Egypt Residual Current Circuit Breaker (RCCB) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

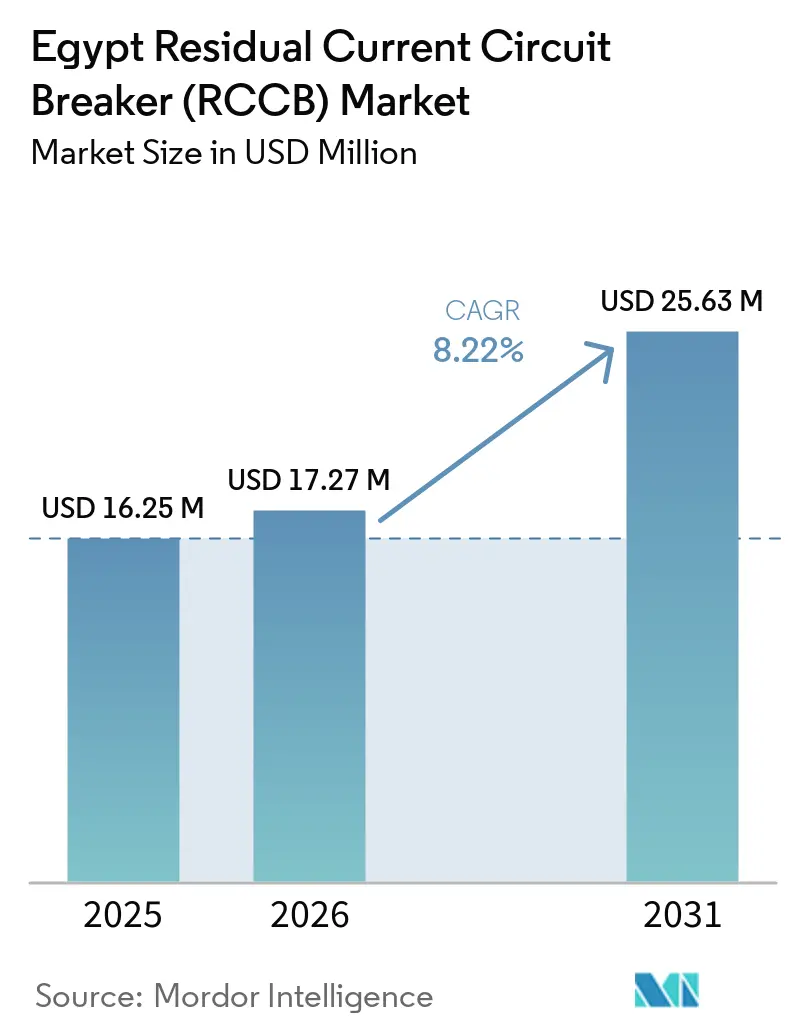

| Base Year Market Size (2025) | USD 16.25 Million |

| Market Size (2026) | USD 17.27 Million |

| Market Size (2031) | USD 25.63 Million |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Residual Current Circuit Breaker (RCCB) Market Analysis by Mordor Intelligence

The Egypt Residual Current Circuit Breaker Market size was valued at USD 16.25 million in 2025 and is estimated to grow from USD 17.27 million in 2026 to reach USD 25.63 million by 2031, at a CAGR of 8.22% during the forecast period (2026-2031). The Egypt residual current circuit breaker market is being supported first by formal housing expansion, because Egypt’s FY2025/2026 development plan targets 310,000 new residential units and sets aside EGP 100 billion, which is approximately USD 2 billion, for electricity and renewable energy infrastructure linked to those communities.[1] Egyptian Ministry of Housing and Urban Communities, “FY2025/2026 Development Plan,” Ministry of Housing and Urban Communities, housing.gov.eg The Egypt residual current circuit breaker market is also being lifted by transmission and substation upgrades, with EGP 26.289 billion, which is approximately USD 565 million, invested in FY2024/2025 to rehabilitate high-voltage substations and transmission lines, widening the base of formal connection points that require compliant protection devices. A dual-tier supply structure shapes competition, with multinational brands competing on certification, lead time, and specification support, while local distributors and lower-cost Asian imports compete more aggressively on price. Demand in the Egypt residual current circuit breaker market remains strongest where installation is tied to code compliance, while premium device adoption is being slowed by solar interconnection pauses, import dependence, and customs-related delays. Over the medium term, the Egypt residual current circuit breaker market has room to move toward higher-spec products as solar, EV charging, utilities, and smart-city projects place more emphasis on formal certification and DC-sensitive protection requirements.

Key Report Takeaways

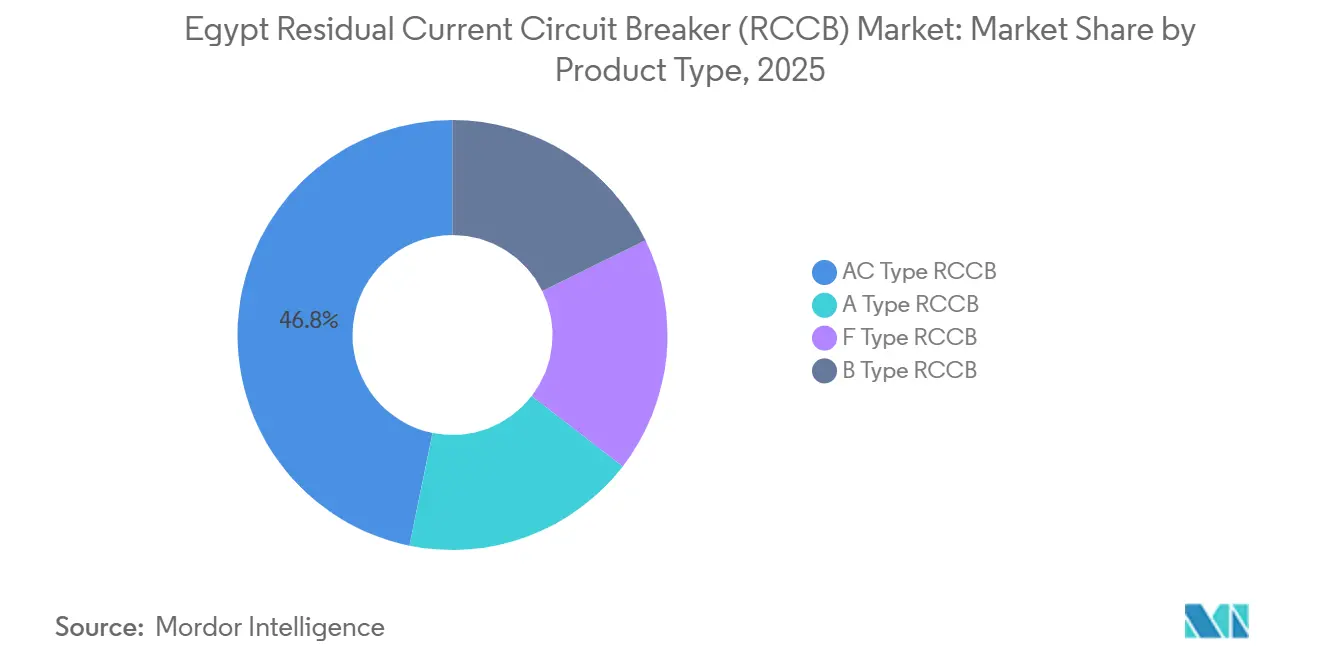

- By product type, AC Type RCCBs held 46.8% of Egypt residual current circuit breaker market share in 2025, while B Type RCCBs are forecast to expand at a 9.4% CAGR through 2031.

- By pole configuration, Two-Pole RCCBs accounted for 61.5% of the segment in 2025, while Four-Pole RCCBs recorded the highest projected CAGR at 8.6% through 2031.

- By rated current, the 25A–63A band captured 52.7% of the Egypt residual current circuit breaker market size in 2025, while the Above 63A tier is advancing at an 8.8% CAGR through 2031.

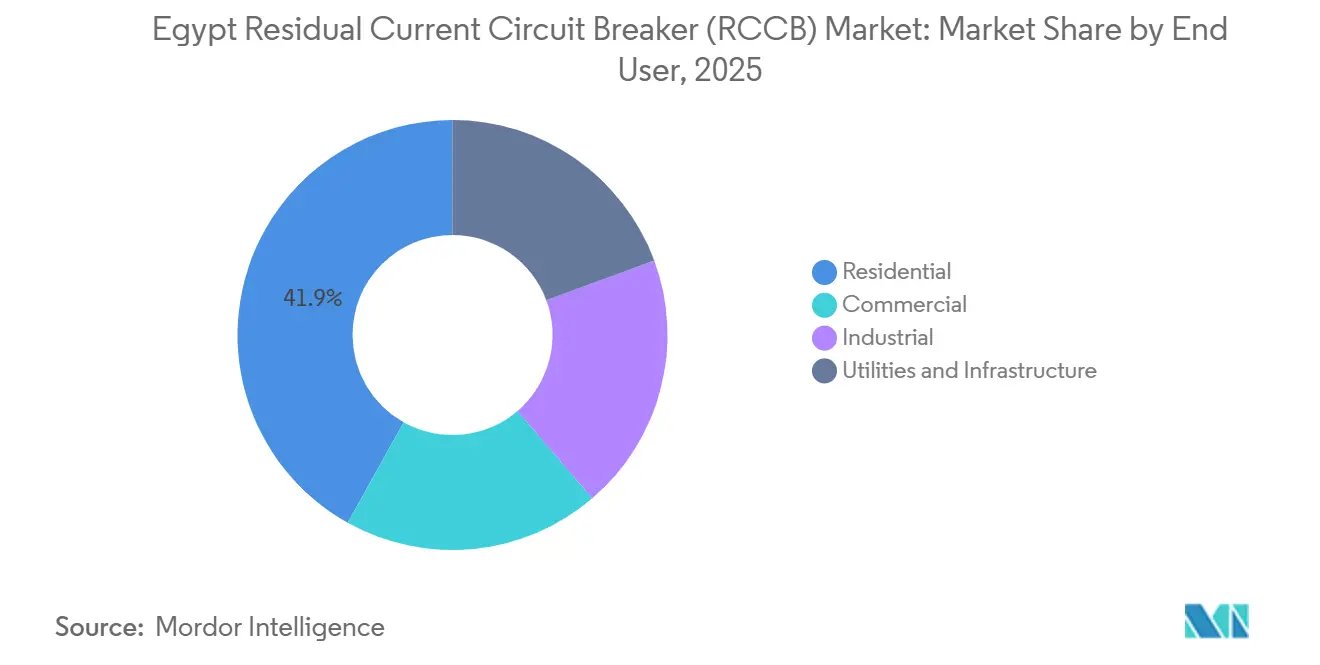

- By end user, Residential held 41.9% of the segment in 2025, while Utilities and Infrastructure is projected to grow fastest at a 9.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Residual Current Circuit Breaker (RCCB) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Wet-Area RCCB Requirements In Formal Wiring | +2.6% | National, with intensity in Greater Cairo, New Administrative Capital, Delta cities | Short term (≤ 2 years) |

| Commercial Safety Certification And Inspection Pressure | +1.3% | National, early gains in Cairo, Alexandria, Sharm El Sheikh | Medium term (2-4 years) |

| Mass Housing And Apartment Electrification Pipeline | +1.9% | National, concentrated in New Administrative Capital and new-city corridors | Short term (≤ 2 years) |

| Grid And Substation Modernization Spending | +0.8% | National, with Sinai, Canal Zone, and Upper Egypt as priority zones | Medium term (2-4 years) |

| Shift Toward Type A And Higher-Spec Protection | +0.7% | National, led by commercial and industrial hubs | Long term (≥ 4 years) |

| Smart-City And Hospitality Project Load Complexity | +0.5% | New Administrative Capital, Red Sea Coast, North Coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory Wet-Area RCCB Requirements And Commercial Inspection Pressure Support Formal Compliance

The Egypt residual current circuit breaker market draws steady residential demand from the Electrical Code requirement that a 30mA RCCB must protect wet-area circuits such as bathrooms, kitchens, and outdoor sockets in formally wired buildings. This rule is enforced through permit approval and final inspection, which means contractors cannot easily bypass the device in formal residential, commercial, and industrial projects. The same compliance logic now supports demand beyond housing because safety certification and inspection pressure are strengthening in commercial properties, hospitals, hospitality projects, and other specification-led buildings where payment and approval depend on documented conformity. That formal compliance environment creates a stable floor for the Egypt residual current circuit breaker market even when broader construction activity becomes uneven. It also explains why lower-cost substitution is much harder in regulated channels than in informal extensions or semi-formal small-contractor work. Procurement under these rules continues to favor devices that carry ES 4819 or IEC markings and that can clear inspection without dispute.

Mass Housing And Apartment Electrification Pipeline Sustains Throughput

Mass housing remains the clearest structural support for the Egypt residual current circuit breaker market because each newly electrified apartment or residential block requires at least one distribution board and at least one RCCB installation event. Egypt’s FY2025/2026 plan targeted 310,000 new units, including 285,000 social housing units, and the 2026 programme also included a 400,000-unit target announced in phased tranches under Sakan Misr, Dar Misr, and Jannah. That pipeline matters because apartment-heavy delivery reinforces recurring demand for two-pole, 30mA, and 25A–63A products that fit typical residential load conditions. The same build-out is also beginning to change product mix because 37 on-grid solar stations of 3 kW each were integrated on social housing blocks in Hadayek Al-Asimah City, introducing solar-readiness into public-housing specifications. If that practice spreads across a wider share of the public housing programme, the Egypt residual current circuit breaker market will gradually shift from AC Type concentration toward broader use of Type A devices. This keeps volume tied to public policy while opening a medium-term path for higher-value product adoption.

Grid And Substation Modernisation Spending Opens Utilities Channel

The Egypt residual current circuit breaker market is also gaining a more important utilities channel because EETC’s FY2024/2025 capital programme committed EGP 26.289 billion, which is approximately USD 565 million, to rehabilitate extra-high and high-voltage substations and extend transmission infrastructure.[2]Ministry of Electricity and Renewable Energy, “FY2024/2025 Transmission Investment Update,” Ministry of Electricity and Renewable Energy, moee.gov.eg That programme expanded the grid to 819 substations, 230,000 MVA of combined capacity, and 61,000 km of transmission lines, which increases the number of formal switchboards and grid-linked protection points. Additional reinforcement is being supported by a EUR 200 million EBRD package linked to a 500 kV substation upgrade in Cairo Governorate under the NWFE programme. Each rehabilitation project typically requires re-specified protection assemblies, including four-pole and higher-current devices used in distribution-level switchboards. Volume in this channel is smaller than residential volume, but project values are larger and procurement standards are stricter. That combination helps the Egypt residual current circuit breaker market generate better margins in utilities than it does in mass residential installations.

Shift Toward Type A, Higher-Spec Protection, And More Complex Loads Upgrades The Mix

The Egypt residual current circuit breaker market is gradually moving toward higher-spec products because modern electrical loads are producing fault conditions that older AC-only devices do not detect as reliably. Type B RCCBs are technically required in EV charging and transformerless solar applications because these systems can generate smooth DC residual currents that make Type AC devices effectively blind under certain fault conditions. Egypt’s EV charging rollout remains early, but the commercial solar pipeline that stalled during the Egyptera approval pause still represents deferred demand for Type B and Type A procurement once the regulatory framework is finalized. The fourth edition of IEC 61008-1 from November 2024 also raised the bar on temporary overvoltage resistance, which is pushing formal tenders to move away from older-generation products. Smart-city, hospitality, and mixed-use developments in the New Administrative Capital, the Red Sea Coast, and the North Coast are reinforcing the same direction because their load profiles are more complex and more specification-led than legacy apartment projects. Over time, this raises the quality threshold within the Egypt residual current circuit breaker market even if AC Type devices still dominate installed residential volume today.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-Led Competition From Low-Cost Channels | -1.3% | National, most acute in informal residential and small-contractor segment | Short term (≤ 2 years) |

| Import Dependence And Compliance Clearance Burden | -0.7% | National, with bottlenecks at Alexandria and Cairo customs | Medium term (2-4 years) |

| Solar Interconnection Pauses Delay Premium Device Uptake | -0.4% | National, concentrated in industrial and commercial rooftop pipeline | Short term (≤ 2 years) |

| Nuisance-Tripping Risk In Harmonics-Heavy Sites | -0.3% | Industrial clusters including 10th of Ramadan, Borg El Arab, and the Suez Canal Zone | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-Led Competition And Nuisance-Tripping Concerns Hold Back Premium Adoption

The Egypt residual current circuit breaker market faces direct pricing pressure from non-compliant and falsely branded electrical products circulating through lower-cost channels. Egypt’s Consumer Protection Agency confiscated 3,000 non-compliant electrical devices in a Qalyubia Governorate enforcement sweep, while the Exporters’ Division said some unlicensed factories were selling devices at prices 50% below certified equivalents by using copper purity as low as 96% instead of the required 99.99%. In practice, that pressure is strongest in informal housing extensions and semi-formal small-contractor work, where procurement decisions often center on upfront cost rather than documented compliance. The effect on the Egypt residual current circuit breaker market is margin compression for certified suppliers and more difficulty sustaining premium pricing in channels where inspection is weak. Nuisance-tripping risk also slows adoption in harmonics-heavy industrial sites because some buyers remain wary of device selection errors in settings with drives, converters, and complex power quality conditions. Formal tenders still protect compliant suppliers, but the gap between formal and informal procurement remains a persistent restraint.

Import Dependence, Compliance Clearance, And Solar Interconnection Pauses Slow Supply And Mix Upgrade

Import dependence remains a constraint in the Egypt residual current circuit breaker market because most RCCB components and many finished devices still come from external suppliers, with China, Germany, and the Czech Republic among key source countries for electrical switchgear. Egyptian pound volatility has raised landed costs, and customs clearance timelines at Alexandria and Cairo add delay and inventory risk that smaller distributors struggle to absorb. Ministerial Decree No. 246/2025, which adopted Egyptian Standard ES 1781 aligned with IEC 60335-1:2020, strengthened conformity requirements for manufacturers and importers and added another layer of documentation for market access. That supports product quality, but it also slows the speed at which new higher-spec devices can enter the market. At the same time, Egyptera’s suspension of solar grid-connection approvals from early 2025, and the end of net metering in December 2025, delayed procurement of premium Type A and Type B units in the distributed-generation segment and affected contracts tied to 270 registered solar companies. The backlog should reopen once the new framework is finalized, but until then it continues to limit higher-margin mix improvement in the Egypt residual current circuit breaker market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: AC Type Dominance Faces Structural Pressure From DC-Sensitive Devices

AC Type RCCBs held 46.8% of Egypt residual current circuit breaker market share in 2025, which reflected the long residential history of specifications built around sinusoidal AC fault protection only. Their position came from installed-base logic more than forward momentum, because two decades of single-phase residential construction normalized AC Type procurement across apartment and villa fit-outs. That legacy still matters in the Egypt residual current circuit breaker market because cost-sensitive public and private housing projects continue to purchase the lowest compliant devices that can satisfy inspection. Wet-area code requirements also reinforce this pattern by concentrating residential buying in basic, standardized protection devices rather than more advanced types. As a result, AC Type remains the largest product group even while formal specifications are shifting.

That shift is becoming clearer in new-city residential projects and commercial fit-outs, where A Type devices are gaining ground as pulsating DC leakage from switch-mode power supplies, inverter-driven appliances, and VFD-controlled HVAC systems becomes harder to ignore. F Type devices are also entering industrial automation and data-center applications, although from a small base. B Type RCCBs are the fastest-growing sub-segment, with a forecast 9.4% CAGR from 2026 to 2031, because EV charging infrastructure and transformerless solar installations require protection that can detect AC, pulsating DC, and smooth DC residual currents. The commercial solar backlog created by the net-metering suspension has delayed this transition, but it has not removed it. Once approvals resume under the new framework, the Egypt residual current circuit breaker market is likely to see a concentrated release of Type B and Type A demand in specification-led procurement cycles.

By Pole Configuration: Two-Pole Prevalence Anchored In Residential DNA

Two-Pole RCCBs secured 61.5% of the segment in 2025, giving them the largest position in the Egypt residual current circuit breaker market because they match the country’s dominant 230V single-phase residential supply. Apartments, villas, and small commercial units all fit naturally into this configuration, which keeps two-pole devices tied closely to housing completions and residential rewiring. The 2026 housing pipeline supported that position because each new unit requires a distribution board and at least one two-pole 30mA RCCB in standard formal wiring. This keeps two-pole volumes closely linked to new-city construction and to public housing delivery across the national development programme. The residential character of Egypt’s current build-out therefore continues to shape configuration demand more than any other factor.

Four-Pole RCCBs are the fastest-growing configuration, with an 8.6% CAGR projected for 2026 to 2031, as three-phase loads become more common in commercial complexes, hospitality assets, and industrial sites. That trend is visible in the New Administrative Capital, where high-rise mixed-use and hospitality developments require more sophisticated distribution systems. Elsewedy Electric’s role in supplying electrical infrastructure and smart systems for Tycoon Tower and Tycoon Center shows how premium projects are increasing demand for three-phase protection assemblies. Utilities investment reinforces the same direction because new and rehabilitated substations use four-pole protection assemblies as part of standard distribution switchboard design. This means the Egypt residual current circuit breaker market still relies on two-pole residential volume today, while its mix is gradually expanding toward four-pole devices in higher-value projects.

By Rated Current: Mid-Range Band Anchors Volume, High-Capacity Tier Leads Growth

The 25A–63A band held 52.7% of the Egypt residual current circuit breaker market size in 2025, which made it the core rated-current range for apartment circuits, air-conditioning feeders, and light-commercial panels. It sits at the center of current demand because Egypt’s housing pipeline remains strongly apartment-led, and most standard residential and small commercial applications fall comfortably into this range. The Up to 25A tier supports lower-load final circuits and auxiliary panels, but it is still secondary to the mid-range band in mainstream formal construction. This structure gives the Egypt residual current circuit breaker market a strong volume base in standardized current ratings. The residential and light-commercial mix therefore keeps the mid-range tier firmly in the lead.

The Above 63A segment is the fastest-growing tier, with an 8.8% CAGR forecast through 2031, as utility substation refurbishments, industrial panel upgrades, and large hospitality or commercial main boards require higher-capacity protection. EETC’s rehabilitation pipeline, backed in part by the EBRD’s EUR 200 million package, is creating recurring procurement for high-current devices in substations and related distribution infrastructure. Gulf of Suez transmission investment also strengthens this demand because wind-linked interconnection projects need larger switchgear and protection assemblies. Utilities tenders in these applications typically require ES 4819 and IEC 61008-1:2024 certification, which raises the entry threshold for suppliers. That is why the Egypt residual current circuit breaker market continues to derive its largest volume from 25A-63A devices, while future growth is strongest in the above-63A tier.

By End User: Residential Scale Meets Utilities Momentum

Residential end users commanded 41.9% of the segment in 2025, which kept them at the center of the Egypt residual current circuit breaker market because formal housing delivery, wet-area protection rules, and social-housing acceleration continue to generate repeat installation demand. New cities such as New Alamein, New Fayoum, New Minia, and New Qena remain part of that support base because formal housing there requires distribution boards and compliant RCCB assemblies. Commercial demand forms the next meaningful layer, supported by hotels, offices, retail, and mixed-use schemes that require better documented certification than informal housing channels. Projects such as PRE Group’s planned agreements with 8 international hotel brands covering 10,000 hospitality units, and Alkan Holding’s EGP 11 billion investment at Citadel Plaza through 2029, show the scale of formal hospitality electrification now entering the pipeline. Industrial buyers also favor traceable compliance and multinational supply where free-zone and factory inspections require documented standards.

Utilities and Infrastructure is the fastest-growing end-user group, with a projected 9.1% CAGR through 2031, because substation rehabilitation and new grid build-outs are formalizing more protection points across the country. EETC’s multi-year work in Sinai, Upper Egypt, and the Gulf of Suez corridor is central to this shift, and Egypt has already invested EGP 46 billion in Sinai electricity infrastructure, including 4,000 km of new cables and 600 transformers. The national target to lift renewable energy to 42% of the power mix by 2030 also keeps long-term interconnection spending active. That creates a durable pipeline for protection devices at new substations, grid interfaces, and distribution assemblies. For the Egypt residual current circuit breaker industry, this means residential remains the scale driver while utilities now provide the strongest medium-term growth momentum.

Geography Analysis

Greater Cairo absorbed the largest share of demand in the Egypt residual current circuit breaker market in 2025 because it combines the capital, satellite cities, and the New Administrative Capital in one concentrated formal construction zone. The New Administrative Capital alone requires 8.3 GVA of Phase 1 loads, supported by 19 main high-voltage substations and 16 future substations, which creates a large installed base for distribution-level protection devices. Cairo’s position is reinforced by public housing deliveries in cities such as New Obour, October City, and Hadayek Al-Asimah, where apartment-heavy construction keeps two-pole residential demand strong. Formal grid investment around the capital also deepens this lead, with Schneider Electric’s distribution control center digitization work stretching from Sharm El Sheikh to Minya, Upper Egypt, and the South Delta. China Southern Power Grid’s South Cairo pilot, which reduced area line loss from 17.6% to 6%, shows how modernization projects are improving technical performance while also supporting protection-device renewal in urban distribution systems.

Alexandria and the Delta form the second-largest demand cluster in the Egypt residual current circuit breaker market because Borg El Arab and the broader Delta manufacturing base sustain formal commercial and industrial electrical demand. The Red Sea and North Coast corridor is also becoming more important as hospitality investment lifts specification quality at resorts and mixed-use properties. Abu Dhabi Tourism Investment Company’s EGP 2.5 billion Mercure Hurghada Resort renovation, Jaz Hotel Group’s planned properties in Hurghada and Marsa Alam, and ELSEWEDY ELECTRIC’s role at Ras El Hekma point to a stronger premium channel in hospitality-led procurement. International hotel brands generally require IEC-certified devices, which helps push resort and hospitality projects away from informal sourcing and toward formal specification-led purchasing.

Upper Egypt, the Canal Zone, and Sinai remain the most forward-looking regional opportunities in the Egypt residual current circuit breaker market because grid investment there is advancing faster than current device volume. New Fayoum, New Minia, and New Qena are receiving social housing with integrated electricity networks that require compliant RCCB assemblies under national code rules. The Gulf of Suez wind corridor is also building a focused high-current demand base through large renewable projects and POWERCHINA’s completed 220 kV substation for the 500 MW Gulf of Suez wind farm. The planned EGP 12 billion transmission line across a 390 km corridor to connect Gulf of Suez wind projects to the national grid will extend that need for switchgear and protection deployments through mid-2027.

Competitive Landscape

The Egypt residual current circuit breaker market remains moderately fragmented, with a clear divide between formal procurement and informal price-led sales. In formal channels, Schneider Electric, ABB, Siemens, Legrand, Eaton, and Hager compete on certification credibility, technical support, service coverage, and the ability to satisfy specification-led tenders. In the informal channel, CHINT and lower-cost imports from China and Turkey compete more heavily on price, which limits pricing power for premium suppliers. This split keeps the Egypt residual current circuit breaker market open to several credible suppliers rather than concentrating control in a very small group. It also means that share gains are often decided by channel strategy and local availability rather than by brand recognition alone.

ABB Egypt’s reported annual turnover of EGP 14 billion and its ISO-certified 10th of Ramadan City complex show the advantage of scale, certification depth, and local manufacturing presence in winning domestic and export-linked work. Schneider Electric has built a similar advantage through expansion at Badr City, where two recent investment tranches totaling EUR 18 million raised low-voltage panel output and lifted local content to around 81%. Those moves improve lead times and reduce exposure to currency swings in a market that still depends heavily on imported components. CHINT remains the most credible price-based challenger in formal commercial and light-industrial applications because it combines an IEC-certified range with cost structures that are difficult for multinational subsidiaries to match.

Local Egyptian players such as Elsewedy Engineering Industries, Prima Electric, and AGEC operate mainly as distributors, project integrators, and after-sales support providers rather than as major RCCB device manufacturers. Elsewedy’s 2024 patent around busway configurations for dense residential and commercial buildings suggests that local differentiation is happening at the system-integration level rather than at the component level. White space still exists in smart and connected RCCBs that combine residual-current protection with remote monitoring and fault reporting, because no supplier holds a meaningful installed base in that niche today. The New Administrative Capital offers a natural pilot setting for those products because its broader infrastructure agenda already favors digital control, smart systems, and formal technical standards. Across the Egypt residual current circuit breaker market, this leaves competition active and multi-layered rather than tightly concentrated around one or two dominant vendors.

Egypt Residual Current Circuit Breaker (RCCB) Industry Leaders

Schneider Electric

ABB Ltd

Legrand

Siemens AG

CHINT Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ABB Egypt reported approximately EGP 14 billion in annual turnover and announced plans to drive local manufacturing expansion across its 10th of Ramadan City complex, with a stated target to power 70% of operations from solar energy by 2028, signalling continued long-term commitment to the Egyptian electrical market.

- April 2026: EETC signed a contract with Kharafi National to add two 500 kV gas-insulated switchgear units to the West Bakr substation in the Canal Electricity Zone, enabling the grid to absorb 2.8 GW of new Gulf of Suez wind energy, a substation upgrade that includes full protection and residual current device assemblies

Egypt Residual Current Circuit Breaker (RCCB) Market Report Scope

Residual Current Circuit Breaker (RCCB) is a pivotal electrical safety device designed to shield humans from potentially fatal electric shocks and to avert electrical fires due to current leakages. The RCCB operates by perpetually overseeing the equilibrium between the incoming and outgoing currents within a circuit.

The Egypt Residual Current Circuit Breaker (RCCB) Market is segmented into product type, pole configuration, rated current, and end-user. By product type, the market is segmented into AC type RCCB, A type RCCB, F type RCCB, and B type RCCB. By pole configuration, the market is segmented into two-pole and four-pole systems. By rated current, the market is segmented into up to 25A, 25A to 63A, and above 63A. By end-user, the market is segmented into residential, commercial, industrial, and utilities and infrastructure sectors. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| AC Type RCCB |

| A Type RCCB |

| F Type RCCB |

| B Type RCCB |

| Two-Pole RCCB |

| Four-Pole RCCB |

| Up to 25A |

| 25A to 63A |

| Above 63A |

| Residential |

| Commercial |

| Industrial |

| Utilities and Infrastructure |

| By Product Type | AC Type RCCB |

| A Type RCCB | |

| F Type RCCB | |

| B Type RCCB | |

| By Pole Configuration | Two-Pole RCCB |

| Four-Pole RCCB | |

| By Rated Current | Up to 25A |

| 25A to 63A | |

| Above 63A | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| Utilities and Infrastructure |

Key Questions Answered in the Report

What is the 2026 value of the Egypt residual current circuit breaker market?

The Egypt residual current circuit breaker market is valued at USD 17.27 million in 2026 and is projected to reach USD 25.63 million by 2031 at an 8.2% CAGR.

What is driving demand for RCCBs in Egypt most strongly?

Formal housing delivery and mandatory wet-area protection rules are the most immediate demand drivers, supported by 310,000 targeted units in FY2025/2026 and broad grid modernization spending.

Which product type is growing fastest in Egypt?

B Type RCCBs are growing fastest, with a projected 9.4% CAGR through 2031, because EV charging and transformerless solar applications require DC-sensitive protection.

Which pole configuration leads current demand?

Two-Pole RCCBs led with 61.5% share in 2025 because Egypt's dominant residential supply remains 230V single phase and apartment-driven construction still shapes volume demand.

Which end-user group offers the strongest future growth?

Utilities and Infrastructure is the fastest-growing end-user segment, with a 9.1% CAGR through 2031, supported by substation rehabilitation and renewable energy grid interconnection projects.

What is the main risk to premium RCCB adoption in Egypt?

Premium adoption is being held back by low-cost non-compliant imports, import dependence, customs delays, and the pause in solar grid-connection approvals that delayed Type A and Type B procurement.

Page last updated on: