Self-Tanning Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

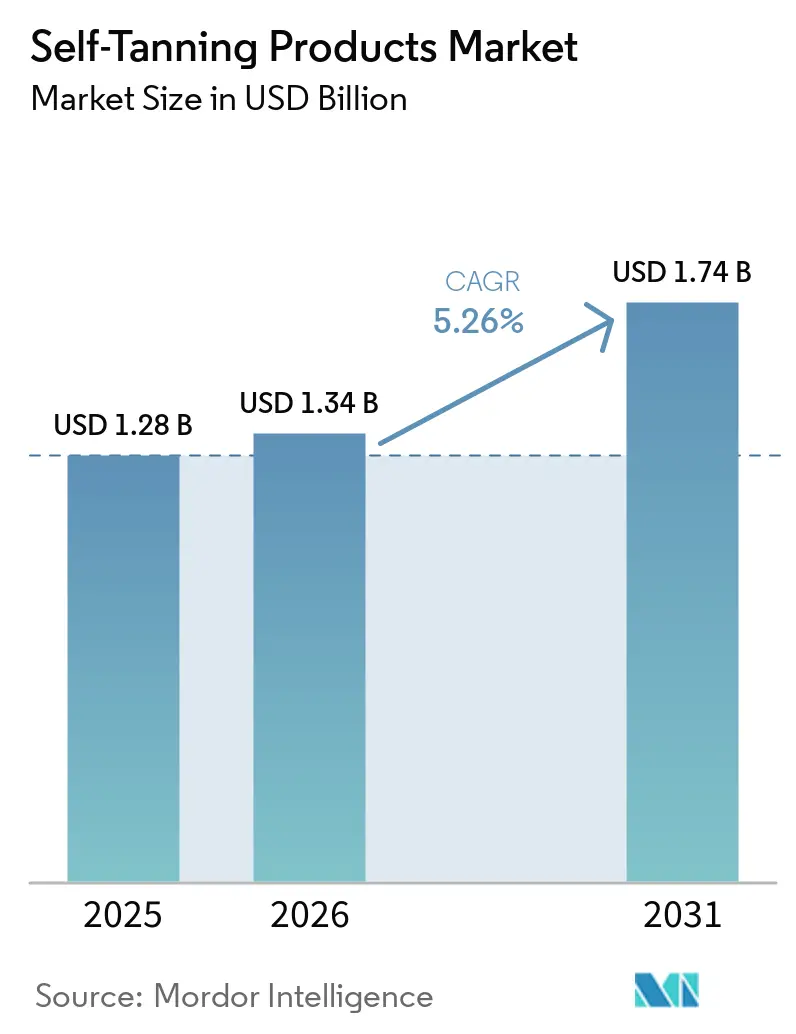

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-Tanning Products Market Analysis by Mordor Intelligence

The global self-tanning market was valued at USD 1.28 billion in 2025 and is projected to grow from USD 1.34 billion in 2026 to USD 1.74 billion by 2031, registering a CAGR of 5.3% during the forecast period (2026–2031). Market growth is primarily driven by increasing consumer awareness regarding the health risks associated with ultraviolet (UV) exposure, accelerating the shift from traditional sunbathing toward safer sunless tanning solutions. Rising consumer preference for convenient, at-home beauty and personal care products is further supporting market expansion. The market is also benefiting from growing dermatological endorsement of self-tanning products as a safer cosmetic alternative to UV-based tanning methods. Additionally, evolving beauty standards, premium skincare integration, and rising demand for multifunctional formulations are strengthening product adoption across key consumer segments. However, market growth is moderately constrained by stringent regulatory requirements surrounding ingredient safety, particularly related to formulation standards and product compliance across major markets. Despite these challenges, increasing e-commerce penetration, recurring consumer purchasing behavior, and sustainability-driven packaging innovation are expected to create significant growth opportunities for the market over the forecast period.

Key Report Takeaways

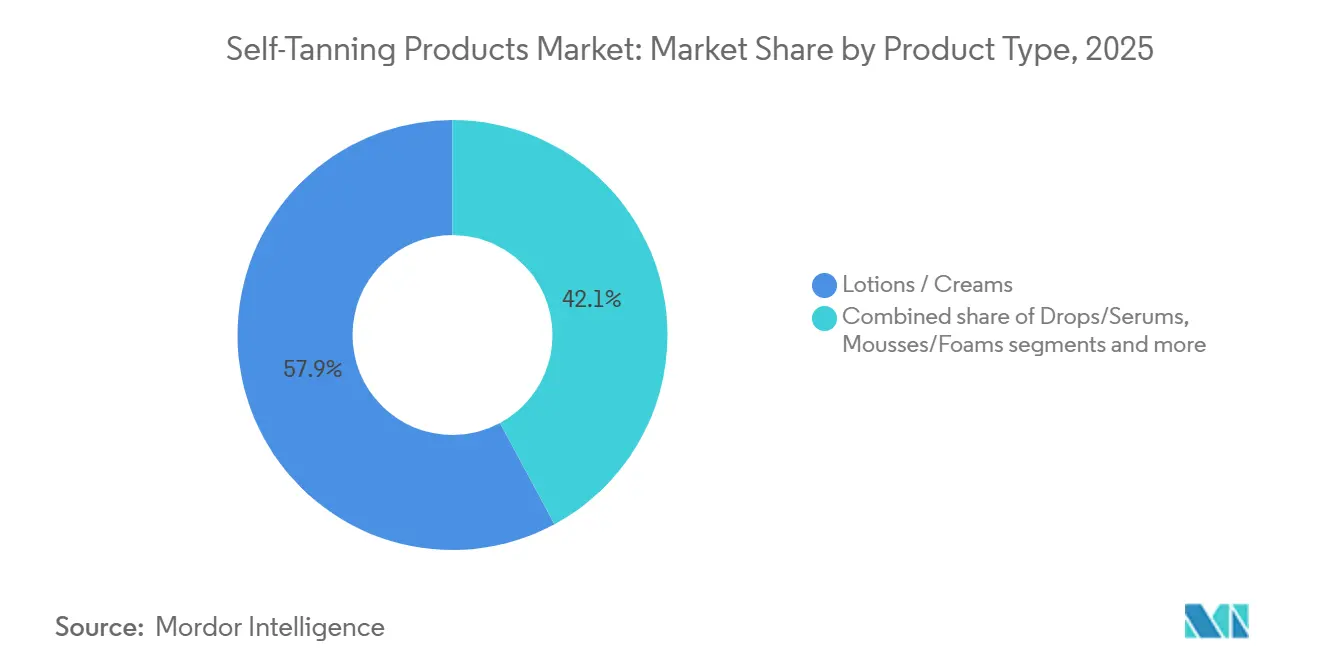

- By product type, lotions and creams led with 57.9% revenue share in 2025, while drops and serums are forecast to expand at 6.9% CAGR through 2031.

- By nature, conventional products held 87.3% of revenue in 2025, while organic and vegan self-tanners are projected to record the highest CAGR at 7.8% through 2031.

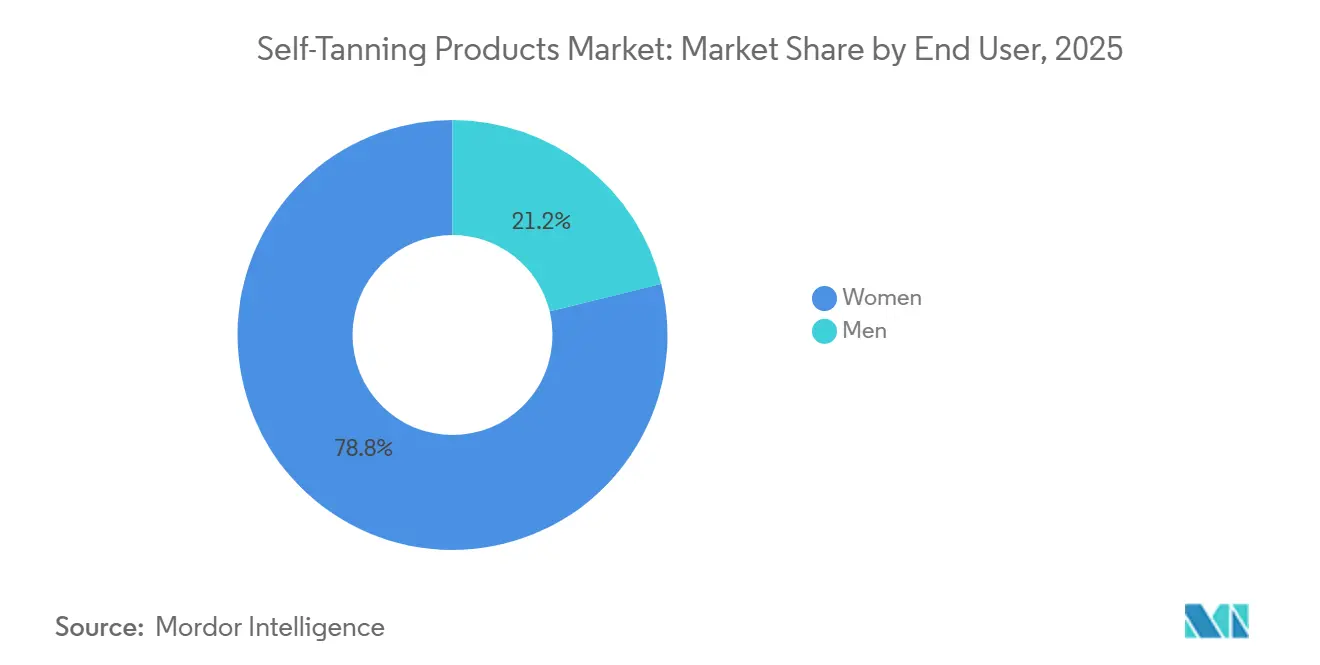

- By end-user, women accounted for 78.8% of revenue in 2025, while men are expected to post the fastest CAGR at 7.5% through 2031.

- By distribution channel, specialty beauty stores held 57.1% of the self-tanning market share in 2025, while online retail stores are projected to advance at 7.1% CAGR through 2031.

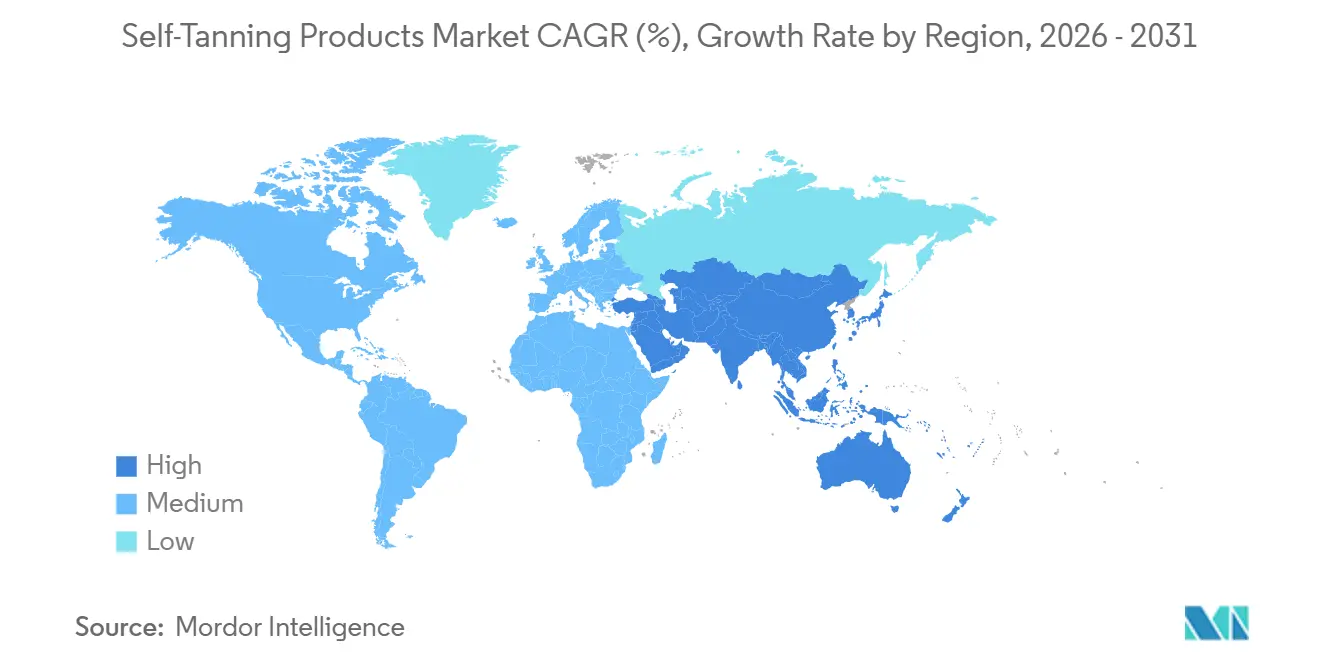

- By geography, North America captured 36.4% of the self-tanning market size in 2025, while Asia-Pacific is forecast to grow at the fastest CAGR of 7.7% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Self-Tanning Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE | |

|---|---|---|---|

| Rising Awareness of UV Radiation Risks And Sun Exposure | +1.4% | Global, with stronger impact in North America and Europe | Short term (≤ 2 years) |

| Growing Demand For Safer Sunless Tanning Alternatives | +1.2% | Global, particularly in high UV exposure regions | Medium term (2-4 years) |

| Evolving Beauty Trends Favoring Tanned Skin | +0.9% | Global, with emphasis on Asia-Pacific and North America | Short term (≤ 2 years) |

| Increasing Preference For Healthy, Glowing Skin | +0.8% | Global, with premium market focus | Medium term (2-4 years) |

| Strong Influence Of Celebrities And Social Media | +0.7% | Global, strongest in digitally connected markets | Short term (≤ 2 years) |

| Rising Demand For Vegan And Sustainable Products | +0.6% | Europe and North America primarily, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Awareness of UV Radiation Risks

The self-tanning market is gaining significant momentum due to growing medical evidence linking ultraviolet (UV) exposure to melanoma and other skin-related health risks. According to the International Agency for Research on Cancer (IARC), over 80% of the 332,000 global cutaneous melanoma cases reported in 2022 were attributed to UV radiation exposure. Additionally, annual melanoma cases are projected to exceed 510,000 by 2040, reinforcing the urgency of UV risk awareness and preventive healthcare measures [1]Source: International Agency for Research on Cancer, “More than 80% of Melanoma Cases Worldwide Attributable to Ultraviolet Radiation Exposure,” IARC Press Release, iarc.who.int. This increasing health awareness is reshaping consumer behavior, shifting demand toward safer sunless tanning alternatives. The trend is particularly prominent in regions such as North America, Australia, and Northern Europe, where strong public health campaigns and high awareness of UV-related risks continue to influence purchasing decisions. As a result, the self-tanning market is witnessing growing adoption among consumers seeking cosmetic tanning solutions without direct sun exposure.

Growing Demand For Safer Sunless Tanning Alternatives

The self-tanning market is expanding as consumers increasingly seek a tanned appearance without the health risks associated with sun exposure and tanning beds. DHA-based self-tanning products offer a safe and convenient alternative by creating a temporary tan through a reaction with amino acids in the outer skin layer, eliminating the need for UV exposure. This has positioned self-tanning products as a practical substitute for traditional tanning methods rather than merely a cosmetic enhancement. Regulatory guidelines further support the shift toward topical self-tanning products. The U.S. FDA permits DHA only for external application and does not approve full-body spray tanning involving potential inhalation or mucous membrane exposure [2]Source: U.S. Food and Drug Administration, “Sunless Tanners & Bronzers,” FDA, fda.gov. This regulatory distinction is driving higher consumer preference for retail-friendly formats such as creams, lotions, drops, and mousses, which offer greater convenience, control, and perceived safety for at-home use. As a result, market growth is being driven not only by rising awareness of UV-related skin damage but also by increasing consumer demand for safer, easy-to-use, and self-applied tanning solutions.

Strong Influence of Celebrities And Social Media

The self-tanning market is increasingly influenced by digital and social media platforms, where product discovery, consumer education, and repeat purchases are accelerating. Visual content such as short-form videos has become highly effective in demonstrating application techniques, before-and-after results, and shade selection, helping consumers better understand product performance and usage. This plays a critical role in the self-tanning market, as purchasing decisions are strongly influenced by visible results, ease of application, and confidence in achieving streak-free outcomes. Celebrity endorsements and influencer partnerships further strengthen brand visibility by enhancing consumer trust, expanding audience reach, and reinforcing aspirational lifestyle positioning. The impact is particularly significant for specialist and direct-to-consumer brands that depend on strong digital engagement and rapid consumer feedback. As a result, the self-tanning market remains highly dynamic, with demand increasingly shaped by social media trends, product innovation, and content-driven purchasing behavior.

Rising Demand For Vegan And Sustainable Products

The self-tanning market is witnessing growing demand for vegan, cruelty-free, and sustainable products as clean beauty preferences continue to influence mainstream consumer purchasing behavior. In response, manufacturers are increasingly investing in plant-based and bioengineered ingredients, along with certified formulations, to strengthen product credibility and meet evolving consumer expectations. Sustainability is also becoming a key differentiator in product packaging. Packaging is also becoming more important because the European Union packaging regulation that applies from August 2026 introduces stricter recyclability and recycled content requirements across cosmetics [3]Source: European Commission, “Regulation EU 2025/40 on Packaging and Packaging Waste,” EUR-Lex, eur-lex.europa.eu. While these regulatory changes add operational complexity and compliance costs, they also create opportunities for brands to strengthen premium positioning through sustainability-led differentiation. As a result, the self-tanning market in North America and Europe is increasingly shifting toward a value proposition centered on high-quality formulations, clean-label claims, and sustainable packaging innovation.

Restraints Impact Analysis*

| RESTRAINT | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE | |

|---|---|---|---|

| Strict Ingredient Safety Regulations | -0.9% | Europe and North America | Medium term (2-4 years) |

| Limited Awareness of Self-Tanning Products | -0.6% | Asia-Pacific, Middle East and Africa, and South America | Short term (≤ 2 years) |

| Risk of Skin Irritation And Allergies | -0.5% | Global, with higher impact in sensitive skin demographics | Long term (≥ 4 years) |

| Sustainability And Packaging Concerns | -0.4% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Ingredient Safety Regulations

Skin sensitivity and allergic reactions remain significant challenges restraining the growth of the self-tanning products market. According to a 2024 study published by PubMed Central, all 44 self-tanning products analyzed across 17 brands contained at least one potential allergen, with an average of nearly 12 allergens identified per product[4]Source: U.S. Food and Drug Administration, “21 CFR § 73.2150, Dihydroxyacetone,” Code of Federal Regulations, law.cornell.edu. In the United States, regulatory restrictions limit DHA use to external application and do not fully approve all-over spray booth tanning, keeping portions of the professional tanning segment under continued regulatory scrutiny. These compliance requirements impact market participants differently, with large companies better positioned to absorb regulatory and testing costs through broader product portfolios, while smaller brands face greater challenges related to reformulation, compliance timelines, and higher operational costs. Although the self-tanning market continues to expand, stringent regulations remain a key restraint by slowing product innovation, limiting formulation flexibility, and increasing the cost of market expansion across regions.

Risk of Skin Irritation And Allergies

The self-tanning market also faces ongoing challenges related to skin irritation, allergic reactions, fragrance sensitivity, and concerns over inconsistent cosmetic results. Consumer hesitation remains high, particularly among first-time users and individuals with sensitive skin, due to concerns such as streaking, uneven application, and potential skin discomfort. Safety concerns associated with certain application methods further influence consumer confidence, particularly where exposure to sensitive areas may occur. In response, manufacturers are increasingly focusing on gentler formulations by reducing DHA concentration, incorporating complementary ingredients such as erythrulose, eliminating fragrances, and adding skincare-focused ingredients to improve skin compatibility. Product innovation is increasingly centered on formulations enriched with hydrating and skin-soothing ingredients, helping brands position self-tanning products as safer and more skin-friendly. As a result, the market is becoming increasingly segmented between mass-market products and premium formulations designed for sensitive skin. While this trend supports value growth through premiumization, it may also limit broader market penetration by maintaining higher product differentiation and pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Serums And Drops Reshaping The Premium Tier

Lotions and creams accounted for 57.9% of the self-tanning market share in 2025, maintaining dominance due to strong consumer familiarity, wide retail availability, and affordable pricing across both mass-market and premium segments. These formats remain a key revenue contributor as they integrate easily into daily body care routines, supporting repeat purchases from existing users while also attracting first-time buyers. Mousses and foams also hold a significant position in the market, driven by consumer preference for faster drying times and easier application.

Meanwhile, drops and serums are projected to grow at a CAGR of 6.9% through 2031, emerging as the fastest-growing product segment. Growth is largely driven by rising demand for multifunctional beauty products that combine tanning benefits with skincare properties. These formats offer buildable coverage, greater application control, and lower risk of uneven results, making them particularly appealing to premium and skincare-focused consumers. The self-tanning market is also witnessing growing demand for gradual tanning products integrated into moisturizers and skincare routines. This trend is expanding category reach by attracting first-time users seeking subtle, customizable results with reduced concerns around streaking, uneven tone, or over-application. As a result, product innovation is increasingly centered on skincare-infused, user-friendly formulations that enhance convenience and improve consumer confidence.

By Nature: Organic Segment Accelerates As Clean Label Expectations Rise

Conventional products accounted for 87.3% of revenue in the nature segment in 2025, highlighting their continued dominance in the self-tanning market. This leadership is driven by established DHA-based formulations, cost-effective production, and strong distribution across pharmacies, mass retail, and beauty stores. Conventional products also offer greater scalability and consistent supply, enabling broad availability across multiple price segments.

In contrast, organic and vegan products are projected to grow at a CAGR of 7.8% through 2031, making them the fastest-growing segment within the market. Growth is primarily fueled by rising consumer demand for plant-based ingredients, cruelty-free formulations, and clean-label beauty products. Increasing retailer focus on sustainable and transparent product portfolios is further accelerating adoption. The organic segment is gaining stronger market credibility as brands invest in advanced formulations that combine clean-label positioning with product performance. Regulatory scrutiny around sustainability, ingredient transparency, and product labeling, particularly in Europe is further encouraging manufacturers to strengthen compliance and clean formulation strategies.

By End-User: Men Add New Growth While Women Remain The Core Base

Women accounted for 78.8% of revenue in 2025, maintaining their position as the dominant end-user segment in the self-tanning market. This leadership is supported by strong product familiarity, wider product availability, and higher repeat purchase rates across multiple categories, including facial tanning, body tanning, express formulas, and gradual tanning products. Women also continue to drive brand engagement through greater experimentation with product formats, shade selection, and multi-step tanning routines.

However, the male segment is projected to register the fastest CAGR of 7.5% through 2031, making it a key growth opportunity within the market. This growth is driven by evolving grooming trends, increasing focus on fitness and appearance, and rising adoption of skincare products among younger male consumers. To capture this expanding segment, brands are increasingly introducing products with lightweight textures, low-residue formulations, and neutral fragrance profiles aligned with male preferences. Initial adoption among men is largely concentrated in gradual tanning and moisturizer-based products, as these formats offer subtle results, easier application, and lower perceived risk.

By Distribution Channel: E Commerce Builds the Repeat Purchase Loop

Specialty beauty stores accounted for 57.1% of revenue in 2025, making them the leading distribution channel in the self-tanning market. Their strong market position is driven by in-store product education, expert merchandising, and personalized guidance, which help reduce consumer hesitation in a category where application technique significantly influences results. Meanwhile, hypermarkets and supermarkets continue to play an important role in driving sales of value-oriented and mass-market products, particularly lotions and gradual tanning products.

Online retail stores are projected to register the fastest CAGR of 7.1% through 2031, driven by growing consumer preference for convenience, easy product replenishment, and broader product accessibility. Digital channels also enable brands to strengthen customer engagement through subscriptions, online communities, personalized recommendations, and continuous product education. In addition, e-commerce platforms support cross-selling opportunities for complementary products such as tanning mitts, primers, and face-specific formulations. Although pharmacies and convenience stores remain relevant for niche and convenience-driven purchases, online channels are becoming increasingly critical for long-term market expansion. As a result, successful market participants are increasingly adopting omnichannel strategies that combine strong specialty retail presence with robust digital and direct-to-consumer capabilities.

Geography Analysis

North America accounted for 36.4% of global revenue in 2025, maintaining its position as the largest regional market for self-tanning products. Regional growth is supported by high consumer spending on beauty and personal care products, strong retail penetration, and widespread awareness of sunless tanning as a safer alternative to UV exposure. The United States remains the largest contributor, supported by established retail networks and strong brand presence across both premium and mass-market segments. Canada and Mexico further contribute to regional growth through rising product adoption and expanding consumer interest in convenient tanning solutions.

Europe represents the second-largest regional market and continues to play a major role in shaping product standards through strict regulatory oversight. Key markets such as Germany, the United Kingdom, France, and Spain drive regional demand, supported by strong consumer awareness of UV-related health risks and growing preference for safer tanning alternatives. The region is also witnessing increasing demand for skincare-infused tanning products, particularly premium formats such as drops and serums. Regulatory developments related to packaging sustainability, product labeling, and ingredient safety continue to influence innovation and product positioning across the European market.

Asia-Pacific is projected to register the fastest CAGR of 7.7% through 2031, making it the fastest-growing regional market. Growth is driven by rising disposable income, expanding beauty and skincare spending, and increasing product awareness through digital platforms. Australia remains a key mature market, while China and India offer strong long-term growth opportunities due to expanding urban consumer bases and increasing skincare adoption. South Korea is also contributing to regional growth through product innovation and strong demand for advanced beauty formulations.

South America is emerging as a developing market, supported by growing beauty consciousness and rising consumer demand in countries such as Brazil and Argentina. Meanwhile, the Middle East & Africa represents the smallest regional market but offers selective growth opportunities, particularly in premium beauty segments across markets such as the UAE and South Africa. Overall, global market expansion is increasingly supported by rising adoption across emerging economies alongside continued growth in established markets.

Competitive Landscape

The self-tanning market is moderately fragmented, with competition driven by both large multinational personal care companies and specialized self-tanning brands. Major players such as L’Oréal, Beiersdorf, Kenvue, and PZ Cussons benefit from strong brand portfolios, extensive R&D capabilities, and broad retail distribution. At the same time, specialist brands such as Coco & Eve, Tan-Luxe, Loving Tan, and Bondi Sands remain highly competitive by leveraging product innovation, strong digital engagement, and performance-driven branding. This competitive mix prevents market concentration and keeps innovation cycles relatively fast, particularly in premium product categories.

Product innovation remains a key competitive differentiator, as companies increasingly compete on tanning finish, undertone compatibility, formulation quality, skin feel, and skincare benefits. Premium segments such as drops and serums are becoming major growth areas due to their ability to support higher pricing and incorporate value-added ingredients such as hyaluronic acid, niacinamide, and peptides. Clean-label formulations, skin-friendly ingredients, and sustainability-focused product development are also becoming increasingly important, particularly in Europe where regulatory compliance and environmental standards strongly influence retail positioning.

Channel expansion and omnichannel execution are equally critical to competitive success. Companies are increasingly balancing specialty retail visibility with strong e-commerce and direct-to-consumer strategies to drive both product discovery and repeat purchases. Strategic retail partnerships, portfolio expansion, and adjacent category innovation continue to shape market dynamics. Overall, the self-tanning market is expected to remain highly competitive, with long-term success dependent on innovation speed, retail penetration, digital brand engagement, and consistent product performance.

Self-Tanning Products Industry Leaders

L’Oréal SA

Kao Corporation

PZ Cussons plc

Beiersdorf AG

Natura & Co Holding SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Palm Beach Tan expanded its footprint by acquiring 14 Bodyheat Tanning salons in Las Vegas. Eight locations will be rebranded and remodeled, while six will merge with nearby existing outlets. This acquisition increases the company’s presence to 648 locations across 35 states and strengthens its position in the Las Vegas market.

- March 2026: Coco & Eve launched Sunny Honey Protect, a glow-focused SPF product line designed to complement self-tanning routines. Available through Ulta Beauty and the brand’s official website, the launch expands Coco & Eve’s portfolio by bridging self-tanning with sun protection, marking a major category expansion for the brand.

- June 2025: James Read introduced a skincare-focused self-tanning line to the United States market through a partnership with Credo Beauty. The Self Glow collection featured four vegan, sustainable products, marking Credo Beauty's first complete sunless tanning range.

- January 2025: Loving Tan sought to redefine the self-tan market with the introduction of its express face and body tanning serums. The 2 HR Express Face Tanning Serum (GBP 32 for 30ml) and the 2 HR Express Tanning Lotion (GBP 32 for 100ml) designed to provide "skin-loving" benefits while achieving a natural-looking tan within just 2 hours

Global Self-Tanning Products Market Report Scope

Self-tanning products are cosmetic formulations designed to provide a tanned or bronzed appearance without exposure to ultraviolet (UV) radiation. These products typically contain Dihydroxyacetone (DHA), an active ingredient that reacts with amino acids in the outer layer of the skin to create a temporary tanning effect. The Self-Tanning Market Report analyzes the market across multiple segments, including product type, nature, end user, distribution channel, and geography. By product type, the market is segmented into lotions/creams, mousses/foams, drops/serums, sprays/mists, and other product types. Based on nature, the market is categorized into organic and conventional products. By end user, the market is segmented into women and men. Based on distribution channel, the market includes hypermarkets/supermarkets, specialty beauty stores, online retail stores, convenience stores, and other channels. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, South America, and Middle East and Africa. Market forecasts are provided in terms of both value (USD)

| Lotions/Creams |

| Mousses/Foams |

| Drops/Serums |

| Sprays/Mists |

| Other Product Types (Wipes, etc.) |

| Organic |

| Conventional |

| Women |

| Men |

| Hypermarkets/Supermarkets |

| Specialty Beauty Stores |

| Online Retail Stores |

| Convenience Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Italy | |

| Sweden | |

| Norway | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Lotions/Creams | |

| Mousses/Foams | ||

| Drops/Serums | ||

| Sprays/Mists | ||

| Other Product Types (Wipes, etc.) | ||

| By Nature | Organic | |

| Conventional | ||

| By End-User | Women | |

| Men | ||

| By Distribution Channel | Hypermarkets/Supermarkets | |

| Specialty Beauty Stores | ||

| Online Retail Stores | ||

| Convenience Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Norway | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the self-tanning sector by 2031?

It is expected to reach USD 1.74 billion by 2031, up from USD 1.34 billion in 2026, at a 5.3% CAGR.

Which product format is growing the fastest?

Drops and serums are the fastest growing product type, with a forecast CAGR of 6.9% through 2031.

Which buyer group remains the largest?

Women remain the largest end-user group, accounting for 78.8% of revenue in 2025, even as men post faster growth.

Which region leads revenue and which region grows the fastest?

North America led with 36.4% share in 2025, while Asia-Pacific is projected to record the fastest CAGR at 7.7% through 2031.

Page last updated on: