analysis by Mordor Intelligence

The United States Thoracic Catheter Market size is expected to increase from USD 153.87 million in 2025 to USD 159.78 million in 2026 and reach USD 196.46 million by 2031, growing at a CAGR of 4.22% over 2026-2031.

The United States thoracic catheter market is being supported by an aging population, a higher cancer burden, and wider use of minimally invasive drainage pathways that reduce the need for more invasive approaches in selected cases. The market is also shaped by 2 distinct demand pools, with acute trauma and postoperative care sustaining conventional drainage volumes, while recurrent pleural effusion care supports the shift toward tunneled and premium catheter systems. This separation in demand is important because the premium side of the US thoracic catheter market is advancing faster than the conventional side, which is changing product mix and supplier priorities over time. Digital drainage-compatible solutions are growing faster than the broader market, which shows that hospitals are placing more value on objective monitoring, earlier mobilization, and workflow standardization in thoracic care. Competition remains active because large suppliers still benefit from broad hospital access and contract coverage, but price pressure on standard kits is pushing manufacturers toward digital integration, differentiated procedure kits, and recurrent revenue models tied to disposables rather than only base catheter sales.

Key Report Takeaways

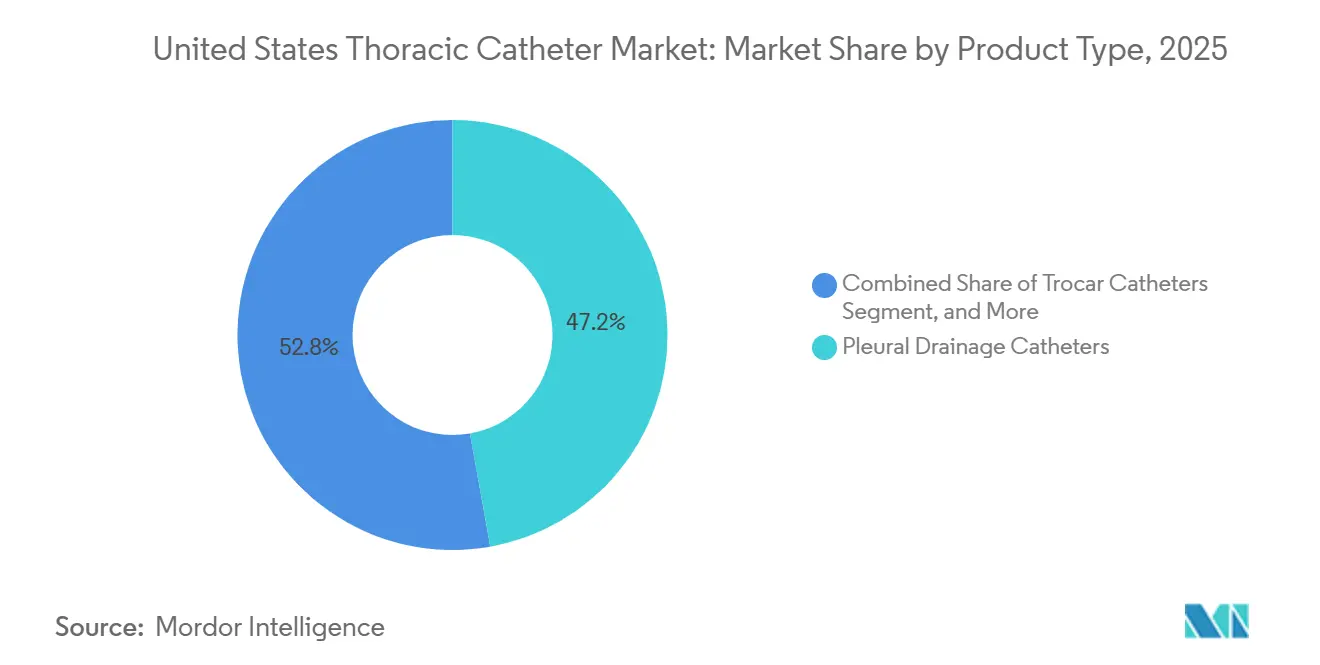

- By product type, pleural drainage catheters led with 47.23% share in 2025, while trocar catheters are projected to grow fastest at a 5.46% CAGR through 2031.

- By application, pleural effusion held 36.83% share in 2025, while pneumothorax is expected to expand fastest at a 5.27% CAGR through 2031.

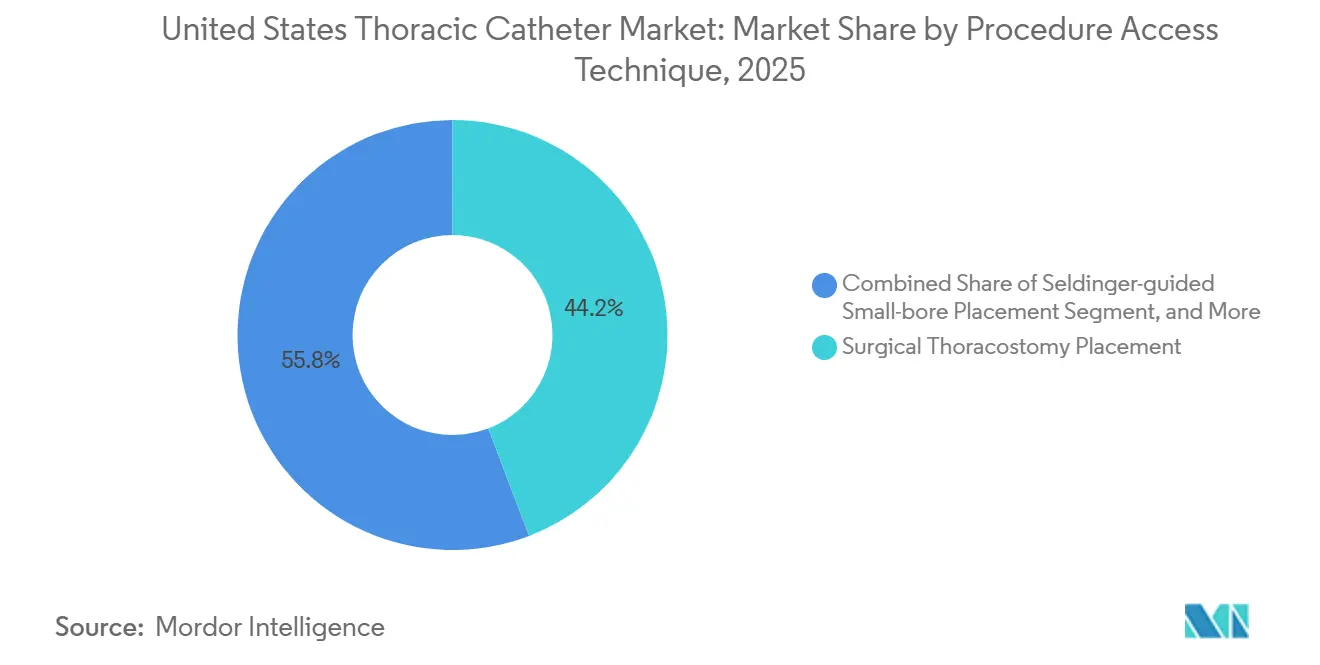

- By procedure or access technique, surgical thoracostomy retained 44.21% share in 2025, while Seldinger-guided placement is forecast to record the highest CAGR at 5.88% through 2031.

- By monitoring modality, conventional analog and water-seal systems accounted for 71.73% share in 2025, while digital drainage-compatible solutions are projected to advance fastest at a 6.65% CAGR through 2031.

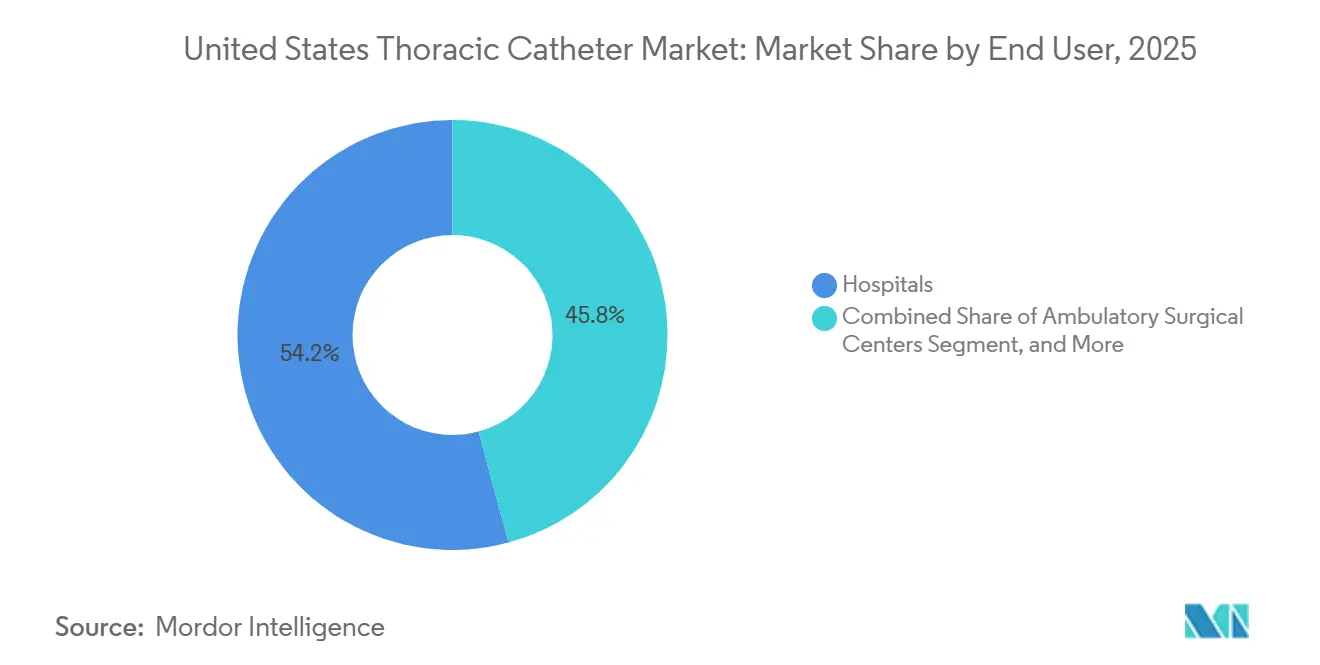

- By end user, hospitals captured 54.21% share in 2025, while ambulatory surgical centers are expected to post the highest CAGR at 6.09% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Thoracic Catheter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Malignant And Recurrent Pleural Effusion Burden | +1.2% | National, concentrated in Northeast and Southeast cancer care corridors | Short term (≤ 2 years) |

| Growth In Thoracic And Cardiothoracic Surgeries | +0.8% | National, strongest in academic medical center hubs in the Northeast, Midwest, and Texas | Medium term (2-4 years) |

| Shift Toward Minimally Invasive Small-Bore Drainage | +0.6% | National, strongest in academic centers and high-volume outpatient procedure settings | Medium term (2-4 years) |

| First-Line Guideline Acceptance Of Indwelling Pleural Catheters | +0.7% | National, with earlier uptake in interventional pulmonology clinics and cancer centers | Medium term (2-4 years) |

| ERAS-Led Adoption Of Digital Drainage Workflows | +0.5% | National, concentrated in thoracic surgery centers with advanced minimally invasive programs | Long term (≥ 4 years) |

| Expansion Of Outpatient And Home-Based Pleural Management | +0.4% | National, with spillover into rural homecare networks through telehealth support | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Malignant and Recurrent Pleural Effusion Burden

Pleural effusion demand remains central to the US thoracic catheter market because malignant pleural effusion continues to create a large and recurring treatment need. Around 150,000 patients receive a malignant pleural effusion diagnosis each year in the United States, which keeps demand high for both inpatient drainage and longer-term outpatient management approaches.[1]National Center for Biotechnology Information, “Understanding the Growing Burden of Malignant Pleural Effusion,” PMC, ncbi.nlm.nih.gov The case burden is also being reinforced by longer survival in cancer care, since patients are living longer with disease and therefore spend a longer period needing symptom control and repeat pleural management. Evidence from pleural care databases has also shown a rise in new malignant pleural effusion diagnoses over time, which supports the same direction of demand pressure described in the US thoracic catheter market. This longer care window increases catheter use per patient because repeat drainage episodes become more likely before pleurodesis or catheter removal can be achieved. As a result, recurrent effusion care is becoming one of the clearest volume drivers for tunneled pleural systems and related accessories in the US thoracic catheter market.

First-Line Guideline Acceptance of Indwelling Pleural Catheters

Guideline acceptance has become a direct growth lever for the US thoracic catheter market because indwelling pleural catheters are no longer treated only as a late fallback option. Guidance from the American Thoracic Society, the British Thoracic Society, and the European Respiratory Society now places indwelling pleural catheters alongside other frontline options for recurrent malignant pleural effusion management. In patients with non-expandable lung, the treatment preference is even clearer because guideline recommendations favor indwelling pleural catheters over talc pleurodesis in this setting. The current care gap also matters because only 24% of eligible United States patients receive guideline-consistent definitive management, which leaves a sizable conversion opportunity for programs that expand pleural intervention access. Clinical experience also supports the model, since one prospective cohort reported spontaneous pleurodesis in 44% of indwelling pleural catheter patients, with higher pleural fluid pH and protein associated with success.[2]General Thoracic and Cardiovascular Surgery, “Advantages of Applying Digital Chest Drainage System for Postoperative Management of Patients Following Pulmonary Resection,” Springer Nature, link.springer.com That combination of stronger guideline backing and underuse in practice gives the United States thoracic catheter market room to grow without depending entirely on new indications.

Growth in Thoracic and Cardiothoracic Surgeries

Thoracic and cardiothoracic surgery volumes continue to support the United States thoracic catheter market because chest drainage remains a routine requirement after lung resection, esophagectomy, and cardiac procedures. The growing use of video-assisted thoracoscopic surgery and robotic-assisted thoracic surgery is also changing the product mix, since minimally invasive procedures more often use smaller and fewer drainage tubes than open surgery cases. This shift supports demand for softer and smaller-bore products, especially in postoperative settings where pain control and early mobilization have become more important clinical goals. Enhanced Recovery After Surgery guidance for thoracic surgery recommends tube removal when daily serous output stays below 450 mL over 24 hours, which shortens management cycles and supports more standardized drainage decisions. A 2024 prospective study also found that a chest tube-focused ERAS program improved surgical recovery, reduced drainage duration, lowered postoperative pain, and shortened hospital stay after video-assisted thoracoscopic surgery.[3]BMC Cardiovascular Disorders, “Enhanced Recovery After Surgery Program Focusing on Chest Tube Management Improves Surgical Recovery After Video-Assisted Thoracoscopic Surgery,” BioMed Central, cardiothoracicsurgery.biomedcentral.com These changes support steady procedure-linked demand in the United States thoracic catheter market while also shifting demand toward products that fit faster recovery pathways.

ERAS-Led Adoption of Digital Drainage Workflows

Digital monitoring is becoming a stronger growth pocket inside the United States thoracic catheter market because thoracic programs want more consistent decisions on air leaks, fluid output, and tube removal timing. A meta-analysis of 12 randomized controlled trials covering 2,000 patients found that digital systems reduced chest tube duration and shortened hospital stay by 0.79 days compared with analog systems, without raising prolonged air leak or cardiopulmonary complication rates. This evidence has carried weight because the ERAS Society and the European Society of Thoracic Surgeons give digital drainage a strong recommendation in thoracic surgery care pathways. The growth rate also stands out, since digital drainage-compatible solutions are expanding 243 basis points faster than the overall market, which shows how quickly hospitals are rethinking monitoring choices. The change matters commercially because digital platforms often pull through proprietary disposables on a recurring basis, which protects margins better than a single commodity catheter sale. Over time, that pattern is likely to widen the gap between premium monitoring ecosystems and basic water-seal systems inside the United States thoracic catheter market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Catheter Blockage, Infection, And Dislodgement Risk | -0.5% | National, more visible in community hospitals with lower procedure volumes | Short term (≤ 2 years) |

| Budget Pressure And GPO-Led Commoditization | -0.6% | National, especially in GPO-heavy integrated systems in the Midwest and South | Medium term (2-4 years) |

| Polymer Qualification And Supply Revalidation Bottlenecks | -0.3% | National, concentrated among contract manufacturers and smaller device makers | Long term (≥ 4 years) |

| Training Variability In Placement And Drainage Protocols | -0.4% | National, stronger in rural community hospitals and non-academic settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budget Pressure and GPO-Led Commoditization

Budget pressure remains a real brake on the United States thoracic catheter market because hospitals continue to buy large volumes of standard drainage products through contracts that reward scale and low unit cost. This matters most for conventional thoracostomy tubes and basic drainage kits, where product differentiation is limited, and procurement teams focus heavily on price consistency across large systems. The effect is a split market where standard products face ongoing price compression, while digitally integrated systems and specialized indwelling pleural catheter platforms have a better chance of defending premium pricing if clinical value is clear. That gap slows adoption because hospital committees often want stronger operational and clinical justification before they add new systems to approved purchasing lists. It also changes supplier behavior, since manufacturers are pushed to package products into procedure-specific kits and monitoring platforms rather than compete only on the base catheter itself. The result is that the United States thoracic catheter market keeps growing, but innovation reaches price-sensitive providers more slowly than it reaches advanced thoracic centers.

Catheter Blockage, Infection, and Dislodgement Risk

Complications continue to limit confidence in parts of the United States thoracic catheter market, especially outside specialized pleural intervention programs. A prospective study reported blockage in 16% of indwelling pleural catheter patients, pleural infection in 9%, and loculation in 9%, with no significant difference between malignant and non-malignant effusion cohorts. These events matter because they can lead to extra interventions, added discomfort, and greater caution in lower-volume centers that do not manage pleural disease as frequently. The burden is especially important in malignant cases, where patients often have limited physiologic reserve and repeated procedures can be harder to tolerate. As a result, many community physicians still apply more conservative patient selection than guidelines would support, which narrows the use of indwelling systems in routine practice. Until complication control improves more consistently across care settings, this issue will continue to slow broader premium adoption in the United States thoracic catheter market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pleural Drainage Catheters Hold Dominance; Trocars Accelerating

Pleural drainage catheters held 47.23% of the US thoracic catheter market size in 2025, which made them the largest product group in the product mix. This leadership reflects their role across both recurrent oncologic effusion management and short-duration drainage in urgent and planned hospital care. Tunneled indwelling pleural catheters continue to gain procedural weight as clinical guidance becomes more supportive and outpatient care pathways become more common. Non-tunneled pigtail catheters still hold an important high-volume role because they are widely used for diagnostic drainage, temporary pleural decompression, and selected pneumothorax cases. In the US thoracic catheter industry, this combination gives pleural drainage catheters both a broad volume base and a strong link to premiumization.

Thoracostomy tubes remain important in trauma, empyema, and postoperative care, but the direction of change is becoming clearer as smaller-bore options gain support in indications where pain reduction and mobility matter. The United States thoracic catheter market is seeing gradual substitution in selected settings because smaller catheters can deliver acceptable outcomes while reducing discomfort and simplifying removal after use. Trocar catheters are the fastest-growing product type, with a 5.46% CAGR through 2031, supported by emergency use cases where placement speed remains a practical advantage. Bundled procedure kits also matter in this segment because they reduce stock complexity for hospitals and help suppliers defend contract positions through convenience as well as price. Product development still moves carefully, since material changes such as movement from PVC to polyurethane or silicone can trigger new qualification work that slows mid-tier innovation cycles under device compliance standards.

By Application: Pleural Effusion Anchors Volume; Pneumothorax Outpaces the Field

Pleural effusion accounted for 36.83% of the US thoracic catheter market size in 2025, which kept it as the largest application category in the country. The size of this segment is tied closely to malignant pleural effusion volume, and that burden remains high with around 150,000 diagnoses each year in the United States. Within pleural effusion care, malignant and non-malignant cases follow different purchasing logic because malignant disease leans more heavily toward indwelling systems and home drainage accessories, while non-malignant fluid often still involves repeat aspiration or shorter-term catheter use. This makes application growth in the US thoracic catheter market more uneven than the headline number suggests, since some sub-indications support premium systems while others continue to favor standard products. The approval history of major tunneled systems has also widened addressable use over time by extending relevance beyond oncology into selected recurrent non-malignant effusion settings.

Pneumothorax is the fastest-growing application segment with a 5.27% CAGR through 2031, and guideline changes are a major reason for that faster rise. The 2024 joint guidance from the European Respiratory Society, the European Association for Cardio-Thoracic Surgery, and the European Society of Thoracic Surgeons supports less invasive approaches for initial primary spontaneous pneumothorax management and conditionally supports ambulatory care in suitable patients PUBMED. That shift is important because it favors small-bore catheter use over older large-bore insertion patterns in part of the treatment pathway. Hemothorax and postoperative drainage still provide a dependable base of demand because they are tied more to trauma and surgical procedure volume than to epidemiology. Empyema remains smaller in value terms, but it keeps large-bore drainage relevant in the US thoracic catheter market because infected or complex pleural collections often require a more aggressive management approach.

By Procedure / Access Technique: Surgical Thoracostomy Leads; Seldinger Technique Gains Ground

Surgical thoracostomy held 44.21% of the US thoracic catheter market share in 2025, which reflects its continued importance in trauma care and postoperative surgical settings. Direct placement remains hard to replace in cases where speed, visibility, and secure positioning matter more than patient comfort alone. This helps explain why the technique still leads despite growing clinical preference for smaller catheters in selected non-trauma indications. Its current role is also reinforced by hospital structure, since large trauma centers and cardiac surgery programs continue to rely on established thoracostomy practice as a routine competency. For the US thoracic catheter market, this keeps a strong base of demand tied to large-bore systems and traditional placement workflows.

Seldinger-guided placement is the fastest-growing access approach, with a 5.88% CAGR through 2031, because evidence increasingly supports small-bore catheter performance across pneumothorax, free-flowing effusion, and selected postoperative drainage settings. Smaller tubes also fit ERAS goals more closely because they are easier to manage at the bedside, they create less pain, and they support earlier ambulation after intervention. Tunneled indwelling placement is also building momentum as oncology and interventional pulmonology programs expand, which gives the US thoracic catheter industry a second growth path in access technique trends. Trocar-assisted placement keeps a defined role where fast decompression is the priority, and procedural simplicity can outweigh the control benefits of Seldinger placement. The access mix is therefore shifting, but it is not collapsing into a single method because each technique still serves a distinct clinical setting.

By Monitoring Modality: Analog Predominance Eroding Under Digital Pressure

Conventional analog and water-seal systems captured 71.73% of the US thoracic catheter market size in 2025, which shows how large the installed base of traditional drainage still is. Their lead reflects long clinical familiarity, straightforward workflow, and a low unit cost that fits hospital purchasing rules for routine drainage products. Even so, the size of that installed base should not be mistaken for strategic strength because replacement decisions are now happening under a stronger evidence base for digital systems. The US thoracic catheter market is clearly shifting here because the digital segment is expanding much faster than the overall category. Meta-analysis evidence continues to support the direction of travel, with digital systems linked to shorter chest tube duration and lower length of stay after pulmonary resection.

Digital drainage-compatible solutions are the fastest-growing access approach, with a 6.65% CAGR through 2031. The NICE review of Medela Thopaz+ also showed that digital drainage can improve decision-making and reduce unnecessary inpatient time, which helped strengthen hospital confidence in objective monitoring models. This shift has broader commercial meaning because digital platforms can lock hospitals into proprietary disposables, which changes revenue quality for manufacturers. The ERAS Society and the European Society of Thoracic Surgeons also give digital drainage a strong recommendation, so thoracic programs have a clinical governance reason to move beyond analog systems. That matters in procurement because the decision is no longer framed only around equipment cost, but also around workflow consistency, discharge timing, and postoperative recovery targets. Over the forecast period, monitoring choice is likely to be one of the clearest areas where the US thoracic catheter market separates into commodity and premium tiers.

By End User: Hospitals Dominant; ASCs Redefine the Growth Horizon

Hospitals held 54.21% of the United States thoracic catheter market share in 2025, and that lead reflects the concentration of trauma care, cardiothoracic surgery, thoracic oncology, and interventional pulmonology inside acute care networks. Large hospitals are also where many advanced drainage decisions are made first, since academic and high-volume centers often adopt new monitoring systems and indwelling catheter pathways before smaller facilities do. This gives hospitals a dual role as both the largest buyer group and the main site where new clinical evidence is translated into purchasing behavior. In the US thoracic catheter market, hospital demand therefore remains essential for both baseline volume and premium product adoption. Their central role also explains why supplier training programs, enterprise contracts, and procedure standardization efforts remain heavily focused on hospital-based teams.

Ambulatory surgical centers are the fastest-growing end-user group, with a 6.09% CAGR through 2031, which shows that a larger share of thoracic and pulmonary procedures is moving into lower-acuity settings. The shift matters because outpatient care pathways favor simpler setups, faster turnover, and devices that support discharge without extensive inpatient monitoring. Specialty clinics also remain important because they align well with indwelling pleural catheter placement, follow-up drainage, and palliative management for recurrent malignant effusion. Homecare is still smaller, but it is strategically meaningful because tunneled systems allow scheduled or symptom-led drainage outside the hospital, which reduces facility dependence for selected patients. As payer pressure on avoidable admissions continues, end-user mix should keep evolving in a way that supports outpatient and home-based models across the United States thoracic catheter market.

Geography Analysis

The United States thoracic catheter market is a single-country market in formal reporting terms, but regional demand patterns still shape adoption speed, product mix, and supplier strategy across the country. The Northeast remains one of the strongest demand corridors because it combines dense academic hospital networks, major cancer centers, and established interventional pulmonology programs. These care settings are well-positioned to use tunneled pleural systems in recurrent malignant effusion and to adopt digital drainage workflows in thoracic surgery pathways. Large integrated delivery networks in this region also increase procurement leverage, which places price pressure on standard products while still allowing premium systems to gain ground if they show system-wide value. This makes the Northeast important not only for unit demand, but also for early commercial validation of higher-end platforms inside the United States thoracic catheter market.

The Sun Belt also carries strong strategic importance because older population migration and cancer burden support higher pleural intervention demand over time. In these states, the US thoracic catheter market benefits from the rising need for recurrent effusion management, while outpatient procedure expansion supports faster uptake of products suited to ambulatory care. Adoption patterns are not uniform, however, because academic centers still move earlier than community hospitals in deploying indwelling pleural catheter programs and digital monitoring pathways. That lag creates a catch-up opportunity for suppliers that can combine physician education, protocol support, and straightforward placement systems. As more pleural care shifts outside long inpatient stays, this region is likely to remain a meaningful contributor to future demand mix change.

The Midwest and Mountain West show a different profile because trauma networks and cardiac surgery programs keep large-bore drainage and traditional thoracostomy demand relatively firm. This part of the United States thoracic catheter market is therefore influenced less by cancer-center concentration alone and more by the operating needs of trauma, thoracic surgery, and postoperative cardiac care. ERAS-related changes still matter here, especially in cardiac and thoracic programs that are looking for better chest tube patency, shorter drainage duration, and more consistent recovery protocols. Rural care delivery also creates a practical barrier for home-based pleural management because nursing access and subspecialty support can be thinner across wide geographies. That makes remote-friendly and easy-to-manage systems especially relevant, even if adoption moves more gradually than in dense academic corridors. Across all regions, the US thoracic catheter market remains nationally unified in reporting but clearly differentiated in how quickly providers move toward premium and digitally connected drainage models.

Competitive Landscape

The United States thoracic catheter market shows moderate-to-high concentration at the top, with Becton, Dickinson and Company, Teleflex, and Getinge AB holding strong positions through established product families, hospital relationships, and training support. These suppliers benefit from broad access to large health systems, which makes switching harder for providers that prefer familiar clinical protocols and stable supply arrangements. Their advantage is not based only on catheter design, but also on bundled drainage systems, procedure support, and institutional familiarity across high-volume settings. This keeps the top tier durable even as the US thoracic catheter market becomes more segmented between conventional and premium categories. At the same time, the presence of several active specialists means the field is not closed, especially in areas tied to tunneled drainage, digital monitoring, or procedure-specific kits.

Competitive strategy is increasingly separating into 3 tracks. One track focuses on defending commodity and conventional drainage volume through contract strength and broad distribution. A second track centers on digital drainage systems that promise clearer air leak measurement, faster mobilization, and shorter postoperative stays, which gives suppliers a stronger value case in thoracic surgery. A third track targets recurrent pleural effusion management, where tunneled catheter systems benefit from stronger guideline support and a growing preference for outpatient symptom control.

Recent company moves also show how suppliers are trying to strengthen their position around adjacent catheter and drainage opportunities. Vygon SA acquired Stiletto and its SlipStream™ technology in February 2026, which shows interest in deepening its United States catheter presence through device expansion. Cook Medical and Purdue University announced a 5-year research and collaboration agreement in May 2025, which supports future catheter and image-guided device development that could influence smaller-bore access pathways. Getinge also updated instructions for use across its Oasis, Ocean, and Express thoracic drains in the United States in April 2024 after a device correction, which reflects continued product stewardship in a highly regulated space. Newer entrants are also trying to open white space, including Pleural Dynamics, which entered active US clinical study for a fully implantable pleural device in 2024. The result is a US thoracic catheter market where scale still matters, but future share gains are likely to come from differentiated workflow fit rather than commodity volume alone.

United States Thoracic Catheter Industry Leaders

AngioDynamics, Inc.

B. Braun Melsungen AG

Cardinal Health, Inc.

Cook Medical

Getinge AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cook Medical and Purdue University announced a 5-year Master Sponsored Research and Collaboration Agreement (MSRCA) targeting advanced medical device manufacturing and image-guided procedures; the partnership strengthens Cook's pipeline for small-bore catheter design innovations relevant to Seldinger-guided placement techniques.

- February 2026: Vygon SA acquired Stilett, a next-generation extended-dwell catheter integrating SlipStream technology, from Avia Vascular (Salt Lake City, UT), signaling Vygon's intent to accelerate United States market penetration in the extended-dwell catheter segment, including thoracic drainage applications.

United States Thoracic Catheter Market Report Scope

The Thoracic Catheter Market comprises the commercial manufacturing, distribution, and sales of flexible medical tubes (chest tubes) used in thoracostomy and thoracic surgery. These devices are essential for draining abnormal accumulations of air, fluid, blood, or pus from the pleural cavity or mediastinum to restore normal breathing and lung function.

The United States Thoracic Catheter Market Report is segmented across several dimensions that define its scope and structure. By product type, it includes thoracostomy tubes, pleural drainage catheters, trocar catheters, and procedure kits. By application, the market covers pleural effusion, pneumothorax, hemothorax, postoperative drainage, and empyema. In terms of procedure/access technique, segmentation includes the Seldinger technique, surgical approach, trocar method, and tunneled procedures. By monitoring modality, products are categorized into conventional analog systems and digital drainage systems. Finally, by end user, the market encompasses hospitals, ambulatory surgical centers (ASCs), specialty clinics, and homecare settings. Market forecasts are provided in terms of value (USD), reflecting the financial scale and growth potential of these segments within the United States thoracic catheter industry.

| Thoracostomy Tubes | |

| Pleural Drainage Catheters | Tunneled Indwelling Pleural Catheters |

| Non-tunneled Pigtail Pleural Catheters | |

| Trocar Catheters | |

| Thoracostomy Procedure Kits and Trays |

| Pleural Effusion | Malignant Pleural Effusion |

| Non-malignant Pleural Effusion | |

| Pneumothorax | Spontaneous Pneumothorax |

| Iatrogenic Pneumothorax | |

| Traumatic Pneumothorax | |

| Hemothorax | |

| Postoperative Chest Drainage | Thoracic Surgery |

| Cardiac Surgery | |

| Empyema and Complicated Pleural Infection |

| Seldinger-guided Small-bore Placement |

| Surgical Thoracostomy Placement |

| Trocar-assisted Placement |

| Tunneled Indwelling Placement |

| Conventional Analog and Water-seal Drainage |

| Digital Drainage-compatible Solutions |

| Hospitals | Academic Medical Centers |

| Community Hospitals | |

| Trauma Centers | |

| Ambulatory Surgical Centers | |

| Specialty Clinics | Interventional Pulmonology Clinics |

| Oncology and Palliative Care Clinics | |

| Homecare Settings |

| By Product Type | Thoracostomy Tubes | |

| Pleural Drainage Catheters | Tunneled Indwelling Pleural Catheters | |

| Non-tunneled Pigtail Pleural Catheters | ||

| Trocar Catheters | ||

| Thoracostomy Procedure Kits and Trays | ||

| By Application | Pleural Effusion | Malignant Pleural Effusion |

| Non-malignant Pleural Effusion | ||

| Pneumothorax | Spontaneous Pneumothorax | |

| Iatrogenic Pneumothorax | ||

| Traumatic Pneumothorax | ||

| Hemothorax | ||

| Postoperative Chest Drainage | Thoracic Surgery | |

| Cardiac Surgery | ||

| Empyema and Complicated Pleural Infection | ||

| By Procedure / Access Technique | Seldinger-guided Small-bore Placement | |

| Surgical Thoracostomy Placement | ||

| Trocar-assisted Placement | ||

| Tunneled Indwelling Placement | ||

| By Monitoring Modality | Conventional Analog and Water-seal Drainage | |

| Digital Drainage-compatible Solutions | ||

| By End User | Hospitals | Academic Medical Centers |

| Community Hospitals | ||

| Trauma Centers | ||

| Ambulatory Surgical Centers | ||

| Specialty Clinics | Interventional Pulmonology Clinics | |

| Oncology and Palliative Care Clinics | ||

| Homecare Settings | ||

Key Questions Answered in the Report

What is the current value of the United States thoracic catheter market?

The United States thoracic catheter market reaches USD 159.87 million in 2026 and is projected to rise to USD 196.46 million by 2031 at a 4.22% CAGR.

Which application leads thoracic catheter demand in the United States?

Pleural effusion is the largest application, with a 36.83% share in 2025, supported by the large malignant pleural effusion burden in the country.

Which product type is growing fastest in the United States thoracic catheter space?

Trocar catheters are the fastest-growing product category, with a projected 5.46% CAGR through 2031.

Why are digital drainage systems gaining traction in thoracic care?

Digital drainage-compatible solutions are projected to grow at a 6.65% CAGR, supported by evidence showing shorter chest tube duration and shorter hospital stay versus analog systems.

Which end users account for most thoracic catheter demand in the United States?

Hospitals remain the largest end-user group with a 54.21% share in 2025 because they concentrate trauma, thoracic surgery, and interventional pulmonology procedures.

Page last updated on: