Nigeria Molded Case Circuit Breaker Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

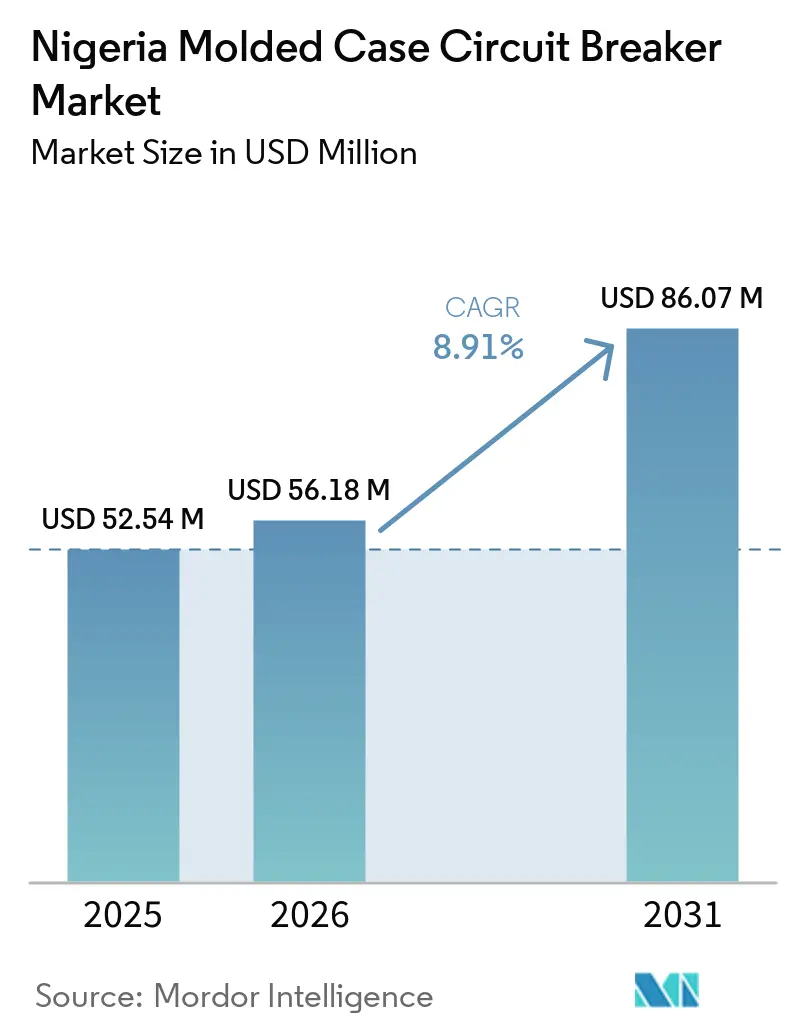

| Base Year Market Size (2025) | USD 52.54 Million |

| Market Size (2026) | USD 56.18 Million |

| Market Size (2031) | USD 86.07 Million |

| Growth Rate (2026 - 2031) | 8.91% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nigeria Molded Case Circuit Breaker Market Analysis by Mordor Intelligence

The Nigeria Molded Case Circuit Breaker Market size is projected to expand from USD 52.54 million in 2025 and USD 56.18 million in 2026 to USD 86.07 million by 2031, registering a CAGR of 8.91% between 2026 to 2031. The Nigeria molded case circuit breaker market is being supported by 2 separate demand streams, one from public grid upgrades and another from private users that continue to build around weak distribution reliability. Captive generation remained a major base of demand, with more than 250 licensed firms and institutions operating large self-supply systems by end-2025, which kept protection equipment purchases active even when utility procurement moved slowly. Federal power policy and transmission rehabilitation are widening the project pipeline, including the National Integrated Electricity Policy and the USD 328.8 million transmission line contract signed under the Presidential Power Initiative in April 2025. Tighter safety enforcement is also shifting buyers toward certified products, as Nigerian Electricity Management Services Agency (NEMSA) expanded audits across Distribution Companies (DISCOs) and pushed for stronger checks on imported electrical equipment. At the same time, suppliers are adjusting their product mix across premium and value tiers, while foreign exchange pressure continues to raise import costs and stretch procurement timelines.

Key Report Takeaways

- By rated current, the 75A to 250A segment held 40.1% share in 2025, while the 250A to 800A segment is forecast to expand at a 9.2% CAGR through 2031.

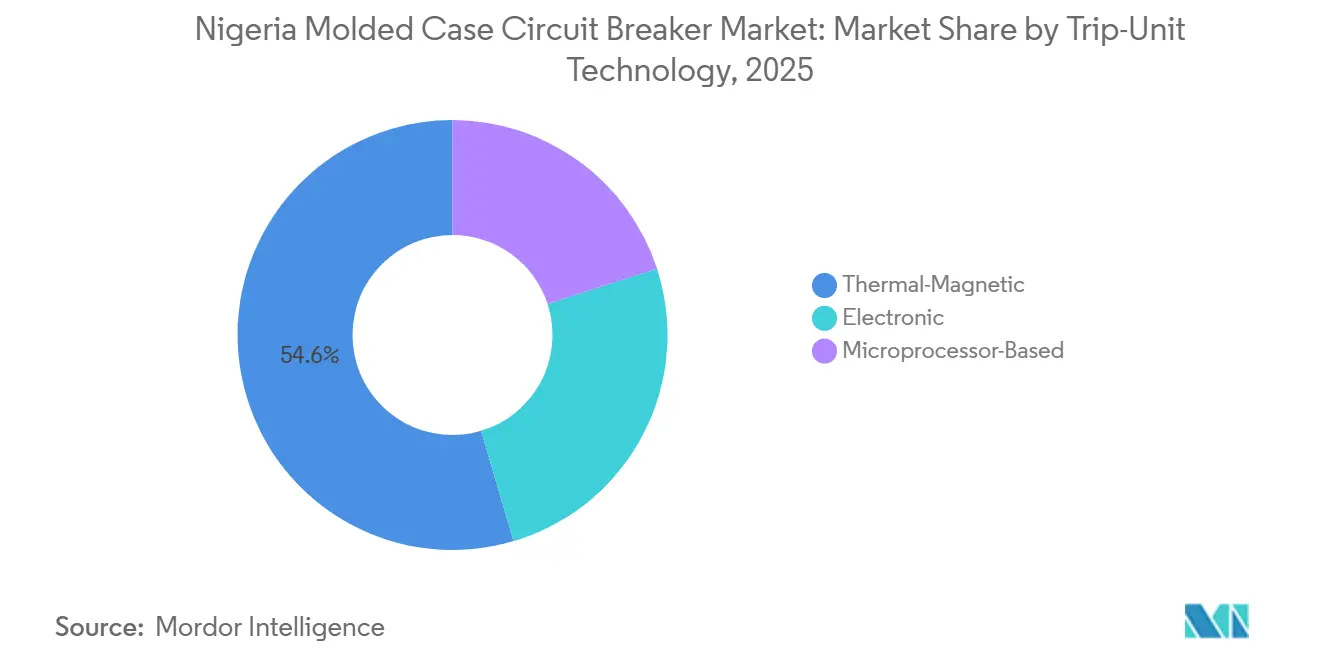

- By trip-unit technology, thermal-magnetic units accounted for 54.6% share in 2025, while microprocessor-based devices are projected to grow at a 10.1% CAGR through 2031.

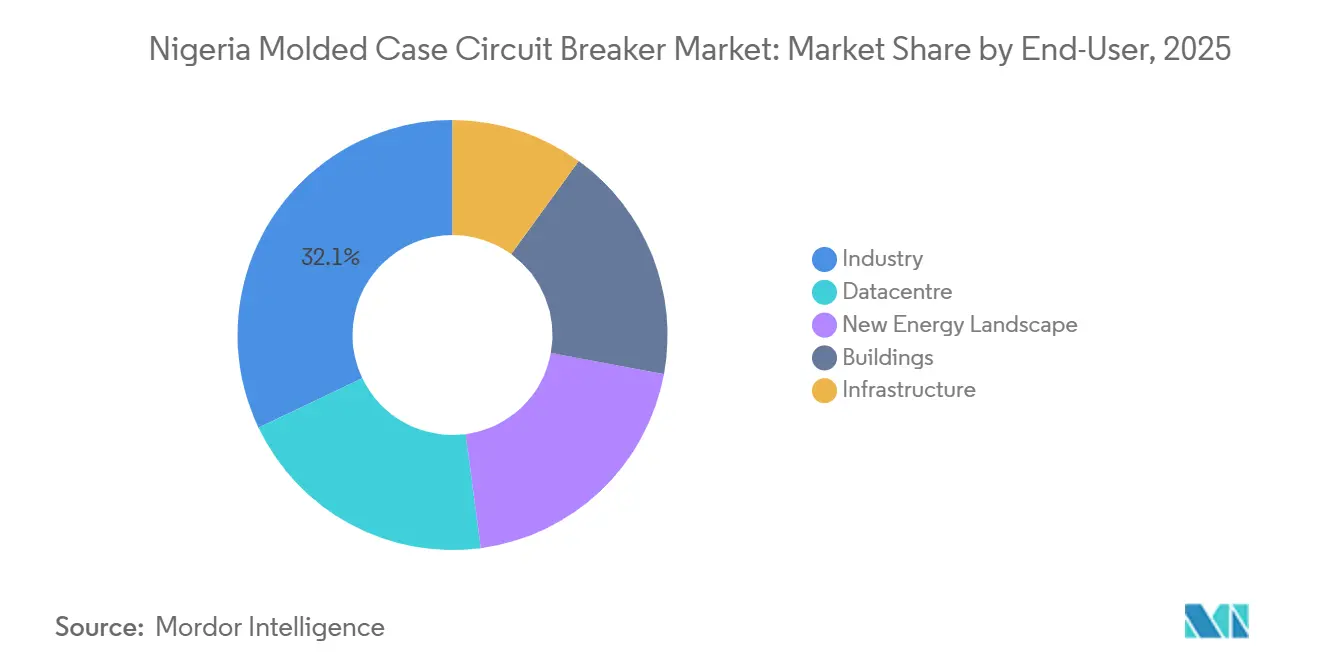

- By end user, industry held 32.1% share in 2025, while datacentre is projected to grow at an 11.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Molded Case Circuit Breaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid rehabilitation and DISCO network reinforcement | +1.8% | National, with concentration in Lagos, Abuja, Kano, and Port Harcourt corridors | Medium term (2-4 years) |

| Solar mini-grid and distributed electrification rollout | +1.2% | National, with early gains in Niger, Kogi, Jigawa, and other underserved states | Short term (≤ 2 years) |

| Commercial and industrial captive-power expansion | +1.5% | Lagos, Abuja FCT, Rivers State, Ogun State industrial clusters | Medium term (2-4 years) |

| Data-centre and critical-facility electrical build-outs | +1.4% | Lagos, with Port Harcourt as an emerging node | Short term (≤ 2 years) |

| Electricity Act-driven state power-market liberalisation | +1.1% | National, with earlier gains in states enacting their own Electricity Acts | Long term (≥ 4 years) |

| NEMSA-led safety enforcement on installations and imports | +0.6% | National, with port-of-entry enforcement concentrated in Apapa, Tin Can Island, and Onne | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Rehabilitation and Distribution Company (DISCO) Network Reinforcement

Nigeria’s grid rehabilitation cycle is creating a steadier demand pattern for molded case circuit breakers because each substation upgrade and feeder extension needs panel-level protection devices. Transmission Company of Nigeria (TCN) said USD 1.16 billion in development partner funding helped lift national wheeling capacity to 8,700 MW in 2025, and the system was targeting another 4,000 MW through Engineering, Procurement, and Construction (EPC) engagements by end-2026. The Nigeria molded case circuit breaker market is also benefiting from the transmission restructuring process, because separate operating entities increase the number of institutional buyers involved in protection procurement. The April 2025 PPI Phase I contract covered 14 brownfield substation upgrades and 21 greenfield substations, which points to direct downstream demand for internationally specified switchgear panels. At the distribution level, utilities have a stronger financial reason to reduce faults and outages on feeders serving higher-paying commercial users. That keeps replacement and upgrade demand active even when large generation projects take longer to move.

Solar Mini-Grid and Distributed Electrification Rollout

Distributed electrification is becoming a reliable volume source for the Nigeria molded case circuit breaker market because each new mini-grid needs protection at the generation output and at the feeder level. REA said it deployed more than 200 mini-grids through 2025 and is working toward 1,350 installations under the USD 750 million DARES program.[1]Source: Rural Electrification Agency, “REA Deploys Over 200 Mini-Grids in 2025,” Rural Electrification Agency, rea.gov.ng The program also moved into implementation in April 2025 when REA signed deals with 8 renewable energy firms for energy access projects in multiple communities. Most isolated systems use smaller breaker ratings, which ties this rollout closely to the 75 A to 250 A product band. As projects move from stand-alone systems to interconnected mini-grids, developers need better coordination between upstream and downstream protection points. That is a slowly increasing demand for adjustable trip units instead of fixed devices in parts of the solar project base.

Commercial and Industrial Captive-Power Expansion

Captive generation remains one of the strongest supports for the Nigeria molded case circuit breaker market because firms continue to invest in self-supply when public network reliability is weak. NERC-linked reporting showed that 249 firms and institutions held captive power permits by end-2025, while another report highlighted that the broader installed base had crossed 6,500 MW among more than 250 licensed entities. In the fourth quarter of 2025 alone, 11 new captive permits were issued with a combined capacity of 130.2 MW, led by Abuja Steel Mill Nigeria Limited and Yongxing Steel Company Limited. The use case is broadening as well, because MTN Nigeria secured permits for 4 Lagos plants with a combined capacity of 15.9 MW, showing that telecom operators are now part of the same demand pool as manufacturers and heavy industry. Each captive site needs MCCBs at the generator output, transfer switching, and sub-distribution points. As plant size rises, the need for higher current ratings and more advanced trip coordination also rises.

Data-Centre and Critical-Facility Electrical Build-Outs

As new digital infrastructures cluster in Lagos, critical facilities are driving the Nigerian molded case circuit breaker (MCCB) market towards more sophisticated protection needs. In July 2025, MTN Nigeria inaugurated its Dabengwa Data and Cloud Centre in Ikeja. Just months earlier, in March 2025, OADC unveiled plans for a USD 240 million, 24 MW hyperscale facility in Lekki. These burgeoning sites, spanning from the main incomer to the UPS and PDU layers, necessitate a comprehensive range of MCCBs. Furthermore, with mandatory backup generation systems in place, there's an added demand for breaker coordination to ensure stable load transfers. This underscores the rising preference for microprocessor-based products in Nigeria. Highlighting the significance of this trend, a June 2025 collaboration between Eaton and Siemens Energy underscored the evolving landscape, with top suppliers now recognizing data centres as a unique channel for integrated power and switchgear solutions.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX volatility and import-cost inflation | -1.5% | National, with the sharpest effect on Lagos-based distributors and project procurement teams | Medium term (2-4 years) |

| Low-cost import price compression | -1.2% | National, with the strongest effect in Alaba International Market and Ojo distribution hubs in Lagos | Short term (≤ 2 years) |

| Certification, customs, and inspection lead-time friction | -0.5% | Apapa, Tin Can Island, and Onne port nodes, with spillover into project timelines nationwide | Medium term (2-4 years) |

| Weak downstream panel quality and installation practices | -0.4% | National, with greater exposure in north-central and south-east states where authorized panel-builder networks are thinner | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FX Volatility and Import-Cost Inflation

Foreign exchange pressure is the clearest near-term restraint on the Nigeria molded case circuit breaker market because most branded products and many components still come from outside the country. MAN said imported materials costs rose 118% to NGN 6.64 trillion in 2024, which was equal to USD 4.1 billion, and member firms recorded NGN 1.62 trillion in cumulative forex losses, equal to USD 1.0 billion.[2]Source: This Day Live. "MAN Bemoans Surge in Imported Raw Materials Cost by 118%, N1.62trn FX Losses." June 2025. thisdaylive.com BusinessDay also noted that the electrical and electronics subsector remained well behind other manufacturing lines in local raw material substitution.[3]Source: Business Day. "Schneider Electric Expands West African Portfolio with GoPact Electrical Solutions." August 2025. businessday.ng For distributors, this makes catalog pricing unstable and reduces willingness to hold inventory for long periods. For contractors, it raises the risk that quoted project budgets will not hold through procurement and delivery. The result is slower order closure, tighter working capital, and more frequent shifts toward cheaper alternatives.

Low-Cost Import Price Compression

Low-cost imports are a second major restraint because they keep pricing pressure high in the commercial and small industrial tiers of the Nigeria molded case circuit breaker market. Chinese and Indian suppliers are widely used through Lagos trading channels and often sell IEC-certified or claimed-certified products at large discounts to European brands. That pricing gap is strongest where project owners care more about first cost than product documentation or lifecycle performance. NEMSA said substandard electrical products continue to enter the country, and it began pursuing closer cooperation with the Nigeria Customs Service to improve screening. Enforcement is improving, but gaps at the distribution tier still allow uncertified products to undercut better-known brands. This keeps the premium segment intact, but it makes margin protection much harder in the mid-tier and entry-level categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rated Current: Industrial Expansion Lifts Mid-to-High Current Demand

The 75 A to 250 A range held 40.1% of the Nigeria molded case circuit breaker market share in 2025. Its lead came from commercial buildings, DISCO feeder panels, and light industrial captive power boards, where this rating band fits common distribution needs. Thermal-magnetic products still dominate much of this bracket because they meet baseline protection requirements at lower cost. The up to 75 A tier remains tied to residential sub-distribution and small retail applications, where purchasing power is weaker, and exposure to substandard imports is higher. The Nigeria molded case circuit breaker market size for the 250 A to 800 A range is projected to grow at a 9.2% CAGR through 2031, which makes it the fastest-moving rated current band in the report.

That faster growth reflects stronger capital spending in industrial captive plants, mini-grid interconnection points, and data-center distribution systems. These applications need more fault-handling capability and better coordination than small commercial panels. The above 800 A segment stays low in unit volume, but it commands higher prices because it is used in substation incomers, heavy industrial motor control centers, and large digital facilities. Demand in the Nigeria molded case circuit breaker market is therefore shifting from older commercial fit-outs toward larger and more technically specified projects. That change does not remove demand in the 75 A to 250 A band, but it does mean that incremental value growth is moving toward mid-to-high current products.

By Trip-Unit Technology: Thermal-Magnetic Retains Volume Lead While Microprocessor-Based Gains Ground

Thermal-magnetic units accounted for 54.6% share in 2025, which kept them in the lead across the Nigeria molded case circuit breaker market. Their position remains strongest in the 75 A to 250 A band and in cost-sensitive installations where fixed-current protection is enough for the job. Electronic trip-unit MCCBs continue to serve as the middle option, especially in commercial projects that need selectivity between breaker levels without full digital functionality. Microprocessor-based devices are projected to grow at a 10.1% CAGR through 2031, which makes them the fastest-growing trip-unit type. That growth is tied to data centers, larger captive plants, and more advanced distribution panels where real-time monitoring and remote control are becoming normal requirements.

Schneider Electric’s August 2025 launch of the MasterPact MTZ Active in West Africa matched this shift because it brought cloud-linked and retrofit-ready functionality into the regional product mix.[4]Source: Engineering News. "Schneider Electric Launches MasterPacT MTZ Active Circuit Breaker in West Africa." August 18, 2025. engineeringnews.co.za The move matters in Nigeria because many existing switchboards need upgrades without full panel replacement. IEC 60947-2 remains the core compliance framework across all trip-unit categories, and NEMSA certification gives tested brands a clearer edge where projects are formally inspected. In practice, thermal-magnetic products will continue to carry most of the volume, while microprocessor-based products take a larger share of project value. That keeps the technology mix broad rather than replacing one product type with another.

By End User: Industry Leads in Share While Data Center Commands the Growth Premium

Industry held 32.1% share in 2025, giving it the leading end-user position in the Nigeria molded case circuit breaker market. Its base is wide, covering steel, petrochemicals, cement, food processing, telecom infrastructure, and other captive-power users that run independent electrical systems. Buildings remained the second-largest user group, supported by office towers, logistics space, retail assets, and apartment projects in Lagos, Abuja, and Port Harcourt. This sustained demand for low-voltage electrical equipment. Infrastructure demand was supported by distribution network upgrades undertaken by electricity distribution companies (DISCOs), Transmission Company of Nigeria (TCN) feeder and substation projects, and public-sector building developments. The expanding deployment of solar mini-grids and hybrid power systems continued to drive demand from the new energy segment.

Data center is forecast to grow at an 11.7% CAGR through 2031, making it the fastest-growing end-user group in the report. That premium reflects a clear build-out path in Lagos, where MTN and Open Access Data centers (OADC) moved forward with large facilities in 2025. A data center uses MCCBs at far more points than a standard commercial building because protection is needed at utility intake, backup generation, uninterruptible power supply (UPS) systems, and power distribution unit (PDU) layers. That higher breaker density means even a limited number of projects can generate strong value demand. It also helps explain why digital facilities are pulling the product mix toward higher ratings and more advanced trip technology.

Geography Analysis

The Southwest was the largest demand center within the Nigeria molded case circuit breaker market in 2025. Lagos and Ogun carried this lead because they combine commercial real estate, industrial clusters, import channels, and nearly all of the country’s large data-centre projects. Lagos also remains the main entry point for imported switchgear and related panel components, which strengthens its role in both distribution and project execution. Schneider Electric’s choice to place its West Africa headquarters in Ikeja with a network of more than 300 channel partners reflected the scale of this corridor. Specification discipline is also stronger in the Southwest because panel builders, distributors, and inspectors are more concentrated there.

The South-South is the main high-current industrial zone for the Nigeria molded case circuit breaker market. Rivers, Delta, Bayelsa, and Akwa Ibom generate demand from oil and gas sites, process industries, and large captive generation systems. Nigeria LNG in Rivers State runs 360 MW of captive power, while Dangote Group’s broader industrial power capacity exceeds 1,500 MW, which shows why larger breaker categories are more common in this zone. Projects in this part of the country also lean more heavily toward electronic and microprocessor-based trip units because coordination with downstream motor protection is more important. The South-South, therefore, contributes more value per project even when the number of sites is lower than in the Southwest.

The North and North-Central form a different demand pool inside the Nigeria molded case circuit breaker market. Abuja, Kano, Kaduna, and surrounding areas rely more on public buildings, state-level commercial construction, manufacturing clusters, and expanding rural electrification activity. Rural Electrification Agency (REA)’s work on more than 21 mini-grid projects in Jigawa illustrated how northern states are starting to generate a steady stream of smaller breaker demand at both generation and distribution points. This region also shows a wider gap between certified and uncertified products because authorized channel coverage is thinner and inspection density is lower. That makes the north important for unit volume growth, but also more exposed to price-led competition and quality variation.

Competitive Landscape

The Nigeria molded case circuit breaker market remains moderately fragmented. Global Tier-1 brands such as Schneider Electric, ABB, Siemens, and Eaton lead the certified-product tier, while CHINT, Legrand, LS Electric, Hager, C&S Electric, Delixi, and other import-driven suppliers compete across the mid-market and value bands. This structure means no single supplier controls demand across all buyer types, because procurement standards differ sharply between industrial projects, utility-linked work, data centers, and informal distribution channels. Schneider Electric has built one of the clearest market positions through a three-level product approach that spans GoPact for price-sensitive buyers, ComPacT NSX for mainstream use, and MasterPacT MTZ Active for advanced industrial and digital applications. The company’s Lagos base and broad partner network also give it a stronger local reach than many multinational peers.

ABB follows a more project-led route in Nigeria through AOS Orwell, where the emphasis is on engineering support and technology transfer rather than broad volume distribution. Eaton and Siemens are also better placed in larger and more technical installations where panel design, coordination, and lifecycle support matter more than entry price. WEG’s expansion of its local manufacturing footprint in May 2026 showed another route into the region, one that can lower lead times and reduce foreign exchange exposure. For mid-tier suppliers, the best opening is in projects that need IEC-compliant products but still face budget pressure. That is especially relevant in solar-hybrid installations, commercial buildings, and generator-backed facilities, where certification standards are rising but buyers still watch landed cost closely.

The main competitive divide in the Nigeria molded case circuit breaker market is therefore not only brand against brand, but certified formal channels against lower-cost informal supply. NEMSA enforcement is slowly raising the barrier for undocumented imports, which favors suppliers that can prove compliance and provide technical support. Even so, Alaba-linked distribution keeps price pressure high in the commercial and SME segments. Strategic moves by leading firms already reflect this split, including Schneider Electric’s dual launch of premium and value MCCB lines, ABB’s engineering-led local capability push, and WEG’s regional manufacturing expansion. The companies that can balance product certification, delivery reliability, and channel depth are likely to gain the most ground over the forecast period.

Nigeria Molded Case Circuit Breaker Industry Leaders

-

Schneider Electric SE

-

ABB Ltd.

-

Siemens AG

-

Eaton Corp plc

-

Chint Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: WEG Africa deepened its local manufacturing footprint in Sub-Saharan Africa in May 2026, reducing import lead times and FX exposure for key electrical product lines. The move positions WEG to compete more effectively against Chinese manufacturers in the sub-USD 250 A switchgear tier across Nigeria and neighboring markets.

- August 2025: Schneider Electric introduced its flagship digital circuit breaker, rated up to 6,300 A with Bluetooth, NFC, and cloud connectivity, in West Africa on August 18, 2025, targeting industrial and data center customers seeking integrated energy management without panel modification.

- June 2025: Eaton and Siemens Energy formalized a collaboration to deliver integrated on-site power generation and standardized modular switchgear systems for data center developers globally, with the African market identified as a priority growth corridor.

- April 2025: The Federal Government signed the EPC&F contract with China Machinery Engineering Corporation for rehabilitation and construction of 544 km of 330 kV and 132 kV transmission lines, with 14 brownfield and 21 greenfield substations requiring switchgear upgrades at the distribution interface.

Nigeria Molded Case Circuit Breaker Market Report Scope

A Molded Case Circuit Breaker (MCCB) is an electrical protection device used to prevent damage to circuits caused by overloads, short circuits, and ground faults. Enclosed in a robust, insulated housing, MCCBs are commonly utilized in commercial and industrial applications with higher amperage requirements, supporting currents of up to 2,500 Amps.

The Nigeria Molded Case Circuit Breaker Market is segmented into rated current, trip-unit technology, end-user, and geography. By rated current, the market is segmented into up to 75A, 75A–250A, 250A–800A, and above 800A. By trip-unit technology, the market is segmented into thermal-magnetic, electronic, and microprocessor-based trip units. By end-user, the market is segmented into buildings, industry, infrastructure, datacentres, and the new energy landscape. The report also covers the market size and forecasts for the molded case circuit breaker market in Nigeria. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Upto 75A |

| 75A - 250A |

| 250A - 800A |

| Above 800A |

| Thermal-Magnetic |

| Electronic |

| Microprocessor-Based |

| Buildings |

| Industry |

| Infrastructure |

| Data Center |

| New Energy Landscape |

| By Rated Current | Upto 75A |

| 75A - 250A | |

| 250A - 800A | |

| Above 800A | |

| By Trip-Unit Technology | Thermal-Magnetic |

| Electronic | |

| Microprocessor-Based | |

| By End User | Buildings |

| Industry | |

| Infrastructure | |

| Data Center | |

| New Energy Landscape |

Key Questions Answered in the Report

What is the current value of the Nigeria molded case circuit breaker space in 2026?

The Nigeria Molded Case Circuit Breaker Market size is projected to expand from USD 52.54 million in 2025 and USD 56.18 million in 2026 to USD 86.07 million by 2031, registering a CAGR of 8.91% between 2026 to 2031.

Which rated current band leads demand in Nigeria?

The 75A to 250A segment led with 40.1% share in 2025 because it fits commercial buildings, feeder panels, and light industrial distribution needs.

Which end-user group is expanding the fastest?

Datacentre is the fastest-growing end-user group with an 11.7% CAGR through 2031, supported by new facilities in Lagos such as the MTN and OADC projects.

Why is captive power so important for breaker demand in Nigeria?

Captive generation keeps demand active outside utility cycles because firms still invest in self-supply systems that need protection at generator, transfer, and sub-distribution points.

What is the main pricing risk for suppliers and distributors?

FX volatility is the clearest risk because imported products and components remain important, which raises landed costs, weakens pricing visibility, and delays procurement decisions.

Which technology type is gaining the most momentum?

Microprocessor-based devices are growing the fastest at a 10.1% CAGR because data centres and larger industrial systems need better monitoring, coordination, and remote control functions.

Page last updated on: