Thoracic Surgery Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

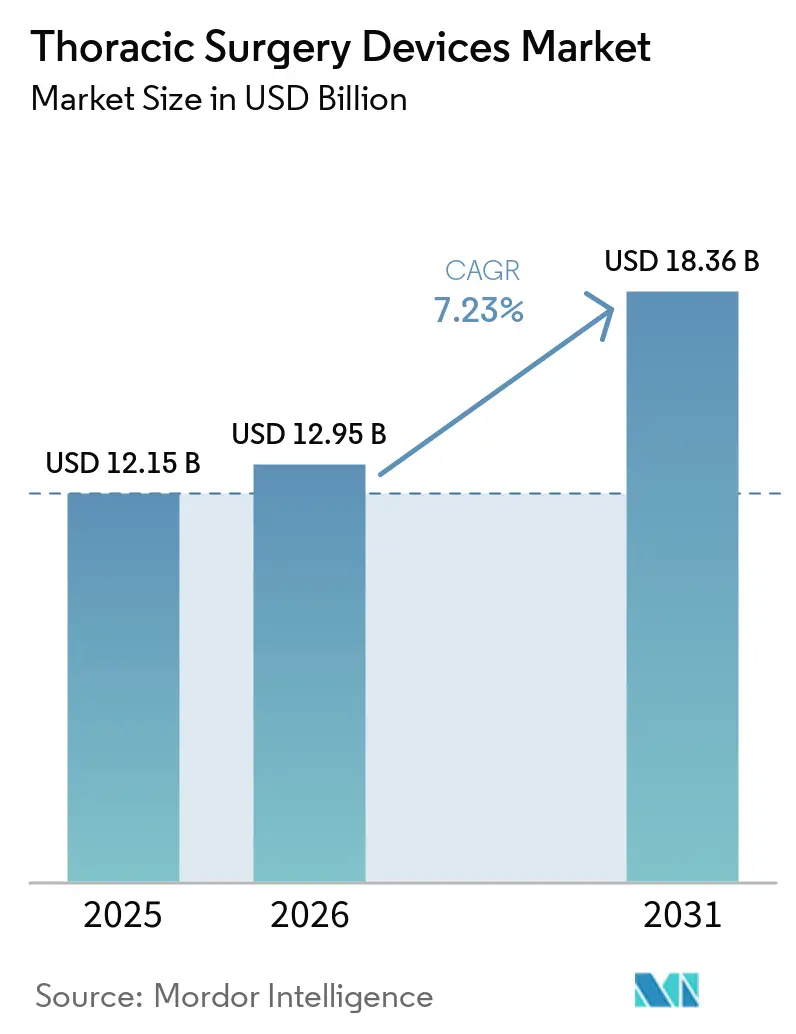

| Market Size (2026) | USD 12.95 Billion |

| Market Size (2031) | USD 18.36 Billion |

| Growth Rate (2026 - 2031) | 7.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thoracic Surgery Devices Market Analysis by Mordor Intelligence

The Thoracic Surgery Devices Market size is projected to be USD 12.15 billion in 2025, USD 12.95 billion in 2026, and reach USD 18.36 billion by 2031, growing at a CAGR of 7.23% from 2026 to 2031.

The thoracic surgery device market is moving away from episodic open procedures and toward technology-enabled and pathway-driven surgery, with lung cancer still supporting the largest procedural base. Robotic platform adoption, artificial intelligence integration, and the movement of selected procedures from inpatient wards to ambulatory and specialty settings are shaping the next phase of the thoracic surgery device market. The thoracic surgery device market is also showing a stronger bundled-services structure, as robotic system makers, imaging specialists, and stapling device suppliers increasingly tie hospitals into recurring instrument, software, and service relationships after the original capital purchase. Competitive conditions remain moderate to high, with large platform vendors defending installed bases while procurement teams gain leverage as more robotic systems approach regulatory clearance. Concentration risk still matters because robotic thoracic procedure growth remains centered in academic medical centers, reimbursement remains uneven across countries, and supply dependence on imaging sensors and actuator components from Taiwan and South Korea leaves the thoracic surgery device market exposed to tariff and component disruptions.

Key Report Takeaways

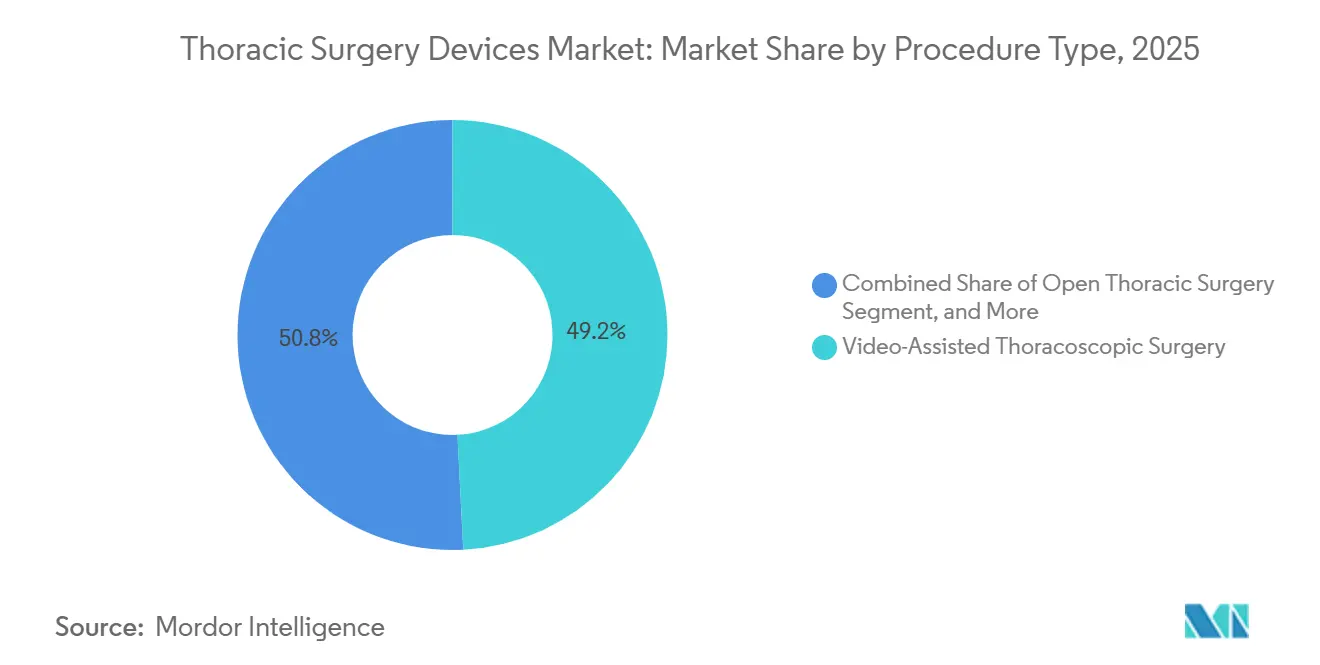

- By procedure type, video-assisted thoracoscopic surgery led with 49.21% share in 2025, while robotic-assisted thoracic surgery is projected to expand at 8.23% CAGR through 2031.

- By product type, robotic platforms held 31.83% share in 2025, while endoscopes and imaging systems are forecast to grow at 7.28% CAGR through 2031.

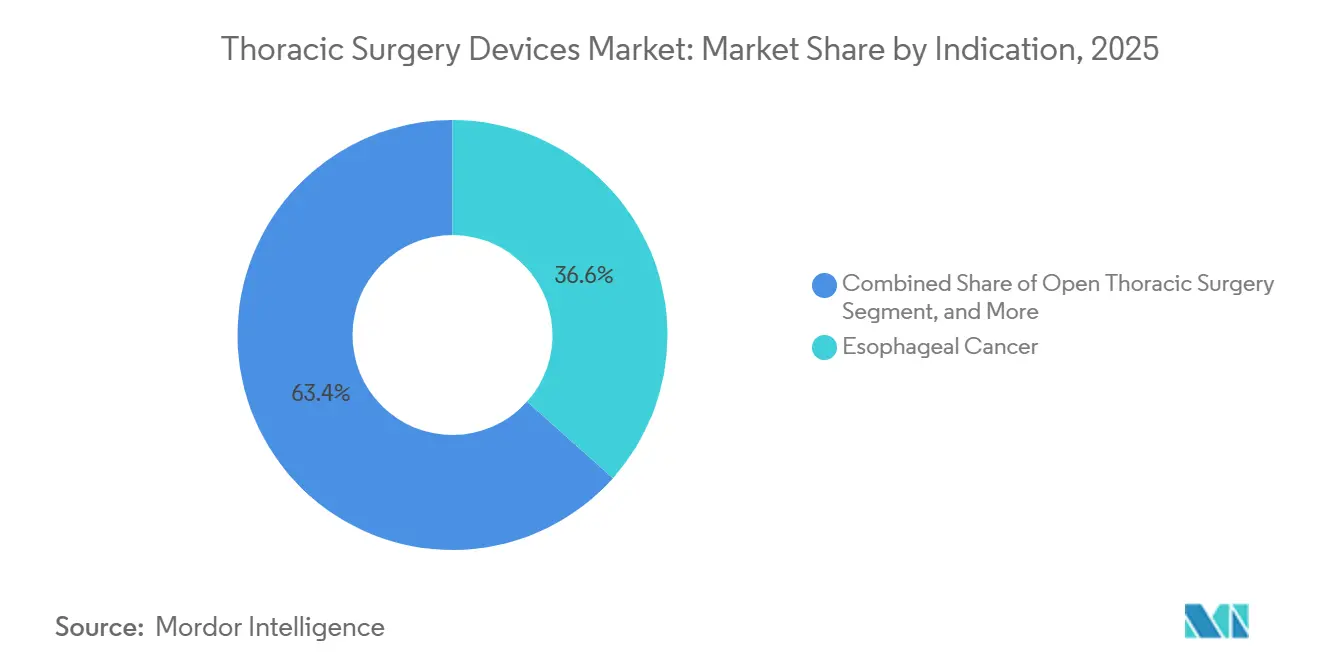

- By indication, esophageal cancer accounted for 36.64% share in 2025, while mediastinal tumors are projected to record the highest CAGR at 8.85% through 2031.

- By end user, hospitals captured 45.23% share in 2025, while specialty thoracic centers are expected to expand at 7.95% CAGR through 2031.

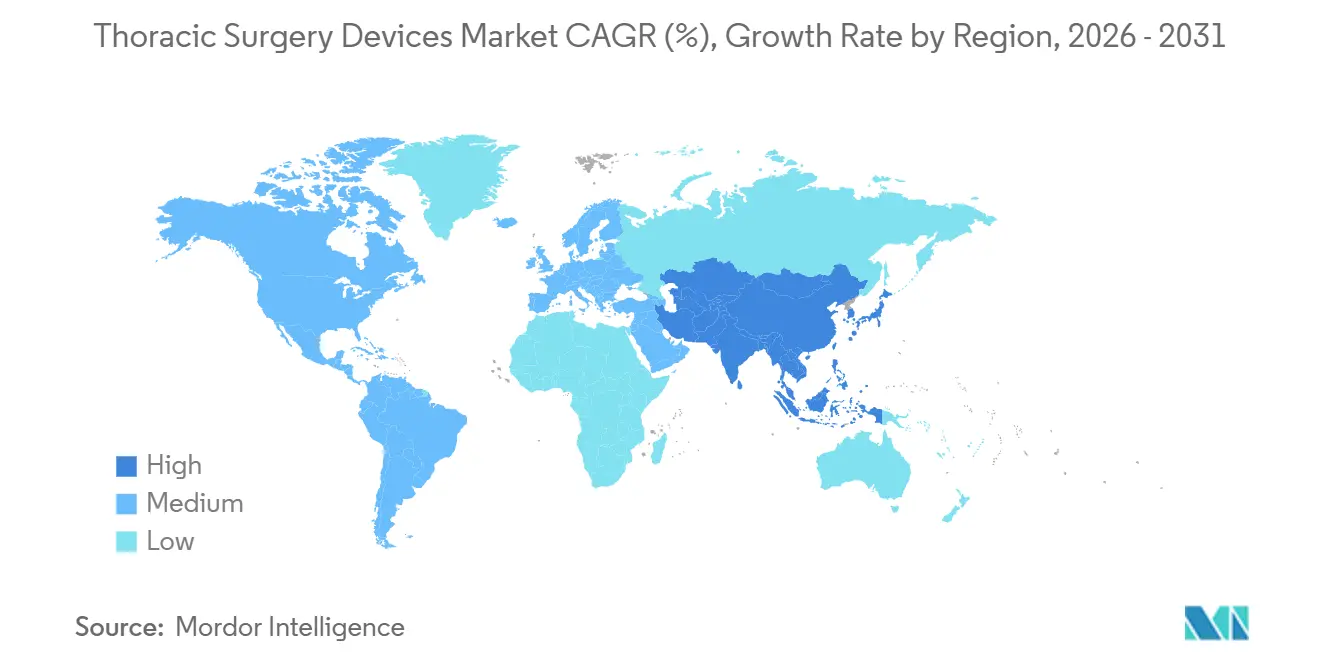

- By geography, North America held 38.23% share in 2025, while Asia-Pacific is forecast to advance at 8.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thoracic Surgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Lung Cancer Screening and Earlier Surgical Referral | +1.5% | Global, with highest intensity in North America and Western Europe | Short term (≤ 2 years) |

| Increasing ERAS Adoption and Same-Day Recovery Pathways | +0.7% | North America, Europe, APAC core | Medium term (2-4 years) |

| AI-Guided Imaging and Workflow Integration | +0.9% | North America, EU, East Asia | Medium term (2-4 years) |

| Reimbursement Expansion for Robotic Thoracic Surgery | +1.0% | China, Japan, Germany, Australia, with spillover to Southeast Asia | Medium term (2-4 years) |

| Subscription-Based Robotic Service Bundling | +0.6% | Global, with early gains in the US, UK, and Scandinavia | Long term (≥ 4 years) |

| Aging Population and Complex Comorbidity Burden | +1.2% | Japan, South Korea, Italy, Germany, with spillover to MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Lung Cancer Screening and Earlier Surgical Referral

Expanded lung cancer screening programs are producing more early-stage diagnoses, and that directly raises the number of patients who move into surgical pathways in the thoracic surgery device market. At OSF HealthCare, an AI-assisted multistep screening program increased the institutional screening rate from 18.2% in 2020 to 42.8% by 2025, while stage I diagnoses rose from 30.9% to 44.6% over the same period.[1]ASCO AI in Oncology, “AI-Assisted Multistep Lung Cancer Screening Program Boosts Uptake Beyond National Averages,” ASCO AI in Oncology, ascoai.org The UK NHS Lung Cancer Screening Programme reported 7,193 lung cancers diagnosed through screening by March 2025, and 63.1% of those cases were stage 1, which shows how screening can shift case mix toward earlier surgical intervention. Earlier detection also expands the volume of staging procedures, image-guided bronchoscopy, and navigational bronchoscopy, so the commercial benefit in the thoracic surgery device market extends beyond formal resection alone. That broader procedural funnel supports demand for endoscopy systems, imaging tools, and access devices as hospitals manage more nodules and more early lesions through organized thoracic pathways.

Increasing ERAS Adoption and Same-Day Recovery Pathways

Enhanced recovery pathways are helping the thoracic surgery device market move selected procedures into ambulatory and same-day discharge settings. A systematic review and meta-analysis in JTCVS Open found that Enhanced Recovery After Thoracic Surgery protocols reduced hospital length of stay by 3 days and lowered overall postoperative complications across 19 studies and 8,447 patients. A bibliometric study covering 617 publications from 2015 to 2024 across 44 countries showed that thoracic ERAS research now exceeds 100 papers annually, with China contributing 214 publications and the United States 155, which points to ongoing protocol refinement rather than isolated adoption.[2]Z. Chen et al., “Trends in Enhanced Recovery After Surgery (ERAS) in Thoracic Surgery from a Bibliometric Insight,” Hereditas, springer.com A 2024 real-world study on VATS day surgery for pulmonary nodule resection showed that prehabilitation, small-diameter drainage tubes, and multimodal pain management enabled faster discharge than standard care. As more centers standardize these pathways, the thoracic surgery device market gains additional volume in lower-cost settings without requiring every case to remain inside traditional inpatient referral channels. This shift also favors platforms and instruments that shorten recovery and simplify postoperative management.

AI-Guided Imaging and Workflow Integration

Artificial intelligence is becoming part of operative planning and intraoperative support, and that is changing how the thoracic surgery device market improves consistency across centers. A multicenter randomized controlled trial in Nature Communications validated the InferOperate Thorax AI-3D system for lung resection planning, showing automated bronchial and vascular segmentation within 2 to 3 minutes and better margin accuracy during segmentectomy.[3]L. Xu et al., “Artificial Intelligence Driven 3D Reconstruction for Enhanced Lung Surgery Planning,” Nature Communications, nature.com Clinical literature also shows that computer vision tools are being deployed in cardiothoracic settings to support workflow segmentation, instrument tracking, and surgeon performance assessment from operative video feeds. That matters because the thoracic surgery device market has long been shaped by performance gaps between high-volume academic programs and smaller hospitals. AI-guided imaging and workflow tools can narrow that gap by making planning, visualization, and technique more repeatable. This makes it more commercially rational for device suppliers to push robotic and advanced imaging systems deeper into community hospitals and mid-tier programs.

Aging Population and Complex Comorbidity Burden

Demographic aging is increasing not only the number of thoracic cases, but also the complexity of each case, which supports more technology-intensive care in the thoracic surgery device market. South Korea’s national lung cancer surgery registry showed that the share of patients aged 70 to 79 rose from 26.3% to 32.3% between 2010 and 2023, while patients aged 80 and older rose from 2.0% to 6.2%, and the share of patients with a Charlson Comorbidity Index of 7 or higher increased from 9.0% to 17.4%. A 2025 observational study in the United Kingdom found that 63.1% of older operative patients lived with multimorbidity, and thoracic surgery carried the heaviest comorbidity burden among elective specialties. A separate 2025 multicenter study reported that robotic-assisted thoracic surgery was safe and technically feasible in very elderly patients, with zero conversions to open surgery in the study population. These patterns support a thoracic surgery device market where age alone matters less than functional suitability, and where precision, visualization, and ergonomic control become more valuable as patient complexity rises. That keeps demand pointed toward minimally invasive and robotic approaches in high-risk case groups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steep Surgeon Learning Curve for Advanced Thoracic Platforms | -0.9% | Global, most acute in emerging APAC markets and community hospitals | Short term (≤ 2 years) |

| High Capital Expenditure and Case-Volume Threshold Risk | -0.8% | Global, most pronounced in South America, MEA, and Tier 2 Asian cities | Medium term (2-4 years) |

| Regulatory Evidence Burden for New Robotic and Energy Devices | -0.5% | North America, EU | Medium term (2-4 years) |

| Supply Chain Exposure to Specialized Components and Tariff Pressure | -0.5% | US, EU, with spillover to APAC-based manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Steep Surgeon Learning Curve for Advanced Thoracic Platforms

The thoracic surgery device market still faces an adoption ceiling because robotic proficiency takes much longer to build than conventional VATS capability. A nationwide population-based study across 28 Korean hospitals found a median learning curve threshold of 110 procedures, and only 8 of the 28 hospitals reached that level during the 2019 to 2022 study period. A Norwegian single-center study of 200 robotic pulmonary lobectomies found a bi-phasic learning curve, with operative time still improving after the 117th procedure and complication rates stabilizing only around the 94th case. This creates an economic trap inside the thoracic surgery device market because hospitals often commit capital before surgeons reach the efficiency needed to justify the program. The problem is sharper in Tier 2 hospitals and emerging markets where proctoring systems, fellowship pipelines, and structured robotic training are less developed. Until those support systems widen, robotic diffusion in the thoracic surgery device market will remain uneven across hospital tiers.

High Capital Expenditure and Case-Volume Threshold Risk

High capital cost remains a major restraint in the thoracic surgery device market, especially where budgets are limited and annual case counts are modest. Flexible acquisition approaches such as 24-month rental programs and operating leases are designed to lower the initial barrier, but they do not remove the need for sustained procedural volume to support recurring instrument and service expenses. Hospitals with fewer than 100 thoracic cases annually still face a meaningful risk that per-procedure economics will compare poorly with established VATS pathways. That slows penetration into community hospitals, even though these centers represent the largest under-served patient base in the thoracic surgery device market. The restraint is strongest in South America, the Middle East and Africa, and Tier 2 Asian cities, where budget discipline and case concentration make platform utilization harder to optimize. As a result, adoption in the thoracic surgery device market continues to cluster around high-volume centers that can spread fixed cost across more cases and clear learning curves faster.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Minimally Invasive Access Dominates, Robotics Reshapes the Ceiling

Video-assisted thoracoscopic surgery held 49.21% of the thoracic surgery device market share in 2025, making it the largest procedure segment in the thoracic surgery device market. Its position reflects long-term clinical evidence, established training pathways, and reliable oncologic outcomes in lung resection. Penetration has already become deep in major academic centers across North America and Europe, but expansion continues in community hospitals through narrower trocars, 4K visualization, and low-pressure insufflation. Robotic-Assisted Thoracic Surgery is projected to grow at 8.23% CAGR through 2031, supported by articulated instruments, tremor filtration, and 3D optics that improve access in mediastinal and subcarinal lymph node territories.

A 2026 multicenter cohort study reported that robotic lobectomy delivered lower conversion-to-open rates and shorter postoperative stays than VATS, which strengthens the case for robotic use in higher-complexity procedures. Open Thoracic Surgery still retains a meaningful place in the thoracic surgery device market for re-operative cases, vascular invasion, and trauma, where minimally invasive access remains limited. Endoscopic Thoracic Surgery remains smaller, but it is growing as navigational bronchoscopy expands biopsy and focal ablation options for peripheral lesions that might otherwise move to resection. In Japan, reimbursement inclusion of robotic lobectomy in 2018 and segmentectomy in 2020 helped robotic thoracic surgery move from less than 1% of lung cancer procedures to more than 15% by 2025, which suggests the regional ceiling for VATS may be lower in Asia-Pacific than current shares indicate. That sequencing matters because the thoracic surgery device market often follows reimbursement expansion before broader platform adoption takes hold.

By Product Type: Robotic Platforms Anchor Share, Imaging Segments Drive Growth

Robotic platforms held 31.83% of product type revenue in 2025, which made them the largest product segment in the thoracic surgery device market. The segment reflects the installed base effect and the premium value attached to core hardware, supporting instruments, and related software. Endoscopes and imaging systems are projected to grow at 7.28% CAGR through 2031, which makes them the fastest-moving product category in the thoracic surgery device market. Growth comes from 4K fluorescence-guided visualization, indocyanine green perfusion imaging for segmental plane mapping, and AI-enhanced overlay tools that now appear in both standalone systems and robotic towers.

Surgical instruments and accessories rise with every expansion in the robotic installed base because replacement and disposable use recur with each procedure. Energy and Stapling Devices face more pressure in standard configurations, but specialized thick-tissue reloads for hilar anatomy and dense esophageal tissue still support premium positioning. The thoracic surgery industry also shows a gradual shift toward ultrasonic energy platforms for selected lobectomy and segmentectomy steps that were once reserved for mechanical staplers. The segment mix, therefore, favors vendors that can pair core capital equipment with repeat-use accessories and imaging upgrades. That pattern keeps the thoracic surgery device market tilted toward vendors with broad portfolios, strong service coverage, and integration across visualization, access, and robotic workflows.

By Indication: Esophageal Cancer Leads in Share, Mediastinal Tumors Gain Ground

Esophageal cancer held 36.64% share in 2025, which kept it as the largest indication segment in the thoracic surgery device market. Its leading position reflects the complexity and high instrument intensity of esophagectomy, which often combines thoracoscopic and laparoscopic access and requires multiple dedicated stapler reloads. Lung Cancer still generates the highest absolute procedure volume in the thoracic surgery device market because disease incidence remains high, but the revenue share per case is moderated by shorter operating room time and lower instrument intensity in wedge resections than in lobectomy. A phase 3 randomized trial published in The Lancet Gastroenterology & Hepatology in 2025 found thoracoscopic oesophagectomy to be non-inferior to open surgery for overall survival in resectable thoracic oesophageal cancer, which supports continued protocol migration toward minimally invasive esophagectomy.

Mediastinal Tumors are projected to grow at 8.85% CAGR through 2031, making them the fastest-growing indication in the thoracic surgery device market. That pace is linked to the shift of thymectomy and anterior mediastinal tumor resection from median sternotomy to robotic and subxiphoid minimally invasive access. The confined mediastinal space favors robotic articulation and flexible movement, which improves control in technically difficult dissections. Clinical evidence published in 2025 showed that robotic-assisted thoracic surgery was safe and technically feasible for thymomas up to 9.5 to 10 cm, which expands the historical size threshold for minimally invasive intervention. Pneumothorax and Hyperhidrosis remain smaller but stable niches, and both rely mainly on mature VATS-based pleural and sympathectomy procedures inside the thoracic surgery device market.

By End User: Hospital Dominance Persists, Specialty Centers Define the Innovation Frontier

Hospitals held 45.23% share in 2025, which preserved their lead position in the thoracic surgery device market. That leadership rests on ICU infrastructure, multidisciplinary tumor boards, resident training, and the ability to manage high-comorbidity patients and complex oncologic resections. Ambulatory Surgical Centers are expanding their role in the thoracic surgery device market as ERAS pathways support same-day discharge in selected wedge resections and smaller lobectomy cases. This shift is tied to lower-cost delivery models and to the growing comfort of surgeons with structured perioperative recovery pathways.

Specialty thoracic centers are projected to grow at 7.95% CAGR through 2031, and within the thoracic surgery device market size outlook, they are the fastest-moving end-user category. Their growth comes from concentrated oncology case mix, earlier adoption of robotic and AI-guided platforms, and a stronger ability to clear robotic learning curves. These centers also serve as evidence-generating sites where vendors place proctoring, training, and workflow support. Credentialing and privileging standards for robotics now matter more because centers that can support multi-platform training are more likely to attract referrals from community hospitals. That dynamic keeps the thoracic surgery device market centered on dedicated specialty hubs for the most complex cases even as lower-acuity volumes begin to spread across more outpatient settings.

Geography Analysis

North America held 38.23% of thoracic surgery device market share in 2025, which made it the largest regional segment in the thoracic surgery device market. This position is supported by a dense robotic installed base, mature ERAS adoption, and a reimbursement structure that still supports complex thoracic procedures across hospital systems. CMS policy documentation for 2026 shows DRG-based reimbursement for complex thoracic procedures under codes 163 to 165 ranging from USD 13,929 to USD 32,613 per case depending on complexity. The United States remains the main volume center in the region because it combines high procedural intensity with broad access to robotic and advanced endoscopic platforms. At the same time, the 2.5% reduction in non-time-based work RVUs for cardiothoracic surgery effective January 1, 2026 creates a near-term margin headwind that could push programs to favor time-efficient pathways and selected site migration rather than reduce procedure volumes outright.

Europe held the second-largest regional position in the thoracic surgery device market, led by Germany and the United Kingdom. The region benefits from strong thoracic center networks, but device adoption remains shaped by a more demanding compliance environment under the EU Medical Device Regulation. In 2025, Guy’s and St Thomas’ NHS Foundation Trust awarded a 7-year direct robotic thoracic surgery contract to Intuitive Surgical through the NHS Supply Chain framework, which shows how public procurement can lock in long-duration vendor relationships once compliance barriers are cleared. France, Italy, Spain, Poland, the Netherlands, and the Scandinavian countries continue to expand VATS and ERAS use within national health system constraints.

Asia-Pacific is projected to grow at 8.92% CAGR through 2031, which makes it the fastest-growing regional segment in the thoracic surgery device market. Japan has already shown how reimbursement can reshape procedure mix, with robotic-assisted thoracic surgery moving from less than 1% of lung cancer procedures in 2017 to more than 15% by 2025 after insurance inclusion widened. China is becoming the most structurally important growth engine in the thoracic surgery device market because domestic robotic brands won more than 50% of public hospital tenders in 2025, while Shanghai Pulmonary Hospital surpassed 1,000 domestic robot-assisted thoracic cases at a single center. India, South Korea, and Australia are also extending minimally invasive and robotic thoracic capacity through reimbursement expansion and high-volume oncology centers, while the Middle East and Africa and South America remain smaller but emerging destinations for investment through private hospital growth and medical tourism infrastructure.

Competitive Landscape

The thoracic surgery device market is moderately concentrated at the premium end and more fragmented in surrounding device categories. Intuitive Surgical remains the strongest force in robotic platforms, while Olympus, Karl Storz, and Fujifilm remain important in endoscopy and visualization, and CONMED, B. Braun, Medtronic, Johnson & Johnson, and Teleflex compete across stapling, access, and energy portfolios. This means the thoracic surgery device market combines a concentrated installed-base structure in robotics with broader fragmentation in the tools and disposables used across procedures. The main commercial advantage still belongs to companies that can combine hardware, service, training, and recurring instrument demand into a durable hospital relationship. That structure keeps procurement power and switching costs at the center of competition in the thoracic surgery device market.

Several strategic moves show how the thoracic surgery device market is opening to a more multi-platform future. In December 2025, Medtronic received FDA clearance for the Hugo robotic-assisted surgery system for urologic procedures, which marked its first U.S. regulatory approval and improved its position to pursue broader multi-specialty expansion over time. In January 2026, Johnson & Johnson submitted the Ottava Robotic Surgical System to the FDA for de novo classification, signaling a direct effort to build a multi-specialty platform with thoracic surgery on the medium-term roadmap. In April 2025, CMR Surgical secured more than USD 200 million in new financing to accelerate its U.S. launch following FDA clearance for Versius, which supports its push around multi-specialty flexibility.

Competition is also shifting geographically inside the thoracic surgery device market. Chinese domestic robotic manufacturers, led by Touchsurgeons and MicroPort’s Shurui system, won more than 50% of public hospital robotic surgery tenders in China in 2025 for the first time, and that change weakens the long-held assumption that imported platforms will dominate the country’s higher-growth segment. The result is likely to be more pricing pressure on instruments and service contracts, even while overall procedure volumes continue to rise. Vendors that can offer flexible financing, faster training support, and integrated imaging workflows will be better positioned as the thoracic surgery device market moves into mid-tier hospitals and regional specialty centers. That leaves the thoracic surgery device market with clear leaders in premium platforms, but with widening competition wherever hospitals begin to evaluate total program cost rather than platform prestige alone.

Thoracic Surgery Devices Industry Leaders

B. Braun Melsungen AG

Boston Scientific Corporation

CONMED Corporation

Medtronic

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Johnson & Johnson submitted the Ottava Robotic Surgical System to the FDA for de novo classification covering multiple upper abdominal procedures; the submission leverages IDE study data and marks a critical step toward multi-specialty deployment, with thoracic indications under active development in parallel IDE programs.

- January 2026: China's National Healthcare Security Administration published the "Surgical and Treatment Auxiliary Operation Medical Service Price Item Establishment Guidelines," formalizing 37 standardized robotic surgery procedure codes. This reimbursement framework is expected to accelerate hospital adoption of robotic thoracic platforms across Chinese public hospitals, representing the single largest regulatory catalyst for the Asia-Pacific segment in the forecast period.

- December 2025: Medtronic received FDA clearance for the Hugo robotic-assisted surgery system for urologic procedures, representing the company's first US regulatory approval; with active thoracic clinical trials underway in Belgium and plans for indication expansion, the clearance positions Hugo as a credible multi-specialty competitor to da Vinci within a 2-3 year window.

- April 2025: CMR Surgical secured more than USD 200 million in new financing to accelerate the commercial launch of Versius in the United States following FDA clearance; the round also supports development of the Versius Plus system and NVIDIA IGX Thor AI integration. The company's installed Versius base has completed over 30,000 procedures globally across more than 30 countries.

Global Thoracic Surgery Devices Market Report Scope

The thoracic surgery device market refers to the industry focused on the development, production, and distribution of specialized medical instruments, imaging systems, energy devices, and robotic platforms used in surgical procedures within the chest cavity. It is driven by technological innovation, the rising prevalence of thoracic conditions, and the growing adoption of minimally invasive and robotic-assisted techniques.

The market is segmented by procedure type, which includes open thoracic surgery, video-assisted thoracoscopic surgery (VATS), robotic-assisted thoracic surgery, and endoscopic thoracic surgery. By product type, it covers surgical instruments and accessories, endoscopes and imaging systems, energy and stapling devices, and robotic platforms. By indication, the market addresses lung cancer, esophageal cancer, pneumothorax, mediastinal tumors, and hyperhidrosis. By end user, it serves hospitals, ambulatory surgical centers, and specialty thoracic centers. Finally, by geography, the market is divided into North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Open Thoracic Surgery |

| Video-Assisted Thoracoscopic Surgery |

| Robotic-Assisted Thoracic Surgery |

| Endoscopic Thoracic Surgery |

| Surgical Instruments and Accessories |

| Endoscopes and Imaging Systems |

| Energy and Stapling Devices |

| Robotic Platforms |

| Lung Cancer |

| Esophageal Cancer |

| Pneumothorax |

| Mediastinal Tumors |

| Hyperhidrosis |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Thoracic Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Type | Open Thoracic Surgery | |

| Video-Assisted Thoracoscopic Surgery | ||

| Robotic-Assisted Thoracic Surgery | ||

| Endoscopic Thoracic Surgery | ||

| By Product Type | Surgical Instruments and Accessories | |

| Endoscopes and Imaging Systems | ||

| Energy and Stapling Devices | ||

| Robotic Platforms | ||

| By Indication | Lung Cancer | |

| Esophageal Cancer | ||

| Pneumothorax | ||

| Mediastinal Tumors | ||

| Hyperhidrosis | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Thoracic Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of thoracic surgery by 2031?

The thoracic surgery market is projected to reach USD 18.36 billion by 2031, rising from USD 12.95 billion in 2026 at a 7.23% CAGR.

Which procedure type leads current demand?

Video-assisted thoracoscopic surgery led with 49.21% share in 2025, reflecting its deep clinical adoption and broad hospital training base.

Why are robotic systems gaining traction in chest procedures?

Robotic-assisted thoracic surgery is projected to grow at 8.23% CAGR through 2031 because surgeons value articulation, tremor filtration, 3D optics, and better access in complex dissections.

Which region is growing the fastest?

Asia-Pacific is expected to expand at 8.92% CAGR through 2031, supported by reimbursement reform, domestic robotic manufacturing, and growing lung cancer surgical volumes.

Page last updated on: