Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

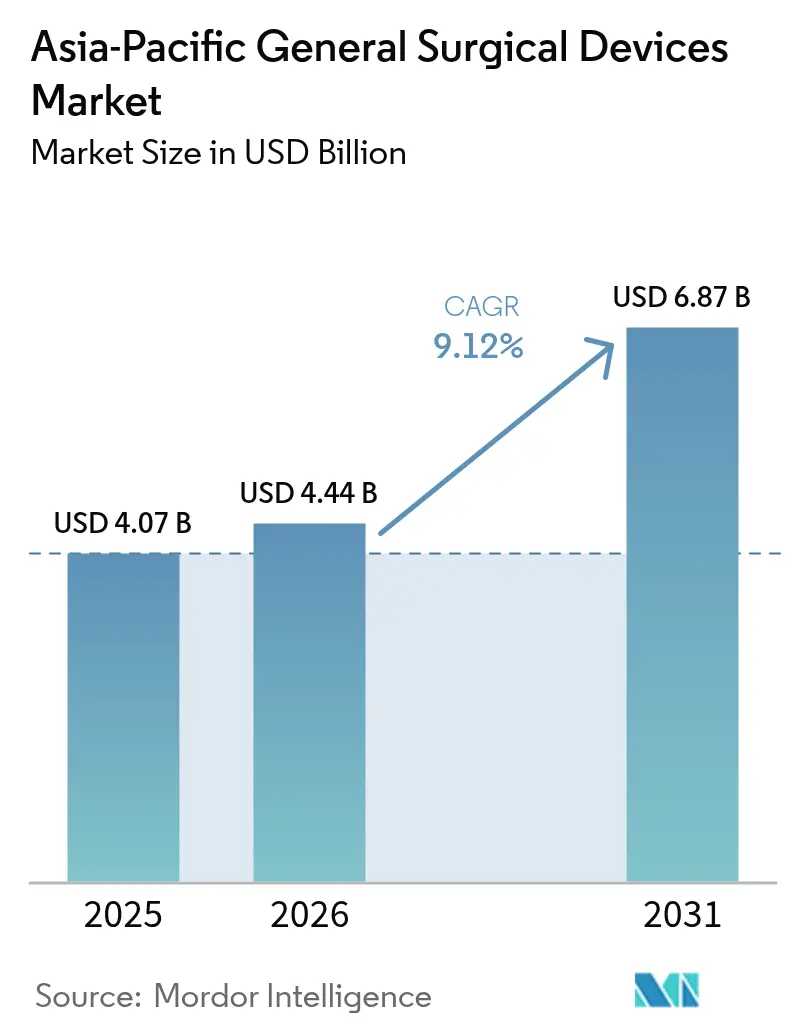

| Base Year Market Size (2025) | USD 4.07 Billion |

| Market Size (2026) | USD 4.44 Billion |

| Market Size (2031) | USD 6.87 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific General Surgical Devices Market Analysis by Mordor Intelligence

The Asia-Pacific General Surgical Devices market size is expected to grow from USD 4.07 billion in 2025 to USD 4.44 billion in 2026 and is forecast to reach USD 6.87 billion by 2031 at 9.12% CAGR over 2026-2031. Sustained modernisation of surgical care, an ageing population, and rapid adoption of minimally invasive and robotic platforms are the primary engines of growth. Converging regulatory regimes, particularly the ASEAN Medical Device Directive, are shortening go-to-market timelines for multinational and regional innovators. China leads regional revenue with a 31.97% stake in 2024, while India shows the fastest trajectory on the back of double-digit healthcare spending increases and strong localisation policies. Minimally invasive procedures dominate operating theatres, underpinning resilient demand for laparoscopic and energy-based tools, even as premium-priced robotic systems register the highest growth. Outpatient migration to ambulatory surgical centres (ASCs) is reshaping procurement strategies toward compact, workflow-oriented equipment, and pan-regional partnerships between global manufacturers and domestic firms are widening access to next-generation technology.[1]Source: Ming Xu, “Regulatory reliance for convergence and harmonisation in the medical device space in Asia-Pacific,” BMJ Global Health, gh.bmj.com

Key Report Takeaways

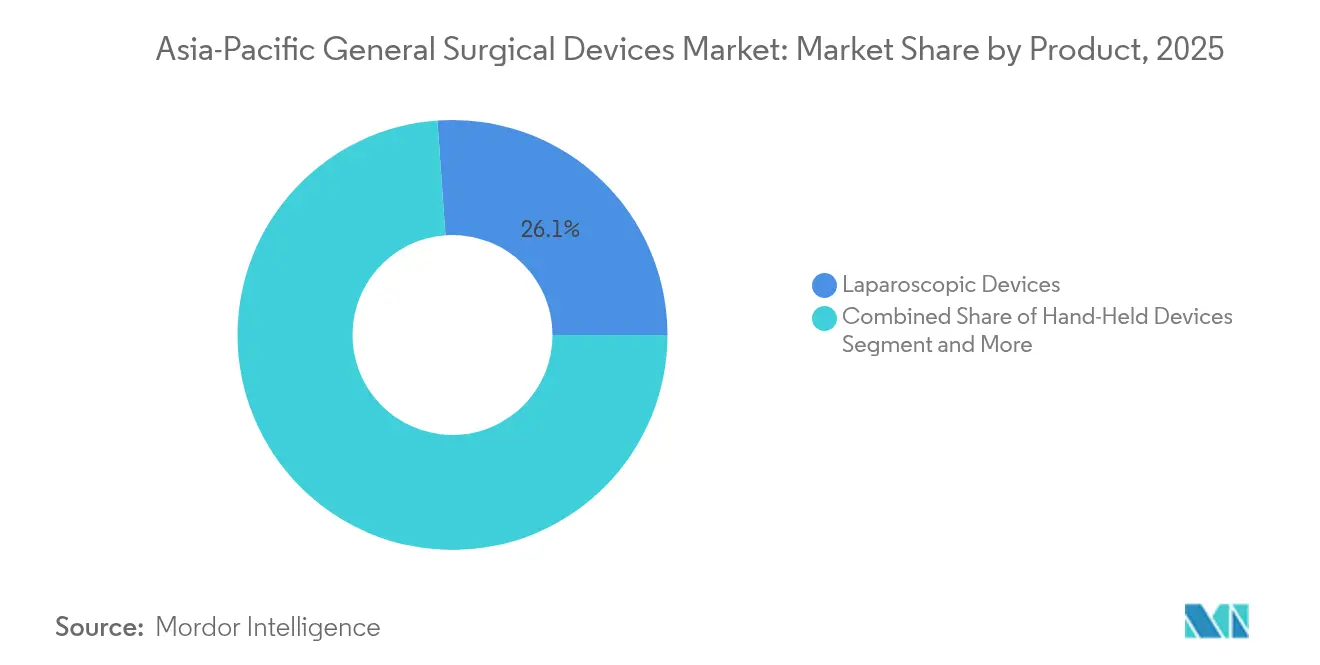

- By product category, laparoscopic devices led with 26.12% revenue share of the Asia Pacific General Surgery Devices market in 2025, whereas robotic-assisted platforms are forecast to advance at a 11.42% CAGR through 2031.

- By procedure approach, minimally invasive surgery held 62.05% of the Asia Pacific General Surgery Devices market share in 2025 and is expected to grow at a 10.05% CAGR to 2031.

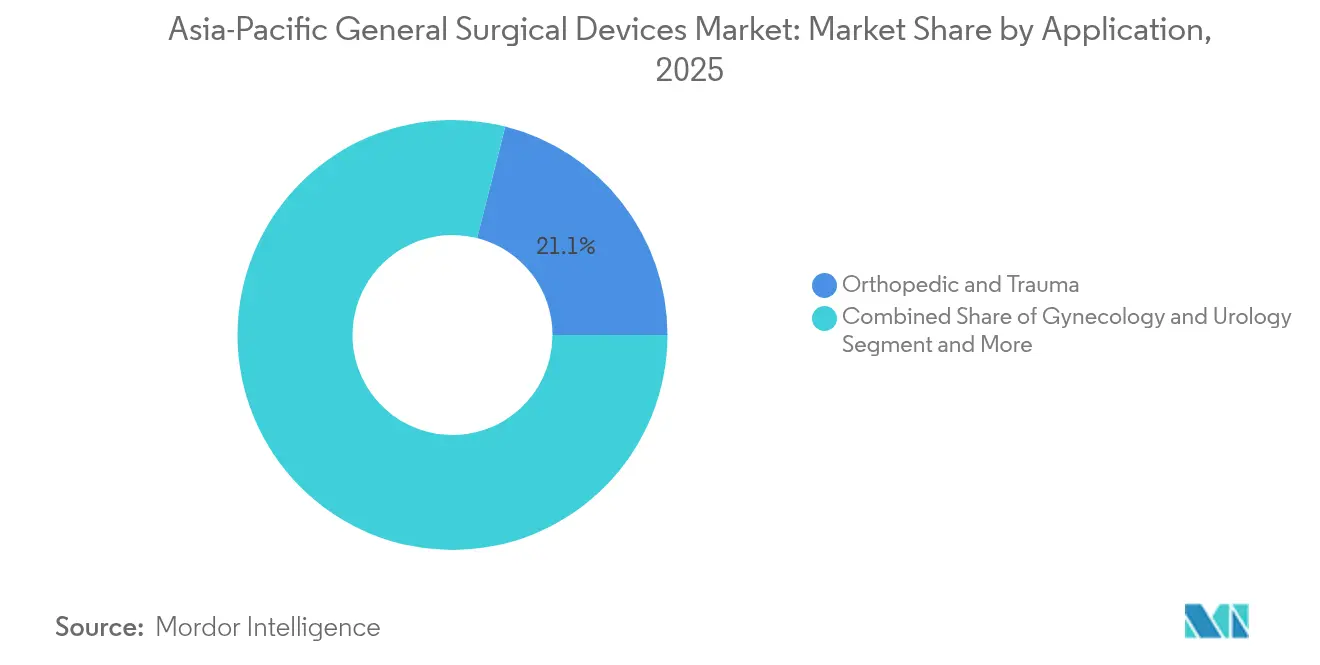

- By application, orthopedic & trauma procedures accounted for 21.05% share of the Asia Pacific General Surgery Devices market size in 2025; bariatric & gastrointestinal surgery is poised to expand at an 10.64% CAGR during 2026-2031.

- By end user, hospitals commanded 66.92% share of the Asia Pacific General Surgery Devices market size in 2025, while ambulatory surgical centres represent the fastest-growing channel with an 10.81% CAGR to 2031.

- By geography, China captured 31.55% of the Asia Pacific General Surgery Devices market in 2025; India is projected to post the highest 10.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Adoption of Minimally-Invasive & Robotic Surgery Across APAC | +2.1% | Global, with early gains in Japan, South Korea, China | Medium term (2-4 years) |

| Rapid Capacity Build-out of Public & Private Surgical Facilities | +1.8% | China, India, Southeast Asia core markets | Long term (≥ 4 years) |

| Ageing Population and Rising Chronic Disease Burden Boosting Surgical Volumes | +1.7% | Japan, China, Australia, spill-over to emerging markets | Long term (≥ 4 years) |

| Escalating Obesity-Linked Demand for Bariatric & GI Procedures | +1.3% | China, India, urban centers across APAC | Medium term (2-4 years) |

| Persistently High Trauma & Orthopedic Injury Incidence | +1.0% | Global, concentrated in high-traffic density regions | Short term (≤ 2 years) |

| Product Launches and Local Partnerships | +0.9% | Japan, China, India with regulatory pathway advantages | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Adoption of Minimally Invasive & Robotic Surgery Across APAC

Hospitals across the region are accelerating procurement of robotic systems as evidence mounts that force-feedback instrumentation and AI-assisted guidance improve resection accuracy and shorten learning curves. Japan recorded its first colorectal procedure with the fifth-generation da Vinci in 2025, underscoring acceptance of data-rich consoles for complex oncology cases.[2]Source: Osaka Keisatsu Hospital, “First da Vinci 5 colorectal procedure,” prtimes.jp China’s National Medical Products Administration cleared domestic robotic platforms offering 0.1 mm precision, signalling policy support for indigenous high-tech solutions. Cross-border 5G demonstrations have proven that expert surgeons can supervise laparoscopy at distances over 1,000 km, opening a viable model for serving remote areas without full-time specialists. AI image-analysis modules now embedded in endoscopic towers provide real-time margin assessment, integrating seamlessly with existing laparoscopic workflows and accelerating the upgrade path for mid-tier hospitals. These gains collectively reinforce the Asia Pacific General Surgery Devices market as a hotbed for digital surgical innovation.

Rapid Capacity Build-out of Public & Private Surgical Facilities

Annual health-budget increases in major economies are translating into bricks-and-mortar expansion of operating suites. India raised central health outlays by 12.59% for FY 2024–25 and activated five new AIIMS institutes, each housing multi-specialty theatres ready for advanced energy devices and robotic carts. China’s coupling-coordination metrics show improved alignment between supply and ageing-related demand, but resource deserts in western provinces persist, spurring policy to fast-track equipment tenders that close service gaps. Multinationals such as Medtronic have responded by opening robotics training studios in Singapore and Korea, creating demonstration hubs that anchor vendor relationships and swing future device standardisation decisions toward their platforms. Construction of dedicated day-surgery centres attached to private hospitals is equally brisk, feeding incremental volumes to suppliers focused on high-turnover consumables.

Ageing Population and Rising Chronic Disease Burden Boosting Surgical Volumes

The number of citizens aged ≥ 60 has surged across Northeast Asia, propelling procedure counts for hernia repair, hip fracture fixation, and cardiac revascularisation. China’s healthcare spend jumped nearly 16-fold between 2007 and 2023, with orthopaedic implants and wound-closure systems among the fastest adopters. Hip-fracture caseloads in Australia are forecast to more than double by 2050, setting a predictable baseline for trauma hardware demand. Japanese payers are under pressure to limit inpatient days, encouraging hospitals to invest in stapling and sealing technologies that permit shorter stays. Epidemiological projections for hernia indicate a 19.7% rise in new cases by 2050, compelling vendors to refine mesh materials suited to elderly tissue integrity. Collectively, demographic ageing locks in a durable expansion pattern for the Asia Pacific General Surgery Devices market.

Escalating Obesity-Linked Demand for Bariatric & GI Procedures

Urban lifestyle shifts have pushed obesity prevalence sharply higher, particularly in China and India, lifting utilisation of laparoscopic sleeve gastrectomy and gastric bypass sets. Bariatric surgery mortality now ranges from 0.03-0.2%, and complication rates hover near 1%, statistics that reassure surgeons and patients alike. Comparative trials show robotic bariatric techniques cut bleeding risk versus conventional laparoscopy, justifying investment in articulating staplers and energy instruments specific to thick-walled gastric tissue. Enhanced-recovery protocols reduce ward occupancy, making bariatric programmes increasingly attractive for ASCs and driving demand for portable high-definition camera stacks. Simultaneously, pre-operative endoscopy uncovers gastritis in over 80% of candidates, underscoring the need for combined diagnostic-therapeutic towers marketed as turnkey suites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged & Complex Regulatory Approval Pathways | -1.4% | China, India, Southeast Asia emerging markets | Medium term (2-4 years) |

| Inconsistent and Limited Reimbursement for Advanced Devices | -1.2% | Regional variations, concentrated in tier-2/3 cities | Long term (≥ 4 years) |

| Capital Constraints in Tier-2/3 Hospitals Favor Refurbished / Low-Cost Equipment | -0.9% | India, China, Southeast Asia secondary markets | Medium term (2-4 years) |

| Shortage of Skilled Surgical Workforce | -0.8% | Global, acute in rural and secondary urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prolonged & Complex Regulatory Approval Pathways

Despite ASEAN moves toward convergence, firms still navigate a mosaic of country-specific forms, device classifications, and import checks that prolong commercial launches. China’s updated medical-device law tightened post-market surveillance, adding iterative testing that can postpone revenue. India’s new marketing code requires explicit disclosure of value transfers, complicating clinician-engagement strategies. Japan continues to experience “device lag” as thorough domestic reviews extend beyond submissions already cleared in the United States or Europe. While third-party conformity assessments are authorised in several jurisdictions, uneven adoption limits their time-saving potential. The net effect clips momentum in the Asia Pacific General Surgery Devices market, especially for SMEs lacking dedicated regulatory staff.

Shortage of Skilled Surgical Workforce

Workforce deficits curb procedure throughput and, therefore, equipment utilisation. Surveys in Hokkaido showed fewer than half of the general surgeons were confident in essential trauma operations. Perioperative nursing shortages elevate turnover and inflate wage bills, leading hospitals to defer capex on new towers when staffing cannot support extra sessions. Young physicians migrate abroad for better training, hollowing talent pipelines in mid-income ASEAN states. COVID-19 backlogs highlighted the absence of formal health-policy curricula in surgical residencies, hampering leaders’ ability to advocate for resource allocation. Collectively, skill scarcity slows adoption of complex systems that require longer credentialing programmes or multi-disciplinary teamwork.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Robotic Platforms Drive Premium Growth

Robotic-assisted platforms represent the fastest-rising product line at a 11.42% CAGR, yet laparoscopic devices still supply the highest absolute revenue with 26.12% share in 2025. Hospitals appreciate laparoscopy’s versatility across gynaecology, GI, and urology, guaranteeing baseline orders for trocar sets and clip appliers. Hand-held instruments remain indispensable for basic tissue manipulation, keeping entry price points accessible in smaller centres. Electrosurgical generators are benefiting from refinements in waveform modulation that cut collateral thermal injury, aligning with safety mandates.

Wound-closure innovations include electroceutical dressings that accelerate chronic-wound granulation, widening indications beyond theatre into postoperative wards. Single-use ancillaries are growing rapidly as infection-control committees weigh sterility assurance against waste-management costs; manufacturers now publicise recycling take-back schemes to overcome sustainability objections. With AI-ready robotic chassis marketed as modular, upgradeable investments, capital budgets are increasingly earmarked for systems that future-proof against data-driven surgical expectations, bolstering long-run value capture in the Asia Pacific General Surgery Devices market.

By Procedure Approach: Minimally Invasive Surgery Dominance

Minimally invasive surgery accounted for 62.05% of the Asia Pacific General Surgery Devices market in 2025 and retains the highest growth forecast at 10.05% CAGR. Hospitals report reduced average length of stay by up to two days for laparoscopic cholecystectomy compared with open techniques, reinforcing procurement of high-definition camera heads and insufflators. Robotic platforms augment the MIS advantage with articulated wrist instruments that deliver suturing accuracy previously possible only via open access.

Innovations such as cold atmospheric plasma for wound sterilisation are entering MIS postoperative protocols, broadening device baskets sold alongside core scopes. AI-guided colonoscopy systems now flag polyps in real time, increasing adenoma-detection rates and expanding revenue for compatible processors. Open surgery retains relevance for extensive oncological resections and polytrauma, but these cases increasingly incorporate adjunct technologies such as smoke evacuation and ultrasonic dissection, ensuring all procedure types continue to consume devices.

By Application: Orthopedic Leadership with Bariatric Acceleration

Orthopedic & trauma surgery held 21.05% share in 2025, reflecting the high incidence of lower-limb fractures and joint reconstructions. Device demand clusters around interlocking nails, cannulated screws, and cementless hip stems. Bariatric & gastrointestinal procedures, while smaller in baseline volume, are slated for an 10.64% CAGR on obesity escalation and wider insurance coverage. Sleeve gastrectomy kits, circular staplers, and reinforced sutures dominate order books, while new articulating robotic staplers command premium pricing.

Gynaecology & urology benefit from accurate energy sealing in hysterectomy and prostatectomy, encouraging adoption of bipolar systems. Neurology & spine cases call for precision drills and expandable cages, a segment now leveraging navigation-enabled robotic arms tailored to narrow pedicles. Cardiology & thoracic applications mirror adoption of endoscopic internal-mammary harvest tools and three-dimensional camera scopes. Remaining “other” applications cover endocrine and paediatric procedures that increasingly transition to single-port access, stimulating demand for compliant flexible instruments.

By End User: Hospital Dominance with ASC Growth

Hospitals owned 66.92% of 2025 revenue owing to ICU support and imaging integration required for complex interventions. Teaching centres in China and Japan allocate dedicated robotics theatres, driving bundled procurement of vision carts, staplers, and energy platforms. ASCs post the fastest 10.81% CAGR by focusing on high-turnover cases such as hernia repair and arthroscopy, which lend themselves to half-day recovery protocols. Device preferences here skew toward portable towers, quick-connect power generators, and lightweight anaesthesia machines.

Specialty clinics serve niche areas—fertility, ENT, or cosmetic— and thus purchase smaller volumes but often invest in latest-generation microscopes or laser platforms to differentiate services. Vendors increasingly tailor pay-per-use and managed-service contracts to ASCs, capturing consumables revenue while easing capital constraints that could otherwise stall uptake of premium equipment.

Geography Analysis

China’s 31.55% share stems from large-scale hospital construction and supportive industrial policy. Domestic brands such as MicroPort secured NMPA approval for a single-port robot in 2025, signalling official intent to nurture homegrown champions. Huge western-province catchment areas catalyse interest in 5G remote surgery solutions, ensuring connectivity vendors collaborate with device makers for end-to-end offerings.

India delivers the region’s fastest 10.18% CAGR, underpinned by record public spending, a USD 612 billion healthcare sector goal by 2025, and localisation policies that curtail refurbished imports and thus boost fresh equipment sales. Japanese facilities display early-adopter behaviour, having deployed da Vinci 5 and domestic hinotori systems, but intense scrutiny on cost-effectiveness tempers unit growth in favour of strategic upgrades.

Australia and South Korea sustain mid-single-digit advances through private-insurance coverage and robust surgeon training networks. Rest-of-APAC markets—Thailand, Indonesia, Vietnam—show rising penetration as ASEAN total medical-device value exceeds USD 4.5 billion and harmonisation simplifies cross-border shipments.

Competitive Landscape

The Asia Pacific General Surgery Devices market exhibits moderate fragmentation with established global players competing alongside emerging regional innovators, creating dynamic competitive tensions that drive technological advancement and market expansion. Johnson & Johnson leverages its Ethicon endomechanical catalogue and development of the OTTAVA robot to protect share while embedding NVIDIA AI chips for analytics at the edge. Medtronic doubles down on surgical robotics training studios to lock purchasing paths in early-stage adopters.

Olympus pursues video-imaging superiority, launching its EVIS X1 4K platform and posting 20% annual endoscopy growth in North America before cascading upgrades to APAC. MicroPort and SS Innovations accelerate time-to-market via cost-efficient designs that underprice multinationals by 20-30%, appealing to tier-2 Chinese and Indian hospitals. Partnerships, patent racing in haptics, and recycling initiatives form the axis of competitive manoeuvring over the next five years.

White-space opportunities exist in pediatric surgical robotics, remote surgery capabilities, and sustainable device solutions, with companies pursuing differentiated positioning through specialized applications and technology convergence. Emerging disruptors include AI-powered diagnostic systems like Anaut's Eureka Alpha and WeMed's ETcath robot, which demonstrate how precision technology can create new market categories.

Asia-Pacific General Surgical Devices Industry Leaders

Johnson & Johnson (Ethicon)

Medtronic plc

B. Braun SE

Boston Scientific Corp.

Stryker Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: King George’s Medical University, Lucknow, India, began offering robotic surgery with two indigenous systems—one CSR-funded and one public-private—expanding access in a government setting.

- February 2025: AIIMS Delhi installed a surgical robot in its general-surgery unit, illustrating public-sector adoption.

- September 2024: Medtronic opened a Robotics Experience Studio in Singapore to strengthen professional education across Southeast Asia.

- June 2024: Olympus established an Offshore Development Centre in Hyderabad, India, in partnership with HCLTech to scale R&D capacity.

Asia-Pacific General Surgical Devices Market Report Scope

As per the scope, surgical devices serve a specific purpose during surgery. Surgical devices have generic use, while some specific tools are designed for particular procedures or surgeries. The Asia-Pacific market for general surgical devices is segmented by Product (Handheld Devices, Laparoscopic Devices, Electrosurgical Devices, Wound Closure Devices, Trocars and Access Devices, and Other Products), Application (Gynecology and Urology, Cardiology, Orthopedic, Neurology, and Other Applications), and Geography (China, Japan, India, Australia, South Korea, and the rest of Asia-pacific). The report offers the value (in USD million) for the above segments.

By Product

| Hand-Held Devices |

| Laparoscopic Devices |

| Electrosurgical Devices |

| Wound-Closure Devices |

| Trocars & Access Devices |

| Robotic-Assisted Platforms |

| Single-Use & Other Ancillary Products |

By Procedure Approach

| Open Surgery |

| Minimally Invasive Surgery (MIS) |

By Application

| Gynecology & Urology |

| Cardiology & Thoracic |

| Orthopedic & Trauma |

| Neurology & Spine |

| Bariatric & Gastrointestinal |

| Other Surgical Applications |

By End User

| Hospitals |

| Ambulatory Surgical Centres |

| Specialty Clinics |

By Country

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Product | Hand-Held Devices |

| Laparoscopic Devices | |

| Electrosurgical Devices | |

| Wound-Closure Devices | |

| Trocars & Access Devices | |

| Robotic-Assisted Platforms | |

| Single-Use & Other Ancillary Products | |

| By Procedure Approach | Open Surgery |

| Minimally Invasive Surgery (MIS) | |

| By Application | Gynecology & Urology |

| Cardiology & Thoracic | |

| Orthopedic & Trauma | |

| Neurology & Spine | |

| Bariatric & Gastrointestinal | |

| Other Surgical Applications | |

| By End User | Hospitals |

| Ambulatory Surgical Centres | |

| Specialty Clinics | |

| By Country | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the projected value of the Asia Pacific General Surgery Devices market by 2031?

Forecasts place the market at USD 6.87 billion by 2031 on a 9.12% CAGR trajectory.

Which product segment currently generates the highest revenue?

Laparoscopic devices led with 26.12% share in 2025.

Which procedure approach is growing the fastest?

Minimally invasive surgery posts a 10.05% CAGR to 2031.

Which country shows the fastest market growth through 2031?

India leads with a 10.18% CAGR, driven by expanded public spending and localisation efforts.

How are ambulatory surgical centres affecting device demand?

ASCs, growing at 10.81% CAGR, favour compact, workflow-oriented equipment and managed-service contracts, shifting procurement patterns.

What key factor restrains rapid adoption of new surgical devices in APAC?

Complex, multi-layered regulatory approval pathways prolong time-to-market, reducing near-term uptake of advanced systems.

Page last updated on: