Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

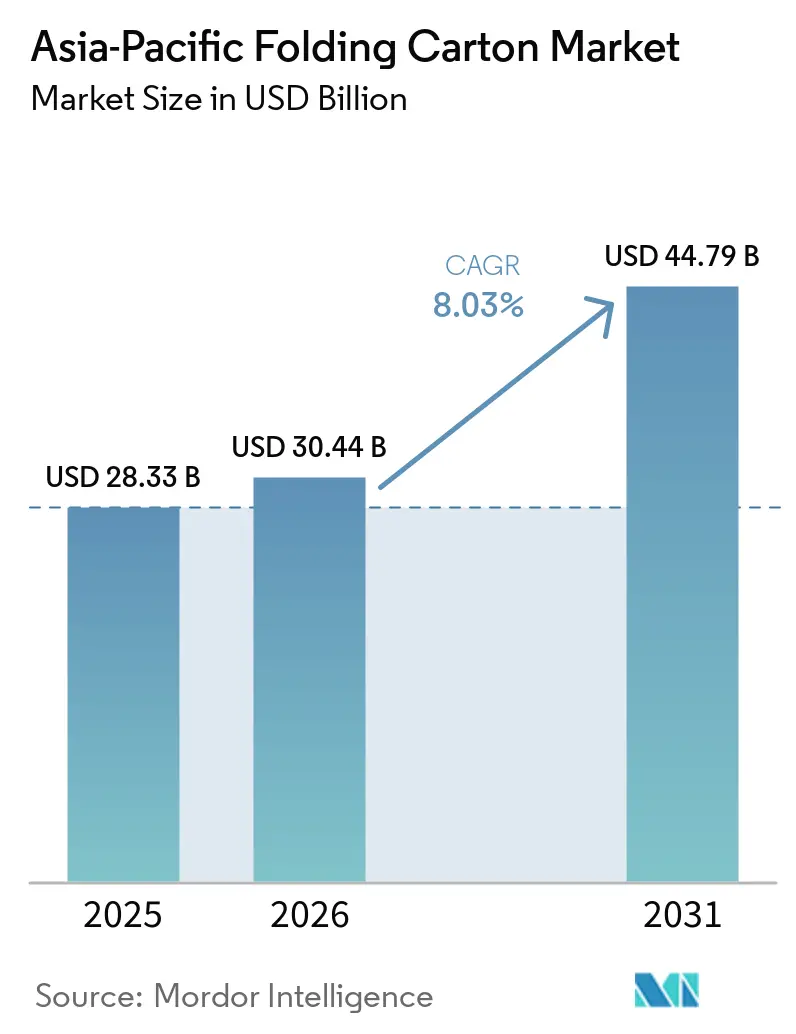

| Base Year Market Size (2025) | USD 28.33 Billion |

| Market Size (2026) | USD 30.44 Billion |

| Market Size (2031) | USD 44.79 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

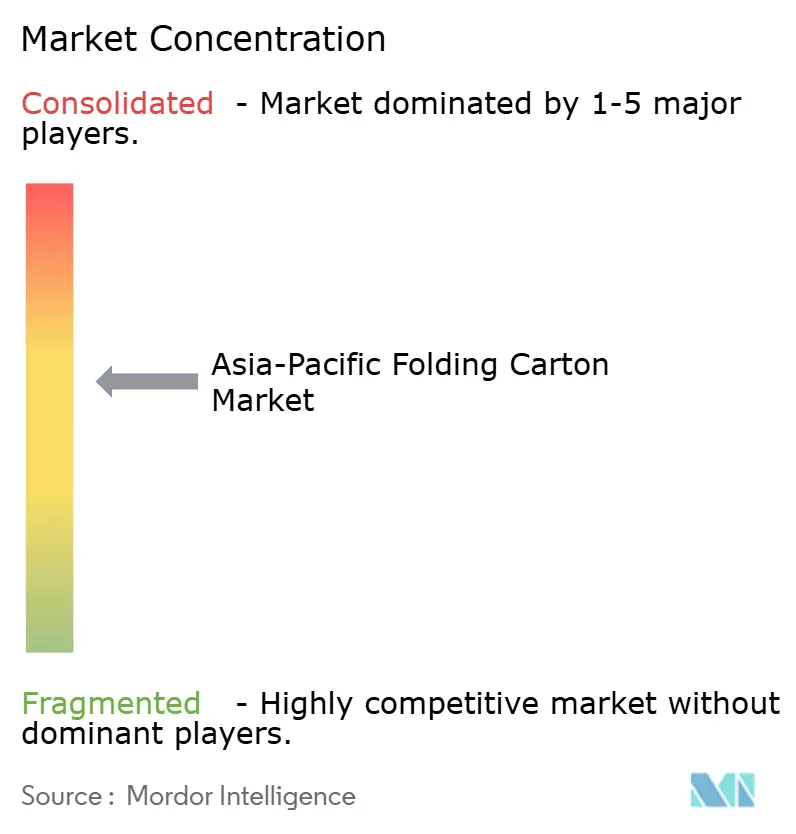

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Folding Carton Market Analysis by Mordor Intelligence

The Asia-Pacific folding carton market size is expected to grow from USD 28.34 billion in 2025 to USD 30.43 billion in 2026 and is forecast to reach USD 44.79 billion by 2031 at 8.03% CAGR over 2026-2031. The Asia-Pacific folding carton market is expanding because packaging buyers across the region are shifting secondary packs toward fiber-based formats that are easier to recycle and more acceptable in regulated retail and export channels. Demand from packaged food, dairy, beverages, and convenience products continues to provide the largest volume base, while premium healthcare, nutraceutical, and beauty applications are lifting the value mix of the region. Japan is adding an important premium layer through freezer-grade board used in convenience meal-kit and ready-meal applications, which differs from the more standard carton demand seen across much of the rest of the region. India and Southeast Asia are also drawing new converting investment as multinational and regional brands seek local suppliers that can meet print quality, compliance, and delivery requirements at scale. Competitive conditions remain moderate because global integrated producers, regional packaging groups, and many domestic converters are all active, although players with stronger paperboard integration are in a better position when raw material costs rise.

Key Report Takeaways

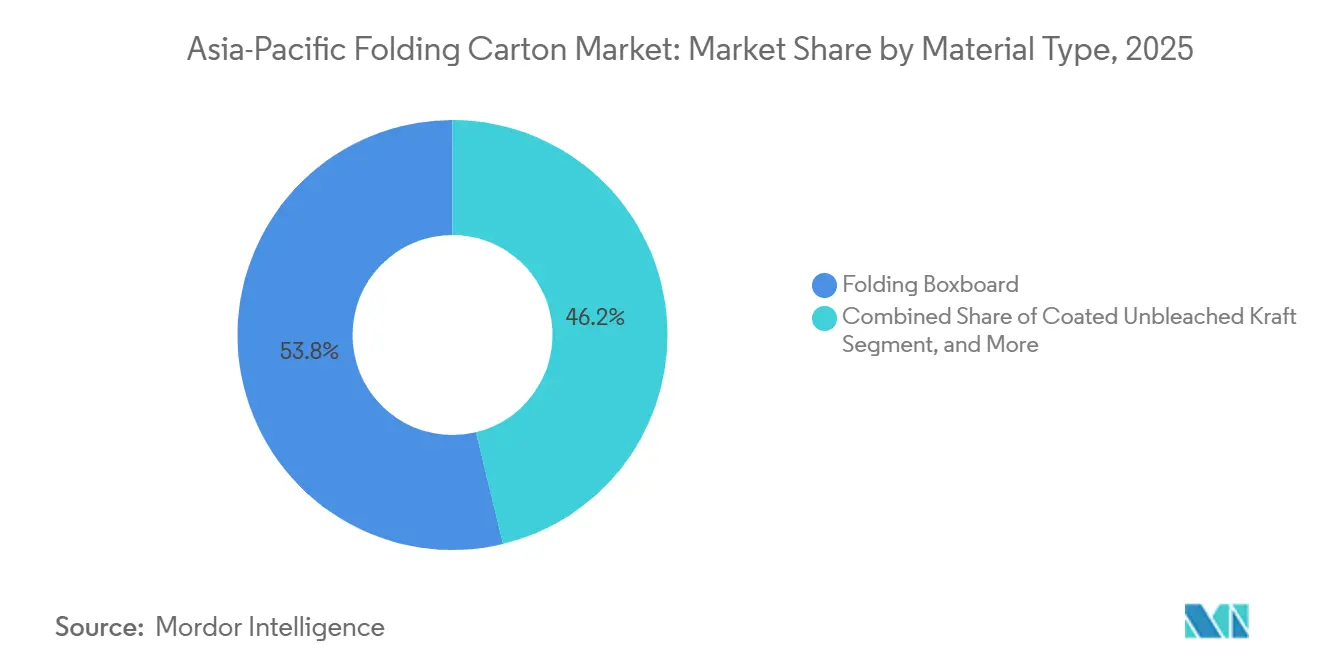

- By material type, folding boxboard captured with 53.78% of the Asia-Pacific folding carton packaging market share in 2025.

- By printing technology, the Asia-Pacific folding carton packaging market size for digital printing is projected to grow at a 10.78% CAGR to 2031.

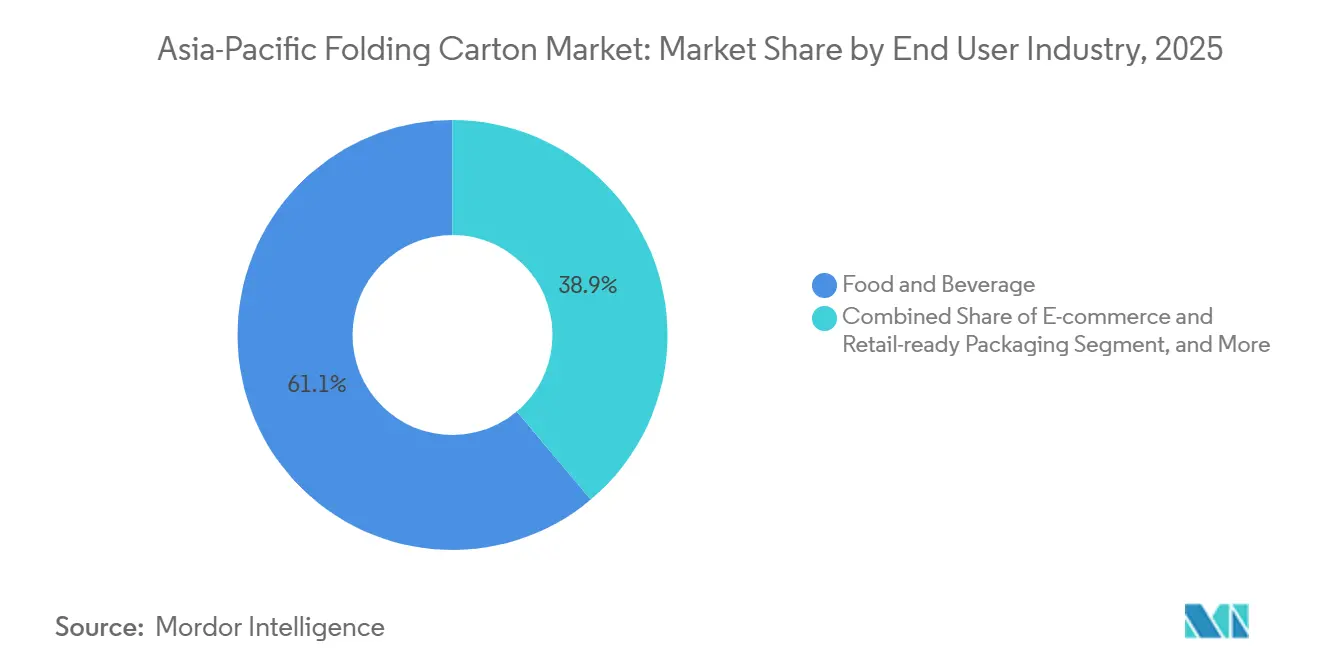

- By end-user industry, the food and beverage industry captured 61.12% of the Asia-Pacific folding carton packaging market share in 2025.

- By geography, the Asia-Pacific folding carton packaging market in India is projected to grow at a 10.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Food and Beverage Consumption in Emerging Asian Economies | +2.2% | APAC core, China, India, Vietnam, Indonesia, Thailand | Short term (≤ 2 years) |

| Shift Toward Sustainable and Recyclable Packaging Materials | +1.8% | Global, with an accelerated pace in China, South Korea, Australia, and ASEAN export hubs | Medium term (2-4 years) |

| Rapid Expansion of E-Commerce and Omni-Channel Retail | +1.4% | China, India, Southeast Asia, Vietnam, Indonesia, Thailand | Short term (≤ 2 years) |

| Increasing Pharmaceutical Production and Healthcare Spending | +1.0% | India, China, South Korea, Japan, and spill-over to Vietnam and Indonesia | Medium term (2-4 years) |

| Government-Led Subsidies for High-Color Digital Carton Printing in Export Hubs | +0.7% | China's export-manufacturing provinces, India | Medium term (2-4 years) |

| Adoption of Fungus-Based Barrier Coatings Replacing Plastic Liners | +0.4% | Early pilots in Japan, South Korea, and commercial interest in Australia and New Zealand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Food and Beverage Consumption in Emerging Asian Economies

Food and beverage demand remains the clearest volume base for the Asia-Pacific folding carton market because secondary packs for dairy, chilled foods, snacks, beverages, and ready meals are needed across modern retail, export channels, and convenience formats. The greatest change is not only higher consumption, but also a steady shift toward packaged products that require better print quality, stronger shelf impact, and food-contact suitability in both domestic and export sales. Vietnam and Indonesia stand out because converters are increasingly serving packaged food flows linked to both local demand and export manufacturing, which lifts the need for more capable board grades and more reliable finishing capacity. Single-serve, chilled, and convenience-oriented formats are also expanding the application base, especially where urban shopping patterns favor smaller packs and more frequent replenishment rather than larger household purchases.

Shift Toward Sustainable and Recyclable Packaging Materials

Sustainability is influencing the Asia-Pacific folding carton market through procurement decisions, because brand owners now screen packaging options more closely for recyclability, fiber content, and alignment with stated environmental targets. This shift matters because folding cartons often fit those requirements more easily than plastic-heavy formats that carry a more difficult recycling profile or a weaker fit with brand sustainability claims. The result is a broader conversation between converters and brand owners, especially in premium food, personal care, and export-oriented consumer goods, where packaging selection now carries a stronger compliance and reputation dimension. Graphic Packaging has reinforced this direction through its Vision 2030 program, which targets 90% renewable fuel use and 100% sustainably managed purchased forest products, showing how sustainability performance is becoming part of supplier positioning in packaging discussions. As these procurement filters spread across regional supply chains, the Asia-Pacific folding carton market benefits from its close association with recyclable, high-print, and increasingly premium fiber-based packaging solutions.

Rapid Expansion of E-Commerce and Omni-Channel Retail

E-commerce adds a separate demand layer to the Asia-Pacific folding carton market, as cartons are now selected not only for in-store display but also for shipping readiness, right-sized protection, and rapid product turnover across online channels. This shift is especially important in categories such as beauty, health supplements, and small packaged foods, where frequent stock-keeping unit changes make flexible printing, fast artwork updates, and shorter production runs more valuable than before. Omni-channel retail also changes replenishment patterns, since suppliers must serve a mix of store shelves, direct-to-consumer orders, and promotional launches that move in shorter cycles and often require smaller batches. BOBST noted that industrial inkjet for folding cartons is expanding rapidly globally, which supports the regional case for converters investing in digital capabilities to handle shorter runs and variable production needs linked to online retail activity.[1]BOBST, “The Essentials of Carton Converting,” BOBST, bobst.com The commercial effect is that converters with a better balance of structural design, finishing flexibility, and quick-turn production are likely to capture a larger share of the emerging online packaging mix.

Increasing Pharmaceutical Production and Healthcare Spending

Healthcare demand is lifting the Asia-Pacific folding carton market in a more durable way, as pharmaceutical secondary packaging requires tighter print control, traceability, tamper-evidence, and cleaner converting conditions than most mass-market carton applications. This changes the economics of the segment, since pharmaceutical cartons are less exposed to pure price competition and more influenced by compliance, consistency, and the ability to manage frequent specification changes. India, Japan, South Korea, and China all contribute to this pattern through a mix of aging populations, export-oriented drug manufacturing, and stricter labeling and coded packaging requirements, which steadily push converters toward higher-grade substrates and better printing systems. Amcor’s April 2026 opening of an advanced healthcare packaging coating facility in Malaysia, with an investment exceeding USD 35 million, shows that suppliers across the value chain are investing in the region’s healthcare packaging opportunity rather than treating it as a short-cycle niche. As a result, the Asia-Pacific folding carton market is gaining a quality-led growth stream that sits above the standard volume profile of food and beverage cartons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Paperboard Raw Material Prices | -2.1% | Global supply chain, concentrated pain in South Korea and Japan, spillover to India and ASEAN | Short term (≤ 2 years) |

| Competition From Flexible Packaging Formats | -1.5% | Southeast Asia, India, price-sensitive segments, global consumer snack and beverage channels | Medium term (2-4 years) |

| Tightening Regional Water-Use Regulations | -0.8% | China, India, Australia | Medium term (2-4 years) |

| Increasing Mill Operating Costs | -0.6% | Japan, South Korea, Australia, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility In Paperboard Raw Material Prices

Raw material volatility remains the clearest near-term constraint on the Asia-Pacific folding carton market because independent converters are exposed whenever paperboard and pulp costs move faster than contract pricing with large consumer goods customers. The pressure is not evenly distributed across the region, since import-dependent markets and converters without backward integration have less room to manage cost swings than mills that control a greater share of their own board supply. This matters for investment behavior because capacity upgrades can be delayed when margin visibility weakens, even in markets where end demand remains healthy. Smurfit WestRock’s first-quarter 2026 results pointed to higher containerboard prices in the region during March and April 2026 due to energy costs and improving demand, confirming that pricing conditions are still moving and that packaging players are operating in a cost environment that remains sensitive. The likely consequence is more differentiation between integrated suppliers that can hold margins through the cycle and smaller converters that compete heavily on standard grades and contract-driven volumes.

Competition from Flexible Packaging Formats

Flexible packaging remains a real restraint on the Asia-Pacific folding carton market, but the pressure is concentrated in categories where low unit cost and light weight matter more than structure, premium branding, or recyclability. Snack foods, confectionery, and single-serve beverage packs in price-sensitive channels still favor pouches and film-based formats in several Southeast Asian and Indian applications because the economics are often simpler for entry-price products. That creates a clear boundary for cartons in rural or low-ticket channels, where presentation value is secondary to cost control and portability. At the same time, the threat is weaker in segments that need tamper evidence, stronger shelf presence, better print quality, or a more credible recyclable packaging message, especially in premium food, healthcare, and beauty lines. The competitive picture is therefore mixed rather than universal, with folding cartons losing some ground in highly price-led formats but gaining relevance in regulated, premium, and export-facing applications across the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Folding Boxboard Leads On Scale, Solid Bleached Board Lifts Premium Value

Folding Boxboard held a 53.78% share of the Asia-Pacific folding carton market in 2025, reflecting the material’s strong fit with mass-market consumer goods that need stiffness, surface quality, and efficient conversion across large production runs. It remains the preferred volume substrate in many food, beverage, household, and general consumer applications because it offers a practical balance between appearance, structural performance, and cost across the region’s largest packaging programs. Other grades still matter, with Coated Unbleached Kraftboard retaining a role where tear strength is important and White-lined Chipboard staying relevant in more recycled-content-oriented applications that align with evolving sustainability requirements. The broad result is a material mix in which Folding Boxboard continues to anchor mainstream demand, especially in the parts of the Asia-Pacific folding carton market that depend on scale, print quality, and established converting familiarity.

Solid Bleached Board is forecast to grow at a 10.23% CAGR from 2026 to 2031, and that pace reflects rising demand in pharmaceutical, premium personal care, nutraceutical, and infant nutrition applications rather than in the high-volume food mainstream. The appeal of this grade is not only its brightness or print appearance, but also its tighter consistency, cleaner fiber profile, and stronger fit for sensitive end uses where safety, product image, and detailed print performance all matter. This makes Solid Bleached Board especially important in the higher-value layers of the Asia-Pacific folding carton industry, where buyers are willing to pay more for dependable carton performance and stronger compliance alignment. Its faster growth therefore says less about broad commoditized expansion and more about the market’s steady movement toward premium substrates in applications where regulation and brand value are both rising.

By Printing Technology: Lithographic Printing Holds the Base, Digital Printing Gains on Flexibility

Lithographic Printing captured 69.53% of the Asia-Pacific folding carton market in 2025 by printing technology, and it maintained that lead because the region still relies heavily on long production runs in food and beverage packaging, where setup costs can be spread across very large volumes. The process remains highly competitive in China, India, and Southeast Asia because converters serving major consumer goods accounts continue to prioritize repeatability, color quality, and efficient output on established equipment. Flexography and gravure stay active in narrower application pockets, but they remain secondary to offset in the main body of the market, where carton jobs still favor the economics of scale. The continued strength of offset means the Asia-Pacific folding carton market still rests on a large production base that rewards run efficiency, yield management, and dependable finishing rather than short-run flexibility alone.

Digital printing is projected to grow at a 10.78% CAGR through 2031, and its momentum comes from applications that need variable data, quicker artwork changes, smaller batches, and a lower penalty for frequent stock-keeping unit turnover. Pharmaceutical and nutraceutical cartons are especially important because coding, anti-counterfeit features, and traceable information can be integrated more directly into production without relying on secondary labeling steps. BOBST has stated that industrial-scale inkjet for folding cartons is growing at a strong pace and that the digital addressable carton volume is expanding quickly, which supports the region’s move toward more digitally enabled converting setups. Over time, this means the Asia-Pacific folding carton market will keep its offset-heavy volume structure, but a larger share of value growth is likely to come from converters that can combine digital printing with higher-complexity finishing and shorter response cycles.

By End User Industry: Food Processing Volumes Anchor Growth, Healthcare Raises the Value Mix

Food and Beverages accounted for 61.12% of the Asia-Pacific folding carton market share in 2025, confirming that the largest demand base still comes from high-volume packaged foods, dairy, beverages, and convenience products moving through retail and foodservice channels. The segment benefits from a close fit between carton performance and end-user needs, because brands want packaging that combines shelf visibility, food-contact suitability, structural reliability, and good print reproduction without moving into more expensive rigid formats. SCG Packaging’s reported demand strength in Vietnam and Indonesia during 2025 also supports the view that food and beverage growth in ASEAN is directly feeding carton demand, especially where branded packaged goods are gaining traction across organized retail and modern trade.[2]SCG Packaging Public Company Ltd., “SCGP Announces Strong 2025 Performance,” SCGP Newsroom, newsroom.scgpackaging.com Japan adds a premium pocket inside this large category through freezer-grade folding board used in convenience meal-kit and ready-meal applications, and that sub-segment carries a noticeably higher value profile than standard ambient food cartons sold elsewhere in the region.

Healthcare/Pharmaceuticals are projected to expand at a 10.62% CAGR from 2026 to 2031, making it the fastest-growing end-user segment and one of the clearest value drivers within the Asia-Pacific folding carton industry. The segment is moving away from commodity-style procurement because serialization, anti-counterfeit printing, traceability, and tighter packaging integrity requirements are raising the importance of substrate consistency and controlled converting. That shift supports premium board grades, especially in cartons for injectables, export medicines, nutraceuticals, and specialist therapies, where the printed carton functions as part of a broader compliance system rather than as a simple outer pack. The combined effect is that the Asia-Pacific folding carton market is no longer driven only by food volumes, because healthcare is steadily raising the ceiling for margins, technical standards, and converter investment across the region.

Geography Analysis

China held 46.63% of the Asia-Pacific folding carton market share in 2025, giving the country a decisive lead based on its scale of consumer goods manufacturing, a large cartonboard base, and broad end-user demand across food, beverages, personal care, electronics, and healthcare. That position is reinforced by the fact that China remains the region’s main center for high-volume packaging conversion, where long runs and broad customer diversity support both mainstream and more specialized carton applications. Smurfit WestRock stated in its 2025 annual report that its Asia-Pacific consumer packaging operations in China, Japan, and Australia were seeing an improving demand profile, which aligns with the region’s stronger packaging activity entering 2026.[3]Smurfit WestRock plc, “2025 Annual Report,” Smurfit WestRock, smurfitwestrock.com Japan, although smaller in volume terms, continues to matter because it supports premium demand for freezer-grade food cartons and tamper-evident pharmaceutical packaging, which usually carry better per-unit margins than standard consumer cartons.

India is projected to record the fastest expansion in the Asia-Pacific folding carton market size by geography, at 10.15% CAGR from 2026 to 2031, supported by a combination of consumer goods demand, pharmaceutical production, and widening organized retail penetration. The growth case is stronger than a simple population story because brand owners increasingly need local suppliers that can deliver tighter print quality, faster design changes, and compliance-ready packaging for both domestic and export programs. This is drawing attention to industrial corridors such as Tamil Nadu and Maharashtra, where new investment and export-linked packaging activity are strengthening the base for local folding carton conversion. Pharmaceutical demand adds another layer because serialization and coded packaging needs favor converters that can deliver more precise printing and higher substrate consistency than the market’s lowest-cost operators. ASEAN capacity priorities set out by SCG Packaging also support the view that India and neighboring markets are being treated as active growth destinations within the broader Asia-Pacific folding carton market, not as distant long-term options.

Australia and New Zealand represented a smaller absolute share of the Asia-Pacific folding carton market, but they remain important because they set a higher benchmark for recyclability, packaging quality, and procurement discipline in premium end uses. That matters for exporters across Southeast Asia, since suppliers serving those markets often need to match stronger packaging expectations on fiber quality, print presentation, and documentation. The Rest of Asia-Pacific, especially Indonesia, Thailand, the Philippines, Malaysia, and Vietnam, continues to generate incremental demand through deeper organized retail penetration, more branded packaged goods, and a growing base of local and multinational manufacturing. As these markets mature, the Asia-Pacific folding carton market is likely to see more demand for certified, better-finished, and more flexible carton supply rather than only higher tonnage from standard grades.

Competitive Landscape

The Asia-Pacific folding carton market remained moderately consolidated at the top end in 2025, with global groups such as Smurfit WestRock and Graphic Packaging competing alongside regional players such as Oji Holdings and SCG Packaging, while a very large field of domestic converters still handled a major share of commodity-grade volume. This structure matters because scale is important in procurement, but local presence, substrate access, and finishing flexibility still shape buying decisions across individual countries and end-use categories. Smurfit WestRock said its merger integration exceeded USD 400 million in targets by the end of 2025 and reported an improving demand profile in Asia-Pacific operations, indicating that large integrated suppliers are entering the current phase with stronger operating leverage. Graphic Packaging reported USD 2,208 million in 2025 net sales for its International Paperboard Packaging segment and continued to use sustainability goals as a commercial differentiator, which strengthens its standing in customer conversations that now combine packaging performance with environmental reporting expectations.

These moves are important because the Asia-Pacific folding carton market rewards players that can pair regional scale with automation, stable quality, and sufficient technical depth to serve both standard consumer goods and more specialized healthcare or premium beauty accounts. At the same time, domestic Chinese and Indian converters continue to absorb a large share of basic carton volumes, which keeps pricing pressure alive in mainstream formats and prevents the market from becoming tightly concentrated. Amcor’s new healthcare packaging coating facility in Malaysia also shows that competition is broadening beyond traditional carton converters and increasingly includes adjacent packaging specialists building positions in higher-value regional packaging segments.[4]Amcor, “Amcor Opens Advanced Healthcare Packaging Coating Facility in Malaysia,” PR Newswire, prnewswire.com The most open competitive spaces remain premium healthcare cartons in faster-growing markets, digitally enabled short-run production for online-first brands, and higher-quality converted board for export-oriented packaged food applications.

The next stage of competition is likely to depend more on process capability than on simple volume alone, because buyers are asking for faster changeovers, more traceable output, and stronger sustainability credentials at the same time. BOBST’s assessment of rising industrial inkjet use in folding cartons supports that direction, since digital systems reduce the minimum efficient run length and make trial orders or frequent design changes easier to serve. Longer term, alternative barrier technologies may create another point of separation, as research highlighted by the American Chemical Society showed that fungus-based coatings combined with cellulose nanofibrils can improve water resistance on fiber-based substrates and may help reduce dependence on plastic liners in future packaging formats. Overall, the Asia-Pacific folding carton market remains competitive and only moderately concentrated because leadership is visible at the top, but a wide domestic supply base still holds meaningful volume across standard applications.

Asia-Pacific Folding Carton Industry Leaders

Graphic Packaging International, LLC

International Paper Company

Smurfit WestRock plc

Stora Enso Oyj

Oji Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Smurfit WestRock plc reported Q1 2026 results showing continued growth across its EMEA and APAC business segment, with containerboard prices in the region increasing in March and April 2026 due to higher energy costs and improving demand.

- April 2026: Amcor plc opened an advanced healthcare packaging coating facility in Subang Jaya, Selangor, Malaysia, representing an investment exceeding USD 35 million. The plant introduces air-knife coating technology to Southeast Asia for the production of coated medical paper used in sterile medical device packaging, strengthening regional supply chain resilience and supporting healthcare customers across the Asia-Pacific region.

- February 2026: SCG Packaging Public Company Ltd. (SCGP) set a 2026 investment budget of THB 10,000 million (USD 300 million) and an EBITDA target of THB 18,300 million (USD 500 million), confirming expansion opportunities in Vietnam and Indonesia, with a market-entry focus on India.

- January 2026: SCG Packaging reported strong 2025 full-year performance, with EBITDA of THB 17,210 million (USD 482 million) and profit of THB 4,069 million (USD 113.4 million) (up 10% year-on-year), despite a 6% decline in total revenue.

Asia-Pacific Folding Carton Market Report Scope

The scope of this report covers the analysis of the Asia-Pacific folding carton market, focusing on its current trends, growth drivers, challenges, and opportunities. Folding cartons are paper-based packaging solutions widely used for consumer goods, including food, beverages, personal care products, and others. The study examines market dynamics, the supply chain, and the competitive landscape, providing insights into market performance during the forecast period.

The Asia-Pacific Folding Carton Packaging Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and More) and Geography (China, Japan, India, South Korea, Australia and New Zealand, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

By Printing Technology

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

By End-User Industry

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current and forecast size of the Asia-Pacific folding carton market?

The Asia-Pacific folding carton market was valued at USD 28.34 billion in 2025, is estimated at USD 30.43 billion in 2026, and is forecast to reach USD 44.79 billion by 2031 at an 8.03% CAGR.

Which end-user segment drives demand for folding cartons in the Asia-Pacific?

Food and Beverages led demand, accounting for 61.12% of 2025 revenue, supported by packaged foods, dairy, beverages, and convenience-oriented retail formats across the region.

Which end-user segment is growing fastest in the region?

Healthcare/Pharmaceuticals is the fastest-growing segment, with a projected 10.62% CAGR from 2026 to 2031, supported by tighter packaging requirements, traceability needs, and higher-value carton specifications.

Which material type has the strongest position in the region?

Folding Boxboard led with a 53.78% share in 2025 because it combines stiffness, print quality, and established converting familiarity across large food, beverage, and consumer goods programs.

Why is digital printing gaining ground in folding carton conversion?

Digital printing is forecast to grow at a 10.78% CAGR because it supports variable data, shorter runs, quicker artwork changes, and better fit for pharmaceutical, nutraceutical, and online-first packaging programs.

Which countries are shaping the regional growth pattern the most?

China remained the largest country with 46.63% share in 2025, while India is expected to grow fastest at a 10.15% CAGR through 2031, with ASEAN markets adding meaningful incremental demand.

Page last updated on: