Switzerland Renewable Gas From Waste Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

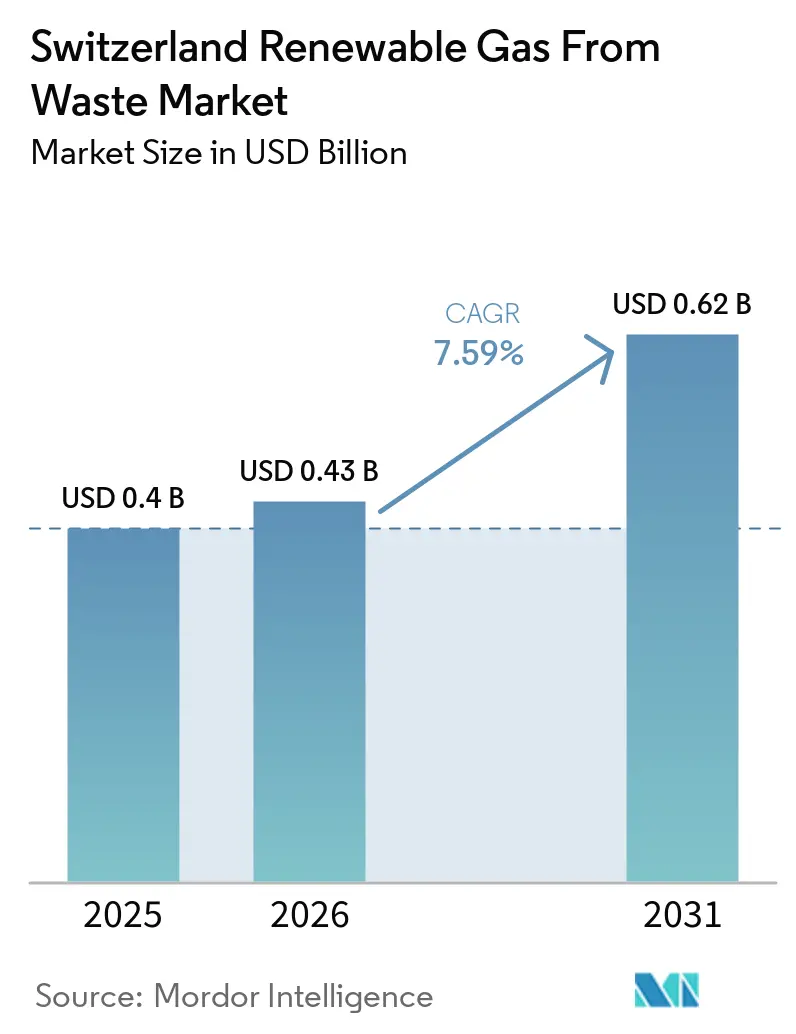

| Base Year Market Size (2025) | USD 0.4 Billion |

| Market Size (2026) | USD 0.43 Billion |

| Market Size (2031) | USD 0.62 Billion |

| Growth Rate (2026 - 2031) | 7.59% CAGR |

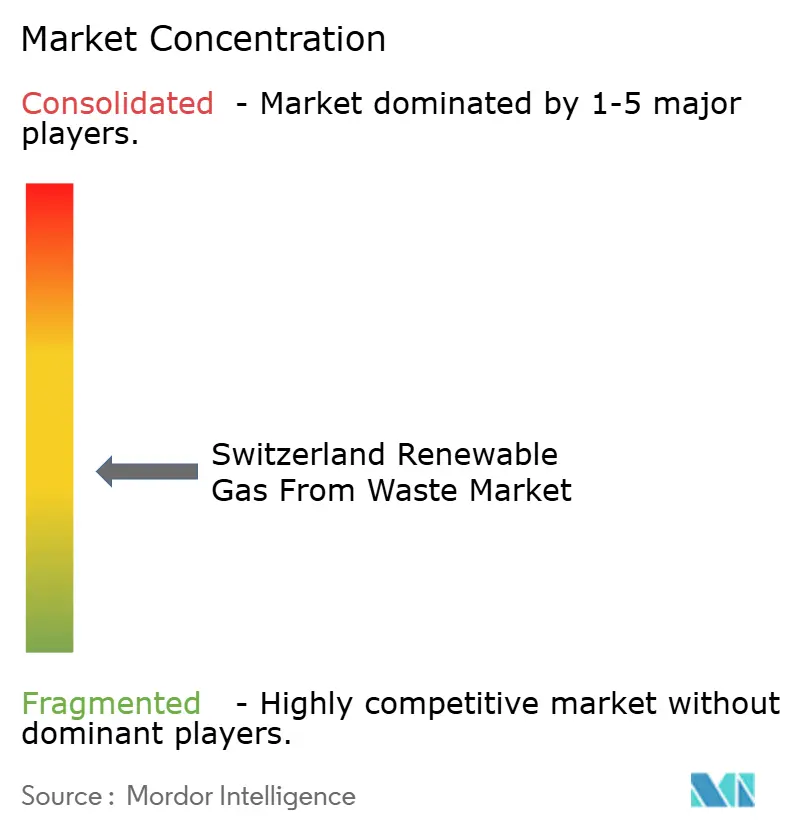

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Renewable Gas From Waste Market Analysis by Mordor Intelligence

The Switzerland Renewable Gas From Waste Market size is projected to expand from USD 0.4 billion in 2025 and USD 0.43 billion in 2026 to USD 0.62 billion by 2031, registering a CAGR of 7.59% between 2026 to 2031.

Switzerland has no domestic fossil gas reserves, and the 2022 energy crisis made gas import dependence a more direct national energy security issue, now shaping the Switzerland renewable gas from waste market as much as climate policy. The policy environment in 2026 is stronger than it was two years earlier because the revised CO2 Act and the updated Energy Promotion Ordinance now support biomethane production, upgrading, and grid injection rather than focusing mainly on electricity output. This shift is moving investor attention toward upgrading infrastructure, certificate-backed production, and projects that can combine federal support with cantonal or private funding. Competition in the Switzerland renewable gas from waste market is rising as utility-linked groups retrofit Combined Heat & Power (CHP)-based biogas plants for grid injection and technology contractors offer modular solutions that shorten payback periods. The largest untapped growth opportunity remains agricultural manure digestion, where the resource base is much larger than the installed plant base. However, the KEV transition and the absence of a federal Gas Market Act still create uncertainty around conversion economics and grid connection terms in the Switzerland renewable gas from waste market.

Key Report Takeaways

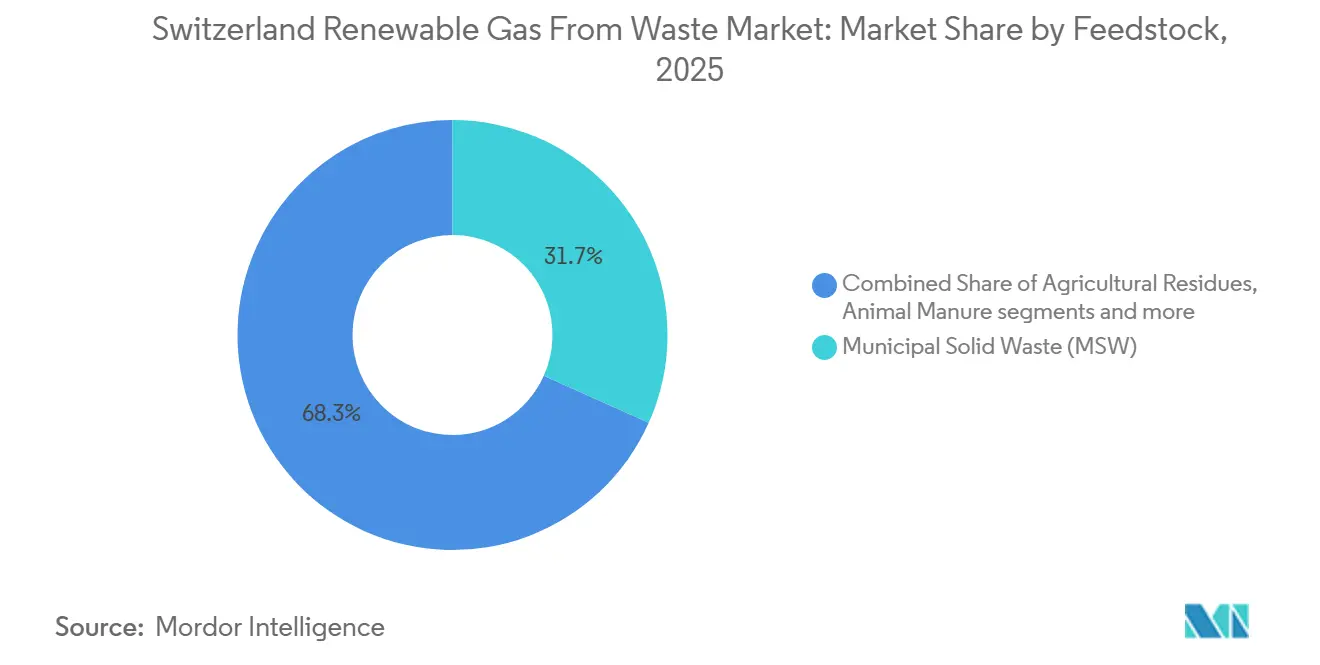

- By feedstock, municipal solid waste held 31.7% of the Switzerland renewable gas from waste market share in 2025, while food waste is projected to expand at an 8.8% CAGR through 2031.

- By technology, anaerobic digestion accounted for 44.4% of the Switzerland renewable gas from waste market size in 2025, while biogas upgrading systems are forecast to grow at a 10.9% CAGR through 2031.

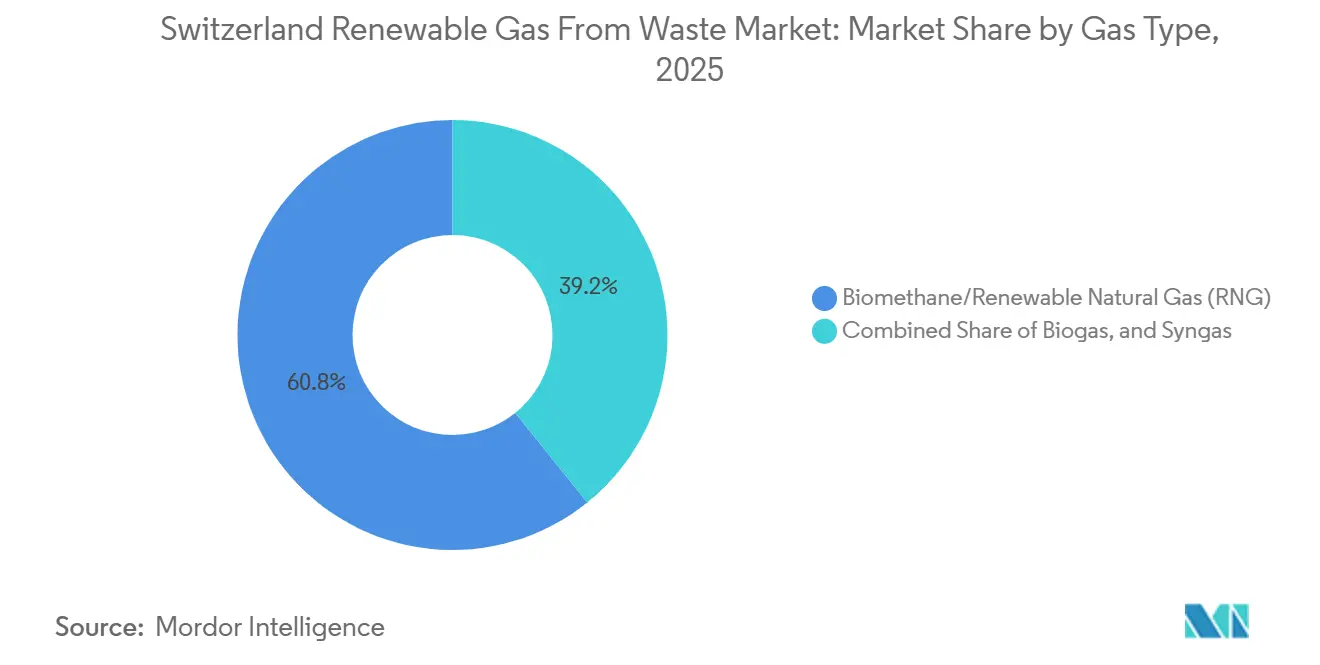

- By gas type, biomethane/renewable natural gas (RNG) held 60.8% of the Switzerland renewable gas from waste market share in 2025 and is projected to expand at an 11.8% CAGR through 2031.

- By application, grid injection accounted for 32.8% of the Switzerland renewable gas from waste market in 2025, while transportation fuel recorded the highest projected CAGR of 12.6% through 2031.

- By component, gas processing and upgrading units accounted for 33.2% of the Switzerland renewable gas from waste market in 2025, while monitoring and control systems are expected to grow at a 10.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Switzerland Renewable Gas From Waste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| New CO2 Act Biomethane Funding Through Grid Injection | +2.5% | National | Short term (≤ 2 years) |

| PSI Study on Biomethane Covering 25% to 50% of Future Gas Demand | +1.8% | National | Long term (≥ 4 years) |

| Revised Energy Promotion Ordinance Support for Waste-Based Plants | +1.5% | National | Medium term (2-4 years) |

| Rising Renewable Gas Demand in Heavy Transport and Municipal Networks | +1.2% | National, with concentration in Zurich, Bern, Lucerne, Basel corridors | Medium term (2-4 years) |

| Axpo and Energie 360° Expansion of Biomethane Grid Injection | +0.8% | German-speaking cantons, expanding nationally | Short term (≤ 2 years) |

| Biomethane Already Supplying Around 8% of Gas Consumption | +0.5% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

New CO2 Act Introducing Dedicated Biomethane Production Funding via Grid Injection

In the Switzerland renewable gas from waste market, the most immediate catalyst is the redesign of federal support rather than a simple increase in subsidy volume. Article 34a of the revised CO2 framework, effective from January 2025, introduced a dedicated investment contribution for new biomethane plants and major extensions to existing plants that upgrade biogas to grid quality for injection or local fuel use. Eligibility depends on a 25% increase in gross energy production over the previous 3-year average, directing support toward real capacity expansion rather than small efficiency gains. The funding can be combined with cantonal support, private financing, and the VSG Biogas Fund, resulting in an effective payback period for qualifying projects that is materially lower than under the earlier framework.[1]Swiss Federal Office of Energy, “Funding Guidelines for Biomethane Plants under the CO2 Act,” Swiss Federal Office of Energy, bfe.admin.ch The rule also excludes existing KEV, feed-in tariff, and market premium recipients, forcing operators to choose between legacy support and the new grid injection route, which is speeding the move away from CHP-only models in the Switzerland renewable gas from waste market.[2]Swiss Federal Council, “Domestic Biomethane Can Make Switzerland More Independent,” Swiss Federal Administration, admin.ch

PSI Study Confirming Domestic Biomethane Can Cover 25–50% of Future Gas Demand

A Paul Scherrer Institute (PSI) study published in early 2026 found that domestic biomethane from wood residues, green waste, and sewage sludge could cover 25% to 50% of Switzerland’s future gas demand, giving the Switzerland renewable gas from waste market a stronger long-term demand foundation than earlier supply-side debates suggested. The study tied that potential to prior electrification of space heating through heat pumps, because a much smaller gas system would make the remaining demand easier to meet with domestic renewable gas. This means the commercial case improves even without absolute growth in gas consumption, since the addressable share for waste-derived gas rises as conventional gas demand falls. PSI also made clear that Switzerland’s topography and population density limit the role of dedicated energy crops, which keeps the demand case aligned with genuine waste and residue streams. That alignment matters because it gives the Switzerland renewable gas from waste market stronger policy durability than a system built around crop-based feedstock would likely receive.

Revised Energy Promotion Ordinance Support for Waste-Based Plants

The revised EnFV, fully effective under the updated Energy Act in January 2025, replaced the older KEV tariff logic with a reference plant system that combines investment contributions with an operating cost contribution paid per kilowatt-hour. For agricultural biomass plants using slurry, manure, and organic residues, the operating cost contribution can reach CHF 29 cents per kWh (USD 36.7 cents per kWh), which is the highest support tier in the framework. Investment support for qualifying winter-producing waste-based plants can cover up to 60% of eligible costs, sharply reducing capital risk for smaller community-scale digesters in colder cantons. Plants that shift from electricity generation to biomethane grid injection can still receive a 15% contribution toward equipment upgrades, making retrofits more viable across the installed plant base of the Switzerland renewable gas from waste market. Pronovo AG now administers these contributions alongside the national HKN renewable gas tracking system, which establishes an auditable link between production, certification, and end use.

Rising Renewable Gas Demand in Heavy Transport and Municipal Networks

The Switzerland renewable gas from waste market is also gaining support from demand channels that do not depend directly on production subsidies. PSI research on heavy-duty transport showed that liquefied biogas used in heavy goods vehicles delivers well-to-wheel emissions that are much lower than those of fossil diesel and LNG. Battery-electric and fuel-cell trucks remain exempt from the LSVA until 2029. Yet that deadline is pushing logistics operators to consider biomethane options for routes where full electrification remains expensive or difficult to deploy. Municipal energy networks constitute a second demand channel because cantonal energy laws are pressuring utilities to increase the share of renewable gas in their sales without replacing existing infrastructure. Energie 360° raised the renewable share in its direct energy sales to 27% in 2024 and was moving toward a 30% target for 2025, with biomethane expansion as a central tool. Together, heavy transport and municipal networks provide the Switzerland renewable gas from waste market with a demand base that remains relevant even as the support system changes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| No Federal Gas Market Act for Grid Connection Cost Allocation | -1.5% | National | Medium term (2-4 years) |

| Uncertainty During KEV Feed-in Tariff Phaseout | -1.2% | National | Medium term (2-4 years) |

| Alpine Topography and Dispersed Feedstock Raising Logistics Costs | -0.9% | Rural and Alpine cantons | Long term (≥ 4 years) |

| Imported Biogas Not Recognized as Renewable Under Current Customs Rules | -0.7% | National, affecting import-dependent suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

No Federal Gas Market Act for Grid Connection Cost Allocation

The strongest structural restraint in the Switzerland renewable gas from waste market comes from legislation rather than technology. Switzerland still lacks a unified federal Gas Market Act, and the current legal basis remains the 1963 Pipelines Act, which only requires transport when it is technically and economically feasible. The Federal Council reopened the issue in September 2025 through a revised draft of the Gas Supply Act that proposed regulated grid access, a market zone operator, and a broader energy regulator, with consultation closing in December 2025. SVGW opposed that draft in December 2025, arguing that it could create additional legal uncertainty and slow the development of renewable gas infrastructure. Until a final law is approved, producers and grid operators must still negotiate access and cost allocation on a case-by-case basis, which gives larger utility-linked players an advantage over smaller independent and agricultural developers in the Switzerland renewable gas from waste market.

Uncertainty During KEV Feed-in Tariff Phaseout

The second major restraint is the transition from the older KEV support structure to the new contribution-based model. Around 320 biomass plants, including waste-based biogas facilities, still receive KEV support, and many plants that entered the system between 2015 and 2019 will see support expiry between 2030 and 2034. Operators that want access to the new framework must opt out of KEV, and entry into the CO2 Act investment route blocks a return to KEV for 10 years. That creates a pause risk for operators that are unsure whether sliding market premiums and spot market revenues will fully cover conversion costs for a move from CHP to grid injection. The reference market price for biomass electricity was CHF 128.62 per MWh (USD 162.8 per MWh) in the first quarter of 2025, suggesting that market revenue alone does not eliminate investment risk for smaller plants in the Swiss renewable gas-from-waste market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Municipal Waste Anchors the Base, Food Residues Lead the Next Wave

In the Switzerland renewable gas from waste market, municipal solid waste accounted for 31.7% of the feedstock mix in 2025, making it the largest single input stream and the clearest base-load source for near-term project economics. This lead comes from dense urban collection systems and long-established source separation practices in cantons such as Zurich, Bern, and Basel-City, where biowaste already moves through organized municipal channels. Sewage sludge and industrial organic waste add stable volumes to the Switzerland renewable gas from waste market because both streams are linked to existing treatment and processing systems rather than discretionary collection behavior. Swiss wastewater treatment plants already produce 90 million cubic meters of biogas each year, and assessed output could rise by more than 20% through technology optimization.

Food waste is the fastest-growing feedstock in the Switzerland renewable gas from waste market and is projected to expand at an 8.8% CAGR from 2026 to 2031. That rise reflects stronger diversion of organic waste from households and food processing, where industrial wastewater and residue streams still include 660 GWh per year of underused biogas potential. Agricultural residues and animal manure represent a large untapped resource, as Switzerland has 40,000 farms but only 110 manure-based anaerobic digestion plants, which currently contribute only 1.2% of national gas consumption, against a sustainably achievable methane potential of 27,000 terajoules. Landfill gas remains marginal because Switzerland has effectively banned the landfilling of organic waste since the 1990s, so future growth in the Swiss renewable gas from waste industry will depend more on mobilizing dispersed farm and food processing streams than on expanding landfill recovery.

By Technology: Anaerobic Digestion Dominates Today, Upgrading Redefines the Economics

Anaerobic digestion accounted for 44.4% of the technology mix in 2025, so it remains the dominant production route in the Switzerland renewable gas from waste market. The installed base comprises more than 100 organic waste biogas plants and around 110 agricultural facilities, providing a much deeper operational foundation for digestion than any thermochemical route. Dry fermentation has been especially important in Switzerland because it suits solid feedstocks such as green waste and biowaste and is widely associated with the KOMPOGAS process licensed by Hitachi Zosen Inova.[3] IEA Bioenergy Task 37, “Case Story, Limeco Switzerland, Power to Gas and Biomethanation in Dietikon,” IEA Bioenergy Task 37, task37.ieabioenergy.com Landfill gas recovery contributes only a limited output because the feedstock base is constrained by longstanding waste policy.

Biogas upgrading systems are the fastest-growing technology category and are projected to expand at a 10.9% CAGR through 2031. The reason is straightforward: upgrading raises the biogas's methane content from a typical range of 55% to 65% to grid-quality biomethane above 97%, which opens access to gas network sales, transport fuel markets, and new federal support. Gasification and pyrolysis remain pre-commercial at scale, while wood gasification and power-to-gas methanation are still led by research and pilot work rather than broad deployment. The funding model itself now strengthens this trend because reference plant calculations make upgrading system costs more visible and more central to contribution levels across the Switzerland renewable gas from waste market.

By Gas Type: Biomethane/Renewable Natural Gas (RNG) Leads Segment Growth

Biomethane/Renewable Natural Gas (RNG) held 60.8% of the Switzerland renewable gas from waste market share in 2025, making it the leading gas type segment in the market. This combined position reflects the strong commercial preference for gas formats that can be moved into grid injection and transport applications, with lower integration barriers than raw biogas. Switzerland’s policy support also favors upgraded, certifiable renewable gas output, thereby strengthening the role of biomethane and RNG within the existing gas network. The segment is projected to grow at a 11.8% CAGR through 2031, supported by rising grid injection and transport fuel demand.

The growth outlook for this segment is supported by its wider strategic role in Switzerland’s gas decarbonization path. Biomethane remains the most immediate route for replacing fossil gas in distribution networks, while RNG adds longer-term value through power-to-gas pathways that can use surplus renewable electricity and captured CO2. This gives the segment a broader operating logic than unconverted biogas, which is still more closely tied to on-site CHP use at plants that have not yet shifted to upgrading. Syngas remains a smaller commercial category because it is still used mainly as an intermediate output within thermochemical conversion processes rather than as a directly marketed gas stream. As the national HKN system becomes more central to certification and traceability, biomethane and RNG are likely to keep gaining importance because they fit most directly with auditable supply, grid compatibility, and supplier compliance needs.

By Application: Grid Injection Dominates, Transportation Fuel Accelerates Sharply

Grid injection accounted for 32.8% of the Switzerland renewable gas from waste market in 2025, making it the largest application. This route is commercially attractive because it uses the existing gas system rather than requiring dedicated distribution assets or changes in end-user equipment. It also aligns with the new support design because federal contributions are explicitly tied to plants that upgrade to injection-quality and either inject into the network or use gas locally as fuel. CHP retains a meaningful installed base, but its relative weight is declining because post-KEV economics favor higher-value biomethane pathways.

Transportation fuel is the fastest-growing application and is projected to grow at a 12.6% CAGR through 2031. The segment is being lifted by stronger interest in liquefied biomethane for heavy transport, especially on long routes and in applications with high payload requirements, where full electrification is difficult. Federal research in 2025 confirmed that liquefied biomethane can deliver strong lifecycle emission advantages, which improves its position in freight decarbonization planning. Industrial, residential, and commercial heating are also rising, supported by cantonal requirements for higher renewable gas content. Still, the strongest capital pull in the Switzerland renewable gas from waste market is now toward injection and transport use.

By Component: Processing Infrastructure Drives Capital Deployment, Smart Systems Scale Fast

Gas processing and upgrading units accounted for 33.2% of component demand in 2025, making them the largest investment category in the Swiss renewable gas-from-waste market. This reflects the shift from raw biogas use in CHP systems to higher-purity biomethane for network injection and transport fuel applications. Pressure swing adsorption and membrane-based systems are the most visible technology paths, and the Dietikon site showed this trend with a CO2 membrane unit installed in February 2024. Digesters and fermentation systems remain the second-largest component group, with increasing standardization in dry fermentation plant design.

Monitoring and control systems are the fastest-growing component segment and are projected to expand at a 10.5% CAGR through 2031. The demand stems from two linked needs: auditable metering for tracking and cost support, and process control to improve gas yield stability. Compressors and storage systems also remain essential because injection into local networks often requires pressure boosts of 5 bar or more at new entry points such as Aarberg. This means component spending in the Switzerland renewable gas from waste market is no longer centered only on digestion vessels, but increasingly on the digital and mechanical layers that qualify output for higher-value markets.

Geography Analysis

In 2026, the Switzerland renewable gas from waste market stands at USD 0.43 billion, but its internal buildout is uneven across the country rather than evenly distributed by canton. Production is concentrated in the German-speaking cantons, especially Zurich, Aargau, Bern, Lucerne, and St. Gallen, where biowaste collection is well established and access to the gas network is more straightforward. The national energy authority recorded 1,700 terajoules of biogas injected into the Swiss gas distribution system in 2024, up from 1,580 terajoules in 2023, which represented 7.6% year-on-year growth before the new 2025 federal support regime had fully worked through the project pipeline. That pattern shows that the Switzerland renewable gas from waste market was already building momentum before the latest policy changes took effect. Urban centers in these cantons also host the densest municipal energy networks, so grid injection economics are strongest where pipeline density and waste availability overlap.

Romandy, including Vaud, Geneva, and Fribourg, is an emerging growth zone for the Switzerland renewable gas from waste market because the resource base is larger than the current waste-to-gas asset base. Regional utilities are active in renewable gas development, yet plant density in the French-speaking region remains below the Swiss average. The Alpine and pre-Alpine cantons, including Uri, Graubünden, and Valais, face higher logistics costs because feedstock is more dispersed and terrain raises transport complexity. Switzerland’s topography and population density also prevent large-scale cultivation of energy crops, which keeps alpine projects tied to local residues rather than alternative feedstocks. As a result, these cantons either need small local digesters linked to farm waste or must rely on biomethane produced in lower-altitude urban areas and moved through the grid.

Within Europe, Switzerland’s renewable gas share, including biomethane certificates, stood in the 6% to 8% range of total gas consumption, putting Switzerland's renewable gas from waste market ahead of the broader European Union average in penetration. Switzerland still trailed frontrunners such as Denmark and Germany because it lacks a formal bilateral framework for CO2 credit transfers for renewable gas with the European Union. That gap limits the ability to count imported biomethane toward domestic obligations, thereby reducing buyers' supply flexibility. At the same time, it supports a premium for domestic production and strengthens the commercial position of Swiss producers in the Swiss renewable gas-from-waste market.

Competitive Landscape

The Switzerland renewable gas from waste market is moderately consolidated around a group of established utility-linked operators, specialized biogas producers, agricultural cooperatives, and waste management companies that collectively control a significant share of the country’s renewable gas production and supply infrastructure. Major participants have strengthened their positions through integration across feedstock procurement, anaerobic digestion, biomethane upgrading, certificate management, and renewable gas commercialization. This integrated operating model reduces supply risk and provides an advantage in securing long-term feedstock contracts and grid access. Smaller independent developers continue to face challenges related to feedstock availability, project financing, and infrastructure access; however, the national renewable gas tracking system introduced in January 2025 has improved market transparency and enabled independent producers to participate more effectively in renewable gas certificate trading.

The strongest growth opportunities remain in agricultural manure digestion and organic waste valorization, where Switzerland has substantial untapped feedstock potential. Companies with strong agricultural partnerships and regional waste collection networks are increasingly positioned to expand production capacity. Another emerging opportunity lies in power-to-gas methanation, where projects such as the Dietikon biomethanation facility have demonstrated the potential to improve renewable gas output and operational flexibility. Competition for high-quality organic waste streams, manure, and agricultural residues is increasing, making reliable feedstock sourcing and long-term supply agreements important competitive differentiators. The EnFV incentives for agricultural biomass further support producers that prioritize waste-based feedstocks and maintain certified renewable gas traceability.

Recent strategic developments illustrate how market participants are strengthening their positions in the Switzerland renewable gas from waste market. New investments in biomethane upgrading, grid-injection facilities, and organic waste processing plants are expanding domestic renewable gas supply. The Aarberg biomethane project, which converted CHP-based biogas generation into grid-injection renewable gas and secured long-term offtake agreements, demonstrates the increasing shift toward higher-value biomethane commercialization. Additionally, investments in local processing infrastructure and pipeline connections are enabling producers to improve supply efficiency and integrate more renewable gas into regional networks. Continuous improvements in upgrading technologies, including CO₂ membrane separation systems demonstrated at the Dietikon power-to-gas project, are further improving plant efficiency and supporting the long-term competitiveness of Swiss renewable gas producers.

Switzerland Renewable Gas From Waste Industry Leaders

Energie 360° AG

Axpo Biomasse AG

Ökostrom Schweiz AG

Swiss Farmer Power Inwil AG

AVAG Umwelt AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Axpo officially announced on 31 March 2026 that Axpo Kompogas Wauwil AG plans to build a new biogas upgrading plant to replace the CHP system. The project involves an investment of ~CHF 3 million, 11.4 GWh/year of biomethane production, a pipeline connection to EWL, and cooperation with Wauwiler Champignons AG.

- February 2026: Axpo announced that the Aarberg fermentation plant replaced its CHP unit with a biomethane upgrading facility. EWB signed a full-offtake agreement. Gas is injected via Seelandgas AG, while GVM is building a pressure-boosting station. The facility processes approximately 20,000 tons of biomass per year.

Switzerland Renewable Gas From Waste Market Report Scope

| Municipal Solid Waste (MSW) |

| Agricultural Residues |

| Animal Manure |

| Industrial Organic Waste |

| Sewage Sludge |

| Food Waste |

| Others |

| Anaerobic Digestion |

| Landfill Gas Recovery |

| Gasification |

| Pyrolysis |

| Biogas Upgrading Systems |

| Others |

| Biogas |

| Biomethane/Renewable Natural Gas (RNG) |

| Syngas |

| Electricity Generation |

| Combined Heat & Power (CHP) |

| Grid Injection |

| Transportation Fuel |

| Industrial Heating |

| Residential & Commercial Heating |

| Others |

| Gas Collection Systems |

| Digesters & Fermentation Systems |

| Gas Processing & Upgrading Units |

| Compressors & Storage Systems |

| Power Generation Equipment |

| Monitoring & Control Systems |

| Others |

| By Feedstock | Municipal Solid Waste (MSW) |

| Agricultural Residues | |

| Animal Manure | |

| Industrial Organic Waste | |

| Sewage Sludge | |

| Food Waste | |

| Others | |

| By Technology | Anaerobic Digestion |

| Landfill Gas Recovery | |

| Gasification | |

| Pyrolysis | |

| Biogas Upgrading Systems | |

| Others | |

| By Gas Type | Biogas |

| Biomethane/Renewable Natural Gas (RNG) | |

| Syngas | |

| By Application | Electricity Generation |

| Combined Heat & Power (CHP) | |

| Grid Injection | |

| Transportation Fuel | |

| Industrial Heating | |

| Residential & Commercial Heating | |

| Others | |

| By Component | Gas Collection Systems |

| Digesters & Fermentation Systems | |

| Gas Processing & Upgrading Units | |

| Compressors & Storage Systems | |

| Power Generation Equipment | |

| Monitoring & Control Systems | |

| Others |

Key Questions Answered in the Report

What is the expected value of Switzerland renewable gas from waste by 2031?

The Switzerland renewable gas from waste market is expected to reach USD 0.62 billion by 2031 from USD 0.43 billion in 2026, growing at a 7.59% CAGR.

Which feedstock currently leads renewable gas production from waste in Switzerland?

Municipal solid waste led with a 31.7% share in 2025 because Switzerland already has dense urban collection and source separation systems.

Which application is growing fastest in Switzerland renewable gas from waste?

Transportation fuel is projected to grow fastest at a 12.6% CAGR through 2031, supported by interest in liquefied biomethane for heavy-duty transport.

Why is Biomethane/Renewable Natural Gas (RNG) gaining importance in Switzerland?

Biomethane/Renewable Natural Gas (RNG) held 46.5% of output in 2025 because it fits grid injection, supplier decarbonization needs, and the new federal support model.

What is the biggest policy support for new biomethane plants in Switzerland?

The revised CO2 framework that took effect in January 2025 created a dedicated investment contribution for new and expanded biomethane plants tied to grid quality upgrading and injection or local fuel use.

Where does the strongest untapped supply potential sit in Switzerland?

Agricultural manure and slurry remain the largest underused resource base, with PSI estimating a sustainably achievable methane potential of 27,000 terajoules.

Page last updated on: