Skin-Lightening Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.52 Billion |

| Market Size (2031) | USD 28.72 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

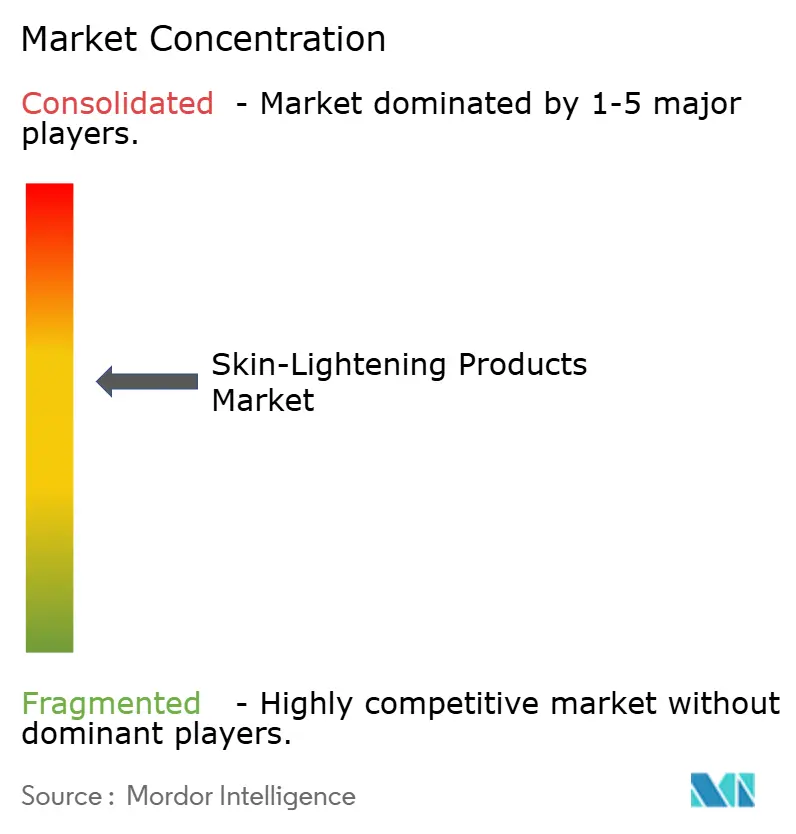

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Skin-Lightening Products Market Analysis by Mordor Intelligence

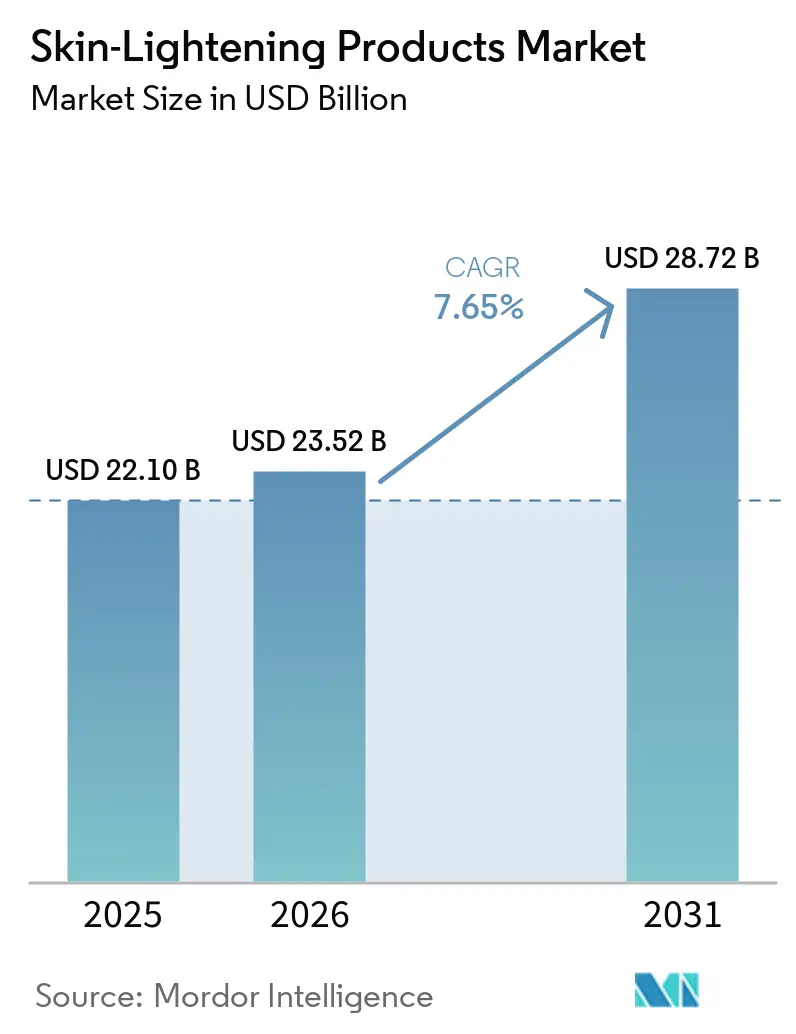

The skin-lightening products market size was valued at USD 22.10 billion in 2025 and is estimated to grow from USD 23.52 billion in 2026 to reach USD 28.72 billion by 2031, at a CAGR of 7.65% during the forecast period (2026-2031). Growth in the skin-lightening products market is being supported by stronger clinical demand for products that address melasma, post-inflammatory hyperpigmentation, and UV-linked dark spots, as long-term maintenance therapy is now part of the recommended care pathway for melasma management. The skin-lightening products market is also being reshaped by ingredient controls in Europe, where tighter limits on kojic acid and continued enforcement against banned substances are forcing reformulation, tighter compliance review, and greater reliance on safer brightening alternatives. Premium positioning remains important because clinically supported products and dermatologist-backed brands are holding pricing power better than undifferentiated mid-tier offers. New interest in botanical and fermentation-based actives is widening formulation options, especially as laboratory work continues to show melanin-inhibiting potential from cleaner ingredient pathways. Competitive intensity in the skin-lightening products market is therefore moving away from simple whitening claims and toward safer actives, better proof of efficacy, stronger online discovery, and formats that fit daily use.

Key Report Takeaways

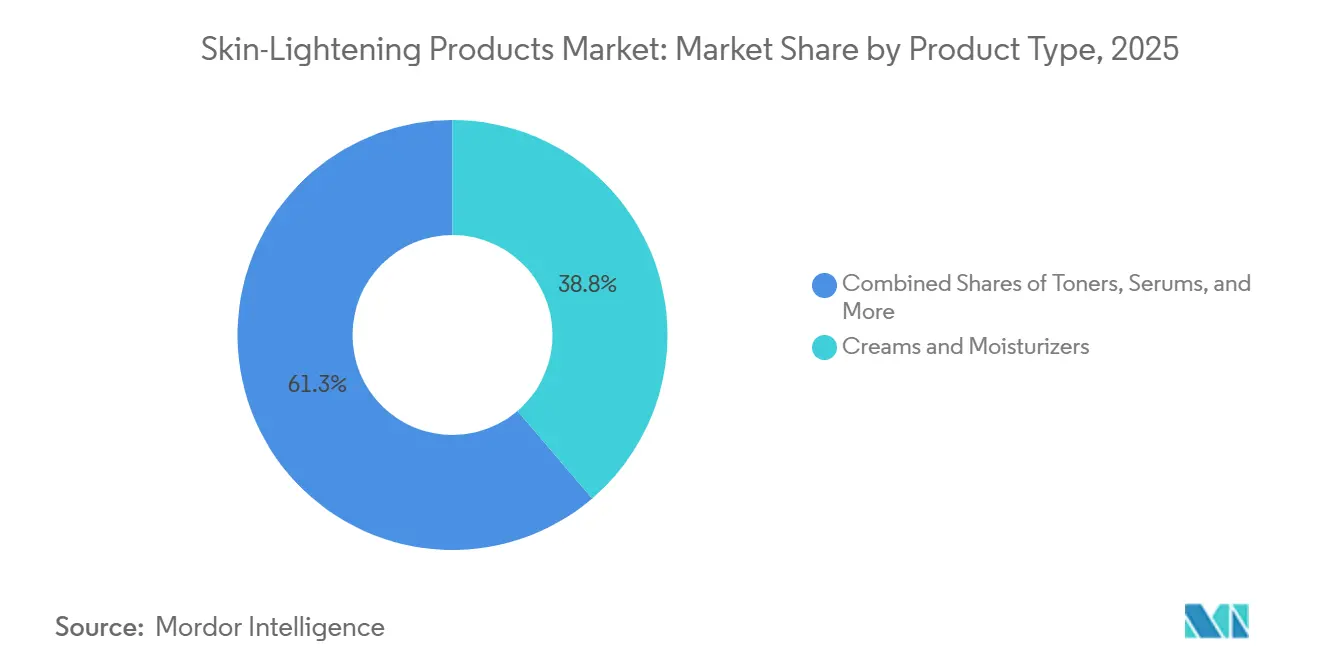

- By product type, creams and moisturizers held 38.75% of the skin-lightening products market size in 2025, while serums are projected to expand at a 9.32% CAGR through 2031.

- By end user, women accounted for 85.32% of the skin-lightening products market share in 2025, while men are forecast to grow at an 8.86% CAGR through 2031.

- By price, mass products captured a 67.83% share in 2025, while premium products are set to grow at a 9.11% CAGR through 2031.

- By category, conventional products held a 70.21% share in 2025, while organic and natural products are expected to advance at a 9.97% CAGR through 2031.

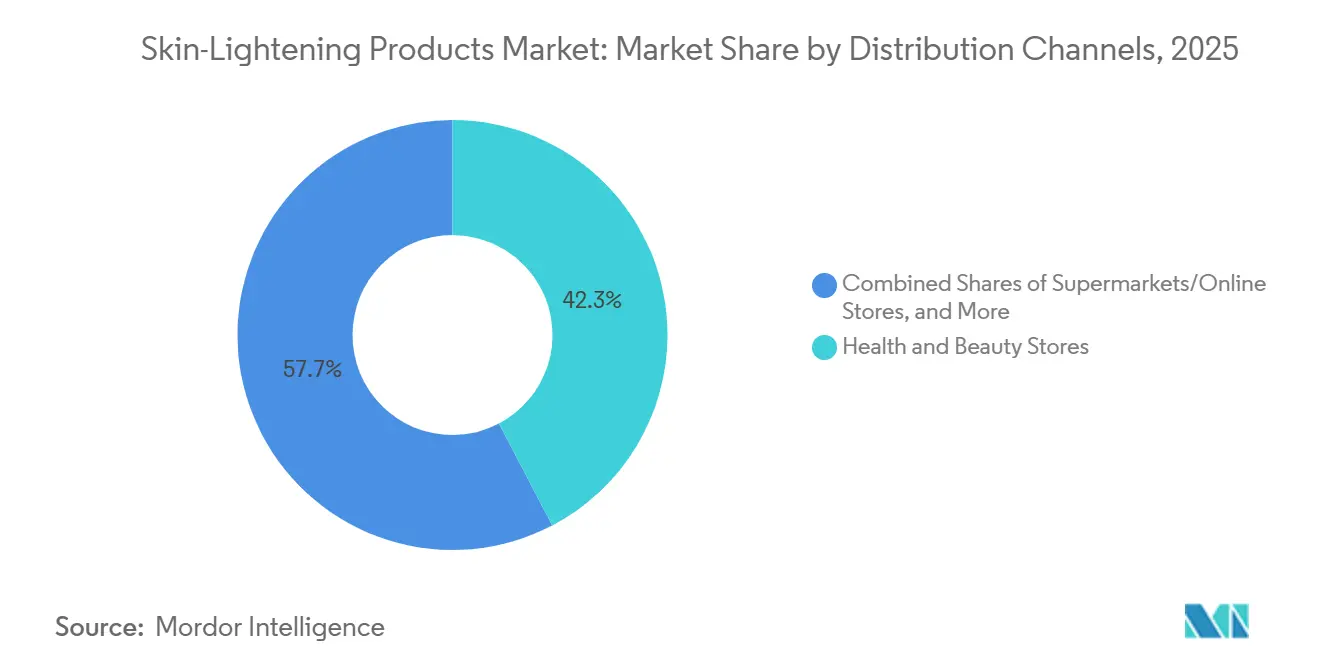

- By distribution channel, health and beauty stores led with a 42.32% share in 2025, while online retail is forecast to grow at a 9.13% CAGR through 2031.

- By geography, Asia-Pacific held 45.46% of the skin-lightening products market size in 2025 and is projected to record the highest CAGR of 9.62% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Skin-Lightening Products Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Even Skin Tone and Pigmentation Correction | +1.3% | Global, concentrated in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Growing Influence of Beauty Standards and Social Media | +1.0% | Asia-Pacific core, with spillover to Middle East and Africa and Latin America | Short term (≤ 2 years) |

| Increasing Skincare Awareness and Dermatology Adoption | +0.9% | North America and Europe, extending to Asia-Pacific | Medium term (2-4 years) |

| Growth in Natural and Botanical Ingredients | +0.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years), Long term (≥ 4 years) |

| Rising Disposable Income in Emerging Economies | +1.1% | Asia-Pacific core, South America, Middle East and Africa | Long term (≥ 4 years) |

| Expansion of E-Commerce and Digital Beauty Platforms | +0.9% | Global, with Asia-Pacific dominant and North America active | Short term (≤ 2 years), Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Even Skin Tone and Pigmentation Correction

Demand in the skin-lightening products market is increasingly linked to persistent pigmentation disorders rather than only appearance-led buying behavior. Melasma, post-inflammatory hyperpigmentation, and UV-driven dark spots tend to recur, which makes consumers more likely to stay on long-term topical routines instead of buying only for short periods. The 2025 global hyperpigmentation guidance summarized by Medscape recommended maintenance therapy as standard care for melasma, which supports repeat purchasing and steadier product rotation over time. This also broadens the consumer base for the skin-lightening products market because the use case extends beyond traditional fairness language and moves into skin tone management, recovery from inflammation, and prevention of visible spots. Pollution exposure, visible light, and routine sun stress also keep demand present in urban markets where consumers may not identify with conventional whitening claims but still seek corrective skincare.

Growing Influence of Beauty Standards and Social Media

The skin-lightening products market continues to be shaped by social pressure, image visibility, and peer comparison, even though the language around product benefits is changing. Social platforms have made before-and-after product results, user reviews, and informal education on active ingredients easier to access, which speeds up trials for new brands and new formats. A 2025 peer-reviewed study found that skin-whitening product use among Chinese adolescents was positively associated with social treatment differences based on skin tone, which shows that demand in some groups is reinforced by visible social bias rather than marketing alone[1]Source: Social Behavior and Personality Authors, “Study on Skin-Whitening Product Use and Colorism Among Chinese Adolescents,” Social Behavior and Personality, sbp-journal.com. This matters because it gives the skin-lightening products market a deeper behavioral foundation in several Asia-Pacific markets, where peer influence and daily image sharing continue to affect purchase decisions. At the same time, social media also raises the standard for proof, since consumers can quickly compare claims, ingredients, and user experiences across many competing products.

Growth in Natural and Botanical Ingredients

The skin-lightening products market is seeing a stronger push toward botanical, fermentation-derived, and cleaner-label actives as brands look for safer and more regulation-resilient formulation paths. This shift is not only a branding exercise because ingredient scrutiny has become tighter and consumers now pay closer attention to how brightening claims are being supported. Research published in January 2026 identified probiotic-derived phenyllactic acid from Limosilactobacillus reuteri as a melanin-inhibiting candidate with pH stability suited to aqueous formats such as toners and serums. That kind of evidence is helping brands in the skin-lightening products market move beyond older restricted actives and build pipelines around ingredients that can fit both efficacy and safety expectations. It also supports premium pricing, because cleaner formulations with a clear mechanism of action are easier to position as advanced skincare rather than simple cosmetic whitening.

Rising Disposable Income in Emerging Economies

Higher household spending power in emerging countries is supporting broader participation in the skin-lightening products market, especially as skincare moves from basic cleansing toward treatment-led routines. Consumers who once stayed in low-cost categories are now more willing to buy serums, specialist creams, and premium brightening products when they believe the efficacy is visible and the regimen is worth repeating. India offers a useful signal, because its men’s grooming category was valued at USD 2.3 billion in 2024, showing that discretionary spending is widening into more specialized personal care segments[2]Source: India Brand Equity Foundation, “India Men’s Grooming Industry, Expanding Product Categories and Consumer Base,” India Brand Equity Foundation, ibef.org. That matters for the skin-lightening products market because adjacent grooming adoption often becomes the entry point for male skincare, multi-step routines, and higher spending per user. As income rises further, the category also benefits from a larger premium consumer base that is more likely to prioritize dermatologist-linked or clinically framed products over low-price alternatives.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Regulatory Restrictions on Ingredients | -1.3% | Europe, United Kingdom, North America, with global compliance spillover | Short term (≤ 2 years) |

| Substitution by Alternative Skincare Treatments | -0.8% | North America, Europe, affluent Asia-Pacific including Japan and South Korea | Medium term (2-4 years) |

| Consumer Skepticism About Product Effectiveness | -0.6% | Global, with sharper effect in North America and Europe | Medium term (2-4 years) |

| Adverse Publicity from Health Incidents | -0.5% | Middle East and Africa, South Asia, Sub-Saharan Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict Regulatory Restrictions on Ingredients

Regulation is one of the strongest limits on expansion in the skin-lightening products market because the category has long depended on active ingredients that attract close safety review. Commission Regulation (EU) 2024/996 restricted kojic acid to 1% in face and hand products and also imposed restrictions that affected alpha-arbutin and arbutin placement in the European market[3]Source: European Commission, “Commission Regulation (EU) 2024/996 of 3 April 2024 Amending Regulation (EC) No 1223/2009,” Publications Office of the European Union, op.europa.eu. Enforcement pressure is also real at the product level, since the EDQM reported that 18% of tested skin-whitening products contained banned substances such as hydroquinone, mercury, or glucocorticoids. This raises reformulation costs, slows launch cycles, and creates a higher barrier for smaller brands that do not have strong regulatory and laboratory support. It also favors brands in the skin-lightening products market that have already built portfolios around niacinamide, tranexamic acid, and other alternatives that face fewer restrictions.

Consumer Skepticism About Product Effectiveness

The skin-lightening products market also faces a trust problem because many consumers now question whether visible results match product promises. Claims that once depended on broad whitening language no longer work as easily with buyers who want clearer evidence, better ingredient rationale, and realistic timelines for pigment correction. This is especially important in urban and premium consumer groups, where buyers compare products more carefully and are less patient with unclear outcomes or exaggerated branding. The result is that dermatologist endorsement, human efficacy testing, and repeated proof of safety are becoming more important in the skin-lightening products market than heavy promotional language alone. Skepticism also increases the risk of substitution, since consumers who lose confidence in topical products can shift toward peels, lasers, and other procedure-based options when access to clinics improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Serums Gain Share as Formulation Science Evolves

Creams and moisturizers held 38.75% of the skin-lightening products market size in 2025, which kept them in the leading position because they fit daily routines, broad price points, and both mass and premium shelf placement. Their strength in the skin-lightening products market also comes from ease of use, because consumers can combine hydration, tone correction, and sun care in one familiar format. Many leading products now blend niacinamide, vitamin C derivatives, and tranexamic acid into moisturizing bases, which helps brands preserve volume while still raising the value proposition. This makes creams and moisturizers more than a legacy format, since they remain the most practical entry point for first-time users and the most repeatable format for routine use. Their leadership also reflects the fact that a large share of consumers still prefers a visible skincare benefit inside a product they already understand and apply every day.

Serums are projected to grow at a 9.32% CAGR through 2031, which makes them the fastest-moving product format in the skin-lightening products market. The appeal of serums is tied to concentrated actives, lighter textures, and stronger perceived performance, especially among consumers who want faster improvement in stubborn spots and uneven tone. In the skin-lightening products industry, this gives serums a stronger clinical image than basic creams, which is important in a category where proof and formulation credibility matter more each year. Masks and peels occupy a different role because they are usually used as add-on treatments, which supports higher ticket prices but lowers purchase frequency. Cleansers continue to matter because they introduce consumers to the category with lower commitment and lower active strength, after which brands can move those users toward serums, spot treatments, and higher-value regimens.

By End User: Men’s Brightening Quietly Reshapes Demand

Women accounted for 85.32% of the skin-lightening products market share in 2025, which shows how strongly the category still depends on established female skincare routines across the largest demand centers. This base has supported volume for years, but it also means that much of the next phase of growth in the skin-lightening products market will come from adjacent user groups rather than from repeated expansion within the same core demographic. Women remain central because they are more likely to maintain multi-step skincare routines, buy across several formats, and stay engaged with both mass and premium products. They also drive strong repeat purchasing when pigmentation concerns are persistent and when product use becomes part of maintenance rather than one-time correction. This gives leading brands a stable core audience, but it also raises the need to widen relevance across new consumer segments.

Men are projected to grow at an 8.86% CAGR through 2031, making them the fastest-growing end-user segment in the skin-lightening products market. A key reason is that male grooming is becoming broader and more treatment-led, especially in South and Southeast Asia, where consumers are moving beyond shaving and cleansing into targeted skincare. India’s men’s grooming category reached USD 2.3 billion in 2024, which signals a strong adjacent spending base for products that address uneven tone, dark spots, and routine skin stress. Another support factor is shaving-related post-inflammatory hyperpigmentation, because regular razor use creates a practical skin health case for brightening products without relying on fairness messaging. That makes the men’s segment attractive in the skin-lightening products market, since brands can frame benefit claims around recovery, clarity, and smoother tone rather than around older cultural language that now attracts more scrutiny.

By Price: Premium Tier Outpaces Mass on Growth Trajectory

Mass products captured 67.83% of the skin-lightening products market size in 2025, which reflects the broad affordability needs of high-volume countries and the continued role of accessible products in category penetration. The mass tier remains vital in the skin-lightening products market because first-time use, daily replenishment, and wide retail availability still depend heavily on price accessibility. This segment works especially well in markets where consumers buy through pharmacy chains, supermarkets, and local beauty stores and where a lower unit price supports higher repeat volume. It also benefits from the fact that creams, cleansers, and entry serums can be positioned with visible benefits without forcing premium spending. The strength of the mass tier, therefore, comes from reach, habit, and the ability to serve very large consumer pools with simple product architectures.

Premium products are forecast to expand at a 9.11% CAGR through 2031, which shows that value growth in the skin-lightening products market is moving toward stronger proof, stronger actives, and better brand trust. Premium buyers are more willing to pay for patented ingredient systems, specialist serums, and better safety positioning, especially where regulations have made older formulations less acceptable. In the skin-lightening products industry, that creates pressure on mid-tier brands that cannot fully compete on either affordability or science-led differentiation. Premium growth is also tied to dermatologist endorsement and the broader shift toward treatment-style skincare, where consumers expect repeated use to produce measurable change. The result is a more polarized pricing structure in which the strongest gains come from widely accessible mass lines on one side and clinically framed premium products on the other.

By Category: Clean Beauty Momentum Lifts Organic Segment

Conventional products held 70.21% of the 2025 market, which kept them in the leading position because they still offer proven performance, lower raw material costs, and high familiarity across many consumer groups. Their continued scale in the skin-lightening products market also reflects the fact that many consumers are comfortable with established active systems as long as the products remain compliant and easy to understand. Conventional lines benefit from broader SKU depth, stronger visibility in mass retail, and the ability to operate at lower price points than many natural alternatives. They also remain important in markets where product choice is driven more by accessibility and habit than by ingredient philosophy. Even so, their leadership is no longer enough on its own because scrutiny around safety and proof is steadily raising the burden on older formula systems.

Organic and natural products are projected to grow at a 9.97% CAGR through 2031, making them the fastest-growing category in the skin-lightening products market. The move is being supported by tighter ingredient review, more consumer interest in transparent formulations, and wider brand investment in plant-based and fermentation-derived brightening solutions. January 2026 research on probiotic-derived phenyllactic acid added to that momentum by showing a cleaner melanin-inhibiting pathway with practical formulation stability. In the skin-lightening products industry, that matters because cleaner actives are not only a marketing tool, they are also a route to long-term compliance resilience. The organic segment is also widening beyond facial care, as brands increasingly treat body brightening washes, lotions, and serums as dedicated products rather than simple extensions of facial ranges.

By Distribution Channels: Online Commerce Reorders Channel Economics

Health and beauty stores held 42.32% of the 2025 distribution share, which kept them in the lead because consumers still value guided purchase environments for visible skin concerns. These outlets matter in the skin-lightening products market because they offer product comparison, trusted retail context, and, in many cases, in-store consultation that is harder to replicate in general retail settings. They are especially important for premium and specialist products, where shoppers want reassurance before spending more on serums, treatment creams, and targeted routines. Physical specialist stores also help brands stage product stories in a clearer way than crowded supermarket shelves. That support remains meaningful, even as a growing share of category growth shifts elsewhere.

Online retail is projected to expand at a 9.13% CAGR through 2031, which makes it the fastest-growing distribution route in the skin-lightening products market. Consumers increasingly research actives, compare ingredient lists, read user reviews, and check claim credibility before purchase, which naturally favors digital channels with more information and faster comparison. The online route also helps new brands enter the skin-lightening products market without depending first on wide physical distribution or expensive shelf negotiation. In the skin-lightening products industry, this changes channel power because discovery moves closer to search, recommendations, reviews, and platform visibility rather than store-led curation alone. Supermarkets and hypermarkets still retain volume in low-priced ranges, but they are less effective for building trust around high-efficacy or clinically framed products that require explanation.

Geography Analysis

Asia-Pacific held 45.46% of global share in 2025 and is projected to record a 9.62% CAGR through 2031, which makes it both the largest and the fastest-growing regional part of the skin-lightening products market. The region combines large population scale, deep-rooted demand for even tone, and a rising middle class that is now spending more on targeted skincare routines. China, India, Japan, and South Korea continue to anchor volume and product innovation, while Southeast Asia adds strong growth potential through expanding digital beauty participation and wider access to specialist skincare. India also offers a useful demand signal because its men’s grooming category reached USD 2.3 billion in 2024, which supports broader adoption of products linked to pigmentation and uneven tone. This concentration gives Asia-Pacific a central role in the skin-lightening products market, since product language, channel behavior, and innovation timing in the region often influence how brands scale globally.

North America and Europe form the next major demand zone, although the drivers differ across the two regions. In North America, demand is supported by a multi-ethnic consumer base and by higher awareness of post-inflammatory hyperpigmentation and other persistent pigment issues, which gives the skin-lightening products market a more clinical and treatment-led character. In Europe, compliance is a stronger competitive filter because ingredient restrictions and surveillance have pushed brands to reformulate, withdraw older products, or strengthen regulatory review processes. Marketing language is also more cautious in both regions, with tone correction and dark spot care more acceptable than overt whitening terminology.

South America and the Middle East and Africa add a different growth profile to the skin-lightening products market because demand is supported by strong beauty engagement, rising pharmacy retail depth, and an active premium tier in selected urban markets. Brazil remains important because dermatologist-linked skincare and pharmacy channels give brands a practical route to communicate efficacy and safety together. In the Gulf, higher-income households support premium beauty spending, while in several African markets the shift from informal products toward regulated branded options remains a major opportunity. This means the skin-lightening products market can still gain from category formalization in these regions, even where regulatory and distribution conditions are less mature than in North America, Europe, or parts of Asia-Pacific.

Competitive Landscape

The skin-lightening products market remains moderately concentrated, with a limited group of multinational companies controlling a large share of premium value while regional players compete harder in volume segments and local niches. L'Oréal, Beiersdorf, Shiseido, and Unilever benefit from broad distribution, higher research budgets, and established brand trust, which allows them to defend leadership as compliance and efficacy expectations rise. Their position in the skin-lightening products market is also supported by proprietary ingredient systems, because differentiated actives help protect premium pricing and reduce direct comparability with lower-cost alternatives. At the same time, regional brands in India, China, and Southeast Asia remain active where they can move faster on local consumer taste, pricing, and online engagement. This creates a split structure in which global leaders are strongest in premium science-backed positioning, while local specialists remain relevant through sharper market adaptation.

Strategic activity is increasingly centered on product upgrades, ingredient platforms, and portfolio expansion. In July 2026, Shiseido announced the planned release of Snow Beauty Brightening Skincare Powder with a proprietary 4MSK delivery system and added niacinamide, showing continued investment in multi-function brightening products. In February 2026, NIVEA extended its Luminous630 line in Canada with two glow-focused launches, reinforcing Beiersdorf’s effort to widen the use cases around a patented pigmentation platform. In March 2026, The Estée Lauder Companies agreed to acquire the remaining 51% of Forest Essentials, which strengthens exposure to premium Ayurvedic skincare and to brightening-linked consumer demand in India.

Competitive pressure is also rising because brand claims are being judged more heavily on safety, transparency, and repeatable results than in the past. Companies that can show clinical support, compliance readiness, and a clear rationale for ingredient choice are better positioned in the skin-lightening products market than brands still relying on generic whitening language. Another clear shift is the growing importance of men’s brightening, body-focused tone correction, and at-home treatment routines, all of which widen the addressable space without depending only on the core female facial-care segment. Overall, the skin-lightening products market is moving toward a structure where scale still matters, but evidence quality and formulation credibility are becoming just as important as distribution reach.

Skin-Lightening Products Industry Leaders

L'Oreal SA

Unilever Plc

Shiseido Co., Ltd

Kao Corporation

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sulwhasoo, the global luxury beauty brand of Amorepacific, launched a new whitening product, the Lumiwise Brightening Ampoule Serum. The formulation combines Ginseng Ectoin, derived from ginseng, with niacinamide, an ingredient commonly used for brightening and tone correction, to address skin dullness associated with aging.

- January 2026: KOSÉ Corporation announced a major upgrade to its flagship DECORTÉ WHITELOGIST brightening skincare line with the launch of the eighth-generation WHITELOGIST CHRONOGENESIS BRIGHTENING CONCENTRATE 1.8X serum and an enhanced intensive brightening mask.

- January 2026: Naturium expanded its skincare portfolio with the launch of the Multi-Bright Milky Toner and Multi-Bright Advanced Serum, a new brightening-focused product duo developed to capitalize on the growing consumer demand for the “glass skin” trend. The products are formulated to improve skin radiance, texture, and tone through a combination of gentle exfoliating, brightening, and hydrating ingredients.

Global Skin-Lightening Products Market Report Scope

| Creams and Moisturizers |

| Masks and Peels |

| Cleansers |

| Serums |

| Others |

| Men |

| Women |

| Mass |

| Premium |

| Conventional |

| Organic |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Creams and Moisturizers | |

| Masks and Peels | ||

| Cleansers | ||

| Serums | ||

| Others | ||

| By End User | Men | |

| Women | ||

| By Price | Mass | |

| Premium | ||

| By Category | Conventional | |

| Organic | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for skin-lightening products?

The skin-lightening products market is projected to reach USD 28.72 billion by 2031 from USD 23.52 billion in 2026, growing at a 7.65% CAGR over 2026-2031.

Which region leads global demand for skin tone correction products?

Asia-Pacific led with 45.46% share in 2025 and is also expected to post the fastest regional growth at a 9.62% CAGR through 2031.

Which product format is growing the fastest in this category?

Serums are the fastest-growing format with a projected 9.32% CAGR through 2031, supported by concentrated actives and stronger treatment positioning.

Why are premium brands gaining momentum in pigmentation care?

Premium products are forecast to grow at 9.11% CAGR because buyers are paying more for patented actives, clinical support, and stronger safety positioning.

Page last updated on: