Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

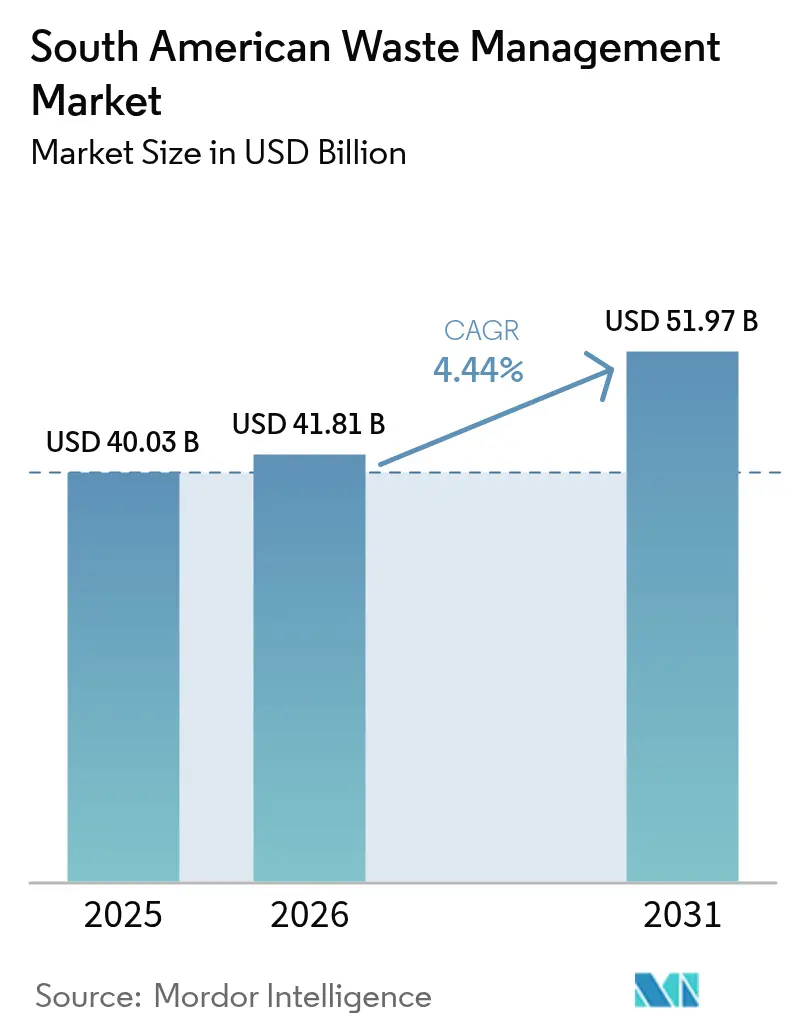

| Base Year Market Size (2025) | USD 40.03 Billion |

| Market Size (2026) | USD 41.81 Billion |

| Market Size (2031) | USD 51.97 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

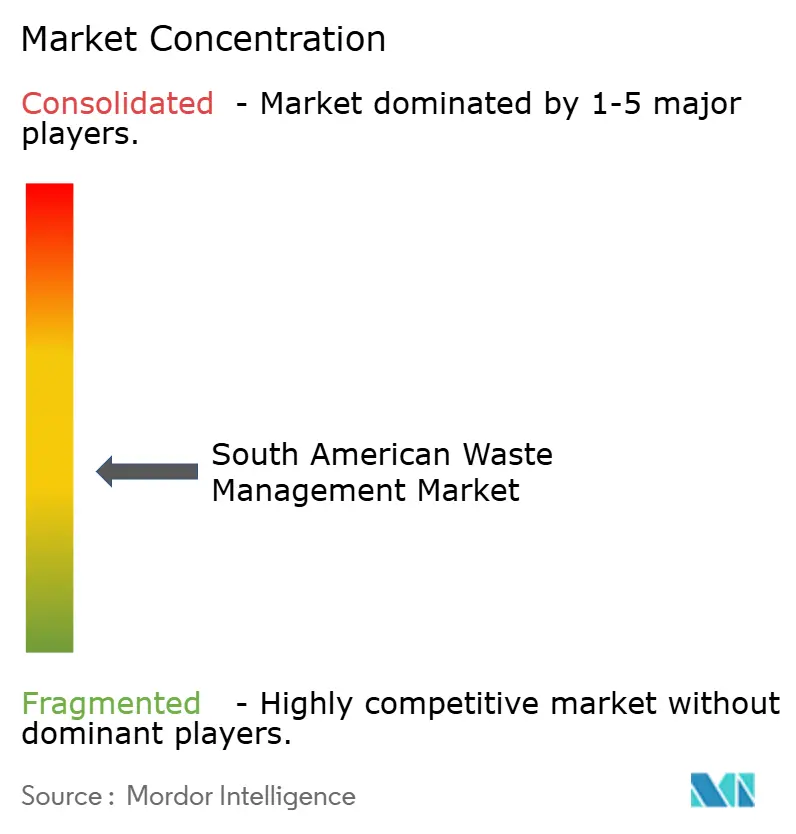

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Waste Management Market Analysis by Mordor Intelligence

The South America Waste Management Market size was valued at USD 40.03 billion in 2025 and estimated to grow from USD 41.81 billion in 2026 to reach USD 51.97 billion by 2031, at a CAGR of 4.44% during the forecast period (2026-2031). Regulatory pivots toward circular-economy models, most clearly the Extended Producer Responsibility (EPR) laws in Brazil, Chile, and Colombia, are steering capital away from legacy landfills and into composting, material-recovery facilities, and waste-to-energy assets. Post-COP30 climate-finance initiatives are enlarging the deal pipeline, with Eco Invest Brasil alone raising USD 13.5 billion for climate-aligned infrastructure. Corporate zero-waste pledges in mining and agribusiness are enlarging demand for industrial-stream recycling, while AI-driven route optimization is lowering collection operating costs by 12-18% and quickening payback periods on new fleets. Persistent barriers remain, including entrenched informal collection networks that still command 40% of Lima’s municipal flows and volatile carbon-credit prices that complicate biomethane and waste-to-energy financing.

Key Report Takeaways

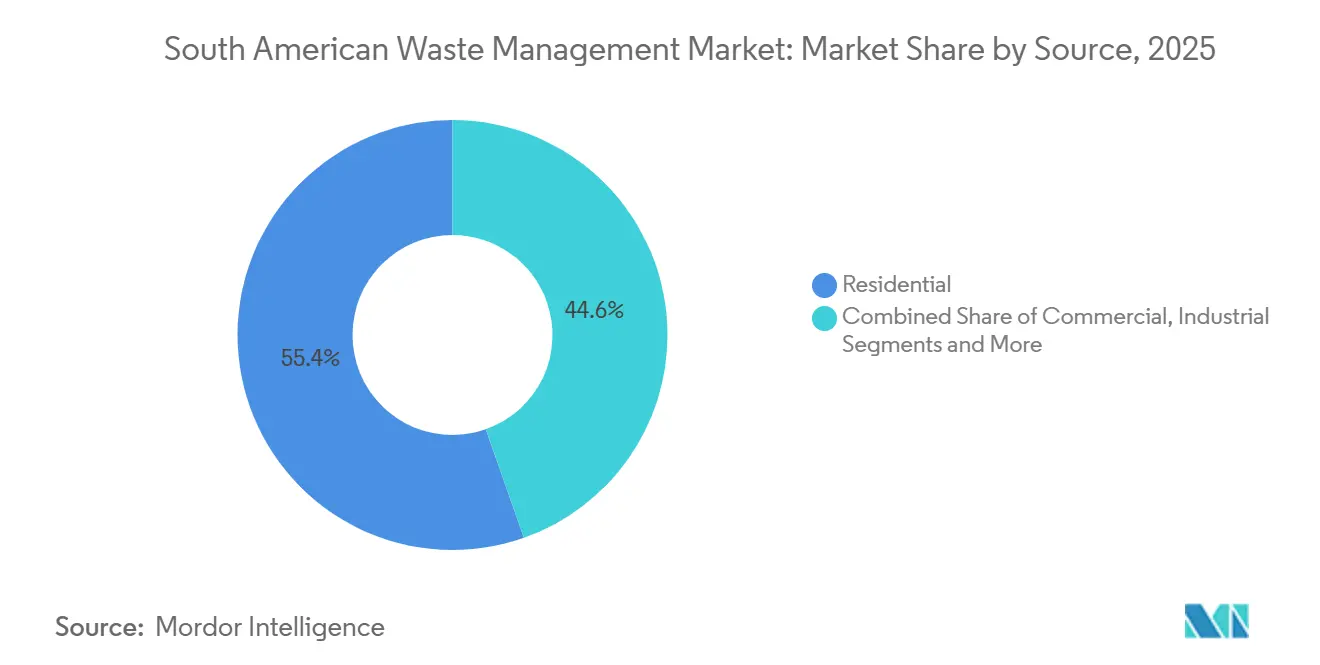

- By source, residential waste led with 55.39% of the South America Waste Management Market share in 2025, while commercial waste is forecast to expand at a 6.19% CAGR through 2031.

- By service type, disposal & treatment captured 48.49% share of the South America Waste Management Market size in 2025, whereas recycling & resource recovery is projected to advance at a 6.29% CAGR to 2031.

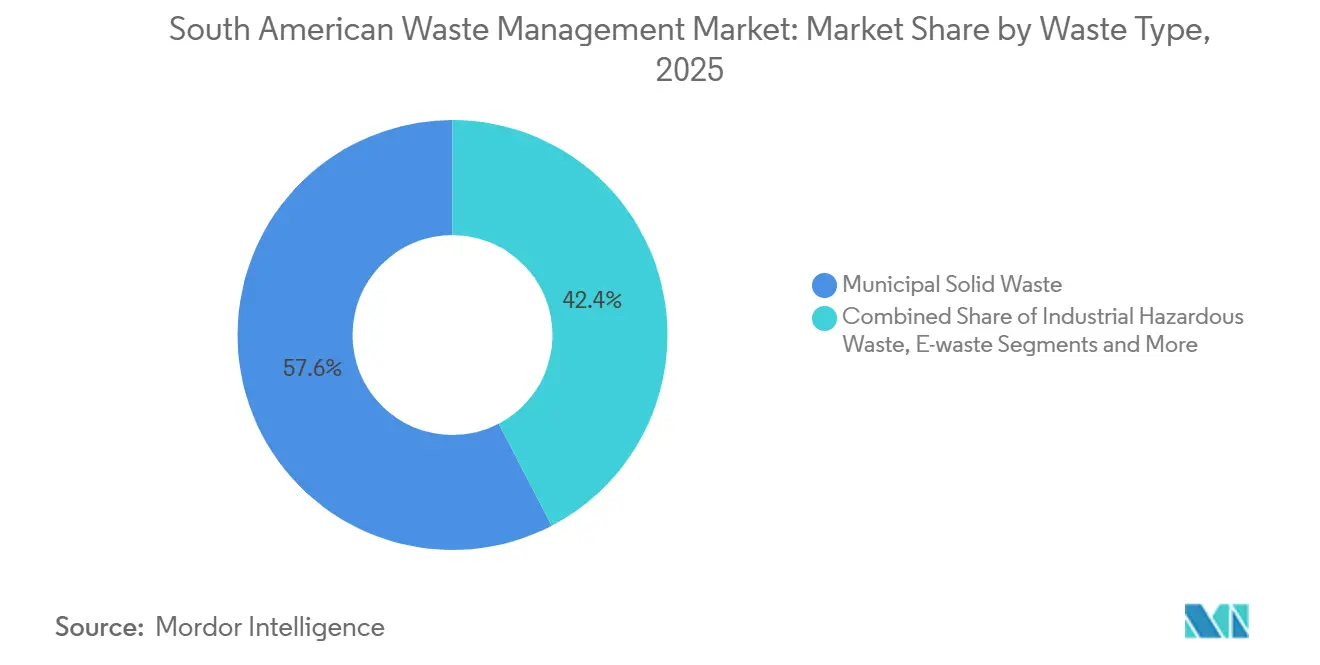

- By waste type, municipal solid waste dominated at 57.63% of the South America Waste Management Market share in 2025, and e-waste represents the fastest-growing stream, rising at a 5.08% CAGR through 2031.

- By geography, Brazil commanded a 47.19% of the South America Waste Management Market size in 2025, and Colombia is set to grow the quickest at a 5.15% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended Producer Responsibility rollout across Brazil, Chile, Colombia | +1.2% | Brazil (national), Chile (national), Colombia (Bogotá, Medellín, Cali) | Medium term (2-4 years) |

| Post-COP30 foreign investment in circular-economy infrastructure | +0.9% | Brazil (Amazon states, São Paulo, Rio de Janeiro), spill-over to Colombia, Peru | Medium term (2-4 years) |

| Urban organics-to-landfill bans stimulating composting & WtE | +0.8% | Brazil (São Paulo, Belém, Curitiba), Chile (Santiago), Argentina (Buenos Aires) | Short term (≤ 2 years) |

| Corporate zero-waste targets in mining & agribusiness | +0.6% | Chile (copper belt), Brazil (Minas Gerais, Pará), Peru (Arequipa, Cajamarca) | Long term (≥ 4 years) |

| Lithium-ion battery recycling corridors in Lithium Triangle | +0.5% | Argentina (Catamarca, Jujuy), Chile (Atacama), Bolivia (Potosí) | Long term (≥ 4 years) |

| AI/IoT route optimization reducing collection OPEX | +0.4% | Brazil (São Paulo, Rio de Janeiro), Chile (Santiago), Colombia (Bogotá) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extended Producer Responsibility Rollout Across Brazil, Chile and Colombia

Brazil’s Decree 12,688 obliges 32% recovery of plastic packaging by 2026 and requires 22% recycled content, compelling brand owners to fund reverse-logistics systems.[1]Brazilian Government, “Decree 12,688/2024,” gov.br Chile’s Law 20.920 has been fully operational since 2023, while Colombia’s Resolution 1407 is still building producer-responsibility organizations, leaving a two-year integration gap. Regional players that can navigate multiple compliance regimes enjoy early-mover advantages in sorting contracts. Brazil’s public-investment program has allocated USD 126 million to formalize waste-picker cooperatives, reducing route-access conflicts. EPR’s medium-term impact stems from the lag between fee collection and infrastructure rollout.

Post-COP30 Foreign Investment in Circular-Economy Infrastructure

Belem’s role as COP30 host unlocked a USD 10 million Global Methane Hub grant for a municipal composting plant, illustrating how climate diplomacy reroutes finance toward waste assets. Eco Invest Brasil mobilized USD 13.5 billion for anaerobic digesters and material-recovery facilities, complemented by a USD 432 million commitment from BNDES for São Paulo projects. New investors favor biomethane, which also earns CBIO decarbonization certificates, although certificate price swings after 2023 defaults inject uncertainty. With a typical 2-4 year build cycle, these funds translate into mid-decade capacity growth across Brazil’s Amazon states and adjoining Andean markets.

Urban Organics-to-Landfill Bans Stimulating Composting and WtE

Cities such as Sao Paulo, Belem, and Curitiba have enacted organics diversion mandates, forcing municipal planners to procure composting capacity or contract private anaerobic digesters. HAM Chile and Lipigas opened South America’s first bio-LNG plant in 2025, converting pork-industry organics into liquefied biomethane. Natura and Ultragaz followed with an on-site biomethane unit that supplies 45% of the factory's energy. Because bans activate at ordinance signing, truck and equipment orders are placed within months, giving the driver a short-term punch even though WtE projects need three-year permitting.

Corporate Zero-Waste Targets in Mining & Agribusiness

Codelco recovered 49.4% of non-hazardous waste in 2024, including 5,835 tonnes of tires, while Vale reprocessed 12.7 million tonnes of tailings for saleable materials. Investor scrutiny and tighter tailings-dam rules incentivize similar programs across Chile’s copper belt and Brazil’s Minas Gerais. Anglo American’s pilot in Brazil converts mine residue into paving blocks, signaling marketable circular applications. Agribusiness exporters are adding digesters to comply with ESG-linked loans. Retrofits and offtake agreements push the benefit to the long-term horizon.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Entrenched informal collection networks | -0.7% | Peru (Lima, Arequipa), Colombia (Bogotá, Medellín), Brazil (favelas in Rio, São Paulo) | Medium term (2-4 years) |

| Fiscal austerity limiting municipal CAPEX | -0.5% | Argentina (national), Brazil (Northeast states), Peru (secondary cities) | Short term (≤ 2 years) |

| Volatile carbon-credit prices weaken WtE financing | -0.4% | Brazil (national, concentrated in São Paulo, Rio de Janeiro, Minas Gerais), spill-over to Chile, Colombia | Medium term (2-4 years) |

| Cross-border e-waste dumping strains enforcement capacity | -0.3% | Peru (Callao port), Chile (Valparaíso, San Antonio ports), Argentina (Buenos Aires, land borders with Paraguay) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Entrenched Informal Collection Networks

Informal pickers manage 40% of Lima’s waste, disrupting planned routes and reducing contracted haulers’ payloads.[2]UNEP, “Informal Waste Sector in Latin America,” unep.org Bogotá’s 15,000 pickers enjoy court-protected access rights, complicating tariff negotiations and quality-of-service metrics. Brazil earmarked USD 126 million to integrate cooperatives, yet uptake differs: São Paulo signed multi-year contracts, while Rio de Janeiro’s favela-based groups remain outside EPR loops. The restraint weighs on the market until cooperative agreements, training and bin-standard upgrades mature, typically taking 30-36 months.

Fiscal Austerity Limiting Municipal CAPEX

Argentina’s debt-service ceilings froze fleet-electrification budgets in 2024 and pushed landfill closures to the next fiscal cycle. Brazil’s Northeast states, where per-capita GDP trails the Southeast by 40%, struggle to meet the co-finance requirements on BNDES loans, slowing sanitary-landfill construction. Peru’s secondary cities lack tax revenue for new transfer stations, forcing reliance on outdated diesel trucks that suffer 20% downtime. Because CAPEX freezes halt equipment orders immediately, the drag emerges in the short term, although producer-funded EPR laws in Buenos Aires partly offset the constraint by shifting cost to brand owners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Residential Dominance Meets Commercial Acceleration

Residential generators delivered 55.39% of the South America Waste Management Market share in 2025 as densely populated metros such as São Paulo, Buenos Aires and Bogotá filled curbside routes with municipal solid waste. Commercial streams, however, are on course for a 6.19% CAGR through 2031, the highest across sources, thanks to retail and office densification in Medellín, Curitiba and Guayaquil and to segregation mandates now embedded in storefront leases. EPR logistics hubs inside supermarkets and shopping malls are funneling cardboard and plastics directly to producer-responsibility organizations, trimming haul distances and boosting bale prices by up to 15%. Industrial players add volume more gradually as mining and agribusiness adopt closed-loop targets; Vale, for example, recaptured 12.7 million tonnes of waste-to-value material in 2024.

The commercial segment’s swift climb recalibrates the South America Waste Management Market size calculus for haulers that long prioritized door-to-door residential density. Franchise contracts in second-tier cities are being rebid with higher scores for source-separated collection vehicles and point-of-sale take-back kiosks. Because informal pickers historically controlled cardboard around wet-markets, new concessionaires are paying cooperatives to supply bales to EPR sorters, an early sign of coexistence. Mining sites in the Chilean copper belt and Brazil’s Minas Gerais increasingly tender specialty recyclers for scrap tires and reagent drums, reinforcing an industrial-grade revenue stream that carries above-average margins and hedges landfill-fee pressure.

By Service Type: Recycling Gains on Disposal’s Legacy Lead

Disposal and treatment preserved a 48.49% slice of the South America Waste Management Market share in 2025, anchored by 3,000+ active landfills that still accept organics despite looming bans. Yet recycling & resource recovery is lined up for a 6.29% CAGR, the field’s quickest, as EPR cash unlocks sorting-line upgrades and battery corridors across the Lithium Triangle. Collection and transport, the gateway service, is becoming smarter: São Paulo’s UTM Leste will employ AI dispatch and optical sorters to lift recovery yields to 87% from the city’s current 32%. Landfill operators hedge lost tonnage by extracting biogas; Estre’s CTR Paulínia pumps 5.5 MW into the grid, cushioning tipping-fee compression.

Recycling projects are now big-ticket: Ascend Elements’ USD 1 billion battery-recycling plant in Argentina will handle 30,000 tonnes of spent cells annually, enough to supply cathode material for 250,000 new EV packs. Bio-LNG plants such as the 2025 HAM Chile unit convert organics to fuel, clinching offtake contracts with long-haul fleets seeking to decarbonize. Consulting and audit services, though still niche, grow as municipalities seek ISO 14001 certification for transfer stations to secure multilateral funding. The South America Waste Management Market size expansion in this segment hinges on how quickly policymakers internalize externalities into landfill tariffs, nudging waste flows toward higher-margin recovery channels.

By Waste Type: E-Waste Outpaces Municipal Solid Waste

Municipal solid waste kept a 57.63% share of overall tonnage in 2025, but the electronics fraction is bursting ahead at a 5.08% CAGR, turbo-charged by smartphone turnover and appliance refresh programs. Chile’s Law 20.920 and Argentina’s 2024 Buenos Aires EPR Law 6,407 force producers to finance collection points in malls, electronics stores, and municipal depots, creating predictable feedstock for recyclers. Because printed-circuit boards hold up to USD 7,000 worth of precious metals per tonne, refiners in Atacama and Jujuy bid aggressively, supporting higher recovery payouts.

Medical waste grows in line with hospital expansion; Veolia’s 2025 buyout of Serquip added two healthcare-specific incinerators that meet updated dioxin norms. Plastic packaging, although a subset of MSW, is tracked on its own because Brazil’s 32% recovery target for 2026 makes it a compliance litmus test. Agricultural residues remain an untapped giant: Natura’s on-site digester shows that commodity processors can shave energy costs by 20% by valorizing husks and bagasse. In net effect, the South America Waste Management Market size dynamic is tilting toward specialized waste flows where regulatory pull and commodity prices intersect.

Geography Analysis

Brazil retained 47.19% of the South America Waste Management Market share in 2025, propelled by BNDES-financed EcoParks in São Paulo and Rio de Janeiro and by Veolia’s acquisition spree that lifted its national managed volume beyond 5 million tonnes annually.[3]CADE, “Merger Ruling #00254/2025 – Veolia,” cade.gov.br Large urban concessions stipulate biometric time-and-attendance for truck crews, encouraging technology adoption that filters down to regional contractors. São Paulo’s organics-diversion plan, enacted in 2025, alone is projected to redirect 3,600 tonnes per day away from landfills by 2028, catalyzing private composting syndicates.

Colombia, while smaller, is the fastest mover with a 5.15% CAGR expected through 2031. Constitutional Court decision T-291 requires Bogotá to embed more than 15,000 informal pickers into formal routes, guaranteeing material rights and spurring cooperative investment in balers and weighbridges. Resolution 1407 introduces packaging EPR fees that averaged USD 22 per tonne in pilot phases, underwriting new MRFs in Medellín and Cali. Because EPR revenue is escrowed in trust funds, lenders extend cheaper project debt, accelerating infrastructure timelines compared with grant-dependent municipalities elsewhere.

Argentina’s fiscal tightening shaved municipal capital budgets, yet Buenos Aires’ EPR law pivots costs to brand owners and sets landfill surcharges that rise to USD 34 per tonne by 2028, double today’s average. Chile benefits from an already mature EPR regime; Santiago’s MetroRail signed a five-year agreement to buy refuse-derived fuel, creating downstream certainty for MRF operators. Peru’s Supreme Decree 016-2024-MINAM obliges secondary-city landfills to install leachate treatment by 2027, but short-term compliance hinges on development-bank co-financing. Across the smaller Andean and Southern Cone nations, post-COP30 foreign funds are cherry-picking biomethane and battery-recycling opportunities, gradually knitting a regional value chain that raises the South America Waste Management Market size above the sum of its national parts.

Competitive Landscape

The competitive field is moderately fragmented. Veolia widened its lead with the May 2025 purchase of Alagoas Ambiental and Serquip, adding three EcoParks and two healthcare incinerators that extend coverage to 80 municipalities across Brazil’s Northeast. Estre’s 2024 Marca Ambiental buyout lifted its footprint to 300 cities and cemented a biogas monetization strategy through the 7.5 MW CTR Paulínia plant. Grupo Solví leans on landfill-gas capture for baseline revenue while piloting AI route scheduling in Salvador and Recife.

Strategic themes revolve around vertical integration, from curbside pickup to energy sales, enabling cost recovery even as tipping fees flatten. Ambipar, which logged USD 1.24 billion in revenue in 2024, uses cross-border spill response units to upsell hazardous-waste contracts in mining corridors. Disruptors such as Ascend Elements and HAM Chile target high-growth niches, battery metals, and bio-LNG, where traditional haulers lack processing know-how. Equipment vendors, mainly European, embed AI controls that raise capture rates and win performance-linked bonuses under EPR contracts.

Municipal tenders increasingly bundle collection with recovery quotas, penalizing landfill-only bids and advantaging operators owning composters or digesters. Informal-sector integration clauses reward bidders able to subcontract cooperatives and demonstrate social-impact metrics. Financial investors view brownfield landfill concessions as yield plays but channel growth capital to recycling and biomethane platforms whose revenues ride producer-funding and decarbonization incentives. Overall, rivalry is intensifying yet still leaves room for regional champions to scale, keeping the South America Waste Management Market both contested and opportunity-rich.

South America Waste Management Industry Leaders

Veolia Latin America

Estre Ambiental

Grupo Solví

Ambipar

Proactiva Medio Ambiente

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: HAM Chile and Lipigas inaugurated South America’s first bio-LNG plant in Ñuble, processing up to 16,500 m³ of organics per day.

- May 2025: Veolia completed its acquisition of Alagoas Ambiental and Serquip Tratamentos Resíduos AL, adding three EcoParks and two healthcare facilities and lifting annual managed tonnage by 15%.

- May 2025: Natura and Ultragaz opened a biomethane unit at Cajamar that now supplies 45% of factory energy and fuels 28 trucks.

- February 2025: BNDES approved USD 22.6 million to expand the CTR Seropedica landfill in Rio de Janeiro, adding 2.8 MW of electricity and biomethane production.

South America Waste Management Market Report Scope

Waste management refers to the various schemes to manage and dispose of waste. It can be by discarding, destroying, recycling, recovering, reusing, or controlling waste. The high objective of waste management is to reduce the quantum of unusable materials and to avert potential health and environmental hazards. A complete background analysis of the South America Waste Management Market, including the assessment of the economy and contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The South America Waste Management Market is segmented by waste type (industrial waste, municipal solid waste, hazardous waste, e-waste, plastic waste, and bio-medical waste) and by disposal methods (collection, landfills, incineration, and recycling).

The report offers market sizes and forecasts in value (USD) for all the above segments.

By Source

| Residential |

| Commercial (retail, office, etc.) |

| Industrial |

| Medical (Health and Pharmaceutical) |

| Construction & Demolition |

| Others (institutional, agricultural, etc) |

By Service Type

| Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill |

| Recycling & Resource Recovery | |

| Incineration & Waste-to-Energy | |

| Others (Chemical Treatment, Composting, etc.) | |

| Others (Consulting, Audit & Training, etc.) |

By Waste Type

| Municipal Solid Waste |

| Industrial Hazardous Waste |

| E-waste |

| Plastic Waste |

| Biomedical Waste |

| Construction & Demolition Waste |

| Agricultural Waste |

| Other Specialized Waste (radio active, etc) |

By Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Source | Residential | |

| Commercial (retail, office, etc.) | ||

| Industrial | ||

| Medical (Health and Pharmaceutical) | ||

| Construction & Demolition | ||

| Others (institutional, agricultural, etc) | ||

| By Service Type | Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill | |

| Recycling & Resource Recovery | ||

| Incineration & Waste-to-Energy | ||

| Others (Chemical Treatment, Composting, etc.) | ||

| Others (Consulting, Audit & Training, etc.) | ||

| By Waste Type | Municipal Solid Waste | |

| Industrial Hazardous Waste | ||

| E-waste | ||

| Plastic Waste | ||

| Biomedical Waste | ||

| Construction & Demolition Waste | ||

| Agricultural Waste | ||

| Other Specialized Waste (radio active, etc) | ||

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the South America Waste Management Market today?

It stood at USD 40.03 billion in 2025 and is projected to reach USD 51.97 billion by 2031, growing at a 4.44% CAGR.

Which waste stream is expanding the fastest across the region?

E-waste leads with a 5.08% CAGR through 2031, propelled by higher smartphone turnover and new EPR mandates.

Why is Colombia viewed as the fastest-growing national opportunity?

A strong EPR framework and the formalization of 15,000+ informal pickers are set to lift Colombia at a 5.15% CAGR, the highest in the region.

What role does biomethane play in new investment plans?

Bio-LNG plants and landfill-gas projects monetize methane and qualify for decarbonization credits, improving returns on organics diversion.

How are AI technologies changing collection economics?

Route-optimization and optical-sorting platforms are trimming diesel and labor costs by up to 18%, accelerating payback on new fleets.

Which service segment should haulers prioritize for growth?

Recycling & resource recovery, forecast to rise at a 6.29% CAGR, offers higher margins than legacy landfill disposal.

Page last updated on: