South Africa Residual Current Circuit Breaker (RCCB) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

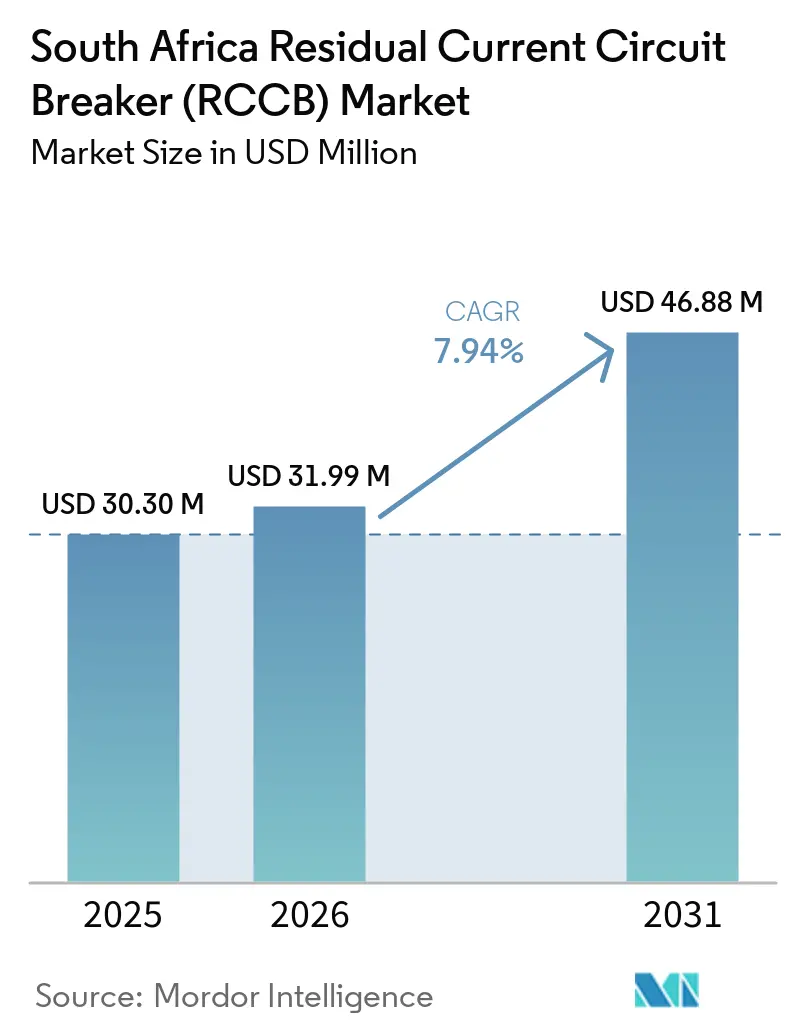

| Base Year Market Size (2025) | USD 30.30 Million |

| Market Size (2026) | USD 31.99 Million |

| Market Size (2031) | USD 46.88 Million |

| Growth Rate (2026 - 2031) | 7.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Residual Current Circuit Breaker (RCCB) Market Analysis by Mordor Intelligence

The South Africa Residual Current Circuit Breaker Market size was valued at USD 30.30 million in 2025 and is estimated to grow from USD 31.99 million in 2026 to reach USD 46.88 million by 2031, at a CAGR of 7.94% during the forecast period (2026-2031). Mandatory compliance with SANS 10142-1 and the legal importance of the Certificate of Compliance keep replacement demand active even when new construction slows, which gives the South Africa residual current circuit breaker market a steady base of recurring demand.[1]Electrical Contractors' Association of South Africa, “SANS 10142-1:2024 Edition 3.2 Released,” ECA(SA), ecasa.co.za The spread of rooftop solar, hybrid backup systems, and EV charging is also changing the protection mix, because more installations now need Type A, Type F, or Type B devices instead of older AC-only units, which raises value growth in the South Africa residual current circuit breaker market without relying only on unit volumes. Eskom tariff increases approved for 2024, 2025, and 2026 are strengthening the case for upgrading boards, adding energy controls, and replacing aging earth-leakage devices across homes and commercial premises. At the same time, South Africa’s public infrastructure pipeline is widening demand across utilities, transport, energy, and public buildings, which means the South Africa residual current circuit breaker market is drawing support from several end uses rather than from one crisis-led channel alone. Competition remains distributor-led and moderately fragmented, while the main downside from slower rooftop solar additions is partly offset by non-discretionary compliance demand and the ongoing move toward higher-spec protection in the South Africa residual current circuit breaker market.

Key Report Takeaways

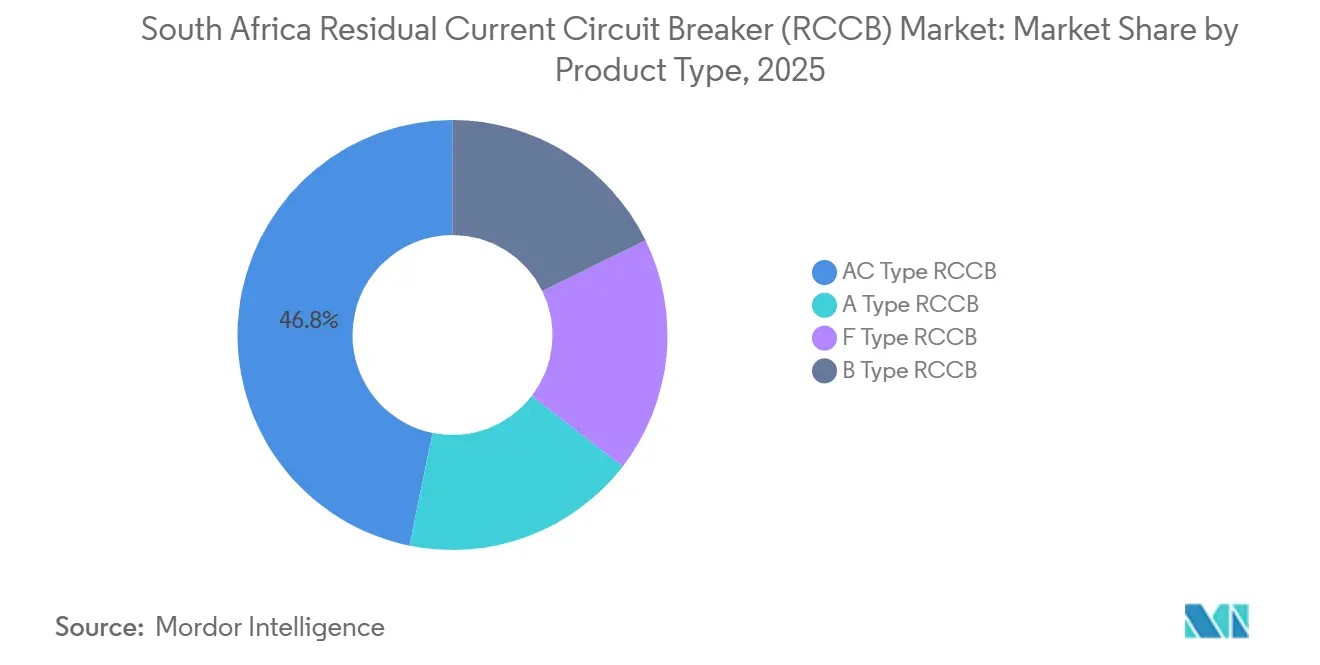

- By product type, AC Type RCCBs held 46.8% of the South Africa residual current circuit breaker market in 2025, while B Type RCCBs are forecast to expand at a 9.4% CAGR through 2031.

- By pole configuration, Two-Pole RCCBs retained 61.5% of the South Africa residual current circuit breaker market in 2025, while Four-Pole RCCBs recorded the highest projected CAGR at 8.1% through 2031.

- By rated current, Above 25A to 63A devices accounted for 52.7% of the South Africa residual current circuit breaker market in 2025, while Above 63A devices are projected to grow at an 8.8% CAGR through 2031.

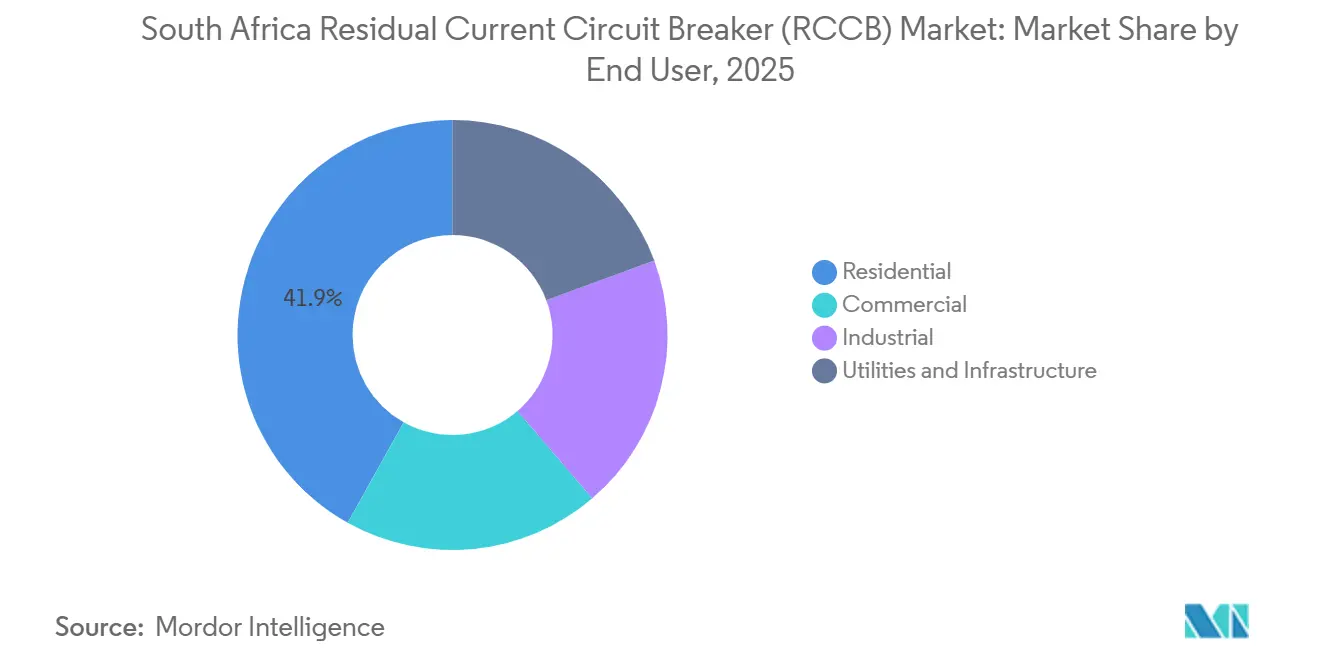

- By end user, Residential users held 41.9% of the South Africa residual current circuit breaker market in 2025, while Utilities and Infrastructure is advancing at the fastest CAGR of 9.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Residual Current Circuit Breaker (RCCB) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory SANS 10142 compliance and CoC enforcement | +2.1% | National, with high enforcement intensity in Gauteng and Western Cape metros | Short term (≤ 2 years) |

| Rooftop solar and hybrid backup-system installations | +1.8% | National, concentrated in Gauteng, Western Cape, and KwaZulu-Natal | Medium term (2-4 years) |

| Electricity tariff inflation driving protection retrofits | +1.2% | National | Medium term (2-4 years) |

| Public infrastructure and building-electrification pipeline | +1.0% | National, with project concentration in Gauteng, Northern Cape, and Eastern Cape | Long term (≥ 4 years) |

| Alternate-supply bonding revisions lifting board reconfiguration demand | +0.6% | National, especially SSEG-connected premises in Eskom-supplied areas | Short term (≤ 2 years) |

| EV charging circuit compliance shifting demand to higher-spec RCCBs | +0.9% | Gauteng and Western Cape, especially along the N1, N2, and N3 corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory SANS 10142 Compliance and CoC Enforcement

South Africa’s electrical safety framework creates a recurring replacement cycle because fixed installations must comply with SANS 10142-1 and property transfers require a valid Certificate of Compliance. That requirement means spending on earth-leakage protection is often not optional, especially when premises are sold, renovated, insured, or audited. SANS 10142-1:2024 Edition 3.2, released in August 2024, tightened requirements for SSEG-connected installations, documentation, and protection coordination, which raised the technical standard installers must meet. In practice, an electrician inspecting an older board that now includes a solar inverter must decide whether an existing Type AC device remains suitable or whether the board needs Type A or Type B protection instead. That review often turns a simple inspection into a broader board upgrade, which lifts both unit demand and value demand. This is one of the main reasons the South Africa residual current circuit breaker market remains resilient even when broader construction activity softens.

Rooftop Solar and Hybrid Backup-System Installations

South Africa’s distributed solar base reached 7,415 MWac of rooftop and small ground-mounted capacity by October 2025, which shows how large the installed base for future protection upgrades has become. The country added 1.6 GW of new solar in 2025 after 1.1 GW in 2024, and SAPVIA reported 4 GW of new PV projects registered with NERSA in 2025, which restored momentum after the previous slowdown. Every new inverter-linked system must align with SANS 10142-1 and SANS 60364-7-712, so the installation of solar and batteries usually creates direct demand for new or replacement RCCBs. The bigger change is in the protection class, because hybrid systems introduce fault-current conditions that are no longer well served by older AC-only devices. That pushes many retrofit decisions toward Type A, Type F, or Type B products, especially in commercial settings with more complex loads. The South Africa residual current circuit breaker market, therefore, benefits not only from more solar sites but also from a richer product mix as installations become more electrically complex.

Electricity Tariff Inflation Driving Protection Retrofits

Eskom implemented three consecutive above-inflation tariff increases for direct customers, 12.74% in April 2024, 12.74% in April 2025, and 8.76% in April 2026, which has kept energy spending under pressure across customer groups. Higher power costs are pushing households, property managers, and businesses to add monitoring, backup supply, and automated load control to reduce exposure to grid costs and outages. Those upgrades usually involve changes to distribution boards, segregation of circuits, or replacement of older protection devices so that the installation remains compliant. Commercial energy audits are also becoming more important, and these audits often identify non-compliant or aging earth-leakage protection that must be replaced. That makes tariff escalation an indirect but durable demand driver rather than a short-term pricing event. The South Africa residual current circuit breaker market gains from this pattern because protection upgrades tend to be bundled with wider electrical improvements.

EV Charging Circuit Compliance Shifting Demand to Higher-Spec RCCBs

South Africa’s public EV charging network exceeded 500 charging points by 2025, and charging sessions doubled during 2024 compared with the previous year, which points to a stronger installed base for specialized protection equipment. Zero Carbon Charge also began building a large off-grid charging network in the Eastern Cape, covering 29 sites with 480 kW ultra-fast chargers, which raises demand for high-current and high-spec protection devices.[2]Zero Carbon Charge, “Eastern Cape Launch,” Zero Carbon Charge, charge.co.za Where chargers do not include IEC 62955-compliant residual direct current detection, Type B RCCBs are required because standard AC or A devices can become ineffective in the presence of smooth DC leakage currents. This matters because Type B units carry a strong price premium over standard alternatives. Even moderate growth in EV charging locations can therefore lift revenue more quickly than unit volumes alone would suggest. That shift is helping reshape the South Africa residual current circuit breaker market toward higher-value products, especially in utilities, infrastructure, and commercial transport corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrical component inflation and tender price pressure | -1.5% | National, amplified by Red Sea shipping rerouting and copper price volatility | Short term (≤ 2 years) |

| Rooftop solar slowdown after easing of load shedding | -0.9% | National, most pronounced in the residential segment across all provinces | Short term (≤ 2 years) |

| SSEG registration, smart-meter, and tariff-migration friction | -0.6% | Eskom-supplied areas, especially suburban and peri-urban locations | Medium term (2-4 years) |

| Installer competency gaps in mixed-source protection coordination | -0.5% | National, more pronounced in semi-urban and rural markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrical Component Inflation and Tender Price Pressure

Copper prices moved above USD 10,000 per metric ton in 2024, while global logistics disruptions linked to Red Sea rerouting extended transit times and raised landed costs for South African electrical component buyers. RCCBs depend on copper in contact systems, bus bars, and trip assemblies, so material inflation feeds directly into supplier cost pressure. Importers and distributors then face a difficult choice between protecting margins and keeping products affordable in price-sensitive channels. The strain is stronger in public tenders, where price-revision mechanisms are often limited during the contract period and bids can be exposed to sudden cost changes. Smaller distributors and local assemblers are more vulnerable because they have less scale for hedging and less flexibility on working capital. This pressure can slow adoption in lower-budget projects and acts as a practical brake on the South Africa residual current circuit breaker market even when underlying compliance demand remains intact.

Rooftop Solar Slowdown After Easing of Load Shedding

The easing of load shedding from mid-2024 reduced the urgency that had driven many residential solar purchases during the peak crisis years. SAPVIA indicated that new solar installations fell from 2.4 GW in the 2023/24 financial year to 1.0 GW in 2024/25, which temporarily narrowed one of the strongest recent demand channels for protection retrofits. Because each new solar installation usually triggers a board inspection and at least one protection adjustment, slower solar deployment translates into softer near-term demand in the residential channel. The deeper issue is that part of the surge in 2022 and 2023 was crisis-led, so normalized grid conditions can expose how much demand had been pulled forward. SAPVIA still expects annual installations to recover toward 3 GW, which limits the downside if tariff pressure and financing remain supportive. The South Africa residual current circuit breaker market, therefore, faces a near-term drag from slower residential solar, but not a collapse, because compliance still sets a floor for replacements and upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: AC Dominance Masking a Rapid Shift to Higher-Order Protection

AC Type RCCBs held 46.8% of the South Africa residual current circuit breaker market share in 2025, which reflected the large installed base of conventional residential and light-commercial circuits built around single-supply AC systems. A Type RCCBs remained the second-largest group because they fit many retrofit applications where solar inverters are present, but protection needs have not yet moved to full smooth-DC detection. B-type RCCBs are projected to expand at a 9.4% CAGR through 2031, making them the fastest-growing product class in the South Africa residual current circuit breaker market. Their stronger growth comes from EV charging stations, variable-frequency drives, and inverter-led systems that can produce leakage patterns outside the range of AC-only devices. The growth gap between AC and B-type products points to a clear mix shift that should lift average selling prices over time. That means revenue growth in this product set is being shaped by technical migration as much as by installation counts.

F Type RCCBs sit between A Type and B Type products and are becoming more relevant in commercial rooftop solar and smaller EV charge-point applications. Their role grows when the charger or related equipment already includes an IEC 62955-compliant RDC-DD, which lowers the need for a full Type B device in some use cases. CHINT’s NB1L-20 Slim RCBO illustrates the direction of product development, with a narrow 18 mm 1P+N footprint and voltage-independent electromagnetic operation for boards where space is limited. Tighter compliance under SANS 10142-1:2024 and EV-related standards is reducing tolerance for under-classified protection, which supports ongoing product upgrades. As a result, even where AC devices still dominate current volume, the South Africa residual current circuit breaker market is steadily moving toward higher-spec protection across new builds and retrofits.

By Pole Configuration: Two-Pole Volume Leadership Contrasted With Four-Pole Commercial Momentum

Two-Pole RCCBs retained 61.5% of the South Africa residual current circuit breaker market in 2025, while Four-Pole RCCBs are projected to grow at an 8.1% CAGR through 2031. Two-Pole units still lead because South Africa’s residential wiring base remains largely single-phase, and most final circuits in domestic boards are served by two-pole devices. That installed base is especially important in Gauteng, Western Cape, and KwaZulu-Natal, where population density, commercial activity, and retrofit intensity remain the highest. The volume foundation for the South Africa residual current circuit breaker market, therefore, still sits with residential two-pole replacement demand. Even so, the pace of new applications is shifting toward more complex boards that require multi-phase protection. This keeps the leading share with two-pole devices while increasing the value contribution from four-pole products.

Schneider Electric’s locally available Resi9 changeover switch shows that even residential-grade boards are being adapted to more complex supply arrangements, such as backup and alternate sources. Infrastructure South Africa is overseeing 305 projects, with 34 projects valued at R259 billion (~USD 15.91 billion) expected to come to market within 12 to 18 months, and these projects often specify three-phase distribution from the design stage. Commercial solar-plus-battery systems in the 50 kVA to 100 kVA range also push more sites toward three-phase boards and four-pole main-board protection. This means four-pole growth is being supported by both retrofit activity and planned construction in public and commercial assets. Over time, that combination should gradually rebalance the South Africa residual current circuit breaker market toward a larger share of higher-value multi-pole protection.

By Rated Current: Mid-Range Dominance With High-Current Growth Driven by Industrial and Infrastructure Loads

Above 25A to 63A devices accounted for 52.7% of the South Africa residual current circuit breaker market size in 2025, which reflects the wide use of 40A and 63A protection in household boards and light-commercial circuits. This current band fits the most common South African domestic configurations, including dedicated protection for stoves, geysers, air conditioners, and solar inverter circuits. It also captures a large share of smaller commercial sub-circuits, which broadens its replacement cycle beyond housing alone. Up to 25A devices remain relevant for lighting circuits, bathroom isolators, smaller loads, and older premises where board subdivision is becoming more common under current compliance expectations. Growth in this lower band is more modest because it depends heavily on incremental board reconfiguration rather than on large new electrical loads. Even so, it remains an important maintenance layer within the South Africa residual current circuit breaker market because enforcement is pushing older installations toward more granular protection layouts.

Above 63A devices are projected to grow at an 8.8% CAGR through 2031, making them the fastest-expanding rated-current segment in the South Africa residual current circuit breaker market. This band is being supported by industrial sub-distribution, utility-grid interface points, and large EV charging bays that operate far above standard residential load levels. Zero Carbon Charge’s 480 kW liquid-cooled DC charging systems illustrate the type of installation where four-pole Type B protection above 63A becomes mandatory. South Africa’s public infrastructure commitment is above R1 trillion, including R70.5 billion (~USD 4.33 billion) for energy infrastructure, adding a structural demand base for higher-current devices in electrification, transport, and utility projects. NERSA’s direct registration requirements for SSEG installations above 100 kVA also make the commercial and industrial compliance route more visible. These factors give suppliers a clearer demand path in the upper current bands than in purely discretionary residential channels.

By End User: Residential Scale Funding the Base, Utilities Providing the Growth Engine

Residential users held 41.9% of the South Africa residual current circuit breaker market share in 2025, while Utilities and Infrastructure are projected to expand at a 9.1% CAGR through 2031. Residential demand stays the largest because South Africa’s housing stock is extensive, and compliance checks at property sale, renovation, and insurance review create recurring replacement demand. That makes the household channel the volume base of the South Africa residual current circuit breaker market, even when new housing activity is uneven. At the same time, the Nedbank Capital Expenditure Project Listing showed R445.9 billion (~USD 27.40 billion) in new projects announced in 2024, up from R210.1 billion (~USD 12.91 billion) in 2023, with public corporations committing R150.5 billion (~USD 9.25 billion) to energy, water, health, airport, and road projects. That project flow creates stronger demand for above-63A, four-pole, and higher-spec Type A and Type B devices in interface panels, reticulation boards, and solar-linked installations. Utilities and infrastructure, therefore, provide the fastest growth engine, while residential replacement work continues to fund the demand base.

Commercial end users add demand through solar self-generation, building-management upgrades, and compliance-driven board modernization across offices, retail centers, and hospitality properties. Industrial users are also moving beyond simple AC protection as variable-frequency drives and mixed-frequency loads become more common in process plants and heavy facilities. More than 1 million South African homes had solar by late 2025, and rooftop PV capacity reached 7,300 MW by September 2025, up 215% from the August 2022 baseline, which creates a large installed base for follow-on protection work. That installed base matters because solar-linked households will continue to need inspection, replacement, and reclassification of protection devices over time. The South Africa residual current circuit breaker market, therefore, gains from both new installation cycles and the service burden attached to the growing solar base. This is why residential remains the largest segment today, even though utilities and infrastructure are set to grow faster over the forecast period.

Geography Analysis

Gauteng remained the leading provincial demand center in 2025 because it combines the country’s largest population base, the biggest concentration of commercial floor space, and an estimated 2.2 GW of embedded rooftop solar by mid-2025. That scale supports demand from both residential retrofit work and commercial board upgrades. Western Cape followed closely because Cape Town continued to see active building approvals, stronger higher-income residential demand, and good conditions for solar-linked investment. KwaZulu-Natal ranked third, supported by light-industrial activity around Durban, logistics demand along the N3 corridor, and the rise of EV charging routes between major urban centers. Compliance under SANS 10142-1:2024 and the NERSA SSEG framework applies across all provinces, so installers cannot reduce specification levels by shifting geography. That uniform compliance floor gives the South Africa residual current circuit breaker market a national baseline, even though provincial demand intensity differs.

The Eastern Cape and Northern Cape are smaller in current volume, but they are strategically important for project-led demand over the next several years. The Eastern Cape hosts Zero Carbon Charge’s 29-station off-grid EV charging rollout and the Coega Special Economic Zone’s 100 MW solar farm, both of which create concentrated demand for four-pole, above-63A, and B Type devices during construction and commissioning. Northern Cape is tied to utility-scale renewables and major logistics infrastructure such as the Boegoebaai Port and Rail Development project, which could lift its contribution later in the forecast period as projects move from planning to execution. Nationally, new projects announced reached R445.9 billion in 2024, more than double the R210.1 billion announced in 2023, with energy and water among the fastest-growing public capex categories. This supports the view that geography within the South Africa residual current circuit breaker market will increasingly be shaped by infrastructure clusters as well as household retrofit demand.

Limpopo, Mpumalanga, and North West form the mining-heavy demand tier, where industrial sub-distribution boards, pump houses, processing plants, and worker accommodation require robust four-pole and above-63A protection. Cost pressure in mining and industrial operations can delay discretionary upgrades, but regulatory compliance and electrical audit programs still preserve a base level of replacement demand. North West Province’s construction sector grew 20.5% in the final part of 2024, which points to near-term improvement in a province that had previously seen less project intensity. Embedded generation projects without a point of connection to the grid are exempt from NERSA registration, but grid-tied SSEG systems below 100 kVA must register with the relevant distributor, which systematically surfaces hidden protection-upgrade needs across provinces. That compliance mechanism keeps the South Africa residual current circuit breaker market active well beyond the main metropolitan demand centers.

Competitive Landscape

The South Africa residual current circuit breaker market is moderately fragmented, with global manufacturers strongest in specification-led channels and Chinese suppliers active in price-sensitive distribution and wholesale. Schneider Electric, ABB, and Siemens lead the premium tier because they benefit from EPC specifications, municipal approval pathways, and the documentation standards tied to compliance work. Schneider Electric’s Acti9 iID RCCB range remains a common benchmark in residential and commercial design specifications and is widely stocked through South African distribution networks. ABB’s F200 B-Type devices address EV charging and variable-frequency-drive installations that require higher-order fault detection, and the company reinforced its protection position through its Enlit Africa 2025 presence and later activity at the AMEU Convention in October 2025. Siemens supports specifier confidence with its 5SV3 RCCB and 5SV1 RCBO portfolio, which presents a clear progression from Type A through Type B use cases in line with IEC 62423. This premium group shapes standards and specifications, but it does not lock up the South Africa residual current circuit breaker market because end demand still moves through many distributors and contractors.

CBI-electric low voltage has an advantage in local manufacturing, and its Switch Ultra range helps the company stay relevant when contractors are sensitive to lead times, availability, and rand-linked import costs. CHINT and Noark compete more aggressively on landed cost, warranty terms, and product breadth, which gives them traction in the middle of the market where buyers compare price and functionality very closely. ElectroMechanica’s 2025/26 catalogue expansion, including Hager quadro evo boards and the ELKO EP partnership, shows how distributors are broadening bundled offerings instead of relying on single-product sales. This channel strategy matters because bundled supply reduces direct product commoditization and makes distributor relationships more valuable than one-off device pricing. It also reinforces the open-channel structure of the South Africa residual current circuit breaker market.

White-space opportunities are strongest in above-63A B Type devices and in smart RCCBs with remote trip, self-test, and monitoring features. No single supplier holds a commanding domestic position, because distributor-led sales keep share dispersed across multiple global, local, and imported brands. Recent strategic moves support that pattern, including Siemens South Africa’s May 2026 localization of 8DA gas-insulated medium-voltage switchgear manufacturing and Schneider Electric’s May 2026 launch of an enhanced breaker communication module for connected low-voltage panels. These moves deepen local capability and digital functionality, but they do not remove the central role of wholesalers and distributors in route-to-market execution. The South Africa residual current circuit breaker market, therefore, remains competitive, specification-sensitive, and open enough for several players to grow without one company taking clear control.

South Africa Residual Current Circuit Breaker (RCCB) Industry Leaders

Schneider Electric

ABB

CBI-electric: low voltage

Hager Group

CHINT Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Siemens South Africa announced the localisation of its 8DA gas-insulated medium-voltage switchgear manufacturing in partnership with Private National Grid (PNG), producing the first locally made 8DA units for the South African market and reducing lead times and import exposure for grid-protection equipment.

- October 2025: Eskom simplified the SSEG compliance and registration process for residential solar customers, allowing DEL-registered persons, instead of ECSA-registered engineers, to sign off systems from October 2025, a regulatory streamlining expected to stimulate renewed rooftop solar installations and associated RCCB upgrades.

South Africa Residual Current Circuit Breaker (RCCB) Market Report Scope

Residual Current Circuit Breaker (RCCB) is a pivotal electrical safety device designed to shield humans from potentially fatal electric shocks and to avert electrical fires due to current leakages. The RCCB operates by perpetually overseeing the equilibrium between the incoming and outgoing currents within a circuit.

The South Africa Residual Current Circuit Breaker (RCCB) Market is segmented into product type, pole configuration, rated current, and end-user. By product type, the market is segmented into AC type, A type, F type, and B type RCCBs. By pole configuration, the market is segmented into two-pole and four-pole systems. By rated current, the market is segmented into up to 25A, above 25A to 63A, and above 63A. By end-user, the market is segmented into residential, commercial, industrial, and utilities and infrastructure sectors. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| AC Type RCCB |

| A Type RCCB |

| F Type RCCB |

| B Type RCCB |

| Two-Pole RCCB |

| Four-Pole RCCB |

| Up to 25A |

| Above 25A to 63A |

| Above 63A |

| Residential |

| Commercial |

| Industrial |

| Utilities and Infrastructure |

| By Product Type | AC Type RCCB |

| A Type RCCB | |

| F Type RCCB | |

| B Type RCCB | |

| By Pole Configuration | Two-Pole RCCB |

| Four-Pole RCCB | |

| By Rated Current | Up to 25A |

| Above 25A to 63A | |

| Above 63A | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| Utilities and Infrastructure |

Key Questions Answered in the Report

What is the 2031 outlook for the South Africa residual current circuit breaker market?

The South Africa Residual Current Circuit Breaker Market size was valued at USD 30.30 million in 2025 and is estimated to grow from USD 31.99 million in 2026 to reach USD 46.88 million by 2031, at a CAGR of 7.94% during the forecast period (2026-2031).

Which product type leads current demand in South Africa?

AC Type RCCBs held the largest share at 46.8% in 2025 because much of the installed base still consists of conventional residential and light-commercial AC systems.

Which RCCB category is growing the fastest in South Africa?

B Type RCCBs are growing the fastest at a 9.4% CAGR through 2031, supported by EV charging, variable-frequency drives, and more complex inverter-based electrical systems.

Why are utilities and infrastructure growing faster than residential demand?

Utilities and Infrastructure are expanding at a 9.1% CAGR because South Africa's large public project pipeline is creating new demand for higher-current, multi-pole, and higher-spec protection devices.

How does rooftop solar affect RCCB demand in South Africa?

Solar and hybrid systems increase both the number of protection upgrades and the shift toward Type A, F, and B devices, although slower residential solar additions after easing load shedding have softened one demand channel.

Which rated-current band is the largest in current installations?

Above 25A to 63A devices led with 52.7% share in 2025 because they fit the most common household and light-commercial load points such as stoves, geysers, air conditioners, and inverter-linked circuits.

Page last updated on: