Scoliosis Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

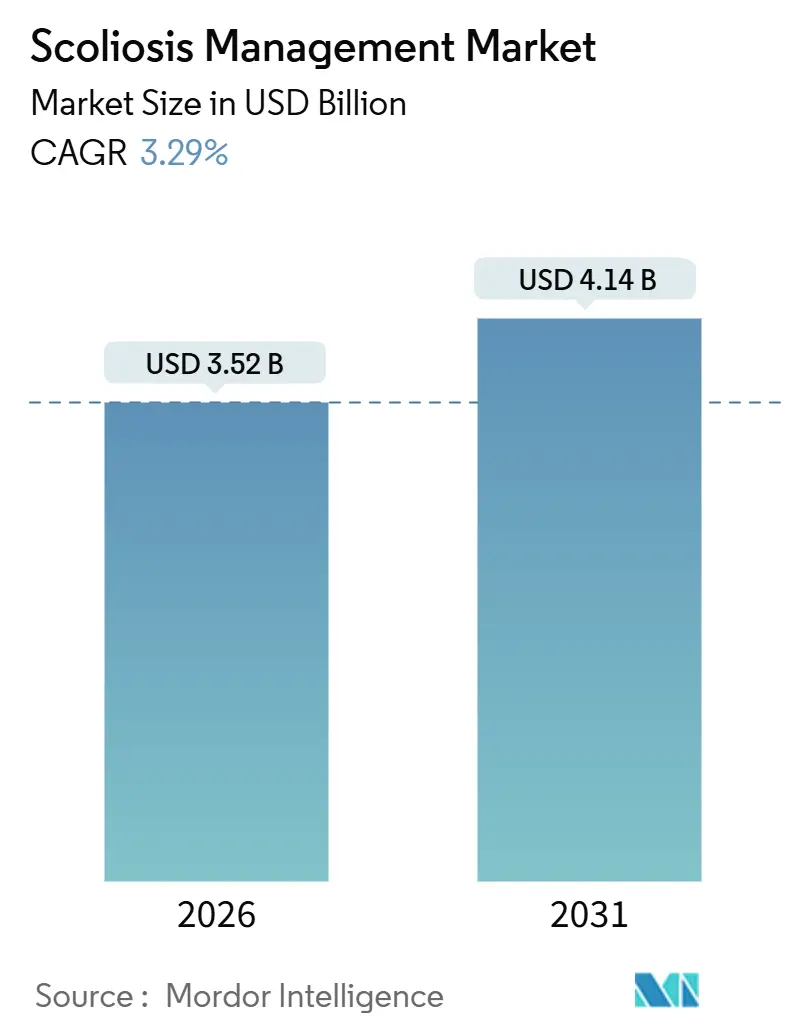

| Market Size (2026) | USD 3.52 Billion |

| Market Size (2031) | USD 4.14 Billion |

| Growth Rate (2026 - 2031) | 3.29% CAGR |

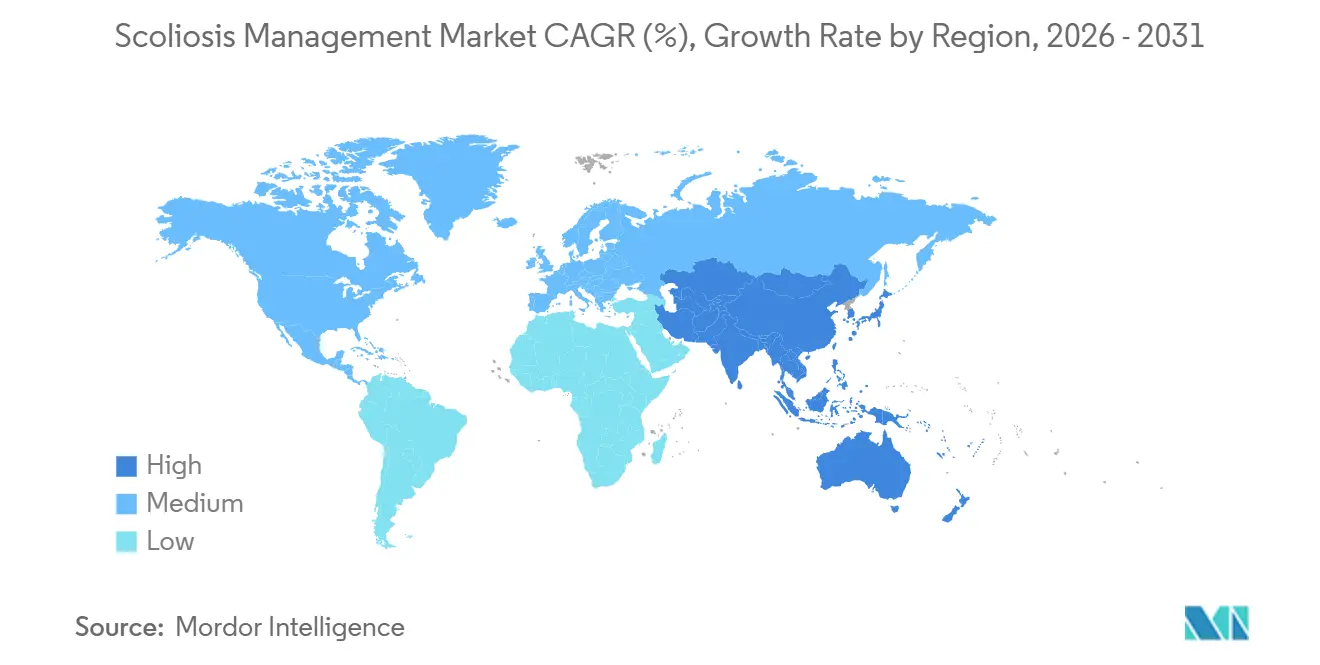

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scoliosis Management Market Analysis by Mordor Intelligence

The Scoliosis Management Market size is estimated at USD 3.52 billion in 2026, and is expected to reach USD 4.14 billion by 2031, at a CAGR of 3.29% during the forecast period (2026-2031).

Orthosis systems remain the primary revenue driver; however, spinal systems are witnessing accelerated growth as surgeons and payers increasingly prioritize motion-preserving implants that address long-term quality-of-life outcomes. Furthermore, expanded adolescent screening programs are directing more mild cases into conservative care pathways. The adoption of 3D-printed custom braces, robotics-guided fusion, and AI-assisted radiograph analysis is enhancing clinical decision-making, reducing revision rates, and improving patient adherence. These advancements collectively support steady, though moderate, revenue growth. Regional performance varies significantly: North America continues to lead in revenue, supported by strong reimbursement frameworks for vertebral body tethering. In contrast, the Asia-Pacific region is emerging as the fastest-growing market, driven by institutionalized school screening programs and expanded pediatric orthopedic capacity in key markets such as China, India, and Japan. The competitive landscape is moderately concentrated, with a few vertically integrated spine companies focusing on posterior fixation and tether systems. However, substantial opportunities exist in sensor-enabled braces, hybrid exoskeletons, and AI-driven progression analytics.

Key Report Takeaways

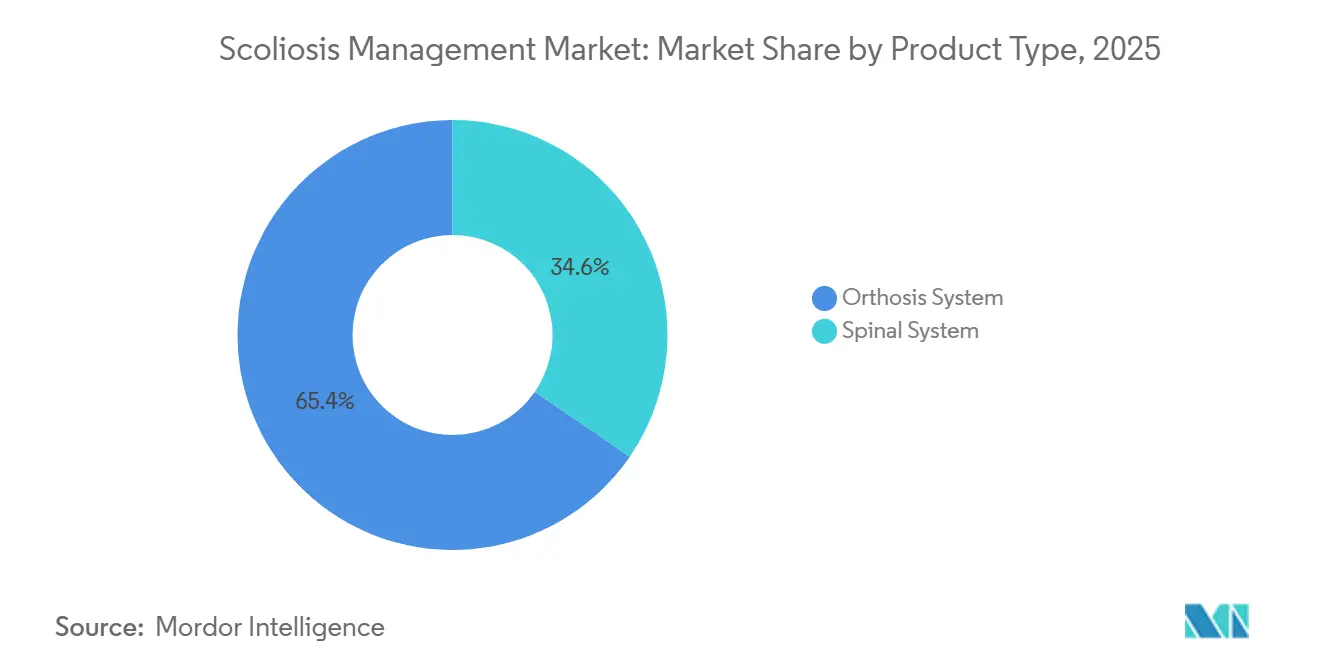

- By product type, orthosis systems captured 65.41% of 2025 revenue, but spinal systems posted the highest 5.21% CAGR through 2031.

- By disease type, idiopathic scoliosis held 75.12% of 2025 cases, and the segment is advancing at a 5.88% CAGR.

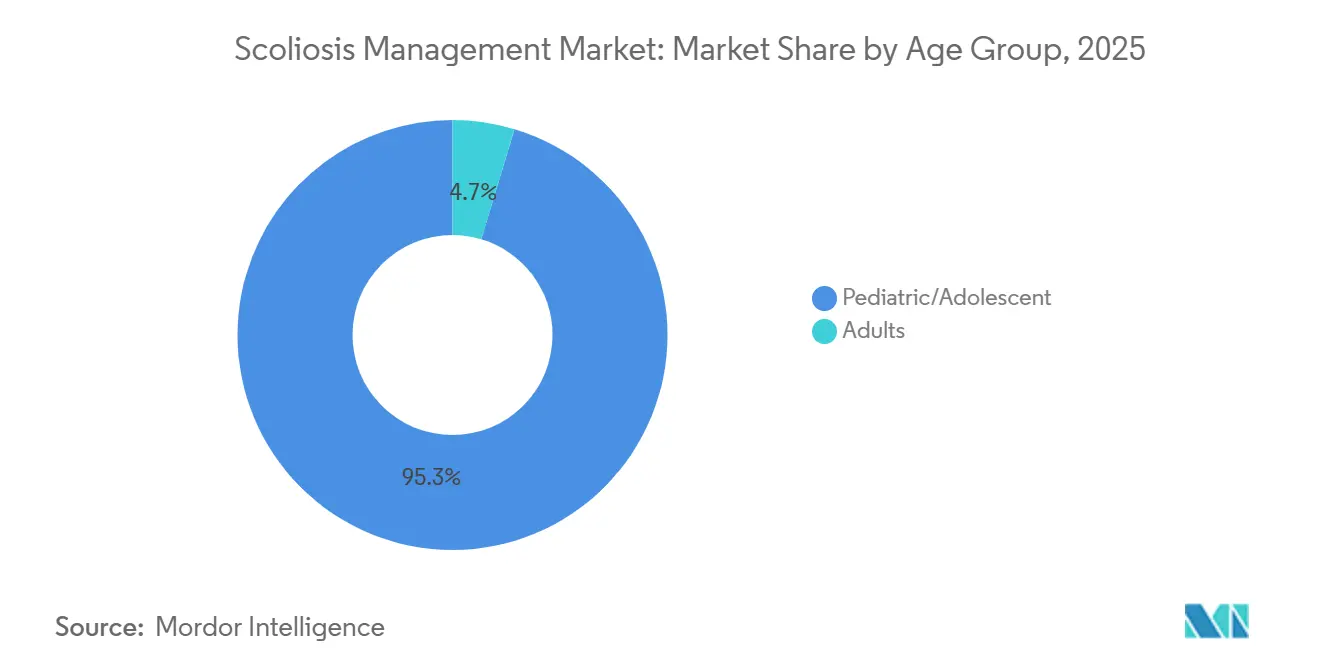

- By age group, pediatric and adolescent patients accounted for 95.34% of the installed base in 2025 and are expected to expand at 6.54% through 2031.

- By end user, specialty clinics and orthopedic centers accounted for 55.93% of 2025 spending, whereas hospitals posted the fastest 6.32% CAGR on the back of complex early-onset and neuromuscular cases.

- By geography, North America accounted for 49.15% of 2025 global revenue, while Asia-Pacific recorded the highest regional CAGR at 5.09%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Scoliosis Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing AIS detection and screening rates across adolescents | +0.8% | Global, with concentration in APAC (China, Japan, South Korea) and select U.S. states | Medium term (2-4 years) |

| Level I evidence for bracing effectiveness and improved compliance monitoring | +0.6% | North America & Europe | Short term (≤ 2 years) |

| Surge in motion-preserving scoliosis surgeries (VBT) and dynamic correction options | +1.2% | North America, spill-over to Europe and APAC urban centers | Medium term (2-4 years) |

| Integration of robotics/navigation and low-dose 3D imaging in deformity workflows | +0.7% | Global, early adoption in North America and Western Europe | Long term (≥ 4 years) |

| AI-enabled radiograph analysis accelerating triage and follow-up decisions | +0.5% | North America, Europe, APAC core markets | Medium term (2-4 years) |

| Digitally designed and 3D-printed custom TLSOs improving comfort and adherence | +0.4% | Global, with faster uptake in North America and Europe | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

Growing AIS Detection and Screening Rates Across Adolescents

Mandatory screening in Japan, South Korea, and several Chinese provinces identifies curves with Cobb angles of 10°–25°, when bracing can still avert surgery and preserve growth. Prevalence data suggest 2%–3% of school-age children exhibit idiopathic scoliosis, yet only a tenth progress to surgical thresholds, underscoring the volume opportunity for conservative devices. In the United States, states that reinstated screening in 2024–2025 widened detection pipelines, and professional societies endorse opportunistic screening during pediatric wellness visits. Low-dose EOS imaging reduces cumulative radiation by up to 90%, enabling serial monitoring without elevating cancer risk. The resulting registries feed machine-learning models that stratify progression risk, refining resource allocation for both bracing and surgery.

Level I Evidence for Bracing Effectiveness and Improved Compliance Monitoring

A 2024 reanalysis of the BrAIST randomized trial affirmed that wearing braces ≥18 hours daily reduces progression to surgery by 56%, moving orthosis therapy from tradition to an evidence-based standard. Real-world data show a median wear of 12 hours, a gap addressed by braces embedding temperature and motion sensors that stream adherence data to cloud dashboards, raising compliance 15%–20% in pilot programs. U.S. insurers are tying reimbursements to objective wear metrics, heightening accountability across patients, orthotists, and payers. Schroth and other exercise regimens complement braces by enhancing trunk muscle endurance, but integration outside specialized European centers varies. Collectively, these dynamics stabilize brace utilization despite emerging surgical alternatives.

Surge in Motion-Preserving Scoliosis Surgeries (VBT) and Dynamic Correction Options

FDA Humanitarian Device Exemption was granted for vertebral body tethering in 2019, and U.S. annual case volumes have risen 40% thanks to expanding surgeon training and selective payer coverage. VBT preserves segmental motion but exhibits 24% tether breakage at 5 years, spurring development of fatigue-resistant polymers and tighter patient-selection protocols. Dynamic systems such as ApiFix and Jazz bands offer alternative load-sharing constructs but lag VBT in evidence depth and reimbursement traction. Premium pricing and narrow indications limit the total number of procedures, yet halo effects improve surgeons' comfort with motion-preserving concepts, indirectly boosting spinal-system innovation. Longer term, successful durability data could meaningfully shift the scoliosis management market toward growth-friendly implants.

Integration of Robotics/Navigation and Low-Dose 3D Imaging in Deformity Workflows

Robotic systems like Mazor X reduce pedicle-screw malposition to below 2% and shorten operative time by 15–20 minutes, improving patient outcomes and reducing bundled economics. Hospitals amortize USD 1 million-plus capital across high-volume deformity caseloads, and service contracts align vendors with outcome-based purchasing. Combined with 3D imaging, intraoperative verification can be performed without additional radiation or repositioning, enhancing workflow efficiency. FDA acceptance of software-only upgrades quickens AI-driven trajectory planning that incorporates vertebral rotation and bone density. As payers reward lower complication rates, robotics-guided deformity correction is gaining strategic importance at leading centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-world bracing adherence challenges and quality-of-life impacts | -0.5% | Global, particularly pronounced in North America and Europe | Short term (≤ 2 years) |

| VBT safety/long-term durability concerns and payer gatekeeping | -0.7% | North America, emerging in Europe | Medium term (2-4 years) |

| High capital and per-case costs for advanced deformity technologies | -0.4% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| HDE annual distribution and pediatric subspecialist capacity constraints | -0.3% | North America, selective impact in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Real-World Bracing Adherence Challenges and Quality-of-Life Impacts

Sensor studies across six U.S. centers revealed median brace wear of 11.2 hours daily, well below the 18-hour prescription benchmark and insufficient to curb curve progression[1]The Spine Journal, “Real-World Adherence to Bracing in Adolescent Idiopathic Scoliosis,” spinejournal.com. Heat buildup, restricted sports participation, and visible contours erode adolescent compliance, generating dropout rates >30% in routine practice. Quality-of-life scores on PedsQL and SRS-22 decline during bracing and rebound only post-treatment, illustrating psychosocial costs. Insurers now require objective wear data to approve replacements, pressuring orthotists to optimize fit and provide behavioral coaching. Until comfort and adherence converge, orthosis effectiveness in the scoliosis management market remains below its clinical potential.

VBT Safety/Long-Term Durability Concerns and Payer Gatekeeping

A 2025 meta-analysis covering 1,200 patients reported 24% tether breakage and 15% revision burden at 5 years, unsettling early optimism for VBT. Commercial insurers label VBT as investigational outside narrow curve windows, resulting in frequent pre-authorization denials. Hospital margins suffer when implant costs of USD 15,000–20,000 match reimbursement for fusion, dampening investment in training. Long-term data on disc health and adjacent-segment kinetics remain sparse, keeping payers cautious. Unless durability demonstrably improves, VBT volume growth will fall short of initial expectations, dampening its boost to the scoliosis management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Orthosis Dominance Yields to Spinal Innovation

Orthosis systems accounted for 65.41% of revenue in 2025, yet spinal systems will outpace them with a 5.21% CAGR, illustrating how value is migrating toward motion-preserving implants that promise durable correction. Within bracing, digitally designed and 3D-printed TLSOs are capturing early adopters by compressing fabrication cycles and improving cosmetic appeal. Nighttime braces gain mindshare among socially sensitive teens, but payers often balk at covering evidence-light designs, capping penetration. Spinal systems are split between posterior fixation workhorses, emergent VBT, and dynamic constructs. Rigid fusion maintains surgical share, but next-gen devices command premium pricing and push the scoliosis management market size for implants upward, even on modest procedure volumes. Enabling technologies—navigation, robotics, orthobiologics—layer incremental revenue, allowing integrated vendors to monetize the full surgical episode.

Secondary growth of the scoliosis management market share within spinal systems comes from growth-friendly rods and hybrid posterior bands aimed at early-onset scoliosis. Although incidence is low, complexity drives device ASPs above USD 30,000, supporting niche profitability. Orthobiologics bundle into fusion cases to accelerate arthrodesis and generate ancillary revenue. Overall, orthosis remains the volume backbone, but spinal systems capture disproportionate value and innovation, a duality that will persist through 2031.

By Disease Type: Idiopathic Scoliosis Commands Volume and Growth

Idiopathic scoliosis accounted for 75.12% of cases in 2025 and is rising at a 5.88% CAGR, driven by universal adolescent screening and heightened parental vigilance. Sub-segmentation shows that adolescent idiopathic scoliosis predominates because its prevalence peaks during puberty, whereas infantile and juvenile variants are rarer. Congenital and neuromuscular curves contribute lower volume but generate higher per-case revenue due to surgical complexity and extended hospital stays. Degenerative adult scoliosis is expanding as populations age, but many cases remain conservatively managed, muting device demand.

The scoliosis management market size for idiopathic curves is poised to expand further as machine-learning tools improve progression prediction, enabling proactive bracing rather than watchful waiting. Genetic insights are emerging but not yet practice-changing. In congenital and neuromuscular cases, growth-friendly instrumentation sustains premium ASPs and raises average procedure costs, underpinning total scoliosis management market growth despite smaller patient counts.

By Age Group: Pediatric Dominance Reflects Disease Epidemiology

Pediatric and adolescent patients accounted for 95.34% of the 2025 installed base and will increase by 6.54% through 2031, reflecting the disease’s childhood onset and the clinical imperative to intervene before skeletal maturity. Early-onset cases, though few, require recurring lengthenings or magnetic adjustments, yielding annuity-style revenue that elevates the growth share of scoliosis management devices. Adult scoliosis cases contribute marginally to total volume yet attract industry focus because self-pay patients seek minimally invasive corrections that promise rapid return to work.

Insurance differentials favor pediatric treatment, and parental advocacy accelerates the adoption of advanced bracing and VBT. Adult indications face stricter payer scrutiny and heightened comorbidity risks, lengthening pre-authorization cycles. Market dynamics, therefore, continue to skew pediatric, reinforcing vendor priorities around child-specific product lines, fellowship training, and family-centric digital engagement.

By End User: Specialty Clinics Lead, Hospitals Accelerate

Specialty clinics and orthopedic centers captured 55.93% of 2025 outlays, benefiting from integrated imaging, bracing, and surgical planning under one roof, while hospital systems are expanding at 6.32% as complex neuromuscular and early-onset cases centralize into tertiary centers. Ambulatory surgery centers chip away at straightforward AIS fusions due to lower overhead, but case complexity limits their ability to tackle severe deformities. Hospitals gain leverage through bundled payments covering implants, surgeon fees, and facility costs, compelling standardization on cost-effective technologies.

Tele-consult platforms extend specialty-clinic reach, pairing virtual evaluations with local brace fabrication, yet liability concerns constrain full clinical delegation. Orthotics labs confront margin pressure from direct-to-consumer brace startups, prompting a pivot to higher-tech 3D printing and compliance-sensor integration. Collectively, the end-user landscape remains fluid, but specialty clinics retain the volume engine, and hospitals accumulate revenue density via high-acuity interventions.

Geography Analysis

North America generated 49.15% of global revenue in 2025, powered by robust commercial insurance coverage, advanced surgeon training, and early adoption of robotics and VBT. Universal health systems in Canada fund scoliosis care but impose capacity caps that push wait times beyond 12 months, driving some patients to cross the border for quicker treatment. Mexico’s expanding private insurance sector attracts U.S. medical tourists seeking lower-cost bracing and fusion without compromising quality.

Europe delivers mixed performance: Germany, France, and the United Kingdom provide full public coverage for bracing and surgery, yet budget constraints in southern and eastern Europe slow uptake of advanced devices. Implementation of the EU Medical Device Regulation in 2024 tightened post-market surveillance, delaying some launches but enhancing patient safety[2]European Spine Study Group, “EU Deformity Registry Annual Report,” essg.eu. Schroth-based exercise protocols temper bracing volumes in German-speaking regions, nudging the scoliosis management market toward more conservative care.

Asia-Pacific posts the fastest 5.09% CAGR through 2031, as China, India, and Japan institutionalize school screening and scale pediatric orthopedic centers[3]China National Healthcare Security Administration, “National Reimbursement List Update,” nhsa.gov.cn. China’s 2024 reimbursement inclusion of scoliosis surgery reduced patient out-of-pocket share to 30%, stimulating procedural demand. Domestic device makers price implants 40% below Western incumbents, accelerating penetration into tier-2 and tier-3 cities. India sees rising middle-class adoption of 3D-printed braces, though pediatric subspecialist scarcity hinders complex surgical growth.

The Middle East and Africa remain underpenetrated, with Saudi Arabia and the UAE acting as regional hubs due to oil-funded health budgets and expatriate surgeon talent. South Africa’s private sector offers advanced care, whereas public hospitals treat only severe cases owing to resource constraints. South America exhibits pockets of excellence in Brazil and Argentina, but high import tariffs add 20%–40% to device prices, dampening rural adoption. Currency volatility further complicates pricing strategies for multinationals operating in the scoliosis management market.

Competitive Landscape

The scoliosis management market is moderately concentrated. Medtronic, OrthoPediatrics, and Orthofix anchor posterior fixation, growth-friendly rods, and robotics portfolios, while Boston Orthotics & Prosthetics and Össur dominate regional orthosis fabrication. Integrated players leverage clinical evidence and surgeon-training ecosystems to entrench installed bases, filing patents on AI-guided planning, bioabsorbable tethers, and smart braces that stream adherence data. Acquisitions of digital-health startups convert one-time implant sales into recurring software revenue, aligning vendors with payers that demand value-based care.

Emerging disruptors challenge incumbents by offering telehealth-linked mail-order braces at half the cost, though concerns over fit accuracy temper clinician endorsement. Niche device makers target congenital and syndromic deformities with patient-specific implants produced via additive manufacturing, sidestepping inventory costs. Regulatory bodies fast-track AI software clears under digital-health pathways, fostering new entrants focused on radiograph analytics and remote monitoring. Competitive stakes rise as hospitals and insurers tie contracting to outcomes and patient-reported metrics, compelling all vendors to sustain real-world evidence programs.

Scoliosis Management Industry Leaders

Boston Orthotics & Prosthetics

Medtronic

Össur

DM Orthotics

Orthofix

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: OrthoPediatrics Corp. launched its new VerteGlide Spinal Growth Guidance System, a search drug designed specifically to treat Early Onset Scoliosis (EOS) in children in the United States. The system represented the company's 80th product developed exclusively for pediatric orthopedic conditions.

- May 2023: Globus Medical, Inc., one of the leading musculoskeletal solutions companies, launched the REFLECT Scoliosis Correction System, which has been granted approval from the US Food and Drug Administration, as the company’s first humanitarian device. REFLECT is designed to correct progressive scoliosis in young patients while preserving motion, maintaining stability, and allowing for future modulated growth.

Global Scoliosis Management Market Report Scope

As per the scope of the report, scoliosis management involves monitoring and treating abnormal lateral curvature of the spine. Treatment options include observation, bracing, or surgery, depending on the severity and progression. The goal is to prevent progression and improve spinal alignment and function.

The Scoliosis Management Market is Segmented by Product Type (Orthosis System and Spinal System), Disease Type (Idiopathic, Congenital, Neuromuscular, and Degenerative), Age Group (Pediatric/Adolescent and Adult), End User (Hospitals, ASCs, Specialty Clinics, and O&P Labs), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Orthosis System | TLSO |

| CTLSO | |

| LSO | |

| Nighttime Braces | |

| Dynamic Soft/Flexible Braces | |

| Spinal System |

| Idiopathic Scoliosis |

| Congenital Scoliosis |

| Neuromuscular Scoliosis |

| Degenerative (Adult) Scoliosis |

| Pediatric/Adolescent |

| Adult |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics / Orthopedic Centers |

| Orthotics & Prosthetics Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Orthosis System | TLSO |

| CTLSO | ||

| LSO | ||

| Nighttime Braces | ||

| Dynamic Soft/Flexible Braces | ||

| Spinal System | ||

| By Disease Type | Idiopathic Scoliosis | |

| Congenital Scoliosis | ||

| Neuromuscular Scoliosis | ||

| Degenerative (Adult) Scoliosis | ||

| By Age Group | Pediatric/Adolescent | |

| Adult | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics / Orthopedic Centers | ||

| Orthotics & Prosthetics Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the scoliosis management market in 2026?

It stands at USD 3.52 billion with a projected CAGR of 3.29% through 2031.

Which product category grows fastest to 2031?

Spinal systems expand at a 5.21% CAGR, outpacing orthosis devices.

Why does idiopathic scoliosis dominate volumes?

Universal adolescent screening identifies most curves, making idiopathic cases 75.12% of 2025 incidence.

What drives Asia-Pacific's rapid growth?

Mandatory school screening and expanded reimbursement in China, India, and Japan produce a 5.09% regional CAGR.

How do smart braces improve outcomes?

Embedded sensors provide objective wear data, boosting adherence by up to 20% in pilot programs.

What are the main barriers to VBT adoption?

Tether breakage concerns and restrictive payer policies slow uptake despite motion-preserving benefits.

Page last updated on: