Germany Renewable Gas From Waste Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

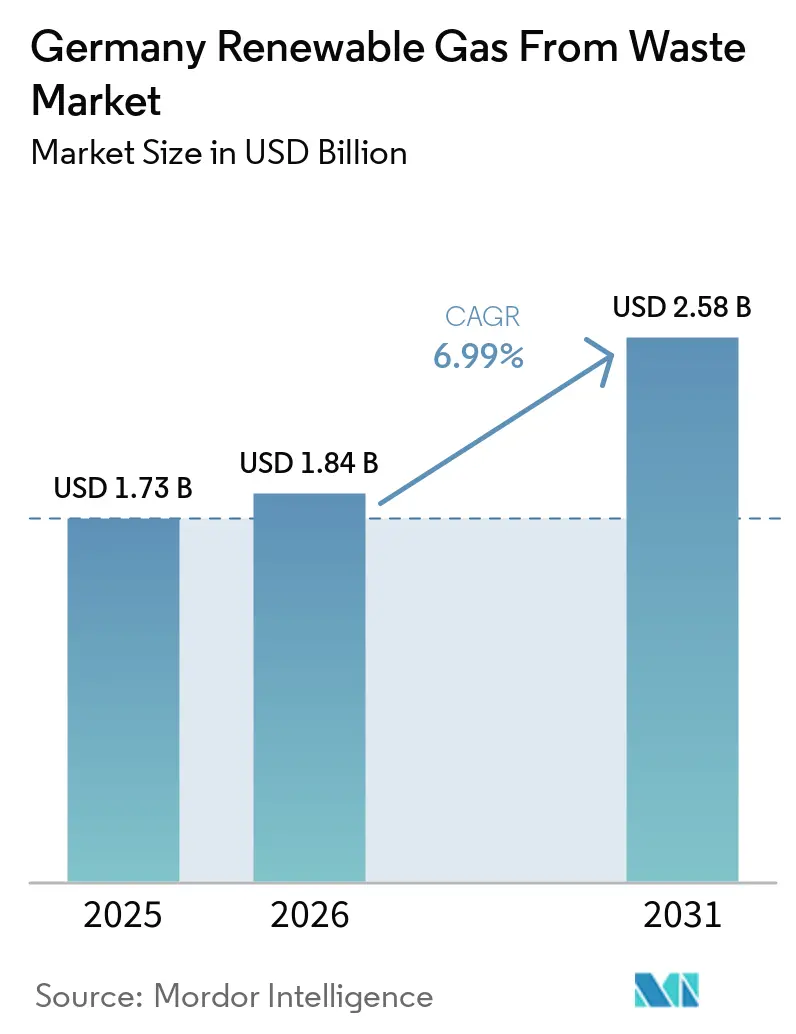

| Base Year Market Size (2025) | USD 1.73 Billion |

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 2.58 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Renewable Gas From Waste Market Analysis by Mordor Intelligence

The Germany renewable gas from waste market size is expected to increase from USD 1.73 billion in 2025 to USD 1.84 billion in 2026 and reach USD 2.58 billion by 2031, growing at a CAGR of 6.99% over 2026-2031.

The Germany renewable gas from waste market is entering a more durable growth phase because electricity, transport, and heating are now drawing on the same feedstock and production base, a clear shift from the earlier single-use model. The country remains the European Union's largest biomethane producer, accounting for close to one-third of EU-27 output, making Germany's renewable gas from waste market central to the bloc's 2030 biomethane expansion path, according to the International Energy Agency (IEA). Growth is being reinforced by three linked policy changes: the expiry of EEG support for older plants, the transport-side pull from the GHG quota system, and the heating-side demand created by the Buildings Energy Act. The Germany renewable gas from waste market still faces near-term friction from quota market volatility, falling wholesale electricity prices, and uncertainty around post-GasNZV grid access, but these issues are slowing project timing rather than undermining the minimum long-term demand supported by regulation and decarbonization targets. Competition remains moderate because technology suppliers, developers, operators, and municipal actors overlap across the value chain. Yet, no single company controls all the key profit pools in Germany renewable gas from waste market.

Key Report Takeaways

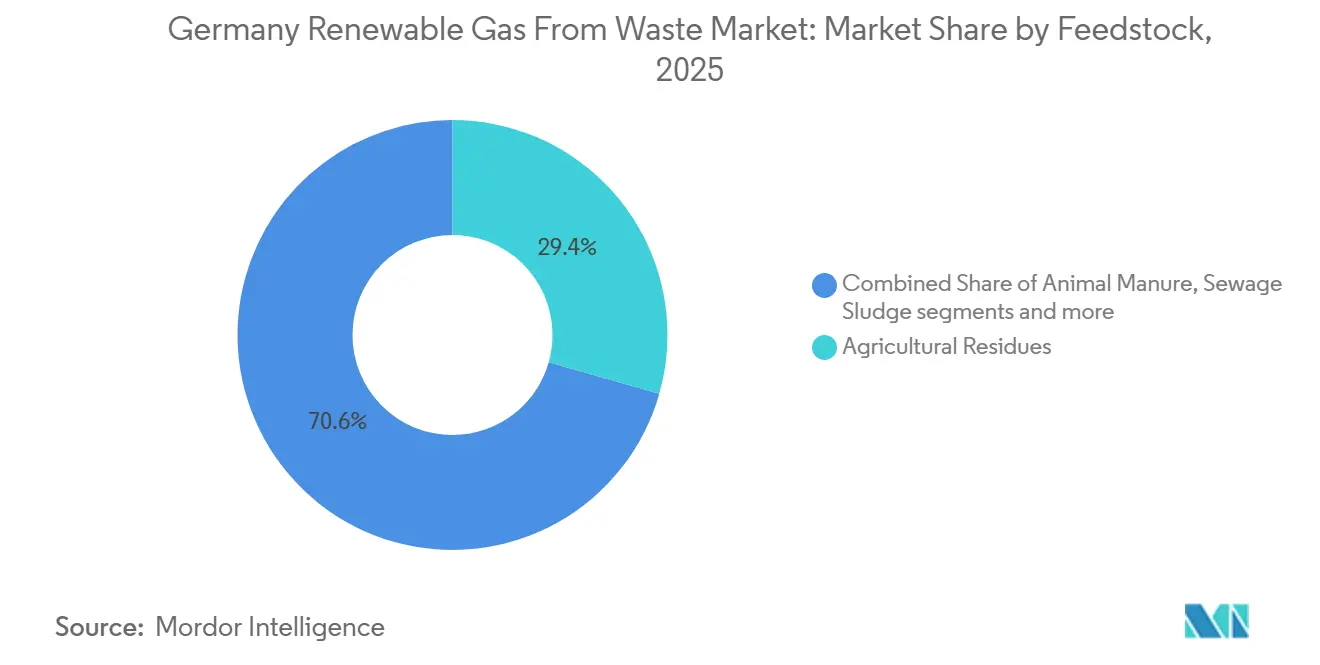

- By feedstock, agricultural residues led with a 29.4% of the Germany renewable gas from waste market size in 2025, while food waste is forecast to expand at a 7.2% CAGR through 2031.

- By technology, anaerobic digestion held a 46.3% of the Germany renewable gas from waste market share in 2025, while biogas upgrading systems recorded the highest projected CAGR at 7.7% through 2031.

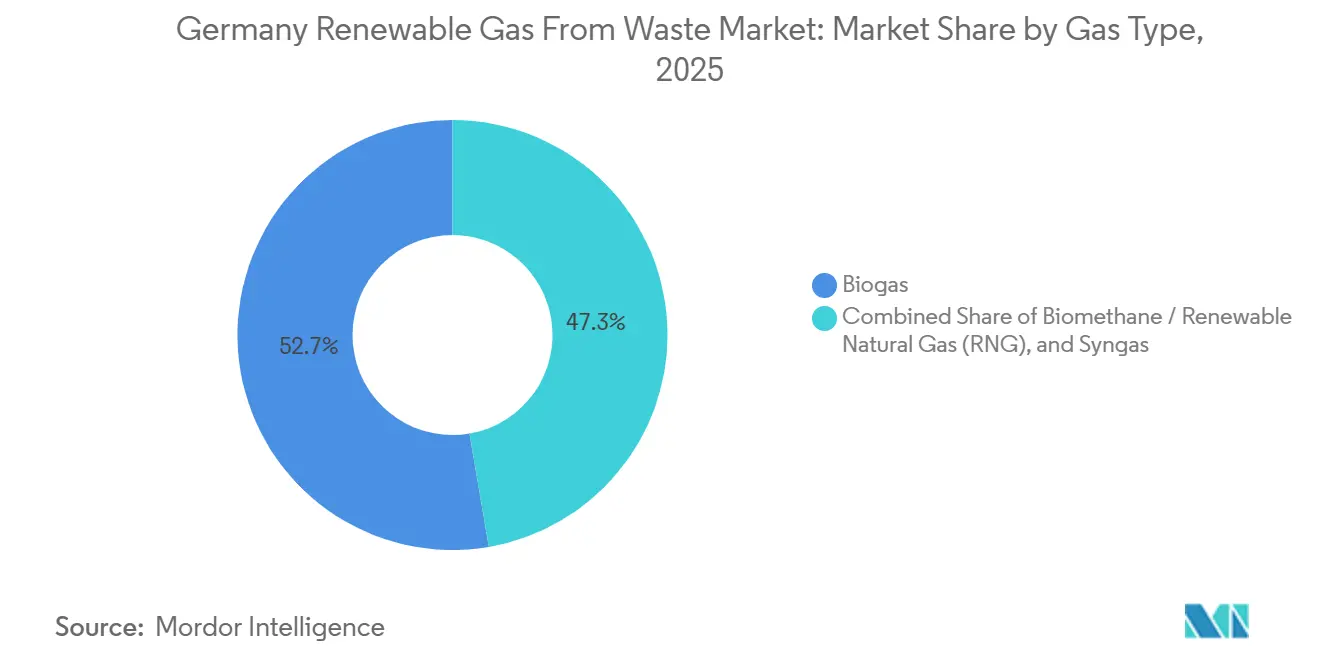

- By gas type, biogas accounted for a 52.7% share in 2025, while biomethane / renewable natural gas is advancing at an 8.3% CAGR through 2031.

- By application, Combined Heat & Power (CHP) captured a 33.5% share in 2025, while transportation fuel is projected to grow at an 8.6% CAGR through 2031.

- By component, digesters and fermentation systems held a 30.1% share in 2025, while gas processing and upgrading units are forecast to grow at a 9.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Renewable Gas From Waste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EEG Tariff Expiry Converting Biogas Fleet Toward Biomethane Grid Injection | +1.9% | National, concentrated in Bavaria, Lower Saxony, Mecklenburg-Vorpommern | Short term (≤ 2 years) |

| GHG Quota System Driving Tripled Biomethane Demand in Transport Fuels | +1.6% | National, with early gains in Hamburg, Munich, and Frankfurt logistics corridors | Medium term (2-4 years) |

| Buildings Energy Act Creating a Large New Biomethane Demand in the Heating Sector | +1.3% | National, dense urban areas including Berlin, Hamburg, Munich, Frankfurt | Long term (≥ 4 years) |

| Rising EU ETS Carbon Prices Narrowing the Biomethane-to-Fossil-Gas Cost Gap | +0.8% | National, buildings, and transport sectors with spillover to small industry | Medium term (2-4 years) |

| EU Methane Regulation and Fertilizer Ordinance Pushing Livestock Farms Toward Biogas | +0.6% | North Germany, Lower Saxony, Bavaria | Medium term (2-4 years) |

| REPowerEU Mandate Requiring Germany's Proportional Biomethane Scale-Up Contribution | +0.4% | National, with European Union-level coordination requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EEG Tariff Expiry Converting Biogas Fleet Toward Biomethane Grid Injection

Germany's 20-year EEG support framework backed a large wave of biogas construction between 2000 and 2012, and that same build cycle is now shaping retrofit demand in Germany renewable gas from waste market. Plants commissioned during the earlier expansion phase are losing fixed-tariff support in successive waves between 2025 and 2028, leaving operators with a direct incentive to shift from power-only generation to biomethane production. For many owners, upgrading and grid injection have become the clearest way to keep assets operating because they open access to transport fuel demand, gas market sales, and future heating demand under the Buildings Energy Act. That is why spending on upgrading units, gas-cleaning systems, and connection infrastructure is not simply optional modernization in the Germany renewable gas from waste market, but a response to expiring revenue protection. EnviTec stated that its EnviThan upgrading line was seeing stronger demand from EEG conversion projects, including contracted work linked to Schleswig-Holstein and Brandenburg sites. FNR also continued to support the biomethane conversion pathway through technical and funding guidance aimed at plants leaving the EEG regime.[1]Fachagentur Nachwachsende Rohstoffe, “FNR,” Fachagentur Nachwachsende Rohstoffe, fnr.de

GHG Quota System Driving Tripled Biomethane Demand in Transport Fuels

The GHG quota regime has become one of the strongest demand anchors for the Germany renewable gas from waste market because it gives fuel distributors a direct compliance reason to buy low-carbon gaseous fuels. Germany approved a revised quota pathway that raised the target to 59% by 2040, providing biomethane producers with a clearer policy horizon for transport demand.[2]Bundesministerium Für Umwelt, Naturschutz, Nukleare Sicherheit Und Verbraucherschutz, “Entwurf Eines Zweiten Gesetzes Zur Weiterentwicklung Der Treibhausgasminderungs-Quote,” BMUV, bundesumweltministerium.de Biomethane adds extra value within that system because waste-based gas qualifies under the advanced biofuels framework and therefore earns stronger decarbonization value per tonne of avoided emissions. Demand for biomethane in transport tripled between 2018 and 2023, reaching close to 10TWh, and continued rising by as much as 10% year over year as compliance requirements tightened, according to the European Union (EU). The upcoming removal of double-counting from 2026 should improve the position of verifiable domestic waste-based supply, thereby strengthening price formation for genuine producers in the German renewable gas-from-waste market. The advanced biofuels sub-quota is due to rise from 2% in 2026 to 8% by 2040, keeping transport as a long-term outlet for renewable gas from waste.

Buildings Energy Act Creating a Large New Biomethane Demand in the Heating Sector

The Buildings Energy Act added a second major demand pillar to the Germany renewable gas from waste market by tying future heating compliance to pathways for blending renewable gas or hydrogen. The 2024 amendment requires new heating systems to deliver at least 65% renewable energy, and existing gas systems installed before local heat planning is finalized must meet biomethane or hydrogen shares of 15% from 2029, 30% from 2035, and 60% from 2040. Mass-balanced biomethane supplied through the gas grid counts toward compliance, allowing demand to rise without waiting for physical pipe-level conversion in each building. A Dena assessment projected that biomethane demand from existing buildings could range from 13.4 TWh to 44.6 TWh by 2040, exceeding Germany's 2023 injected biomethane base and thereby materially widening the long-term addressable market. With more than 56% of heating systems still using gas, the compliance pathway created a large installed base that can continue to draw biomethane into the Germany renewable gas from waste market over time. The practical effect is gradual but durable demand growth from 2027 onward as local heat plans are published and building owners choose the least disruptive compliance route.

Rising European Union ETS Carbon Prices Narrowing the Biomethane-to-Fossil-Gas Cost Gap

Carbon pricing is improving the relative economics of Germany renewable gas from waste market, even when biomethane production costs remain sticky. Germany's national CO2 price stood at USD 61 per tonne in 2025, and in 2026 it is operating within an auction corridor of approximately USD 61 to USD 72 per tonne, based on the conversion values in the source material. EU ETS2 is due to begin in 2028, and published modeling points to carbon pricing near USD 91 per tonne or higher once the system is established, with tighter scenarios rising well above that level in the early 2030s. At the same time, biomethane production costs in Europe still span a wide range, from approximately USD 55 to USD 191 per MWh, indicating that the competitive shift is driven more by rising fossil gas cost exposure than by any rapid decline in renewable gas production costs.[3]Howard Rogers and Katja Yafimava, “Biomethane in Europe,” Oxford Institute for Energy Studies, oxfordenergy.org That change matters for buildings, transport fleets, and smaller industrial users because carbon cost pass-through is making certified renewable gas harder to dismiss on total-cost grounds. The result is a steadier economic case for the Germany renewable gas from waste market in segments where buyers are also managing Scope 1 emission targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expiry of GasNZV Grid Access Regulation Creating Long-Term Investment Uncertainty | -0.9% | National, acute for rural East Germany and remote northern Germany | Short term (≤ 2 years) |

| High Capital Expenditure and Aging Biogas Infrastructure Increasing Modernization Challenges | -0.7% | National, with EU-level regulatory spillover | Short term (≤ 2 years) |

| Lack of Gas Grid Access for Remote Biogas Plants Constraining Biomethane Conversion | -0.5% | Rural East Germany, northern Bavaria, and remote Lower Saxony | Medium term (2-4 years) |

| Declining Wholesale Electricity Prices and Ineffective EEG Tendering Reduce Revenue Diversification | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expiry of GasNZV Grid Access Regulation Creating Long-Term Investment Uncertainty

The expiry of GasNZV at the end of 2025 created the clearest near-term policy gap in Germany renewable gas from waste market. The earlier framework gave developers explicit connection rights, cost-sharing rules, and acceptance obligations, which supported financing for upgrading systems and injection projects over long asset lives. Industry groups warned that reverting to the broader EnWG framework without an equally clear successor would weaken investment certainty and increase connection risk for new projects. A transitional clause under Section 118(4) EnWG still protects projects that submit advance payments by December 31, 2026, but it does not fully solve the visibility problem for projects launched after that window. This has compressed the near-term pipeline, as existing projects are being rushed forward while new project origination is slowing until the legal framework becomes clearer. The Germany renewable gas from waste market, therefore, still has demand support. Still, the timing of capacity additions is becoming more uneven because grid access certainty is not keeping pace with demand growth.

High Capital Expenditure and Aging Biogas Infrastructure Increasing Modernization Challenges

The Germany renewable gas from waste market faces significant restraints due to the high capital investment required for upgrading existing biogas facilities into advanced biomethane production plants. A substantial share of Germany’s biogas infrastructure was developed during earlier renewable energy expansion phases and now requires modernization, including gas upgrading systems, digital monitoring technologies, and improved efficiency measures to meet evolving market requirements. However, the high costs of plant retrofitting, equipment replacement, and technological upgrades create financial pressure, particularly for small- and medium-sized operators. Consequently, many existing facilities delay biomethane conversion and capacity expansion, limiting the pace of growth in Germany renewable gas from waste market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Agricultural Base Dominates, Food Waste Leads the Next Growth Phase

Agricultural residues accounted for 29.4% of the feedstock base in the Germany renewable gas from waste market in 2025, making them the largest feedstock base. That lead reflects the country's long-term build-out of farm-scale biogas under EEG support and the strong presence of mixed-farming regions with steady substrate availability. The fertilizer ordinance, last amended in December 2024, keeps the cap on organic nitrogen application from livestock manure at 170kg total N/ha/year, which supports continued use of digestion as a practical waste management route for larger farms. Animal manure is also gaining a clearer role in the German renewable gas from waste industry because the EU methane framework has tightened monitoring requirements for livestock-linked energy operations.

Food waste is projected to grow at a 7.2% CAGR through 2031, making it the fastest-growing feedstock in the German renewable gas-from-waste market. The growth path is supported by the EU requirement for separate biowaste collection, which widened the available pipeline of municipal and commercial organic material from 2024 onward. Food processing residues, retail organics, and urban food waste offer a different growth profile from farm waste because volumes are concentrated and methane yields are often attractive. Industrial organic waste from breweries, dairies, and food plants is increasingly attractive because it offers reliable off-take structures and a predictable composition. Sewage sludge and landfill gas remain established inputs, but tighter sustainability rules under RED III may limit their contribution to the long-run mix. The broader effect is that the Germany renewable gas from waste market is becoming less dependent on any single feedstock, even though agricultural residues remain the current anchor.

By Technology: Upgrading Systems Set to Outpace Core Digestion in Growth Rate

Anaerobic digestion accounted for 46.3% of Germany renewable gas from waste market in 2025, confirming its position as the dominant technology. That leadership comes from the large installed fleet built under the EEG era, where digestion served as the core conversion route for agricultural and mixed organic waste. The installed base still matters because most near-term capacity comes from extending, retrofitting, or optimizing existing assets. At the same time, biogas upgrading systems are forecast to grow at a 7.7% CAGR through 2031, the fastest among the technology categories in the German renewable gas-from-waste market. This faster growth is directly tied to the EEG exit cycle, since plants moving away from power-only generation need to upgrade their equipment to meet grid-quality gas standards.

EnviTec's contract flow for modular EnviThan pressure swing adsorption units in 2025 and 2026 showed that first-time customers are entering the upgrading space as the retrofit wave expands. Landfill gas recovery, gasification, and pyrolysis are still smaller, but they are gaining attention because they widen feedstock flexibility beyond the traditional farm and municipal digestion base. This matters in the German renewable gas from waste industry because industrial waste generators and local authorities are looking for routes that can handle more varied material streams. The revised Industrial Emissions Directive is also likely to support more farm-linked anaerobic digestion investment at larger livestock sites, helping the core technology maintain meaningful scale even as other routes develop. The likely outcome is not a quick replacement of digestion, but a more layered technology mix where upgrading captures growth while digestion holds the installed-volume center of the market.

By Gas Type: Grid-Capable RNG Gains Fastest, Biogas Stays the Volume Anchor

Biogas accounted for 52.7% of Germany renewable gas from waste market in 2025, making it the largest gas type by volume and value. That position reflects the long-standing use of unupgraded biogas in combined heat and power systems located at or near the point of production. Biomethane / renewable natural gas is forecast to grow at an 8.3% CAGR through 2031, making it the fastest-expanding gas type in Germany renewable gas from waste market. The main reason is straightforward: RNG can move through the gas grid and therefore serve transport, heating, and broader balancing uses that raw biogas cannot serve as easily. Germany's extensive gas network remains a major asset because it lowers the need for entirely new end-use distribution systems. The Bundesnetzagentur's ZuBio determination also maintains technical standards for injection quality after GasNZV expired, supporting continued commercial use of grid-delivered biomethane.

Biomethane sits at the center of this shift because it is the upgraded form that satisfies natural gas grid specifications and most policy-linked demand channels. Syngas remains smaller and more specialized, with a better fit for specific industrial combustion applications than for broad gas-grid use. Across Europe, biomethane production rose 34% between 2015 and 2024, reaching 232TWh, with Germany remaining the leading national contributor. The European Commission has already linked the 35 bcm REPowerEU target to coordinated member-state scale-up, which gives Germany an outsized role in the future growth of renewable gas supply. For that reason, the Germany renewable gas from waste market is likely to keep biogas as its volume anchor while directing most new growth capital toward grid-capable RNG and biomethane pathways.

By Application: Transport Fuel Displacement Moves Fastest, CHP Retains Majority

CHP accounted for 33.5% of the Germany renewable gas from waste market in 2025, making it the largest application segment. The installed base of farm and industrial cogeneration units still gives CHP a large operating footprint even as policy incentives shift toward grid injection and fuel use. Transportation fuel is forecast to grow at an 8.6% CAGR through 2031, making it the fastest-growing application in the Germany renewable gas from waste market. The driver is the GHG quota regime and the stronger long-term role given to advanced biofuels in the revised policy framework. Biomethane used as bio-CNG or bio-LNG is already one of the most developed transport outlets because heavy-duty operators face rising pressure to cut fleet emissions without waiting for slower infrastructure transitions. The Germany renewable gas from waste market is therefore seeing transport pull harder on upgraded gas volumes even while CHP remains the main outlet for legacy assets.

Grid injection is also gaining pace because it provides the main commercial route for plants exiting EEG support and for new projects aimed at heating and mobility demand. Residential and commercial heating remains smaller in current volume terms, but the GEG is steadily raising its strategic importance as a destination for certified gas delivered through the network. Industrial heating is also becoming increasingly relevant as energy-intensive users prepare for greater carbon cost exposure ahead of the EU ETS2. The USDA's 2026 assessment of German biofuel mandates noted that RED III implementation materially strengthens the sub-quota structure supporting transport-side demand. The practical result is a more balanced application mix in which CHP remains large, but transport, grid injection, and heating claim a rising share of new demand in the Germany renewable gas from waste market.

By Component: Gas Processing and Upgrading Units Drive Premium Equipment Demand

Digesters and fermentation systems held a 30.1% share in 2025, making them the largest component group in the Germany renewable gas from waste market. Their position reflects the scale of the existing installed base and the ongoing need for maintenance, refurbishment, and selective expansion. Gas processing and upgrading units are forecast to grow at a 9.1% CAGR through 2031, which makes them the fastest-growing component category. That pattern is closely tied to plant conversion economics because every asset moving from direct electricity generation toward grid injection needs an upgrading stage. In that sense, the component mix in the Germany renewable gas from waste market captures both legacy volumes and new transition spending simultaneously. The legacy side sits in digesters and fermentation systems, while the growth side sits in gas cleaning, upgrading, and injection-ready processing equipment.

Compressors and storage systems are also becoming increasingly important because they enable higher-pressure injection and more flexible gas handling at the network interface. Gas collection systems remain relevant in landfill and municipal waste applications, where collection efficiency continues to shape project economics. Power generation equipment remains necessary for the installed CHP fleet, but its investment growth is likely to lag that of grid-oriented equipment. Monitoring and control systems are gaining ground because methane measurement, reporting, and verification requirements are now tighter under EU Regulation 2024/1787. Remote gas quality sensors and predictive maintenance tools are expanding the role of digital systems from pure compliance to operational efficiency, adding a recurring revenue stream to the Germany renewable gas from waste market.

Geography Analysis

Bavaria and Lower Saxony remain the strongest production centers because they combine dense agricultural activity with long-established biogas infrastructure. Bavaria alone hosts more than 2,500 biogas plants, making it the largest single state contributor to the country's renewable gas supply. Lower Saxony also has a strong position because its high livestock density creates a clear case for manure digestion under the nitrogen cap in the fertilizer ordinance. The European Commission noted that agricultural substrates still dominate Germany's biomethane system, and that agricultural maturity remains well above the wider EU average.

North Rhine-Westphalia, Hamburg, and Berlin stand out more as demand centers than as feedstock hubs in the German renewable gas-from-waste market. Their importance stems from large building stocks with gas heating, which provides a direct link to future biomethane demand under the GEG framework. Hamburg's waste infrastructure creates potential for larger municipal solid waste and organic waste projects. At the same time, Munich remains an important urban demand node because its utility procurement activity supports renewable gas uptake. East German states such as Brandenburg, Saxony, Saxony-Anhalt, and Mecklenburg-Vorpommern offer a different opportunity set centered on larger land parcels, lower land costs, and the ability to develop cluster models around dispersed feedstock. Those same regions also face harder grid access conditions, which means project value often depends on shared upgrading and connection strategies rather than single-site development. Schleswig-Holstein is emerging as a useful model because recent upgrading projects there show how agricultural states can move from local biogas use toward stronger biomethane grid integration.

Germany's state-level differences matter beyond the domestic picture because Germany renewable gas from waste market has a central role in the wider European Union scale-up plan. The European Commission's biomethane agenda under REPowerEU points to EUR 37 billion (USD 43.5 billion) in EU-wide investment needs to reach 35 bcm of annual production by 2030. Because Germany is the bloc's largest producer, a meaningful share of that expansion burden will depend on how quickly the country converts regional feedstock potential into deliverable volumes. The Bundesnetzagentur's ongoing work on injection rules and the federal government's gas law reforms will therefore shape not only domestic supply growth, but also Germany's position in future cross-border renewable gas trade.

Competitive Landscape

The Germany renewable gas from waste market is moderately fragmented, with competition spanning technology suppliers, plant builders, operators, traders, utilities, and municipal waste actors. Companies are not all competing for the same margin pool, since one group focuses on equipment and engineering, another on operating assets and marketing gas, and a third on integrated utility or waste-management platforms. This layered structure limits the chance of a single company dominating the full value chain in the Germany renewable gas from waste market. Technology providers compete primarily on efficiency, modularity, operating reliability, and after-sales service, as these factors directly shape the returns from EEG-exit conversion projects. Operators and traders compete more on feedstock contracts, access to injection points, certification quality, and their ability to monetize transport and heating demand.

Recent company disclosures show how exposed commercial outcomes still are to policy execution. EnviTec reported FY 2025 output of EUR 376.4 million (USD 442.8 million) and linked future growth prospects to rising demand for upgrading projects, even though near-term earnings remained under pressure. Verbio produced a record 1,040GWh of biomethane in the first 9 months of FY 2025/26 and raised its EBITDA guidance to EUR 100 million to EUR 140 million (USD 117.6 million to USD 164.7 million), demonstrating that large-scale domestic biomethane operations can still perform strongly when volumes and policy conditions align. EnviTec's commissioning of 2 new EnviThan upgrading plants for Loick Bioenergie in Schleswig-Holstein and Brandenburg was a clear example of companies positioning around the EEG retrofit cycle. Verbio's public support for RED III ratification was another example, because it signaled confidence that tighter certification rules will favor domestic producers with auditable waste-based supply chains.

Vertical integration is emerging as the clearest strategic pattern in the Germany renewable gas from waste market. Companies are trying to connect feedstock sourcing, plant operation, upgrading, injection, certification, and final fuel or heating sales into a more controlled chain. That approach helps protect margins in a market where quota prices, grid rules, and certification quality all influence realized value. Growth opportunities remain strongest in urban food waste projects, digital monitoring systems tied to methane compliance, and shared cluster models for remote plants that cannot justify dedicated upgrading on a stand-alone basis. Certification through ISCC and RedCert remains a practical barrier to entry, as customers in transport and heating require a traceable supply and documented sustainability performance. The combined effect is a competitive field where scale matters, but execution across regulation, feedstock, and infrastructure still matters more than size alone in the German renewable gas-from-waste market.

Germany Renewable Gas From Waste Industry Leaders

EnviTec Biogas AG

Verbio SE

bmp greengas GmbH

Nordfuel GmbH

BioEnergie Tauberfranken GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The German Bundestag ratified the national implementation of the revised Renewable Energy Directive (RED III), correcting systemic GHG quota market distortions by abolishing double-counting for certain advanced biofuel imports and introducing mandatory witness audits in countries of origin. Verbio SE publicly highlighted this as restoring fair market conditions for domestically produced biomethane from verified waste feedstocks, which had been undercut by fraudulently certified foreign biofuels since 2022.

- March 2026: Verbio SE raised its EBITDA forecast for financial year 2025/26 to EUR 100 million to EUR 140 million (USD 117.6 million to USD 164.7 million), driven by record biomethane production of 1,040 GWh in the first 9 months of FY 2025/26, up from 865 GWh in the same prior-year period, reflecting persistently strong demand from the GHG quota transport market and increasingly favorable regulatory conditions.

- February 2026: Germany's Federal Network Agency confirmed an increased price cap ceiling for biomethane EEG auction rounds in 2026, reflecting stronger policy recognition of biomethane's grid-injection economics amid rising grid demand from GEG compliance.

Germany Renewable Gas From Waste Market Report Scope

The Germany Renewable Gas From Waste Market is Segmented by Feedstock (Municipal Solid Waste, Food Waste, and More), by Technology (Anaerobic Digestion, Gasification, Pyrolysis, and More), by Gas Type (Biogas, Syngas, and More), by Application (Electricity Generation, Grid Injection, and More), and by Component (Gas Collection, Digesters & Fermentation, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Municipal Solid Waste (MSW) |

| Agricultural Residues |

| Animal Manure |

| Industrial Organic Waste |

| Sewage Sludge |

| Food Waste |

| Others |

| Anaerobic Digestion |

| Landfill Gas Recovery |

| Gasification |

| Pyrolysis |

| Biogas Upgrading Systems |

| Others |

| Biogas |

| Biomethane / Renewable Natural Gas (RNG) |

| Syngas |

| Electricity Generation |

| Combined Heat & Power (CHP) |

| Grid Injection |

| Transportation Fuel |

| Industrial Heating |

| Residential & Commercial Heating |

| Others |

| Gas Collection Systems |

| Digesters & Fermentation Systems |

| Gas Processing & Upgrading Units |

| Compressors & Storage Systems |

| Power Generation Equipment |

| Monitoring & Control Systems |

| Others |

| By Feedstock | Municipal Solid Waste (MSW) |

| Agricultural Residues | |

| Animal Manure | |

| Industrial Organic Waste | |

| Sewage Sludge | |

| Food Waste | |

| Others | |

| By Technology | Anaerobic Digestion |

| Landfill Gas Recovery | |

| Gasification | |

| Pyrolysis | |

| Biogas Upgrading Systems | |

| Others | |

| By Gas Type | Biogas |

| Biomethane / Renewable Natural Gas (RNG) | |

| Syngas | |

| By Application | Electricity Generation |

| Combined Heat & Power (CHP) | |

| Grid Injection | |

| Transportation Fuel | |

| Industrial Heating | |

| Residential & Commercial Heating | |

| Others | |

| By Component | Gas Collection Systems |

| Digesters & Fermentation Systems | |

| Gas Processing & Upgrading Units | |

| Compressors & Storage Systems | |

| Power Generation Equipment | |

| Monitoring & Control Systems | |

| Others |

Key Questions Answered in the Report

What is the 2026 value of Germany renewable gas from waste market?

The sector is estimated at USD 1.84 billion in 2026 and is forecast to reach USD 2.58 billion by 2031, with a 6.99% CAGR.

Which feedstock currently leads renewable gas production from waste in Germany?

Agricultural residues lead with a 29.4% share in 2025, as Germany has a large, mature farm-based biogas base.

Which technology is growing fastest in Germany renewable gas from waste market?

Biogas upgrading systems are projected to grow at a 7.7% CAGR through 2031 as more EEG-exit plants move toward grid injection.

Why is demand for transport fuel biomethane rising so quickly in Germany?

The GHG quota system is pushing fuel suppliers toward lower-carbon fuels, and transportation fuel is projected to grow at an 8.6% CAGR through 2031.

How is the Buildings Energy Act affecting renewable gas demand in Germany?

The law sets rising thresholds for blending renewable gas or hydrogen into gas heating systems, creating a long-term pull for certified biomethane in buildings.

What is the biggest near-term risk for project developers in Germany?

Grid access uncertainty after the GasNZV expiry is the clearest short-term risk, as new projects may face less predictable connection costs and timelines.

Page last updated on: