Skin Toner Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

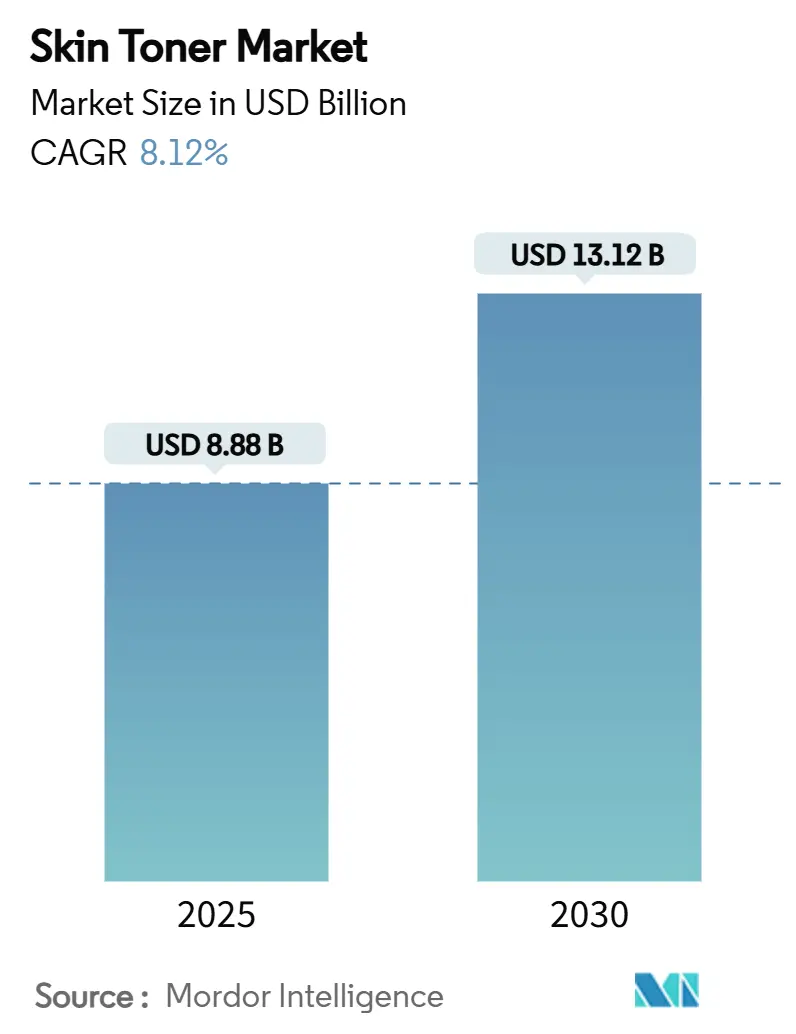

| Market Size (2025) | USD 8.88 Billion |

| Market Size (2030) | USD 13.12 Billion |

| Growth Rate (2025 - 2030) | 8.12% CAGR |

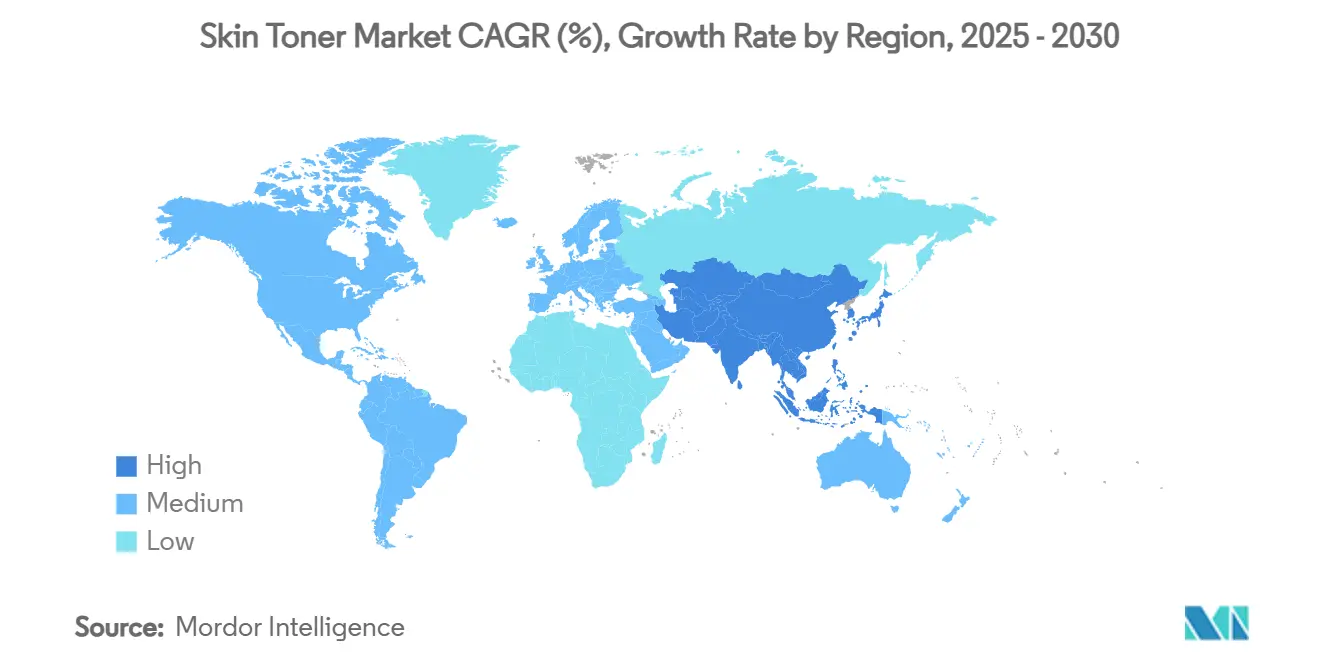

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Skin Toner Market Analysis by Mordor Intelligence

The global skin toner market size is USD 8.88 billion in 2025 and is projected to reach USD 13.12 billion by 2030, expanding at a CAGR of 8.12% during the forecast period. The global skin toner market is witnessing robust growth, driven by increasing consumer awareness of skincare and a demand for targeted, multifunctional products. Data from the U.S. FDA and the European Commission reveal a consumer pivot towards ingredient safety and transparency, propelling the market towards 'clean beauty'. This shift is evident in the surging popularity of alcohol-free toners and those enriched with active ingredients, such as niacinamide, with products like The Ordinary’s Glycolic Acid 7% Toning Solution leading the charge. Once seen merely as cleansing agents, toners are now recognized for their efficacy in addressing acne, hydration, and pigmentation issues. In the Asia-Pacific region, South Korea and Japan are spearheading innovation, with brands like COSRX and Hada Labo introducing toners that harness fermented ingredients and boast low pH formulas. Furthermore, technology is reshaping consumer interactions, as showcased by AI-driven platforms like L’Oréal’s Skin Genius, which offers personalized product recommendations based on skin analysis. The growing influence of social media platforms and beauty influencers is also playing a pivotal role in educating consumers and driving product adoption.

Key Report Takeaways

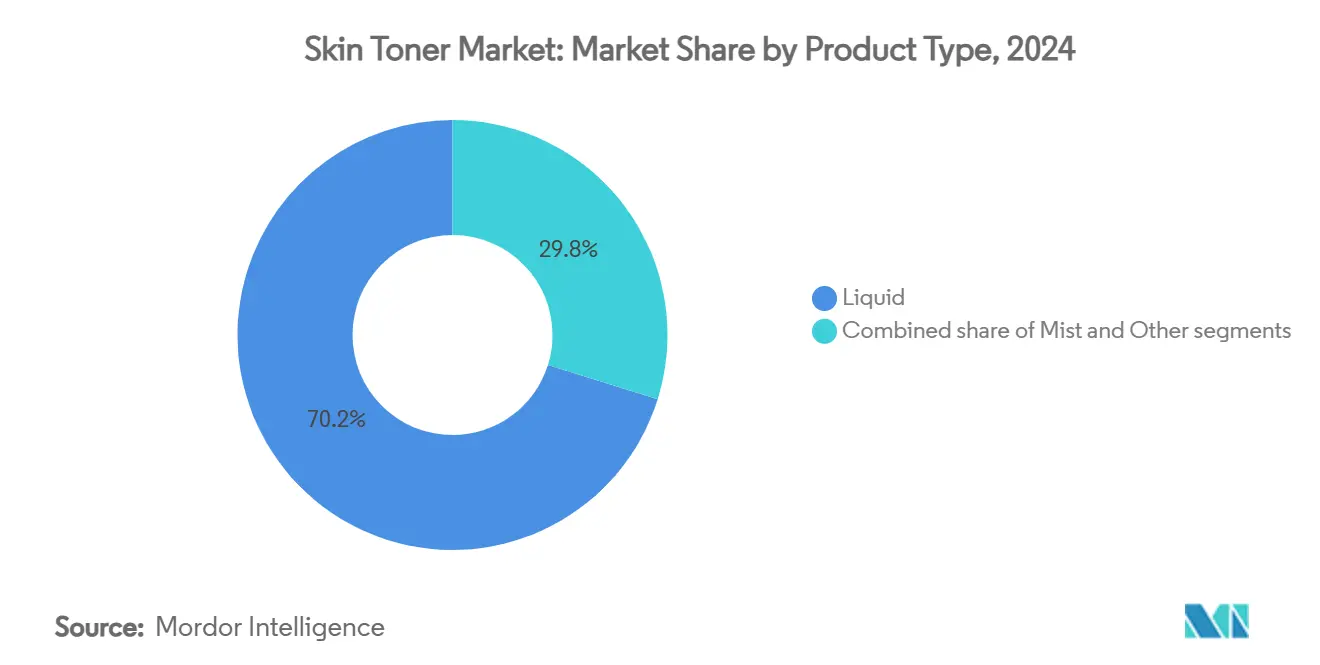

- By product type, liquid formulations held 70.15% of the skin toner market share in 2024, while mist products are projected to expand at a 7.48% CAGR through 2030.

- By category, conventional products accounted for 78.13% of the skin toner market size in 2024, whereas organic and natural alternatives are advancing at an 8.54% CAGR through 2030.

- By end user, adults represented 94.65% of the skin toner market share in 2024, yet children’s products are forecast to grow at an 8.45% CAGR to 2030.

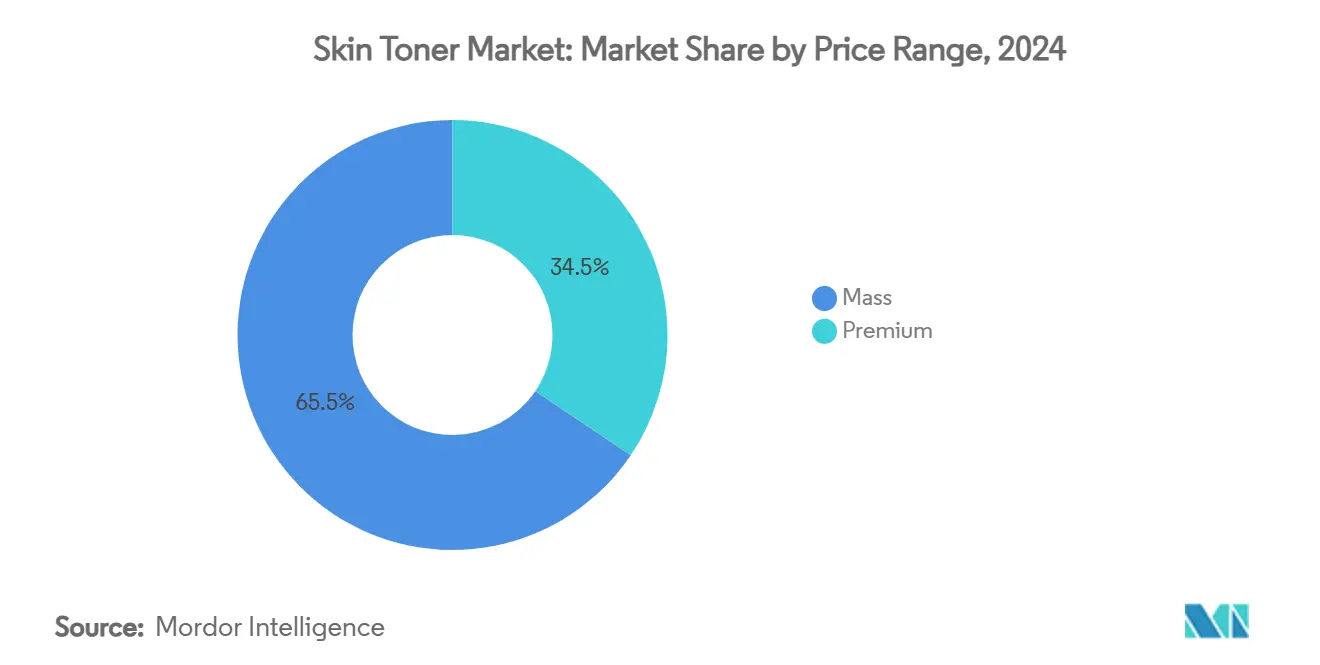

- By price range, mass products dominated with 65.45% of revenue in 2024, while premium and luxury formats are on track for 9.12% CAGR expansion.

- By distribution channel, health and beauty stores held a 34.52% share in 2024, with online channels climbing at an 8.97% CAGR through 2030.

- By geography, in 2024, Asia-Pacific commanded a 32.43% share and is projected to expand at a CAGR of 9.13% through 2030.

Global Skin Toner Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer awareness of skincare routines | +1.5% | Global, strongest in North America and Asia-Pacific cities | Medium term (2-4 years) |

| Demand for natural and chemical-free products | +1.2% | Europe and North America, moving into Asia-Pacific | Long term (≥ 4 years) |

| Advanced active ingredients and premium formulations | +1.0% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Influence of social media and beauty influencers | +1.1% | Global, peak effect among youth in Asia-Pacific and North America | Short term (≤ 2 years) |

| Growing demand for eco-friendly packaging and sustainability | +0.8% | Europe and North America leadership, rising Asia-Pacific adoption | Long term (≥ 4 years) |

| Personalization technology and AI-driven customized products | +0.6% | Tech-forward markets in North America and Europe, selective Asian cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Awareness of Skincare Routines

As consumers become more aware of skincare routines, toners have shifted from being optional to essential in daily regimens. Younger demographics, particularly Generation Alpha, are adopting multi-step routines earlier, a trend heavily influenced by social media and dermatological education. The rise of "skinimalism" underscores the demand for multifunctional products, making toners that hydrate, exfoliate, and address skin concerns increasingly sought after. Platforms inundated with educational content have enlightened consumers about active ingredients like niacinamide, hyaluronic acid, and glycolic acid. Aveeno’s 2024 State of Skin Sensitivity report highlights that 71% of global consumers now report skin sensitivity, fueling a demand for gentle formulations that steer clear of harsh surfactants and allergens [1]Source: Kenvue Inc.," Aveeno State of Sensitivity 2024," aveeno.com. Brands like La Roche-Posay offer a Soothing Lotion Toner, and Aveeno presents the Calm + Restore Toning Lotion, both hypoallergenic and fragrance-free, catering to sensitive skin. KraveBeauty’s Kale-Lalu-yAHA toner, blending glycolic acid with soothing botanicals, showcases the balance of efficacy and gentleness that today’s consumers crave. This heightened ingredient awareness and sensitivity consciousness particularly favors premium, science-backed brands that champion minimalist, transparent, and clinically validated solutions.

Demand for Natural and Chemical-Free Products

The global skin toner market is on an upward trajectory, propelled by a rising appetite for clean and natural formulations. California has set a precedent: for a product to flaunt the labels “organic” or “made with organic,” it must contain a minimum of 70% organic content [2]Source: California Department of Public Health, "Cosmetic Safety Program", cdph.ca.gov. This initiative not only fortifies consumer trust in ingredient authenticity but also champions transparency in the market. Echoing this sentiment, a March 2025 NSF survey highlighted that 74% of U.S. consumers prioritize organic ingredients in their personal care products [3]Source: NSF International, “Global Consumer Insights on Organic Personal Care,” nsf.org. . In response to regulatory clarity and heightened consumer expectations, brands are adapting. Take, for instance, Herbivore’s Jasmine Green Tea Balancing Toner and Indie Lee’s CoQ-10 Toner; both spotlight minimalist, certified formulations that resonate with ingredient-savvy consumers. Shiseido’s toners, infused with fermented camellia seed extract, demonstrate how fermentation innovations can enhance potency while adhering to a natural philosophy. Additionally, Fresh’s Rose Deep Hydration Toner, crafted from rosewater derived from byproduct streams, underscores the importance of sustainable sourcing in bolstering brand credibility. These shifting priorities are set to drive the market's growth through 2030, encompassing both traditional and natural/organic toner categories.

Advanced Active Ingredients and Premium Formulations

As consumer expectations evolve, the skin toner market is witnessing a transformation, driven by advanced active ingredients and premium formulations. Today's shoppers are not just looking for basic hydration; they want toners that deliver visible, dermatologically-proven results. In 2024, Estée Lauder rolled out its Micro Essence Treatment Lotion Fresh, infused with Sakura Ferment. By harnessing the power of fermented sakura and amino acids, the brand targets issues like dullness and uneven texture, catering to the discerning, ingredient-conscious consumer. In a similar vein, Lancôme introduced its Clarifique Refining Enzymatic Dual Essence Toner, which combines glycolic acid and enzymes. This formulation not only refines pores but also enhances skin clarity, effectively positioning the product as both a toner and a gentle exfoliant. Responding to the rising demand for products that are both sensorial and functional, Fresh upgraded its Rose Deep Hydration Facial Toner, now featuring a double rose extract for enhanced hydration and soothing benefits. These instances underscore a shift: premium toners are evolving into treatment-grade solutions, enticing consumers to move away from traditional formats.

Influence of Social Media and Beauty Influencers

Social media and beauty influencers are reshaping product discovery and trust, driving the skin toner market's growth. A 2024 University of Portsmouth survey found that 60% of consumers trust influencer recommendations, with nearly half of purchasing decisions swayed by these endorsements [4]Source: University of Portsmouth, “Influencer Impact on Consumer Skincare Choices,” port.ac.uk. . This shift has led brands to heavily invest in partnerships with creators. Glow Recipe’s Watermelon Glow PHA+BHA Toner went viral on TikTok, trending with #glowrecipe, thanks to endorsements from top influencers like Skincare by Susan and Beauty Within. This buzz led to repeated sellouts at Ulta and Sephora. The Ordinary’s Glycolic Acid 7% Toning Solution, a consistent bestseller, is often highlighted by creators for its budget-friendly effectiveness. Influencer-owned brands are also expanding the category. Hyram Yarbro’s Selfless by Hyram launched its Pore Clearing & Oil Control Toner, which saw a sales surge after promotions on Hyram’s multi-million-follower platforms. These instances underscore how influencer storytelling enhances product credibility and translates social engagement into sales, fueling the global toner market's rapid expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensitivity concerns and potential skin irritation from active ingredients | -0.6% | Global, heightened in North America and Europe | Short term (≤ 2 years) |

| Consumer skepticism and preference for simplified or multifunctional skincare products | -0.5% | Mature markets in North America and Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| DIY solutions like rose water or aloe vera reducing market demand | -0.4% | Asia-Pacific tradition-based buyers and cost-conscious segments worldwide | Medium term (2-4 years) |

| Supply-chain disruptions and raw material price fluctuations | -0.6% | Global, strongest in Middle East and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sensitivity Concerns and Potential Skin Irritation from Active Ingredients

As formulations grow more potent, concerns about sensitivity and potential skin irritation from active ingredients are emerging as significant restraints on the skin toner market's growth. While active ingredients like glycolic acid, salicylic acid, and niacinamide deliver visible results, they also risk causing irritation, dryness, or disrupting the skin barrier, particularly in sensitive skin types. In 2023, a popular K-beauty brand faced consumer backlash after launching a glycolic acid-based toner. Reports of stinging and redness circulated on Reddit and TikTok, leading the brand to revise its formula and issue patch testing warnings. Similarly, despite its popularity, The Ordinary's Glycolic Acid 7% Toning Solution drew criticism for being overly harsh on sensitive or rosacea-prone users. This heightened scrutiny has led some consumers to either avoid toners or pivot to gentler alternatives, dampening adoption in specific segments. Dermatologists and influencers are increasingly warning against the overuse of exfoliating toners, bolstering the belief that high-concentration actives aren't suitable for every skin type. In response, brands are recalibrating by introducing diluted versions, pH-balanced formulas, and fragrance-free options. However, the persistent risk of adverse reactions continues to temper the market's overall expansion.

Consumer Skepticism and Preference for Simplified or Multifunctional Skincare Products

Market growth is being curtailed by consumer skepticism regarding the necessity of toners, coupled with a rising inclination towards simplified or multifunctional skincare routines. A significant number of consumers, especially those leaning into the "skinimalism" trend, are opting for all-in-one products, such as hydrating cleansers or treatment moisturizers, in place of traditional toners. This shift aims to streamline their routines and minimize clutter. In 2023, CeraVe’s Hydrating Cleanser, infused with Niacinamide, emerged as a popular toner substitute. Influencers and dermatologists underscored its dual role in cleansing and bolstering the skin's barrier, thereby diminishing the perceived need for a standalone toner. Likewise, La Roche-Posay’s Toleriane Double Repair Moisturizer is frequently endorsed in toner-free routines, thanks to its combined benefits of hydration, soothing properties, and prebiotic support. With the rising popularity of these hybrid products, consumers are increasingly scrutinizing the added value of toners, especially when alternative steps tout similar or enhanced benefits. This behavioral shift, bolstered by minimalist marketing and expert-driven content, is constricting the toner’s traditional role in skincare routines. This is particularly evident among price-sensitive or time-constrained demographics, leading to a deceleration in the broader adoption of toners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Dominance Faces Mist Innovation

In 2024, liquid formulations command a dominant 70.15% share of the skin toner market. Their popularity stems from compatibility with intricate active ingredient blends and a deep-rooted consumer affinity for traditional skincare rituals. These liquid formulations shine in premium and treatment-focused products, where absorption and efficacy take center stage. Take, for instance, Estée Lauder’s Micro Essence Treatment Lotion and Kiehl’s Iris Extract Activating Treatment Essence. Both exemplify how liquid formats can elevate high-performance routines, targeting key concerns like hydration, firmness, and clarity. Their seamless integration into established multi-step regimens further cements their appeal across a broad spectrum of consumers.

On the other hand, mist formats are rapidly gaining traction, boasting a robust 7.48% CAGR through 2030. Their surge is largely attributed to their convenience, especially for consumers on the move, who prioritize quick and mess-free hydration. Products such as Glow Recipe’s Watermelon Glow Ultra-Fine Mist and Innisfree’s Green Tea Seed Mist highlight this trend, presenting a lightweight and portable solution that marries skincare with a delightful sensory experience. The growing preference for minimalistic and travel-friendly skincare solutions further fuels the demand for mist formats.

By Category: Conventional Strength Meets Natural Acceleration

In 2024, conventional skin toners dominate the market with a commanding 78.13% share, underscoring their lasting appeal to consumers who trust established formulations. Thanks to robust supply chains and competitive pricing, these toners are easily accessible to a wide audience. Brands like Neutrogena, with its Alcohol-Free Toner, and L’Oréal, featuring the HydraFresh Anti-Ox Toner, exemplify the strength of time-tested formulations, consistently appealing to both price-sensitive and mass-market consumers. Additionally, the familiarity and reliability of these products continue to foster consumer loyalty, further solidifying their market position. The segment also benefits from consistent product innovation, such as the introduction of multifunctional toners that combine hydration, exfoliation, and pore-tightening properties.

Meanwhile, organic and natural toners are rapidly gaining traction, boasting the industry's fastest growth rate at a projected CAGR of 8.54% through 2030. This momentum is primarily driven by the burgeoning clean beauty movement and increased focus on ingredient safety. Products such as Pai Skincare’s Rice Plant & Rosemary BioAffinity Toner and Herbivore’s Jasmine Green Tea Balancing Toner highlight the market's shift towards natural and sustainably sourced ingredients. Furthermore, the rising consumer demand for eco-friendly packaging and cruelty-free certifications is amplifying the appeal of this segment. The segment is also benefiting from increased marketing efforts by brands to educate consumers on the benefits of natural ingredients, further accelerating adoption.

By End User: Adult Dominance Challenged by Youth Adoption

In 2024, adults dominate the skin toner market, holding a commanding 94.65% share. This trend is driven by their established skincare routines, strong purchasing power, and a preference for premium, targeted formulations. Adults gravitate towards toners that address anti-aging, hydration, and pore-tightening needs. Products like Kiehl’s Calendula Herbal Extract Toner and Lancôme’s Tonique Confort resonate with this demographic, aligning with mature skin concerns and benefiting from steadfast brand loyalty. Moreover, adults exhibit a keen interest in potent active ingredients, which not only justifies premium pricing but also drives impressive repurchase rates.

Conversely, the children's segment is on a robust growth trajectory, with a projected CAGR of 8.45% through 2030. This expansion is particularly notable in developed markets, where early skincare education and parental guidance are paramount. Social media platforms, especially TikTok, have emerged as influential players, seamlessly integrating skincare routines into the daily lives of pre-teens and molding their aspirational habits. In response, brands are introducing products specifically designed for younger audiences. Products like Evereden’s Balancing Face Toner and Bubble’s Bounce Back Toner, both dermatologist-tested and devoid of harsh actives, are gaining traction in the tween market. These introductions highlight a rising demand for safe, age-appropriate skincare solutions, a demand further intensified by education-centric marketing strategies.

By Price Range: Mass Appeal Versus Premium Growth

In 2024, mass market toners capture a dominant 65.45% market share, thanks to their affordability, frequent repurchases, and easy retail access. Leading brands like Neutrogena, Clean & Clear, and L’Oréal Paris cater to middle-income consumers with reliable, dermatologist-tested products priced below INR 500 (or USD 10). These products are prominently available in supermarkets, drugstores, and online platforms, ensuring they are both visible and accessible. Furthermore, brands often employ bundling strategies, such as offering cleanser-toner-moisturizer kits, to boost sales volume. A standout feature of this segment is its agility in addressing trending concerns, be it acne, oil control, or hydration, without necessitating extensive consumer education.

The premium/luxury toner segment is on an upward trajectory, projected to grow at a 9.12% CAGR through 2030. This growth is driven by consumers increasingly seeking targeted, scientifically-backed skincare solutions. For example, Lancôme’s Tonique Confort and Shiseido’s Eudermine Revitalizing Essence Toner, for instance. Both epitomize this trend, boasting advanced formulations and unique sensory experiences that justify their premium pricing. Lancôme’s Tonique Confort, enriched with acacia honey and sweet almond oil, offers deep hydration, making it a favorite among mature and dry skin consumers who value comfort. On the other hand, Shiseido’s Eudermine, with its fermented ingredients and storied brand heritage, positions itself as a time-tested revitalizing treatment.

By Distribution Channel: Traditional Retail Meets Digital Acceleration

In 2024, health and beauty stores command a dominant 34.52% share of the distribution landscape, highlighting their pivotal role as trusted destinations for skincare purchases. These outlets leverage in-person consultations, curated product assortments, and immediate access, fostering customer trust and encouraging product trials. Retail giants like Watsons, Ulta Beauty, and Shoppers Drug Mart are not just retailers; they're educators, offering informed merchandising and trained staff guidance, especially on frequently purchased items like toners. Positioned as hubs for product discovery, these stores are instrumental in amplifying brand exposure and facilitating initial product adoption, particularly in emerging markets with evolving skincare routines.

Online retail is rapidly emerging as the dominant channel, boasting a robust CAGR of 8.97% projected through 2030, driven by a consumer appetite for convenience and tailored shopping experiences. Leading platforms like Nykaa in India, Tmall in China, and Soko Glam in the U.S. are harnessing AI-driven recommendation engines and virtual consultations to refine the shopping journey. Brands such as Paula’s Choice and Drunk Elephant are capitalizing on direct-to-consumer strategies, rolling out exclusive bundles, subscription services, and loyalty initiatives to bolster consumer ties. The Asia-Pacific region showcases digital prowess, with online beauty purchases constituting high sales in China and Korea. Meanwhile, omnichannel approaches like L'Oréal’s “Click & Collect” and Sephora’s app-driven skin assessments are seamlessly merging online research with offline shopping, crafting a cohesive purchasing journey that benefits both digital platforms and physical stores.

Geography Analysis

In 2024, Asia-Pacific not only holds the largest market share at 32.43% but also emerges as the fastest-growing region, boasting a 9.13% CAGR projected through 2030. The region's growth is propelled by ingrained beauty rituals, skincare education amplified by social media, and an uptick in disposable incomes. South Korea's K-beauty routines, emphasizing hydration and skin preparation, prominently feature toners like Laneige’s Cream Skin Refiner and Innisfree’s Green Tea Balancing Toner. Meanwhile, Japan's skincare landscape is dominated by brands like Hada Labo, known for their minimalist and science-driven formulations.

North America and Europe stand as mature markets, where the principles of clean beauty, potent actives, and ingredient transparency shape consumer choices. In North America, leading toners such as Paula’s Choice Skin Balancing Pore-Reducing Toner and Thayers Witch Hazel Toner resonate with a discerning clientele, owing to their targeted, dermatologist-backed benefits. European markets, particularly Germany and France,has a tradition of pharmacy-centric skincare brands like La Roche-Posay and Bioderma dominate pharmacy aisles, while the rising demand for sustainable, non-toxic formulations sees clean beauty brands like REN Clean Skincare gaining traction..

While South America, the Middle East, and Africa are slowly integrating skin toners into their skincare regimens, challenges like underdeveloped infrastructure and regulatory inconsistencies hinder widespread adoption. In Brazil, heightened skincare awareness and the influence of local marketing are propelling brands like Natura into the forefront of the toner category. The Middle East's burgeoning appetite for halal-certified beauty sees brands like MooGoo and Saeed Ghani making inroads or amplifying their presence.

Competitive Landscape

The skin toner market features a moderately fragmented landscape marked by fierce competition between global players like L'Oréal, Estée Lauder, and Shiseido employ a blend of clinical positioning, celebrity endorsements, and dermatological credibility in their multi-channel marketing, bolstering consumer trust. K-beauty frontrunners, including Sulwhasoo and Missha, captivate digitally savvy audiences with their minimalist branding, rapid innovation, and ingredient-centric narratives, particularly emphasizing fermentation and botanical actives. Simultaneously, brands like The Ordinary and CeraVe, straddling the 'masstige' segment, attract discerning, value-driven consumers with their high-efficacy claims and transparent pricing.

In the toner market, technology is not just an add-on; it's a pivotal differentiator. L'Oréal, in collaboration with IBM, has rolled out the AI-driven Cell BioPrint system, enabling real-time skin analysis for personalized toner recommendations, mimicking the expertise of in-store consultations. Shiseido, on the other hand, is anchoring its premium offerings in science, investing in biotech innovations like fermented camellia seed extract and OBP2A protein delivery. Meanwhile, indie and direct-to-consumer brands are harnessing virtual skin diagnostics and augmented reality try-ons, amplifying both engagement and conversion rates.

To solidify their market stance, companies are embracing a spectrum of strategies, from acquisitions to innovations spurred by regulatory changes. Beauty behemoths are not just eyeing tech-savvy disruptors but also niche ingredient pioneers, bolstering their innovation trajectories. Furthermore, brands are venturing into overlooked segments, introducing age-specific toners for Generation Alpha and pioneering refillable packaging systems. These initiatives not only resonate with the values of sustainability and personalization but also serve as a buffer against market volatility.

Skin Toner Industry Leaders

-

L'Oréal S.A.

-

The Estée Lauder Companies Inc.

-

Shiseido Company, Limited

-

The Procter & Gamble Company

-

Kenvue Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Estée Lauder partnered with India’s Startup India to fund women-founded beauty ventures aimed at product innovation and domestic manufacturing.

- May 2024: Amorepacific’s Hanyul line entered the United States exclusively through Sephora, highlighting Korean botanicals such as yuja and artemisia in toner formulations.

- March 2024: Kao Corporation launched carbonated foam toners under Sensai, Kanebo, and Curél to deliver active ingredients through enhanced micro-bubbles

Global Skin Toner Market Report Scope

| Liquid |

| Mist |

| Others |

| Organic and Natural |

| Conventional |

| Adults |

| Kids/Children |

| Mass |

| Premium/Luxury |

| Supermarkets/Hypermarkets |

| Beauty and Health Stores |

| Online Retail Stores |

| Others Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Liquid | |

| Mist | ||

| Others | ||

| By Category | Organic and Natural | |

| Conventional | ||

| By End User | Adults | |

| Kids/Children | ||

| By Price Range | Mass | |

| Premium/Luxury | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Beauty and Health Stores | ||

| Online Retail Stores | ||

| Others Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global skin toner market in 2030?

The forecast places the skin toner market at USD 13.12 billion by 2030.

Which region leads growth in the category?

Asia-Pacific holds the largest share and is expanding at more than 9% CAGR through 2030.

Which product format dominates sales?

Liquid toners generated over 70% of 2024 revenue due to versatility and ingredient-rich formulas.

How fast are premium price tiers growing?

Premium and luxury toners are advancing at about 9.12% CAGR, outpacing the overall market.

Page last updated on: