North America Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

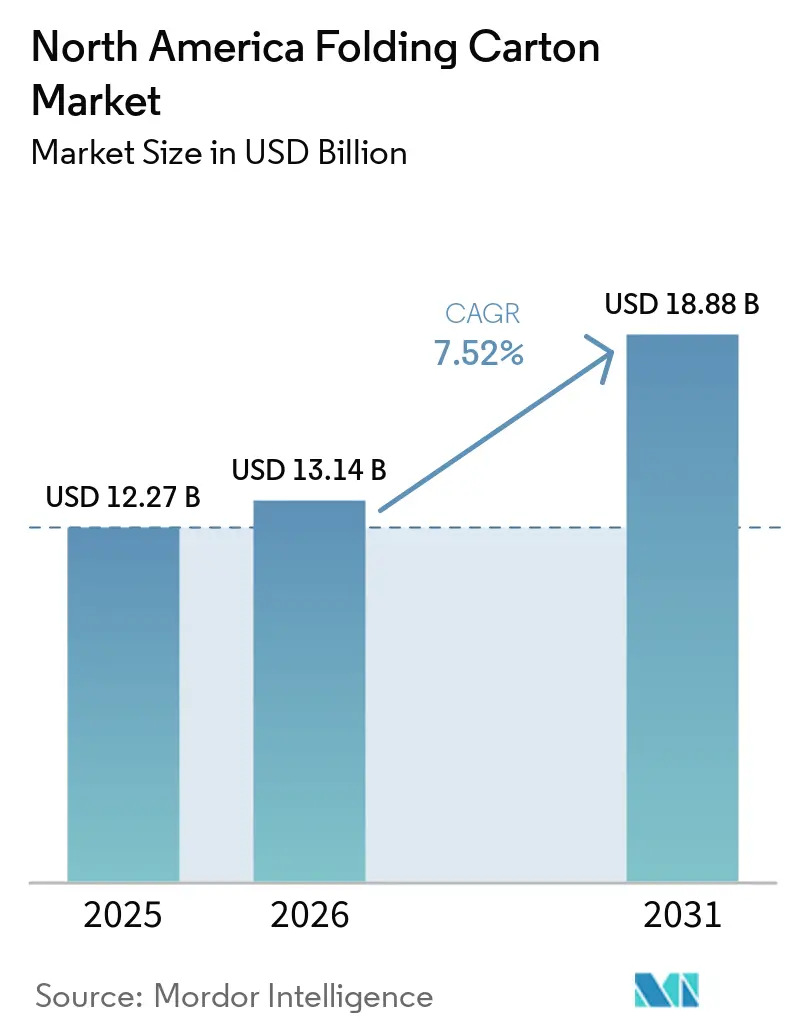

| Base Year Market Size (2025) | USD 12.27 Billion |

| Market Size (2026) | USD 13.14 Billion |

| Market Size (2031) | USD 18.88 Billion |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

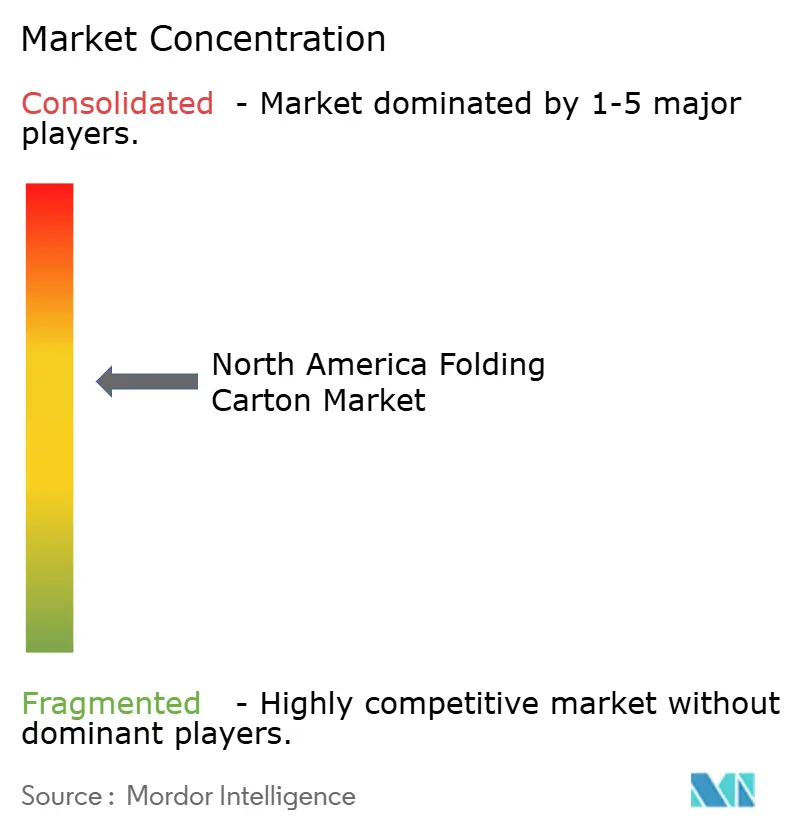

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Folding Carton Market Analysis by Mordor Intelligence

The North America folding cartons market size is projected to expand from USD 12.27 billion in 2025 and USD 13.14 billion in 2026 to USD 18.88 billion by 2031, registering a CAGR of 7.52% between 2026 to 2031. E-commerce fulfillment centers, state-level sustainability mandates, and nearshoring of consumer-goods manufacturing are collectively accelerating carton demand. Integrated producers are pruning low-margin tonnage and redirecting capital toward high-graphic, design-led solutions that carry stronger pricing power. Material choice is shifting as brand owners balance visual appeal, barrier performance, and recyclability, while converters race to automate die-cutting and gluing in order to shorten lead times. Fiber-price volatility and PFAS compliance remain the chief headwinds, but vertical integration and long-term fiber contracts are insulating the largest suppliers.

Key Report Takeaways

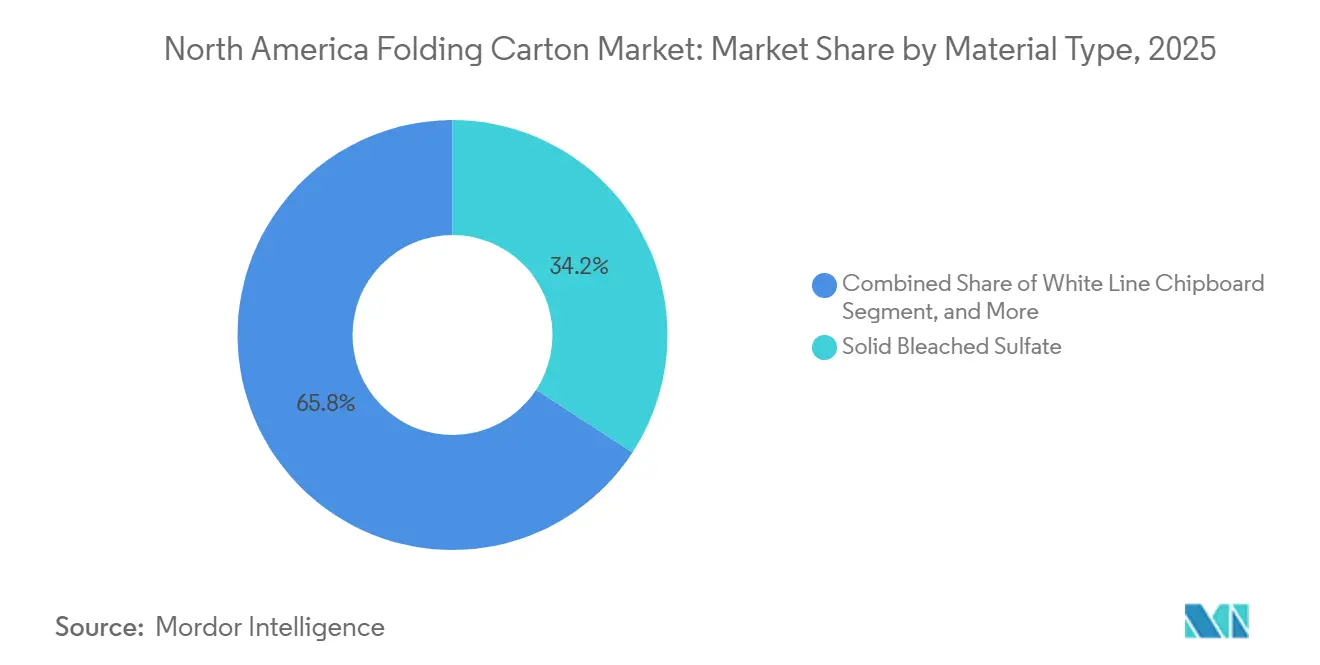

- By material type, solid bleached sulfate captured 34.21% of the North America folding cartons market share in 2025.

- By printing technology, the North America folding cartons market size for the digital printing segment is forecast to advance at a 9.85% CAGR through 2031.

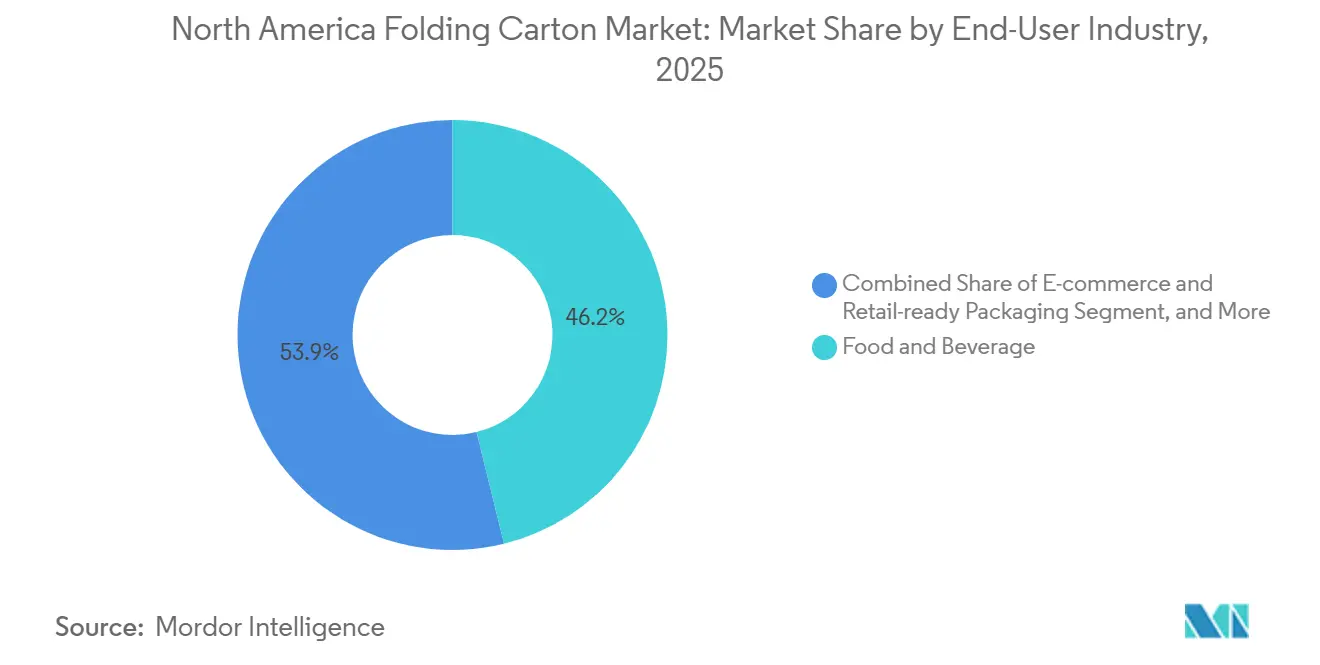

- By end-user industry, food and beverage captured 46.15% of the North America folding cartons market share in 2025.

- By country, the North America folding cartons market size for Mexico is forecast to advance at an 8.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In E-Commerce Shipments Requiring Shelf-Ready Packaging | +2.1% | United States and Canada, accelerating in Mexico | Short term (≤ 2 years) |

| Growing Preference For Sustainable Fiber-Based Substitutes To Plastics | +1.8% | North America-wide, strongest in California, Washington, and Canadian provinces | Medium term (2-4 years) |

| Advances In Water-Based Barrier Coatings Enabling Frozen Food Cartons | +1.2% | United States and Canada; limited Mexico penetration | Medium term (2-4 years) |

| Automation Of High-Speed Die-Cutting And Gluing Lines | +0.9% | United States and Mexico manufacturing hubs | Medium term (2-4 years) |

| Lightweighting Of Paperboard To Cut Logistics Costs | +0.7% | Cross-border USMCA shipments | Long term (≥ 4 years) |

| Retailer Mandates For Scannable, High-Graphic Packaging | +0.6% | United States retail chains; emerging in Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce Shipments Requiring Shelf-Ready Packaging

E-commerce retailers now ask suppliers to deliver folding cartons that move straight from inbound docks to store shelves, eliminating secondary handling. Amazon, Walmart, and Target introduced mandatory scannable, pre-printed carton specifications in 2025, prompting converters to invest in high-graphic digital and litho printing that supports RFID tagging.[1]Walmart Corporate, “Packaging Standards,” walmart.com Same-day turnaround has become a decisive differentiator, and converters with automated die-cutters near fulfillment hubs are gaining a growing share of the North America folding cartons market. Mexico is feeling the pull as new manufacturing clusters in Monterrey and Guadalajara demand localized, shelf-ready packaging.

Growing Preference for Sustainable Fiber-Based Substitutes to Plastics

Extended producer responsibility laws in California and Canada compel brands to switch from plastic to recyclable paperboard, lifting demand for premium fiber grades certified by the Forest Stewardship Council and the Sustainable Forestry Initiative.[2]Sustainable Packaging Coalition, “Extended Producer Responsibility Framework 2024-2025,” sustainablepackaging.org Stora Enso’s Performa Lumi paperboard achieved broad adoption in cosmetics by 2025 because it pairs high graphic fidelity with high recycled content. Integrated producers have responded with portfolio-wide “plastic-to-paper” programs, further enlarging the North America folding cartons market footprint.

Advances in Water-Based Barrier Coatings Enabling Frozen Food Cartons

Water-based coatings that match the grease- and moisture-resistance of fluorochemicals now satisfy the frozen-food supply chain while remaining curbside recyclable. H.B. Fuller’s AquaSeal platform and cellulose-nanofiber coatings demonstrated oxygen transmission rates low enough for frozen pizza cartons and paved the way for PFAS-free compliance.[3]H.B. Fuller, “AquaSeal Water-Based Barrier Coatings,” hbfuller.com With multiple U.S. states banning intentional PFAS use in food packaging, converters are rushing to retrofit coating lines, reinforcing high-margin demand across the North America folding cartons market.[4]Washington State Department of Ecology, “PFAS in Food Packaging Ban,” ecology.wa.gov

Automation of High-Speed Die-Cutting and Gluing Lines

Automated systems such as Bobst’s Mastercut 106 PER shrink makeready times to under 15 minutes, lift throughput to 10,000 sheets per hour, and trim setup waste by roughly one-third. Mid-sized converters that added robotics reported capacity jumps of 20–25%, enabling same-day fulfillment for regional e-commerce accounts. Capital spending is heaviest in the United States and Mexico, where labor shortages and wage inflation justify rapid payback periods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Recycled Fiber Supply Prices | -1.3% | North America-wide, amplified in export-dependent regions | Short term (≤ 2 years) |

| Capital-Intensive Compliance With PFAS Regulations | -0.8% | United States and Canada; Mexico exempt for now | Medium term (2-4 years) |

| Competition From Flexible Pouch Formats In Snacks | -0.5% | United States and Canada snack aisles | Medium term (2-4 years) |

| Limited Commercial Scaling Of Digital Print For Long Runs | -0.3% | Region-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recycled Fiber Supply Prices

Mill closures in China and new Asian export restrictions cut recovered-paper availability, pushing North American recycled-paperboard prices up or down by double digits in back-to-back quarters. Integrated producers that control curbside collection and possess pulp mills lock in long-term fiber contracts, shielding margins and concentrating North America's folding cartons market share among the top tier. This volatility is also prompting brand owners to diversify sourcing strategies and prioritize suppliers with stable fiber access and pricing visibility.

Capital-Intensive Compliance With PFAS Regulations

Washington, California, Maine, and Minnesota now outlaw intentional PFAS use in food packaging, forcing mills to spend USD 50-100 million apiece on new barrier-coating assets and validation testing. Smaller converters turn to toll-coated board from the integrated majors, losing differentiation and channel leverage. Although Mexico currently avoids these rules, multinational brand specifications mean the cost advantage is temporary.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Cost-Efficent Chipboard Gains Momentum

White Line Chipboard is projected to grow at a 7.94% CAGR, outpacing the overall 7.52% expansion, as e-commerce retailers accept its lower brightness for secondary and shelf-ready applications. Solid Bleached Sulfate retained the largest 34.21% share of the North America folding cartons market in 2025, a position secured by pharmaceutical and cosmetic serialization demands. Supply tightened when Smurfit WestRock shuttered its Quebec SBS machine, lifting price discipline and nudging converters toward chipboard when print fidelity is less critical. Folding Boxboard maintains steady food and beverage orders, yet snack brands continue to migrate to lightweight pouches for on-the-go convenience. Coated Unbleached Kraft serves niche organic food labels that value the natural brown appearance. Overall, material decisions now pivot more on total delivered cost and recyclability certification than on historical substrate loyalties. Converters that can switch grades quickly capture incremental opportunities in the North America folding carton market as brand-owner priorities evolve.

Demand for White Line Chipboard is most visible in the United States, where e-commerce penetration breached 15% of retail sales in 2025. Retailers’ focus on cost control encourages brand owners to trade down to a lower-cost substrate without sacrificing shelf impact. In Mexico, nearshoring has sparked interest in chipboard for consumer electronics cartons, as a low-cost substrate offsets higher logistics overhead. Canada continues to support premium SBS for regulated pharmaceuticals, but rising freight costs and a strong U.S. dollar are opening conversations about chipboard substitution. As supply chains regionalize, mills able to furnish multiple grades from a single complex can rebalance output faster, protecting margins and deepening engagement across the North America folding cartons market.

By Printing Technology: Digital Moves From Pilot to Production

Flexographic equipment maintained a dominant 51.91% share in 2025, thanks to unrivaled cost efficiency on runs of 10,000 or more impressions, a norm for mainstream food and beverage brands. Yet digital output is accelerating at a 9.85% CAGR, the quickest among all formats, as direct-to-consumer labels demand short runs, variable data, and personalized designs. Digital’s footprint reached roughly 1.1% of installed capacity in 2025, up from 0.5% two years earlier, and is expected to climb as inkjet speeds pass 6,000 sheets per hour. Click charges remain four to five times costlier than flexo inks, capping economic run lengths near 20,000 sheets. Still, converters tout the ability to charge premium pricing for same-day jobs, capturing fresh slices of the North America folding cartons market. Lithographic presses remain the benchmark for ultra-high-graphic cosmetics and pharmaceuticals, and gravure continues to serve million-unit confectionery and tobacco orders.

Digital’s relative gains are most pronounced in premium beauty, nutraceuticals, and seasonal gift packs, where SKUs proliferate, and life cycles shorten. HP Indigo and Xerox Iridesse platforms introduced automated calibration in 2025, reducing color-matching time to minutes and reducing labor and rework. U.S. converters located within 100 miles of e-commerce fulfillment hubs deploy hybrid lines that gang run flexo bases with inkjet personalized sleeves. Mexican facilities increasingly earmark a digital cell for pilot orders that prove the concept before capital-intensive nationwide launches. Over the forecast horizon, digital will not rival flexo in raw tonnage, but its strategic value for speed-to-market and brand interaction will ensure a growing revenue share in the North America folding cartons market.

By End-User Industry: E-Commerce Tops the Growth Chart

Food and Beverage delivered the largest 46.15% contribution in 2025, yet growth decelerates as flexible pouches erode snack-category share. E-commerce and Retail-Ready Packaging outpaces all peers with an expected 8.91% CAGR, bolstered by retailer guidelines that mandate perforated tear strips, scannable surfaces, and RFID integration. Healthcare and Pharmaceuticals expand steadily on the back of Drug Supply Chain Security Act serialization, while Personal Care and Cosmetics brands emphasize premium unboxing experiences to elevate perceived value. Electrical and Electronics, Household and Industrial Goods, and Tobacco show modest gains, with tobacco buoyed only by flavored cigarillos and premium line extensions.

Shelf-ready mandates slashed labor at distribution centers by an estimated 15-25%, a savings that more than offsets carton cost premiums. Amazon’s 2026 RFID requirement adds USD 0.05-0.10 per unit but delivers real-time inventory accuracy, further entrenching converters able to embed inlays inline. International Paper shifted portions of its Paper and Specialty segment toward e-commerce formats that match ship-in-own-container tests, adding weight to the North America folding cartons market growth narrative. Food manufacturers continue to specify barrier-coated boards for frozen entrées, balancing recyclability with microwave performance. The interplay of these drivers sustains segment diversification and cushions converters against downside in any single category.

Geography Analysis

The United States accounted for 61.81% of the North America folding carton market in 2025 due to its vast consumer base, advanced e-commerce ecosystem, and dense pharmaceutical supply chain. Packaging Corporation of America invested USD 5.2 billion during the past decade to modernize mills and absorb Greif’s containerboard assets, expanding capacity to 800,000 tons annually and securing high-margin contracts. Smurfit WestRock’s withdrawal from 1.2 billion square meters of low-margin volume underscores a pivot toward pharmaceutical, cosmetics, and e-commerce niches that deliver superior contribution margins. Mounting PFAS regulations in Washington, California, Maine, and Minnesota are driving costly barrier-coating upgrades, but they also erect entry barriers that favor the established leaders.

Mexico is projected to post the fastest CAGR of 8.19% through 2031, as USD 41 billion in foreign direct investment poured into manufacturing during the first three quarters of 2025. Industrial real estate absorption jumped more than 60% year over year in Ciudad Juárez, signaling robust demand for localized cartons that meet USMCA rules of origin. Tetra Pak’s MXN 1 billion (USD 54.6 million) expansion in Mexicali lifted output by 60% and deepened Mexico’s role as a supply hub serving both North and South America. Government-backed infrastructure funding of MXN 722 billion (USD 40.6 billion) for 2026 targets energy and water upgrades that mitigate grid bottlenecks in the north.

Canada delivers moderate growth centered in Ontario and British Columbia, where population density and cross-border flows with the United States stabilize folding-carton demand. The closure of Smurfit WestRock’s La Tuque SBS machine in 2025 reduced domestic premium-grade supply, increasing reliance on U.S. mills. Federal plastics bans and provincial extended producer responsibility regimes reinforce a swing toward fiber packaging, yet higher capital costs restrain large-scale mill investments. Overall, geography-driven diversification enables converters to balance mature U.S. volume with high-growth Mexican capacity while Canada provides steady cash flow, preserving resilience within the broader North America folding cartons market.

Competitive Landscape

The top five producers, Smurfit WestRock, International Paper, Packaging Corporation of America, Graphic Packaging, and Georgia-Pacific, account for roughly 55-60% of regional capacity, giving the North America folding cartons market a moderately concentrated profile. Smurfit WestRock targets North American adjusted EBITDA of USD 4.2 billion by 2030 by prioritizing high-margin, design-led contracts and leveraging its Design2Market platform, which unites 2,000 designers across 34 experience centers.

International Paper completed the DS Smith integration and plans to spin off its consumer packaging arm, sharpening its focus on corrugated and releasing white space for nimble folding-carton specialists. Packaging Corporation of America invested USD 5.2 billion in mill modernization and energy self-sufficiency, installing natural gas turbines that shield operations from electricity volatility. Graphic Packaging commissioned water-based barrier-coating lines at its Waco, Texas, mill to capture frozen-food and pet-food applications previously dependent on wax laminations.

Huhtamaki spent USD 30 million to embed digital presses in its Paris, Texas, plant, serving foodservice chains that demand frequent menu updates. Smaller converters unable to match the capital intensity are seeking mergers or divesting commodity accounts. Competitive advantage now hinges on fiber integration, deep automation, barrier-coating innovation, and proximity to e-commerce hubs, consolidating pricing power and market influence.

North America Folding Carton Industry Leaders

Graphic Packaging Holding Company

Smurfit Westrock plc

International Paper Company

Georgia-Pacific LLC

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Nefab opened a 3,000 m² advanced engineering center in Guadalajara, creating 60 jobs to serve electronics, semiconductor, healthcare, and automotive sectors across Mexico and the Americas.

- March 2026: Packaging Corporation of America detailed its USD 5.2 billion investment program and announced a USD 70 per ton containerboard price increase effective March 1, 2026.

- March 2026: Smurfit WestRock set a 2030 target of USD 7.0 billion adjusted EBITDA, forecasting North America margin expansion from 14.7% to 20%+.

- February 2026: Sonoco outlined 2026-2028 goals during Investor Day after posting USD 7.5 billion 2025 sales and a 19.2% EBITDA margin in Industrial Paper Packaging.

North America Folding Carton Market Report Scope

The North America folding cartons market refers to the production and commercialization of paperboard-based packaging solutions that are folded into cartons for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The North America Folding Cartons Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries), and Geography (United States, Mexico, Canada). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| United States |

| Mexico |

| Canada |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries | |

| By Country | United States |

| Mexico | |

| Canada |

Key Questions Answered in the Report

What is the current North America folding cartons market size and how fast is it growing?

The North America folding cartons market size stands at USD 13.14 billion in 2026 and is projected to reach USD 18.88 billion by 2031, recording a 7.52% CAGR.

Which material type is gaining share against premium grades?

White Line Chipboard is expected to outpace other substrates with a 7.94% CAGR through 2031 as retailers prioritize cost efficiency.

Why is Mexico the fastest-growing national market?

Nearshoring has attracted USD 41 billion in manufacturing investment, boosting demand for localized folding-carton supply and driving an 8.19% CAGR.

How are PFAS regulations impacting packaging suppliers?

New bans in several U.S. states force mills to invest USD 50-100 million in PFAS-free barrier solutions, favoring large integrated producers.

What role does digital printing play in carton production?

Digital presses support short-run, high-graphic jobs and are expanding at a 9.85% CAGR, although they still represent roughly 1% of installed capacity.

Which end-user segment is expanding the fastest?

E-commerce and Retail-Ready Packaging leads growth with an expected 8.91% CAGR, driven by retailer mandates for shelf-ready, scannable cartons.

Page last updated on: