China Skin Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

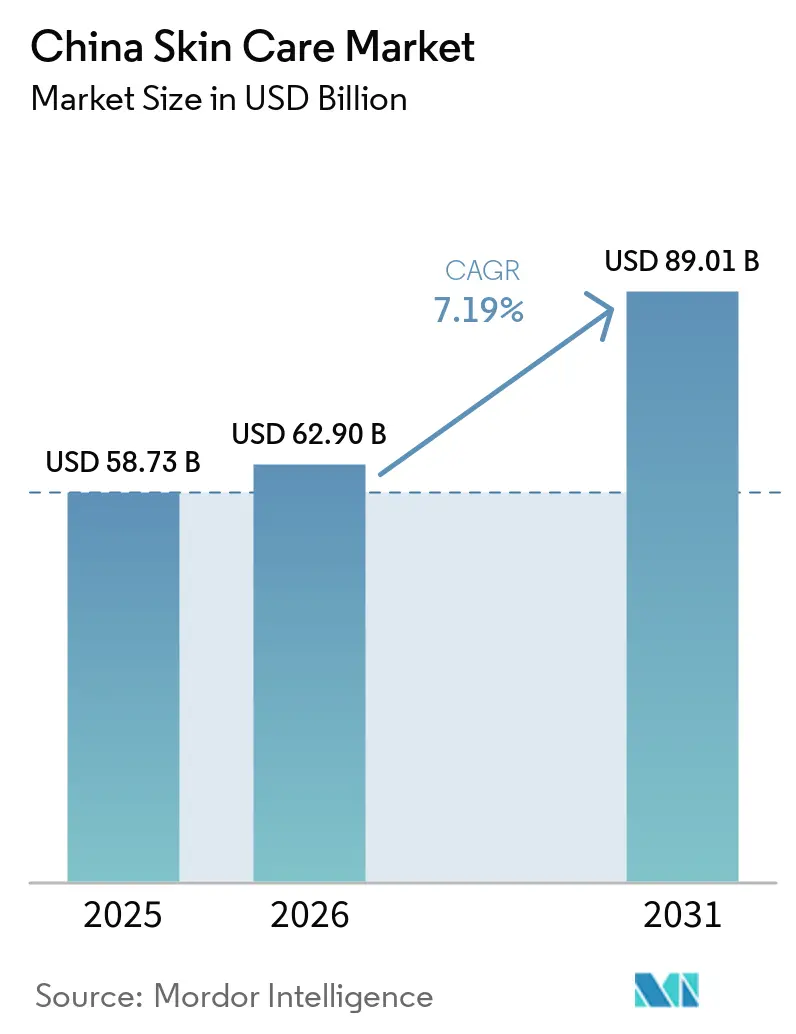

| Base Year Market Size (2025) | USD 58.73 Billion |

| Market Size (2026) | USD 62.90 Billion |

| Market Size (2031) | USD 89.01 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Skin Care Market Analysis by Mordor Intelligence

The China skin care products market size is projected to be USD 58.73 billion in 2025, USD 62.90 billion in 2026, and reach USD 89.01 billion by 2031, growing at a CAGR of 7.19% from 2026 to 2031. The China skin care products market is expanding through wider daily use across age groups and income bands, so growth is no longer tied only to a narrow premium upgrade cycle. Domestic brands also reshaped the competitive balance, with their aggregate share reaching a significant percentage in 2025 and the number of brands crossing the CNY 100 million transaction threshold rising from 746 in 2023 to 839 in 2025. Counterfeit goods and tighter regulation are also shaping the China skin care products market, and brands that treat compliance as a core product discipline are in a stronger position to protect trust and secure distribution as enforcement deepens through 2031.

Key Report Takeaways

- By product type, facial care products led with 83.43% of revenue in 2025, and facial care products are also forecast to expand at 7.37% CAGR through 2031.

- By price, mass products held 66.87% of revenue in 2025, while premium products recorded the highest projected CAGR at 8.11% through 2031.

- By category, conventional products accounted for 72.04% of revenue in 2025, while organic and natural products are projected to grow at 7.86% CAGR through 2031.

- By end-user, women held 84.35% of revenue in 2025, while kids and children are forecast to expand at 8.39% CAGR through 2031.

- By distribution channel, health and beauty stores captured 46.25% of revenue in 2025, while online retail stores are projected to grow at 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Skin Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| K-beauty and C-beauty trends drive product innovation | +1.5% | National, with Tier 1 and New Tier 1 cities representing 69.2% of anti-aging engagement | Short term (≤ 2 years) |

| Demand for natural ingredients supports premium product sales | +1.4% | National, with Douyin strongest in Tier 1 to Tier 3 and RED concentrated in affluent urban users | Short term (≤ 2 years) |

| Social media influences skin care purchases and brand discovery | +1.2% | National, with strongest pull from Tier 1 and Tier 2 cities including Shanghai, Beijing, and Shenzhen | Medium term (2-4 years) |

| Men's grooming trends expand the skin care consumer base | +0.9% | National, with early scale in coastal Tier 1 cities and further expansion into Tier 2 cities | Long term (≥ 4 years) |

| Demand for anti-aging solutions supports market growth | +0.8% | National, with principal volume growth from Tier 3 to Tier 5 cities | Long term (≥ 4 years) |

| Increasing urbanization encourages adoption of advanced skin care routines | +0.6% | National, with early gains in Shanghai, Beijing, and Guangzhou and spillover into Tier 3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Anti-Aging Solutions Supports Market Growth

Anti-aging is shaping the China skin care products market at the ingredient, format, and channel levels. Online anti-aging skin care sales reached billions in 2025, and the category sustained year-over-year growth in every month. New cosmetic ingredient filings with anti-aging efficacy claims increased by more than 40% between 2024 and 2025, which shows that both domestic and international formulators are moving R&D resources toward clinically supported actives. Demand is also starting earlier in life, as the 31 to 35 age group now represents 23.4% of anti-aging purchases, up from 20.7%, which signals that preventive use has become standard practice instead of a late-stage response. This shift gives the China skin care products market a broader repeat-purchase base and supports more premium treatment formats over time.

Social Media Influences Skincare Purchases and Brand Discovery

Social commerce has become the main route to market for the China skin care products market rather than a supporting sales channel. Douyin overtook Tmall in 2025 and generated RMB 270 billion in beauty gross merchandise value, while Tmall generated RMB 221 billion. Douyin's beauty category also generated nearly RMB 20 billion in gross merchandise volume in July 2025 alone and grew year over year. RED plays a different role because it shapes trust, trial intent, and brand validation, especially for premium and international labels. Brands that separate awareness building on RED from conversion on Douyin are responding to how Chinese consumers now move through the purchase journey. This platform split favors fast-testing domestic brands, but it also gives international players a workable structure for premium storytelling inside the China skin care products market.

K-Beauty and C-Beauty Trends Drive Product Innovation

The China skin care products market is moving through a visible formula and positioning shift as domestic C-beauty brands take more of the innovation lead. K-beauty's share of Chinese online cosmetics exports fell between 2022 and 2025, which shows that imported influence did not disappear but was absorbed into a more local innovation cycle. K-beauty cream sales on Tmall also dropped between May 2025 and May 2026, as consumers shifted toward anti-aging and higher-performance products where simple hydration claims no longer differentiate strongly. Domestic brands responded by blending Traditional Chinese Medicine botanical actives such as ginseng, red yeast, and standardized Bencao extracts with synthetic biology fermentation and recombinant collagen. Global groups have started to invest in that local formulation space, as shown by L'Oréal's minority stake in Lan and its earlier strategic investment in Chando [1]Source: Reuters, "L'Oréal buys second Chinese skincare stake as C-Beauty brands snare market share", reuters.com. This pattern suggests that the China skin care products market is rewarding brands that can combine local ingredient language, visible efficacy, and faster launch cycles within a regulated raw material framework.

Demand for Natural Ingredients Supports Premium Product Sales

Natural ingredient demand is supporting premium growth in the China skin care products market, but consumers are judging these products by results rather than by label language alone. Plant ingredient skin care unit volumes rose year over year in the 12 months to mid-2024 and reached a million units, which was many times faster than the broader beauty and skin care category. Registered brands in this area increased, and related social media posts rose to a million, which shows that demand is widening across both supply and consumer attention. Premium buyers increasingly expect natural formulas to show clear efficacy, and claims such as overnight repair or visible firming now need stronger proof to hold their price position. China's green packaging push also added a sustainability layer to the category in 2025, which raised attention to packaging materials alongside ingredient transparency. The brands that are gaining ground in the China skin care products market are the ones that treat naturally and measurable performance as linked parts of the same offer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit products undermine consumer trust in brands | -0.7% | National, with the sharpest pressure on Douyin and secondary e-commerce platforms | Short term (≤ 2 years) |

| Regulatory compliance requirements increase operational complexities | -0.5% | National, with higher operating strain in coastal manufacturing hubs such as Guangdong and Zhejiang | Medium term (2-4 years) |

| Ingredient safety concerns affect consumer purchasing decisions | -0.4% | National | Medium term (2-4 years) |

| Environmental concerns increase scrutiny of product packaging | -0.3% | National, with earlier adoption in Tier 1 cities and export-facing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products Undermine Consumer Trust in Brands

Counterfeit cosmetics remain a direct drag on trust in the China skin care products market, especially for brands that scale quickly through social commerce before their enforcement systems catch up. In the first half of 2024, Douyin deleted 1.8 million fake product listings, closed more than 160,000 stores, and supported criminal investigations that led to the seizure of CNY 5.94 billion in counterfeit assets and the arrest of 400 suspects. The distortion is more serious in newer and niche categories, where fake products can outsell originals among buyers who are still price-led and not yet loyal to one brand. Counterfeit anti-aging serums and creams have also been found in the source draft to contain lead, mercury, and unauthorized preservatives, which raises the risk that harm from fake goods is blamed on legitimate brands. That problem affects more than one company because it weakens category trust in the same digital spaces where discovery and conversion now happen fastest. The China skin care products market, therefore carries a trust cost that can slow premium conversion even when consumer demand remains strong.

Regulatory Compliance Requirements Increase Operational Complexities

The China skin care products market is also facing a heavier regulatory burden, and that burden is raising the effective cost of participation. Since May 1, 2025, all cosmetic registrants and notifiers have had to submit complete safety assessment reports, which ended the earlier simplified reporting option. The NMPA added the Administrative Measures for Cosmetic Safety Risk Monitoring and Assessment in August 2025, and in November 2025, it issued a 24-measure reform agenda that set the direction of supervision through 2030 ZMUNI. July 2025 also brought 34 new cosmetics standards projects covering ingredient safety, PFAS detection, and siloxane testing thresholds. Larger multinational companies can absorb this more easily because they already have compliance systems, while smaller domestic innovators face slower launch cycles just when speed matters most. The China skin care products market is therefore becoming harder to enter and harder to operate in without stronger documentation, testing systems, and raw material control.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Formulations Anchor Value; Body Anti-Aging Opens New Frontiers

Facial care products accounted for 83.43% of the China skin care products market in 2025, and the same segment is also projected to grow at 7.37% CAGR through 2031. This lead reflects the depth of China's multi-step facial routine, where serums, essences, masks, moisturizers, and targeted treatments continue to take a larger share of wallet than body or lip products. In 2025, SK-II led the serum segment with CNY 1.45 billion in sales, while Forest Cabin tripled serum revenue to CNY 1.29 billion and entered the top 3. Moisturizers and creams also held the majority of the skin care subsegment in 2024 and grew in 2024, which shows how basic routine categories still anchor volume even as treatment formats gain attention. Facial care remains the core of the China skin care products market because it captures both routine replenishment demand and the highest-value upgrade cycle.

Body care products start from a smaller base, but they offer one of the clearest adjacency opportunities in the China skin care products market. Body anti-aging grew significantly in the first half of 2025, which shows that consumers are extending facial care logic to the neck, hands, and chest area. Foot and hand cream formats are also moving higher in value as concentrated active ingredients that were once limited to facial care shift into body care routines. Lip care remains the smallest product type, but its role is improving as hydrating serums and barrier-repair actives push lip products closer to treatment territory. Safety assessment rules introduced in 2025 apply across facial, body, and lip products, which favors brands that already hold compliant ingredient libraries and can extend faster across adjacent categories

By Price: Mass Drives Volume, Premium Drives Value Growth

Mass products commanded 66.87% of the China skin care products market in 2025, supported by frequent purchase behavior and strong traffic in Douyin's sub-CNY 200 price bands. The lowest price band of CNY 0 to 100 grew year over year in 2025, which shows that entry pricing remains an efficient route for consumer acquisition. At the same time, products priced above CNY 1,000 also recorded strong sales growth in 2025, which shows that premium demand did not weaken as lower-priced products expanded. The pattern is better described as a barbell, because spending is expanding at the value end and the premium end while the middle narrows. The CNY 300 to 500 range faced the most pressure, which suggests more selective buying rather than uniform downtrading across the China skin care products market.

Premium products are forecast to expand at 8.11% CAGR through 2031, which keeps them ahead of the broader China skin care products market. Growth at the top end is tied to consumers who are more ingredient-literate and more willing to pay for visible proof, dermatologist positioning, or stronger claims support. Beiersdorf benefited from this shift after NMPA approved Thiamidol in November 2024, and the company launched Eucerin Spotless Brightening Pro Serum in 2025 and reached the number 1 position in China's derma anti-pigment serum category. China's median disposable income per capita reached CNY 34,707 in 2024 and rose 5.5% year over year, which supports a stable base for continued premium trading-up. The China skin care products market therefore continues to reward premium offers that can combine science-led differentiation with local relevance.

By Category: Conventional Holds Critical Scale, Organic Accelerates from a Differentiated Base

Conventional products held 72.04% of market value in 2025, which keeps them at the center of scale manufacturing, broad retail access, and high-volume replenishment. Organic and natural products are projected to grow at 7.86% CAGR through 2031, making them the fastest-growing category in the China skin care products market. Plant ingredient skin care unit volumes increased year over year through mid-2024 and reached 210 million units, which shows that ingredient-led demand has already moved into meaningful scale. The same source draft reported that registered brands in this area increased 15% to 7,257, and related social media posts rose to 12.26 million, which shows that both supply and consumer attention continue to widen. Conventional products still hold the larger base, but organic and natural formats are becoming more commercially relevant in the China skin care products market.

Organic and natural products are gaining strength because consumers are now judging botanical claims by performance, texture, and visible results rather than by simple label wording alone. Brands using clinically documented actives such as Tibetan Rhodiola, Yunnan Centella Asiatica, and standardized Bencao extracts are moving faster than brands that rely mainly on certification language. This means that the China skin care products industry is treating naturality and efficacy as linked value points rather than as separate ideas. Sustainable packaging is also becoming part of the category discussion as China strengthened the policy focus on packaging materials and waste reduction in 2025. The brands best placed in this category are the ones that can keep ingredient storytelling credible while still delivering measurable product performance.

By End-User: Women Anchor the Market, Kids Segment Unlocks Per-Child Spending Premiumization

Women represented 84.35% of market value in 2025 and remain the core demand base for the China skin care products market. Their spending covers daily moisturizers, serums, brightening treatments, and premium anti-aging routines, which means the segment supports both volume and margin across almost every channel. Tier 1 and New Tier 1 cities accounted for the majority of anti-aging engagement, while Tier 2 cities' share increased, which shows that women's premium demand is still centered in large cities but is gradually widening outward. Brands are also building more occasion-based offers for women, including travel use, recovery after medical procedures, and support for night-shift skin stress. The women's segment remains the main proving ground for new claims, textures, and premium pricing logic in the China skin care products market.

Kids and children are projected to grow at 8.39% CAGR through 2031, which makes them the fastest-growing end-user group and a clear China skin care products market size opportunity. Growth here is being driven by higher spending per child rather than by demographic expansion. The source draft states that China's children's cosmetics market exceeded CNY 500 billion in 2025, after rising from CNY 136.4 billion in 2014 at a 12.5% CAGR, based on data released by the State Administration for Market Regulation. The same source draft also states that, as of June 2025, 28,168 children's cosmetic products were on file with NMPA, and brands are increasingly using claims tied to sun protection, anti-sensitivity, and barrier repair. The China skin care products industry is also seeing steady development in men's routines, as younger male consumers adopt anti-aging, oil control, and barrier-care steps that move them closer to regular replenishment behavior.

By Distribution Channel: Health and Beauty Stores Lead in Share, Online Retail Accelerates

Health and beauty stores held 46.25% of the market value in 2025, which left them as the leading offline route in the China skin care products market. Specialist chains support the first purchase and repeat purchase because they combine a curated assortment, product trial, and assisted selling for higher-value skin care. This matters most for serums, essences, and targeted treatment products that often need more explanation before conversion. Supermarkets and hypermarkets remain relevant for mass-tier products, especially in lower-tier cities where value, convenience, and basket shopping still shape routine buying. Other store-based channels still serve supporting roles, but specialist beauty retail remains the main offline anchor for the China skin care products market.

Online retail stores are forecast to grow at 8.02% CAGR through 2031, making them the fastest-growing distribution format and a rising China's skin care products market. Douyin's content-commerce model reduces the time between product discovery and purchase, which lowers the cost of testing new launches and reformulations. RED continues to play a separate role because it helps brands build trust, trial intent, and product validation before conversion moves to a commerce platform. Cross-border e-commerce remains useful for international brands that want a faster entry route, while pharmacy-linked formats are gaining relevance as dermo-cosmetics move closer to health care demand. The China skin care products market is becoming more channel-specific, with brands using each route for a different role instead of expecting one format to do every job.

Competitive Landscape

The China skin care products market remains moderately fragmented, with rivalry spread across price points, product formats, and channel models rather than concentrated under one dominant supplier. L'Oréal led among international groups in 2025 with online brand revenue above CNY 10.0 billion. Helena Rubinstein, YSL, and La Mer all grew faster than the broader pace in anti-aging, which shows that luxury labels still retain pricing power where strong efficacy and brand equity meet. This leaves the China skin care products market with a clear competitive split, where multinationals lean on clinical heritage and domestic players lean on faster product iteration, local ingredient stories, and platform-native content execution.

Strategic investment has become a major competitive tool in the China skin care products market. In November 2025, L'Oréal took a minority stake in Chinese mass-market skin care brand Lan and followed an earlier strategic investment in Chando, which showed a shift from direct displacement toward partnership with domestic labels that already connect with local consumers. In April 2026, L'Oréal's China Research and Innovation Center was elevated to global-level status, and the first co-developed outcome with Huashan Hospital Pudong Fudan University made its global debut as a supramolecular oil-control skin care product [2]Source: Shanghai Municipal People's Government, "L'Oreal's China R&D center elevated to global level", english.shanghai.gov.cn. Bloomage Biotechnology also deepened its technology position in 2025 through a strategic partnership with LG Household & Health Care focused on synthetic biology and glycobiology for next-generation skin longevity products. These examples show that leadership in the China skin care products market now depends on brand equity, local science links, ingredient platforms, and execution speed at the same time.

White-space demand remains strongest in clinical men's skin care in Tier 2 and Tier 3 cities, premium baby and children's products, and body anti-aging where no brand yet holds clear leadership. Estée Lauder strengthened its local operating base in April 2026 by opening its China Fulfillment Center and Group Open Innovation Center in Shanghai, while the company also reported year-over-year growth in mainland China organic net sales in Q2 FY2026. Compliance is also becoming a stronger competitive filter in the China skin care products market because stricter safety and standards rules raise the cost of staying active for underprepared sellers. As that process continues, brands with better dossiers, stronger supply control, and faster digital execution are more likely to capture the share that weaker operators lose.

China Skin Care Industry Leaders

-

L'Oréal S.A.

-

The Estée Lauder Companies Inc.

-

Unilever PLC

-

Shiseido Company, Limited

-

Moët Hennessy Louis Vuitton

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Proya Cosmetics acquired an additional 12.6% stake in Flower Knows for CNY 351 million, pushing its total indirect holding to 51% and bringing the brand fully onto Proya's balance sheet, making it the group's second-largest cosmetics brand by revenue. The deal strengthens Proya's position in the accessible premium cosmetics segment and diversifies its portfolio beyond its core science-backed skin care line.

- April 2026: L'Oréal's China Research and Innovation Center was elevated to global-level status by the Shanghai Municipal Commission of Commerce, the first such recognition for a foreign-funded R&D center in the Jing'an district. The Center's first co-developed outcome with Huashan Hospital, Pudong Fudan University, a supramolecular oil-control skin care product, made its global debut, marking a reproducible model for industry, academic, and clinical product development.

- September 2025: Bloomage Biotechnology signed a strategic partnership agreement with LG Household & Health Care to launch a joint project combining advanced skin research with synthetic biology-based ingredient manufacturing, with glycobiology positioned as the foundational technology for next-generation skin longevity products.

China Skin Care Market Report Scope

The market comprises facial care, body care, and lip care products, including cleansers, moisturizers, serums, essences, toners, etc., designed to maintain skin health, hydration, protection, and appearance across mass and premium segments. The China Skin Care Market Report is Segmented by Product Type (Facial Care Products, Body Care Products, and More), Price (Mass and Premium), End-User (Men, Women, Other), Category (Organic and Conventional), and Distribution Channel (Supermarkets/Hypermarkets, Online Retail Stores, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Facial Care Products | Cleansers |

| Moisturizers and Creams | |

| Serums and Essence | |

| Toners | |

| Face Masks | |

| Other Facial Care Products | |

| Skin Care Products | |

| Body Care Products | Body Lotion |

| Foot and Hand Cream | |

| Other Body Care Products | |

| Lip Care Products |

| Premium |

| Mass |

| Organic |

| Conventional |

| Men |

| Women |

| Kids/Children |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Channels |

| Product Type | Facial Care Products | Cleansers |

| Moisturizers and Creams | ||

| Serums and Essence | ||

| Toners | ||

| Face Masks | ||

| Other Facial Care Products | ||

| Skin Care Products | ||

| Body Care Products | Body Lotion | |

| Foot and Hand Cream | ||

| Other Body Care Products | ||

| Lip Care Products | ||

| Price | Premium | |

| Mass | ||

| Category | Organic | |

| Conventional | ||

| End-User | Men | |

| Women | ||

| Kids/Children | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

Key Questions Answered in the Report

What is the projected value of China skin care products by 2031?

The China skin care products market is projected to reach USD 89.01 billion by 2031, rising from USD 62.9 billion in 2026 at a 7.19% CAGR.

Which product type leads skin care spending in China?

Facial care products lead by a wide margin, accounting for 83.43% of market value in 2025, supported by strong demand for serums, essences, masks, and treatment formats.

Which price tier is growing fastest in China skin care products?

Premium products are growing fastest at 8.11% CAGR through 2031, even though mass products still held the largest share at 66.87% in 2025.

Why is anti-aging so important in China skin care demand?

Anti-aging drives ingredient development, premium conversion, and channel traffic, with online anti-aging sales reaching billion in 2025.

Page last updated on: