Europe Renewable Gas From Waste Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

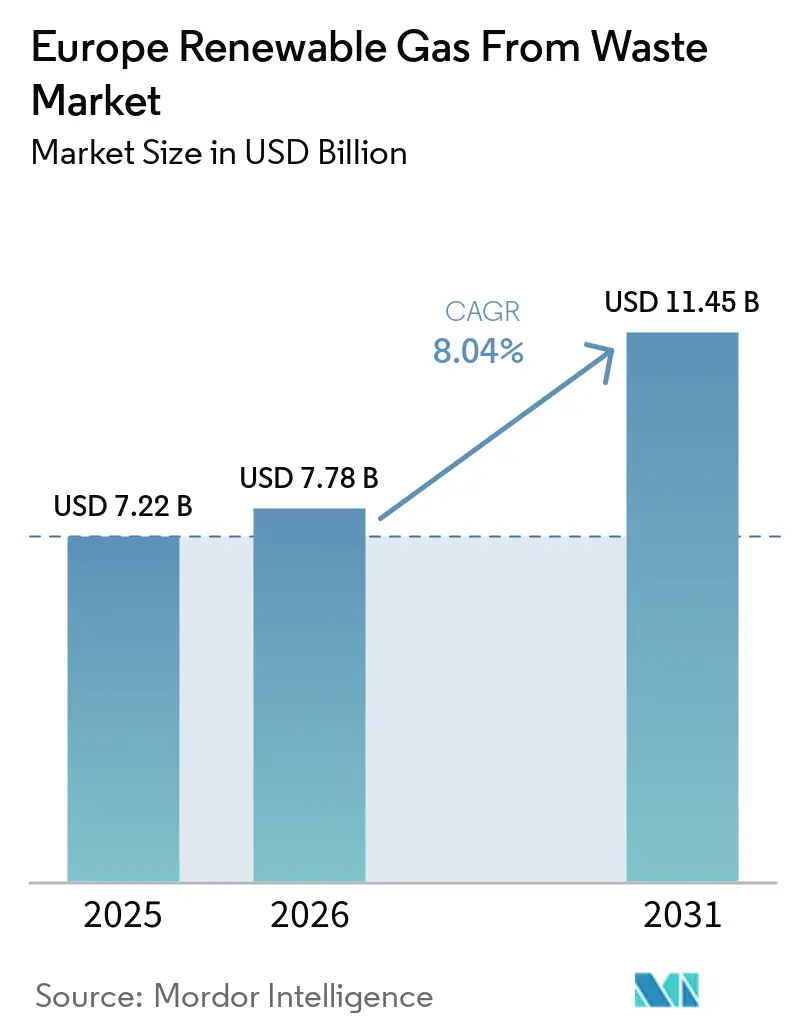

| Base Year Market Size (2025) | USD 7.22 Billion |

| Market Size (2026) | USD 7.78 Billion |

| Market Size (2031) | USD 11.45 Billion |

| Growth Rate (2026 - 2031) | 8.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Renewable Gas From Waste Market Analysis by Mordor Intelligence

The Europe Renewable Gas From Waste Market size was valued at USD 7.22 billion in 2025 and is estimated to grow from USD 7.78 billion in 2026 to reach USD 11.45 billion by 2031, at a CAGR of 8.04% during the forecast period (2026-2031).

The Europe renewable gas from waste market is moving faster than it did in the last cycle, as the earlier 7.8% historical growth rate has given way to stronger momentum from binding energy security targets, tighter carbon policy, and broader utility and infrastructure investment. The European Commission's REPowerEU plan has given the Europe renewable gas from waste market a clear long-term demand signal through its 35 bcm biomethane target for 2030, which has improved project visibility for developers, gas grid operators, and financiers across the value chain. The January 2024 requirement for separate biowaste collection has also widened the available feedstock pool, which makes supply less reliant on agricultural surpluses and more stable during periods of crop price volatility. Competition in the Europe renewable gas from waste market is broadening as waste management groups, specialist developers, infrastructure funds, and transmission-linked operators pursue the same asset base under different national incentive regimes. Growth is still being held back by biomethane production costs that remain above wholesale gas prices and by permitting timelines that can stretch from six months to more than four years, yet low gas storage levels have strengthened the strategic case for domestic renewable gas capacity across Europe.

Key Report Takeaways

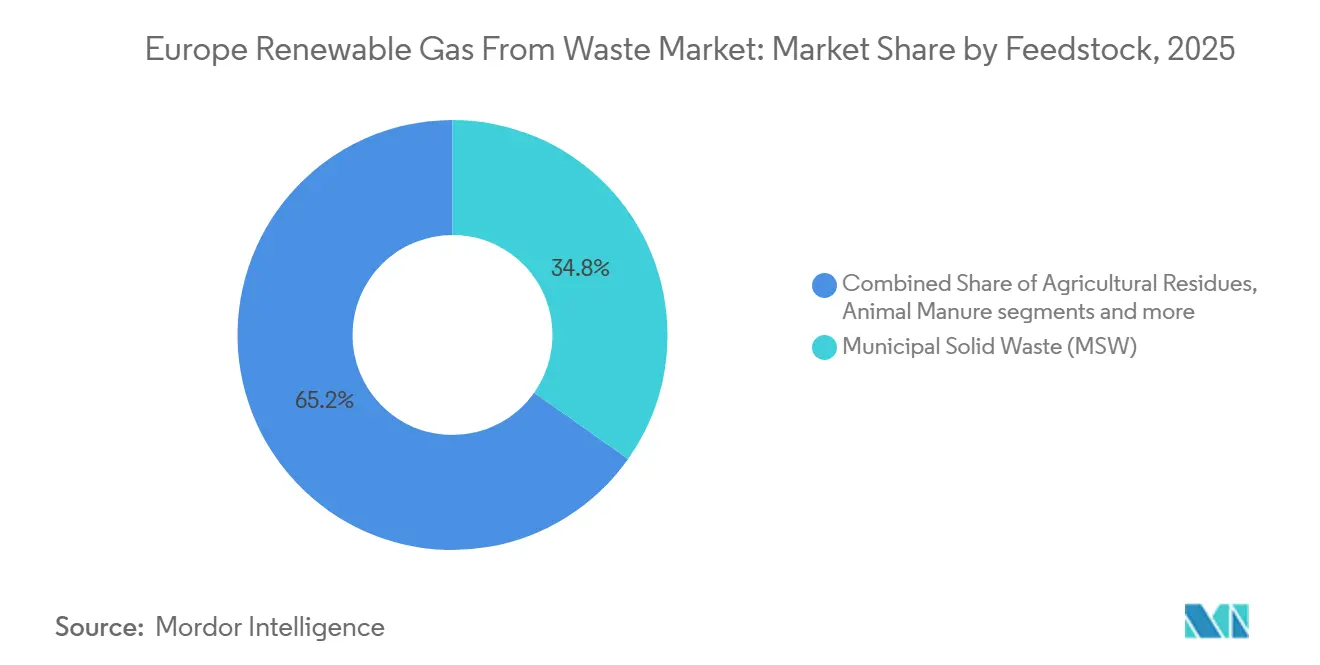

- By feedstock, municipal solid waste accounted for 34.8% of the Europe renewable gas from waste market share in 2025, while food waste is forecast to expand at a 9.9% CAGR through 2031.

- By technology, anaerobic digestion held a 45.1% share in 2025, while biogas upgrading systems are projected to grow at a 9.3% CAGR through 2031.

- By application, electricity generation accounted for 35.2% in 2025, while transportation fuel is forecast to advance at a 10.3% CAGR through 2031.

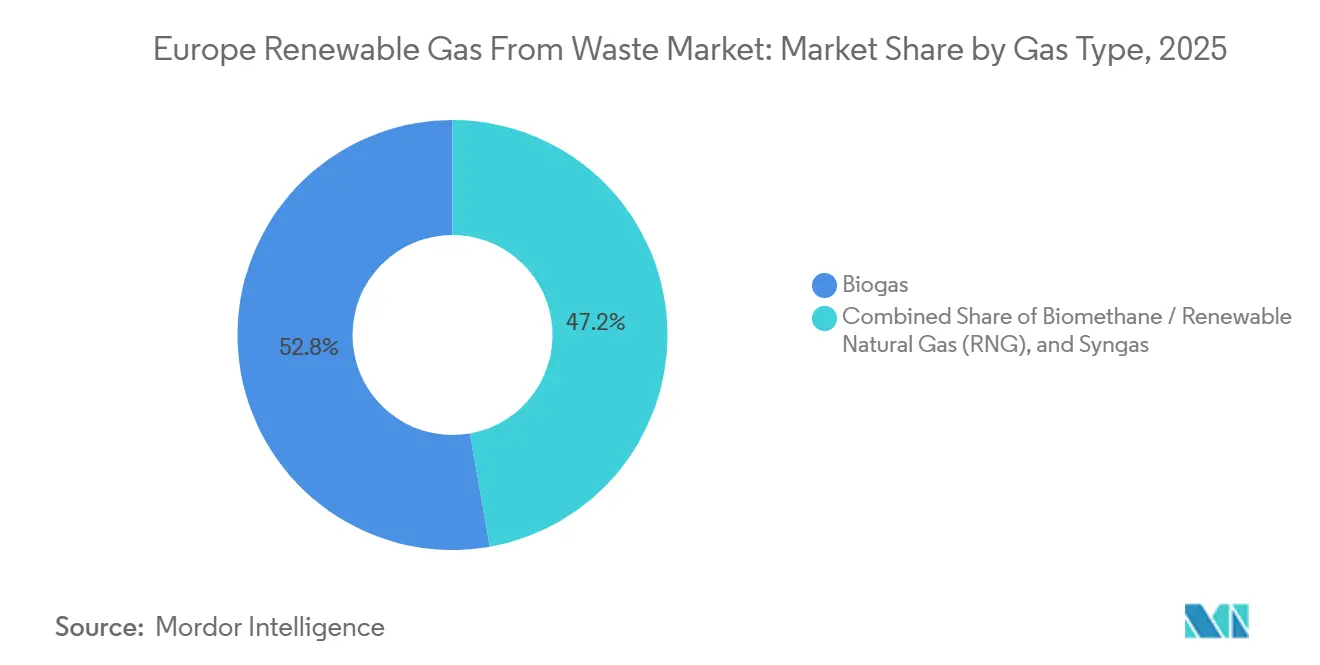

- By gas type, biogas held a 52.8% share in 2025, while biomethane / renewable natural gas is projected to expand at a 10.8% CAGR through 2031.

- By component, gas processing and upgrading units accounted for 31.6% of the Europe renewable gas from waste market in 2025, while monitoring and control systems are projected to grow at a 9.3% CAGR through 2031.

- By geography, Germany held a 24.0% of the Europe renewable gas from waste market size in 2025, while Denmark is projected to grow at an 11.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Renewable Gas From Waste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| REPowerEU Binding Biomethane Target Driving Waste-to-Gas Investment | +2.5% | EU-27 and the United Kingdom, with the strongest effect in the largest biomethane build-out markets | Long term (≥ 4 years) |

| European Union Biowaste Landfill Ban Expanding Anaerobic Digestion Feedstock Supply | +2.2% | Germany, France, Italy, Poland, Spain, and other EU member states | Medium term (2-4 years) |

| Declining Dispatchable Power Capacity Boosting Demand for Storable Renewable Gas | +1.8% | Germany, the United Kingdom, the Netherlands, and wider Western Europe | Short term (≤ 2 years) |

| German EEG Tariff Expiry Triggering Mass Biogas-to-Biomethane Conversion | +1.4% | Germany, with secondary effects across nearby registry-linked markets | Short term (≤ 2 years) |

| RED III Double-Counting Provisions Enhancing Commercial Viability in Transport | +1.1% | Netherlands, Germany, France, and other transport mandates markets | Medium term (2-4 years) |

| Rising ETS Carbon Prices Accelerating Industrial Fossil Gas Substitution | +0.8% | Germany, France, the Netherlands, Belgium, and other countries ETS-heavy industrial bases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

REPowerEU Binding Biomethane Target Driving Waste-to-Gas Investment

The REPowerEU plan set a target of 35 bcm of biomethane production by 2030, sharply raising policy certainty for renewable gas investment in Europe[1]European Commission, “REPowerEU Plan,” EUR-Lex, eur-lex.europa.eu. That target is materially higher than earlier policy expectations, so it has given the Europe renewable gas from waste market a larger and more durable demand horizon. The related investment need was estimated at EUR 37 billion (USD 43.5 billion), indicating that public policy expects infrastructure-scale deployment rather than a gradual, pilot-led expansion. The European Biogas Association reported in April 2026 that animal manure, agricultural residues, and industrial wastewater together account for 81% of Europe’s technically achievable biomethane potential, underscoring the importance of waste-linked feedstock access to project economics.[2]European Biogas Association, “Policy Gaps Hold Back Biomethane Scale-Up Despite Available Potential and Geopolitical Momentum,” European Biogas Association, europeanbiogas.eu This changes how investors screen opportunities, because developers with reliable access to waste streams can move faster than players still dependent on open-market biomass procurement. It also means national schemes that translate the 2030 target into funding and permitting support are likely to pull forward project decisions in the Europe renewable gas from waste market over the next several years.

European Union Biowaste Landfill Ban Expanding Anaerobic Digestion Feedstock Supply

The European Union Waste Framework Directive required separate biowaste collection across member states from January 1, 2024, which expanded the formal supply base for anaerobic digestion projects. This matters for the Europe renewable gas from waste market because feedstock access becomes less exposed to seasonal swings in crop output and agricultural commodity pricing. The Biomethane Action Plan also linked biowaste diversion to dual benefits: each tonne diverted from landfill can reduce methane and CO2-equivalent emissions while producing usable gas. The European Biogas Association identified Germany, France, Italy, Poland, and the United Kingdom as the main concentration of mobilizable biomethane potential, so collection quality in those countries will have an outsized effect on future supply. The landfill framework adds further pressure because the EU still expects landfill dependence to decline toward the 2030 target of no more than 10% of municipal waste. As compliance tightens, the Europe renewable gas from waste market stands to benefit from a steadier, more regulated flow of segregated organic waste.

Declining Dispatchable Power Capacity Boosting Demand for Storable Renewable Gas

The imbalance between renewable gas supply and demand supports the Europe renewable gas from waste market because renewable gas can be stored, moved through existing networks, and used when needed rather than only when it is generated. ENTSOG’s Winter Supply Outlook for 2025-26 showed that gas storage could fall to very low levels in a cold weather scenario, with demand response needs equivalent to 92 TWh even under reference LNG supply conditions. ACER also confirmed that EU gas storage ended the 2025-26 winter near a three-year low, reinforcing the value of domestic renewable gas beyond simple fossil-substitution economics.[3]Agency for the Cooperation of Energy Regulators, “Key Developments in European Gas Wholesale Markets, Winter 2025-2026,” ACER, acer.europa.eu Columbia University’s Center on Global Energy Policy further noted that Europe entered the 2026 injection season with only 31 bcm in storage, its lowest starting point since 2018. This reinforces the strategic value of dispatchable renewable gas assets, which short-duration batteries cannot effectively substitute on a seasonal scale.

German EEG Tariff Expiry Triggering Mass Biogas-to-Biomethane Conversion

Germany remains the single most important installed base in the Europe renewable gas from waste market because it has the region’s largest fleet of aging biogas plants. Many of these assets have reached the end of their original 20-year support periods since 2024, forcing operators to evaluate new revenue streams. BMWK announced the revised EEG biomass package in December 2024, and the new framework was published in February 2025, with a clearer path toward more flexible, biomethane-linked operation. The Bundesnetzagentur then set a maximum auction price of EUR cents per kWh (approximately USD 0.247/kWh) for biomethane plants in the 2025 rounds, providing investors with a clear reference point for conversion economics. Germany’s advantage is both practical and financial, as many sites already have feedstock-handling systems, operating digesters, and grid connections in place. That makes retrofitted upgrading capacity one of the lowest-capital pathways for near-term expansion in the Europe renewable gas from waste market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Production Cost Disadvantage Versus Wholesale Natural Gas | -1.3% | France, Spain, the Netherlands, and other competitive gas price markets | Long term (≥ 4 years) |

| Fragmented National Permitting Delaying Project Commissioning | -0.9% | Broadly across the EU, with acute bottlenecks in Ireland, Poland, Spain, and Italy | Medium term (2-4 years) |

| Incompatible Guarantee of Origin Registries Limiting Cross-Border Trade | -0.6% | DACH, Nordics, the United Kingdom, and parts of Central and Southern Europe | Medium term (2-4 years) |

| Organic Waste Feedstock Competition Tightening Biomass Availability | -0.4% | United Kingdom, Germany, and the Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Production Cost Disadvantage Relative to Wholesale Natural Gas

Biomethane production from anaerobic digestion in Europe still costs EUR 50 to EUR 175 per MWh (USD 58.8 to USD 205.9 per MWh), which remains above wholesale natural gas pricing for much of the forecast period. The Oxford Institute for Energy Studies stated in January 2026 that there is still limited evidence of meaningful reductions in production costs compared with the 2010s, which keeps subsidy dependence in place for many projects. This constraint is harder to solve than it was in solar or wind, because feedstock transport, biological conversion limits, and grid injection costs do not decline as quickly as manufactured hardware. Support instruments such as Guarantees of Origin and feed-in premiums help narrow the gap, but their value still varies widely across countries, creating uneven commercial conditions. Lower gas prices would further complicate the case for unsubsidized projects, especially in countries where support has become more selective. As a result, the Europe renewable gas from waste market is still not on a clear path to large-scale subsidy-free expansion by 2031.

Fragmented National Permitting Frameworks Delaying Project Commissioning

Permitting timelines for biomethane projects still range from six months to more than four years, depending on the country, feedstock category, and environmental review path. In February 2026, the Informal Coalition on Permitting called for enforceable time limits, digital tracking tools, and a single point of contact, citing cases that had dragged on for 7 years. Grid connection rules add a second layer of complexity because national technical and commercial requirements still differ materially under the evolving gas framework. The Net-Zero Industry Act requires member states to establish single-point contact authorities and provide indicative timelines, but implementation remains uneven across the bloc. This weakens the pace at which the Europe renewable gas from waste market can convert policy support into operating capacity. It also favors experienced developers who can manage local permitting risk across multiple jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Waste Hierarchy is Reshaping Feedstock Economics

Municipal solid waste accounted for 34.8% of the Europe renewable gas from waste market in 2025, making it the largest feedstock group in the region. Its lead reflects the maturity of collection, sorting, and processing systems across Germany, France, the Netherlands, and the United Kingdom. These established municipal waste flows give project developers a more stable and visible supply base than several narrower agricultural or industrial streams. Agricultural residues and animal manure remained the next major feedstock block, and manure continues to benefit from a regulatory edge because RED III gives it double-counting status in transport fuel applications. Industrial organic waste and sewage sludge remained important middle-tier categories, especially where wastewater infrastructure already lowers the capital burden for digestion and gas recovery projects.

Food waste is projected to record the fastest growth at 9.9% CAGR from 2026 to 2031 in the Europe renewable gas from waste market. This trajectory is closely tied to the EU requirement for separate biowaste collection, which has steadily increased the volume of segregated food waste available for valorization. That policy support also improves long-term visibility into feedstocks for developers building urban and municipal waste-based gas assets. Landfill waste remains relevant, particularly at legacy sites, where methane capture serves both environmental compliance and energy recovery goals under tighter landfill and emissions rules. The feedstock mix is therefore moving toward waste-stream operators with control over regulated organic flows, which strengthens their position across the Europe renewable gas from waste market.

By Technology: Upgrading Systems are Outpacing Established Conversion Pathways

Anaerobic digestion held 45.1% of the Europe renewable gas from waste market share in 2025, keeping it as the leading technology platform across the region. Its position rests on a long operating history, an established regulatory framework, and broad compatibility with municipal, agricultural, and industrial organic feedstocks. The technology also benefits from digestate output, which can support plant economics where biofertilizer demand is present. Landfill gas recovery remained the second key route, supported by the commercial viability of converting existing landfill assets into renewable gas production sites without requiring greenfield anaerobic digestion development, a model demonstrated by containerized upgrading units deployed directly at landfill sites across several European markets. Gasification and pyrolysis remained earlier in the commercial cycle, but they continue to attract interest where dry residual waste streams are less suitable for digestion.

Biogas upgrading systems are projected to expand at 9.3% CAGR through 2031, making them the fastest-growing technology segment in the Europe renewable gas from waste market. The main driver is the conversion of older biogas plants into biomethane-capable assets, especially in Germany, as post-subsidy facilities seek new revenue pathways. This conversion route is more capital-efficient than greenfield development because the digestion process is already in place, and many sites already have grid access. It also fits the broader shift from electricity-only generation toward higher-value gas injection and transport fuel use. Across Europe, in the renewable gas from waste industry, that trend is improving demand for membrane systems, scrubbing units, compression packages, and retrofit engineering services.

By Gas Type: Biomethane / RNG is Emerging as the Highest-Value Molecule

Biogas retained 52.8% of the market value in 2025, making it the largest gas type in the Europe renewable gas from waste market. This reflects its role as the primary intermediate product generated by most waste-to-gas facilities before upgrading or downstream conversion. Even so, raw biogas faces growing pressure as policy and commercial systems increasingly favor pipeline-grade and transport-grade gas. Biomethane has continued to gain ground because it is easier to certify, inject into the grid, and trade across structured offtake channels. Syngas remains a smaller category in Europe, though demonstration projects in gasification and pyrolysis continue to progress in selected northern markets.

Biomethane / renewable natural gas is forecast to grow at a 10.8% CAGR from 2026 to 2031, making it the fastest-expanding gas type in the Europe renewable gas from waste market. RED III transport incentives, rising demand from hard-to-electrify transport segments, and compatibility with existing compressed and liquefied gas infrastructure are supporting its growth. That compatibility reduces distribution investment needs and enables faster commercial scaling than for several newer low-carbon fuels. It also helps explain why transport and logistics users are increasingly willing to contract certified renewable gas volumes under multi-year agreements. In the Europe renewable gas from waste market, this is shifting value toward upgraded, certified molecules rather than toward intermediate gas production alone.

By Application: Grid Injection is Displacing Traditional On-Site Power Use.

Electricity generation remained the largest application segment in 2025, accounting for 35.2% of the Europe renewable gas from waste market. Its lead reflects the legacy of earlier support systems that favored on-site power generation and electricity feed-in over gas injection. Combined heat and power remained an important option because it can extract both thermal and electrical outputs from the same feedstock stream, thereby improving overall energy efficiency. Grid injection is becoming more important as gas network rules, blending frameworks, and certificate systems create stronger demand for pipeline-quality renewable gas. That shift reduces exposure to volatile spot electricity prices and makes gas sales more attractive to a growing share of operators.

Transportation fuel is projected to grow at 10.3% CAGR through 2031, making it the fastest-growing application in the Europe renewable gas from waste market. Heavy road transport and maritime fuel demand are the main drivers, as these segments require lower-carbon fuels compatible with existing operating systems. The economic case is also improving as carbon costs continue to pressure conventional fossil fuel use in transport and industrial value chains. Industrial heating is also becoming a more relevant outlet, particularly in sectors such as ceramics, glass, and food processing, where electrification remains difficult. Residential and commercial heating still form part of the demand base, though most of that use comes through grid blending rather than direct dedicated supply.

By Component: Upgrading and Digital Control Systems are Leading the Capital Cycle

Gas processing and upgrading units accounted for 31.6% of the Europe renewable gas from waste market share in 2025, making them the largest component category in the region. This reflects the strong need for scrubbing, separation, and purification systems before renewable gas can be injected into the grid or sold into transport fuel channels. The segment is also benefiting from the conversion of older biogas plants into biomethane-ready assets, especially in Germany and other mature markets where operators are shifting away from electricity-only use. Digesters and fermentation systems remain important in greenfield project development, particularly in southern and eastern Europe, where anaerobic digestion penetration is lower. Gas collection systems, compressors, and storage equipment also retain a steady role because they support feedstock handling, gas flow management, and injection readiness across the Europe renewable gas from waste market.

Monitoring and control systems are projected to grow at 9.3% CAGR between 2026 and 2031, making them the fastest-growing component segment in Europe renewable gas from waste market. This growth is driven by rising requirements for traceability, metering, certification, and gas quality verification rather than by automation alone. As regulatory compliance becomes more data-intensive, operators are placing greater value on systems that can provide real-time monitoring of feedstock intake, upgrading performance, and grid injection quality. Power generation equipment is seeing a relative capital shift because some operators now prefer to redirect gas volumes toward grid injection and transportation fuel applications with stronger revenue visibility. Across Europe, in the renewable gas from waste industry, suppliers that combine upgrading hardware with digital monitoring capabilities are improving their competitive position.

Geography Analysis

Germany held 24.0% of the Europe renewable gas from waste market in 2025, making it the largest national market in the region. Its lead rests on the continent’s densest installed biogas fleet and on a policy framework that is now pushing more assets toward biomethane injection rather than pure electricity generation. The February 2025 EEG biomass package and related auction structure sharpened that shift by improving visibility for plants moving to more flexible, gas-linked operating models. France and Italy form the next major tier, with both markets supported by waste availability, established gas networks, and national incentive systems that still favor the build-out of biomethane. The Europe renewable gas from waste market in these three countries remains the largest near-term source of project volume.

Denmark is the fastest-growing national segment, with the Europe renewable gas from waste market size in that country projected to grow at 11.8% CAGR through 2031. Its momentum comes from strong manure-based digestion economics, mature certification practices, and a policy structure that supports broader gas substitution through the national network. The Netherlands sits in the same northern European leadership cluster because it combines high infrastructure quality, strong industrial gas demand, and active development of large biomethane projects. The United Kingdom remains important, though it now operates outside the EU framework and follows its own support and certificate arrangements. This creates a distinct regulatory path, but it does not diminish the country’s relevance, as feedstock availability and network-ready gas demand remain strong.

Spain and the wider Iberian market remain at an earlier stage of development, providing substantial long-term growth potential. Still, they offer a longer runway because AD penetration starts from a lower base, and organic waste volumes are large. Poland and the Czech-adjacent Central European cluster are also gathering pace, with first-mover strategies centered on high feedstock availability and lower competitive intensity. Slovakia’s Horovce plant, launched in 2025, demonstrated that larger biomethane facilities can now come online in smaller regional markets using biodegradable food-industry waste as feedstock. The European Biogas Association stated in April 2026 that 60% of Europe’s technically achievable biomethane potential is concentrated in Germany, France, Italy, Poland, and the United Kingdom, which means geographic diversification remains a real issue for investors in the Europe renewable gas from waste market.

Competitive Landscape

The Europe renewable gas from waste market exhibits moderate concentration, characterized by a mix of large integrated operators and regional specialists. Waste management groups such as Veolia and SUEZ benefit from direct access to municipal and industrial waste streams, which gives them a durable advantage in feedstock security. Specialist developers still compete effectively because they focus on high-value niches such as transport fuel, landfill upgrading, and digitally managed certification pathways. Waga Energy is a clear example, as its WAGABOX model continues to expand the commercial use of legacy landfill gas sites through a specialized operating approach. The Europe renewable gas from waste market, therefore, rewards both feedstock control and technology specialization rather than scale alone.

Verbio is another useful benchmark because its biomethane production reached 1,040 GWh in the nine months to March 2026, up 20% from the prior-year period, demonstrating how focused operators are on capturing value through gas quality optimization and quota monetization. EnviTec has taken a different route by strengthening downstream fuel access, including the acquisition of LIQVIS, which extends its presence from production into heavy transport distribution. SUEZ’s purchase of a controlling stake in ARA Cursus also shows how larger groups are entering underpenetrated geographies through portfolio deals rather than waiting for slower organic expansion. These moves suggest that competition is spreading across the full chain, from waste sourcing and plant conversion to certification, logistics, and downstream offtake. The Europe renewable gas from waste market is also developing a clear divide between operators that can manage compliance and cross-border registry complexity and those that remain limited to local asset ownership.

A notable opening still exists in the mid-sized plant segment, where project sizes are often too small for large infrastructure funds and too operationally diverse for narrow specialists. That gap could favor aggregation models, cooperatives, or platform operators able to bundle multiple subscale assets under common certification and financing structures. Financial investors are also becoming more active, increasing the likelihood of further consolidation through 2026 and 2027. EQT’s June 2025 move into exclusive negotiations for a majority stake in Waga Energy showed that infrastructure capital now treats waste-to-gas as a core asset class rather than an experimental energy transition theme.

Europe Renewable Gas From Waste Industry Leaders

Shell Plc

EnviTec Biogas AG

Verbio SE

Storengy SAS

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Andion CH4 announced the acquisition of an Italian biogas plant for conversion to biomethane, reflecting continued consolidation of legacy agricultural biogas assets into upgraded biomethane production infrastructure across the Po Valley.

- April 2026: The European Biogas Association published its Accelerate EU companion report, confirming Europe's current biogas output at 22 bcm and highlighting that policy momentum remains insufficient to reach 35 bcm by 2030 without accelerated Member State implementation of RED III permitting and support provisions.

- February 2026: The Informal Permitting Coalition, comprising more than 18 European and national industry organizations, published a joint statement calling for enforceable permitting timelines, single-point-of-contact authority models, and the mandatory digitalization of tracking tools across the European Union Member States, citing delays of up to 7 years in complex cases.

Europe Renewable Gas From Waste Market Report Scope

| Municipal Solid Waste (MSW) |

| Agricultural Residues |

| Animal Manure |

| Industrial Organic Waste |

| Sewage Sludge |

| Food Waste |

| Others |

| Anaerobic Digestion |

| Landfill Gas Recovery |

| Gasification |

| Pyrolysis |

| Biogas Upgrading Systems |

| Others |

| Biogas |

| Biomethane / Renewable Natural Gas (RNG) |

| Syngas |

| Electricity Generation |

| Combined Heat & Power (CHP) |

| Grid Injection |

| Transportation Fuel |

| Industrial Heating |

| Residential & Commercial Heating |

| Others |

| Gas Collection Systems |

| Digesters & Fermentation Systems |

| Gas Processing & Upgrading Units |

| Compressors & Storage Systems |

| Power Generation Equipment |

| Monitoring & Control Systems |

| Others |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Benelux (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Feedstock | Municipal Solid Waste (MSW) |

| Agricultural Residues | |

| Animal Manure | |

| Industrial Organic Waste | |

| Sewage Sludge | |

| Food Waste | |

| Others | |

| By Technology | Anaerobic Digestion |

| Landfill Gas Recovery | |

| Gasification | |

| Pyrolysis | |

| Biogas Upgrading Systems | |

| Others | |

| By Gas Type | Biogas |

| Biomethane / Renewable Natural Gas (RNG) | |

| Syngas | |

| By Application | Electricity Generation |

| Combined Heat & Power (CHP) | |

| Grid Injection | |

| Transportation Fuel | |

| Industrial Heating | |

| Residential & Commercial Heating | |

| Others | |

| By Component | Gas Collection Systems |

| Digesters & Fermentation Systems | |

| Gas Processing & Upgrading Units | |

| Compressors & Storage Systems | |

| Power Generation Equipment | |

| Monitoring & Control Systems | |

| Others | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the market size of the Europe renewable gas from waste market in 2026, and how is it expected to grow by 2031?

The Europe renewable gas from waste market stood at USD 7.78 billion in 2026 and is forecast to reach USD 11.5 billion by 2031 at an 8.04% CAGR.

Which feedstock leads to renewable gas from waste generation across Europe?

Municipal solid waste led in 2025 with 34.8% share, helped by mature collection and sorting systems in major Western European markets.

Which technology is expanding the fastest in this space?

Biogas upgrading systems are projected to grow at a 9.3% CAGR through 2031, mainly due to the conversion of existing biogas plants for biomethane injection.

Why is transport becoming a key outlet for renewable gas from waste?

Transportation fuel is the fastest-growing application, with a 10.3% CAGR, supported by RED III incentives and rising pressure to cut emissions in heavy transport.

Which country is the largest market in Europe today?

Germany led with a 24.0% share in 2025 due to its large installed biogas base and policy support for converting to biomethane injection.

What is the main barrier to faster project scale-up?

Production costs remain above wholesale natural gas prices in many markets, and permitting timelines still range from 6 months to more than 4 years.

Page last updated on: