Thoracic Surgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

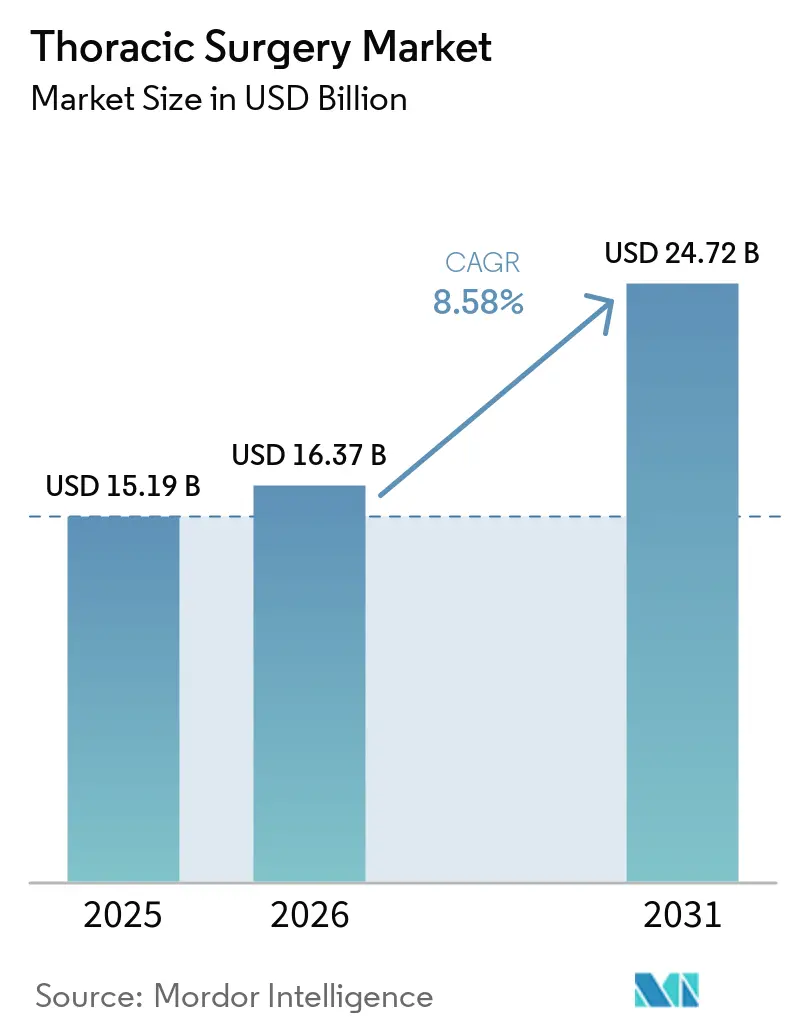

| Market Size (2026) | USD 16.37 Billion |

| Market Size (2031) | USD 24.72 Billion |

| Growth Rate (2026 - 2031) | 8.58% CAGR |

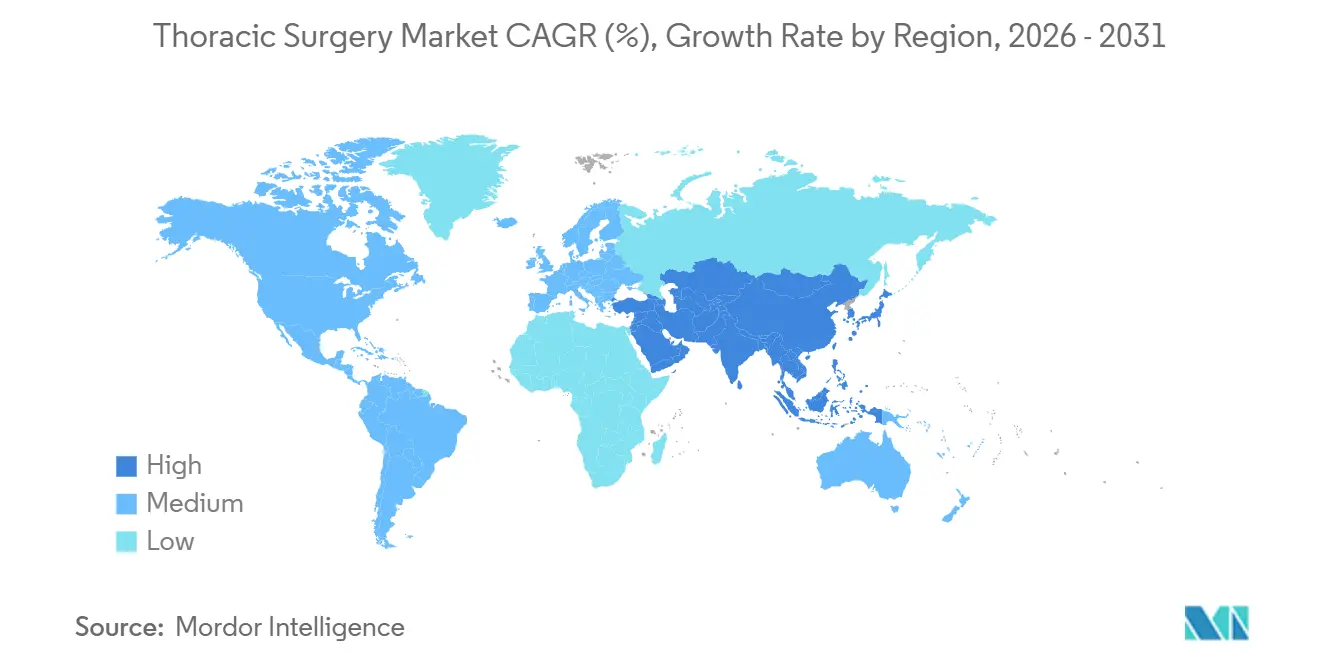

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

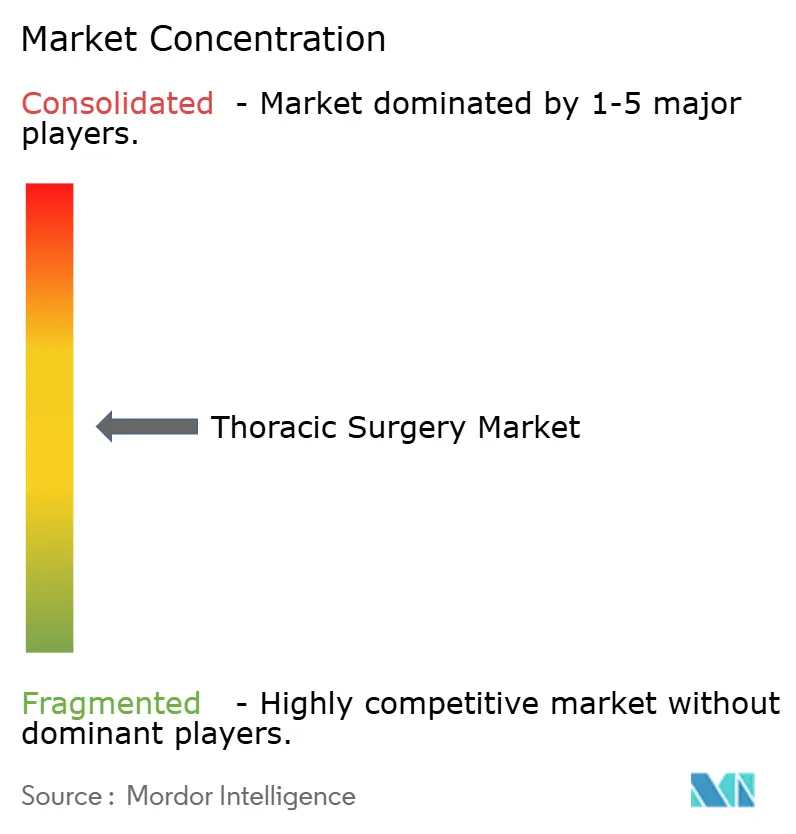

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thoracic Surgery Market Analysis by Mordor Intelligence

The Thoracic Surgery Market size is expected to grow from USD 15.19 billion in 2025 to USD 16.37 billion in 2026 and is forecast to reach USD 24.72 billion by 2031 at 8.58% CAGR over 2026-2031.

The thoracic surgery market is expanding because lung, esophageal, and other thoracic conditions continue to create a large surgical workload across both planned and urgent care settings. The thoracic surgery market is also benefiting from the steady move from open thoracotomy to video-assisted and robotic techniques, as hospitals use these approaches to shorten recovery time and improve procedural control. A wider push toward ambulatory care pathways is opening new room for case migration in selected procedures, which is changing purchasing patterns for instruments, imaging systems, and service support. Competitive activity remains focused on robotic platform expansion, system-linked consumables, navigation tools, and training services, while adoption still depends on whether hospitals can justify capital spending and secure enough skilled surgeons. The thoracic surgery market therefore sits in a position where demand remains strong, but the pace of adoption still depends on labor availability, budget capacity, and evidence that newer workflows can be scaled safely.

Key Report Takeaways

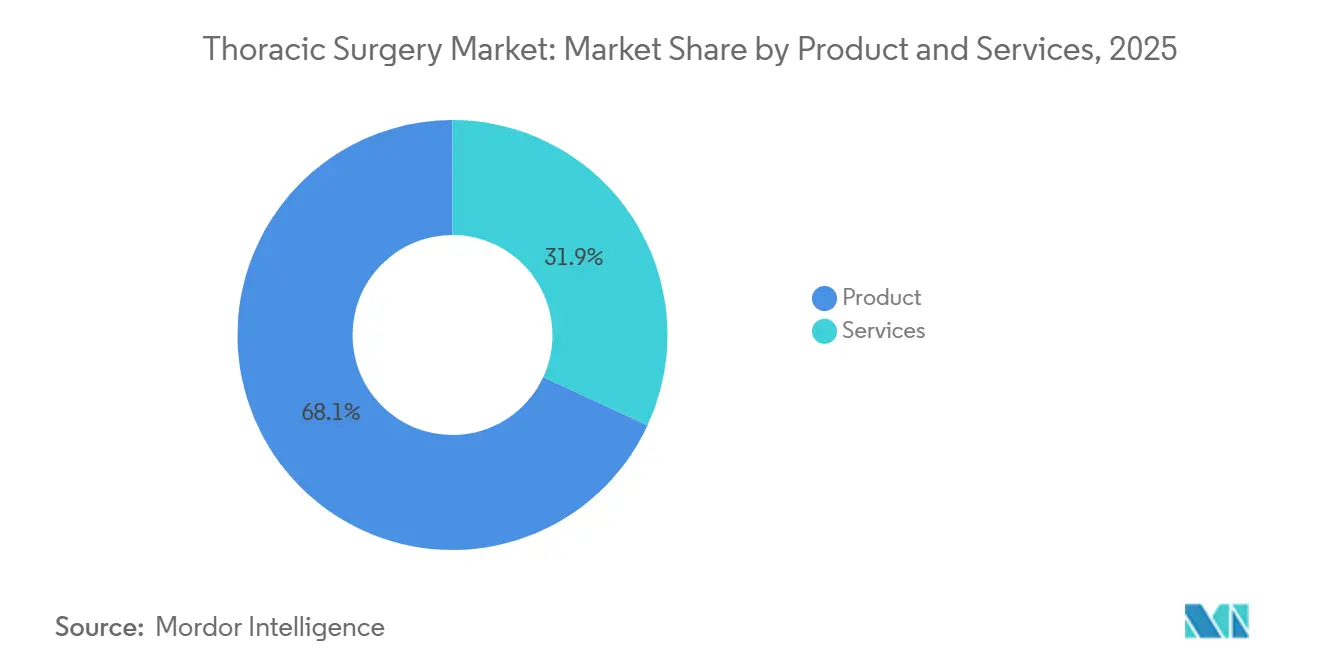

- By product and services, product segment held 68.13% of revenue in 2025, while services are projected to grow at 8.78% CAGR through 2031.

- By procedure type, VATS accounted for 49.21% of revenue in 2025, while RATS is forecast to expand at 10.42% CAGR through 2031 in the thoracic surgery market.

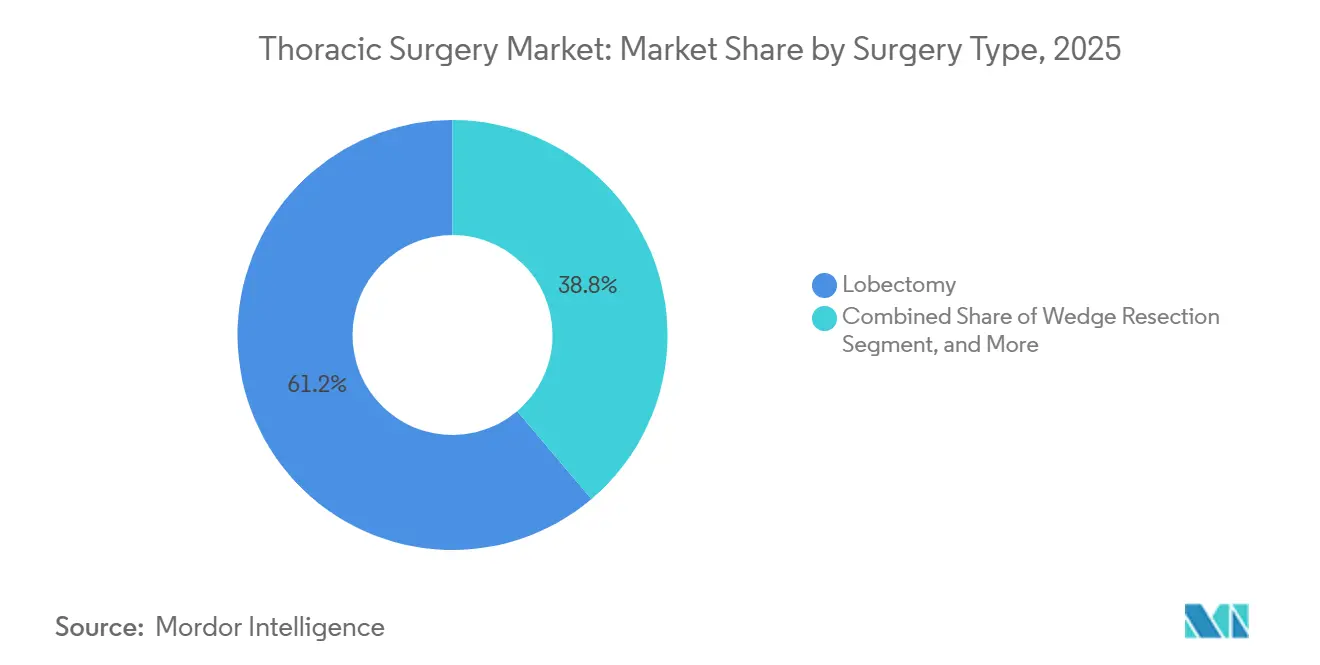

- By surgery type, lobectomy held 61.16% of revenue in 2025, while Pneumonectomy is projected to grow at 9.83% CAGR through 2031.

- By medical condition, esophageal cancer represented 35.64% of revenue in 2025 in the thoracic surgery market, while Pneumothorax is forecast to grow at 10.98% CAGR through 2031.

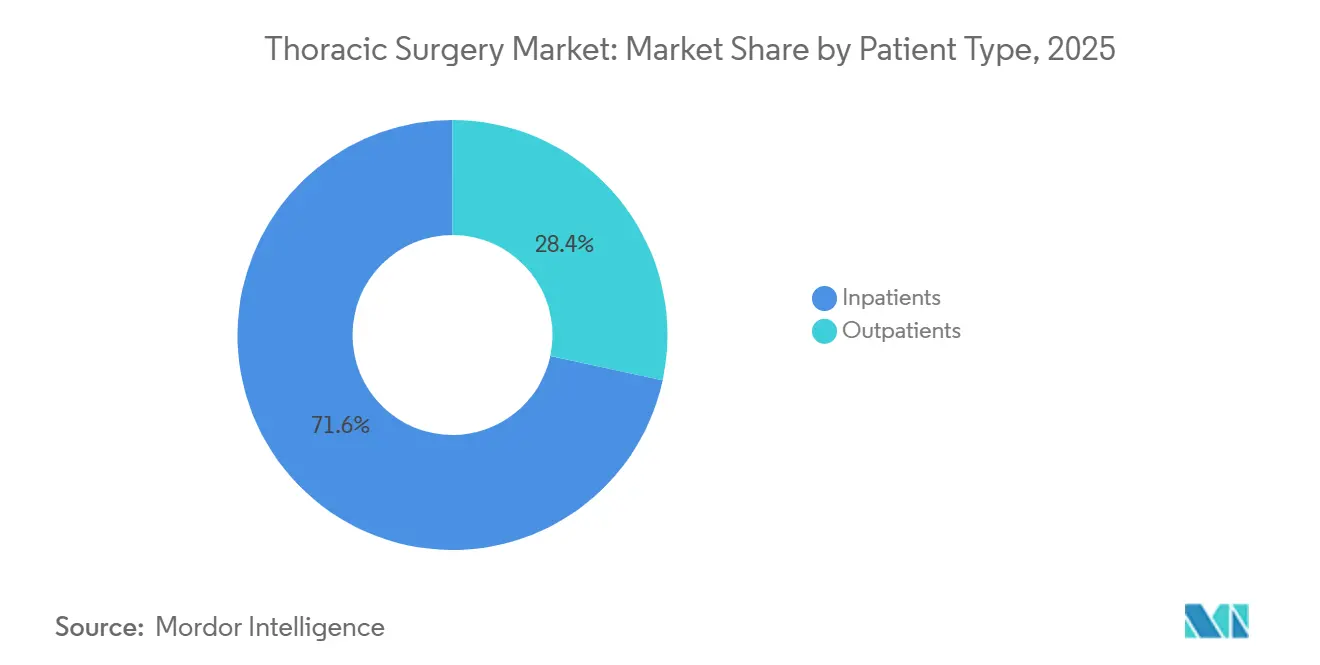

- By patient type, inpatients accounted for 71.63% of revenue in 2025, while outpatients are projected to expand at 9.06% CAGR through 2031.

- By surgical approach, the standard open approach held 64.11% of revenue in 2025, while the minimally invasive approach is projected to grow at 9.31% CAGR through 2031.

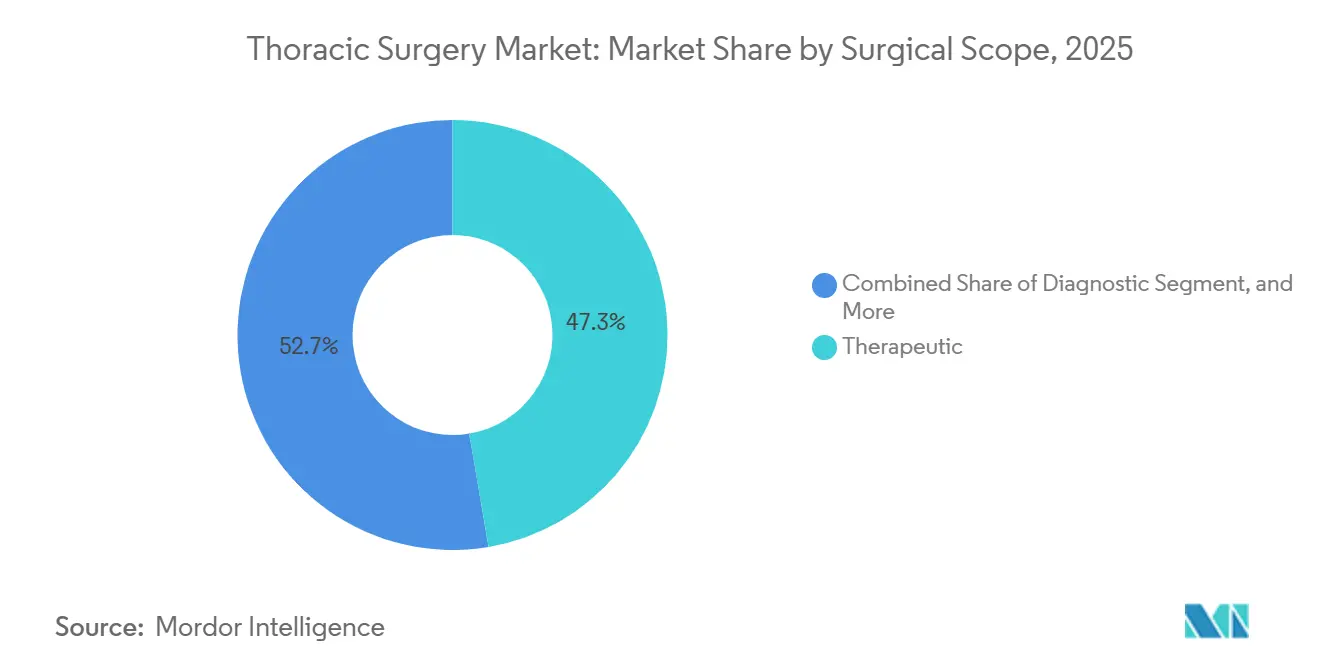

- By surgical scope, therapeutic procedures accounted for 47.32% of revenue in 2025 in the thoracic surgery market, while diagnostic procedures are forecast to grow at 10.01% CAGR through 2031.

- By end user, hospitals held 49.23% of revenue in 2025, while ambulatory surgical centres / outpatient centres are projected to grow at 11.12% CAGR through 2031.

- By geography, North America accounted for 39.03% of revenue in 2025, while Asia-Pacific is projected to expand at 8.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thoracic Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Thoracic Disease Burden | +2.1% | Global, most acute in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Shift Toward Minimally Invasive Thoracic Surgery | +1.8% | North America and Europe, with early adoption gains in Asia-Pacific | Medium term (2-4 years) |

| Adoption of Robotics and Image Guidance | +2.4% | North America and Europe, with early uptake in Asia-Pacific | Medium term (2-4 years) |

| Expansion of Ambulatory Thoracic Care Pathways | +1.2% | North America, with early gains in Germany and Australia | Short term (≤ 2 years) |

| OR Throughput Pressure from Reprocessing and Turnover Constraints | +0.7% | North America and Europe | Short term (≤ 2 years) |

| Aging Population and Complex Comorbidity Burden | +1.2% | Japan, South Korea, Italy, Germany, with spillover to MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Thoracic Disease Burden

The thoracic surgery market is being supported by a disease mix that continues to generate demand across cancer care, emergency care, and complex hospital-based treatment. GLOBOCAN findings published in 2025 reported 2.48 million incident tracheal, bronchial, and lung cancer cases and 1.82 million deaths in 2022, which keeps lung resection volumes central to the care pathway.[1]BMC Cancer, “Global Burden of Respiratory System Cancers in 2022 and 2050, Incidence and Mortality Estimates from GLOBOCAN,” BMC Cancer, link.springer.com The same study showed that male incident lung cancer cases are projected to rise from 1.6 million to 2.95 million by 2050, while female cases are projected to increase 83.3% over the same period. Esophageal cancer adds another layer of demand because 511,054 new cases and 445,391 deaths were recorded globally in 2022, and 75% of cases were concentrated in Asia. The thoracic surgery market also remains exposed to pneumothorax, empyema, and mediastinal disease, which keeps surgical workloads active beyond oncology alone. This combination means hospitals are not dealing with a single source of growth, but with several disease pathways that all require operating room time, instruments, imaging support, and trained teams.

Shift Toward Minimally Invasive Thoracic Surgery

The thoracic surgery market is moving further toward minimally invasive care because clinical practice is no longer centered only on open thoracotomy in large referral centers. A National Cancer Database analysis covering 301,123 oncologic lung resections showed that RATS exceeded VATS case volume in the United States by 2019, and by 2021 RATS represented 65.4% of all minimally invasive cases.[2]National Cancer Database Study, “National Adoption of Robotic-Assisted Thoracoscopic Surgery for Oncologic Lung Resections,” PubMed, pubmed.ncbi.nlm.nih.gov That change matters because it shows surgeons are not only trying robotic tools, but are making them part of routine case selection in a major care market. Academic programs have moved faster than community centers, and metropolitan hospitals have moved faster than rural hospitals, which points to a diffusion pattern that can continue as pricing and training barriers ease. A 2026 multicenter cohort study from the ATS of Milan found that RATS delivered perioperative advantages over VATS in recovery and conversion outcomes, which strengthens adoption beyond flagship teaching hospitals. The thoracic surgery market is therefore shifting not only because the tools are newer, but because the clinical case for broader use has become harder for hospitals to ignore.

Adoption of Robotics and Image Guidance

The thoracic surgery market is also advancing through deeper integration between robotic systems, navigation software, and image-guided diagnostic workflows. In March 2025, Johnson and Johnson MedTech received FDA 510(k) clearance for MONARCH QUEST, which added an NVIDIA accelerated computing platform and delivered 260% greater real-time computational power for robotic bronchoscopy navigation.[3]Johnson & Johnson MedTech, “Johnson & Johnson MedTech Announces Clearance of MONARCH QUEST for Enhanced Robotic-Assisted Bronchoscopy,” Johnson & Johnson, jnj.com That step is important because bronchoscopy is becoming more tightly linked to downstream resection planning, rather than sitting apart as a separate diagnostic event. In April 2025, Intuitive Surgical received FDA clearance for the SP SureForm 45, the first fully wristed stapler designed for single-port robotic surgery across thoracic, colorectal, and urologic use, which shows how platform vendors are extending procedure-specific accessory portfolios. The thoracic surgery market is responding to this shift because hospitals increasingly value systems that connect access, imaging, stapling, and workflow support within one purchasing logic. As a result, growth is not coming only from more procedures, but also from a broader revenue mix tied to each robotic case.

Expansion of Ambulatory Thoracic Care Pathways

The thoracic surgery market is beginning to see a wider outpatient opportunity, although that opportunity is still selective and concentrated in lower-complexity cases. The move matters because wedge resections, pleural interventions, and selected segmentectomies can shift into settings that place more pressure on device efficiency and turnaround time. This change also affects what providers buy, since lighter instrumentation, workflow support, and service-linked training become more relevant when discharge windows are shorter. In North America and selected European centers, enhanced recovery protocols are helping providers test same-day or next-day pathways for carefully selected patients. The thoracic surgery market may not see a full migration of core resection volume into ambulatory settings, but the direction of travel is clear in cases where clinical risk, staffing, and reimbursement allow it. That makes ambulatory readiness an operational question for manufacturers as much as a care-delivery question for hospitals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Thoracic Systems | -1.9% | Asia-Pacific, Middle East and Africa, and South America, with secondary pressure in Europe | Long term (≥ 4 years) |

| Shortage of Skilled Thoracic Surgeons | -1.4% | Global, most acute in Middle East and Africa, Southeast Asia, and parts of Asia-Pacific | Long term (≥ 4 years) |

| Regulatory and Evidence Burden for New Devices | -0.9% | North America and Europe | Medium term (2-4 years) |

| Capital Budget Prioritization Versus Competing Surgical Specialties | -0.6% | Asia-Pacific, Middle East and Africa, emerging markets, and community hospitals across regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Thoracic Systems

The thoracic surgery market still faces a major adoption ceiling because advanced robotic systems demand a capital outlay that many hospitals cannot absorb easily. Platform acquisition costs remain at USD 1.5-3 million per system, and annual maintenance plus consumables add another USD 150,000-300,000 to the operating burden. A 2024 review in the Annals of Esophagus found that robotic-assisted minimally invasive esophagectomy carried 9% higher direct surgical costs than non-robotic alternatives. The same review noted that outpatient robotic procedures were financially unfavorable under current reimbursement structures, which shows why smaller providers still struggle to justify platform ownership. This creates a two-speed pattern where high-volume academic hospitals move ahead, while lower-volume centers continue to rely on VATS or open surgery for cost reasons. The thoracic surgery market can widen only gradually under these conditions, unless pricing models, leasing arrangements, or shared platform access reduce the burden on mid-tier hospitals.

Shortage of Skilled Thoracic Surgeons

The thoracic surgery market is also constrained by a specialist workforce that is not expanding at the same pace as procedural demand. The Society of Thoracic Surgeons has estimated that 900 cardiothoracic surgeons are expected to retire by 2035, while demand is projected to rise 20%, leaving enough qualified operators to cover only 69% of expected cases, according to the user-supplied draft. This matters because the issue is not simply the number of hospitals with equipment, but the number of surgeons able to use advanced systems safely and consistently. In South Korea, 95 of 107 cardiothoracic trainees resigned in 2024 during a dispute over medical school policy, which showed how quickly training pipelines can weaken in a specialty already treated as undersupplied. The thoracic surgery market may see some mitigation through telenavigation, simulation-based training, and robotic tools that improve precision, but those measures do not replace the need for a stable specialist base. If staffing pressure persists, hospitals may delay program expansion even when there is clear patient demand and available device technology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product and Services: Robotic Platforms Define the Next Revenue Cycle

Product held 68.13% of revenue in 2025, which shows that the thoracic surgery market still draws most of its value from equipment, instruments, and procedural consumables rather than stand-alone service lines. Surgical instruments and accessories support this position because thoracic resections require repeated use of staplers, energy devices, graspers, and retraction tools across open and minimally invasive cases. Energy and stapling devices remain especially important because even a standard lobectomy can involve several sequential firing and sealing steps in one operation. Endoscopes and imaging systems are also moving higher in value as 4K visualization, fluorescence support, and image-led identification features become more integrated into operative planning and execution. In April 2025, Intuitive Surgical expanded this product-side logic through FDA clearance of the SP SureForm 45, a fully wristed stapler built for single-port robotic surgery.

Services are projected to grow at 8.78% CAGR through 2031, which makes this the fastest-moving side of the thoracic surgery market size within this segmentation. That pace reflects a steady shift toward preoperative planning, intraoperative navigation, postoperative monitoring, teleconsultation, and structured training support. Hospitals are showing more willingness to pay for services that reduce variation, shorten room turnover, and help surgeons adopt advanced workflows with fewer disruptions. Training is a notable part of that change because each new robotic indication creates a commercial need for credentialing, simulation, and procedural support before full-scale rollout. The thoracic surgery industry is therefore seeing service revenue move closer to the device sale, rather than sitting outside the commercial model. Over time, this makes recurring support income more important to vendors that once depended mainly on capital placement and disposable usage.

By Procedure Type: RATS Momentum Challenges VATS Incumbency

VATS held 49.21% of the thoracic surgery market share in 2025, which confirms that the thoracic surgery market still relies heavily on an established minimally invasive technique with a broad surgeon base. Its lead is supported by familiarity, a strong clinical evidence base, and compatibility with operating rooms that do not yet have advanced robotic capacity. Open surgery remains necessary in selected cases with dense adhesions, unstable anatomy, or urgent control requirements, while endoscopic thoracic surgery continues to support bronchoscopy-driven diagnosis and early lesion sampling. These patterns show that procedure choice still depends on case complexity, staffing, infrastructure, and budget rather than a single universal standard. Even so, the center of gravity in procedure planning has started to move.

RATS is forecast to grow at 10.42% CAGR through 2031, which makes it the strongest growth engine in this procedure mix. A National Cancer Database study showed that RATS overtook VATS in U.S. case count by 2019, and by 2021 it represented 65.4% of minimally invasive oncologic lung resections. A 2026 multicenter study from Milan also found perioperative advantages for RATS over VATS in recovery and conversion outcomes. The thoracic surgery market is reacting to this evidence because hospitals can now frame robotic expansion as both a clinical and economic decision, especially in complex resections. The thoracic surgery industry is therefore entering a period where VATS remains the volume base, but RATS shapes the higher-growth and higher-value direction of procedural spending.

By Surgery Type: Lobectomy Remains the Revenue Anchor, Pneumonectomy Grows on Complexity

Lobectomy held 61.16% of revenue in 2025, which gives it the leading position in this surgery mix and makes it a major anchor of the thoracic surgery market size. The segment stays dominant because lobar resection remains standard care for a large share of stage I and II non-small cell lung cancer. A 2024 study in the Journal of Cardiothoracic Surgery found that VATS can deliver long-term survival outcomes comparable to RATS in lobectomy, which supports continued high procedural volume through established thoracoscopic pathways. Wedge resection and segmental resection remain important for earlier lesions and selective anatomical preservation, while pleurectomy stays relevant in pleural disease and recurrent pneumothorax. This means the largest surgery type is not only widespread, but also linked to clinical pathways that are already well embedded in hospital practice.

Pneumonectomy is projected to grow at 9.83% CAGR through 2031, even though absolute case volume remains lower than lobectomy and wedge procedures. Its growth rate reflects the fact that complex and locally advanced disease still presents in settings where lesser resections are not possible. A 2024 study reported that minimally invasive pneumonectomy reached 27% of institutional cases, including 19% by VATS and 8% by RATS, which shows that even highly complex resections are starting to shift into less invasive formats. Device use per case is also high because major vascular division and extensive stapling are common in these operations. The thoracic surgery market therefore receives a disproportionate revenue contribution from pneumonectomy relative to its volume because complexity raises both instrument intensity and platform value.

By Medical Condition: Esophageal Cancer's Market Value Exceeds its Case Share

Esophageal cancer held 35.64% of revenue in 2025, which made it the largest medical condition segment in the thoracic surgery market. That ranking may appear counterintuitive beside the global incidence of lung cancer, but the revenue pattern reflects the heavier resource use associated with esophagectomy. The procedure often combines thoracic and abdominal phases, requires multiple stapling and sealing devices, and can involve long operating times when robotic access is used. A 2024 review found that robotic-assisted esophagectomy had 9% higher direct surgical costs than open alternatives, while total hospitalization costs moved closer because complications and ICU stays were lower. This makes esophageal cases highly valuable on a per-procedure basis, even when total case counts are lower than in lung cancer.

Pneumothorax is projected to grow at 10.98% CAGR through 2031, which makes it the fastest-growing condition category in this segmentation. The rise reflects greater use of video-assisted pleurodesis and a wider willingness to intervene surgically rather than rely only on conservative drainage in selected patients. Lung cancer still generates the broadest raw procedure volume, but its revenue is spread across more operation types and clinical pathways, which lowers average value per case in this segment view. Mediastinal tumors and empyema remain smaller segments, yet they carry specific device needs that can still support premium visualization and access tools in confined operative fields. The thoracic surgery market thus shows a clear difference between case volume leadership and revenue leadership, and that difference is most visible in the contrast between lung and esophageal surgery.

By Patient Type: Inpatient Dominance Masks the Outpatient Acceleration

Inpatients accounted for 71.63% of revenue in 2025, which shows that the thoracic surgery market is still mainly rooted in hospital admission pathways. Lobectomy, esophagectomy, complex resections, and patients requiring chest drainage or respiratory support continue to need structured postoperative monitoring that is difficult to compress into same-day discharge in most settings. Inpatient care also remains central where hospitals lack mature enhanced recovery protocols or where payer systems still support longer stays. This keeps bed-based infrastructure, respiratory care, and surgical nursing support tightly linked to the revenue base of thoracic care. The dominance of inpatients, therefore, reflects both clinical need and the uneven spread of pathway modernization across regions.

Outpatients are projected to grow at 9.06% CAGR through 2031, making them the fastest-moving patient pathway in the thoracic surgery market. Growth is being supported by selected wedge resections, pleural procedures, and lower-acuity interventions that fit enhanced recovery protocols more easily than major resections. The shift is stronger in North America and parts of Europe, where hospitals and ambulatory centers have started to align discharge planning, pain control, and follow-up more tightly around shorter stays. This movement changes the commercial mix because providers in outpatient settings tend to value efficiency, workflow support, and procedure standardization more intensely. The thoracic surgery market is therefore not leaving inpatient care behind, but it is steadily widening the share of procedures that can be handled in lower-cost settings when patient selection is appropriate.

By Surgical Approach: Open Surgery's Persistence Signals Transition, Not Stagnation

Standard open approach held 64.11% of revenue in 2025, which shows that the thoracic surgery market is still in transition rather than in full conversion to minimally invasive care. Open thoracotomy remains necessary in cases with dense pleural adhesions, prior radiation changes, chest wall involvement, or unstable emergencies that require direct access and rapid control. Open access also remains common in lower-resource systems where robotic platforms and advanced thoracoscopic capability are still limited. This means open surgery persists for practical and clinical reasons, not simply because hospitals are slow to change. Its large share is therefore a sign of case mix and infrastructure reality more than resistance to innovation.

The minimally invasive approach is projected to grow at 9.31% CAGR through 2031, giving it the fastest trajectory in this segmentation. The growth is tied to wider RATS uptake, continued VATS use, and stronger evidence that less invasive pathways can support recovery and lower conversion risk in selected patients. Importantly, open surgery revenue is not necessarily falling in absolute terms because many shared instruments and energy devices are used across both approaches. The thoracic surgery market is instead adding a larger minimally invasive layer on top of a still-relevant open base. Over the forecast period, that faster expansion should narrow the gap between open and minimally invasive revenue even if open techniques remain essential for selected cases.

By Surgical Scope: Therapeutic Leads, Diagnostic Accelerates on Robotic Bronchoscopy

Therapeutic procedures held 47.32% of revenue in 2025, which kept them at the center of the thoracic surgery market because resection and reconstruction continue to absorb the highest case complexity. These procedures include the operations that typically require the greatest use of stapling, energy, imaging support, and postoperative care. Emergency scope procedures remain a smaller share, but they still create meaningful device demand through chest drainage, pleural decompression, and urgent VATS-based control in trauma or acute thoracic events. This gives the segment a broad clinical spread, from planned cancer operations to high-intensity acute intervention. Therapeutic work, therefore, remains the principal revenue foundation of the category.

Diagnostic procedures are projected to grow at 10.01% CAGR through 2031, which makes them the fastest-growing scope category in the thoracic surgery market size. This acceleration is linked to robotic bronchoscopy and related pathways that move suspicious lung nodules from detection to biopsy and then to surgery with less fragmentation. In March 2025, Johnson and Johnson MedTech received clearance for MONARCH QUEST, which strengthened the computational and navigation side of robotic bronchoscopy. That matters because diagnostic bronchoscopy is becoming more valuable when it improves staging, speeds treatment planning, and fits into a unified thoracic workflow. The thoracic surgery market is therefore seeing diagnostic activity become a commercial growth driver in its own right, rather than only a feeder stage before therapeutic surgery.

By End User: Hospitals Anchor Volume, ASCs Capture Growth

Hospitals held 49.23% of revenue in 2025, which kept them as the largest end-user base in the thoracic surgery market. Their position is supported by tumor boards, thoracic anesthesia teams, ICU backup, and the ability to manage complex resections, cardiothoracic crossover cases, and higher-acuity complications. Hospitals are also the main setting for robotic programs that need sustained procedural volume, credentialed teams, and cross-specialty support. Specialty clinics hold a smaller share and remain more relevant in bronchoscopy-based diagnosis and pleural intervention than in major resection programs. This means hospitals continue to define the center of operational gravity for the category.

Ambulatory surgical centers/outpatient centers are projected to grow at 11.12% CAGR through 2031, which makes them the fastest-growing end-user segment in the thoracic surgery market. Their rise reflects a gradual shift of selected lower-complexity procedures into settings that can operate with shorter stays and lower facility costs. For manufacturers, this expands the need for equipment and consumables that fit tighter turnover windows, smaller footprints, and simpler service models. The thoracic surgery industry is likely to treat this channel as a strategic commercial priority because the site of care is becoming a more important determinant of purchasing behavior. As a result, the end-user mix is widening even though hospitals will continue to dominate advanced thoracic resection volume.

Geography Analysis

North America held 39.03% of the thoracic surgery market share in 2025, which kept it as the largest regional contributor by revenue. The region benefits from mature reimbursement systems, a dense concentration of academic thoracic centers, and broad access to robotic and thoracoscopic infrastructure. It is also further along in linking diagnosis, surgery, and postoperative pathway management into structured care models for lung and esophageal disease. This means regional growth is being shaped more by procedural upgrading and care setting shifts than by a simple rise in disease incidence. The thoracic surgery market in North America remains important because new technologies tend to reach commercial scale here earlier than in most other regions.

Europe remained the second-largest regional block, led by Germany, the United Kingdom, and France in the user-supplied draft. Germany has continued to expand robotic thoracic activity, and the University Hospital of Heidelberg initiated robotic-assisted bronchoscopy in March 2025 as part of preparation for national lung cancer screening. A 2026 study based on France's PMSI administrative database found a 15.6% year-over-year rise in robotic hospital stays between 2021 and 2022, with thoracic surgery accounting for 7% of all robotic procedures nationally. Regulatory compliance under EU MDR 2017/745 continues to favor companies that already have strong certification capacity and post-market support structures. The thoracic surgery market in Europe, therefore, combines healthy technology adoption with a regulatory environment that can slow smaller entrants.

Asia-Pacific is projected to grow at 8.92% CAGR through 2031, giving it the fastest regional expansion in the thoracic surgery market size. China is a major driver because surgical robot procurement reached CNY 691 million in Q1 2025, equal to USD 95 million, after a 43% year-over-year increase in the user-supplied draft. Domestic manufacturers are widening access by pricing systems at 50-70% of imported alternatives, which supports adoption beyond top-tier city hospitals in the user-supplied draft. India is opening more room for cancer surgery volumes through broader health coverage in the user-supplied draft, while Japan has expanded reimbursement support for robotic-assisted lobectomy in the user-supplied draft. South America, the Middle East, and Africa remain smaller markets, but private hospital groups in Brazil, Saudi Arabia, and the United Arab Emirates are using thoracic robotics as a differentiation tool, while workforce shortages across parts of Africa continue to limit addressable volume.

Competitive Landscape

The thoracic surgery market shows moderate concentration in the product tier and much broader fragmentation in services and regional instrument supply. A small group of global medtech companies, including Intuitive Surgical, Medtronic, Johnson and Johnson, and Olympus, controls a large share of platform and advanced instrument revenue in the user-supplied draft. At the same time, a long tail of regional suppliers competes in procedure-specific instruments, reusable tools, and lower-cost access products. This creates a market where competitive strength comes from system placement, clinical evidence, service support, and recurring consumable sales rather than from one-time capital deals alone. The thoracic surgery market is therefore competitive at several layers, but not in the same way across all product categories.

One clear strategy is ecosystem lock-in through system-linked accessories and workflow expansion. Intuitive Surgical strengthened that position in April 2025 through clearance of the SP SureForm 45, a fully wristed stapler purpose-built for single-port robotic surgery. Another strategy is multi-specialty platform expansion, which helps vendors spread capital value across more hospital departments and defend purchasing decisions over time. Medtronic moved in that direction when the Hugo RAS system received FDA clearance in December 2025 for urologic surgery, with thoracic relevance still under clinical evaluation in the user-supplied draft. Johnson and Johnson MedTech also added to the competitive pressure in March 2025 with MONARCH QUEST, strengthening the image-guided bronchoscopy side of the pathway.

Emerging challengers are focusing on lower capital intensity and more flexible deployment. CMR Surgical has been expanding Versius in European regional centers as a lower-cost robotic option in the user-supplied draft, while domestic Chinese manufacturers are pushing robotic access into hospitals that previously could not justify imported systems. Olympus is also moving through endoluminal robotics and endoscopy-linked capabilities, which could influence future access pathways in thoracic procedures in the user-supplied draft. The thoracic surgery market still leaves room for growth in single-use flexible endoscopes, AI-guided navigation for community programs, and remote supervision tools for underserved areas. Competitive advantage will likely remain strongest with companies that can combine device performance, training, regulatory capacity, and recurring support into a practical hospital offering.

Thoracic Surgery Industry Leaders

B. Braun Melsungen AG

Boston Scientific Corporation

CONMED Corporation

Medtronic

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Johnson & Johnson disclosed pivotal study results for the OTTAVA Robotic Surgical System, confirming safety and performance in Roux-en-Y gastric bypass procedures across a prospective multicenter trial; the system's multi-specialty design positions it as a future entrant in thoracic robotics upon FDA submission.

- April 2026: Getinge AB acquired Pennamed, a UK-based distributor of endoscopic consumables serving NHS and independent healthcare providers, broadening Getinge's commercial reach in endoscope reprocessing and thoracoscopy workflow supply in the United Kingdom.

- December 2025: Medtronic received FDA clearance for the Hugo RAS system for urologic surgical procedures, becoming the first large medtech company positioned to compete with Intuitive in the US robotic surgery market, with thoracic and general surgery indications under active clinical evaluation.

Global Thoracic Surgery Market Report Scope

The thoracic surgery market refers to the global industry encompassing surgical procedures performed on the chest cavity, including the lungs, esophagus, mediastinum, and pleura. It covers both the clinical services and the devices used, driven by rising incidences of thoracic diseases and advancements in minimally invasive and robotic techniques.

The market is segmented by products and services, which include surgical instruments and accessories, endoscopes and imaging systems, energy and stapling devices, and robotic platforms, alongside services such as preoperative planning, intraoperative navigation, postoperative monitoring and follow-up, teleconsultation, and surgical training and support. By procedure type, it spans open thoracic surgery, video-assisted thoracoscopic surgery (VATS), robotic-assisted thoracic surgery, endoscopic thoracic surgery, and other specialized procedures. By surgery type, it includes lobectomy, wedge resection, pneumonectomy, pleurectomy, segmental resection, and other thoracic surgeries. By medical condition, the market addresses lung cancer, esophageal cancer, mediastinal tumors, pneumothorax, empyema, and other thoracic disorders. By patient type, it is divided into inpatients and outpatients. By surgical approach, it covers minimally invasive and standard open approaches. By surgical scope, it includes diagnostic, therapeutic, and emergency procedures. Finally, by end user, the market serves hospitals, ambulatory surgical centers/outpatient centers, specialty clinics, and other healthcare providers.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Product | Surgical Instruments and Accessories |

| Endoscopes and Imaging Systems | |

| Energy and Stapling Devices | |

| Robotic Platforms | |

| Services | Preoperative Planning Services |

| Intraoperative Navigation Services | |

| Postoperative Monitoring And Follow-Up Services | |

| Teleconsultation Services | |

| Surgical Training And Support Services |

| Open Thoracic Surgery |

| Video-Assisted Thoracoscopic Surgery |

| Robotic-Assisted Thoracic Surgery |

| Endoscopic Thoracic Surgery |

| Other Thoracic Procedures |

| Lobectomy |

| Wedge Resection |

| Pneumonectomy |

| Pleurectomy |

| Segmental Resection |

| Other Surgery Types |

| Lung Cancer |

| Esophageal Cancer |

| Mediastinal Tumors |

| Pneumothorax |

| Empyema |

| Other Thoracic Conditions |

| Inpatients |

| Outpatients |

| Minimally Invasive Approach |

| Standard Open Approach |

| Diagnostic |

| Therapeutic |

| Emergency |

| Hospitals |

| Ambulatory Surgical Centers/Outpatient Centre |

| Specialty Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product And Services | Product | Surgical Instruments and Accessories |

| Endoscopes and Imaging Systems | ||

| Energy and Stapling Devices | ||

| Robotic Platforms | ||

| Services | Preoperative Planning Services | |

| Intraoperative Navigation Services | ||

| Postoperative Monitoring And Follow-Up Services | ||

| Teleconsultation Services | ||

| Surgical Training And Support Services | ||

| By Procedure Type | Open Thoracic Surgery | |

| Video-Assisted Thoracoscopic Surgery | ||

| Robotic-Assisted Thoracic Surgery | ||

| Endoscopic Thoracic Surgery | ||

| Other Thoracic Procedures | ||

| By Surgery Type | Lobectomy | |

| Wedge Resection | ||

| Pneumonectomy | ||

| Pleurectomy | ||

| Segmental Resection | ||

| Other Surgery Types | ||

| By Medical Condition | Lung Cancer | |

| Esophageal Cancer | ||

| Mediastinal Tumors | ||

| Pneumothorax | ||

| Empyema | ||

| Other Thoracic Conditions | ||

| By Patient Type | Inpatients | |

| Outpatients | ||

| By Surgical Approach | Minimally Invasive Approach | |

| Standard Open Approach | ||

| By Surgical Scope | Diagnostic | |

| Therapeutic | ||

| Emergency | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers/Outpatient Centre | ||

| Specialty Clinics | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for thoracic surgery revenue?

The thoracic surgery market is forecast to reach USD 24.72 billion by 2031 from USD 16.37 billion in 2026, growing at 8.58% CAGR over 2026-2031.

Which procedure type is expanding the fastest in thoracic care?

RATS is the fastest-growing procedure type with a projected 10.42% CAGR through 2031, while VATS remained the largest procedure segment in 2025.

Why does esophageal cancer generate such a large revenue share in thoracic surgery?

Esophageal cancer led the medical condition mix with 35.64% share in 2025 because esophagectomy usually requires more devices, more operative steps, and longer platform use per case.

Which care setting is growing the fastest for thoracic procedures?

Ambulatory surgical centres / outpatient centres are projected to grow at 11.12% CAGR through 2031, reflecting gradual migration of selected lower-complexity procedures.

Which region is growing the fastest for thoracic surgery demand?

Asia-Pacific is the fastest-growing region with an 8.92% CAGR through 2031, supported by wider robotic adoption and expanding access in large healthcare systems.

What is the biggest barrier to broader robotic adoption in thoracic surgery?

High platform cost remains the main barrier, with system prices at USD 1.5-3 million and annual maintenance plus consumables at USD 150,000-300,000.

Page last updated on: