Finland Renewable Gas From Waste Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

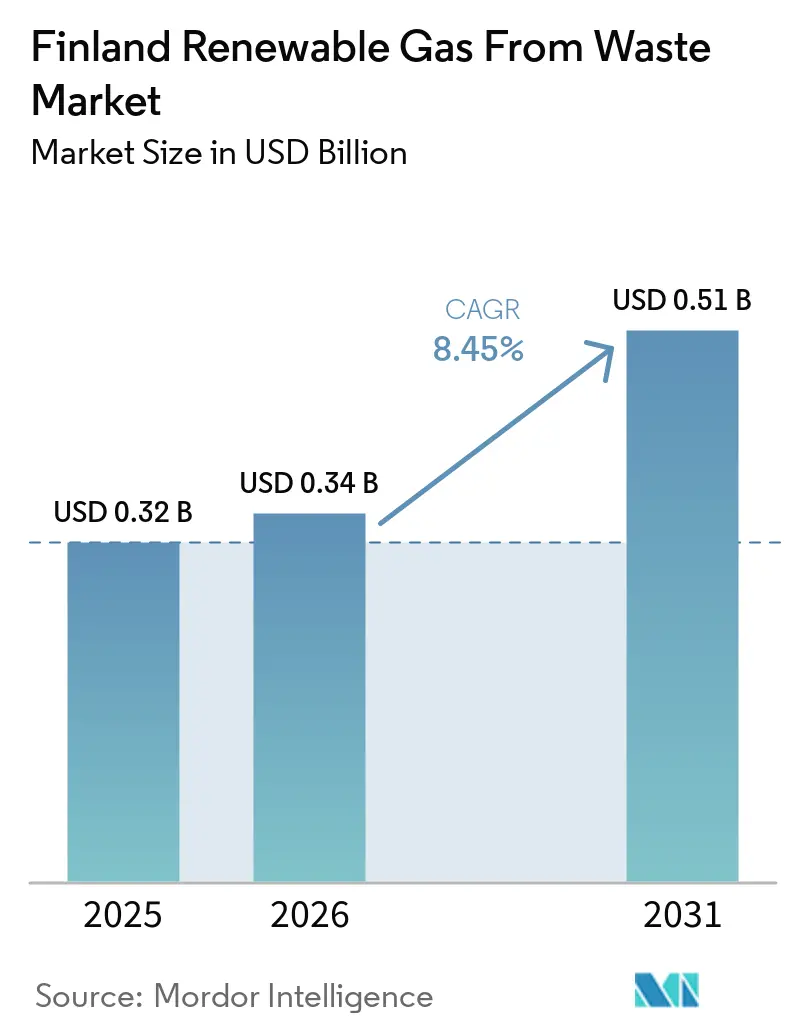

| Base Year Market Size (2025) | USD 0.32 Billion |

| Market Size (2026) | USD 0.34 Billion |

| Market Size (2031) | USD 0.51 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

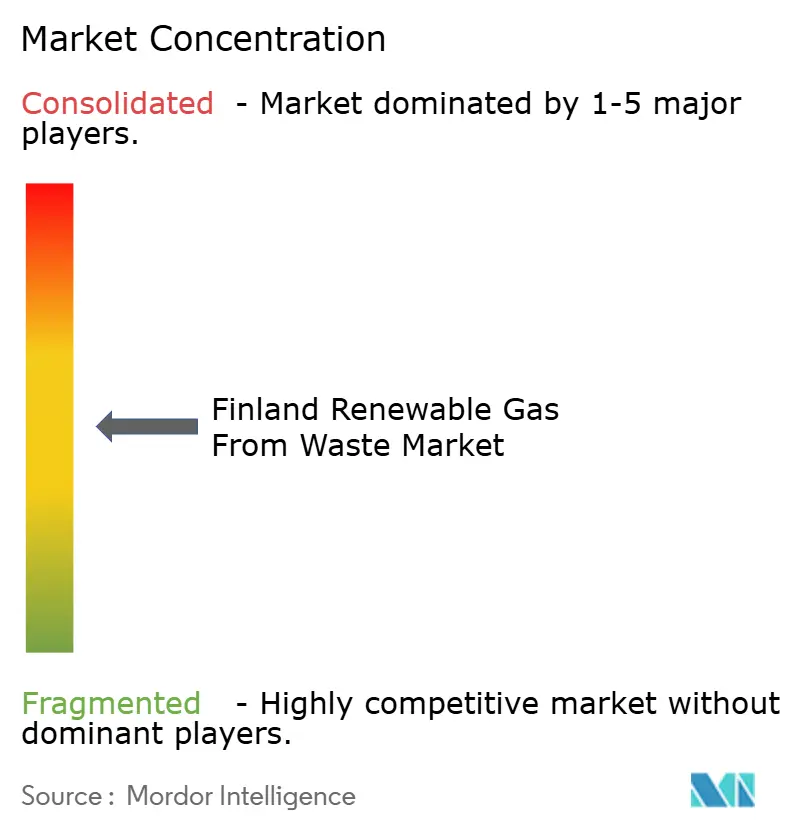

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finland Renewable Gas From Waste Market Analysis by Mordor Intelligence

The Finland Renewable Gas From Waste Market size is expected to grow from USD 0.32 billion in 2025 to USD 0.34 billion in 2026 and is forecast to reach USD 0.51 billion by 2031 at 8.45% CAGR over 2026-2031.

The favorable outlook for the Finland renewable gas from waste market reflects a stronger policy base, deeper public funding support, and a transport sector moving away from fossil gas toward renewable alternatives. Biomethane’s inclusion in Finland’s biofuel distribution obligation in 2022 created a legally enforceable demand floor, improving revenue visibility for new projects and reducing financing risk for developers. Public support also moved from pilot-scale to larger project backing, with energy aid for clean energy projects from 2022 to 2024, and major grants continuing in 2025. This support helped shift the Finland renewable gas from waste market toward larger plants, liquefaction, and upgrading capacity rather than small local heat-only assets. Domestic supply still trails demand in the Finland renewable gas from waste market, as biogas guarantees of origin imported into Finland rose by 86% in 2024 to nearly 450 GWh and continued to rise by 20% year on year in the first quarter of 2025, showing that buyers are already sourcing beyond domestic output. A second demand channel is now in place through FuelEU Maritime. At the same time, the lack of a dedicated biomethane production target in Finland’s updated NECP (National Energy and Climate Plan) still leaves part of the long-term regulatory signal incomplete for projects with long asset lives.

Key Report Takeaways

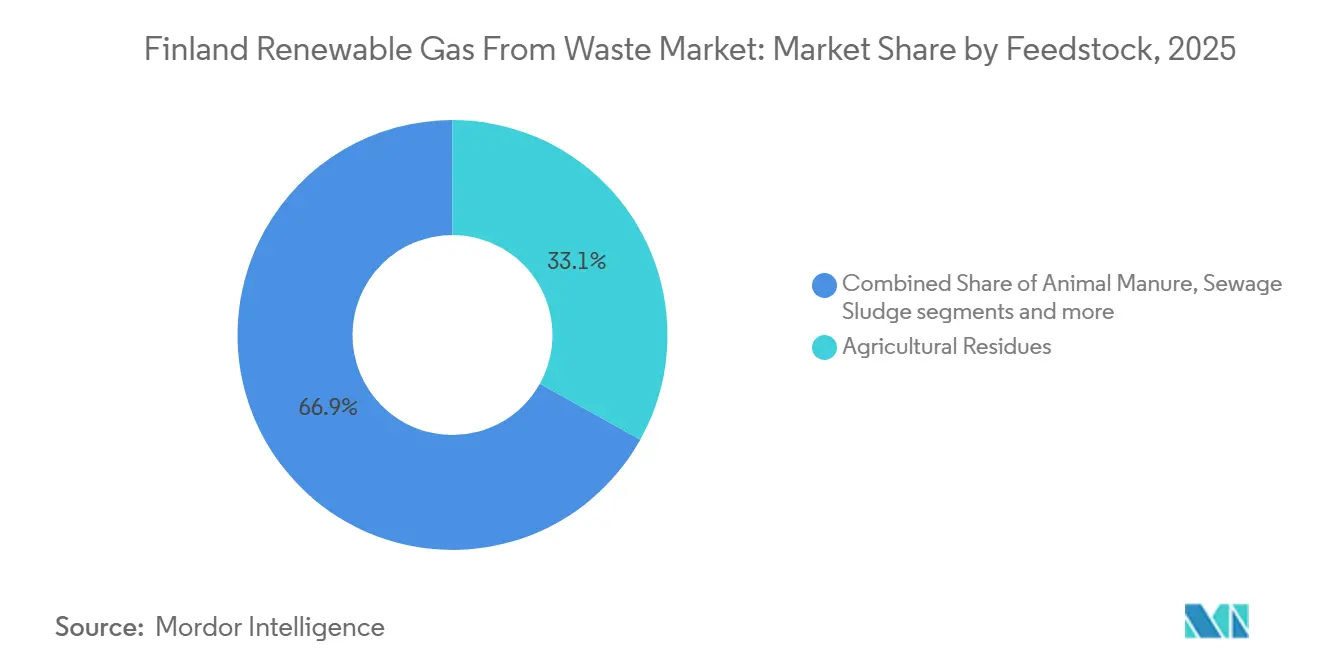

- By feedstock, agricultural residues held 33.1% of the Finland renewable gas from waste market share in 2025, while food waste is forecast to grow at a CAGR of 9.4% through 2031.

- By technology, anaerobic digestion accounted for 41.7% of the Finland renewable gas from waste market size in 2025, while gasification is projected to grow at a CAGR of 11.5% through 2031.

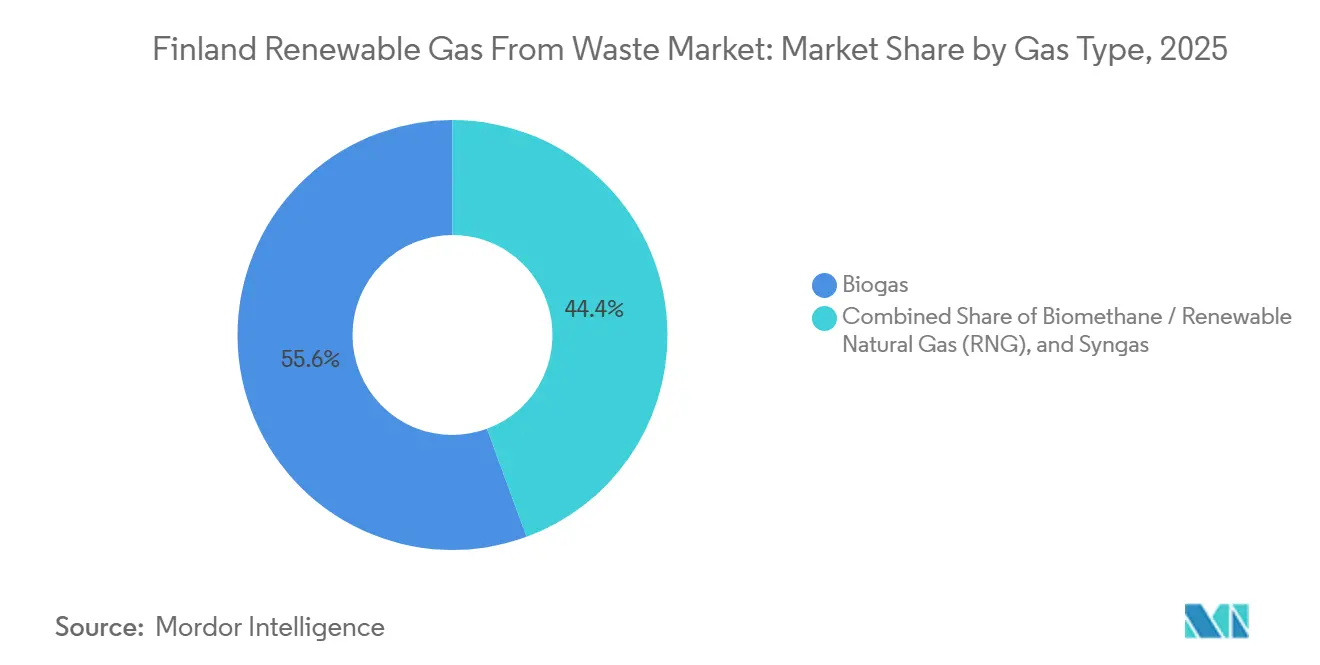

- By gas type, biogas captured 55.6% of the market in 2025, while biomethane / renewable natural gas is expected to record the fastest growth at 12.6% through 2031.

- By application, combined heat & power (CHP) led with a 36.2% share in 2025, while transportation fuel is projected to grow at a CAGR of 13.0% through 2031.

- By component, digesters and fermentation systems held 29.5% of the market in 2025, while gas processing and upgrading units are expected to advance at 11.2% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Finland Renewable Gas From Waste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Finland's Biogas Sector Vision Targeting 4 TWh Production by 2030 is Supporting Investment Activity | +2.2% | National, with early gains in Northern Ostrobothnia and Central Finland | Short term (≤ 2 years) |

| Up to 50% State Investment Subsidies for Biogas Plant Construction Lowering Entry Barriers | +1.8% | National, concentrated in agricultural regions such as Ostrobothnia and South Ostrobothnia | Medium term (2-4 years) |

| European Union REPowerEU Biomethane Targets Aligning with and Reinforcing Finland's National Policy | +1.5% | National, with spillover to Nordic and Baltic export markets | Long term (≥ 4 years) |

| Biomethane Inclusion in National Biofuel Blending Obligation Since 2022 Boosting Transport Demand | +1.0% | National, concentrated in the Helsinki-Tampere-Oulu transport corridor | Medium term (2-4 years) |

| Surging Liquefied Biogas (LBG) Demand in Heavy Road Transport and Maritime Shipping | +0.8% | National road corridors and Baltic Sea ports | Medium term (2-4 years) |

| 86% Rise in Biogas Guarantee of Origin Imports in 2024 Signaling Strong Market Demand | +0.5% | National, concentrated in industrial and district heating clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Finland's Biogas Sector Vision Targeting 4 TWh Production by 2030 is Supporting Investment Activity

Finland’s 4 TWh biogas production target by 2030 remains one of the strongest signals of demand and capacity in the Finland renewable gas from waste market. The target was backed in 2024 through the Biokaasuvisio2030 declaration, which was signed by Bioenergia ry, MTK, and other sector bodies, giving the goal broader cross-industry support rather than leaving it as a narrow policy statement. The importance of this target exceeds its numerical value because it frames the next phase of plant construction, feedstock contracting, and grid or liquefaction investment across the value chain. Finland’s technical-economic production potential still stands at nearly 10 TWh per year, so the 2030 target does not signal saturation and instead points to a longer runway for the Finland renewable gas from waste market. This gap between current ambition and broader potential supports staged investment opportunities for producers, technology suppliers, and infrastructure operators through the rest of the decade.

Up to 50% State Investment Subsidies for Biogas Plant Construction Lowering Entry Barriers

State aid has become a major cost bridge for new projects in the Finland renewable gas from waste market. Between 2022 and 2024, the Ministry of Economic Affairs and Employment directed EUR 469 million (USD 551.7 million) in European Union Recovery and Resilience Facility energy aid to 77 clean energy projects, with a significant share tied to biogas plant construction. Individual awards have already reached EUR 26 million (USD 30.6 million) for Nivala Biokaasu, EUR 19.2 million (USD 22.6 million) for Suomen Lantakaasu’s Kiuruvesi facility, and EUR 28 million (USD 32.9 million) for Nordic Ren-Gas’s methanation demonstration project in Lahti. In June 2025, the Finnish Ministerial Finance Committee approved another EUR 49.5 million (USD 58.2 million) for three new demonstration projects, including EUR 11.6 million (USD 13.6 million) for Lännen Biokaasu’s liquefied biomethane plant in Kurikka. Beyond capacity expansion, subsidies are accelerating the commercialization of emerging technologies but also helping normalize first-of-their-kind technologies such as methanation, high-solids digestion, and integrated CO2 handling, which should improve replication economics in the Finland renewable gas from waste market.

European Union REPowerEU Biomethane Targets Aligning with and Reinforcing Finland's National Policy

European Union policy is reinforcing Finland’s domestic growth path for the renewable gas from waste market. The REPowerEU Plan set a target of 35 billion cubic meters of biomethane production across European Union member states by 2030, which raised the policy cost of delay and created a clearer regional demand framework for producers across Europe. For Finland, this matters because guarantees of origin issued through the EECS (European Energy Certificate System) framework administered by Gasgrid Finland can support cross-border trade with other AIB (Association of Issuing Bodies) member states. The European Commission also stated in its June 2024 Council Recommendation that Finland should take further measures to promote sustainable biomethane production, adding another layer of policy pressure to future planning rounds. This alignment gives the Finland renewable gas from waste market a stronger export case while strengthening the local policy signal.

Biomethane Inclusion in National Biofuel Blending Obligation Since 2022 Boosting Transport Demand

Transport policy has moved renewable gas from a voluntary option to a compliance fuel in the Finland renewable gas from waste market. Finland included biomethane in the national biofuel distribution obligation on 1 January 2022, allowing fuel distributors to use it toward compliance rather than treating it solely as a niche decarbonization product. The obligation rises from 19.5% in 2026 to 34% by 2030, and the advanced biofuel sub-quota reaches 10% by 2030, which supports waste-based biomethane from eligible feedstocks. This change improved project bankability because lenders can now underwrite offtake against a visible legal demand floor rather than relying solely on voluntary purchases. Finland reduced the blending obligation during 2022 and 2023 to address fuel price pressures. However, the pathway from 2024 onward restored the broader direction and confirmed that demand support in the Finland renewable gas from waste market remains structurally intact.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Current Output of ~1 TWh Far Below 10 TWh Theoretical Production Potential | -1.3% | National, most visible in regions lacking processing infrastructure | Long term (≥ 4 years) |

| Geographically Dispersed Feedstock Raising Logistics Costs and Reducing Plant Profitability | -0.9% | National, especially in sparsely populated agricultural areas such as Lapland, North Ostrobothnia, and Kainuu | Medium term (2-4 years) |

| Unstable Policy Environment and Insufficient Long-Term Incentives Dampening Investor Confidence | -0.6% | National | Medium term (2-4 years) |

| Limited Biomethane Infrastructure and Grid Connectivity | -0.5% | National, affecting EU coordination and cross-border investment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Current Output of ~1 TWh Far Below 10 TWh Theoretical Production Potential

The Finland renewable gas from waste market remains supply-constrained. Finland produced 3,359 TJ of biogas in 2024, equivalent to 0.93 TWh, which was less than 10% of the country’s estimated 10 TWh technical-economic production potential. The feedstock mix is also shifting, with on-farm agricultural waste facilities increasing output by 14% in 2024 while landfill sites declined by 18% as older disposal assets lost gas-producing organic loads. This explains why new project announcements alone do not remove the bottleneck, because the timing gap between the project pipeline and producing assets still limits available domestic volumes. As a result, the Finland renewable gas from waste market is currently unable to capture all local value from rising demand and has had to rely on imports to fill the shortfall.

Geographically Dispersed Feedstock Raising Logistics Costs and Reducing Plant Profitability

Feedstock location remains a structural cost issue in the Finland renewable gas from waste market. Finland has strong aggregate availability of manure, crop residues, municipal biowaste, and forestry side streams, but those resources are spread across a large land area with low population density outside the main corridors. The European Parliament Research Service noted in 2026 that the binding issue in markets such as Finland is not only feedstock volume but also the cost and coordination required to aggregate enough material at a single site for efficient biomethane production. For larger plants, transport can absorb a meaningful share of operating costs when local concentration is low, reducing the number of locations that can support industrial-scale economics. This makes plant siting and feedstock clustering central to project viability across the Finland renewable gas from waste market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Agricultural Roots, Food Waste Frontier

Agricultural residues accounted for 33.1% of the Finland renewable gas from waste market share in 2025, making them the largest feedstock base by value. This position reflects Finland’s large agricultural base and the policy focus on better use of manure and other farm side streams within domestic biogas expansion. The national energy strategy states that Finland has around 20 million tonnes of biogas-suitable feedstocks available each year, and a large share of that volume comes from agricultural sources, giving this segment a strong structural role in the Finland renewable gas from waste market. European Union sustainability rules also strengthen the position of waste-derived agricultural inputs, as they align with the compliance logic that supports premium treatment for low-carbon fuels and certified gas.

Municipal solid waste, sewage sludge, and industrial organic waste remain important to the Finland renewable gas from waste industry because they support established co-processing assets and wastewater-linked production. Co-processing plants produced 1,782 TJ of biogas in 2024, up 6% from the prior year, while wastewater treatment plants added 750 TJ, indicating that municipal and industrial waste streams remain a stable production base even as the investment narrative shifts toward agricultural expansion. Food waste is forecast to grow at a CAGR of 9.4% through 2031, driven by expanding separate collection obligations and circular economy measures that improve the consistency of incoming biowaste volumes. Landfill waste is moving in the opposite direction because Finland’s landfill diversion policies are reducing the amount of organic material sent to disposal sites, shrinking the long-term role of landfill gas and redirecting capital toward purpose-built digestion assets.

By Technology: Digestion Dominates, Gasification Gains Altitude

Anaerobic digestion accounted for 41.7% of the Finland renewable gas from waste market in 2025, keeping it clearly ahead of other technology pathways. Its leading position stems from extensive operating experience in municipal co-processing plants, farm digesters, and wastewater-linked facilities, all of which align with Finland’s dominant feedstock streams. The installed base also benefited from known upgrading routes and lower execution risk compared with less mature conversion routes. Doranova’s Vesilahti-Lempäälä Biopower project shows how this part of the Finland renewable gas from waste market is still improving in performance, with high-solids digestion and planned biogenic CO2 liquefaction extending revenue options beyond methane alone.

Gasification is projected to grow at 11.5% through 2031, making it the fastest-expanding technology segment. The main reason is that gasification opens access to woody residues and other materials that are less suitable for standard biological digestion, which matters in Finland because forestry side streams remain an important resource base. The Wood2Biogas project, piloted in Finland between 2022 and 2024, demonstrated the technical feasibility of combining gasification with digestion to produce biochar, broadening the use case for mixed residue systems. Landfill gas recovery is likely to keep losing ground as waste policy shifts away from disposal. At the same time, pyrolysis and upgrading systems continue to gain commercial attention as the Finland renewable gas from waste market moves toward grid-quality gas and higher-value transport use.

By Gas Type: Biogas Foundation, Biomethane / Renewable Natural Gas (RNG)

Biogas retained the largest share of the Finland renewable gas from waste market at 55.6% in 2025, reflecting the broad installed base of co-processing plants, farm digesters, and wastewater facilities serving heat and power needs. Finland produced 3,359 TJ of biogas in 2024, and only 9% was flared, down from 11% in 2023, indicating tighter demand and better use of output than in the prior year. This raw biogas base still underpins the current economics of the Finland renewable gas from waste market because many operating assets were built around CHP or local energy use rather than premium fuel markets. Even so, its share is likely to narrow over time as more plants add upgrading systems and move into certified biomethane.

Biomethane / renewable natural gas is forecast to grow at 12.6% through 2031, the fastest rate among gas types in the Finland renewable gas from waste market. The strongest immediate proof of this demand comes from the import side, where Finland brought in nearly 450 GWh of biogas guarantees of origin in 2024, up 86% from 2023, and first-quarter 2025 volumes were already 20% above the prior-year period. Syngas remain smaller emerging category, with commercial momentum tied mainly to Power-to-Gas projects rather than to the current digestion base. Nordic Ren-Gas and Gasum agreed that Gasum would purchase 160 GWh per year of e-methane from the Tampere plant beginning in 2026, which gives the Finland renewable gas from waste market a repeatable template for future projects that combine novel production pathways with long-term offtake.

By Application: CHP Incumbency, Transport Fuel Disruption

Combined Heat & Power (CHP) held the largest share at 36.2% in 2025, reflecting the historical fit between biogas production and Finland’s district heating and local industrial heat networks. This use case provided steady baseload demand and helped many earlier projects reach commercial viability before the shift toward transport-grade biomethane took hold. Nevel’s Finnish biogas operations in Lahti, Forssa, Pori, and Juuka demonstrate that established assets in the Finland renewable gas from waste market have long supplied industrial and municipal customers through heat-linked models. CHP, therefore, remains the incumbent application even as newer investments increasingly target upgraded gas and liquefaction.

Transportation fuel is projected to grow at 13.0% through 2031, making it the fastest-growing application in the Finland renewable gas from waste market. The demand case rests on 3 linked supports: the distribution obligation, heavy-duty fleet adoption, and FuelEU Maritime, which started creating an additional compliance-based outlet for low-carbon gas from January 2025. This is important because transport-grade biomethane and LBG usually deliver higher realized prices than raw biogas sold into local heat systems. Grid injection, industrial heating, and residential and commercial heating are also expanding as more producers install upgrading units and seek certified pipeline-quality gas, which broadens the end-market mix for the Finland renewable gas from waste market.

By Component: Digesters at the Core, Upgrading Units Scaling Fast

Digesters and fermentation systems accounted for the largest segment, with a 29.5% share in 2025, keeping them at the center of capital spending in the Finland renewable gas from waste market. The main reason is straightforward: anaerobic digestion remains the dominant production route, and new plant programs still require large primary process equipment even when downstream upgrading becomes more important. Large Finnish projects in Kiuruvesi, Nivala, and Vesilahti illustrate this shift toward industrial-scale equipment, including thermophilic and high-solids systems built to handle larger feedstock volumes and support biomethane-oriented business models. This component base shows how the Finland renewable gas from waste industry is moving away from scattered, farm-scale units toward larger, integrated assets.

Gas processing and upgrading units are expected to grow at 11.2% through 2031, making them the fastest-rising component category. Their momentum comes from the price premium available for biomethane, the value of guarantees of origin, and the wider customer base that opens once gas reaches pipeline or transport quality. Biovoima’s BIOliquefierCO2 system adds another layer to this shift by capturing and liquefying biogenic carbon dioxide from the upgrading process, creating a second saleable stream from the same plant. Landfill gas collection systems face a weaker outlook as landfill-linked production declines. In contrast, compressors, storage systems, and control equipment should expand in line with overall capacity growth in the Finland renewable gas from waste market.

Geography Analysis

Northern Ostrobothnia has become one of the strongest emerging zones because it combines livestock density, arable land, and manure availability with growing interest in larger biogas plants. The Nivala Biokaasu project is one of the clearest examples of this regional direction, with government-backed support helping position the area for industrial-scale agricultural gas production. This matters because regions with dense manure and residue volumes can support larger plant economics with lower collection complexity than sparsely supplied areas. Northern cluster growth therefore reflects the practical siting logic shaping the Finland renewable gas from waste market.

Central and southwestern Finland form a second cluster that blends agricultural biogas with technology-intensive projects. Tampere stands out through Nordic Ren-Gas’s e-methane program, while Nurmo and Kiuruvesi are linked to Suomen Lantakaasu’s manure-based expansion model. The national alternative fuels distribution infrastructure program, launched in 2024, supports this corridor with funding for biomethane, electricity, and hydrogen infrastructure, which is most useful where refueling density and freight flows are already stronger. These areas show that the Finland renewable gas from waste market is no longer centered solely on waste treatment sites and is now connecting more directly to transport and industrial fuel use.

Southern Finland and the coastal belt function as the maritime-facing side of the Finland renewable gas from waste market. FuelEU Maritime took effect in January 2025 and created a direct compliance channel for LBG and other low-carbon marine fuels on Baltic Sea routes serving Finnish ports. That change gives coastal projects a natural demand advantage because marine fuel buyers are concentrated around the main port network rather than near inland agricultural feedstocks. Eastern Finland remains smaller in strategic weight, but operating assets such as Nevel’s Juuka activity show that regional production outside the main growth corridors still contributes to the national system. Overall, the geography of the Finland renewable gas from waste market is being shaped less by administrative regions and more by the overlap of feedstock density, technology fit, and access to transport or industrial customers.

Competitive Landscape

The Finland renewable gas from waste market is moderately concentrated, with a few larger integrated operators shaping project pipelines, distribution access, and offtake structures. At the same time, many regional producers and specialist technology companies remain active. The main strategic pattern is vertical integration, in which companies seek control over feedstock supply, production, upgrading, and customer delivery rather than competing at only one step in the chain. This can be seen in long-term manure and side-stream sourcing models, investment in liquefaction or upgrading units, and early efforts to secure guaranteed customers before construction. The Finland renewable gas from waste market is also seeing a stronger role for project finance and infrastructure capital as plant sizes move beyond the scale that municipalities and farms typically handled in the past. That shift changes competition because access to capital, permitting capability, and offtake security now matter as much as process know-how.

A second competitive pattern is the use of long-term commercial agreements to reduce risk before projects start operating. Nordic Ren-Gas’s offtake agreement with Gasum for Tampere e-methane from 2026, followed by a letter of intent covering additional output from future plants, shows how demand security is being built into project finance from the beginning. Suomen Lantakaasu is using a different but equally important model, tying feedstock supply to dairy farm networks and building industrial-scale manure projects that can support biomethane, fertilizer products, and biogenic CO2 revenue streams. Nevel strengthened its position in 2024 through the acquisition of Labio’s Lahti business, expanding its portfolio and deepening its exposure to established biogas production and customer relationships. These moves show that scale in the Finland renewable gas from waste market is being built through both new projects and selective consolidation.

Technology providers are also becoming more visible competitive actors in the Finland renewable gas from waste market. Doranova is differentiating through high-solids digestion and planned CO2 liquefaction at the Vesilahti-Lempäälä plant, while Biovoima is positioning around biogenic carbon capture linked to upgrading processes. St1 Biokraft also added a network angle by opening its first 3 Finnish LBG refueling sites in 2024 as part of a broader Nordic buildout strategy. Compliance with RED III (Renewable Energy Directive III)-linked sustainability rules and guarantees of origin access is likely to continue influencing where financing flows, because certified, tradable output gives projects a wider buyer base and stronger revenue quality in the Finland renewable gas from waste market.

Finland Renewable Gas From Waste Industry Leaders

Gasum Oy

Suomen Lantakaasu Oy

Nordic Ren-Gas Oy

St1 Biokraft

Nevel Oy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Suomen Lantakaasu delivered the first manure load to its Nurmo biogas plant, marking the start of industrial-scale manure-based biogas production at the EUR +60 million (USD +70.57 million) facility that will produce biomethane, biofertilizers, and biogenic CO₂.

- June 2025: The Finnish Ministerial Finance Committee approved EUR 49.5 million (USD 58.2 million) in investment aid across three renewable energy demonstration projects, including EUR 11.6 million (USD 13.6 million) for Lännen Biokaasu Oy's liquefied biomethane plant in Kurikka and EUR 27.9 million (USD 32.8 million) for Vanadis Fuels Ab Oy's renewable methanol plant in Kokkola.

Finland Renewable Gas From Waste Market Report Scope

The Finland Renewable Gas From Waste Market is Segmented by Feedstock (Municipal Solid Waste, Food Waste, and More), by Technology (Anaerobic Digestion, Gasification, Pyrolysis, and More), by Gas Type (Biogas, Syngas, and More), by Application (Electricity Generation, Grid Injection, and More), and by Component (Gas Collection, Digesters & Fermentation, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Municipal Solid Waste (MSW) |

| Agricultural Residues |

| Animal Manure |

| Industrial Organic Waste |

| Sewage Sludge |

| Food Waste |

| Others |

| Anaerobic Digestion |

| Landfill Gas Recovery |

| Gasification |

| Pyrolysis |

| Biogas Upgrading Systems |

| Others |

| Biogas |

| Biomethane / Renewable Natural Gas (RNG) |

| Syngas |

| Electricity Generation |

| Combined Heat & Power (CHP) |

| Grid Injection |

| Transportation Fuel |

| Industrial Heating |

| Residential & Commercial Heating |

| Others |

| Gas Collection Systems |

| Digesters & Fermentation Systems |

| Gas Processing & Upgrading Units |

| Compressors & Storage Systems |

| Power Generation Equipment |

| Monitoring & Control Systems |

| Others |

| By Feedstock | Municipal Solid Waste (MSW) |

| Agricultural Residues | |

| Animal Manure | |

| Industrial Organic Waste | |

| Sewage Sludge | |

| Food Waste | |

| Others | |

| By Technology | Anaerobic Digestion |

| Landfill Gas Recovery | |

| Gasification | |

| Pyrolysis | |

| Biogas Upgrading Systems | |

| Others | |

| By Gas Type | Biogas |

| Biomethane / Renewable Natural Gas (RNG) | |

| Syngas | |

| By Application | Electricity Generation |

| Combined Heat & Power (CHP) | |

| Grid Injection | |

| Transportation Fuel | |

| Industrial Heating | |

| Residential & Commercial Heating | |

| Others | |

| By Component | Gas Collection Systems |

| Digesters & Fermentation Systems | |

| Gas Processing & Upgrading Units | |

| Compressors & Storage Systems | |

| Power Generation Equipment | |

| Monitoring & Control Systems | |

| Others |

Key Questions Answered in the Report

What is the expected value of Finland's renewable gas from waste by 2031?

The market is expected to reach USD 0.51 billion by 2031, up from USD 0.32 billion in 2025, driven by policy mandates, project funding, and stronger transport demand.

Why is biomethane / renewable natural gas growing faster than raw biogas in Finland?

Biomethane / renewable natural gas benefits from the biofuel distribution obligation, grid injection economics, and marine fuel demand, which together support a 12.6% growth rate through 2031.

Which feedstock base is leading renewable gas production from waste in Finland?

Agricultural residues led with a 33.1% share in 2025, driven by Finland's large agricultural by-product base and policy support for manure use.

Which application is growing the fastest in Finland?

Transportation fuel is growing the fastest, with a projected 13.0% CAGR through 2031, as heavy transport and maritime users adopt LBG and biomethane.

What is the main constraint on Finland’s production outlook?

The main issue is supply, not demand. Finland produced only 0.93 TWh in 2024 against an estimated 10 TWh technical-economic potential, and dispersed feedstock also raises logistics costs.

How important is government support for new projects?

Finland directed EUR 469 million (USD 551.7 million) to clean energy projects from 2022 to 2024, and additional aid continued in 2025 for new demonstration and liquefied biomethane projects.

Page last updated on: