Morocco Residual Current Circuit Breaker (RCCB) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

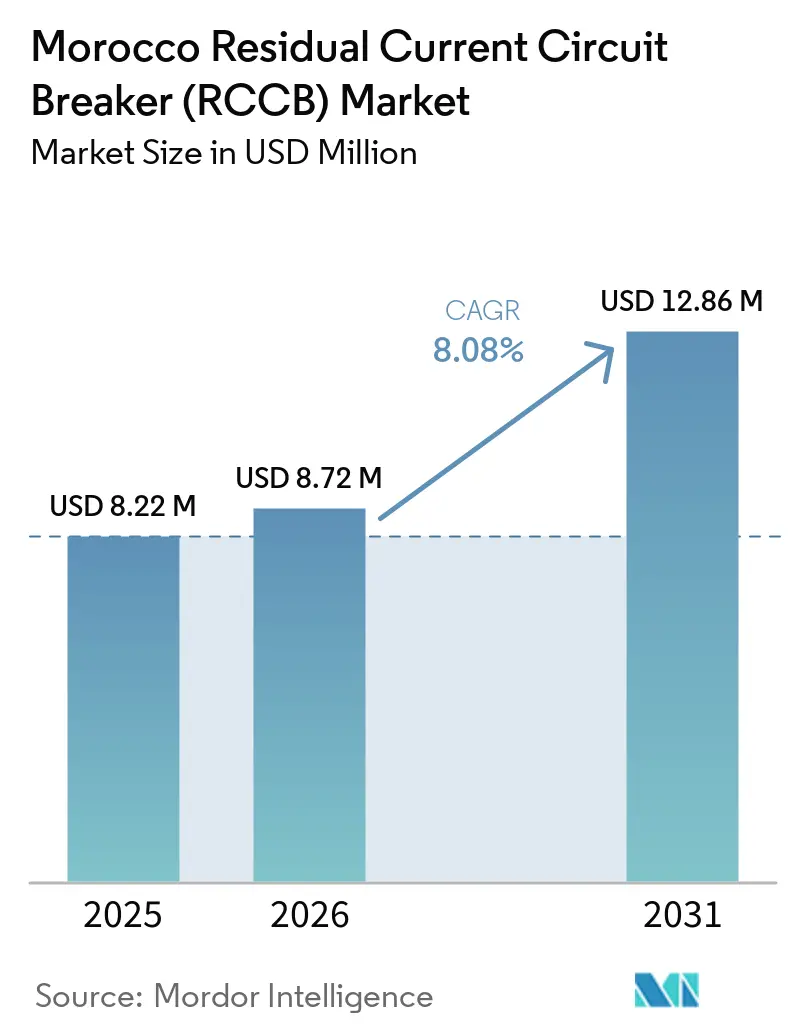

| Base Year Market Size (2025) | USD 8.22 Million |

| Market Size (2026) | USD 8.72 Million |

| Market Size (2031) | USD 12.86 Million |

| Growth Rate (2026 - 2031) | 8.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Residual Current Circuit Breaker (RCCB) Market Analysis by Mordor Intelligence

The Morocco Residual Current Circuit Breaker Market size is expected to grow from USD 8.22 million in 2025 to USD 8.72 million in 2026 and is forecast to reach USD 12.86 million by 2031 at 8.08% CAGR over 2026-2031. The Morocco residual current circuit breaker market is growing on the back of stricter installation safety expectations, expanding construction activity, and a steady move toward higher-specification protection in circuits that use electronics and power conversion. Demand is no longer tied only to new residential panels, because commercial retrofits, industrial automation, and utility-linked upgrades are also widening the addressable base for compliant devices. The product mix is also shifting in a way that supports value growth, since Type A, Type F, and Type B devices carry higher average selling prices than legacy Type AC units when installers specify them correctly for solar, HVAC, automation, and digitally managed loads. The Morocco residual current circuit breaker market also benefits from a visible pipeline of transport, hospitality, industrial, and digital infrastructure projects that require denser protection architecture across low-voltage panels. Competitive conditions remain moderate, with global brands holding an advantage in certified project channels while lower-cost imports and uneven installer practices continue to limit margin expansion in entry-level residential demand.

Key Report Takeaways

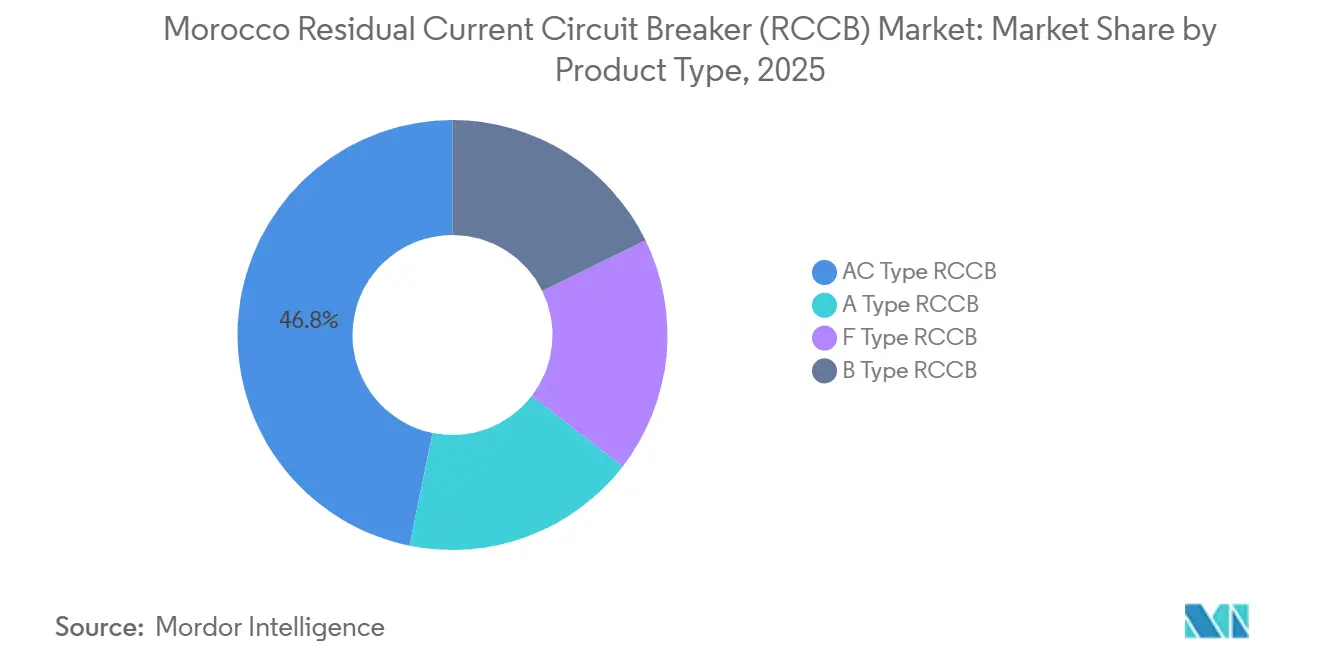

- By product type, AC Type RCCB led with 46.8% share in 2025, while B Type RCCB is forecast to expand at 8.9% CAGR through 2031.

- By pole configuration, Two-Pole RCCB held 63.5% of the Morocco residual current circuit breaker market share in 2025, while Four-Pole RCCB recorded the highest projected CAGR at 8.6% through 2031.

- By rated current, 25A to 63A accounted for 52.4% of the Morocco residual current circuit breaker market size in 2025, while Above 63A is projected to grow at 8.7% CAGR through 2031.

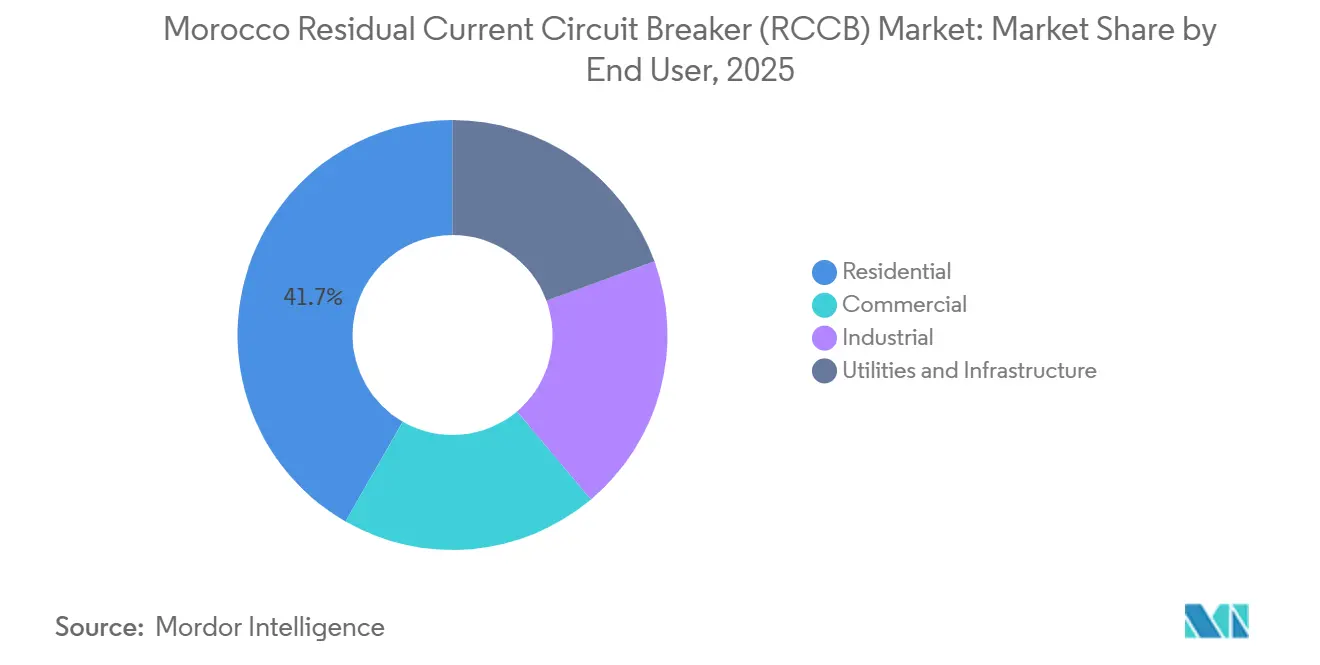

- By end user, Residential captured 41.7% share in 2025, while Utilities and Infrastructure is forecast to expand at 8.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Morocco Residual Current Circuit Breaker (RCCB) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory 30 mA Differential Protection In Low-Voltage Installations | +1.8% | Morocco-wide, with stronger enforcement in urban and peri-urban networks | Short term (≤ 2 years) |

| Construction And Infrastructure Buildout Ahead Of Major Public Projects | +2.0% | Casablanca-Settat, Rabat-Salé-Kénitra, Tanger-Tétouan, Marrakech-Safi | Medium term (2-4 years) |

| Industrial Expansion In Automotive And Export Manufacturing Clusters | +1.5% | Tanger-Kenitra industrial corridor, with spillover into Casablanca | Medium term (2-4 years) |

| Rooftop Solar Self-Consumption Rollout In Industrial And Tertiary Sites | +1.2% | Industrial zones and commercial buildings nationwide | Medium term (2-4 years) |

| Data-Center And Digital Infrastructure Loads Raising Protection Intensity | +0.8% | Casablanca, Rabat, Dakhla | Long term (≥ 4 years) |

| Shift From Type AC Toward Type A And Type F In Electronics-Heavy Circuits | +0.7% | Urban Morocco circuits influenced by global compliance norms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory 30 mA Differential Protection In Low-Voltage Installations

Mandatory residual-current protection remains one of the clearest supports for unit demand in the Morocco residual current circuit breaker market. Safety compliance at the consumer panel level keeps RCCB adoption tied to the basic structure of low-voltage installations rather than to discretionary spending alone. This matters because each new hookup, each panel replacement, and each compliance-driven refurbishment creates a repeat need for certified protection at the board level. The Morocco residual current circuit breaker market, therefore, draws support from both new urban construction and the gradual formalization of older installations that need better leakage protection. The effect is broader than a single end-use category, because the same compliance logic applies across households, small shops, and service buildings. That broad regulatory base also gives established brands a clearer path to volume stability when enforcement is applied through formal connection and inspection channels.

Construction And Infrastructure Buildout Ahead Of Major Public Projects

Large public project activity is raising commercial and institutional demand across the Morocco residual current circuit breaker market. Stadiums, airports, hotels, transport links, and supporting urban works all require multi-circuit low-voltage panels with higher device density than typical residential boards. This project mix is especially important because it lifts demand for four-pole products, higher current ratings, and certified devices that can pass formal engineering review. The Morocco residual current circuit breaker market also gains from the timing profile of these projects, since procurement begins during fit-out phases and continues through commissioning and post-handover maintenance. Hospitality and transit assets add another layer of demand because kitchens, laundry systems, HVAC equipment, and back-of-house services depend on reliable protection across electronically controlled circuits. As a result, construction-led demand is not only expanding volumes, but it is also improving the sales mix toward products with better pricing and specification discipline.

Industrial Expansion In Automotive And Export Manufacturing Clusters

Industrial electrification is becoming a more important growth base for the Morocco residual current circuit breaker market. Automotive, logistics, and export manufacturing sites use drives, robotics, converters, and process equipment that require stronger protection coordination than basic residential circuits. That changes the mix toward Type F and Type B devices in applications where pulsating or smooth DC leakage can appear during operation. Tanger Automotive City completed its third expansion phase in September 2025, adding 140 hectares and more than 70 industrial lots, which support a continuing pipeline of plant fit-outs and electrical panel procurement.[1]Tanger Med, “A New Step in the Expansion of Tanger Automotive City,” Tanger Med, tangermed.ma The Morocco residual current circuit breaker market is therefore gaining from a pattern of repeated procurement events, because each new industrial unit needs incoming protection, sub-distribution, and equipment-specific device selection. This industrial layer is valuable for suppliers because it tends to favor certified products, engineering support, and better after-sales coverage over simple low-price bidding.

Rooftop Solar Self-Consumption Rollout In Industrial And Tertiary Sites

Solar self-consumption is opening a new specification layer for the Morocco residual current circuit breaker market. Once solar moves from concept to active deployment, protective device selection becomes more complex because inverter outputs and associated electronics require device types that legacy Type AC units cannot always safely serve. Updated IEC 60364 guidance has strengthened this direction by setting clearer expectations for Type A, Type F, and Type B RCCB use in circuits with electronic controls and PV-related loads.[2]W9 Group, “New IEC 60364 Updates, What Do Stricter RCCB Requirements Mean for Your Projects,” W9 Group, w9-group.com This matters for the Morocco residual current circuit breaker market because rooftop solar in factories, offices, and tertiary buildings brings demand from customers that usually buy through formal engineering and electrical contracting channels. Those buyers are less likely to accept off-specification products where compliance, uptime, and insurance requirements are material. Over time, solar-linked demand should also support replacement activity in adjacent boards, because installations often trigger wider upgrades to distribution architecture and protection coordination.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Sensitivity And Informal Low-Cost Imports | -1.2% | Nationwide, with stronger concentration in peri-urban and rural channels | Short term (≤ 2 years) |

| Installer Preference For Basic Protection Architectures | -0.7% | Nationwide, especially rural and peri-urban areas | Medium term (2-4 years) |

| Nuisance-Tripping Concerns In Hot, Dusty, And Variable-Quality Installations | -0.6% | Southern and arid regions, plus industrial peripheries | Medium term (2-4 years) |

| Slow Low-Voltage Residential Solar Rule Implementation | -0.5% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity And Informal Low-Cost Imports

Price pressure remains one of the clearest restraints on value expansion in the Morocco residual current circuit breaker market. Entry-level residential demand is highly sensitive to upfront device cost, which creates room for low-cost imports to compete even when their compliance quality is uncertain. That weakens pricing power for established brands in the highest-volume channels and slows migration toward higher-grade specifications. The Morocco residual current circuit breaker market is especially exposed in self-build and small-contractor purchases, where buying decisions can still be driven by shelf price rather than lifecycle safety performance. This pressure does not eliminate demand, but it does cap the pace at which average selling prices can rise across the broader market. It also forces leading suppliers to balance certification, channel support, and affordability more carefully than in project-led commercial demand.

Installer Preference For Basic Protection Architectures

Installer behavior is another practical limit on mix improvement in the Morocco residual current circuit breaker market. Many electricians still default to the simplest familiar device architecture when the load profile is not reviewed in detail at the point of installation. That tends to preserve Type AC selection in smaller jobs even when the circuit contains electronics, motor drives, or inverter-based equipment that would justify a higher type specification. The result is slower adoption of Type A, Type F, and Type B products in the long tail of residential and light-commercial projects. The Morocco residual current circuit breaker market, therefore, depends not only on product availability but also on training, distributor guidance, and specification discipline at the installer level. Until that behavior changes more broadly, the technical case for higher-value RCCBs will continue to convert into sales more slowly than the underlying application trend would suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Transition Load Reshapes The AC-Type Baseline

AC Type RCCB held 46.8% of the Morocco residual current circuit breaker market size in 2025, and it remained the largest product category because single-phase residential boards still form the broadest installed base. Its leadership reflected low unit cost, basic familiarity among installers, and the continued presence of price-sensitive demand in peri-urban and rural channels. The category also benefited from the fact that many households and small shops still run circuits with simple appliance mixes that do not immediately force a switch to higher-specification protection. Even so, the Morocco residual current circuit breaker market is moving away from a pure AC-type baseline as electronics become more common in daily loads. Type A, therefore, continued to gain ground in urban housing and commercial settings where appliances, lighting controls, and compact power electronics are more common. This shift matters because even modest migration from AC Type to Type A improves the value mix of the Morocco residual current circuit breaker industry without requiring a dramatic jump in unit volumes.

The faster part of the product story sits in higher-sensitivity applications. B Type RCCB is forecast to grow at 8.9% CAGR through 2031, making it the fastest-growing product segment in the Morocco residual current circuit breaker market as solar and EV-linked use cases expand. This segment addresses applications where smooth DC leakage can impair the performance of lower-type devices, which gives it a clear technical role in modern electrical architecture. F Type RCCB also occupies a meaningful niche, especially where variable-speed drives, inverter compressors, and mixed-frequency loads appear in HVAC and industrial circuits. IEC 61008-1 fourth edition took effect on November 21, 2024 and added temporary overvoltage resistance testing while strengthening the compliance baseline for RCCBs used in household and similar applications. That change supports the ongoing mix shift in the Morocco residual current circuit breaker market because device selection is now more closely tied to actual load characteristics rather than to a lowest-cost default. Over time, the product ladder should become more segmented, with AC Type retaining scale, Type A widening across general electronics-heavy circuits, and Types F and B taking a larger share of premium applications.

By Pole Configuration: Four-Pole Demand Mirrors Commercial Construction Intensity

Two-Pole RCCBs accounted for 63.5% of the Morocco residual current circuit breaker market share in 2025, which reflected the dominance of single-phase residential wiring across the country. The configuration remained the volume leader because most household boards and many small-business installations still rely on phase and neutral protection in compact panel formats. This makes two-pole devices central to base demand, especially in lower-ticket projects where installation simplicity and replacement compatibility matter. The Morocco residual current circuit breaker market also keeps this segment active because housing additions and ordinary refurbishments occur across a much wider footprint than large commercial builds. Within that installed base, the configuration is not static, because more boards now include electronics-heavy circuits that can gradually pull Type A, Type F, or even Type B specifications into the two-pole range.

Four-Pole RCCB is projected to grow at 8.6% CAGR through 2031, making it the fastest-growing pole configuration in the Morocco residual current circuit breaker market. Its momentum comes from hotels, airports, stadiums, factories, data facilities, and other three-phase environments where protection must cover more complex panel arrangements. This segment benefits from the same commercial and infrastructure pipeline that is lifting demand for higher current ratings and better-certified device families. As a result, the volume gap with two-pole products will remain wide, but the value contribution of four-pole units will continue to rise. That pattern matters to the Morocco residual current circuit breaker industry because project-driven demand usually favors engineering review, documented compliance, and stronger service support. It also helps large brands, since multi-pole project orders are less exposed to informal low-cost imports than residential shelf sales. The pole configuration mix, therefore, shows a market that still depends on household scale, but is increasingly shaped by professional commercial procurement.

By Rated Current: Above 63A Segment Anchors Industrial And Infrastructure Demand

The 25A to 63A band held 52.4% of the Morocco residual current circuit breaker market size in 2025, and it remained the broadest rated-current category because it covers the most common household and light-commercial panel requirements. This band sits at the center of unit demand, since common residential ratings and many small service installations fall within it. It also faces the strongest price competition, which keeps margin pressure visible in the very part of the market that sells the highest number of devices. Up to 25A products serve a narrower role in smaller sub-circuits and legacy installations, so they continue to matter for replacement demand even if they add less to overall value growth. The Morocco residual current circuit breaker market, therefore, still leans heavily on the mid-band current range for volume stability.

The growth story is stronger above that range. Above 63A RCCB is forecast to expand at 8.7% CAGR through 2031, making it the fastest-growing rated-current class in the Morocco residual current circuit breaker market. This segment is closely tied to feeder circuits, industrial sub-mains, large HVAC systems, and commercial or utility boards where current intensity is materially higher than in standard household applications. Those use cases are growing because infrastructure, manufacturing, and digital facilities need larger protected loads and more structured panel design. In practice, that gives certified suppliers an advantage because higher-current applications are more likely to go through formal specification and testing review. The Morocco residual current circuit breaker market also sees less direct substitution risk here, since off-specification devices are harder to place in professionally engineered panels. Over time, the rated-current mix should continue to tilt upward as more value comes from industrial and infrastructure projects rather than from basic residential additions alone.

By End User: Utilities Growth Signals A Structural Shift Beyond Residential Dominance

Residential remained the largest end-user category with 41.7% share in 2025, which underlined how strongly the Morocco residual current circuit breaker market still depends on housing stock, ordinary panel demand, and routine low-voltage protection needs. The segment kept its lead because every dwelling unit needs board-level protection, and that gives residential demand a much wider footprint than any single project-driven channel. It also remained the most exposed segment to price sensitivity, informal supply, and installer default behavior, which is why high volume did not automatically translate into the strongest value growth. Even so, residential demand will remain important throughout the forecast period because urban housing additions and retrofit activity continue to replenish the installed base. The Morocco residual current circuit breaker industry still draws its volume foundation from this segment, even as higher-value growth shifts elsewhere.

Utilities and infrastructure are projected to grow at 8.4% CAGR through 2031, making it the fastest-growing end-user segment in the Morocco residual current circuit breaker market. This reflects the buildout of transport-linked facilities, grid reinforcement activity, public infrastructure works, and other large low-voltage installations that require heavier protection architecture. The segment is important because it aligns with the faster-growing product profiles seen elsewhere in the market, including four-pole devices, higher current ratings, and more advanced RCCB types. Commercial demand also remains solid, supported by hospitality, retail, and service-sector fit-outs, while industrial demand benefits from manufacturing expansion and equipment-heavy panel design. These mid-range segments do not yet displace residential scale, but they are steadily raising the average technical requirement of the Morocco residual current circuit breaker market. That shift supports branded suppliers that can serve engineering-led tenders and provide documentation, local support, and a wider product range. It also makes future growth less dependent on low-ticket residential volume alone.

Geography Analysis

The Morocco residual current circuit breaker market does not split into formal country sub-markets, so regional analysis is best understood through demand concentration by economic corridor. Casablanca-Settat remained the largest demand center because it combines the country’s biggest concentration of commercial real estate, transport assets, services activity, and electrical contracting capacity. This makes the region the main anchor for commercial panels, hospitality fit-outs, and utility-linked low-voltage installations. The area also matters on the supply side because leading global brands and local assemblers rely on Casablanca-based distribution, engineering, and service relationships to reach national customers. In practical terms, that gives Casablanca-Settat an outsized role in shaping the near-term direction of the Morocco residual current circuit breaker market, especially where project-specified demand is concerned.

Tanger-Tétouan-Al Hoceïma is the fastest-rising industrial demand corridor in the Morocco residual current circuit breaker market because factory, logistics, and export-oriented facilities continue to deepen the need for higher-specification protection. Tanger Automotive City expanded again in September 2025, with 140 hectares delivered and more than 70 industrial lots added, reinforcing the pipeline for new panel installations and electrical fit-outs. This corridor is especially relevant for Type F and Type B demand, since automation, converters, and electronically controlled production lines create a stronger case for advanced protection types. The region also supports larger rated-current devices because manufacturing and logistics facilities use feeder and sub-main architectures that sit above ordinary residential needs. As a result, Tanger is becoming one of the clearest regional drivers of value growth in the Morocco residual current circuit breaker market.

Rabat-Salé-Kénitra adds a different layer to the Morocco residual current circuit breaker market because it combines administrative demand, industrial activity, and a growing digital infrastructure profile. Kenitra supports equipment-heavy industrial installations, while Rabat contributes demand from government buildings, service facilities, and professionally specified electrical rooms. Southern urban centers such as Marrakech and Agadir also matter because hospitality and event-linked construction require three-phase protection across hotels, support services, and venue infrastructure. Taken together, these corridors show that the Morocco residual current circuit breaker market is still national in scope, but growth is increasingly concentrated in regions where commercial, infrastructure, and industrial investment overlap.

Competitive Landscape

The Morocco residual current circuit breaker market shows moderate concentration, with multinational OEMs holding the strongest position in project-led commercial and industrial channels. Schneider Electric, ABB, Legrand, Hager, and Siemens benefit from established distribution, technical support, and brand recognition in certified installations. Their advantage is strongest where customers need documented compliance, broad product portfolios, and engineering assistance for panel design. At the same time, the Morocco residual current circuit breaker market is not tightly closed, because local and imported brands remain active in price-sensitive residential channels. This keeps competition balanced between specification strength at the top end and aggressive pricing in the high-volume entry tier.

Schneider Electric remains one of the most visible competitive forces in the Morocco residual current circuit breaker market because it has paired channel depth with localization moves aimed at faster project delivery. Its 2025 manufacturing partnership with GROUPELEC for low-voltage switchboard customization is a practical example of how leading suppliers are positioning for infrastructure-led demand. Legrand continues to compete strongly in the commercial specification tier through its low-voltage protection portfolio and regional channel reach. Hager also remains relevant because its RCCB offering covers the AC, A, and B types that are most important as the market moves beyond legacy residential selection. These companies are better placed when buyers prioritize compliance, product breadth, and training support over simple shelf-price comparisons.

Local manufacturer Ingelec retains a meaningful position in the Morocco residual current circuit breaker market because local inventory depth and channel relationships still matter in routine distribution sales. At the lower end, CHINT and Delixi remain aggressive on pricing, especially in residential volume demand, where brand loyalty can be weaker. A second competitive opening sits in Type B and Type F supply, where solar, EV-adjacent use cases, and converter-heavy loads are creating room for specialists such as ETI Elektroelement and Doepke. IEC 61008-1, fourth edition, has also raised the technical bar for compliant products, which supports vendors that can prove alignment with updated testing requirements. The result is a market where scale and certification matter more in project channels, while affordability and distribution reach still drive outcomes in mass residential sales. That balance is why the Morocco residual current circuit breaker market remains moderately consolidated rather than highly concentrated.

Morocco Residual Current Circuit Breaker (RCCB) Industry Leaders

Schneider Electric

ABB Ltd

Legrand

Hager Group

Eaton Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Nexus Core Systems signed a MAD 12 billion (USD 1.29 billion) MoU with Morocco's Ministry of Digital Transition and AMDIE at GITEX Africa 2026 to build an AI data-center factory, a high-performance computing facility, and an innovation hub in Morocco, the country's largest single digital infrastructure commitment and a direct driver of high-intensity electrical protection procurement in Casablanca and Dakhla.

- March 2026: Morocco's government published Decree No. 2.25.100 in the Official Gazette, entering into force on June 9, 2026, and formally enabling solar self-consumption with grid surplus sales of up to 20% of annual production; installations between 11 kW and 5 MW must obtain a grid connection agreement, activating mandatory Type A/B RCCB specifications at tens of thousands of prospective industrial and commercial rooftop sites.

Morocco Residual Current Circuit Breaker (RCCB) Market Report Scope

Residual Current Circuit Breaker (RCCB) is a pivotal electrical safety device designed to shield humans from potentially fatal electric shocks and to avert electrical fires due to current leakages. The RCCB operates by perpetually overseeing the equilibrium between the incoming and outgoing currents within a circuit.

The Morocco Residual Current Circuit Breaker (RCCB) Market is segmented into product type, pole configuration, rated current, and end-user. By product type, the market is segmented into AC type RCCB, A type RCCB, F type RCCB, and B type RCCB. By pole configuration, the market is segmented into two-pole RCCB and four-pole RCCB systems. By rated current, the market is segmented into up to 25A, 25A to 63A, and above 63A. By end-user, the market is segmented into residential, commercial, industrial, and utilities and infrastructure sectors. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| AC Type RCCB |

| A Type RCCB |

| F Type RCCB |

| B Type RCCB |

| Two-Pole RCCB |

| Four-Pole RCCB |

| Up to 25A |

| 25A to 63A |

| Above 63A |

| Residential |

| Commercial |

| Industrial |

| Utilities and Infrastructure |

| By Product Type | AC Type RCCB |

| A Type RCCB | |

| F Type RCCB | |

| B Type RCCB | |

| By Pole Configuration | Two-Pole RCCB |

| Four-Pole RCCB | |

| By Rated Current | Up to 25A |

| 25A to 63A | |

| Above 63A | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| Utilities and Infrastructure |

Key Questions Answered in the Report

What is the 2031 outlook for Morocco residual current circuit breaker demand?

The Morocco residual current circuit breaker market is forecast to reach USD 12.86 million by 2031 from USD 8.72 million in 2026, with growth supported by construction, industrial electrification, and a higher-specification product mix.

Which product type is growing the fastest in Morocco?

B Type RCCB is the fastest-growing product segment, with an expected 8.9% CAGR through 2031 because solar, EV-adjacent, and converter-based circuits need smooth DC detection capability.

Why do two-pole devices still lead sales in Morocco?

Two-pole RCCB held 63.5% share in 2025 because the installed base is still led by single-phase residential wiring, which keeps household panel demand at the center of unit volumes.

Which end-user group is expanding the quickest?

Utilities and Infrastructure is the fastest-growing end-user segment at 8.4% CAGR through 2031, reflecting the role of public works, transport-linked facilities, and grid-related installations.

How is industrial growth changing RCCB demand in Morocco?

Industrial projects are shifting demand toward Above 63A, Type F, and Type B devices because factory and automation environments use larger feeders, drives, robotics, and electronically controlled equipment.

What is the biggest commercial challenge for suppliers in Morocco?

Price sensitivity remains the main challenge because low-cost imports and installer preference for basic architectures slow the move toward higher-value compliant products in residential and light-commercial channels.

Page last updated on: