Poland Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

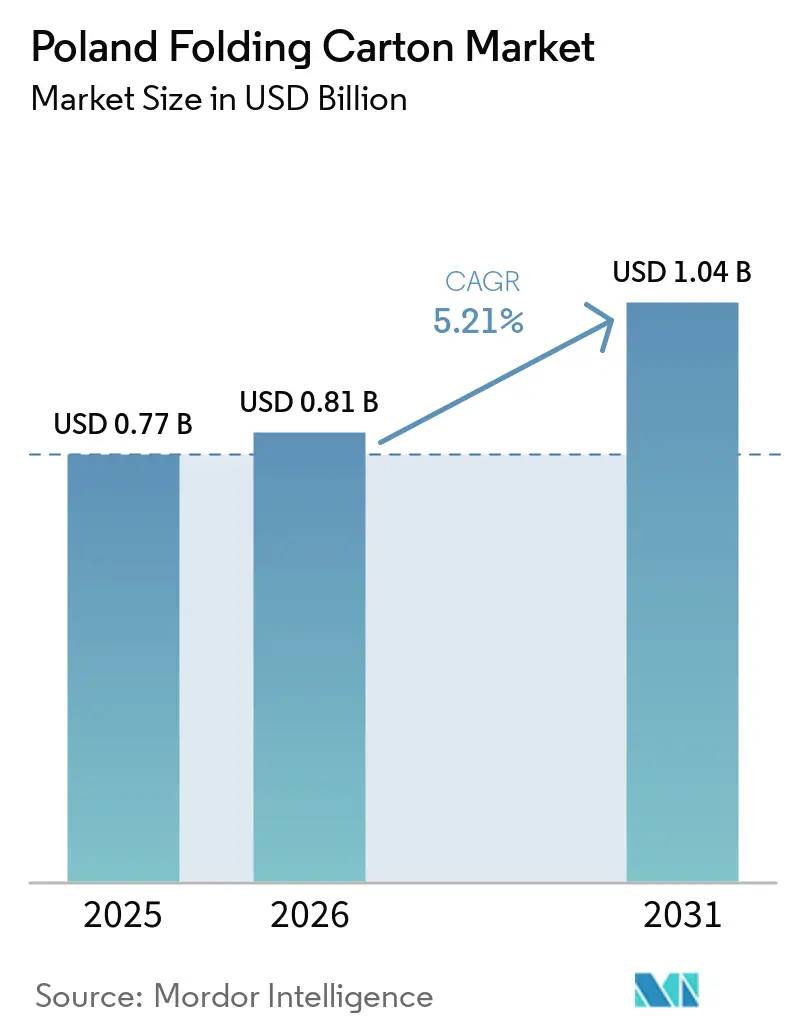

| Base Year Market Size (2025) | USD 0.77 Billion |

| Market Size (2026) | USD 0.81 Billion |

| Market Size (2031) | USD 1.04 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Folding Carton Market Analysis by Mordor Intelligence

The Poland Folding Carton Market size is projected to expand from USD 0.77 billion in 2025 and USD 0.81 billion in 2026 to USD 1.04 billion by 2031, registering a CAGR of 5.21% between 2026 and 2031. Poland's folding carton market growth pivots on the country’s role as the European Union’s second-largest packaging exporter, its rail-linked proximity to German, Dutch, and French demand centers, and the rapid scale-up of e-commerce fulfillment capacity. Brand owners are migrating toward recyclable paper-based formats to meet consumer sustainability preferences, while pharmaceutical investments in Gdańsk and Poznań are driving demand for compliance-driven cartons with security features. Technology upgrades, especially digital short-run presses, help small and medium-sized enterprises (SMEs) personalize packaging without the cost drag of plate changes, although converters continue to battle pulp price volatility and margin compression. Competition intensity is moderate, but multinational mills are using vertical integration and continuous-digester projects to raise quality benchmarks and shield substrate supply.

Key Report Takeaways

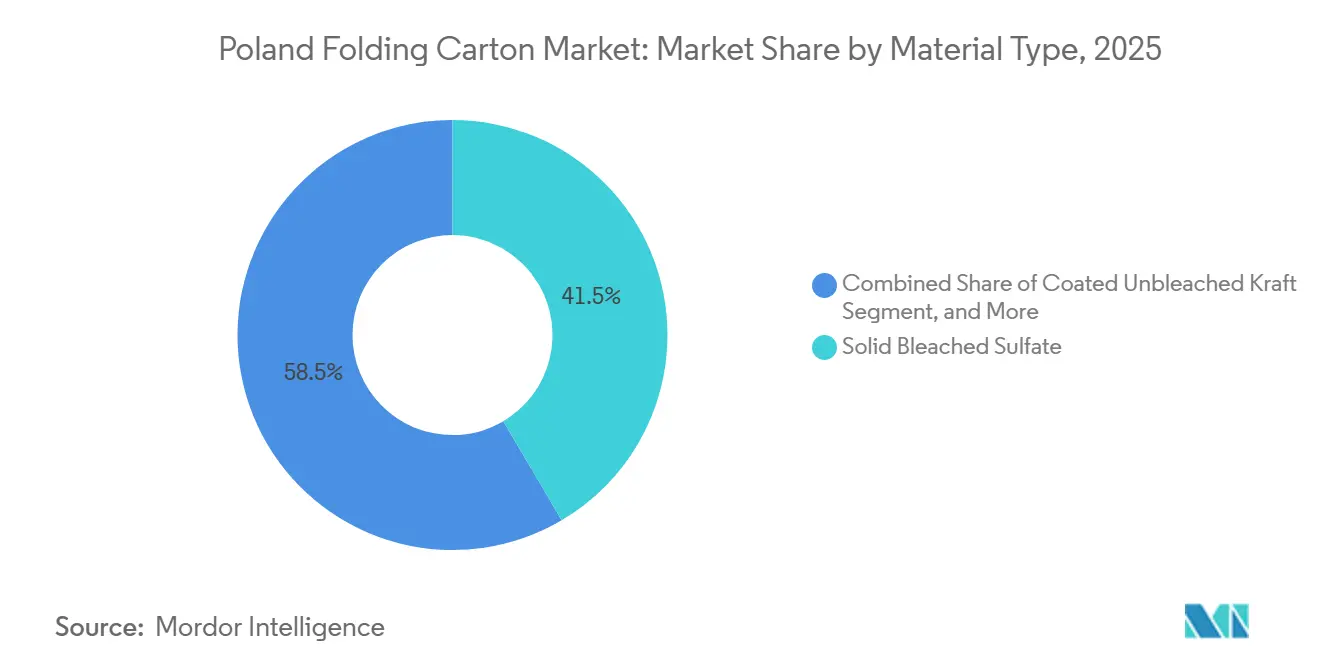

- By material type, solid bleached sulfate captured with 41.52% of the Poland folding carton market share in 2025.

- By printing technology, the Poland folding carton market size for digital platforms is projected to grow at a 6.38% CAGR to 2031.

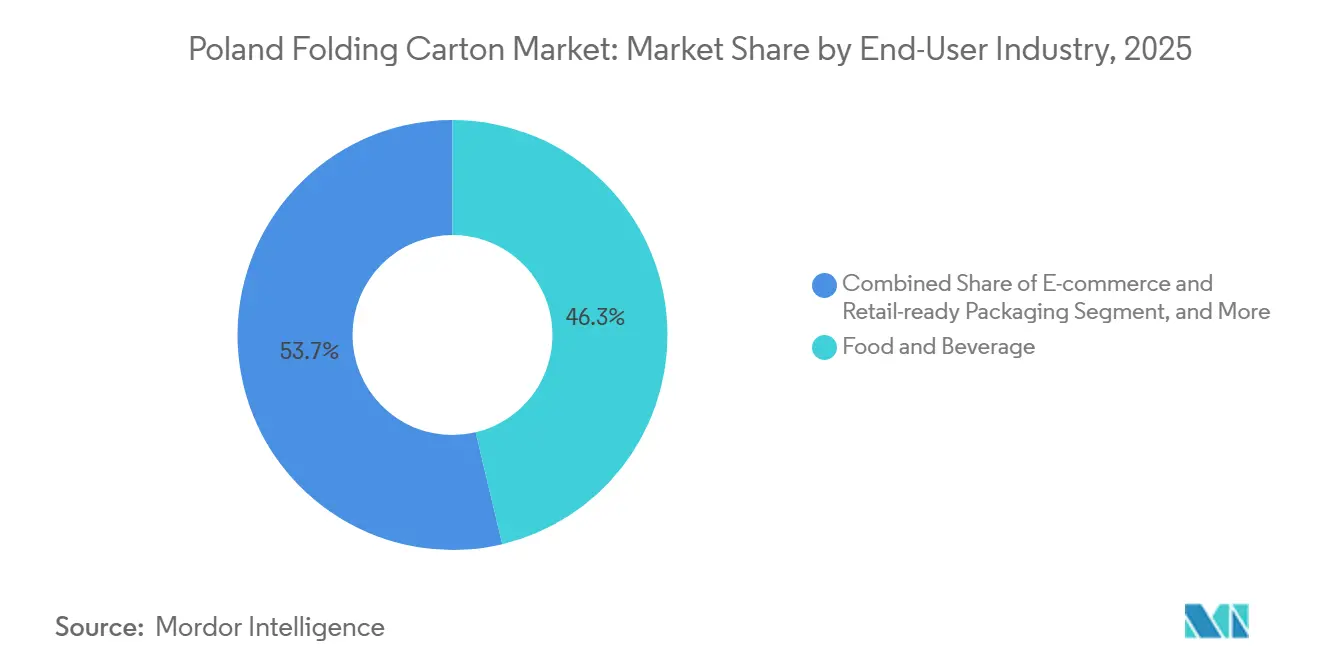

- By end-user industry, the food and beverage industry captured 46.28% of the Poland folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Preference for Recyclable Paper-Based Packaging Among Polish Consumers | +0.9% | Poland and Central Europe | Medium term (2-4 years) |

| EU Regulations Accelerating Plastic-to-Paper Substitution in Poland | +1.2% | Poland, aligned with EU-27 directives | Long term (≥ 4 years) |

| E-commerce Fulfillment Growth Demanding Durable Lightweight Cartons | +1.1% | Warsaw, Kraków, Gdańsk urban centers | Short term (≤ 2 years) |

| Surge in Pharmaceutical Manufacturing Investments in Poland Boosting Folding Carton Demand | +0.7% | Gdańsk and Poznań regions | Medium term (2-4 years) |

| Rising Adoption of Digital Short-Run Printing by Local SMEs for Personalized Cartons | +0.5% | Wielkopolska and Mazovia SME clusters | Medium term (2-4 years) |

| Export-Oriented Carton Production Leveraging Poland’s Proximity to Western Europe | +0.8% | Cross-border flows to Germany, Netherlands, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Preference for Recyclable Paper-Based Packaging Among Polish Consumers

Cardboard’s 95% recycling rate across Europe confirms its circular credentials, yet Poland’s overall packaging recycling rate reached only 51% in 2022, signaling collection-system constraints that hamper full material capture. Consumer surveys showed that 74% of Polish shoppers favored eco-friendly packaging by late 2024, but only one-third consistently chose reusable or refillable options, indicating that convenience and price still steer final purchases. Converters able to verify chain-of-custody sourcing through Forest Stewardship Council (FSC) certification, such as Akomex, capture loyalty from the 34% of buyers willing to pay a modest eco-premium. Retailers’ reluctance to absorb certification costs, however, pressures converters to balance environmental positioning with shelf-price competitiveness. Collaborative take-back schemes with municipalities offer an avenue to improve post-consumer collection and reinforce brand commitments to closed-loop goals.

EU Regulations Accelerating Plastic-to-Paper Substitution in Poland

The European Union’s Packaging and Packaging Waste Regulation, in force since 2024, establishes harmonized recyclability labels and mandates recycled-content thresholds that increase through 2030. Poland’s October 2025 deposit-return system covers beverage containers first but signals broader extended producer responsibility schemes that will soon touch folding cartons. Designs scoring highly under the 4evergreen alliance’s recyclability guidelines will enjoy lower eco-fees, tilting procurement toward coated-kraft and recycled-content grades that meet upcoming performance tests. Mayr-Melnhof’s EUR 660 million (USD 746 million) upgrade at Kwidzyn adds high-purity pulping capability to supply compliant substrates ahead of 2027 label mandates. Regulatory exemptions for virgin fiber in direct food-contact pharmaceuticals create a two-tier market, pushing converters to manage parallel substrate portfolios to protect margin in segments where recycled content remains restricted.

E-Commerce Fulfillment Growth Demanding Durable Lightweight Cartons

Parcel volumes expanded 52% in 2024 as InPost’s locker network surpassed 20,000 units nationwide, redefining structural performance benchmarks for secondary packaging. Smurfit WestRock’s Pruszków site introduced lightweight carton formats capable of meeting a 1.2-meter drop standard without corrugated liners, reducing transport cost while safeguarding automated sortation integrity. Graphic Packaging added display-ready features at its Poznań plant in November 2025, enabling direct-to-consumer brands to ship, shelf, and merchandise in one structure. However, Bank Pekao identified that converters’ limited pricing power during 2024-2025 compressed net profitability to 4.9% despite surging volumes, underscoring the need for lean production models. The agility to customize dielines to meet parcel-locker constraints without inflating costs now differentiates winning suppliers.

Surge in Pharmaceutical Manufacturing Investments in Poland Boosting Folding Carton Demand

More than EUR 1 billion (USD 1.13 billion) in pharmaceutical capital inflows between 2024 and early 2026 spurred secondary packaging demand that values tamper-evidence, Braille, and holographic security. Sharp Services’ sterile injectables expansion in Gdańsk and Preston Packaging’s clinical-trial material line-upgrades require serialized cartons compliant with the EU Falsified Medicines Directive. Akomex leverages 50 years of pharmaceutical expertise and FSC-certified workflows, positioning itself as a preferred partner for high-complexity runs. CeTeAPI’s new active pharmaceutical ingredient hub will strengthen regional supply chains, encouraging on-site fill-finish and in-country packaging to shorten lead times and increase demand elasticity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Virgin Pulp Prices Compressing Converter Margins | -0.8% | Poland with global market linkages | Short term (≤ 2 years) |

| Competition From Flexible Pouches in the Snack and Pet Food Segments | -0.6% | Urban retail channels in Poland | Medium term (2-4 years) |

| Limited Domestic Recycling Capacity for High-Quality White Fiber | -0.4% | Nationwide fiber supply chain | Long term (≥ 4 years) |

| Skilled Press-Operator Shortage Hindering Advanced Printing Adoption | -0.3% | Manufacturing clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Virgin Pulp Prices Compressing Converter Margins

Northern Bleached Softwood Kraft hit USD 1,600 per tonne in January 2026 following mill increases of USD 100 per tonne for kraftliner grades, while Bleached Eucalyptus Kraft moved to USD 1,240 per tonne, a 10% swing inside six weeks. Stora Enso rolled out a similar pulp-based price hike across its European board portfolio, citing energy and fiber inflation as the principal drivers. Huhtamaki’s 2024 annual report revealed that rising fiber and labor inputs cut regional margins despite EUR 122.6 million (USD 138.6 million) in Polish sales, a dynamic replicated among smaller Polish folding carton market independents that lack hedging instruments. The lack of wide hedging liquidity forces converters into spot negotiations, eroding the predictability of multi-year brand contracts. While some firms insert pulp-index pass-through clauses, most SMEs must shoulder fluctuations or risk volume loss, deepening cash-flow strain.

Competition From Flexible Pouches in Snack and Pet Food Segments

EPac’s Bydgoszcz plant expanded digital pouch output in 2025, offering high-barrier films that undercut folding cartons on gram-per-unit costs and freight weight.[1]ePac corporate newsroom, “ePac Poland expands digital printing capacity for pet food pouches,” Epacflexibles.com CWL Packaging’s showcase of recyclable and compostable pouches at Warsaw Pack 2026 signaled the flexible sector’s pivot from purely plastic credentials to hybrid paper-barrier structures marketed as paper feel. Mondi’s recyclable paper pouch with integrated barrier blurs format boundaries and could cannibalize its own carton volumes while protecting total portfolio share. Brand owners, especially in price-sensitive pet food, weigh the product-to-package ratio, tilting specifications toward stand-up pouches that maximize shelf density. Carton converters now test hybrid solutions that sleeve flexible inners, yet these assemblies add cost and assembly complexity, dampening widespread uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Grades Gain as Brands Seek Natural Aesthetics

The material-type hierarchy remained anchored by Solid Bleached Sulfate, which held 41.52% of Poland folding carton market share in 2025. Poland folding carton market size expansion through 2031, however, skews toward Coated Unbleached Kraft, whose forecast 6.65% CAGR exceeds the headline rate as premium food and cosmetics labels embrace natural brown surfaces for artisanal storytelling. Folding Boxboard occupies mid-tier positions, balancing stiffness and economics, while White Line Chipboard captures eco-driven buyers despite muted brightness. Mayr-Melnhof’s continuous-digester upgrade enables higher-consistency virgin kraft, improving surface uniformity and helping brand owners print muted palettes without sacrificing registry.

Unilever’s Kraft carton launch for its premium tea line demonstrated how substrate color can reposition a legacy product without altering formulation, allowing converters to up-sell by leveraging perceived authenticity. Stora Enso’s 20,000-tonne boost at Ostrołęka increases access to both bleached and unbleached grades, granting converters substrate agility.[2]Stora Enso investor relations, “Stora Enso increases Ostrołęka capacity by 20,000 tonnes,” Storaenso.com Yet Kraft’s lower brightness caps its viability for neon cosmetics or metallic pantones, keeping Solid Bleached Sulfate dominant in high-graphics pharmaceuticals. Mill diversification into specialty coatings and metallized layers offers niches, but volume resides in the kraft-versus-bleached trade-off that now shapes brand procurement roadmaps.

By Printing Technology: Digital Gains as SMEs Bypass Plate Economics

Flexographic Printing retained 36.18% share of Poland folding carton market in 2025, but Digital Printing’s 6.38% projected CAGR signals steady erosion of the plate-based cost advantage at sub-10,000 impression runs. Poland's folding carton market is growing, driven by regional breweries and confectioners leveraging variable-data graphics for seasonal campaigns. ePac’s ability to profitably print cartons in batches of 500 units, combined with CZK’s Scodix digital spot-UV enhancement for QR-code engagement, showcases the personal-branding premium that buyers now pay.

Offset lithography still dominates high-fidelity cosmetics and pharma, but servo-driven flexo presses such as Edale’s FL6p close the registration gap, letting converters keep per-unit costs low for runs above 50,000 while adding inline cold-foil. Gravure remains a niche for long-cycle tobacco cartons due to its cylinder amortization horizon. SMEs that blend a hybrid park flexo for base volumes, digital for variable overlays capture both categories, but operator cross-training costs and machine redundancy challenge working-capital budgets, especially during pulp-price shocks.

By End-User Industry: Pharma Outpaces Food as Compliance Drives Premiumization

Food and Beverage dominated 46.28% of Poland folding carton market size in 2025, yet Healthcare and Pharmaceuticals’ anticipated 6.82% CAGR through 2031 leads segment growth as Poland becomes a contract-manufacturing hub for Western clients. Serialization mandates, tamper-evidence, and Braille embossing lift average selling prices, cushioning converters from commodity exposure. CeTeAPI’s new API site cements upstream scale, encouraging fill-finish investments that drive localized carton demand.

Within Food and Beverage, dairy and baked goods thrive on Poland’s surplus milk solids and grains, exporting to Germany and the Netherlands, whereas frozen foods cede shelf real estate to flexible pouches that promise better freezer-burn defense. Personal Care and Cosmetics marry tactile varnishes and structural graphics for premium placement, a sweet spot for digital enhancement houses. Electrical and Electronics maintain steady panel and inserts orders, leveraging the rigidity advantage of folding cartons over flexibles for shock protection. E-commerce-ready packaging grows in lock-step with InPost’s locker ecosystem, though its share hides within branded food or beauty subcategories, further blurring channel versus industry segmentation.

Geography Analysis

Poland captured a 12.2% share of total EU packaging exports in 2025, outperforming a region-wide decline and reinforcing its status as the supply hub closest to Western demand. Smurfit WestRock’s 600-meter rail bridge between its Hoya mill in Germany and Polish converting nodes removes 1,400 truckloads per year, slashing freight emissions and cutting logistics spend by approximately 15%. Poland's folding carton market is directly benefiting from the expansion, as integrated rail lowers landed substrate costs, enabling competitive delivered pricing into Frankfurt and Amsterdam fulfillment centers.

The Gdańsk-Pomerania corridor hosts pharmaceutical and medical device packaging, anchored by Sharp Services and Akomex, and draws on Gdańsk’s port access for API imports. Wielkopolska, centered on Poznań, remains the food-carton workhorse, with Graphic Packaging’s display-ready upgrade bolstering premium snack and beauty output. Mazovia leans on Warsaw’s e-commerce ecosystem, feeding InPost’s last-mile network through quick-response carton lines. Border-adjacent Lower Silesia and Kuyavia-Pomerania absorb corrugated capacity expansions such as Aquila’s FOSBER line, leveraging highway proximity for just-in-time truck shipping into Saxony and Brandenburg.[3]VPK Group media, “Aquila installs FOSBER corrugator at Września February 2025,” Vpkgroup.com

Poland folding carton market share gains also reflect favorable labor arbitrage: national hourly wages averaged 35% below Germany’s in 2025, yet skills in press operation and structural design continue to tighten, risking wage-led margin squeezes. Recycling infrastructure lags, with 300 professional facilities serving 38 million residents, forcing exports of recovered white fiber to German mills for high-purity reprocessing. Meeting EU 65% recycling targets by 2025 will require capital deployment into optical sorting and de-inking, a prerequisite for Poland to sustain its value proposition as a low-cost, low-carbon supplier to Western Europe.

Competitive Landscape

Multinationals dominate volume yet face nimble domestic challengers. Mondi’s plan to build Europe’s largest corrugated factory in Poland signals an aggressive vertical-integration play that secures containerboard supply while synergistically feeding its folding carton demand.[4]Mondi newsroom, “Mondi to build Europe’s largest corrugated factory in Poland,” Mondigroup.com Mayr-Melnhof’s USD 746 million continuous-digester project at Kwidzyn underscores its commitment to brightness and strength differentiation, which small converters cannot easily replicate. Smurfit WestRock’s Pruszków expansion to 500 million boxes demonstrates scale economies in e-commerce cartons.

Domestic firms exploit white-space niches. Akomex leverages FSC certification, hologram application, and Braille embossing to secure premium pharmaceutical contracts often overlooked by volume-driven globals. Werner Kenkel’s EcoVadis Silver award signals environmental alignment, securing standing on procurement lists of multinationals that deploy ESG scorecards. ePac’s Bydgoszcz digital hub and CZK’s Scodix enhancements let them serve regional craft brands with sub-1,000 unit runs, a demand pocket that sprawling mills struggle to price competitively.

Technology adoption frames the competitive chessboard. Edale servo-flexo installations elevate registration precision, eroding offset litho’s historical graphics moat, while hybrid digital-flexo lines broaden service portfolios without duplicative overhead. Sustainability metrics increasingly decide tender awards; converters without traceable fiber sourcing or recycling pathways risk exclusion from EU-funded projects. Still, margins remain thin: Bank Pekao pegged industry net profitability at 4.9% in 2025, challenging reinvestment even as demand rises.

Poland Folding Carton Industry Leaders

Mayr-Melnhof Karton AG

Stora Enso Oyj

Graphic Packaging Holding Company

Smurfit WestRock plc

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Smurfit WestRock began moving paper on 600-meter trains from Germany to Poland, eliminating 1,400 annual truck journeys and securing feedstock for the enlarged Pruszków plant.

- April 2026: Werner Kenkel received an EcoVadis Silver Medal for sustainability performance, enhancing its ESG credentials with multinational brand owners.

- February 2026: Mondi unveiled plans for Europe’s largest corrugated factory in Poland to reinforce vertical integration.

- November 2025: Graphic Packaging finished a premium beauty and food carton upgrade at its Poznań site.

Poland Folding Carton Market Report Scope

This study provides a comprehensive analysis of the Poland folding carton market, focusing on market trends, growth factors, challenges, and emerging opportunities. Folding cartons, paper-based packaging solutions widely used across industries such as food and beverage, personal care, and pharmaceuticals, are lightweight, customizable, and recyclable, making them a popular choice for sustainable packaging applications. The study includes an in-depth examination of market dynamics, including supply chain analysis, the competitive landscape, and the regulatory framework.

The Poland Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Poland folding carton market size in 2026 and its expected value by 2031?

The Poland folding carton market size is USD 0.81 billion in 2026 and is projected to reach USD 1.04 billion by 2031.

Which material type is growing fastest within Polish folding cartons?

Coated Unbleached Kraft is forecast to grow at a 6.65% CAGR through 2031 as brands favor its natural brown aesthetics.

How are EU regulations influencing substrate choices in Poland?

Harmonized recyclability labels and rising recycled-content thresholds are accelerating a plastic-to-paper switch, especially for non-food applications.

Why is digital printing gaining share in Polish folding cartons?

SMEs use short-run digital presses to personalize packaging without plate costs, making runs under 10,000 units economical and fast.

Which end-user segment offers the highest margin potential?

Healthcare and Pharmaceuticals, driven by serialization and tamper evidence requirements, commands premium pricing and the fastest segment CAGR.

What is Poland’s main competitive advantage as an exporter of folding cartons?

Rail-linked proximity to Western Europe lowers freight costs and emissions, enabling just-in-time delivery to German, Dutch, and French customers.

Page last updated on: