Circuit Breaker Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 21.61 Billion |

| Market Size (2030) | USD 28.36 Billion |

| Growth Rate (2025 - 2030) | 5.59% CAGR |

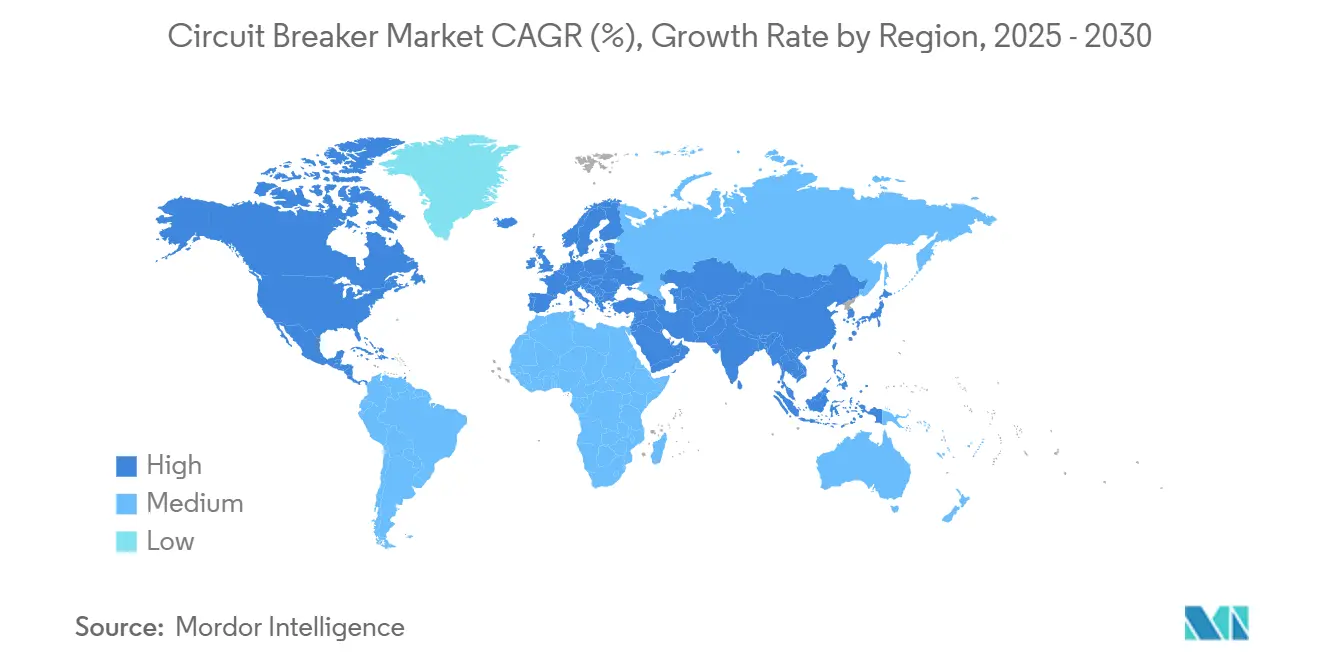

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

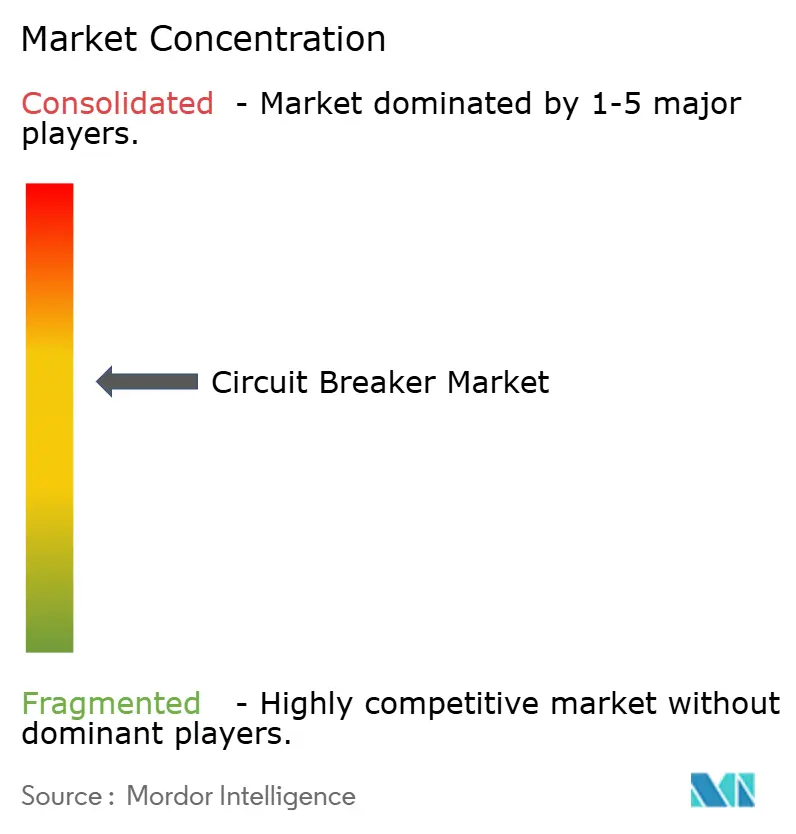

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Circuit Breaker Market Analysis by Mordor Intelligence

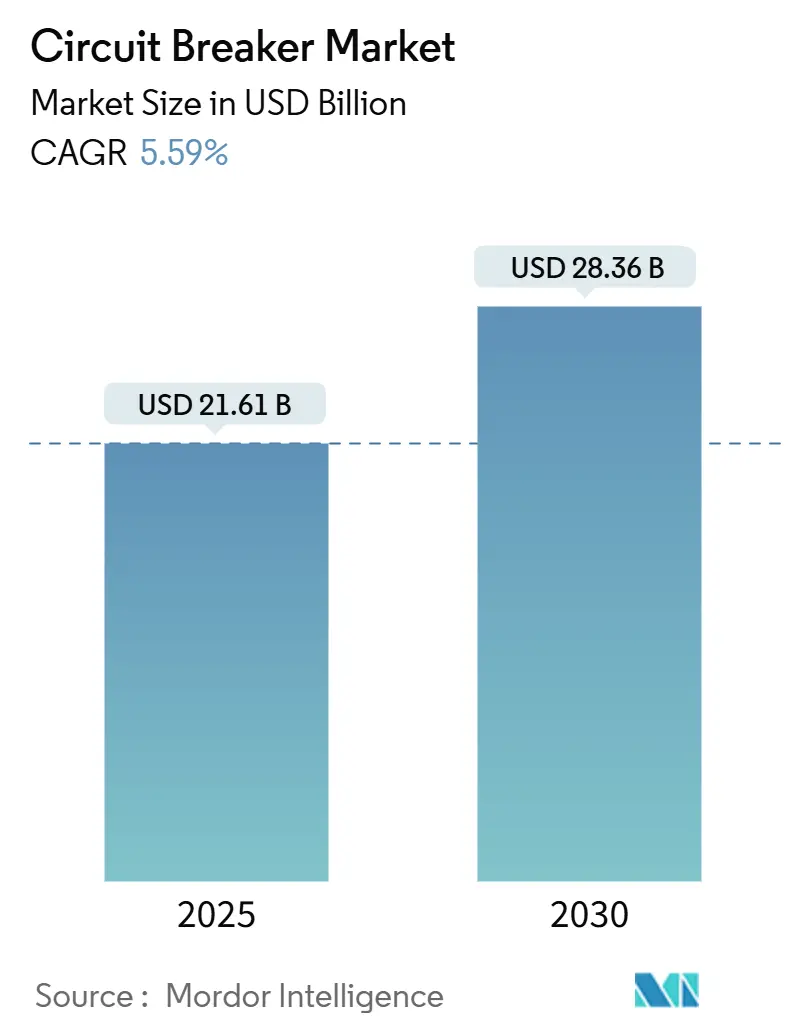

The Circuit Breaker Market size is estimated at USD 21.61 billion in 2025, and is expected to reach USD 28.36 billion by 2030, at a CAGR of 5.59% during the forecast period (2025-2030).

Grid-modernization outlays, renewable-energy interconnections, and industrial electrification are reshaping the circuit breaker market, compelling utilities and large industrial users to select solutions that pair fast interruption speed with digital monitoring. Demand is clustering in medium-voltage installations that must manage bidirectional flows from distributed solar and wind assets. Rising capital expenditure in data-center campuses and EV charging corridors is accelerating procurement of solid-state and vacuum devices, while environmental mandates are phasing out SF₆ in favor of eco-gases and solid-dielectric technologies. Manufacturers are balancing cost control against R&D spending on next-generation interruption media, even as copper and semiconductor price gyrations tighten profit margins.

Key Report Takeaways

- By type, vacuum circuit breakers commanded 39.5% of the circuit breaker market share in 2024,; while solid-state technology is projected to expand at an 8.6% CAGR to 2030.

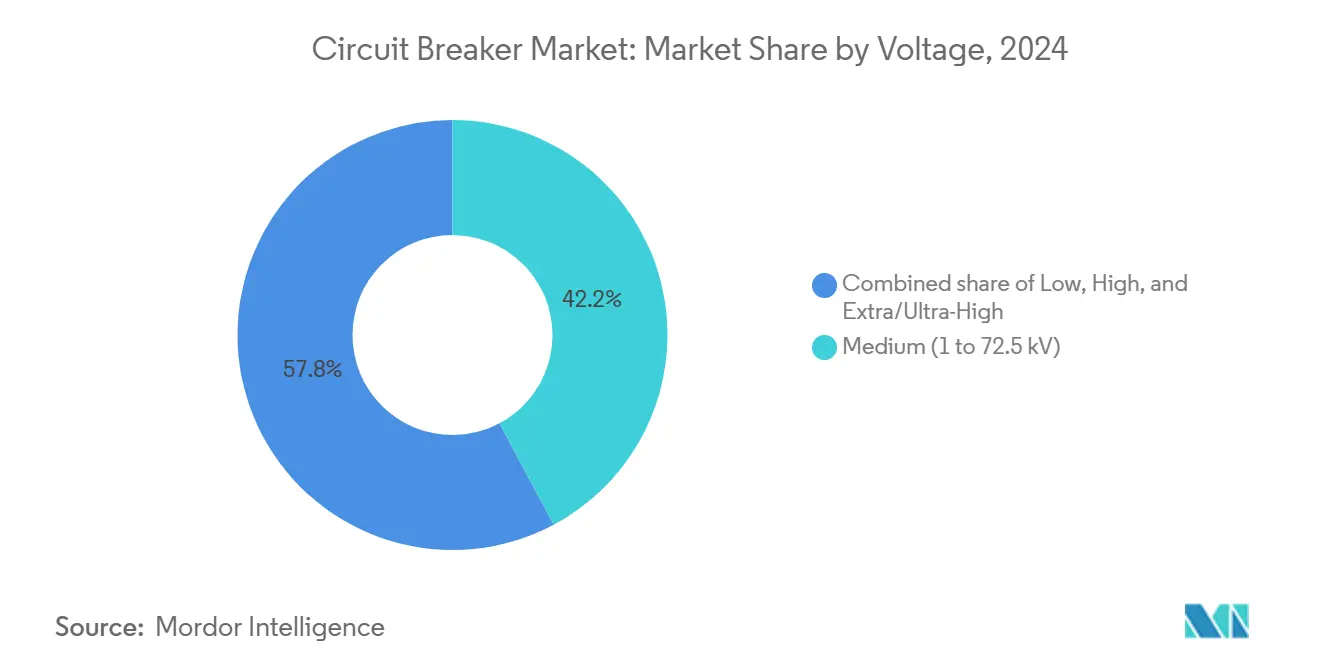

- By voltage, medium-voltage equipment held 42.2% of the circuit breaker market share in 2024, while extra/ultra-high-voltage units are advancing at a 9.5% CAGR through 2030.

- By mounting design, live-tank variants led with 41.4% share of the circuit breaker market size in 2024, whereas dead-tank products are forecast to rise at 7.9% CAGR between 2025-2030.

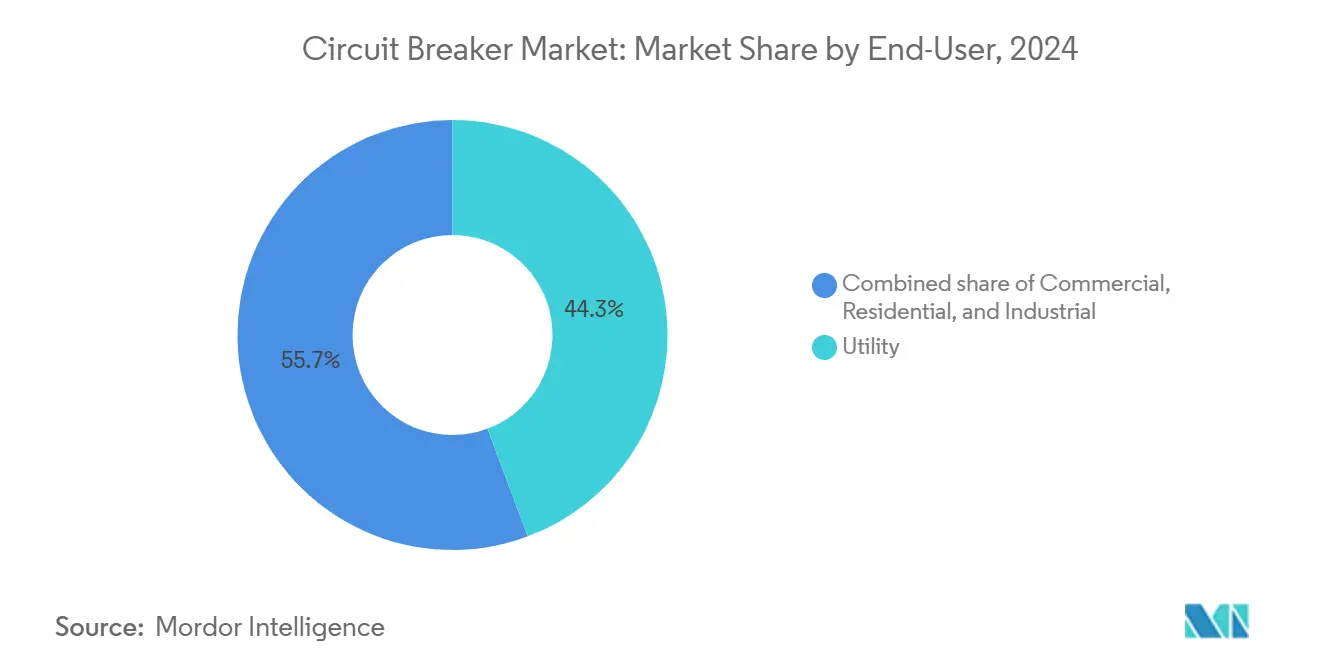

- By end-user, utilities accounted for a 44.3% share of the circuit breaker market size in 2024 and will record 5.9% annual growth through 2030.

- By geography, the Asia-Pacific commanded 45.7% revenue share in 2024; the circuit breaker market share in Asia-Pacific is also forecasted to register the fastest 6.6% CAGR to 2030.

Global Circuit Breaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-modernization investments | +1.8% | North America & Asia-Pacific | Medium term (2-4 years) |

| Distributed-renewables integration push | +1.2% | European Union & North America | Long term (≥ 4 years) |

| Industrial electrification momentum | +0.9% | Asia-Pacific core; North America spill-over | Medium term (2-4 years) |

| Data-center zero-downtime switching demand | +0.7% | North America & EU; expanding to APAC | Short term (≤ 2 years) |

| OEM shift to solid-state breakers in EV platforms | +0.5% | Global, early in EU & North America | Long term (≥ 4 years) |

| SF₆-free mandates in EU & Japan | +0.4% | EU & Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Modernization Investments Drive Infrastructure Renewal

Utility companies are overhauling substation assets that have operated for over 25 years, funneling budget into digital protection devices supporting automated fault location and remote re-closing. FirstEnergy’s USD 1.42 billion Pennsylvania plan is emblematic, focusing on vacuum breakers fitted with fiber-optic sensors that signal real-time condition anomalies.(1) U.S. federal funding of USD 2.2 billion for grid resilience catalyzes similar projects, while China’s State Grid earmarked USD 83 billion for transmission expansion, enlarging the procurement pipeline for 72.5 kV–245 kV switchgear.(2) These initiatives favor vacuum designs because of their maintenance-free operating profile, reinforcing the 39.5% segment share captured in the circuit breaker market.

Distributed Renewables Integration Accelerates Technology Evolution

Surging rooftop solar and onshore wind additions subject distribution feeders to fluctuating fault currents and voltage swings, spurring utilities to specify breakers with fast recovery characteristics. Medium-voltage interrupters rated 15 kV–38 kV enable the disconnection of inverter-based generation that can feed faults from both the grid and the renewable side. Solid-state devices switch within microseconds, preventing arc re-ignition during asymmetrical fault currents, a performance trait underpinning their 8.6% CAGR outlook in the circuit breaker market.(3) European procurement frameworks that tie tariff eligibility to fault-ride-through compliance are hastening the transition toward fully digital breakers.

Industrial Electrification Expands High-Voltage Motor Applications

Factories replacing combustion-driven equipment with electric drivetrains require circuit breakers that clear high-inrush motor faults without nuisance trips. The World Economic Forum anticipates electricity’s share of final energy to exceed 50% by 2050, implying pervasive uptake of high-voltage motor controls.(4) Battery-cell gigafactories and EV charger rollouts adopt DC breakers that manage rapid duty cycles and arc-less interruption. ABB’s medium-voltage portfolio integrates energy-storage analytics, enabling predictive shutdown before thermal limits are breached. Asia-Pacific remains the epicenter in the circuit breaker industry because Chinese policies subsidize electric-powered industrial machinery.

Data-Center Zero-Downtime Requirements Drive Premium Switching Solutions

Hyper-scale operators equate a one-hour outage to more than USD 1 million in lost service revenue. Circuit breakers, therefore, must incorporate redundant trip coils, cybersecurity-compliant communication stacks, and self-diagnostic sensors. ABB’s SACE Emax 3 is the first IEC 62443 SL2-certified air breaker, illustrating product differentiation around digital resilience.(5) Forecasts place global data-center power demand at 3-4% of total generation by 2030, ensuring robust pull for fast-acting breakers and arc-flash mitigation modules in the circuit breaker market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex versus contactors & fuses | -0.8% | Cost-sensitive emerging markets | Short term (≤ 2 years) |

| Semiconductor & copper price volatility | -0.6% | Global; intense in APAC | Medium term (2-4 years) |

| Vacuum-interrupter lead-time spikes | -0.4% | North America & EU | Short term (≤ 2 years) |

| Lengthy certification cycles for eco-design breakers | -0.3% | EU & Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure Challenges Adoption in Cost-Sensitive Applications

Contactors that start and stop motors at a fraction of breaker cost continue to displace circuit breakers in basic switching roles. Eaton’s study shows contactors rated 800 A offer higher mechanical endurance and a smaller footprint, reducing installed cost by up to 70% relative to breaker-centric panels. Emerging-market industrial clients often combine fuses for fault isolation with contactors for operation, postponing investment in full-featured breakers until tariffs incentivize power-quality compliance in the circuit breakers market.

Semiconductor Price Volatility Pressures Manufacturing Margins

Solid-state breakers rely on insulated-gate bipolar transistors (IGBT) that saw spot prices rising 40% during 2024’s supply disruptions. Hurricane Helene’s damage to quartz mines in North Carolina underscored raw-material fragility. Simultaneously, a 50% U.S. tariff on copper may inflate conductor costs for Asian exporters. Mitsubishi Electric’s USD 110 million U.S. factory investment seeks to localize supply and buffer volatility in the circuit breakers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Solid-State Innovation Challenges Vacuum Dominance

The circuit breaker market continues to be led by vacuum technology, which delivered 39.5% of 2024 revenue owing to its sealed design and suitability for 1 kV-72.5 kV grids. By contrast, though presently niche, solid-state devices are tracking an 8.6% CAGR through 2030 thanks to their microsecond clearing and negligible mechanical wear. ABB claims its new silicon-carbide platform slashes power losses 70% relative to air-magnetic units and supports fully digital coordination. The circuit breaker market size devoted to SF₆ units is contracting as EU rules enforce phase-out deadlines, accelerating migration to vacuum and g³-gas hybrids. Oil and air breakers persist in cost-oriented installations but face gradual displacement.

Market adoption patterns reveal installers favor hybrid air-vacuum modules to balance capex and environmental targets. Hitachi Energy’s 550 kV SF₆-free GIS supplied to China’s grid confirms high-voltage viability of alternative media. Patent filing trends within IEC working groups highlight active R&D in solid-dielectric interrupters able to substitute SF₆ at 245 kV and above, suggesting long-term erosion of legacy gas-filled designs within the circuit breaker market.

By Voltage: Extra-High Voltage Drives Premium Growth

Medium-voltage assemblies captured 42.2% revenue because factories, campuses, and wind parks operate within the 1 kV-38 kV envelope. Nevertheless, the extra/ultra-high-voltage category surpasses all others with a projected 9.5% CAGR as countries build 500 kV-800 kV corridors to move renewable energy from remote regions to load centers. Japan’s 1,100 kV gas breaker development set the performance benchmark for transient recovery voltage handling.

Within transmission projects, utilities demand circuit breaker market size allocations that factor in higher per-unit pricing: a single 550 kV dead-tank breaker can cost 30 times a 15 kV vacuum unit, inflating vendor revenue despite lower shipment volumes. GE Vernova’s latest platform supports 5,000 A continuous current at 550 kV, reflecting ruggedization needs for bulk power corridors.

By Mounting: Dead-Tank Technology Gains Momentum

With a 41.4% 2024 share, live-tank breakers remain prevalent because of lower mass and simplified erection requirements. Yet the safety advantages of dead-tank housings, which sit at ground potential, persuade utilities to shift procurement. In the circuit breakers market, dead-tank shipments are rising 7.9% annually, tied to renewable integration sites where line-side transients can induce radio-frequency interference harmful to nearby telemetry.

Live-tank designs still dominate substations with constrained budgets, but hybrid projects often combine dead-tank breakers on critical feeders and live-tank units elsewhere. GE Vernova’s contract for 69 dead-tank breakers in Queensland underlines this technology’s traction in modern grids seeking reliability and eco-gas compatibility

By End-User: Utilities Lead Infrastructure Modernization

Utility entities generated 44.3% of 2024 spending, directing funds to replace aging air-magnetic units with vacuum devices interfaced to SCADA in the circuit breaker market. Their annual budget is inching up 5.9% as decarbonization mandates raise transmission-expansion targets. Industrial operators trail but post strong volume because EV-battery plants, petrochemical upgrades, and semiconductor fabs all need arc-resistant switchgear.

Residential and commercial segments gravitate to smart breakers incorporating Wi-Fi metering and load-shedding logic. ABB’s ReliaHome launch signals OEM focus on modular retail panels that feed rooftop solar into the grid. Government incentives for energy-efficient buildings in Europe will likely expand this sub-segment’s contribution to the circuit breaker market.

Geography Analysis

Asia-Pacific held 45.7% of global revenue in 2024 and is pacing at 6.6% CAGR through 2030, propelled by Chinese and Indian grid extensions that award bulk contracts for 72.5 kV and 252 kV breakers. GE Vernova’s USD 16 million investment in Indian manufacturing denotes regional supply localization in the circuit breakers market. Japanese innovations at 1,100 kV illustrate APAC technological leadership, reinforcing equipment exports to Southeast Asian projects.

North America’s market expands on a foundation of stimulus-supported resilience programs. The circuit breaker market gains from USD 2.2 billion in U.S. federal grants that leverage nearly USD 10 billion in utility matching funds. Data-center projects add premium demand: 2024 construction spending climbed 43.1%, leading to design-build contracts that specify breaker cybersecurity and real-time harmonic analytics.

Europe remains a regulatory bellwether, enforcing SF₆ bans by 2026 for ≤24 kV equipment and by 2031 for higher voltages. Manufacturers such as Siemens Energy and Hitachi Energy are racing to commercialize g³ and vacuum solutions to safeguard European revenue streams. South America, the Middle East & Africa represent emergent frontiers where hydro project build-outs and industrial diversification sustain double-digit volume growth despite smaller absolute bases.

Competitive Landscape

The circuit breaker industry features moderate concentration: the top five vendors collectively control 55-65% of global sales. ABB’s acquisition of Gamesa Electric’s power-electronics line expands its reach into renewable inverters, complementing its core breaker portfolios. Hitachi Energy’s USD 70 million Pennsylvania expansion underpins its strategy to own SF₆-free intellectual property and domesticate production for U.S. grid projects.

Start-ups such as Atom Power are introducing fully digital semiconducting breakers that switch 3,000-fold faster than mechanical units, unlocking centralized software control for multi-circuit panels. The circuit breaker market analysis indicates that incumbents respond by partnering with silicon-carbide device makers and embedding artificial-intelligence firmware for predictive maintenance. Supply chain integration is likewise strategic; Mitsubishi Electric’s new facilities aim to secure vacuum-interrupter capacity and buffer copper-price swings. Intellectual-property battles over eco-gas mixtures and arc-quenching ceramic composites intensify as patents approach expiry.

Circuit Breaker Industry Leaders

ABB Ltd.

Schneider Electric SE

Siemens AG

Mitsubishi Electric

Eaton Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ABB posted record Q2 orders of USD 9.8 billion and rolled out the SACE Emax 3, the first SL2-certified cyber-secure air breaker for critical infrastructure.

- May 2025: Hitachi Energy shipped the world’s first SF₆-free 550 kV gas-insulated switchgear to China’s State Grid.

- April 2025: Hitachi Energy invested over USD 70 million in Pennsylvania for EconiQ SF₆-free breaker production.

- March 2025: Hitachi Energy pledged an additional USD 250 million to expand transformer component output worldwide.

Global Circuit Breaker Market Report Scope

| Air |

| Vacuum |

| SF₆ |

| Oil |

| Hybrid (Air-Vacuum, Vacuum-SF₆) |

| Solid-State |

| Low (Below 1 kV) |

| Medium (1 to 72.5 kV) |

| High (72.5 to 245 kV) |

| Extra/Ultra-High (Above 245 kV) |

| Fixed |

| Withdrawable |

| Live Tank |

| Dead Tank |

| Commercial |

| Residential |

| Industrial |

| Utility |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Air | |

| Vacuum | ||

| SF₆ | ||

| Oil | ||

| Hybrid (Air-Vacuum, Vacuum-SF₆) | ||

| Solid-State | ||

| By Voltage | Low (Below 1 kV) | |

| Medium (1 to 72.5 kV) | ||

| High (72.5 to 245 kV) | ||

| Extra/Ultra-High (Above 245 kV) | ||

| By Mounting | Fixed | |

| Withdrawable | ||

| Live Tank | ||

| Dead Tank | ||

| By End-User | Commercial | |

| Residential | ||

| Industrial | ||

| Utility | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the circuit breaker market in 2030?

The market is expected to reach USD 28.36 billion by 2030, reflecting a 5.59% CAGR over 2025-2030.

Which technology segment is growing fastest within global circuit protection?

Solid-state circuit breakers are expanding at an 8.6% CAGR due to microsecond switching speed and digital control features.

Why are utilities replacing SF? circuit breakers?

European and Japanese regulations mandate SF?-free equipment, prompting a shift to vacuum and eco-gas alternatives that lower greenhouse-gas impact.

How does data-center growth influence circuit breaker market demand?

Data-center operators require zero-downtime power architecture, driving procurement of cyber-secure breakers with predictive-maintenance analytics.

Which region holds the largest circuit breaker market share?

Asia-Pacific leads with 45.7% revenue share, supported by extensive grid-expansion projects and local manufacturing capacity.

What factors are restraining rapid adoption in emerging markets?

High upfront cost compared to contactors and fuses, plus raw-material volatility in copper and semiconductors, slows penetration of advanced breakers.

Page last updated on: