South Africa Renewable Gas From Waste Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

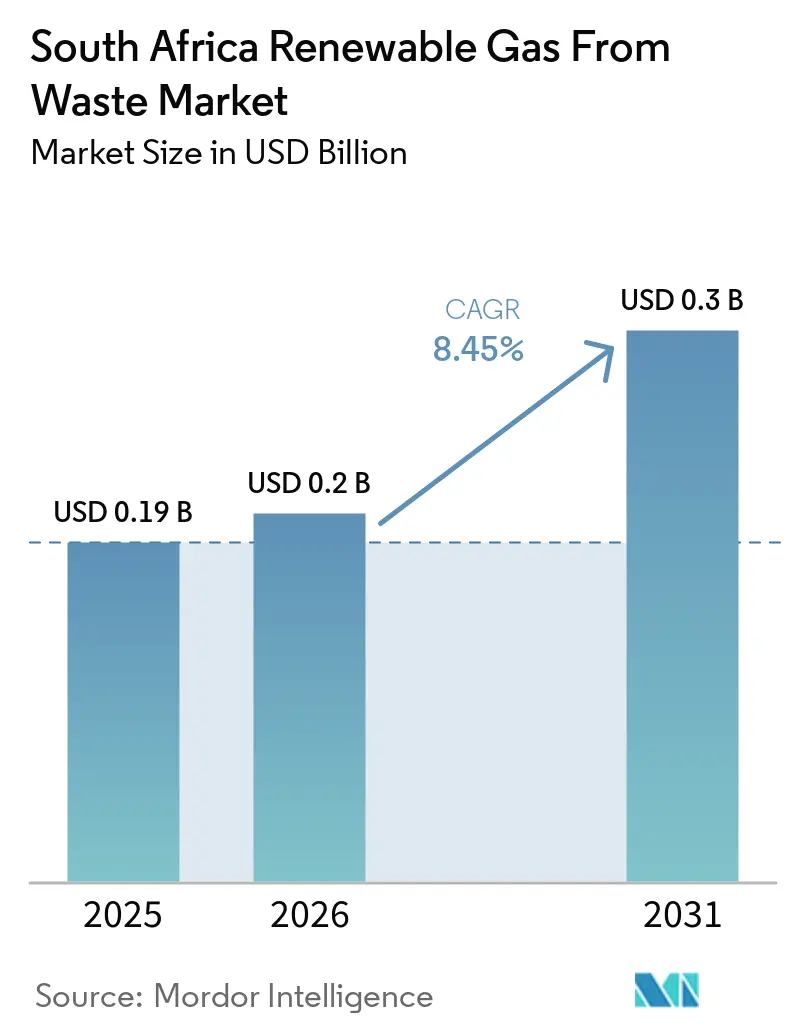

| Base Year Market Size (2025) | USD 0.19 Billion |

| Market Size (2026) | USD 0.2 Billion |

| Market Size (2031) | USD 0.3 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

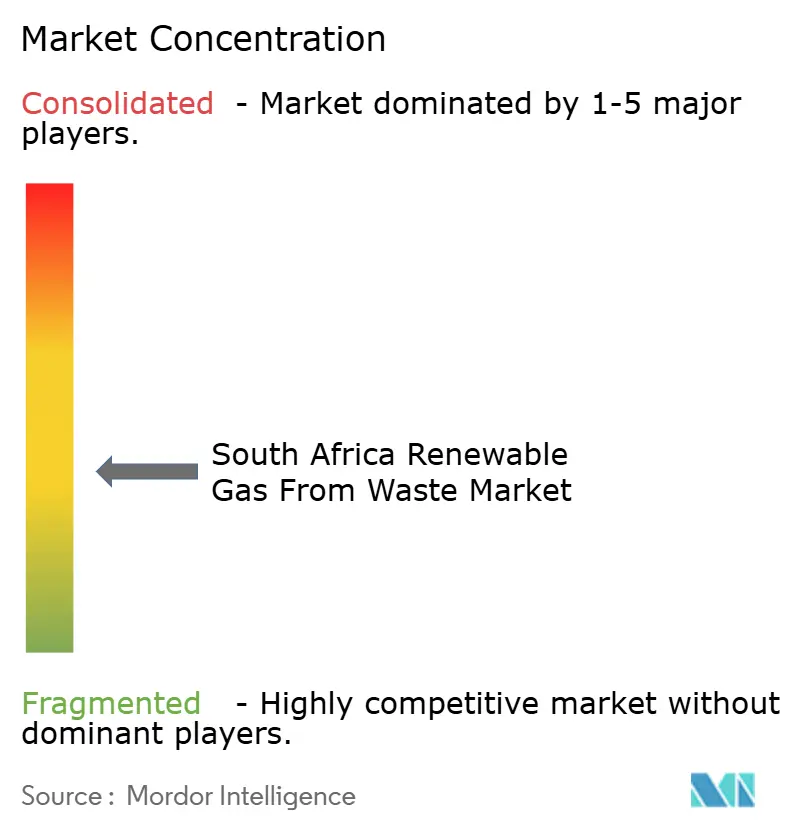

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Renewable Gas From Waste Market Analysis by Mordor Intelligence

The South Africa Renewable Gas From Waste Market size is projected to be USD 0.19 billion in 2025, USD 0.2 billion in 2026, and reach USD 0.3 billion by 2031, growing at a CAGR of 8.45% from 2026 to 2031.

South Africa’s economy lost USD 168.3 billion due to load shedding in 2023, and even though the loss fell to USD 28.9 billion in 2024, the experience pushed many industrial users toward on-site and dispatchable renewable gas projects. The Climate Change Act 22 of 2024, South Africa’s second NDC, submitted in October 2025, and the rise in carbon tax from USD 14.2 in 2025 to USD 18.5 per ton of CO₂e from January 2026 have made landfill diversion and gas recovery more commercially relevant for major emitters. The JET-IP and the October 2025 IRP approval have also strengthened the setting for the South Africa renewable gas from waste market by expanding access to concessional finance and creating a stronger gas-to-power demand signal for domestic renewable gas. Even with these supportive market conditions, the South Africa renewable gas from waste market still faces slower monetization in projects that depend on grid injection, REIPPPP (Renewable Energy Independent Power Producer Procurement Program) access, or wheeling, which keeps competition focused on feedstock security, captive offtake, and bilateral deal execution rather than pure scale.

Key Report Takeaways

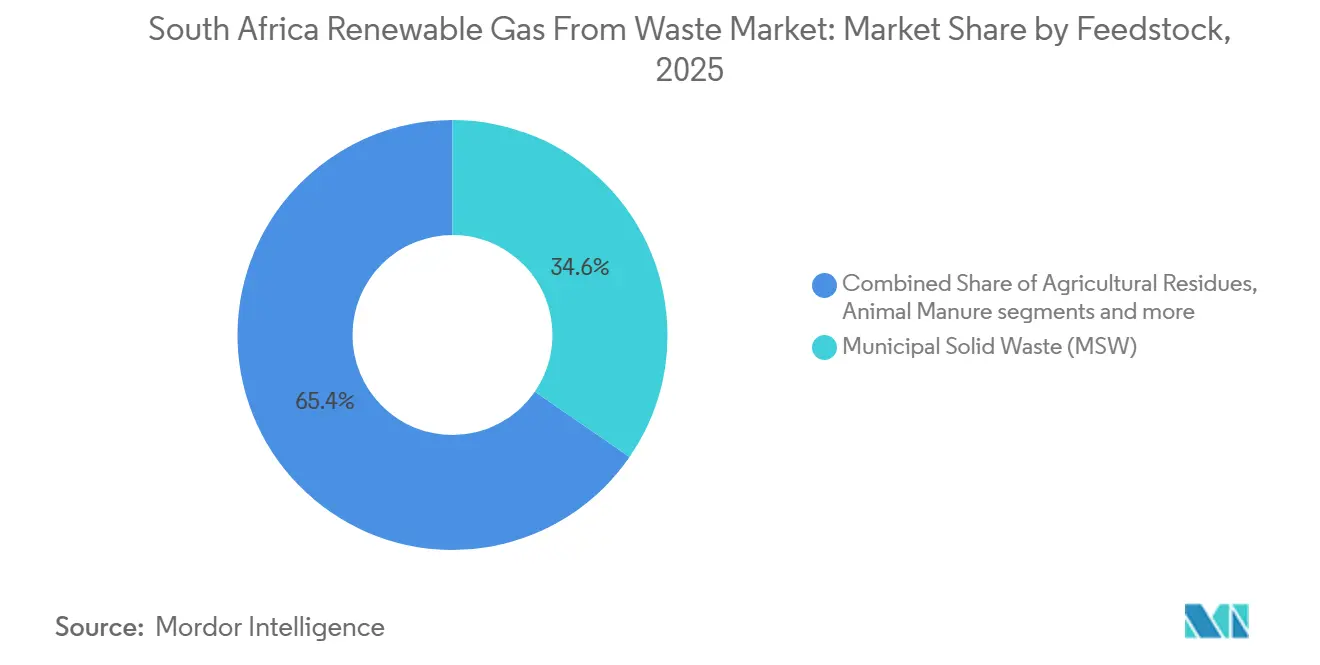

- By feedstock, municipal solid waste accounted for 34.6% of the South Africa renewable gas from waste market share in 2025, while food waste is forecast to expand at a 9.5% CAGR through 2031.

- By technology, landfill gas recovery accounted for 38.4% of the South Africa renewable gas from waste market size in 2025, while biogas upgrading systems are projected to grow at a 10.8% CAGR through 2031.

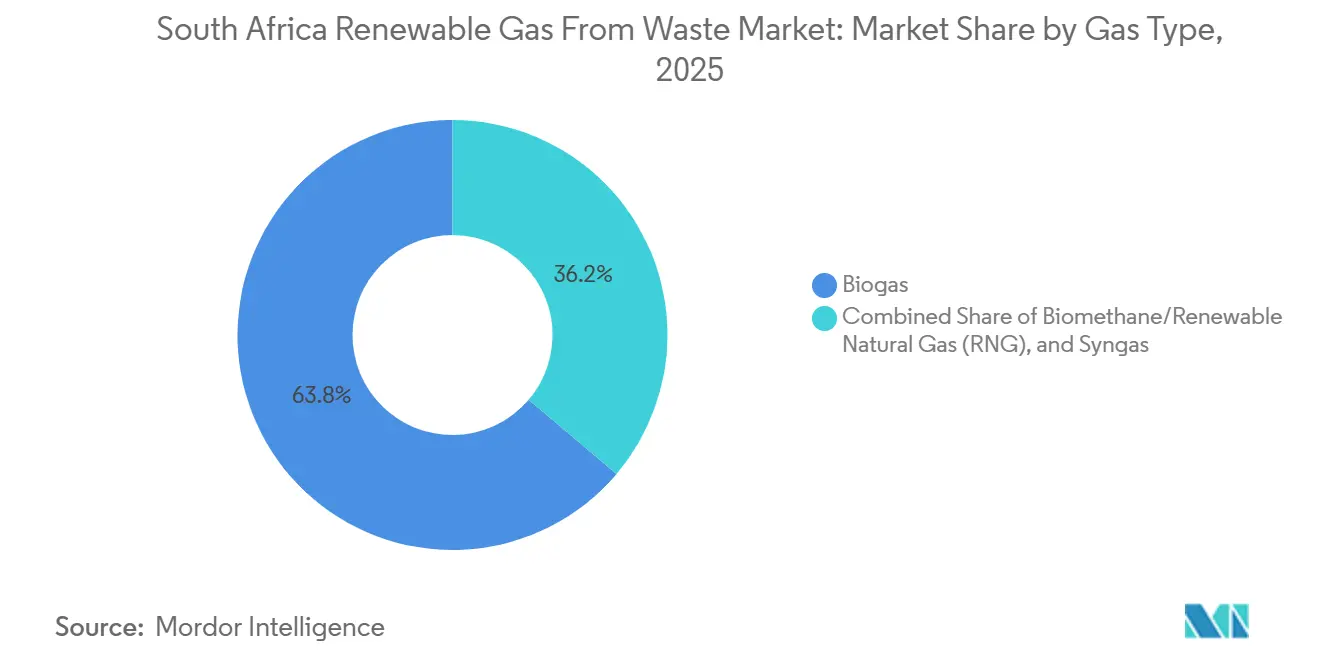

- By gas type, biogas held 63.8% share in 2025, while biomethane/renewable natural gas is expected to record the fastest growth at an 11.9% CAGR through 2031.

- By application, electricity generation accounted for 44.2% of the market in 2025, while transportation fuel is forecast to expand at a 12.5% CAGR through 2031.

- By component, gas collection systems led with 34.7% share in 2025, while monitoring and control systems are projected to advance at an 11.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Renewable Gas From Waste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Load Shedding Creating Urgent Demand for On-Site Renewable Gas Energy | +2.0% | National, with concentrated impact in Gauteng, Western Cape, and KwaZulu-Natal industrial belts | Short term (≤ 2 years) |

| REIPPPP Landfill Gas Category Enabling Long-Term Power Purchase Agreements with Eskom | +1.7% | National, with early gains in Gauteng and Western Cape, where landfill gas assets are concentrated | Medium term (2-4 years) |

| Just Energy Transition Plan Mobilizing Concessional Finance for Waste-to-Gas Projects | +1.4% | National, with spillover to Mpumalanga and KwaZulu-Natal industrial transition zones | Medium term (2-4 years) |

| Escalating Carbon Tax Creating Financial Incentive for Fossil Fuel Substitution | +1.1% | National, with near-term impact on energy-intensive sectors in Gauteng and Mpumalanga | Medium term (2-4 years) |

| Climate Change Act 2024 Establishing Legally Binding Sectoral Emissions Targets | +0.8% | National, with the highest impact on the liquid fuels and power generation sub-sectors | Short term (≤ 2 years) to Medium term (2-4 years) |

| Abundant Agro-Industrial Organic Waste Providing High-Yield Captive Feedstock | +0.6% | Western Cape, KwaZulu-Natal, Free State, and Limpopo agro-industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Load Shedding Creating Urgent Demand for On-Site Renewable Gas Energy

South Africa’s long load shedding cycle changed how industrial users value on-site and dispatchable power. Eskom’s 2025 annual statements recorded 329 days of load shedding during the financial year ended March 2024, and the same filing cited CSIR’s estimate that the economy lost USD 168.3 billion in 2023 because of outages. Eskom’s recovery plan then delivered 310 consecutive load-shedding-free days between March 2024 and January 2025, and only 26 hours of load shedding were recorded in winter 2025. That improvement did not reverse earlier investment decisions, because years of grid unreliability had already pushed many industrial firms to build capital plans around self-generation and bilateral supply. In the South Africa renewable gas from waste market, this matters because biogas offers dispatchable output and more stable baseload characteristics than solar alone, which keeps off-taker interest intact even as grid performance improves.[1]Eskom SOC Limited, “Annual Financial Statements for the Year Ended 31 March 2025,” Eskom, eskom.co.za

REIPPPP Landfill Gas Category Enabling Long-Term Power Purchase Agreements with Eskom

The REIPPPP (Renewable Energy Independent Power Producer Procurement Program) has treated landfill gas and biogas as eligible technologies since the program began, which gave the South Africa renewable gas from waste market an early institutional route to long-term offtake. Bid Window 7 was structured to procure up to 5,000 MW across eligible renewable technologies, including biomass and biogas within the organic waste and landfill gas grouping. Preferred bidders announced in December 2024 and July 2025 mainly reflected solar allocations, yet the core value of the program for waste-to-gas developers remains the 20-year PPA framework with Eskom. That structure reduces financing risk for gas capture and digestion assets whose returns need longer payback periods than merchant projects usually allow. It also pushes municipalities and landfill operators to maintain more reliable gas capture conditions, because revenue certainty depends on stable gas yields and compliant landfill management.[2]Development Bank of Southern Africa, “ITP PQBs and REIPPPP BW7 Summary,” DBSA, dbsa.org

Just Energy Transition Plan Mobilizing Concessional Finance for Waste-to-Gas Projects

The JET-IP for 2023-2027 set funding needs at USD 90.1 billion, and international pledges had reached USD 12.9 billion by the latest JET PMU reporting. This financing pool matters for the South Africa renewable gas from waste market because many early projects need concessional structures before commercial lenders will support them at scale. Cabinet approval of IRP 2025 in October 2025 added another layer of support by allocating 6,000 MW of gas-to-power capacity through 2030. That allocation creates a stronger demand signal for domestic renewable gas at a time when dependence on imported pipeline gas still carries supply and geopolitical risk. Waste-to-gas developers that can demonstrate methane avoidance and fossil fuel displacement are, therefore, better placed to access blended finance instruments aligned with the just transition agenda.[3]Government of the United Kingdom, “12-Month Just Energy Transition Partnership Leaders’ Update 2025,” GOV.UK, gov.uk

Escalating Carbon Tax Creating Financial Incentive for Fossil Fuel Substitution

South Africa’s carbon tax rose from ZAR 236 (USD 14.2) per tonne of CO2e in 2025 to ZAR 308 (USD 18.5) per tonne of CO2e, effective 1 January 2026, increasing the direct cost of emissions-intensive energy use for industrial operators. This matters for renewable gas from waste because methane capture and fossil fuel substitution now offer a clearer compliance value alongside energy generation. The 2026 amendments to revenue laws and the updated environmental levy framework also sharpen the emissions accounting basis that waste-gas producers and major emitters must work within. For landfill operators, food processors, and other organic waste generators, the financial case for diverting waste to gas recovery has become stronger, as uncontrolled emissions now carry a higher tax burden. This is helping shift renewable gas from waste from a discretionary sustainability option toward a more practical operating and compliance decision in South Africa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence of Biomethane Grid Injection Standards and Pipeline Access Framework | -1.8% | National, with the highest penalty in Gauteng and Western Cape, where upgrading-grade projects are most viable | Long term (≥ 4 years) |

| Complex Regulatory and Project Development Challenges for Small-Scale Renewable Gas Projects | -1.3% | National, most acute for sub-5 MW agricultural and community biogas developers | Medium term (2-4 years) |

| Low Legacy Electricity Tariffs and High Wheeling Charges Limiting Project Viability | -1.0% | National, most pronounced for rural projects dependent on cross-network wheeling | Short term (≤ 2 years) to Medium term (2-4 years) |

| Poor Waste Segregation and Underdeveloped Collection Infrastructure Constraining Feedstock Quality | -0.7% | Urban metros and smaller municipalities, with relatively lower impact in Cape Town | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Absence of Biomethane Grid Injection Standards and Pipeline Access Framework

South Africa still has no published biomethane grid-injection standard for producers seeking to inject upgraded gas into the transmission network. The National Energy Regulator of South Africa (NERSA) regulates the piped gas industry. Yet, no clear gas-quality specification or third-party access rule has been issued for the injection of biomethane into the ROMPCO and Sasol systems. Cabinet approved the Draft Gas Bill 2025 in December 2025 for submission to Parliament, and the bill modernizes the legal framework for gas transport and distribution. Even so, the approved draft does not yet solve the biomethane-specific injection gap, which means upgrading projects remain tied to captive use or virtual pipeline distribution. This keeps margins lower than they could be for large pipeline-linked projects and slows the development of a higher-value layer of the South Africa renewable gas from waste market.

Complex Regulatory and Project Development Challenges for Small-Scale Renewable Gas Projects

The South Africa renewable gas from waste market faces significant challenges due to complex regulatory processes, high upfront development costs, and limited financial support mechanisms for small-scale projects. Lengthy environmental approvals, multiple licensing requirements, detailed feasibility studies, and grid connection procedures increase project development timelines and raise early-stage investment risks. Smaller municipalities, agricultural operators, and emerging independent developers often struggle to secure funding for project preparation before achieving revenue certainty. Furthermore, the absence of dedicated large-scale procurement pathways and limited long-term offtake security reduces investor confidence. As a result, a considerable share of renewable gas from waste projects in South Africa continues to depend on private commercial agreements and self-consumption models, restricting faster market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Municipal Waste Anchors Scale While Food Waste Redefines Returns

Municipal solid waste accounted for 34.6% of the South Africa renewable gas from waste market share in 2025, confirming that metro-scale waste volumes still anchor the commercial base of current projects. Gauteng, Western Cape, and KwaZulu-Natal remain the main feedstock hubs because they combine larger waste streams with stronger hauling and disposal systems. These conditions make municipal waste the default choice for landfill gas recovery and other larger projects that need long-duration offtake and stable throughput. Agricultural residues, animal manure, industrial organic waste, sewage sludge, landfill waste, and other streams each serve narrower but important roles across the market.

Food waste is projected to grow at a 9.5% CAGR from 2025 to 2031, making it the fastest-rising feedstock in the South Africa renewable gas from waste market. This shift reflects increasing regulatory and commercial pressure on producers, retailers, and processors to divert organic waste from landfill under the Climate Change Act and waste regulations already in force. Food processors in the Western Cape and KwaZulu-Natal are therefore moving toward gate-fee-plus-energy structures that improve project returns and reduce direct emissions exposure. Sewage sludge remains underused even though the 2025 Springer review noted that South Africa has a significant wastewater treatment plant base with limited biogas harvesting relative to that asset pool. The smaller role of co-digestion and other blended streams also leaves room for better feedstock optimization in the South Africa renewable gas from waste market.

By Technology: Landfill Gas Recovery Dominates, but Upgrading Systems Signal the Next Value Layer

Landfill gas recovery accounted for 38.4% of South Africa renewable gas from waste market size in 2025, reflecting South Africa’s installed landfill base in major metros and the lower capital burden of passive gas extraction compared with digestion-based systems. This technology has also benefited from long-standing eligibility within REIPPPP, which helped establish a path to contracted offtake and bankable revenue. Anaerobic digestion holds the next major position, especially in agro-industrial and food-sector projects that operate under bilateral supply arrangements. Gasification and pyrolysis remain at an earlier stage because they need higher capital intensity and more consistent feedstock quality than much of the current waste stream can support.

Biogas upgrading systems are forecast to expand at a 10.8% CAGR from 2025 to 2031, which marks a clear move toward higher-value gas products. This change suggests that developers are no longer focusing solely on electricity sales and are instead targeting industrial gas users with stronger margins. Projects using membrane separation, pressure swing adsorption, or water scrubbing can serve customers through virtual pipeline models even while formal grid injection remains unresolved. That gives upgrading a practical role in the South Africa renewable gas from waste market before pipeline access rules are fully developed. The technology mix is therefore shifting from basic extraction and flaring toward more differentiated gas-processing capabilities.

By Gas Type: Biogas Holds Volume Command but Biomethane/Renewable Natural Gas (RNG) is Rewriting the Revenue Ceiling

Biogas accounted for 63.8% of the market in 2025, showing that most operating projects still use captured landfill gas or digester output directly for electricity or thermal energy. This setup keeps capital costs lower and operating complexity more manageable, which explains its broad use in Gauteng and Western Cape projects. Biomethane/renewable natural gas (RNG) and syngas together account for a smaller part of the portfolio, and syngas in particular remains tied to pilot-scale gasification and pyrolysis rather than a full commercial rollout. The present structure, therefore, favors simpler operating models over a deeper capture of the gas value chain.

Biomethane/renewable natural gas (RNG) is forecast to grow at a 11.9% CAGR from 2025 to 2031, making it the fastest-growing gas type in the South Africa renewable gas from waste market. The driver is closely linked to South Africa’s broader gas diversification agenda and the 6,000 MW gas-to-power allocation in IRP 2025. Domestic RNG from waste offers industrial users a route to lower import dependence and less exposure to cross-border pipeline risk. That shift moves project economics beyond electricity parity and toward gas substitution, which offers a higher ceiling for quality and logistics management. It is one of the most commercially significant developments in the forecast period, even though its current volume base is still smaller than that of conventional biogas.

By Application: Power Generation Anchors Revenue, but Transportation Fuel is the Wild Card

Electricity generation accounted for 44.2% of the South Africa renewable gas from waste market in 2025, reflecting the continued dominance of landfill gas-to-power projects and corporate biogas power arrangements. Combined heat and power also plays an important role, especially in food processing, beverage production, and agricultural facilities that require both electricity and heat. Grid injection remains commercially limited because formal biomethane injection standards are still absent, so much of the activity linked to grid participation centers on wheeled electricity rather than physical gas movement. Industrial heating and smaller heating uses serve practical process needs where direct fuel substitution offers cost and reliability benefits.

Transportation fuel is projected to grow at a 12.5% CAGR from 2025 to 2031, making it the fastest-growing application in the South Africa renewable gas from waste market. Interest in compressed biomethane is rising for refuse trucks, agricultural logistics fleets, and industrial transport, where diesel replacement can support both cost and emissions goals. The JET implementation plan includes a New Energy Vehicles portfolio, which enhances the policy fit for alternative fuels derived from domestic waste streams. The circular-economy value proposition is strengthened because collected waste can be converted into transport fuel. This creates a stronger anchor demand for upgrading projects than intermittent electricity pricing alone can provide.

By Component: Collection Systems Form the Backbone, While Digital Controls Define the Frontier

Gas collection systems accounted for 34.7% of the market in 2025, reflecting the fundamental reality that gas must first be captured before downstream value can be created. In landfill gas projects, this means wellheads, piping, headers, blowers, and condensate systems absorb a large share of early capital deployment. Digesters and fermentation systems held the next major component position, supported by the rising number of agricultural and food-sector digestion plants. Gas processing units, compressors, storage systems, and power generation equipment each serve distinct roles depending on whether a project targets electricity, heat, or upgraded gas sales.

Monitoring and control systems are forecast to grow at a 11.1% CAGR from 2025 to 2031, indicating that the South Africa renewable gas from waste market is moving toward more complex facility management. Projects with multiple feedstocks and outputs need better process visibility to maintain gas yield and contract compliance. The financing case is also changing, as carbon reporting, performance verification, and structured development finance increasingly depend on higher data quality. The 2026 Frontiers in Climate study identified monitoring and reporting capability as a condition that improves access to stronger financing structures in South African biogas settings. This means digital controls are becoming commercial infrastructure rather than a discretionary add-on.

Geography Analysis

Gauteng remained the dominant provincial cluster in the South Africa renewable gas from waste market in 2025 because it combines large municipal waste flows, industrial organic waste, and financially capable offtakers. The province also benefits from its concentration of food processing and manufacturing activity, which improves the case for bilateral contracts and co-digestion models. Bio2Watt’s Bronkhorstspruit Biogas Plant has operated in Gauteng since 2015 and has contributed close to 100 GWh to the national grid, making the province one of the most visible operating references in the country. Gauteng also stands out because it hosts many of the larger emitters most likely to face tighter carbon budget pressure under the Climate Change Act, which reinforces project demand from both compliance and energy security.

The Western Cape was the second-largest and fastest-growing provincial cluster for the South Africa renewable gas from waste market. Its position rests on stronger municipal execution, a concentrated food and beverage processing base, and a track record in both landfill gas and anaerobic digestion. Fountain Green Energy’s projects at Coastal Park and Vissershok have given Cape Town a meaningful installed base, and the Stellenbosch landfill gas extraction system was commissioned in April 2025 with containerized equipment from Renew Technologies. The province’s dairy, fruit processing, and abattoir activities also create more controlled organic streams than mixed municipal waste, which supports better project bankability. The EEAS-backed 2025 wastewater-to-green-methanol investment linked to sewage sludge processing and co-located solar capacity also shows that the Western Cape and nearby value chains could host more advanced renewable gas applications over time.

KwaZulu-Natal, the Eastern Cape, and the rest of the country form the next growth frontier for the South Africa renewable gas from waste market. KwaZulu-Natal has strong feedstock potential from sugar operations, abattoirs, and Durban’s broader municipal and industrial base. Even so, weaker segregation and collection systems still limit how much of that theoretical supply becomes bankable feedstock supply. Similar conditions are evident in other provinces, where underfunded municipal infrastructure and lower developer density slow deployment despite strong agricultural waste potential. Over the medium term, JET-linked transition planning and wider provincial renewable energy programs are likely to support more manure and residue-based projects in Mpumalanga, Limpopo, and KwaZulu-Natal.

Competitive Landscape

The South Africa renewable gas from waste market is moderately fragmented, with no single operator holding a dominant installed position across all feedstocks and technologies. The market comprises a diverse range of participants, including project developers, engineering specialists, landfill gas operators, and industrial users with captive assets. Unlike fully integrated utilities, these players focus on specific segments of the value chain. As a result, competition in the market revolves around critical factors such as securing feedstock control, establishing bankable offtake agreements, ensuring operational reliability, and structuring bilateral contracts effectively. This fragmentation highlights the market's evolving nature and the opportunities for specialized players to carve out niches.

AgriGas Africa is pursuing a different route by targeting biomethane injection around Sasolburg and building a customer pipeline for 2 PJ of offtake commitments. That strategy reflects one of the clearest open spaces in the South Africa renewable gas from waste market, industrial gas substitution rather than pure electricity sales. Bio2Watt’s 2024 framework agreement with Nijhuis Saur Industries is another important move because it brings external technology support into BEH’s African biogas pipeline. International partnerships of that kind matter because upgrading, gas quality certification, and downstream logistics remain early-stage capabilities in the local market.

The next layer of competition is being shaped by financing discipline and digital operating capability. Operators with stronger monitoring systems, better gas-quality reporting, and clearer carbon accounting are better positioned to secure concessional finance and comply with performance-linked contracts. NERSA’s 2025 wheeling rules and Eskom’s tariff changes have also pushed developers to favor captive and co-located demand over network-reliant delivery. That means the strongest players are not simply those with the most projects, but those that can combine feedstock security, reliable operations, and commercially workable offtake in the right location.

South Africa Renewable Gas From Waste Industry Leaders

Bio2Watt Energy Holdings (Pty) Ltd

AGAMA Biogas (Pty) Ltd

AgriGas Africa (Pty) Ltd

Anaergia Africa (Pty) Ltd

Veolia Services Southern Africa (Pty) Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Effective January 1, 2026, South Africa's carbon tax rate is USD 18.5 per ton of CO₂e, as outlined in the 2026 Budget Review. Amendments to the Carbon Tax Act, 2019, update emission factors and net calorific values, increase penalties for methane emissions, and support waste-to-gas projects.

- April 2026: Eskom's FY2027 Schedule of Standard Prices, effective April 1, 2026, revises wheeling tariffs by increasing the fixed Generation Capacity Charge from 20% to 30% and excluding it from energy credits under wheeling and net-billing. This raises wheeling-based renewable gas power costs, pushing waste-to-gas developers toward captive and co-located offtake models.

South Africa Renewable Gas From Waste Market Report Scope

| Municipal Solid Waste (MSW) |

| Agricultural Residues |

| Animal Manure |

| Industrial Organic Waste |

| Sewage Sludge |

| Food Waste |

| Others |

| Anaerobic Digestion |

| Landfill Gas Recovery |

| Gasification |

| Pyrolysis |

| Biogas Upgrading Systems |

| Others |

| Biogas |

| Biomethane/Renewable Natural Gas (RNG) |

| Syngas |

| Electricity Generation |

| Combined Heat & Power (CHP) |

| Grid Injection |

| Transportation Fuel |

| Industrial Heating |

| Residential & Commercial Heating |

| Others |

| Gas Collection Systems |

| Digesters & Fermentation Systems |

| Gas Processing & Upgrading Units |

| Compressors & Storage Systems |

| Power Generation Equipment |

| Monitoring & Control Systems |

| Others |

| By Feedstock | Municipal Solid Waste (MSW) |

| Agricultural Residues | |

| Animal Manure | |

| Industrial Organic Waste | |

| Sewage Sludge | |

| Food Waste | |

| Others | |

| By Technology | Anaerobic Digestion |

| Landfill Gas Recovery | |

| Gasification | |

| Pyrolysis | |

| Biogas Upgrading Systems | |

| Others | |

| By Gas Type | Biogas |

| Biomethane/Renewable Natural Gas (RNG) | |

| Syngas | |

| By Application | Electricity Generation |

| Combined Heat & Power (CHP) | |

| Grid Injection | |

| Transportation Fuel | |

| Industrial Heating | |

| Residential & Commercial Heating | |

| Others | |

| By Component | Gas Collection Systems |

| Digesters & Fermentation Systems | |

| Gas Processing & Upgrading Units | |

| Compressors & Storage Systems | |

| Power Generation Equipment | |

| Monitoring & Control Systems | |

| Others |

Key Questions Answered in the Report

What is driving growth in renewable gas from waste in South Africa?

The strongest drivers are tighter climate regulation, higher carbon tax, abundant organic waste, and the long-lasting shift toward on-site energy after years of load shedding. The market is projected to rise from USD 0.2 billion in 2026 to USD 0.3 billion by 2031 at an 8.5% CAGR.

Which feedstock leads current project deployment?

Municipal solid waste leads current deployment with 34.6% share in 2025 because large metros offer stronger waste volumes, hauling systems, and landfill-based project opportunities.

Which technology is growing the fastest?

Biogas upgrading systems are the fastest-growing technology with a 10.8% CAGR through 2031 as developers target higher-value biomethane and renewable natural gas sales.

Why is transportation fuel becoming more important?

Transportation fuel is forecast to grow at a 12.5% CAGR because compressed biomethane is becoming more relevant for refuse trucks, agricultural logistics, and industrial fleets looking for diesel alternatives.

Which provinces are the most important for project development?

Gauteng remains the main provincial base because of industrial demand and waste volumes, while the Western Cape is the second-largest and fastest-growing cluster due to stronger municipal execution and agro-processing waste streams.

What is the main barrier to larger biomethane projects?

The biggest structural barrier is the absence of biomethane grid injection standards and a clear third-party pipeline access framework, which keeps upgraded gas projects limited to captive use or virtual pipeline models.

Page last updated on: