Minimally Invasive Thoracic Surgery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

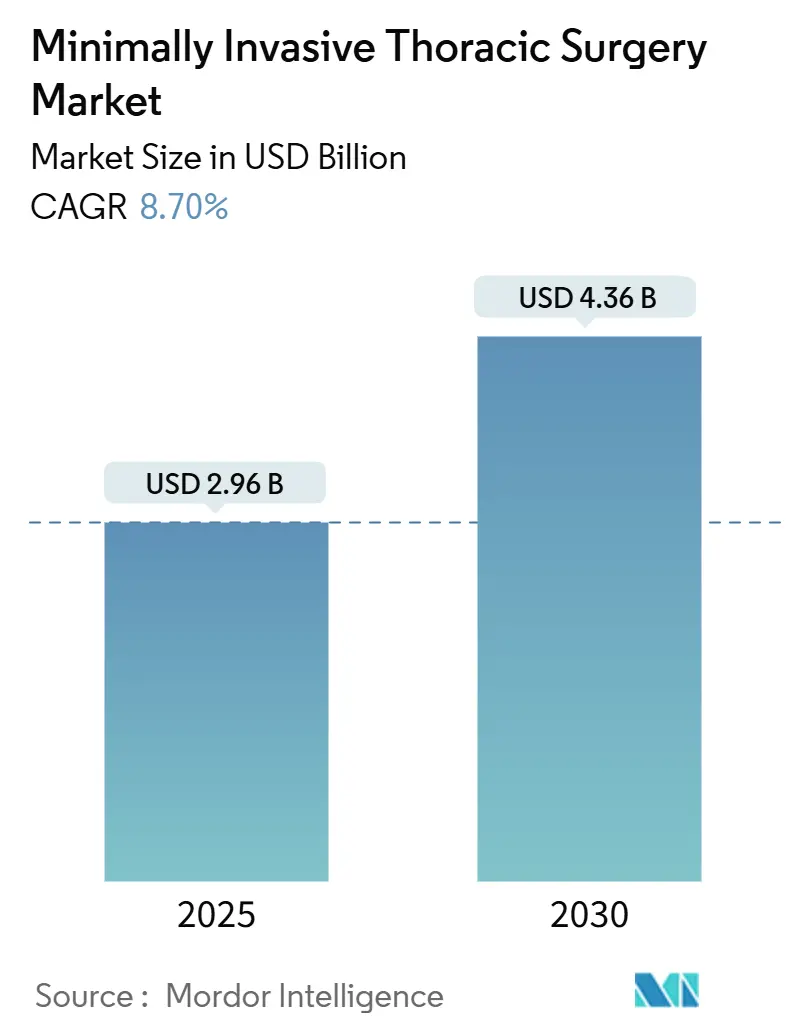

| Market Size (2025) | USD 2.96 Billion |

| Market Size (2030) | USD 4.36 Billion |

| Growth Rate (2025 - 2030) | 8.70% CAGR |

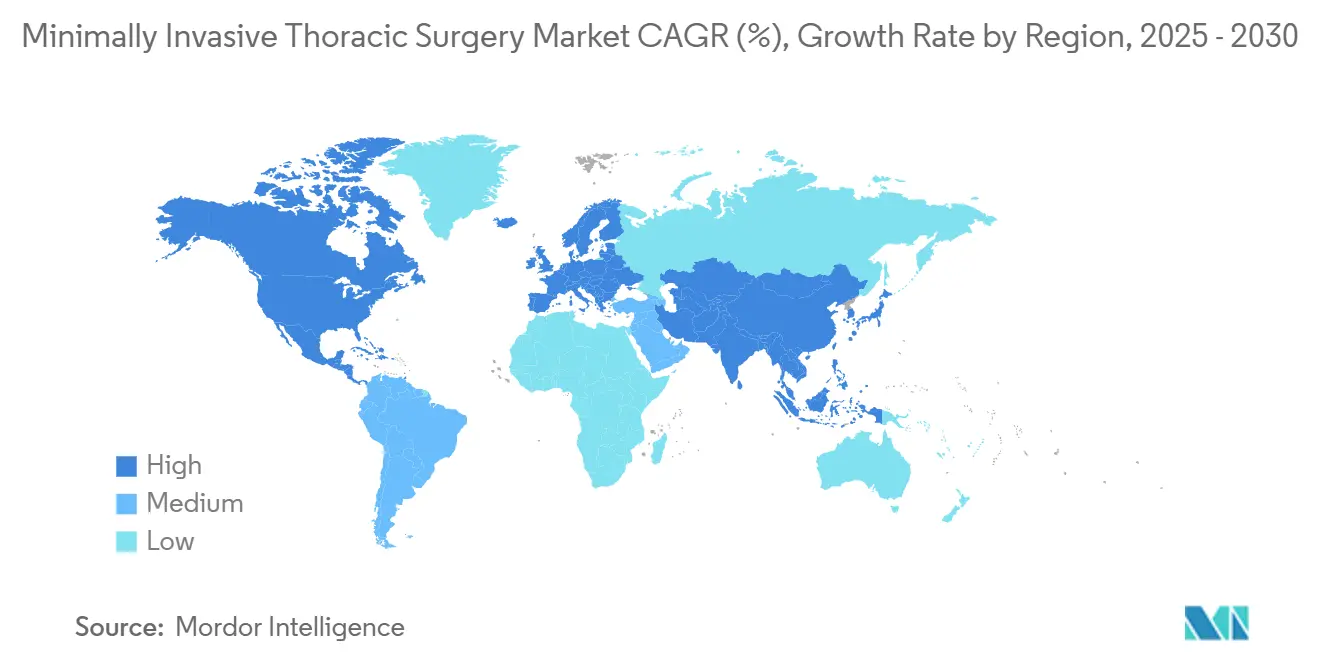

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Minimally Invasive Thoracic Surgery Market Analysis by Mordor Intelligence

The minimally invasive thoracic surgery market reached USD 2.96 billion in 2025 and is forecast to climb to USD 4.36 billion by 2030, translating into an 8.70% CAGR over the period; the current market size reflects momentum behind precision-guided techniques that limit tissue trauma while preserving oncologic control. Broader technology convergence—particularly the pairing of AI-enhanced imaging with next-generation robotic platforms—has redefined procedural workflows, shortened recovery times, and strengthened the value case for outpatient care settings. Surgeons increasingly favor image-guided, multi-port and single-port solutions that combine 3-D visualization, haptic feedback, and machine-learning-powered predictive analytics to raise resection accuracy and shave 15–20% off average operative time. Hospital systems are likewise adopting enhanced recovery after surgery (ERAS) pathways to gain measured reductions in length of stay and readmission rates while satisfying evolving value-based reimbursement schemes. On the competitive front, established instrument makers are vying with robotics specialists, each bundling hardware, software, disposables, and proctoring programs to lock in customers and capture the minimally invasive thoracic surgery market’s recurring revenue streams.

Key Report Takeaways

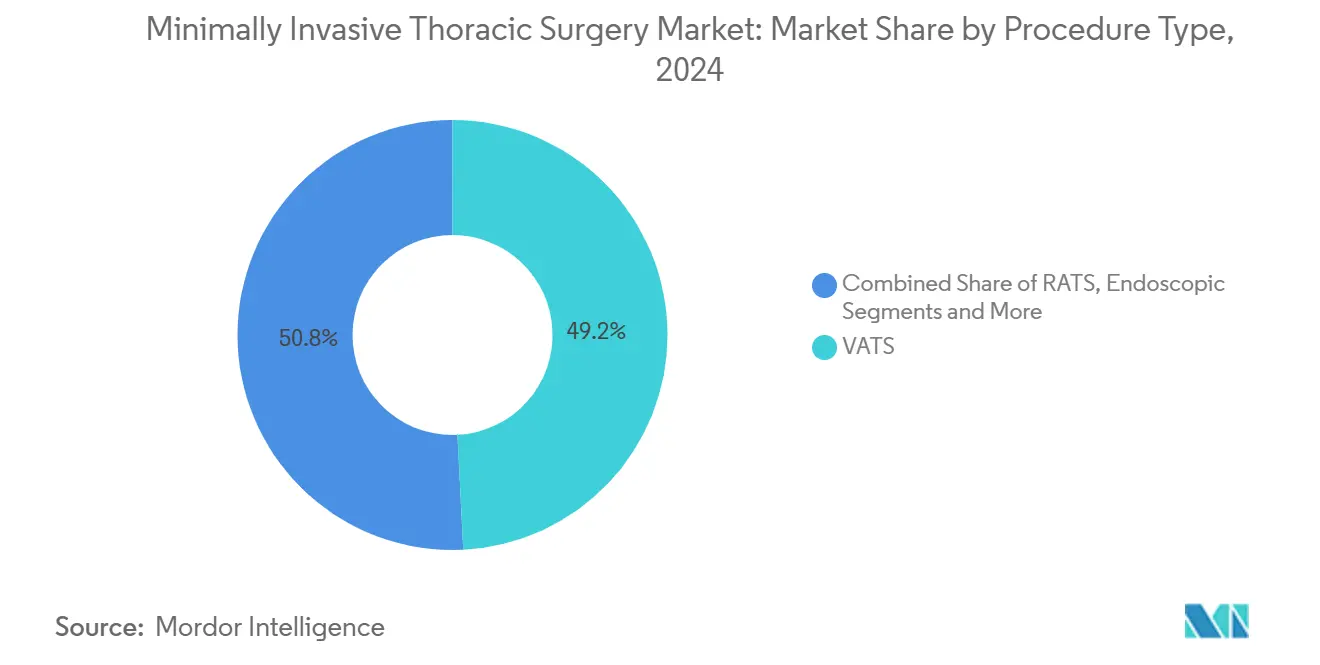

- By procedure type, video-assisted thoracoscopic surgery led with 49.2% of the minimally invasive thoracic surgery market share in 2024. Robotic-Assisted Thoracic Surgery is expanding at an 8.5% CAGR to 2030, the fastest among all procedure types.

- By indication, lung cancer accounted for 52.3% revenue share of the minimally invasive thoracic surgery market size in 2024. Esophageal cancer procedures are projected to advance at a 7.5% CAGR through 2030, the quickest across indications.

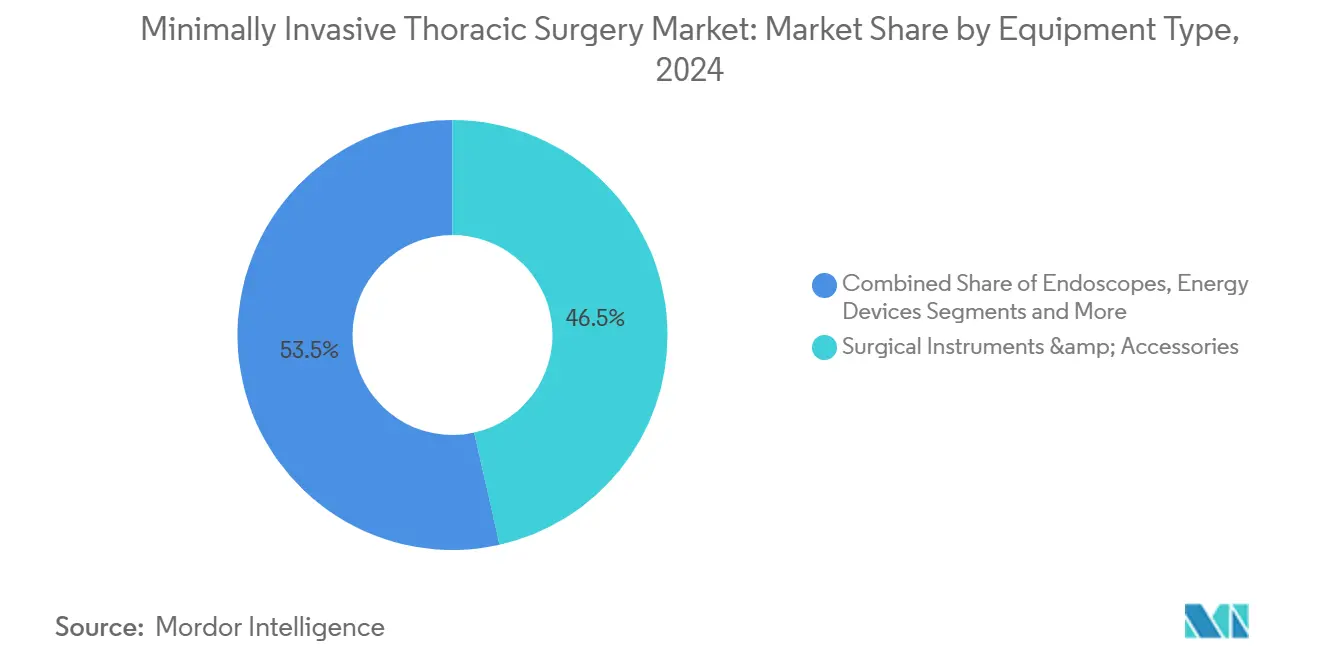

- By equipment type, hospitals captured 61.9% share of the minimally invasive thoracic surgery market size in 2024, while Ambulatory Surgical Centers are registering the highest CAGR at 10.7% through 2030.

- Geographically, North America held 38.2% of the minimally invasive thoracic surgery market share in 2024; Asia Pacific is on track for a 9.50% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Minimally Invasive Thoracic Surgery Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Enabled Intra-Operative Imaging | +1.20% | North America & EU lead, global diffusion | Medium term (2–4 years) |

| Increasing Adoption of ERAS Protocols | +1.50% | Global; strongest in North America & Europe | Short term (≤ 2 years) |

| Rising Lung-Cancer Screening Rates | +1.80% | North America, Europe, expanding Asia Pacific | Medium term (2–4 years) |

| Reimbursement Expansion for RATS | +1.10% | United States core, selective EU states | Long term (≥ 4 years) |

| Robotic Platform Cost Declines | +0.90% | Global, pronounced in Asia Pacific | Long term (≥ 4 years) |

| Aging Population & Comorbidity Burden | +1.30% | Developed economies worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Intra-Operative Imaging

AI integration now supplies 3-D, millimeter-level anatomic reconstructions that sharpen dissection planes and protect vital structures during lobectomies and esophagectomies, in turn driving safer resections and faster OR turnover.[1]Wei Huang et al., “Robotic versus Video-Assisted Thoracic Surgery for Lung Cancer,” pmc.ncbi.nlm.nih.gov Machine-learning models also flag hemodynamic anomalies in real time, enabling pre-emptive corrective steps that cut postoperative morbidity. These gains are magnified in robotic cases, where enhanced visual context compensates for attenuated tactile feedback and helps junior surgeons flatten their learning curve. Institutions logging >100 AI-guided thoracic cases have documented 15–20% operating-time reductions and higher nodal harvest counts, outcomes that link directly to longer disease-free survival and shorter hospital stay metrics.

Increasing Adoption of ERAS Protocols

Comprehensive ERAS bundles—covering carbohydrate loading, opioid-sparing analgesia, early ambulation, and minimally invasive approaches—shortened average postoperative length of stay by 25–30% and reduced 30-day readmissions by 20% among high-volume U.S. thoracic centers in 2024.[2]Christian Galata et al., “Risk Factors for Surgical Complications After VATS,” onlinelibrary.wiley.com Because ERAS relies on standardized pathways, hospitals that scale these protocols witness higher OR throughput, lower consumables waste, and improved patient-reported outcomes. The program has become a strategic differentiator as payers move toward bundled payments that penalize complications and extended hospitalization. Surgeon champions in Europe reported broad ERAS rollouts accomplished within 12 months, financed primarily by savings realized from fewer ICU days and reduced pharmacy utilization.

Rising Lung-Cancer Screening Rates

Stage I–II detection has spiked 40–50% in jurisdictions adopting low-dose CT screening, feeding a predictable stream of surgical candidates that favor minimally invasive resections over chemoradiation.[3]Dominique Gossot et al., “Thoracic Surgery in France,” ncbi.nlm.nih.gov Higher early-stage volume allows facilities to justify investments in robotic consoles, endoscopic staplers, and fluorescence-guided imaging platforms. Public-health bodies in the U.S., Canada, and Japan now reimburse annual screening for at-risk cohorts aged 50–80, a policy move that has materially lifted lobectomy and segmentectomy volumes and thereby accelerated surgeon proficiency development.

Reimbursement Expansion for RATS

CMS created new DRG add-on payments for thoracic robot cases beginning in FY 2025, citing lower readmission and pneumonia rates that ultimately trim total episode cost. Several private U.S. insurers followed, publishing coverage policies tying full payment to surgeon credentialing and institution case-volume thresholds. Select German and French sickness funds launched pilot tariffs for robotic lobectomy in 2024, contingent on registry data submission. These policies nudge hospitals toward technology adoption by de-risking capital-expense recovery and rewarding superior outcomes.

Restraints Impact Analysis of Minimally Invasive Thoracic Surgery Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steep Learning Curve for Surgeons | -0.80% | Global; sharper in low-volume centers | Short term (≤ 2 years) |

| High Capital Expenditure | -1.20% | Worldwide, acute in cost-sensitive markets | Medium term (2–4 years) |

| Limited Access in Low-Income Nations | -0.60% | Rural sites in emerging economies | Long term (≥ 4 years) |

| Regulatory Delays for New Robots | -0.40% | Market-specific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Steep Learning Curve for Surgeons

Credentialing bodies advise 50–75 robotic lobectomies to achieve technical proficiency, a requirement that constrains adoption in centers lacking case density. Prolonged console time, higher initial complication rates, and scheduling complexities during the training phase strain hospital resources and risk surgeon burnout. Emerging markets feel the pinch most acutely because structured proctoring programs and dual-console systems are scarce, forcing prolonged mentorship travel or cross-border fellowships that inflate training costs.

High Capital Expenditure

Robotic consoles list at USD 2–3 million, while annual maintenance can reach USD 200,000, pushing five-year total ownership above USD 5 million for busy centers. Facilities must also budget for dedicated rooms, upgraded imaging infrastructure, and disposable instruments that add USD 2,000–3,000 per case. Although bundled procurement can soften the blow, administrators in Latin America and parts of Southeast Asia still regard the spend as prohibitive absent clear reimbursement assurances.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Minimally Invasive Thoracic Surgery Market Segment Analysis

By Procedure Type:

RATS Gains Despite VATS DominanceVideo-Assisted Thoracoscopic Surgery held 49.2% of minimally invasive thoracic surgery market share in 2024, underscoring three decades of accumulated evidence supporting safety, oncologic adequacy, and favorable cost profiles. The segment’s growth now moderates as penetration approaches saturation in tertiary centers. Yet capacity expansions continue in community hospitals, aided by 4-K visualization, narrow-instrument trocars, and low-pressure insufflation systems that elevate procedural efficiency. In contrast, Robotic-Assisted Thoracic Surgery is posting an 8.5% CAGR through 2030, buoyed by surgeon demand for articulated instruments, tremor filtration, and immersive 3-D optics that ease complex mediastinal dissections. Evidence from multicenter propensity-score analyses shows robotic lobectomy trimming conversion-to-open rates by 40% compared with VATS, a quality metric that directly drives payer preference.

Endoscopic thoracic interventions—chiefly parietal pleurectomy, sympathetic chain clipping, and biopsy workups—capture a smaller but growing user base as single-port and needlescopic platforms reduce incision count and enhance cosmetic appeal. Centers deploying these ultra-minimally invasive modalities report higher same-day discharge rates, a factor aligning well with ASC expansion strategies. Collectively, the interplay between RATS innovation and VATS ubiquity keeps the minimally invasive thoracic surgery market size on a steady uptick as facilities rebalance case mix to optimize margins and outcomes.

By Indication:

Esophageal Cancer Accelerates GrowthLung cancer surgeries commanded 52.3% of minimally invasive thoracic surgery market share in 2024 thanks to wide screening adoption, high disease prevalence, and strong guideline endorsement for lobectomy and segmentectomy in stage I-II tumors. Robotic stapling, fluorescence mapping, and sub-segmental resection tools now allow parenchyma-sparing approaches that preserve pulmonary function and quality of life. Meanwhile, esophageal cancer represents the fastest-rising indication with a 7.5% CAGR, catalyzed by robotic micro-anastomotic capability that slashes leak rates and enhances lymphadenectomy completeness. Asian high-volume centers posted 30-day mortality below 1% for robot-assisted McKeown esophagectomies in 2024, a benchmark previously unattainable with open surgery.

Elsewhere, pneumothorax management sustains a reliable procedural pipeline due to heightened imaging availability and rising smoking cessation program referrals, allowing early intervention through VATS bullectomy and pleurodesis that minimize recurrence. Mediastinal tumors and rib-fracture fixation cases comprise niche but strategically important segments that drive instrument innovation and surgeon skill diversification. Altogether, shifting indication-level dynamics support robust volume growth and diversification within the minimally invasive thoracic surgery market.

By Equipment Type:

Robotics Drive Premium GrowthSurgical instruments and accessories accounted for 46.5% of minimally invasive thoracic surgery market size in 2024, a testament to the ongoing need for energy devices, staplers, and clip appliers adaptable to multiple access platforms. Yet robotic systems are registering a 13.2% CAGR to 2030, reflecting hospitals’ preference for enclosed ecosystems that integrate imaging, instrumentation, and analytics. Multi-port robots dominate today, but single-port architectures are drawing surgeon interest for sub-lobar resections, where limited incision burden correlates with reduced postoperative pain.

Imaging modules—4-K scopes, fluorescence-guided lenses, and AI-supported overlay software—advance steadily as vendors embed them into robotic towers or standalone stacks, protecting average selling price amid commoditization of legacy HD scopes. Stapling and energy categories face price compression because competitive parity has increased; however, specialized reloads tuned for dense hilar anatomy or thick lower-esophageal tissue sustain premium margins. Platform convergence is the strategic watchword: vendors bundling robotics with imaging and disposables lock customers into subscription-style procurement pathways that bolster recurring revenue.

By End User:

ASCs Challenge Hospital DominanceHospitals retained 61.9% of minimally invasive thoracic surgery market share in 2024 given their superior ICU infrastructure, multidisciplinary tumor boards, and resident training mandates. Nonetheless, ambulatory surgical centers are capturing a 10.7% CAGR as ERAS protocols enable same-day discharges for selected lobectomies and wedge resections. Payer incentives under site-neutral reimbursement rules further encourage case migration to ASCs, slicing facility fees by 15–25% relative to inpatient settings. Health-system-owned ASC chains are therefore adding negative-pressure thoracic OR suites and extended-stay bays, accelerating the outpatient tipping point.

Specialty thoracic institutes fill an intermediary niche, functioning as referral hubs for high-risk or revision cases, while providing surgeon-training fellowships that disseminate best practices across broader networks. Their concentration of complex cases sustains equipment vendor feedback loops, informing iterative refinements in robotic instrument design and AI imaging algorithms. Together, these end-user shifts diversify purchase channels and magnify growth vectors for the minimally invasive thoracic surgery market.

Geography Analysis

North America Minimally Invasive Thoracic Surgery Market

North America controlled 38.2% of minimally invasive thoracic surgery market share in 2024 owing to broad insurance coverage, high surgeon adoption, and strong clinical-trial infrastructure. U.S. tertiary centers run 24/7 lung-cancer screening, fast-tracking early-stage finds to robotic resection within two weeks, a throughput feat unmatched elsewhere. Canada’s single-payer system, while cost-conscious, has nonetheless funded multi-hospital robotic consortia that amortize consoles across provincial networks, extending access without bloating capital budgets.

APAC Minimally Invasive Thoracic Surgery Market

Asia Pacific is on pace for a 9.50% CAGR to 2030, the sharpest worldwide, propelled by national health-insurance reforms in China that cover select robotic lobectomies, subsidy programs in India that offset equipment import duties, and Japanese MOH mandates favoring minimally invasive esophagectomy for T1-T3 tumors. High-fidelity simulation labs in Korea and Singapore churn out fellowship-trained surgeons who repatriate to neighboring countries, fuelling regional know-how.

EMEA and South America Minimally Invasive Thoracic Surgery Market

Europe advances at a measured clip as public-hospital procurement cycles lengthen, yet cross-border research alliances strengthen evidence bases that shape reimbursement allocations. Middle East & Africa plus South America remain early-stage but opportunistic, with Gulf states buying full robotic fleets to become medical-tourism magnets, while Brazilian private hospitals leverage favorable exchange rates to import capital goods.

Competitive Landscape

Competitive intensity is moderate; Intuitive Surgical heads the robotic category with a 78-console global install base exceeding 9,000, while Johnson & Johnson’s Verb Surgical and Medtronic’s Hugo platforms chase share through modular cost-of-ownership models. Traditional powerhouses—Stryker, Olympus, and Karl Storz—double down on imaging and instrumentation to remain indispensable regardless of console brand. Alliances between hardware makers and cloud analytics firms proliferate, promising OR dashboards that benchmark surgeon performance against anonymized global datasets.

Strategic plays include vertical integration: Medtronic’s 2024 acquisition of Fortimedix delivered single-port intellectual property that complements its multi-port robot. Johnson & Johnson bundles verb-specific staplers and energy devices at locked-in pricing, tying disposable revenues to console penetration. Emerging Asian vendors differentiate on upfront price and AI co-pilot features, enticing price-sensitive buyers yet facing durability perception hurdles. Overall, portfolio breadth, training ecosystems, and data analytics depth determine ongoing advantage in the minimally invasive thoracic surgery market.

Minimally Invasive Thoracic Surgery Industry Leaders

Intuitive Surgical

Johnson & Johnson

Medtronic Plc

Stryker Corp.

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Minimally Invasive Thoracic Surgery Market Companies Covered in this Report

- Intuitive Surgical

- Johnson & Johnson (Ethicon & Auris)

- Medtronic

- Stryker

- Olympus

- Karl Storz

- Zimmer Biomet

- BD (Becton, Dickinson)

- Teleflex

- Conmed

- Richard Wolf

- Applied Medical Resources

- Smiths Group

- FUJIFILM

- Tofur Surgical

- Shenzhen Mindray Bio-Medical

- Asensus Surgical

- Wego Surgical

- CMR Surgical

- MicroPort

Recent Industry Developments in Minimally Invasive Thoracic Surgery Market

- April 2025: Ethicon obtained FDA clearance for the SP SureForm 45 stapler purpose-built for robotic thoracic procedures.

- March 2025: FDA granted 510(k) clearance for Intuitive Surgical’s da Vinci 5 multi-port robotic system, adding enhanced 3-D optics and AI-assisted workflow guidance.

- December 2024: Medtronic closed its USD 485 million purchase of Fortimedix Surgical, accelerating single-port platform development.

Global Minimally Invasive Thoracic Surgery Market Report Scope

Segmentation Overview

| Video-Assisted Thoracoscopic Surgery (VATS) |

| Robotic-Assisted Thoracic Surgery (RATS) |

| Endoscopic Thoracic Surgery |

| Lung Cancer |

| Esophageal Cancer |

| Pneumothorax |

| Mediastinal Tumors |

| Others (e.g., Hyperhidrosis) |

| Surgical Instruments & Accessories |

| Endoscopes & Imaging Systems |

| Energy & Stapling Devices |

| Robotic Platforms |

| Hospitals |

| Specialty Thoracic Centers |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Type | Video-Assisted Thoracoscopic Surgery (VATS) | |

| Robotic-Assisted Thoracic Surgery (RATS) | ||

| Endoscopic Thoracic Surgery | ||

| By Indication | Lung Cancer | |

| Esophageal Cancer | ||

| Pneumothorax | ||

| Mediastinal Tumors | ||

| Others (e.g., Hyperhidrosis) | ||

| By Equipment Type | Surgical Instruments & Accessories | |

| Endoscopes & Imaging Systems | ||

| Energy & Stapling Devices | ||

| Robotic Platforms | ||

| By End User | Hospitals | |

| Specialty Thoracic Centers | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the minimally invasive thoracic surgery market in 2030?

The market is expected to reach USD 4.36 billion by 2030 based on an 8.70% CAGR.

Which procedure type is growing fastest in thoracic surgery?

Robotic-Assisted Thoracic Surgery is increasing at an 8.5% CAGR through 2030.

Why are Ambulatory Surgical Centers gaining share?

ERAS pathways now enable same-day discharge for selected cases, letting ASCs offer cost-effective outpatient thoracic procedures while posting a 10.7% CAGR.

Which region is forecast to grow most quickly?

Asia Pacific leads with a 9.50% CAGR, propelled by healthcare infrastructure investments and larger at-risk populations.

What remains the main restraint on wider robotic adoption?

High capital expenditureUSD 23 million per console plus maintenancecontinues to slow uptake in cost-sensitive markets.

How are AI tools improving thoracic surgery outcomes?

AI-powered intra-operative imaging supplies real-time anatomic guidance, cutting operative time by up to 20% and reducing conversion-to-open rates.

Page last updated on: