China Renewable Gas From Waste Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

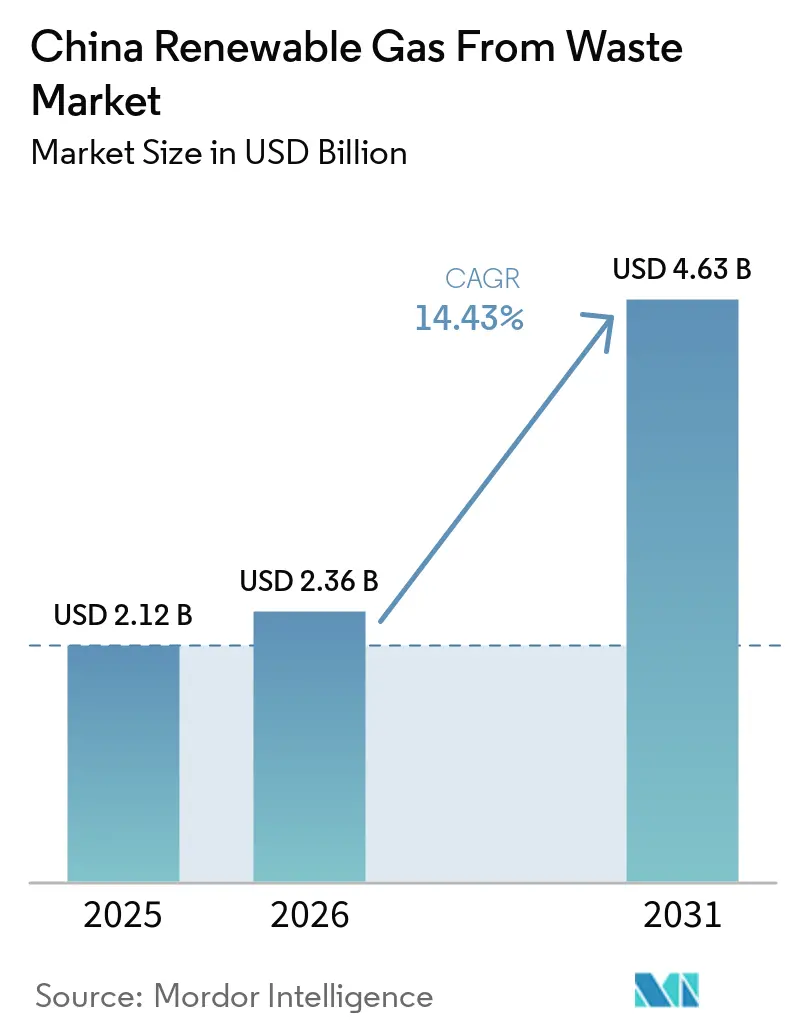

| Base Year Market Size (2025) | USD 2.12 Billion |

| Market Size (2026) | USD 2.36 Billion |

| Market Size (2031) | USD 4.63 Billion |

| Growth Rate (2026 - 2031) | 14.43% CAGR |

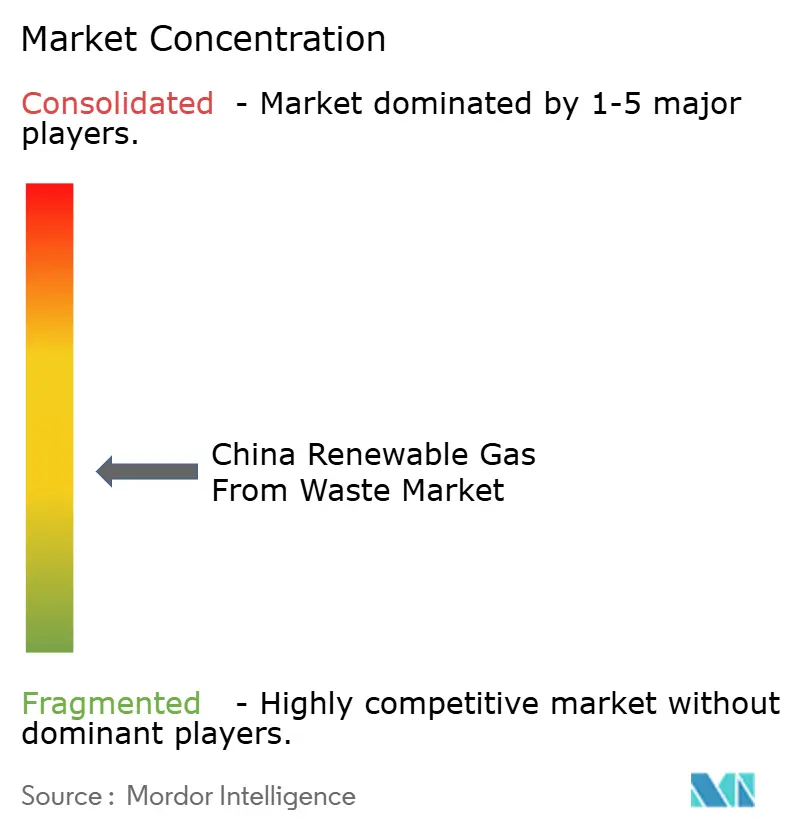

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Renewable Gas From Waste Market Analysis by Mordor Intelligence

The China Renewable Gas From Waste Market size is projected to expand from USD 2.12 billion in 2025 and USD 2.36 billion in 2026 to USD 4.63 billion by 2031, registering a CAGR of 14.43% between 2026 to 2031.

The faster expansion reflects a firmer legal basis for biomethane after the Energy Law took effect in January 2025, moving renewable gas from policy encouragement into the formal energy framework. Demand conditions are also improving because the national carbon market now subjects more industrial emitters to compliance pressure, thereby raising the value of lower-carbon gas supply contracts for steel, cement, and aluminum users. The China renewable gas from waste market is also becoming more structured as PetroChina and Sinopec build early positions in grid injection, trading, and certification, which narrows the room for smaller players to secure first-mover scale. Even so, the lack of a national production subsidy still leaves project economics sensitive to regional gas prices and collection costs, especially where feedstock is scattered and pipeline access is limited. The China renewable gas from waste market, therefore, offers the strongest near-term opportunity in counties and cities where waste density, gas infrastructure, and policy enforcement already align.

Key Report Takeaways

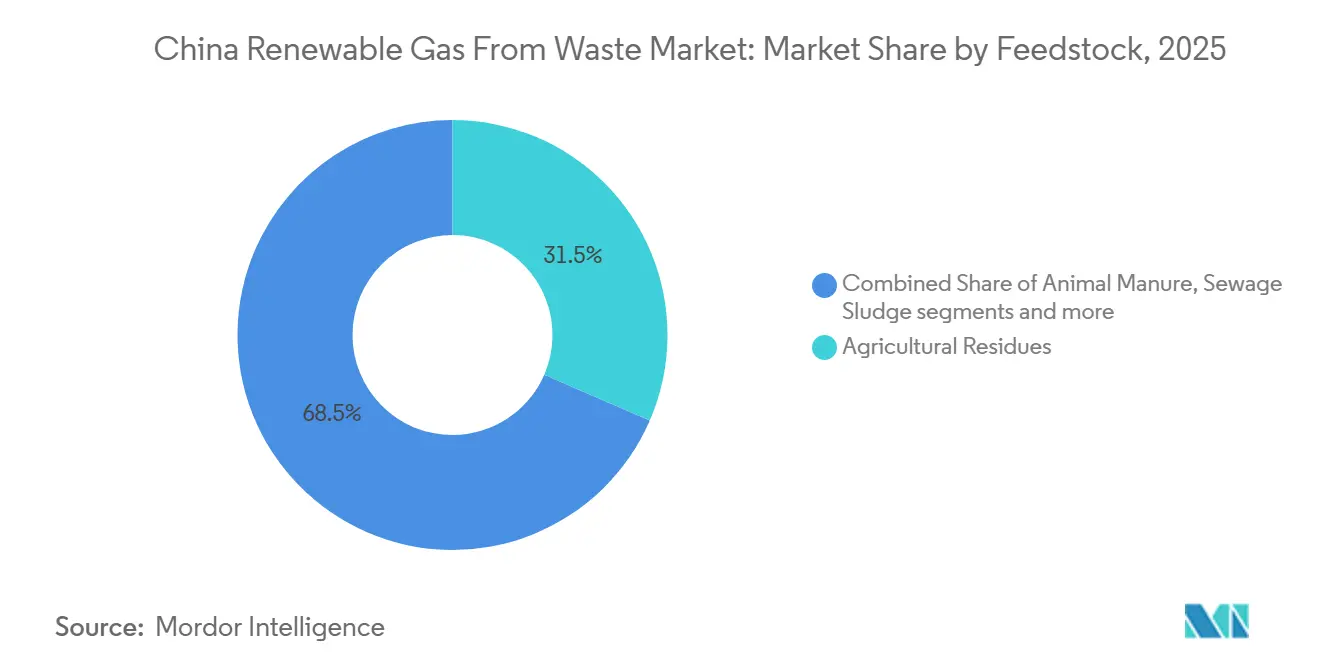

- By feedstock, agricultural residues accounted for 31.50% of the China renewable gas from waste market share in 2025, and food waste is projected to grow at a 14.32% CAGR through 2031.

- By technology, anaerobic digestion accounted for 43.60% of the China renewable gas from waste market size in 2025, and gasification is projected to grow at a 15.10% CAGR through 2031.

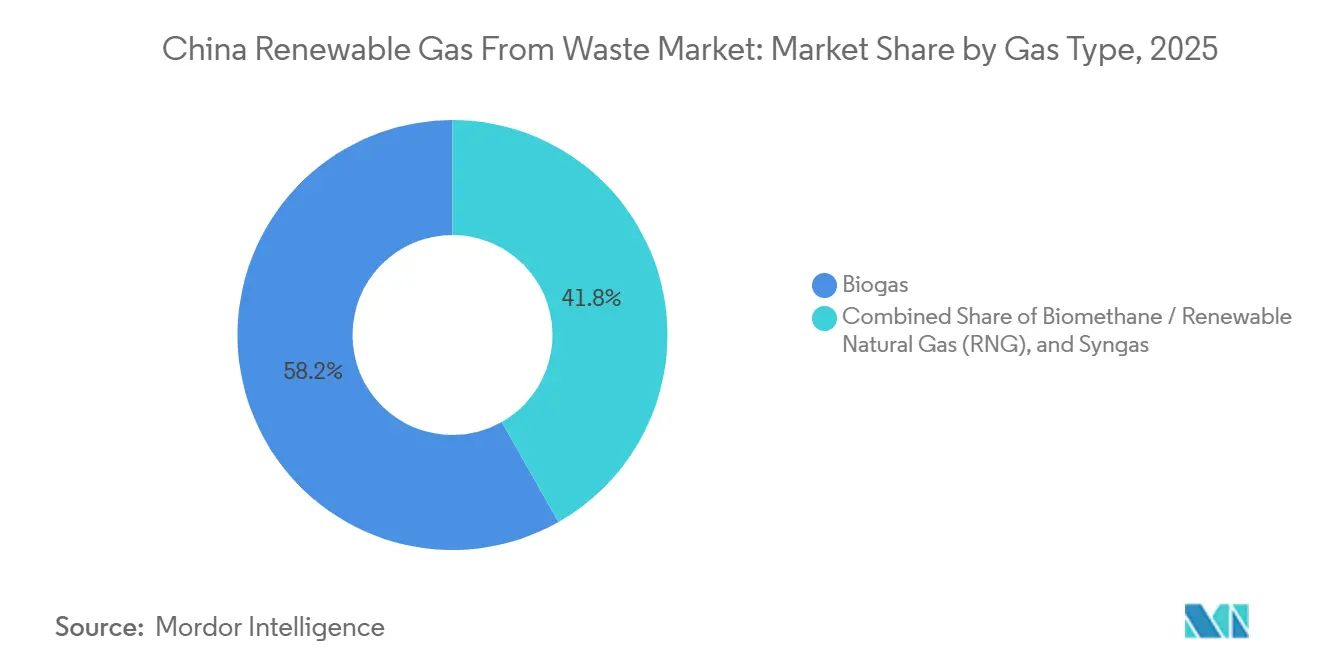

- By gas type, biogas led with a 58.20% share in 2025, and renewable natural gas is projected to grow at a 15.46% CAGR through 2031.

- By application, electricity generation accounted for 41.40% of the market in 2025, and transportation fuel is projected to grow at a 13.25% CAGR through 2031.

- By component, digesters and fermentation systems accounted for 31.20% of the market in 2025, and gas processing and upgrading units are projected to grow at a 15.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Renewable Gas From Waste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dual Carbon Goals Accelerating Bio-Natural Gas Policy Mandates | +4.2% | National, with concentrated gains in Heilongjiang, Henan, Sichuan, and Inner Mongolia | Short term (≤ 2 years) |

| Energy Law Strengthening Biomethane Integration | +3.1% | National, with early gains in Guangdong, Jiangsu, and Zhejiang | Short term (≤ 2 years) |

| State-Owned Enterprise Entry Validating and Scaling the Biomethane Sector | +2.8% | National, with priority corridors in Southwest and Northeast China | Medium term (2-4 years) |

| Mandatory Urban Food Waste Sorting Expanding Centralized Feedstock Supply | +2.3% | Municipal China, especially Shanghai, Beijing, Chengdu, and Shenzhen | Medium term (2-4 years) |

| National Carbon Market and SOE Emission Disclosure Driving Industrial Biomethane Offtake | +1.9% | National, with the strongest pull in Hebei, Shanxi, and Liaoning | Medium term (2-4 years) |

| Agricultural Waste Management Crisis Creating Policy-Driven Feedstock Push | +1.4% | Rural agricultural provinces, including Shandong, Hunan, Anhui, and Jilin | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dual Carbon Goals Accelerating Bio-Natural Gas Policy Mandates

China’s carbon peak and carbon neutrality agenda is now shaping the China renewable gas from waste market through rules, measurement systems, and project-level compliance expectations rather than broad policy signaling alone. The National Development and Reform Commission (NDRC) 2024 action plan on carbon peak and carbon neutrality standards strengthened the measurement and verification base that renewable gas projects need to document emissions outcomes at the enterprise level. That shift matters because developers now need stronger data quality and more bankable reporting before projects can secure offtake confidence from utilities and industries. It also raises entry barriers for smaller firms that lack verified monitoring systems and formal reporting capabilities. In practice, the China renewable gas from waste market is moving closer to sectors where legal recognition, carbon accounting, and access to infrastructure must work together before scale can follow.

Energy Law Strengthening Biomethane Integration

The Energy Law of the People’s Republic of China took effect on January 1, 2025, and gave bio-natural gas a clearer statutory position within the national energy system. The law encourages the use of biomass energy according to local conditions and also requires the energy system to improve its ability to accept and allocate renewable energy. That legal change reduces the ambiguity that city gas distributors previously used to resist access to the biomethane grid. Project developers can now negotiate long-term supply arrangements with better institutional backing than the China renewable gas from waste market had before 2025. The result is a more predictable commercial path for grid injection projects in provinces with dense municipal gas networks.

State-Owned Enterprise Entry Validating and Scaling the Biomethane Sector

State-owned enterprise participation is reshaping the China renewable gas from waste market by validating project quality, improving price discovery, and strengthening downstream access. PetroChina’s Southwest Oil and Gasfield Company launched its first biomethane business in 2024 and later completed grid injection from the Dayi County project, which processes 350,000 tonnes of agricultural waste each year and supplies pipeline-quality biomethane into Chengdu’s municipal network. Sinopec also launched the country’s first gas-certificate-integrated biomethane online trading platform in September 2024, providing the sector with a formal platform for transaction visibility and green certification. The Ministry of Ecology and Environment (MEE)'s 2025 national carbon market report indicated that central State-Owned Enterprises (SOEs) maintained full compliance with emissions trading requirements, while 72 subsidiaries utilized China Certified Emission Reductions (CCERs) to meet compliance obligations, supporting demand for biomass-derived carbon credits. This combination reduces verification risk and makes the China renewable gas from waste market easier for lenders and industrial buyers to underwrite.

Mandatory Urban Food Waste Sorting Expanding Centralized Feedstock Supply

Mandatory waste sorting is improving visibility of feedstock for the China renewable gas from waste market, especially in larger cities where kitchen waste volumes are concentrated. The State Council’s 2024 policy on waste circular utilization called for faster construction of kitchen waste treatment infrastructure and gave energy use a direct policy role in organic waste handling. In May 2026, national reporting confirmed that waste sorting was already in place across 297 prefecture-level cities and above, supporting a more stable pipeline of separated food waste. Cleaner and more consistent feedstock reduces contamination and improves digestion efficiency at urban renewable gas sites. That makes city-based projects easier to scale than many older plants that depended on poorly sorted mixed waste streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence Of A National Biomethane Production Subsidy Framework Undermining Viability | -2.8% | National, with the strongest effect in central and western provinces with weaker gas infrastructure | Medium term (2-4 years) |

| High Feedstock Logistics Costs Limiting Viable Project Geographies | -1.9% | Rural agricultural provinces, including Shandong, Henan, Anhui, and Yunnan | Long term (≥ 4 years) |

| Fragmented Multi-Ministry Regulatory Structure Causing Approval Delays | -1.4% | National, with added friction in provinces where NDRC (National Development and Reform Commission), MEE (Ministry of Ecology and Environment), and MOA (Ministry of Agriculture and Rural Affairs) roles overlap | Medium term (2-4 years) |

| Mass Abandonment Of Household Digesters Eroding Distributed Production Base | -0.8% | Rural North China and South China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Absence of a National Biomethane Production Subsidy Framework Undermining Viability

The China renewable gas from waste market still lacks a national per-unit production subsidy, leaving many projects dependent on local gas prices, by-product sales, and carbon revenues. This matters most in regions where distribution networks are weaker, and developers cannot rely on premium urban offtake channels. The MEE’s December 2025 release of new CCER methodologies for pig farm manure biogas recovery and agricultural waste centralized processing helps part of the revenue stack. Still, it does not replace a direct production support mechanism. Without a national subsidy, stronger balance sheets remain a major competitive advantage, favoring SOEs and large environmental firms over smaller developers. As a result, project deployment remains selective even when the resource base is large.

High Feedstock Logistics Costs Limiting Viable Project Geographies

High collection and transport costs remain a structural limit to the China renewable gas from waste market, especially for straw and manure spread across rural counties. Even where provinces generate very large waste volumes, developers still need dependable county-level aggregation systems before those resources can support commercial plants. People’s Daily reported in May 2025 that Hubei alone produces large volumes of straw and livestock manure, but the economic challenge lies in moving and consolidating those materials at scale. Until logistics support improves, the China renewable gas from waste market will continue to favor dense feedstock clusters near gas infrastructure rather than broad rural coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Agricultural Residues Anchor Volumes, Food Waste Accelerates

Agricultural residues accounted for 31.50% of the China renewable gas from waste market share in 2025, making them the largest feedstock base in the sector. Their lead reflects the scale of crop output and the wide availability of straw and related residues across major farming provinces. In practical terms, these streams provide the volume needed for county-level plants where collection systems are already in place. The China renewable gas from waste market also benefits from the fact that agricultural residues align with broader rural waste treatment and resource-use goals.

Food waste is forecast to expand at 14.32% through 2031, making it the fastest-growing feedstock category in the market. Animal manure, industrial organic waste, sewage sludge, and landfill waste serve different compliance and disposal needs within the China renewable gas from waste market. Manure is especially important because livestock waste treatment is no longer optional in many areas, and the Ministry of Agriculture and Rural Affairs has pushed for nationwide comprehensive utilization rates of 80% or more. This growth reflects mandatory urban sorting, cleaner incoming feedstock, and new CCER methodologies that improve the revenue potential of centralized biogas processing from organic waste streams.

By Technology: Anaerobic Digestion Dominates, Gasification Emerges as Fastest-Growing Technology Segment.

Anaerobic digestion accounted for 43.60% of the China renewable gas from waste market size in 2025, making it the leading technology platform across agricultural and urban waste projects. Its dominance stemmed from a long operating history, familiarity with existing plants, and a broad installed base built around manure and mixed organic feedstocks. The technology also remains central because most current projects still begin with raw biogas production before any upgrading step. This gives anaerobic digestion a foundational role in the China renewable gas from waste market, even as newer pathways gain ground.

Gasification is projected to grow at 15.10% through 2031, which makes it the fastest-growing technology category in the forecast period. Biogas upgrading systems, landfill gas recovery, pyrolysis, and monitoring systems all support a broader, increasingly sophisticated technology stack. China Everbright Environment’s first biomass gasification project in Xiao County, Anhui, showed that thermochemical conversion can move beyond pilot status and widen the usable feedstock base to drier materials that are less suitable for digestion. That matters because renewable gas from the waste industry in China requires multiple conversion routes to process the full range of municipal, agricultural, and industrial organic waste.

By Gas Type: Biogas Leads in Volume, Renewable Natural Gas Captures the Premium Trajectory

Biogas accounted for 58.20% of the gas type segment in 2025, making it the largest category in the China renewable gas from waste market. Its lead came from the large installed base of anaerobic digestion assets across agricultural, food, and municipal organic waste streams. Most operating projects still produce raw biogas with 50% to 70% methane content and use it locally for heat and power rather than for grid injection. This keeps biogas as the dominant volume stream even as higher-value gas products gain traction. The China renewable gas from waste market is therefore moving from basic gas production toward cleaner and more standardized gas output.

Biomethane / Renewable natural gas is forecast to grow at 15.46% through 2031, the fastest among gas types, because it benefits most directly from grid injection and transportation fuel demand. The segment is gaining importance because it sits at the center of the market’s shift toward pipeline-quality renewable natural gas. PetroChina also launched its first biomethane business in Southwest China in 2024, using winery wastewater feedstock, and achieved GBT41328-2022 Class I biomethane quality through PSA purification.

By Application: Electricity Generation Retains Scale, Transportation Fuel Leads Growth

Electricity generation accounted for 41.40% in 2025, making it the largest application across the China renewable gas from waste market. That leadership reflects the long-standing use of biogas in power generation and the fact that many older facilities were designed around on-site energy conversion. Combined heat and power also remains relevant because it improves energy use efficiency in food processing, industrial parks, and agricultural settings. Together, these established applications still account for a large share of the installed asset base.

Transportation fuel is expected to grow at 13.25% through 2031, making it the fastest-growing application segment. The National Energy Administration stated in 2024 that vehicle use and gas network integration were among the priority end uses for biomass energy development, which supports biomethane use beyond electricity production. The application also benefits from limits on heavy-duty truck electrification and from the need for lower-carbon fuel options in logistics fleets. As a result, the China renewable gas from waste market is gradually shifting from legacy power uses toward transport and grid-linked fuel value pools.

By Component: Digesters Drive Installed Base, Upgrading Units Capture Value Shift

Digesters and fermentation systems accounted for 31.20% of the component segment in 2025, making them the largest installed equipment category. That position reflects years of project construction centered on digestion as the core conversion process for manure, food waste, and mixed organic streams. Gas collection systems, compressors, storage, and power equipment grew alongside this installed base and supported local heat and electricity models. The China renewable gas from waste market, therefore, still carries a large stock of equipment tied to raw biogas generation rather than upgraded gas output.

Gas processing and upgrading units are projected to grow at 15.34% through 2031, which makes them the fastest-growing component category. This growth follows the market’s shift toward pipeline-quality biomethane and certified renewable gas sales rather than lower-value local use. PetroChina’s Dayi County project used wet desulfurization and PSA purification to meet the national Class I biomethane standard, demonstrating that standardized upgrading is now commercially viable at the county scale. Monitoring and control systems are also gaining ground as larger operators need stronger process visibility across multiple project sites.

Geography Analysis

Northeastern provinces such as Heilongjiang, Jilin, and Inner Mongolia have large concentrations of straw and manure due to their grain and livestock bases. These areas offer strong feedstock volume, but colder operating conditions can reduce anaerobic digestion efficiency if plant design and heat management are weak. Heilongjiang’s integrated biogas projects illustrate how provincial coordination can bring straw and manure into a single treatment chain at a meaningful scale. Even so, thinner gas grid coverage outside larger northern cities still limits the speed of grid injection growth in many of these areas.

Eastern and coastal provinces show the opposite pattern in the China renewable gas from waste market. Jiangsu, Zhejiang, Guangdong, and Shandong have denser urban populations, stronger municipal gas networks, and more stringent enforcement of waste-sorting. Shanghai’s Zero Waste City regulations and municipal solid waste rules support a more dependable urban feedstock supply chain for food waste projects and improve the economics of smaller grid-connected plants. Waste sorting coverage across 297 prefecture-level and above cities also strengthens bankability for urban organic waste projects by making feedstock availability easier to plan. This gives the coast a clear advantage in food waste collection, gas distribution, and industrial offtake access.

Central and southwestern provinces are becoming the main expansion belt for the China renewable gas from waste market through 2031. Sichuan combines the availability of agricultural waste with improved pipeline access, which is why PetroChina’s Dayi County project has become a reference case for county-scale grid injection. Anhui is also moving forward with county-level circular models that combine multiple stations and pipeline links into a single integrated system, with full commissioning expected in 2026, according to the user-supplied draft. The NDRC’s October 2024 renewable energy substitution action plan further supports agricultural and rural renewable gas development in central and western regions, where the potential for coal replacement remains high.

Competitive Landscape

The China renewable gas from waste market is moderately fragmented. PetroChina and Sinopec now sit at the center of the upper tier because they control critical advantages in infrastructure access, commercial credibility, and downstream gas relationships. Large environmental groups also hold a strong position because they can expand existing waste-processing operations into biomethane production and carbon monetization. This gives leading companies more room to absorb policy delays and uneven regional pricing than smaller independent developers do. The China renewable gas from waste market is therefore no longer a pilot-heavy space where technology alone decides who scales first.

Recent strategic moves show how the leading players are building control over different parts of the value chain. PetroChina completed the Dayi County municipal grid injection project in December 2024, which set a practical benchmark for agricultural waste-to-pipeline gas conversion at a commercial scale. Sinopec launched the first gas-certificate integrated online biomethane trading platform in September 2024, which gave the sector an early national mechanism for pricing and certification. China Everbright Environment reported in March 2026 that its first biomethane project was already supplying gas to Jingjiang Special Steel, which shows how environmental firms are linking waste assets to industrial offtake contracts. These moves matter because they cover infrastructure, trading, and end-market monetization rather than just plant construction.

The middle layer of the China renewable gas from waste market still offers room for specialists, especially in county-scale projects and process optimization. Independent providers can compete where feedstock aggregation has been proven, but national SOEs have not yet moved aggressively. Their best openings are in upgrading systems, digital monitoring, and operating efficiency rather than in pure balance sheet competition. Still, competitive intensity is increasing as CCER eligibility, gas quality verification, and grid connectivity become more important to project finance and offtake confidence.

China Renewable Gas From Waste Industry Leaders

PetroChina Company Limited

China Petroleum & Chemical Corporation (Sinopec Corp.)

CNOOC Refining and Petrochemical Co., Ltd.

China Gas Holdings Limited

ENN Energy Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: China's Ministry of Housing and Urban-Rural Development confirmed that urban household waste sorting is now in place across all residential communities in 297 prefecture-level cities, targeting a 76% recycling rate by 2030. This milestone secures a legally mandated food waste feedstock pipeline for urban Biomethane projects at the national scale.

- March 2026: China Everbright Environment Group announced 2025 annual results, reporting the first commercialization of biomethane production technology, with the Group's first biomethane project supplying gas to Jingjiang Special Steel Co. Ltd, and 2 new projects secured, totaling approximately RMB 72 million (USD 10.3 million) in investment, with a designed biomethane supply capacity of 10,000,000 Nm³/year.

- December 2025: The MEE released 2 new CCER methodologies specifically covering large-scale pig farm manure biogas recovery (CCER-15-001-V01) and agricultural waste centralized processing (CCER-15-002-V01), creating a carbon credit monetization pathway for biogas projects that had previously operated outside China's voluntary carbon market.

- September 2025: The MEE released the Progress Report of China's National Carbon Market (2025), confirming 100% ETS compliance by all central SOEs for 3 consecutive cycles and that 72 central SOE subsidiaries used CCERs to offset allowance surrender obligations, creating sustained institutional demand for bio-sourced carbon credits.

China Renewable Gas From Waste Market Report Scope

| Municipal Solid Waste (MSW) |

| Agricultural Residues |

| Animal Manure |

| Industrial Organic Waste |

| Sewage Sludge |

| Food Waste |

| Others |

| Anaerobic Digestion |

| Landfill Gas Recovery |

| Gasification |

| Pyrolysis |

| Biogas Upgrading Systems |

| Others |

| Biogas |

| Biomethane / Renewable Natural Gas (RNG) |

| Syngas |

| Electricity Generation |

| Combined Heat & Power (CHP) |

| Grid Injection |

| Transportation Fuel |

| Industrial Heating |

| Residential & Commercial Heating |

| Others |

| Gas Collection Systems |

| Digesters & Fermentation Systems |

| Gas Processing & Upgrading Units |

| Compressors & Storage Systems |

| Power Generation Equipment |

| Monitoring & Control Systems |

| Others |

| By Feedstock | Municipal Solid Waste (MSW) |

| Agricultural Residues | |

| Animal Manure | |

| Industrial Organic Waste | |

| Sewage Sludge | |

| Food Waste | |

| Others | |

| By Technology | Anaerobic Digestion |

| Landfill Gas Recovery | |

| Gasification | |

| Pyrolysis | |

| Biogas Upgrading Systems | |

| Others | |

| By Gas Type | Biogas |

| Biomethane / Renewable Natural Gas (RNG) | |

| Syngas | |

| By Application | Electricity Generation |

| Combined Heat & Power (CHP) | |

| Grid Injection | |

| Transportation Fuel | |

| Industrial Heating | |

| Residential & Commercial Heating | |

| Others | |

| By Component | Gas Collection Systems |

| Digesters & Fermentation Systems | |

| Gas Processing & Upgrading Units | |

| Compressors & Storage Systems | |

| Power Generation Equipment | |

| Monitoring & Control Systems | |

| Others |

Key Questions Answered in the Report

What is the 2031 outlook for renewable gas from waste in China?

The sector is forecast to reach USD 4.63 billion by 2031 from USD 2.12 billion in 2025, with a 14.43% CAGR over 2026 to 2031.

Which feedstock currently generates the most revenue in China?

Agricultural residues led in 2025 with a 31.50% share because they offer large available volumes across major farming provinces.

Which feedstock is expected to grow the fastest through 2031?

Food waste is expected to grow the fastest, at 14.32%, as mandatory waste sorting improves feedstock quality and supply visibility.

Why are SOEs so important in this sector?

PetroChina and Sinopec are shaping scale through grid injection, trading platforms, certification, and downstream gas relationships, which lowers risk for buyers and lenders.

Which application is expanding the fastest in China?

Transportation fuel is projected to grow at 13.25% through 2031 as logistics operators seek lower-carbon alternatives where full electrification is more difficult.

What is the main barrier to wider project deployment?

The biggest hurdle remains economics, especially the lack of a national production subsidy and the high logistics cost of collecting dispersed agricultural waste.

Page last updated on: