Russia Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.36 Billion |

| Growth Rate (2026 - 2031) | 3.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Folding Carton Market Analysis by Mordor Intelligence

The Russia folding carton market size is projected to expand from USD 1.12 billion in 2025 and USD 1.16 billion in 2026 to USD 1.36 billion by 2031, registering a CAGR of 3.23% between 2026 and 2031. A rapid escalation of extended producer responsibility targets, rising from 55% in January 2025 to full compliance in 2027, is tilting material choice toward higher-recycled grades. Margin compression is intensifying because virgin kraftliner prices averaged RUB 56,122 per metric ton (USD 594.3 per metric ton) in March 2026, even as finished carton prices slipped in early 2026, widening the cost-price gap that favors vertically integrated mills over stand-alone converters. E-commerce demand, although no longer surging at pandemic-era rates, continues to anchor incremental growth as Wildberries and Ozon tighten packaging specifications that mandate recyclable, stackable formats. At the same time, digital printing investments by Kappa Rus and Printomir are reshaping run-length economics, enabling converters to monetize personalization and variable data. Domestic processed-food and pharmaceutical localization programs further amplify folding-carton uptake by requiring on-shore primary and secondary packaging that meets new traceability and food-contact rules.

Key Report Takeaways

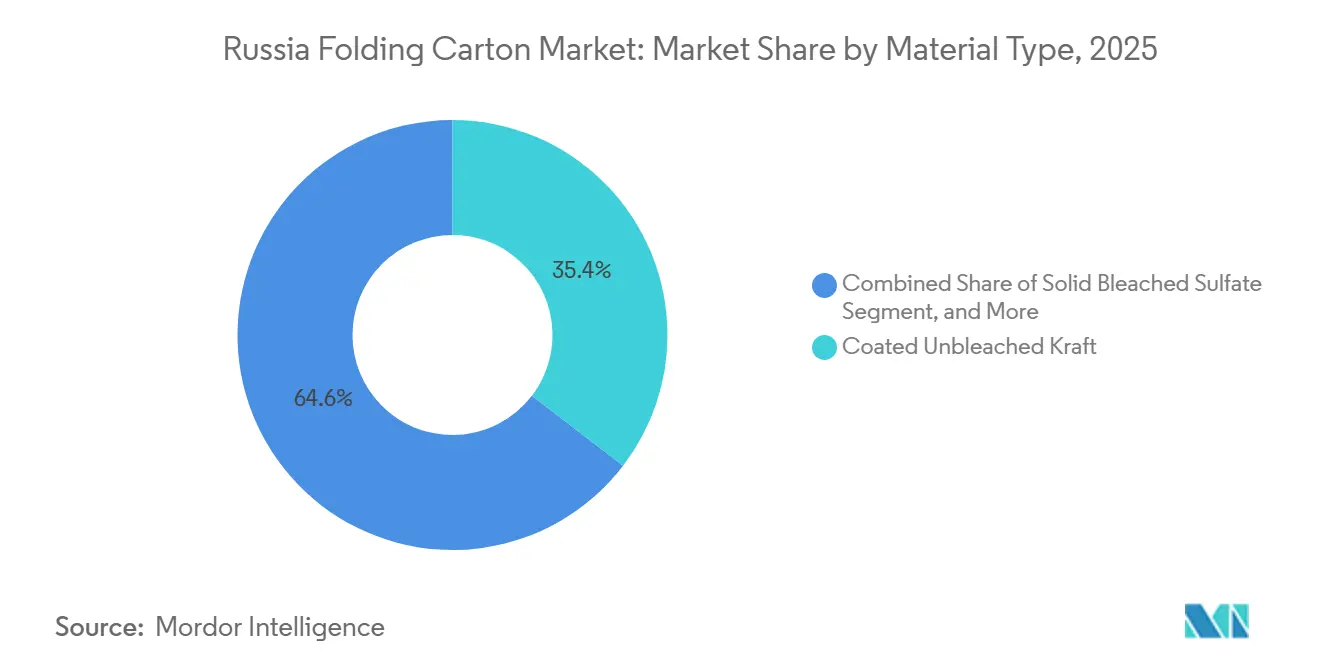

- By material type, coated unbleached kraft captured with 35.41% of the Russia folding carton market share in 2025.

- By printing technology, the Russia folding carton market size for digital platforms is projected to grow at a 4.73% CAGR to 2031.

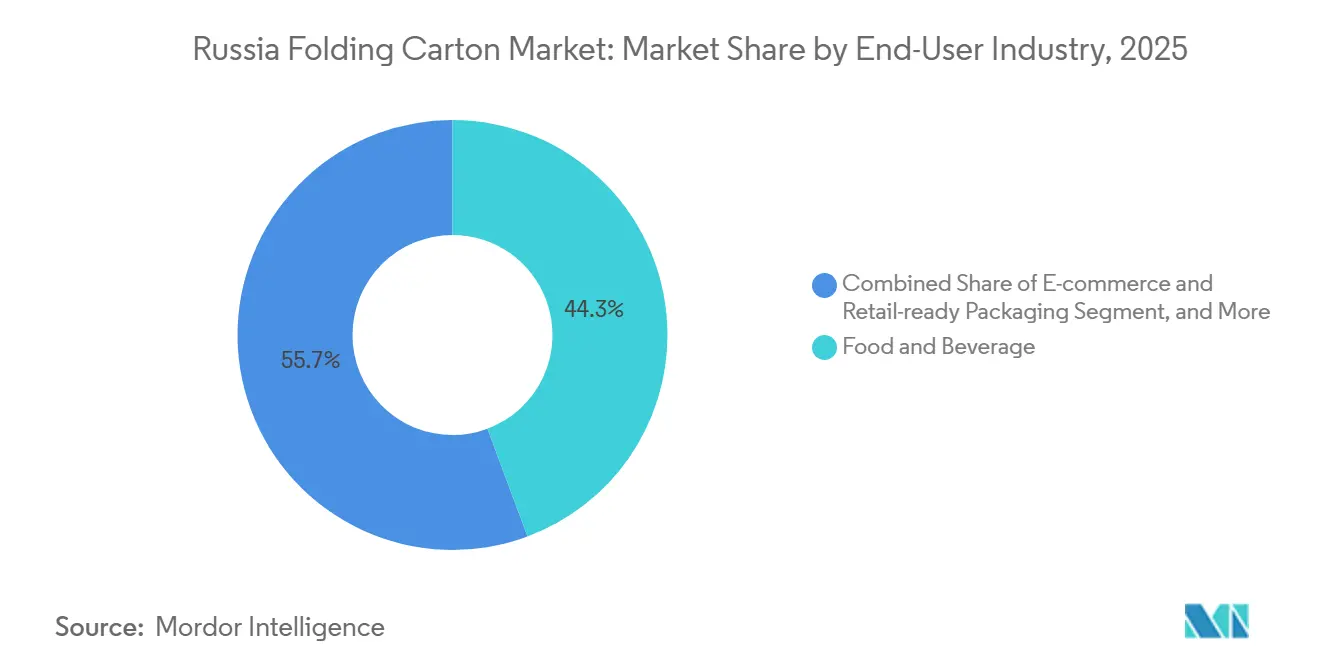

- By end-user industry, the food and beverage industry captured 44.32% of the Russia folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sustainable Packaging From Food and Beverage Brands | +0.9% | National, concentrated in Moscow, St. Petersburg and major food-processing hubs | Medium term (2-4 years) |

| Growth of Russia's E-commerce Sector Accelerating Carton Demand | +0.7% | National, highest intensity in Moscow, Leningrad, Novosibirsk, Yekaterinburg regions | Short term (≤ 2 years) |

| Expansion of Domestic Processed Food Manufacturing Capacity | +0.6% | National, emphasis on meat-processing clusters in Central, Southern and Volga Federal Districts | Medium term (2-4 years) |

| Stringent Government Regulations on Plastic Packaging | +0.5% | National, enforced by Rospotrebnadzor and Ministry of Natural Resources | Long term (≥ 4 years) |

| Surge in Localized Pharmaceutical Production Under Import Substitution Programs | +0.4% | National, early gains in Moscow, Leningrad, Kaluga, Yaroslavl pharmaceutical clusters | Medium term (2-4 years) |

| Investment in High-Color Digital Printing Lines Enabling Personalized Cartons | +0.3% | National, concentrated in Moscow, Leningrad, Perm, Rostov converter hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Packaging from Food and Beverage Brands

Brand owners are shifting procurement toward mono-substrate folding cartons that satisfy the 75% recycling mandate set for 2026 and the 100% threshold fixed for 2027. Government Order No. 2414, issued in December 2023, tightened recycling obligations and raised environmental fees by 15% in 2025, directly linking material choice to fiscal exposure. As meat-processing projects worth more than RUB 40 billion (USD 424.5 million) came online in 2025, premium product lines relying on moisture-resistant cartons rose to 23% of total output, forcing converters to balance barrier performance with recyclability. Marketplace giants Wildberries and Ozon revised supplier guidelines in February 2026, formally preferring stackable, recyclable cartons and displacing laminates in dry-grocery and confectionery categories. Converters able to document ISO 14001 and FSSC 22000 compliance are now de facto preferred partners for multinational FMCG tenders, cementing sustainability as both a regulatory and commercial imperative.

Growth of Russia's E-commerce Sector Accelerating Carton Demand

Wildberries and Ozon still accounted for 77% of online retail revenue in 2024 and, although their combined growth moderated to roughly 25-32% in 2025, the absolute uplift in shipped parcels remains material for carton converters. The platform shift toward small-batch, branded mailers inspired E-pak to secure concessional financing in March 2026 to modernize digital presses for short-run printing across the Urals. Packaging mandates issued in February 2026 require recyclable structures that fit automated fulfillment systems, giving folding cartons an edge over irregular flexible pouches. Kappa Rus’s 90,000-metric ton linerboard acquisition in Novgorod underlines the vertical-integration trend aimed at securing substrate supply for e-commerce formats. Consequently, the Russia folding carton market continues to expand on a value basis even as parcel-volume growth decelerates.

Expansion of Domestic Processed Food Manufacturing Capacity

More than 30 processed-food projects totaling RUB 40 billion (USD 424.5 million) were executed in 2025, pushing value-added meat products up by 4 percentage points year on year. The prevalence of Industrial Internet of Things systems in 60% of large plants increases real-time throughput, requiring carton suppliers to synchronize just-in-time deliveries, achieve higher color fidelity, and apply anti-moisture coatings. Molopak’s RUB 2.6 billion (USD 27.6 million) line extension, scheduled for 2026, targets aseptic beverage cartons modeled after Tetra Pak and SIG Combibloc, a shift that fortifies domestic control over liquid-food packaging. Decree No. 719, effective January 2026, incentivizes integrated primary and secondary packaging lines, anchoring folding-carton demand as processors seek local partners with food-contact certifications.

Stringent Government Regulations on Plastic Packaging

Recycling targets that climb to 100% in 2027 and a proposed ban on 28 single-use plastic formats by 2030 are redirecting capital toward cartonboard. Environmental fee hikes in 2025 and upgraded Rospotrebnadzor migration limits for recycled board intensify compliance costs for non-paper substrates. While technical complexity rises for small converters who must add barrier coatings and laboratory testing, the regulatory climate clearly elevates cartonboard as the preferred substitute in beverage, dairy, and frozen-food channels, encouraging investment in nano-cellulose and seaweed-based coatings that retain recyclability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Pulp Prices Pressuring Converter Margins | -0.6% | National, acute for non-integrated converters in Moscow, Leningrad, Perm regions | Short term (≤ 2 years) |

| Competition From Flexible Packaging Formats in Beverage and Snack Applications | -0.5% | National, concentrated in beverage and snack categories with high-speed filling lines | Medium term (2-4 years) |

| Supply-Chain Disruptions From Geopolitical Sanctions on Machinery Imports | -0.4% | National, affecting converters dependent on European or North American equipment | Long term (≥ 4 years) |

| Limited Availability of Domestic Food-Grade Barrier Coatings | -0.3% | National, bottlenecks in extrusion-coating and lamination capacity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility In Virgin Pulp Prices Pressuring Converter Margins

Virgin Kraftliner averaged RUB 56,122 per metric ton (USD 594.3 per metric ton) in March 2026, even as carton prices slipped early the same year, widening the squeeze on stand-alone converters. Ilim Group and Segezha Group each posted heavy losses in 2025, underscoring that even integrated producers struggle to absorb cost shocks when Central Bank rates are 16-21%. Paper-product deflation of 4-5% year on year during January-February 2026 underscores weak downstream pricing power. Without captive pulp or large recycled-fiber loops, smaller converters face immediate cash-flow stress, and high interest costs limit working-capital buffers.

Competition From Flexible Packaging Formats in Beverage and Snack Applications

Atlantis-Pak’s RUB 19 billion (USD 200 million) revenue in 2025, supported by SIBUR’s metallocene investments targeting high-barrier films, confirms ongoing innovation in lightweight flexible substrates.[1]Atlantis-Pak, “Annual Revenue Statement,” atlantis-pak.ru Flexible pouches retain speed and unit-cost advantages on vertical form-fill-seal lines, especially in dairy, snacks, and beverage concentrates, where folding cartons need costly aseptic fillers to compete. The proposed plastic restrictions may redirect some volume, but hybrid formats like bag-in-box still leverage lighter weight and superior barrier performance against moisture ingress, sustaining a competitive headwind for carton converters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Shift Toward Recycled Grades Under EPR Mandates

White Line Chipboard is forecast to account for a rising share of the Russia folding carton market, growing at a 4.21% CAGR through 2031, reflecting converters' substitution of virgin fiber with post-consumer content to meet rising recycling thresholds. Coated Unbleached Kraft retained 35.41% of Russia folding carton market share in 2025, benefiting from printability and moisture resistance that food brands still demand.

Solid Bleached Sulfate continues to serve premium pharmaceutical and cosmetics applications despite exposure to pulp price shocks, whereas Folding Boxboard holds middle-tier food segments but faces discount pressure from procurement teams. L-Pak’s decision to source 80% recycled feedstock illustrates the competitive premium now attached to auditable sustainability claims, while Arkhangelsk PPM’s 700,000-metric ton expansion slated for 2027 shows integrated players hedging input-cost risk with scale and captive fiber.[2]Moscow Region Government, “L-Pak Kashira SEZ Project Details,” mosreg.ru

By Printing Technology: Digital Lines Unlock Personalized Runs

Lithographic presses held 43.76% of the Russia folding carton market share in 2025, yet Digital printing is on track for a 4.73% CAGR between 2026 and 2031 as converters deploy high-resolution inkjet systems that satisfy market demand for quick artwork changes. The increasing preference for shorter production runs and customization is further fueling the adoption of digital printing technologies. The shift towards digital printing is also enabling faster turnaround times, meeting the evolving needs of end-users.

Kappa Rus’s 2,400 dpi installation and Printomir’s cold-foil capabilities illustrate how converters monetize shorter cycles and premium finishes, while flexography maintains cost efficiency on long corrugated runs. Gravure and screen processes are drifting toward niche security and ultra-long commodity campaigns, reinforcing a bifurcated equipment landscape in the Russian folding carton market. The diversification of printing technologies reflects the market's adaptation to varied production demands and customer preferences.

By End-User Industry: Omnichannel Retail Reshapes Demand Mix

Food and Beverage accounted for 44.32% of the Russia folding carton market in 2025, underpinned by value-added processed foods that require barrier coatings and high-color graphics. However, e-commerce and retail-ready formats are projected to rise at a 4.43% CAGR, becoming the fastest-moving adopter class through 2031. The growing focus on sustainable packaging solutions is also expected to significantly influence market dynamics.

Wildberries and Ozon’s specification updates impose recyclability and cube-optimization constraints that cartons meet more readily than flexible packs, while Decree No. 719 drives pharmaceutical producers to install integrated carton lines. Personal-care brands accelerate premiumization through cold foil and tactile coatings, underscoring the role of high-spec converters in capturing margin in the Russian folding carton market.

Geography Analysis

The Moscow region commands the largest concentration of capacity inside the Russia folding carton market, anchored by integrated mills, port access, and the headquarters of leading FMCG customers. L-Pak’s Kashira complex, Printomir’s Noginsk plant, and Harmens Molokovo’s press upgrades collectively underscore how special economic-zone tax abatements tilt new investment toward the capital’s periphery. Leningrad follows closely, with Svetogorsk PPM’s duplex board line and Kappa Rus’s 156 million square-meter upgrade cementing the Northwest as an export-ready hub.

Perm and the Urals form a secondary cluster, where Perm Paper Company’s new Chinese corrugator and E-pak’s digital upgrade satisfy regional e-commerce growth. Southern regions focus on flexible substrates, but SFT Group’s Maykop facility and Atlantis-Pak’s Rostov base illustrate material overlap that creates cross-category competition.[3]SFT Group, “Robotization and Regional Footprint,” sftgroup.ru Farther north, Arkhangelsk PPM’s USD 1.4 billion containerboard expansion positions the forest-rich region as a strategic fiber supplier, while Bryansky Karton’s 30% output jump reflects provincial governments' co-financing capacity to lift local employment.

Regional disparities are widening because Central Bank rates still sit well above pre-crisis norms, limiting provincial access to affordable credit. Special economic zones that cut profit tax to 2% offer a safeguard, explaining why Kashira and Voronezh attract both board and aluminum can capacity. Enforcement of Rosstandart food-contact rules varies by oblast, so multinational auditors increasingly channel high-spec jobs to certified converters in Moscow and Leningrad, leaving smaller provincial firms to serve lower-risk domestic SKUs.

Competitive Landscape

Russia's folding carton market remains moderately fragmented. Ilim Group, despite holding roughly one-quarter of domestic cardboard output, recorded a RUB 16.5 billion (USD 174.3 million) loss in 2025 as elevated interest rates undercut modernization outlays. Segezha Group’s RUB 88 billion (USD 1.1 billion) shortfall the same year reflects currency strength and soft export lumber demand, proving size alone does not insulate earnings. Taiga Group’s acquisition of Karelia Pulp and Arkhangelsk PPM’s greenfield project highlights vertical-integration plays aimed at stabilizing fiber cost.

Mid-tier challengers deploy automation to outflank legacy inefficiencies. SFT Group operates 24 robot-aided sites across seven regions, while L-Pak’s fully automated tray line and robotic palletizers illustrate how labor-saving technology boosts yield per employee. Digital and embellishment investments exemplified by Kappa Rus’s high-res line and Printomir’s cold-foil press differentiate converters in premium, short-run niches valued by cosmetics and marketplace sellers.

Machinery embargoes push 71% of equipment imports toward Chinese vendors, yet domestic packaging-machinery output fell 12.5% in the first nine months of 2025, prolonging reliance on overseas CNC systems and sensors.[4]Ministry of Industry and Trade, “Packaging Machinery Import Statistics,” minpromtorg.gov.ru Consequently, uptime and precision remain pain points, propelling larger converters to dual-source critical spares. Certifications such as FSSC 22000 and ISO 9001 have become thresholds for multinational tenders, entrenching a compliance moat that advantages scale players over unaccredited regional shops.

Russia Folding Carton Industry Leaders

Ilim Group JSC

Harmens Group

Arkhangelsk PPM JSC

Segezha Group PJSC

Svetogorsk PJSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Segezha Group and Ilim Group, both integrated producers, had recalibrated their mill logistics and internal pricing models. This adjustment was a strategic move to better absorb the severe margin shocks caused by tight domestic central bank interest rates, which ranged from 16% to 21%.

- April 2026: Molopak had pushed forward with the RUB 2.6 billion (USD 27.6 million) expansion of its manufacturing line. This infrastructure program was tailored for the high-volume production of domestic aseptic folding liquid-board cartons, ensuring stability in food-contact distribution pipelines.

- March 2026: E-pak had secured long-term concessional financing, aiming to modernize its digital inkjet press infrastructure. This capital deployment was focused on enhancing high-resolution short-run printing capabilities throughout its distribution network in the Urals.

- February 2026: Brand owners had pivoted their local procurement strategies, favoring mono-substrate folding cartons. This shift aligned with the Russian Federation's state-enforced 75% recycling mandate, set to take effect soon. Notably, this regulatory threshold was on track to escalate to 100% by 2027.

Russia Folding Carton Market Report Scope

The Russia folding carton market comprises the manufacturing, printing, and conversion of cartonboard into folding containers that are subsequently erected, filled, and sealed. The study examines market dynamics, including growth drivers, challenges, and trends, while providing insights into the competitive landscape, supply chain, and forecasted growth during the study period.

The Russia Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

How large will the Russia folding carton market be by 2031?

The Russia folding carton market size is forecast to reach USD 1.36 billion by 2031, advancing at a 3.23% CAGR from 2026.

Which material type leads current demand?

Coated Unbleached Kraft held the largest share at 35.41% in 2025, driven by its cost advantage and food-contact printability.

What is the fastest growing end-user segment?

E-commerce and retail-ready packaging is projected to expand at a 4.43% CAGR through 2031 as marketplace platforms tighten recyclability rules.

How are regulations influencing packaging choices?

Rising extended producer responsibility fees and pending bans on 28 plastic formats are pushing brand owners toward recyclable folding cartons and away from laminates.

Which printing technology is gaining the most traction?

Digital printing is expected to post a 4.73% CAGR through 2031, as its short-run economics and variable-data capabilities align with personalized e-commerce orders.

What is the main threat to folding cartons in beverages and snacks?

High-barrier flexible pouches, supported by SIBUR’s metallocene polyethylene investments, continue to outpace cartons on filling-line speed and unit cost.

Page last updated on: