Cardiopulmonary Bypass Equipment Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

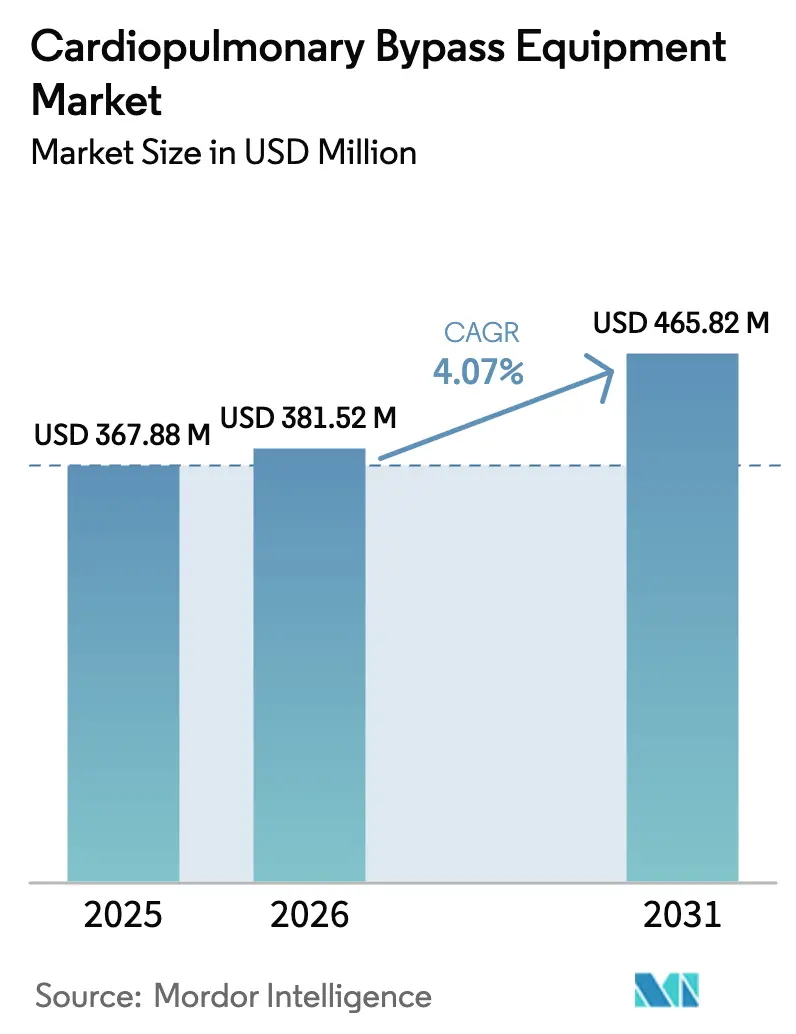

| Market Size (2026) | USD 381.52 Million |

| Market Size (2031) | USD 465.82 Million |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

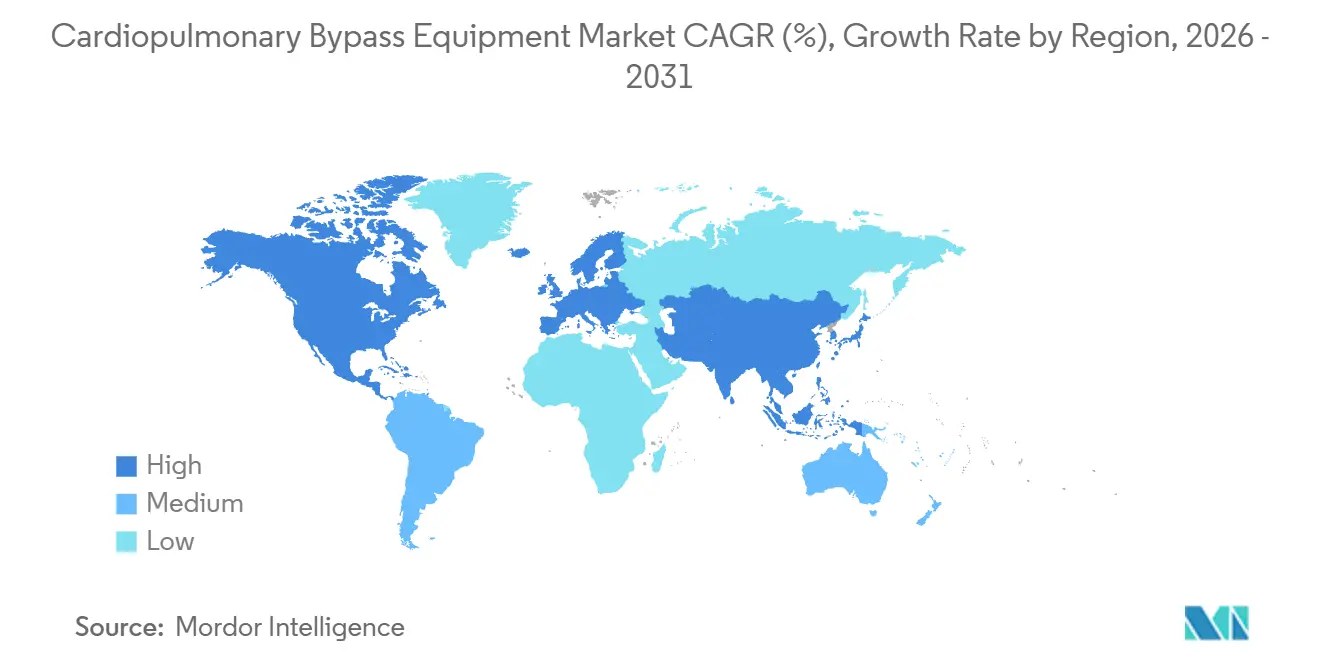

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiopulmonary Bypass Equipment Market Analysis by Mordor Intelligence

Cardiopulmonary Bypass Equipment Market size in 2026 is estimated at USD 381.52 million, growing from 2025 value of USD 367.88 million with projections showing USD 465.82 million, growing at 4.07% CAGR over 2026-2031.

The steady ascent of market reflects an aging global population that drives surgical demand, regulatory endorsement of centrifugal pumps that limit haemolysis, and early-stage deployment of AI-guided perfusion analytics that curb intraoperative error. Hospitals remain the primary buyers, yet ambulatory surgical centres are emerging as viable outlets for lower-acuity coronary procedures by pairing compact, single-use circuits with payer incentives that reward same-day discharge. North America maintains the largest revenue pool on the strength of high per-capita surgery volumes and rapid adoption of Class-III device upgrades, while Asia-Pacific offers the fastest runway for vendors, as China and India subsidize local pump and oxygenator production. Competitive intensity is moderate because the five leading manufacturers hold only about half of the installed base, leaving room for regional specialists that combine lower-cost hardware with subscription-based software.

Key Report Takeaways

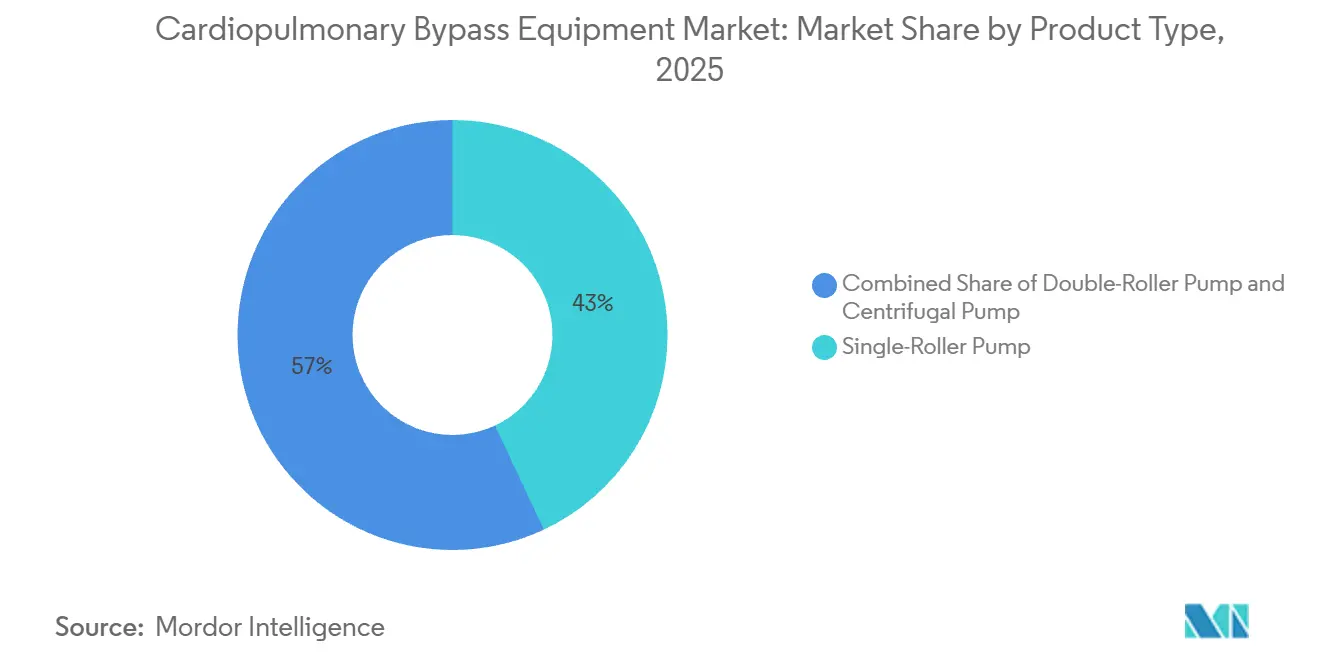

- By product type, single-roller pumps held 43.01% of cardiopulmonary bypass equipment market share in 2025, while centrifugal systems are pacing ahead at a 7.09% CAGR through 2031.

- By application, cardiac surgery generated 56.87% of revenue in 2025; acute respiratory failure is forecast to expand at a 7.84% CAGR to 2031.

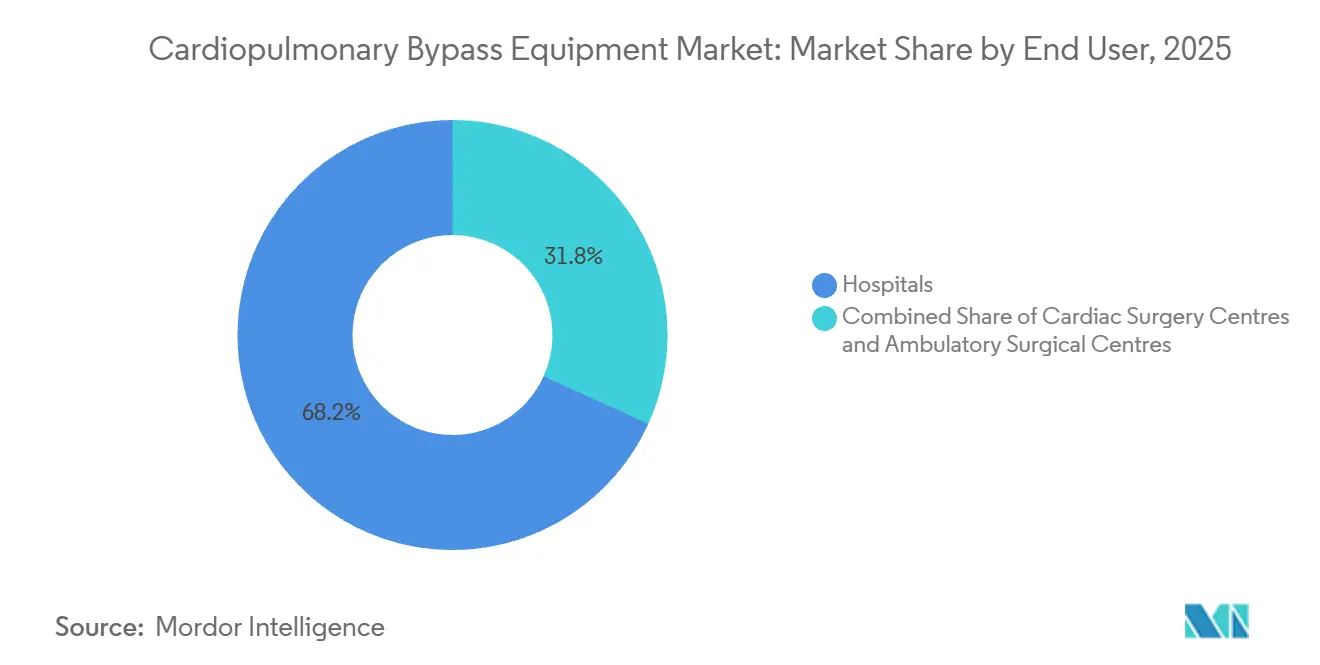

- By end user, hospitals accounted for 68.22% of the cardiopulmonary bypass equipment market size in 2025, and ambulatory surgical centers are advancing at a 9.69% CAGR through 2031.

- By geography, North America led with 36.83% revenue share in 2025, whereas Asia-Pacific is expected to rise at a 10.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cardiopulmonary Bypass Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cardiac-surgery volumes in aging populations | +1.2% | North America, Western Europe, Japan, and urban Asia-Pacific | Long term (≥ 4 years) |

| Technological advances in oxygenators and pumps | +0.9% | Early adoption in North America and the EU, spill-over to the Asia-Pacific | Medium term (2-4 years) |

| Higher adoption of minimally invasive CABG | +0.7% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| AI-guided perfusion analytics | +0.5% | North America, select EU centres, pilots in China and India | Long term (≥ 4 years) |

| Supply-chain localization in China and India | +0.6% | Asia-Pacific core, spill-over to the Middle East and Africa | Short term (≤ 2 years) |

| Growing adoption of minimally invasive procedures | +0.8% | Global, led by North America and the EU, is widening in the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cardiac-Surgery Volumes in Aging Populations

Cardiovascular disease risk accelerates after age 60, and the 65-plus cohort is set to reach 1.6 billion by mid-century, sharply enlarging the surgical pool.[1]United Nations, “World Population Prospects,” un.org Japan documented 68,000 open-heart operations in 2025, a 4% gain despite a shrinking total population, illustrating how age structure outweighs headcount. U.S. Medicare claims show individuals older than 75 generate over half of coronary artery bypass grafting cases, and this subgroup is expanding by 3.1% annually to 2031. Regulatory frameworks that mandate ISO 10993 testing ensure blood-contact materials meet strict biocompatibility standards for older patients with more comorbidities. Emerging economies lag on absolute procedure counts today, yet tertiary hubs in Mumbai, São Paulo, and Johannesburg already post double-digit growth as non-communicable disease prevalence rises.

Technological Advances in Oxygenators and Pumps

Hollow-fibre oxygenators launched in 2024 with polymethyl pentene coatings cut plasma leakage by 30%, allowing longer runs without circuit change-out. Magnetic-levitation centrifugal pumps introduced by major manufacturers drive free haemoglobin below 5 mg/dL, extending safe pump time to 12 hours for challenging aortic repairs.[2]Medtronic, “Form 10-K 2025,” medtronic.com In March 2025, the FDA cleared a modular console that integrates blood-gas analytics with automated heparin dosing, reducing the perfusionist workload by roughly one-fifth. The EU’s MDR now requires clinical evidence for oxygenators marketed for more than 6 hours of use, raising the entry bar and rewarding companies that hold long post-market datasets. Asian start-ups are licensing surface-modification patents to manufacture heparin-bonded tubing at 40% lower cost than Western counterparts, finding traction in cost-sensitive public hospitals.

Higher Adoption of Minimally Invasive CAB

Port-access and robotic revascularization require mini-CPB circuits with priming volumes below 500 mL, minimizing haemodilution in tight surgical fields. Registry data show minimally invasive CABG rose 11% in 2025, aided by recovery times that trimmed the median length of stay from 6.2 days to 3.8 days. New platforms integrate vacuum-assisted venous return and kinetic drainage to sustain flow with smaller cannula and have secured reimbursement codes in Germany and France that mirror the added complexity. IEC 60601 electrical safety standards and ISO 14971 risk management documents state that trimming circuit volume does not impair oxygenation or temperature control. Uptake in rural hospitals lags because teams lack training, and robotic consoles remain capital-intensive, concentrating adoption in academic centres.

AI-Guided Perfusion Analytics

Machine-learning models trained on 50,000 cases can flag metabolic acidosis or coagulopathy 15 minutes before clinical signs appear, enabling timely adjustments in flow and pressure. A European trial of LivaNova’s Essenz system cut variation in oxygen delivery by 18%, standardizing care across shifts. The U.S. certifying body now recognizes AI-assisted decision support as valid continuing education, signalling mainstream professional acceptance. FDA classifies such software as Class II when it alerts rather than autonomously controls pumps, while the EMA requires an MDR Annex XV investigation for any closed-loop function, creating patchwork pathways. Data privacy gaps in emerging markets restrain adoption because electronic records and cloud connectivity remain sporadic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and consumable costs | -0.8% | Global, most acute in price-sensitive public hospitals | Long term (≥ 4 years) |

| Stringent Class-III regulatory approvals | -0.5% | Global, pronounced in EU and U.S. | Medium term (2-4 years) |

| Global shortage of certified perfusionists | -0.6% | North America, Western Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Competition from off-pump and transcatheter procedures | -0.9% | North America and EU, spreading to urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Costs

Fully equipped CPB suites cost USD 200,000–300,000, with annual maintenance at 10% and single-use oxygenator kits priced between USD 600 and USD 1,200 per case. Public hospitals operating on sub-USD 800 case budgets in parts of Africa and South Asia sometimes reuse oxygenators, a practice prohibited in the U.S. and EU but tolerated locally if endotoxin tests clear. Scandinavian and U.K. value-based procurement models negotiate 15-20% discounts by bundling consumables with implants, though smaller hospitals lack the same level of leverage. A 12% rise in polypropylene resin prices during 2025 forced manufacturers to pass roughly half the cost to buyers, further squeezing hospital margins.

Stringent Class-III Regulatory Approvals

The EU MDR lengthens time-to-market to upward of 24 months and adds five-year post-market follow-up requirements that cost roughly EUR 500,000 per product line.[3]BSI Group, “MDR Compliance Costs,” bsigroup.com The FDA now requests clinical cases when the age of the predicates exceeds 10 years, requiring bench and haemolysis testing, as well as small clinical cohorts. China offers a nine-month priority path for domestically innovated devices, but foreign firms still face standard 18-month reviews and must appoint local legal holders. Annual surveillance audits under ISO 13485 add USD 50,000-100,000 in recurring fees for mid-sized makers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Centrifugal Systems Extend Momentum

In value terms, single-roller pumps retained 43.01% of the cardiopulmonary bypass equipment market share in 2025, driven by lower upfront prices and long-standing familiarity among perfusion teams. The centrifugal category, however, is expanding at 7.09% CAGR, and its share of the cardiopulmonary bypass equipment market size is set to widen through 2031 as hospitals favour lower haemolysis rates and compatibility with minimally invasive CABG.

Roller designs will remain staples in budget-constrained settings due to their low maintenance and seamless integration with existing oxygenator inventories. Yet magnetic-levitation centrifugal pumps eliminate mechanical seals, cut free haemoglobin release by 40%, and meet tightened FDA haemolysis criteria, attributes that resonate with centres pursuing enhanced-recovery pathways. European and Japanese hospitals are the fastest adopters, encouraged by reimbursement frameworks that reward shorter ICU stays. Chinese manufacturers entering with 30% lower list prices could accelerate the pivot, but lingering concerns over long-term durability data may temper uptake outside domestic tenders.

By Application: Acute Respiratory Failure Surges Ahead

Cardiac surgery remained the dominant application, accounting for 56.87% of revenue in 2025, yet acute respiratory failure is charting a 7.84% CAGR, positioning it as the prime growth frontier for the cardiopulmonary bypass equipment market. ECMO capacity jumped by 1,200 beds across North America and Europe between 2023 and 2025, and expanded reimbursement codes now cover COVID-19 and influenza-related ARDS.

Hospitals further justify ECMO investments by cross-utilizing pumps and oxygenators in bridge-to-transplant or intraoperative lung transplant support, boosting asset utilization. Asia-Pacific shows the steepest acceleration in respiratory indications, as air-pollution-related lung disease rises in tandem with critical-care infrastructure spending, according to the. Cardiac surgery growth remains tied to aging demographics in mature markets and the build-out of subspecialty centres in emerging economies, anchoring a stable base even as some coronary and valve volumes migrate to catheter interventions.

By End User: Ambulatory Centers Accelerate

Hospitals accounted for 68.22% of the cardiopulmonary bypass equipment market in 2025, owing to their monopoly over complex cases that require extensive ICU support. Ambulatory surgical centres, however, are clocking a 9.69% CAGR, propelled by payer push to move low-risk bypasses to lower-cost sites and by compact single-use circuits that cut setup time to 20 minutes.

States without certificate-of-need barriers, Florida, Texas, and California, lead adoption, whereas unionized regions and strict licensure rules still funnel most volume to hospitals. Cardiac surgery centres of excellence sit in between: they focus on high-volume throughput and advanced robotics yet must now differentiate against ambulatory rivals by marketing complex-case expertise and bundled care pathways.

Geography Analysis

North America maintained a 36.83% revenue share in 2025, driven by roughly 400,000 cardiac surgeries, premium reimbursement, and the rapid adoption of AI-guided consoles and magnetic-levitation pumps. Growth in the region now hinges on replacement demand for aging equipment and on the migration of eligible cases to ambulatory surgical centres, a segment expanding nearly 10% yearly as insurers waive patient cost-sharing for outpatient CABG. Strict FDA post-market vigilance adds cost but underpins device safety, while Canadian bulk-buy contracts squeeze vendor pricing while securing multi-year volumes.

Europe generated revenue higher than North America but lower than Asia-Pacific. Germany, France, and the U.K. together perform 180,000 procedures per year and reward vendors that achieve lower transfusion rates or shorter ICU stays through diagnosis-related group payments. The MDR’s rigorous clinical-evidence requirements extend approvals but simultaneously fortify incumbent share by making it harder for small entrants to clear regulatory hurdles. Southern European systems lean on reprocessed circuits due to fiscal constraints; an approach manufacturer discourage for liability reasons.

Asia-Pacific is the growth engine with a 10.27% CAGR projection. China performed 120,000 cardiac surgeries in 2025 and uses subsidies and local-content quotas to reshape competitive positioning in favour of domestic makers. India’s procedure count hit 80,000 in 2025 and is set to double by 2031 due to urbanization and dietary shifts. Japan’s aging society raises procedure volume even as its total population falls, and recent reimbursement changes allow AI-assisted perfusion fees, bolstering premium pump uptake. Australia, South Korea, and Southeast Asian nations pursue ISO-aligned regulatory frameworks, which smooth regional approvals but expose Western vendors to intense price competition from subsidized Chinese exports.

Oil-rich Gulf states fund state-of-the-art suites that attract medical tourists, whereas South Africa and Brazil split demand between private-sector imports and public-sector refurbished equipment. Argentina’s economic swings lengthen console lifecycles to beyond 12 years, and hospitals rely on third-party service contracts. Pan-American regulatory harmonization now trims redundant testing, aiding region-based manufacturers that compete on cost while meeting ISO 13485.

Competitive Landscape

Five multinational corporations, Medtronic, LivaNova, Getinge, Terumo, and Fresenius Medical Care, command a significant portion of global sales, evidencing a moderately concentrated structure where scale matters yet sizable white space remains for niche players. Incumbents funnel R&D into AI-enabled consoles, magnetic-levitation pumps, and heparin-bonded circuits that justify premium pricing in high-income markets. Regional challengers in China and India pursue cost leadership through localization subsidies, often pricing hardware 25-30% below Western equivalents while partnering with domestic logistics networks.

Strategic manoeuvres illustrate dual tracks. LivaNova paid EUR 85 million for a German software firm in 2024 to integrate predictive analytics into its Essenz platform, confirming the pivot toward digital ecosystems. Getinge forged a partnership with a Taiwanese oxygenator producer to extend its footprint in Asia without committing to costly greenfield plants. Patent activity centres on membrane coatings and pump-bearing architectures; Medtronic filed 14 new CPB patents in 2025 alone, including a predictive venous drainage algorithm awaiting FDA clearance.

Cost pressure persists as hospitals consolidate purchasing through group purchasing organizations that leverage multi-year contracts to extract 12-18% discounts. In response, vendors bundle equipment with training, service, and perfusion analytics subscriptions that smooth revenue and embed switching costs. Ambulatory centres present a fertile niche because they value single-use circuits and pay-per-case pricing, a model nimble startups can exploit while larger firms experiment with as-a-service offerings.

Cardiopulmonary Bypass Equipment Industry Leaders

Boston Scientific Corporation

Abbott Laboratories

Gettinge AB

Fresenius Medical Care

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Medtronic earmarked USD 120 million to expand perfusion-system manufacturing in Tijuana, Mexico, adding 40,000 m² of cleanroom space to diversify supply chains and serve rising Latin American centrifugal-pump demand.

- December 2025: LivaNova secured FDA 510(k) clearance for the Essenz AI-guided perfusion platform after training algorithms on 60,000 cardiac cases to predict metabolic acidosis and coagulopathy up to 20 minutes early.

- August 2025: LivaNova initiated the first commercial rollout of the Essenz Perfusion System in China under the latest NMPA provisions, opening the world’s second-largest heart-lung machine market to its AI-enabled console.

Global Cardiopulmonary Bypass Equipment Market Report Scope

The Cardiopulmonary Bypass Equipment Market encompasses medical devices used to maintain blood circulation and oxygenation during surgical procedures where the heart must be stopped, such as coronary artery bypass grafting (CABG), valve repair/replacement, and congenital heart defect correction.

The Cardiopulmonary Bypass Equipment Market Report is Segmented by Product Type (Single-Roller Pump CPB, Double-Roller Pump CPB, Centrifugal Pump CPB), Application (Cardiac Surgery, Lung Transplant Operations, Acute Respiratory Failure, Others), End User (Hospitals, Cardiac Surgery Centres, Ambulatory Surgical Centres), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Single-Roller Pump CPB |

| Double-Roller Pump CPB |

| Centrifugal Pump CPB |

| Cardiac Surgery |

| Lung Transplant Operations |

| Acute Respiratory Failure |

| Others |

| Hospitals |

| Cardiac Surgery Centres |

| Ambulatory Surgical Centres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Single-Roller Pump CPB | |

| Double-Roller Pump CPB | ||

| Centrifugal Pump CPB | ||

| By Application | Cardiac Surgery | |

| Lung Transplant Operations | ||

| Acute Respiratory Failure | ||

| Others | ||

| By End User | Hospitals | |

| Cardiac Surgery Centres | ||

| Ambulatory Surgical Centres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the cardiopulmonary bypass equipment market?

The market was valued at USD 381.52 million in 2026 and is projected to hit USD 465.82 million by 2031.

Which segment grows fastest within cardiopulmonary bypass equipment?

Centrifugal pump systems are expanding at a 7.09% CAGR through 2031, driven by lower haemolysis and compatibility with minimally invasive surgery.

Which application is seeing the highest growth momentum?

Acute respiratory failure usage of CPB circuits is advancing at a 7.84% CAGR as hospitals expand ECMO capacity.

Which region offers the greatest growth potential?

Asia-Pacific leads with a forecast 10.27% CAGR, driven by China and India’s localization policies and rising surgery volumes.

How are ambulatory surgical centres impacting demand?

They are increasing at a 9.69% CAGR by adopting compact, single-use circuits that enable same-day discharge for select bypass cases.

Page last updated on: