Kenya Molded Case Circuit Breaker Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

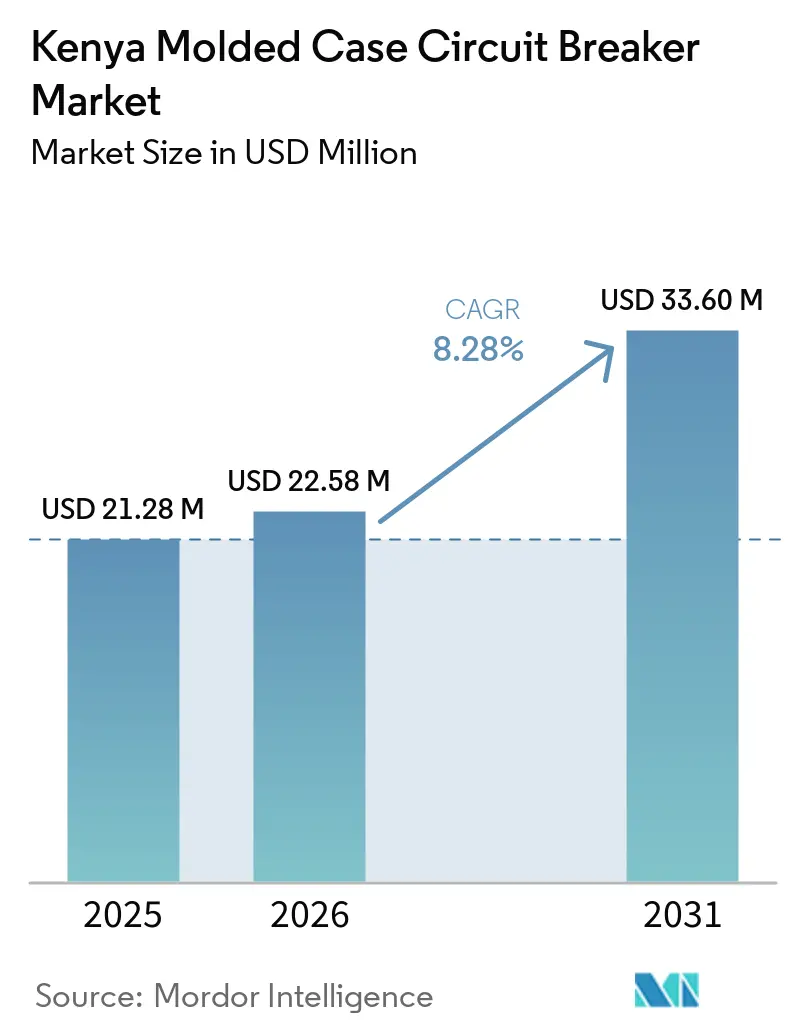

| Base Year Market Size (2025) | USD 21.28 Million |

| Market Size (2026) | USD 22.58 Million |

| Market Size (2031) | USD 33.60 Million |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

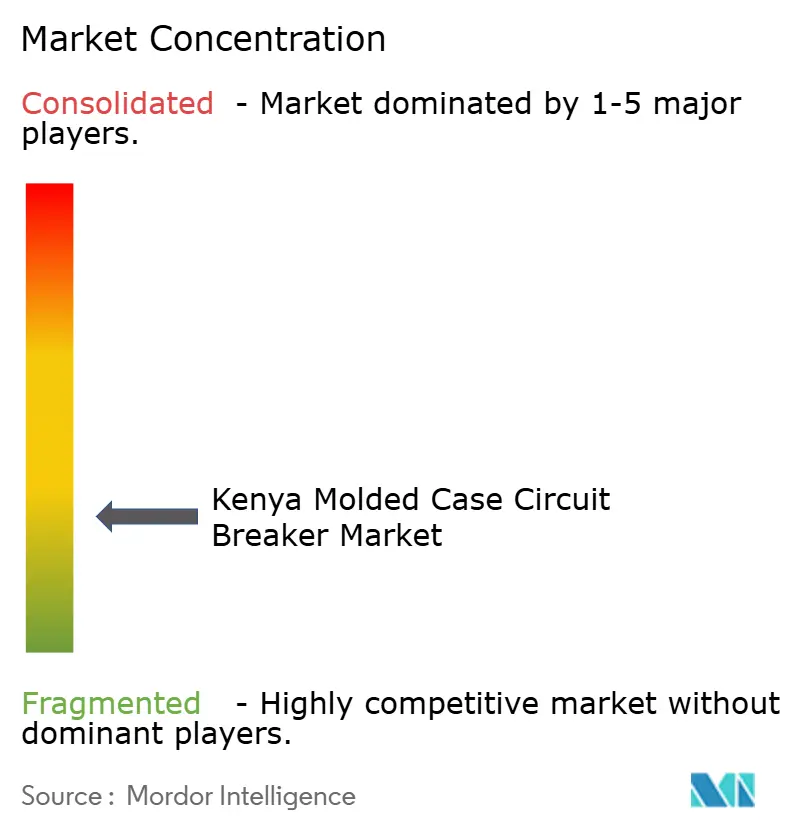

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya Molded Case Circuit Breaker Market Analysis by Mordor Intelligence

The Kenya Molded Case Circuit Breaker Market size is projected to expand from USD 21.28 million in 2025 and USD 22.58 million in 2026 to USD 33.60 million by 2031, registering a CAGR of 8.28% between 2026 to 2031. The demand base is supported by a government target to connect all 15.6 million households within 3 years, which keeps downstream switchgear demand tied to structural electrification rather than only short-cycle construction spending.[1]Source: Deputy President Kithure Kindiki, “Commissioning Address at Maragima Village Electrification Project, Kieni Constituency, Nyeri County,” Radio Generation, radiogeneration.co.ke The molded case circuit breaker Kenya market is also being lifted by the Public-Private Partnership (PPP) - funded transmission program, Kenya Electricity Transmission Company (KETRACO)’s December 2025 agreement with Africa50 and Power Grid Corporation of India, and a sharp rise in the housing budget for 2025/26, which together sustain both substation and building-level procurement.[2]Source: Kenya National Bureau of Statistics, “Economic Survey 2026,” Kenya Broadcasting Corporation, kbc.co.ke Renewable integration, data-center build-outs, and facility-level energy management rules are pushing buyers toward higher-specification protection devices and faster adoption of microprocessor-based trip units. Competition remains strongest between premium global brands that dominate specification-led projects and Asian suppliers that are gaining share in price-sensitive channels through shorter lead times and broader distributor reach. Import conformity checks and counterfeit substitution still weigh on the addressable premium base, although stronger surveillance by Kenya Bureau of Standards (KEBS) should improve the position of certified suppliers over the forecast period.[3]Source: Anti-Counterfeit Authority of Kenya, “Awareness and Extent of Counterfeiting in Kenya Firm-Level Survey Report 2025,” Anti-Counterfeit Authority of Kenya, aca.go.ke

Key Report Takeaways

- By rated current, 75 A-250 A held 38.2% of the molded case circuit breaker Kenya market share in 2025, while the molded case circuit breaker Kenya market size for Above 800 A is projected to expand at an 8.7% CAGR through 2031.

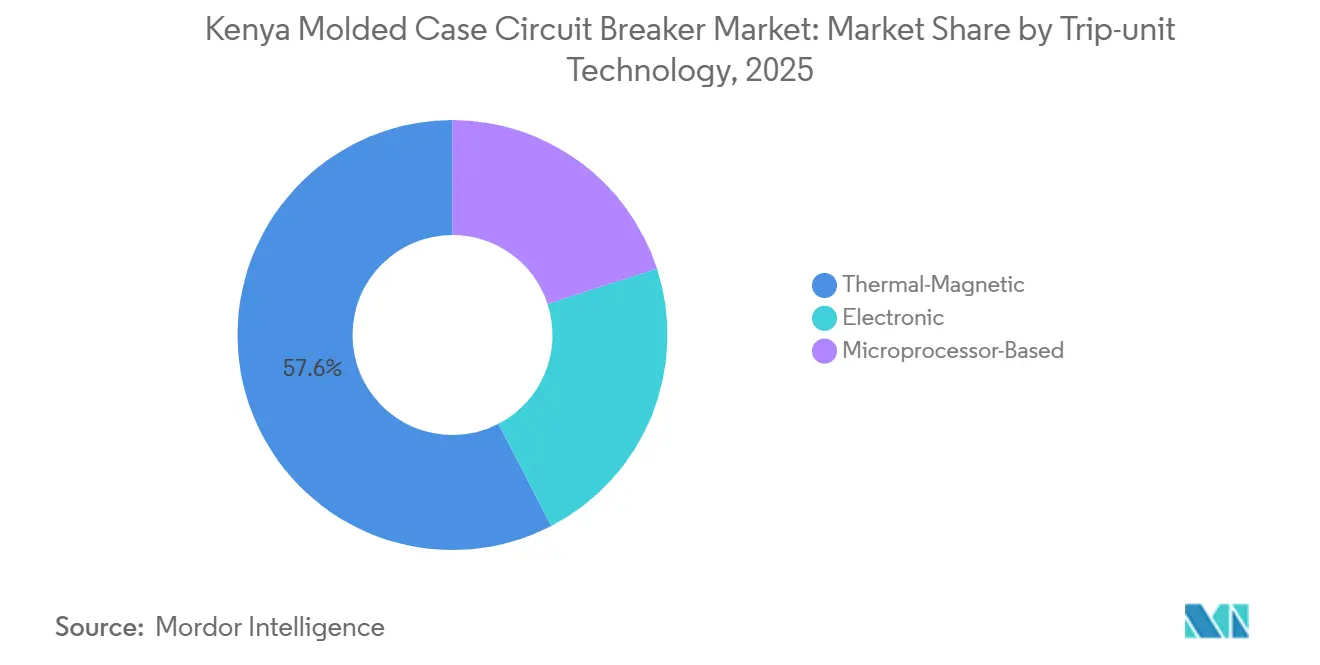

- By trip-unit technology, Thermal-Magnetic accounted for 57.6% of the molded case circuit breaker Kenya market size in 2025, while Microprocessor-Based trip units are forecast to grow at a 9.1% CAGR through 2031.

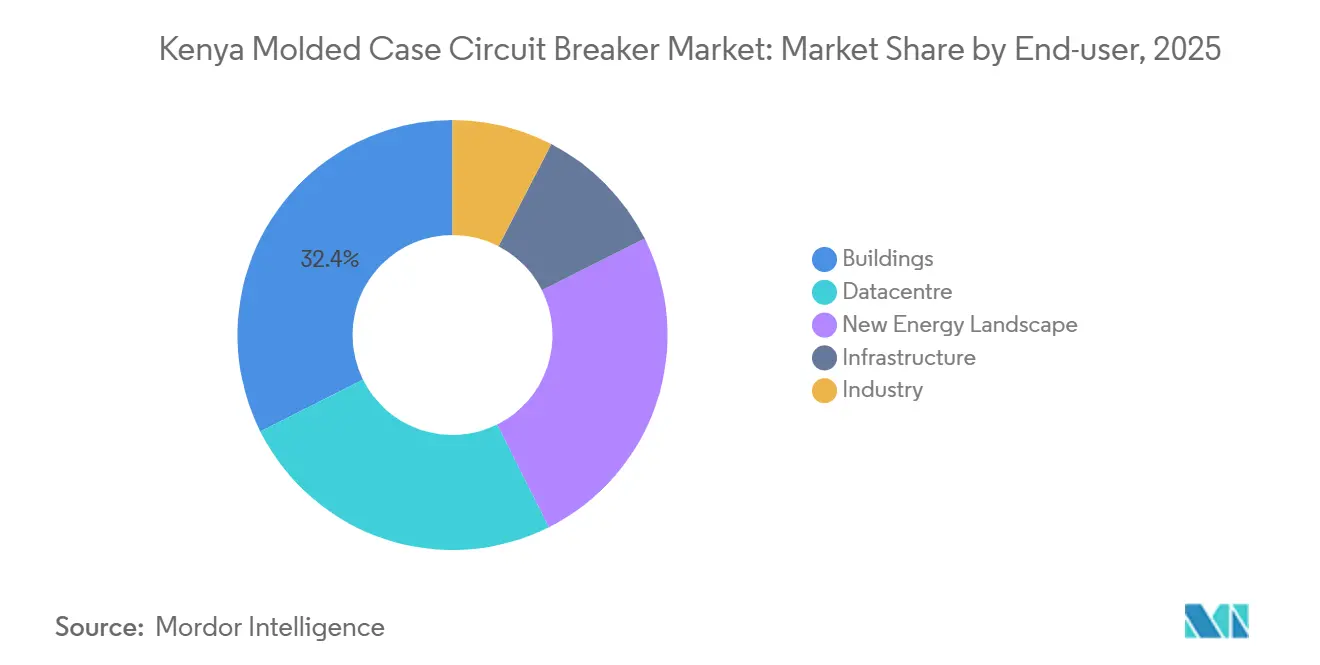

- By end user, Buildings captured 32.4% of the molded case circuit breaker Kenya market share in 2025, while Data Center is expected to record the fastest growth at a 10.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kenya Molded Case Circuit Breaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid Densification And PPP-Funded Transmission and Distribution (T&D) Build-Out | +2.1% | National, with early gains in Nairobi, Western Kenya, and Coast corridor | Short term (≤ 2 years) |

| Affordable-Housing and Commercial-Construction Rebound | +1.8% | National, concentrated in Nairobi, Mombasa, and Nakuru urban clusters | Short term (≤ 2 years) |

| Renewable Integration Across Geothermal, Solar, Wind, And Battery Energy Storage Systems (BESS) | +1.5% | Rift Valley geothermal belt, Kajiado wind zone, Coast solar corridor | Medium term (2-4 years) |

| Hyperscale Data Center And Cloud-Campus Build-Outs | +0.8% | Nairobi metropolitan area, spillover to Konza Technopolis Special Economic Zone (SEZ) | Medium term (2-4 years) |

| Energy and Petroleum Regulatory Authority (EPRA) Energy-Management Compliance In Designated Facilities | +0.6% | National, with high concentration in Nairobi, Mombasa, and Kisumu industrial zones | Medium term (2-4 years) |

| SEZ, Industrial-Park, And E-Mobility Load-Cluster Expansion | +0.9% | Dongo Kundu in Mombasa, Olkaria in Naivasha, Vipingo in Kilifi, and Eldoret | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Densification and PPP-Funded T&D Build-Out

Kenya’s shift toward PPP-financed transmission remains the strongest near-term driver for the molded case circuit breaker Kenya market. Kenya Electricity Transmission Company (KETRACO)’s Transmission Master Plan 2025-2044 mapped 9,771 MW of new generation additions and USD 5 billion in transmission investment needs, with PPPs moving to the center after a USD 4 billion public funding gap became clear.[4]Source: KETRACO, “Transmission Master Plan 2025-2044,” Global Transmission Report, globaltransmission.info The first USD 311 million PPP package covers the 400 kV Lessos-Loosuk and 220 kV Kibos-Kakamega-Musaga lines, and construction was scheduled to begin in August 2026. Each new substation creates a second wave of low-voltage protection demand, especially for 250A-800A and above-800A feeder and bus-coupler applications. The Mariakani 400/220 kV substation commissioned in May 2026 shows how regional interconnection projects are multiplying procurement nodes beyond Nairobi and widening the geographic footprint of the molded case circuit breaker Kenya market.

Affordable-Housing and Commercial-Construction Rebound

The housing program has become one of the most dependable volume pipelines for the molded case circuit breaker Kenya market. Kenya National Bureau of Statistics data showed 96.3% expenditure utilization against the KSh 79 billion 2024/25 housing budget, followed by an increase to KSh 116.7 billion for 2025/26, which signaled continuity in project flow and procurement activity. Standardized housing clusters draw heavily on 75 A-250 A breakers for riser protection, tenant boards, and common-area metering, which reinforces the scale advantage of this range. The commercial spillover is equally important because major housing zones also trigger retail, office, and service construction that uses higher-specification devices than the residential units themselves. Schneider Electric’s May 2026 launch of the EasyPact CVS C4 range in East Africa reflects that shift, especially in the 800A-1600A range used in mid-rise commercial applications.

Renewable Integration Across Geothermal, Solar, Wind, and BESS

Kenya’s power mix is creating protection requirements that are more complex than those found in conventional thermal-led systems, and this is supporting the molded case circuit breaker Kenya market. Geothermal accounted for 43% of electricity generation in 2024, hydropower for 28%, and wind for 14%, which shows how strongly renewable generation already shapes the operating environment. Variable-output solar and wind assets need higher interrupt ratings and more precise fault-clearance performance at inverter outputs and interconnection boards. The Siruai wind and storage project in Kajiado County adds another specification layer because battery integration raises the need for DC-rated protection devices and tighter control of interconnection performance. KenGen’s renewable and BESS expansion program, which is expected to be operational by 2027, also favors electronic and microprocessor-based devices because real-time load sensing becomes more valuable as storage and variable generation grow in the system.

Hyperscale Data Center and Cloud-Campus Buildouts

Data center demand carries the highest value intensity in the molded case circuit breaker Kenya market. The launch of Oracle Cloud Infrastructure’s Nairobi region at iXAfrica’s 22 MW campus in January 2026 confirmed that carrier-neutral and modular facilities are the clearest near-term growth path for Kenya’s data-center build-out. These sites need high-specification devices at the critical distribution layer, and they also require large volumes of branch-circuit protection under N+1 or 2N redundancy designs. The delay to the Microsoft-G42 Olkaria plan did not remove demand, but it shifted expectations toward smaller and more grid-compatible deployments in the 4 MW to 20 MW range. That change still favors microprocessor-based MCCBs because logging, communication, and integration with building management systems are now standard expectations in facilities above 2 MW.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import Conformity Checks And Sourcing-Cycle Friction | -1.2% | National, most acute at Mombasa port entry point | Short term (≤ 2 years) |

| Price-Led Procurement And Counterfeit Breaker Substitution | -1.5% | National, concentrated in informal construction and peri-urban commercial segments | Short term (≤ 2 years) |

| Transmission-Project Financing Gaps And Order-Timing Delays | -0.8% | National, concentrated in counties dependent on exchequer-funded grid projects | Medium term (2-4 years) |

| Limited Field Capability for Smart MCCB Configuration | -0.6% | National, most acute in secondary cities and industrial zones outside Nairobi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import Conformity Checks and Sourcing-Cycle Friction

Kenya’s pre-shipment conformity regime creates a steady delay risk for the molded case circuit breaker Kenya market. Exporters must obtain a Certificate of Conformity (CoC) before shipment, and any mismatch between the certified item and the delivered product can extend clearance times by 4 weeks to 8 weeks. This issue is most visible at Mombasa port, where KEBS found a July 2025 consignment materially non-compliant despite being accompanied by a CoC. Smaller developers and contractors are hit hard because they cannot absorb long lead times or carry large safety stocks. The result is a structural advantage for distributors with local inventory, which concentrates project-winning capacity among a limited number of import agents and raises working-capital requirements for contractors on fixed commissioning schedules.

Price-Led Procurement and Counterfeit Breaker Substitution

Counterfeit substitution remains a structural restraint on the molded case circuit breaker Kenya market, especially in informal and semi-formal construction channels. The Anti-Counterfeit Authority’s 2025 firm-level survey confirmed that circuit breakers were among the most widely counterfeited products in Kenya’s energy and electrical sector. Price-driven purchasing behavior allows uncertified products to compete directly with branded devices in smaller commercial and peri-urban projects. The immediate cost problem is only part of the challenge because breaker failure under fault conditions can destroy electrical rooms and trigger wider liability concerns for every supplier involved on the site. This keeps sales cycles longer for certified vendors, even where specifiers prefer quality, because buyers often revisit prices before making final approval.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rated Current: High-Power Feeders Gaining on a Maturing Mid-Range Base

The 75 A-250 A segment held 38.2% of the market in 2025, which made it the largest current tier in the molded case circuit breaker Kenya industry. That position came from residential distribution, light-commercial fit-outs, and the government’s housing program, all of which favor standardized sub-250A panel configurations across a large number of simultaneous projects. The Up to 75 Range remained tied to final-circuit protection in residential and light commercial settings, were cost control and installation familiarity matter most. The molded case circuit breaker Kenya market kept a strong volume bias in this band, which supported distributor-led sales and limited direct Original Equipment Manufacturer (OEM) engagement in the most price-sensitive projects.

Above 800A is projected to grow at an 8.7% CAGR through 2026-2031, giving it the fastest expansion among current tiers in the molded case circuit breaker Kenya market. Demand is driven by substation buildouts under KETRACO’s PPP program, data-center incoming breakers, and large SEZ power infrastructure. Utility-scale battery projects add another layer because bus-tie and feeder applications in these systems often need devices rated above 1,600 A, where supplier qualification is far narrower under International Electrotechnical Commission (IEC) 60947-2:2024 testing standards. The Kimuka 400kV substation Phase II project also points to a continued pipeline for substation Low Voltage (LV) auxiliaries, which should keep high-current specification activity active through the forecast period.

By Trip-Unit Technology: Thermal-Magnetic Volume, Smart MCCB Value

Thermal-Magnetic trip units commanded 57.6% of the market in 2025, reflecting their cost advantage and broad acceptance across the molded case circuit breaker Kenya industry. Their appeal was not based on price alone because passive protection without auxiliary power supply suits housing panels, rural mini-grid settings, and many light-commercial applications. Electronic trip units filled the middle ground where industrial motor-feeder circuits and medium-sized commercial buildings needed adjustable protection curves and fewer nuisance trips. This left Thermal-Magnetic devices dominant in volume terms even as purchasing criteria became more demanding in higher-value projects.

Microprocessor-Based trip units are forecast to expand at a 9.1% CAGR through 2031 in the molded case circuit breaker Kenya market. The strongest pull comes from data-center operators that need fault logging, communication capability, and integration with building management systems, and from EPRA-designated facilities that need better monitoring for energy compliance. The technology is also being helped by tighter benchmarks under IEC 60947-2:2024, which make certification and performance verification more important in public and development-finance-backed procurement. As the installed base becomes more digital, suppliers that can support configuration and commissioning should see a stronger position than those competing only on device price.

By End User: Buildings Lead Volume, Data Centers Lead Value Intensity

Buildings held a 32.4% share in 2025, which kept them as the largest end-user group in the molded case circuit breaker Kenya market size. This came from a broad construction cycle that included affordable housing, commercial office and retail fit-outs, and hospitality activity across Nairobi and secondary cities. Industry remained the next major demand pool, supported by tea factories, agro-processing, and light manufacturing where protective upgrades follow both grid improvements and self-generation investments. Kenya Tea Development Agency (KTDA) Power’s 32% rise in hydropower output during 2025 showed how power-related investment in tea processing can translate into wider electrical equipment upgrades at factory distribution boards.

Data Center is projected to expand at a 10.4% CAGR through 2031, making it the fastest-growing end-user category in the molded case circuit breaker Kenya market. Oracle Cloud’s activation at iXAfrica’s 22 MW Nairobi campus established a repeatable model based on modular deployment, high rack densities, and uptime-driven protection design. New Energy Landscape also continues to grow as solar, wind, BESS, and geothermal applications require technically distinct protection architectures that differ from conventional power distribution. For suppliers, Data Centers matter more than their volume share suggests because each megawatt of IT load carries a much higher MCCB value density than a large batch of residential units.

Geography Analysis

Nairobi and Central Kenya remain the largest demand center in the molded case circuit breaker Kenya market. The capital posts the highest absolute consumption because it combines commercial construction, flagship housing projects, major hospital and education infrastructure, and the strongest concentration of datacenter fit-outs. Nairobi also benefits from its position as the main location for consulting engineers, distributors, and project procurement teams, which gives it an advantage in specification-led sales. Internationally financed projects in this corridor tend to favor certified European and Indian brands in the 250 A-800 A range because compliance and after-sales capability carry more weight in the approval process.

The Coast region is emerging as the fastest-rising geography in the molded case circuit breaker Kenya market. KETRACO’s KSh 15.8 billion transmission project in Kilifi and the expansion of the Malindi substation should improve supply reliability and support downstream industrial connections across the coast corridor. The Mariakani 400/220 kV substation commissioned in May 2026 strengthens the high-voltage backbone feeding Mombasa and the Dongo Kundu Special Economic Zone. Dongo Kundu and Vipingo SEZ create parallel demand for above-800 A MCCBs because tenant infrastructure, substations, and renewable support systems are being installed in phases rather than as a single build. Mombasa port also remains the main import entry point, which gives coast-based distributors an inventory advantage but also exposes them first to tighter conformity enforcement.

Western Kenya and the Rift Valley form the next structural growth corridor for the molded case circuit breaker Kenya market. The 132 kV Sondu-Homa Bay line energized in February 2026 improved supply stability in South Nyanza and opened stronger conditions for tea factories and agro-processing loads that had relied more heavily on diesel-based backup. The PPP-backed Kibos-Kakamega-Musaga line should extend high-voltage access into Western Kenya and create a new substation-driven procurement wave when construction begins. In the Rift Valley, Olkaria’s position as both a geothermal hub and a gazetted SEZ is drawing industrial tenants whose protection needs begin at the 250 A-800 A tier and move upward with heavier industrial loads.

Competitive Landscape

The molded case circuit breaker Kenya market is moderately concentrated in the premium specification tier and far more fragmented in the sub-premium tier. Schneider Electric, ABB, Siemens, and Eaton hold the strongest position on institutional, PPP-funded, and consultant-specified projects because compliance, service support, and brand approval are part of the buying decision. Chinese suppliers such as CHINT, NADER Electric, and Beijing People Electric compete more aggressively in commercial and affordable-housing channels where price and lead time carry more weight. This split keeps the overall market from becoming highly concentrated, even though premium projects remain difficult for smaller brands to penetrate.

Schneider Electric has taken one of the clearest strategic steps in the molded case circuit breaker Kenya market through the May 2026 launch of the EasyPact CVS C4 range in East Africa. That product closes a gap in the 800A-1600A range, where mid-rise commercial and light-industrial projects were previously more exposed to lower-cost alternatives. Schneider also opened a Nairobi innovation and training hub in May 2026, which moves its approach beyond pure distribution and into technical capability-building for installers and engineers. ABB is following a related path through digital design support, and its April 2026 Application Configurator release supports engineers working on grid-feeding protection systems for distributed energy resources. These moves matter because buying decisions are increasingly being shaped before the tender reaches distributors.

The competitive bar is also rising because IEC 60947-2:2024 tightened testing expectations for electronic and microprocessor-based devices, which strengthens the position of suppliers that can prove full certification and field performance. That shift is especially relevant in data centers, renewable interconnection, and substation-linked applications where failure costs are high and low-end substitution is less acceptable. At the same time, a service gap remains because the wider installer base is still less prepared for smart MCCB configuration than for conventional thermal-magnetic devices. Suppliers that combine product availability, training, and commissioning support should therefore defend share better than those relying only on catalog breadth.

Kenya Molded Case Circuit Breaker Industry Leaders

Schneider Electric SE

ABB Ltd.

Siemens AG

Eaton Corp plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Schneider Electric launched the EasyPact CVS C4 moulded-case circuit breaker range in East Africa, extending its portfolio to cover 800A-1600A applications and addressing a longstanding gap in mid-range commercial and industrial protection. The launch is targeted at residential developments, commercial buildings, and small to medium-sized industries across the region.

- January 2026: iXAfrica Data Center collaborated with Oracle to deliver Kenya's first Oracle Cloud Infrastructure public cloud region, hosted at iXAfrica's 22 MW hyperscale-ready campus in Nairobi. The activation directly amplifies demand for high-specification MCCBs in the Data Center end-user segment.

- December 2025: KETRACO signed a KSh 40.4 billion, USD 311 million, PPP agreement with Africa50 and Power Grid Corporation of India for the 400 kV Lessos-Loosuk and 220 kV Kibos-Kakamega-Musaga transmission lines, with construction scheduled to commence in August 2026. The project will include new substations and extends high-voltage grid access into Western Kenya for the first time.

- August 2025: EPRA gazetted the Energy Management Regulations 2025, requiring all facilities consuming more than 180,000 kWh annually to conduct licensed energy audits every 4 years and implement 50% of recommended savings, creating a compliance-driven upgrade cycle for energy-monitoring MCCBs in industrial and commercial segments.

Kenya Molded Case Circuit Breaker Market Report Scope

A Molded Case Circuit Breaker (MCCB) is an electrical protection device used to prevent damage to circuits caused by overloads, short circuits, and ground faults. Enclosed in a robust, insulated housing, MCCBs are commonly utilized in commercial and industrial applications with higher amperage requirements, supporting currents of up to 2,500 Amps.

The Kenya Molded Case Circuit Breaker Market is segmented into rated current, trip-unit technology, end-user, and geography. By rated current, the market is segmented into up to 75 A, 75 A-250 A, 250 A-800 A, and above 800 A. By trip-unit technology, the market is segmented into thermal-magnetic, electronic, and microprocessor-based trip units. By end-user, the market is segmented into buildings, industry, infrastructure, datacentres, and the new energy landscape. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Upto 75A |

| 75A - 250A |

| 250A - 800A |

| Above 800A |

| Thermal-Magnetic |

| Electronic |

| Microprocessor-Based |

| Buildings |

| Industry |

| Infrastructure |

| Datacentre |

| New Energy Landscape |

| By Rated Current | Upto 75A |

| 75A - 250A | |

| 250A - 800A | |

| Above 800A | |

| By Trip-Unit Technology | Thermal-Magnetic |

| Electronic | |

| Microprocessor-Based | |

| By End User | Buildings |

| Industry | |

| Infrastructure | |

| Datacentre | |

| New Energy Landscape |

Key Questions Answered in the Report

What is the 2026 value of Kenya's molded case circuit breaker space?

The Kenya Molded Case Circuit Breaker Market size is projected to expand from USD 21.28 million in 2025 and USD 22.58 million in 2026 to USD 33.60 million by 2031, registering a CAGR of 8.28% between 2026 to 2031.

Which rated current category leads demand in Kenya?

The 75 A-250 A segment led in 2025 with a 38.2% share because it is widely used in housing, light commercial fit-outs, and standard building distribution boards.

Which technology is growing fastest in Kenya's MCCB demand base?

Microprocessor-Based trip units are growing fastest, at a 9.1% CAGR through 2031, supported by data-center deployment and energy-management compliance needs.

Which end-user group creates the largest revenue pool today?

Buildings held the largest share at 32.4% in 2025, driven by affordable housing, commercial construction, and hospitality activity.

Why are Data Centers important for suppliers even if their volume base is smaller?

Data Centers are forecast to grow at a 10.4% CAGR through 2031, and each megawatt of IT load generates far higher MCCB value than a large batch of residential units.

What are the main risks affecting supplier growth in Kenya?

The main restraints are import conformity delays, counterfeit substitution, and the need for stronger field capability in smart MCCB configuration and commissioning.

Page last updated on: