Germany Folding Carton Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

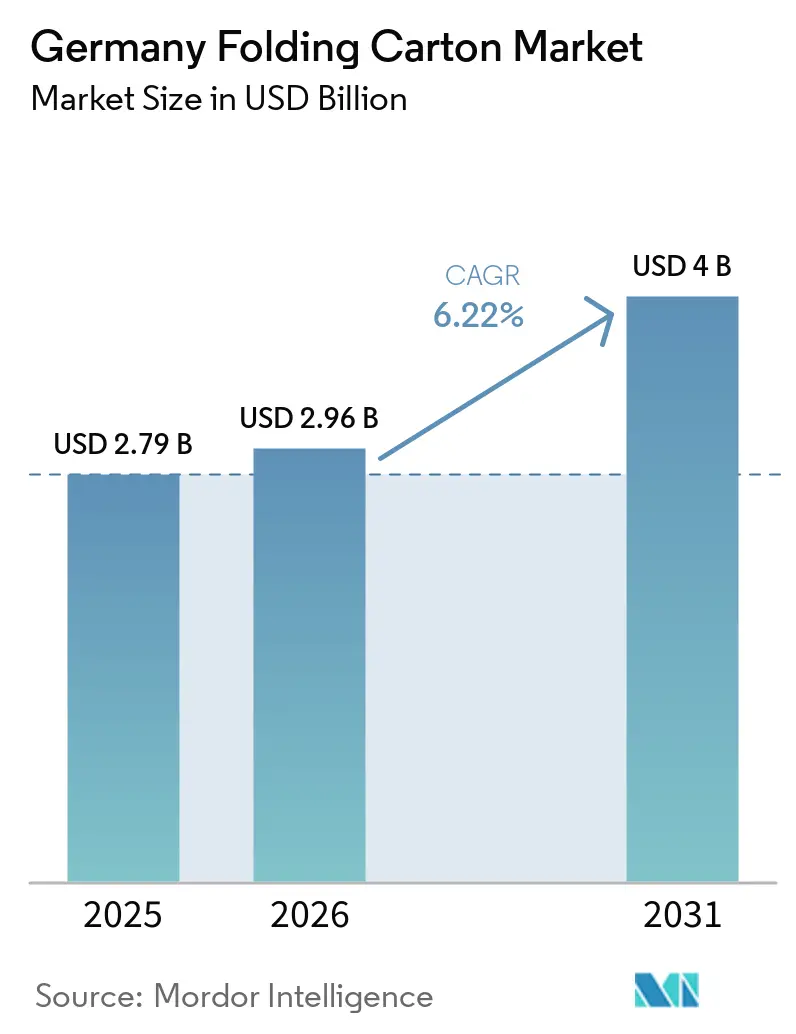

| Base Year Market Size (2025) | USD 2.79 Billion |

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 4 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

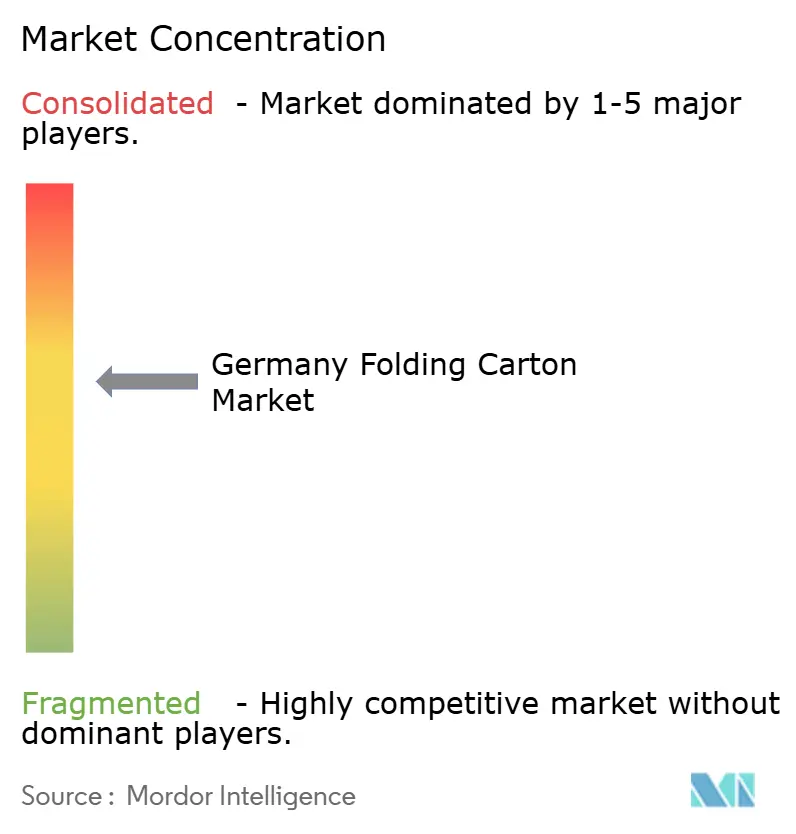

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Folding Carton Market Analysis by Mordor Intelligence

The Germany folding carton market size is expected to increase from USD 2.79 billion in 2025 to USD 2.96 billion in 2026 and reach USD 4.00 billion by 2031, growing at a CAGR of 6.22% over 2026-2031. The steady climb reflects Germany’s combination of stringent recycling mandates, e-commerce density, and premiumization trends that collectively favor fiber over flexible plastics. Brand owners in food, beverage, cosmetics, and pharmaceuticals continue to specify mono-material carton because they meet evolving retailer scorecards on recyclability and unlock visible sustainability messaging. Rapid automation in urban micro-fulfillment centers reinforces demand for shelf-ready carton that cut in-store labor, while rising labor costs push retailers toward formats that arrive pre-assembled and presentation-ready. Parallel advances in digital printing enable converters to profitably serve limited-edition SKUs, subscription gifting, and pharmaceutical serialization runs of fewer than 5,000 units, giving the German folding carton market a robust innovation pipeline. Converters that invested early in PFAS-free barrier coatings and lightweight virgin-fiber substrates now hold a compliance and cost advantage as the European Union deadline for fluorochemical elimination draws near.

Key Report Takeaways

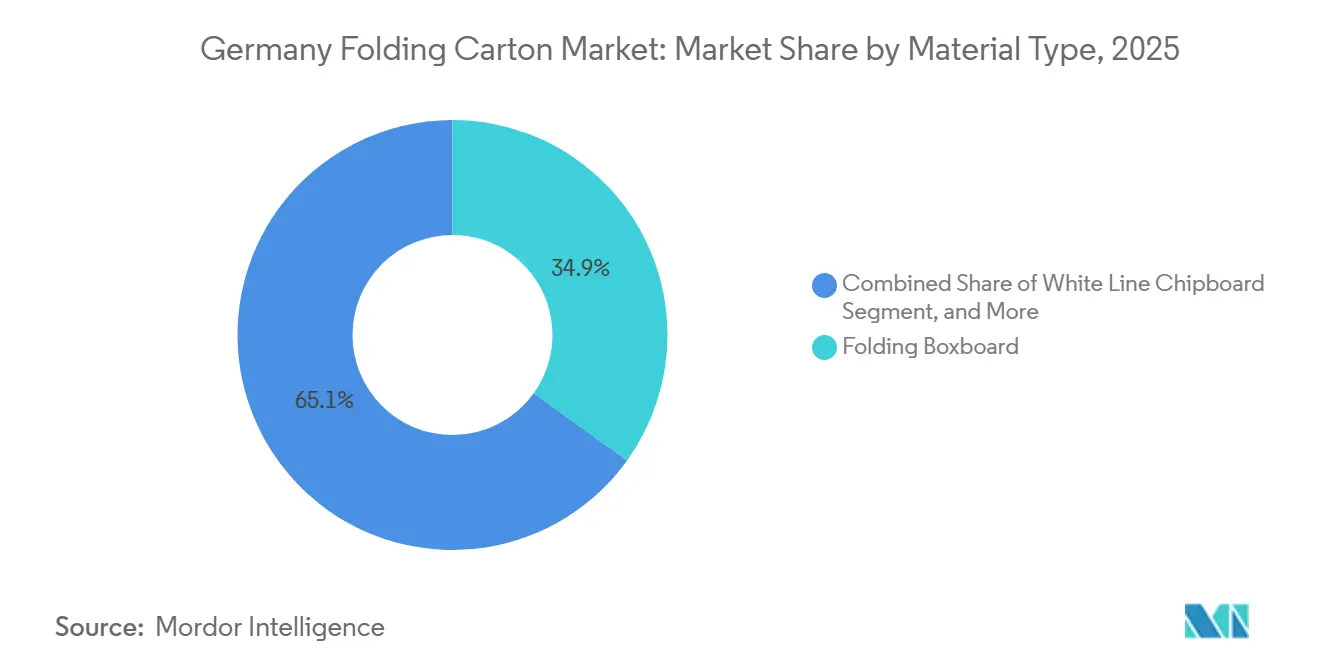

- By material type, folding boxboard led with 34.91% of the Germany folding carton market share in 2025.

- By printing technology, digital presses are forecast to grow at an 8.54% CAGR between 2026-2031, reflecting the shift toward short-run personalization inside the Germany folding carton market.

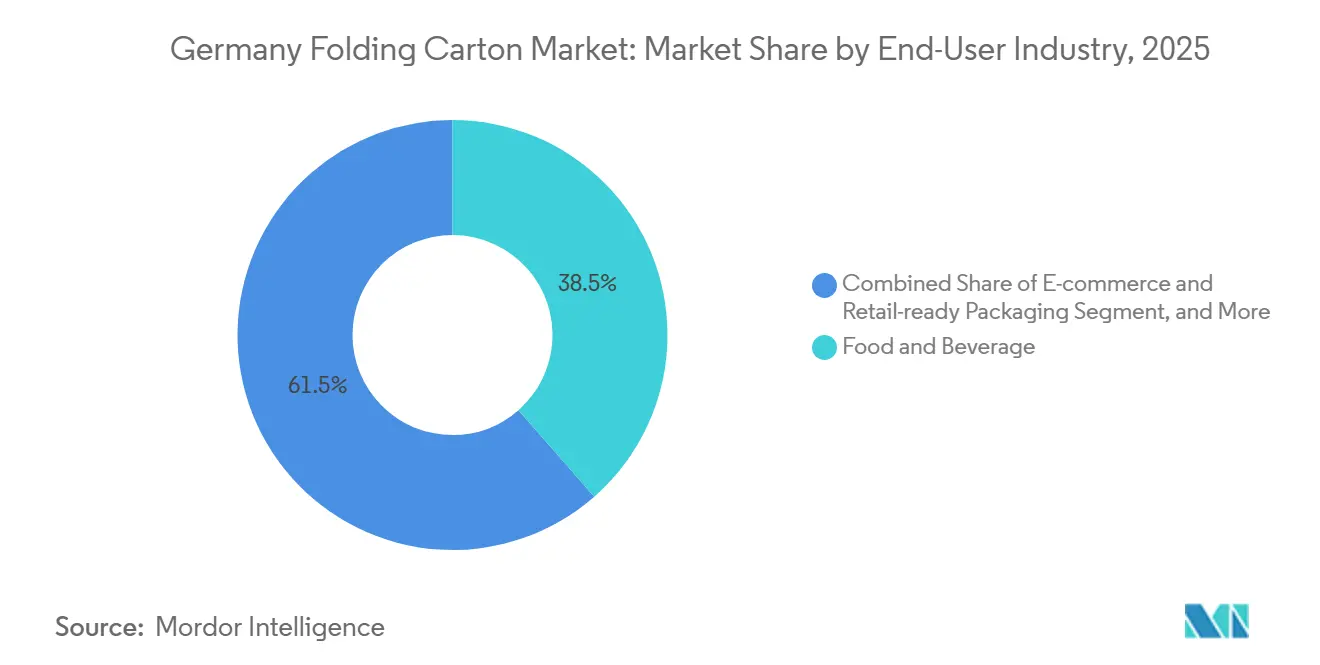

- By end-user industry, food and beverage generated 38.54% of 2025 demand, retaining the largest stake in the Germany folding carton market size.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand For Sustainable Packaging In Food And Beverage | +1.80% | Germany, spillover Austria and Benelux | Medium term (2-4 years) |

| Government Regulations Encouraging Recyclable Materials | +1.50% | Germany, aligned with EU PPWR and national VerpackG | Long term (≥ 4 years) |

| Expansion Of E-Commerce Sector | +1.20% | Urban hubs Berlin, Hamburg, Munich, Rhine-Ruhr | Short term (≤ 2 years) |

| Advancements In Digital Printing Customization | +0.90% | Pharmaceutical and cosmetics clusters | Medium term (2-4 years) |

| Rising Brand Owner Focus On Premiumization | +0.60% | Premium food and personal-care segments | Medium term (2-4 years) |

| Shift Toward Lightweighting For Logistics Efficiency | +0.40% | National distribution networks and export corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand For Sustainable Packaging In Food And Beverage

Food and beverage producers are accelerating the switch from multilayer films to fiber-based carton to satisfy retailer sustainability scorecards and consumer expectations for readily recyclable packaging. Verified lifecycle-assessment data shows an 8% drop in fossil CO₂ equivalent per tonne of carton between 2021 and 2024, reinforcing procurement decisions that link packaging to Scope 3 decarbonization commitments. German dairies and bakery brands highlight these gains in annual ESG reports, translating carton adoption into marketable climate credentials. The sector’s 87% European recycling rate already surpasses the VerpackG target and is moving toward 90%, giving carton an end-of-life infrastructure advantage over flexible plastics. Converters capable of issuing third-party-audited chain-of-custody documents now win volume even in cost-sensitive private-label channels because retailers view transparent data as insurance against future greenwashing fines.[1]PRO-CARTON, “Faltschachtelverpackungen: Messbare CO₂-Reduktion, hohe Recyclingquote und nachhaltige Kreislaufwirtschaft,” procarton.com

Government Regulations Encouraging Recyclable Materials

Extended producer-responsibility fees under the German Packaging Act rise sharply for formats deemed hard to recycle, tilting total system costs in favor of mono-material folding carton. The August 2026 EU ban on PFAS in food-contact packaging removes a critical barrier performance edge that fluoropolymer-coated films held, compelling converters to adopt water-based or bio-polymer coatings that preserve oil resistance without fluorinated chemistry. Early movers who partnered with chemical suppliers for PFAS-free solutions now control approved capacity and command premium pricing. On top of national rules, the EU Packaging and Packaging Waste Regulation will require every package on the market to be recyclable by 2030, effectively sidelining most multilayer flexible structures unless chemical recycling scales up. German converters’ early compliance secures long-term contracts from multinational quick-service restaurants aiming to avoid costly mid-decade package transitions.[2]ARCHROMA, “Cartaseal OGB F10 PFAS-Free Oil and Grease Resistant Coating for Food and Non-Food Board,” archroma.com

Expansion Of E-Commerce Sector

Germany’s dense last-mile delivery network fuels demand for retail-ready carton that travel directly from automated fulfillment centers to store shelves. Carton formats with integral tear strips and print-in-place barcodes reduce in-store labor by eliminating unpacking and shelf facing, delivering measurable cost savings for big-box retailers facing rising wages. Direct-to-consumer beauty and nutraceutical brands leverage digitally printed folding carton to embed AR markers and serialized QR codes for engagement and anti-counterfeiting assurance. Converters supplying these channels invest in inline gluing and robotics that swap SKUs without extended downtime, meeting the e-commerce expectation of 24-hour art-to-pack lead times. Urban micro-fulfillment centers now specify cube-optimized carton that reduce void fill and limit transport emissions, deepening penetration of the German folding carton market into segments once held by poly-mailers and padded envelopes.[3]THIMM GROUP, “Automated Packaging Solutions with Integrated Digital Codes,” thimm.com

Advancements In Digital Printing Customization

Variable-data digital presses lower economic run lengths to the 1,000-unit range, unlocking profit in personalized gifting, subscription unboxing, and regulatory serialization. Pharmaceutical fillers frequently request packs carrying unique 2D DataMatrix codes, lot numbers, and even patient-specific language, tasks that offset lithography cannot meet without prohibitive plate costs. German converters deploying HP Indigo, Heidelberg Cartonmaster, or Koenig and Bauer hybrid units report order cycles slashed from two weeks to 48 hours, aligning packaging timelines with agile product-launch calendars. Although digital ink carries a higher cost per square meter, make-ready elimination and zero waste balance the economics at short lengths, supporting price parity with traditional processes for SKUs under 5,000 sheets. Brand owners view rapid graphics changeovers as a hedge against inventory obsolescence, further embedding digital capacity within the Germany folding carton market.[4]THIMM GROUP, “Automated Packaging Solutions with Integrated Digital Codes,” thimm.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Recycled Fiber Prices | -0.70% | Germany, tied to European recovered-paper export flows | Short term (≤ 2 years) |

| Competition From Flexible Plastic Packaging | -0.50% | Segments prioritizing barrier over recyclability | Medium term (2-4 years) |

| High Capital Expenditure For Advanced Printing Presses | -0.30% | Barrier for small and mid-tier converters | Long term (≥ 4 years) |

| Supply-Chain Disruptions For Specialty Coatings | -0.20% | Dependence on BASF, Evonik, Henkel for water-based barriers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility In Recycled Fiber Prices

Recovered-paper prices spiked by EUR 20-30 (USD 22-33) per tonne in April 2025 when export demand collided with a domestic collection dip, cutting converters’ margins on recycled-content grades. Because folding boxboard and white-line chipboard carry contract ceilings on price pass-through, mid-tier converters absorbed temporary losses, which curbed discretionary capital spending. Spot-market swings also destabilized forecast accuracy for supply-chain planners, leading brand owners to hedge their exposure by splitting volumes between virgin and recycled substrates. Larger integrated groups blunted volatility through captive pulp lines, but independent German converters faced procurement risk that complicated long-term capacity planning. Continuing fiber price sensitivity remains the most unpredictable constraint on the German folding carton market.

Competition From Flexible Plastic Packaging

Flexible films retain moisture and oxygen barrier supremacy in high-fat, frozen, and extended-shelf-life foods, keeping carton on the defensive in those categories. Multi-serve confectionery bags still ship lighter and cube more efficiently than equivalent carton, maintaining a cost edge despite higher disposal fees. Although PFAS-free barriers narrow the functional gap, folding-carton coatings add cost and production complexity, sometimes offsetting recyclability gains in buyer evaluations. Consequently, the Germany folding carton market focuses on segments where visual impact, shelf presentation, or regulatory serialization outweigh barrier performance, ceding certain high-barrier niches to polymer rivals while seeking technology partnerships that can close the gap without compromising curbside recyclability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Grades Ride Natural Aesthetics And Cost Efficiency

Coated Unbleached Kraft’s share acceleration reflects quick-service restaurants and industrial suppliers embracing natural-brown fibers as visual shorthand for sustainability. The format’s 7.18% forecast CAGR positions it as the growth engine of the German folding carton market size for materials. Lightweighting advances from suppliers such as Stora Enso push grammage into the 205-310 g/m² range, translating into logistics savings without sacrificing stiffness. In contrast, Solid Bleached Sulfate holds premium ground in luxury chocolate and fragrance gift sets, but its uptick slows as brand owners reconcile glossy whiteness with decarbonization pledges. White Line Chipboard, though price-competitive, faces margin pressure when recovered-paper indices surge, underscoring the volatility restraint already noted. Folding Boxboard remains the anchor at 34.91% market share, straddling printability and cost but facing incremental loss to kraft, where natural-look trays meet functional needs. The German folding carton market share for specialty metalized boards remains niche, serving frozen entrées and household blade cartridges that demand dual-side barrier yet accept higher unit prices.

Second-generation coating lines now integrate water-based oil- and grease-resistance directly into kraft substrates, eliminating an extra laminating pass and shortening cycle time. Mayr-Melnhof’s lifecycle audit quantifies 16-30% carbon savings compared with average European production, arming converters with data for brand-owner RFP scoring. As carbon accounting tightens, the German folding carton market gravitates toward grades that offer verified cradle-to-gate transparency and end-of-life recyclability.

By Printing Technology: Digital Captures The Short-Run Sweet Spot

Although lithographic presses account for 42.13% of 2025 output, converters signal a plateau in new-build investments as SKU proliferation erodes average run length. Digital’s 8.54% projected CAGR outsizes every other technology, driven by e-commerce gift messaging and pharmaceutical serial numbers that change every batch. Gravure retains footholds in tobacco carton with multi-million-unit orders, justifying cylinder costs that digital cannot amortize, yet its share sees a slow bleed as tobacco volumes contract. Flexographic units serve the detergent and DIY segments where graphics demand is moderate, and speed trumps resolution.

The German folding carton market size for hybrid press installations is rising, as converters hedge by pairing offset units with inline inkjet personalization bars. Heidelberg’s Cartonmaster CX 145 typifies the trend of a single platform that runs static CMYK litho and variable-data inkjet in a single pass, satisfying both cost and agility metrics. Competitive distinction increasingly centers on workflow software that links ERP order entry to digital front ends, enabling 24-hour art turnaround. Converters lacking color management and data-handling infrastructure risk disqualification from tenders that weigh responsiveness equal to price.

By End-User Industry: E-Commerce Packaging Surges Past Incumbents

Food and Beverage’s 38.54% lead anchors volume but shows mid-single-digit growth amid grocery inflation, dampening product launches. Conversely, the E-commerce and Retail-ready segment’s 7.76% projected CAGR makes it the fastest-growing segment in the German folding carton market. Direct-to-consumer cosmetics and nutraceutical brands specify packs that arrive shelf-ready, integrating transit protection, branding, and easy-open features. Healthcare and Pharmaceuticals remain high-margin due to mandatory Braille embossing and tamper-evident gluing, requirements that favor carton rigidity over flexible blisters in over-the-counter formats. Personal Care skews premium, leveraging kraft-board textures and metallic debossing to convey natural luxury.

Mature sectors such as household appliances and tobacco see flattish trajectories, with volumes tied more to macro consumption patterns than to packaging innovation. Serialization deadlines in the EU Falsified Medicines Directive intensify demand for carton-based data carriers, further embedding folding carton within pharma’s supply chain. Automotive aftermarket kits shifting from plastic clamshells to carton sleeves for toolsets add incremental tonnage, rounding out diversified demand sources.

Geography Analysis

Germany remains the epicenter of European folding-carton conversion capacity, drawing substrate from Austrian, Finnish, and Polish mills through efficient rail corridors. The German folding carton market is bolstered by proximity to the headquarters of multinational food, cosmetics, and chemical companies, concentrated in North Rhine-Westphalia and Baden-Württemberg. Federal recycling quotas and extended producer-responsibility surcharges further shift demand toward recyclable cartonboard formats, while regional governments co-fund automation along the Rhine-Main logistics corridor, supporting e-commerce fulfillment.

Neighboring Netherlands and Czech Republic facilities compete through lower labor costs but lack the just-in-time responsiveness of German plants, especially for high-specification pharmaceutical orders requiring delivery within 72 hours. International Paper and DS Smith rationalized corrugated assets post-merger while retaining folding-carton lines, indicating the segment’s strategic importance. This selective consolidation underscores the resilience of folding carton within Germany’s broader packaging landscape.

PFAS-free barrier coating capacity is increasingly localized in Lower Saxony’s chemical clusters, reducing supply-chain complexity and lead times for compliant materials. While Eastern European converters continue to attract commodity-grade production, regulatory pressures and sustainability requirements are redirecting premium, high-compliance jobs back to Germany. These dynamics collectively sustain growth momentum and reinforce Germany’s leadership in the European folding carton market.

Competitive Landscape

Market concentration remains moderate, with the top five players accounting for an estimated 62–65% of domestic revenue. Mayr-Melnhof Group leverages vertical integration across substrate production and converting operations to reduce unit costs and intensify competitive pressure on smaller firms. Smurfit Westrock has shifted focus toward specialty segments after closing two commodity sites, reallocating capital expenditure toward hybrid press technologies, while private-equity-backed Grenadier Packaging is driving consolidation through acquisitions in the Netherlands and Poland to strengthen regional supply into Germany.

Mid-sized family-owned firms are responding with targeted investments in digital printing, PFAS-free coating technologies, and ISO-certified cleanroom facilities tailored for medical-device packaging. Strategic developments in 2026 include Faller Packaging receiving capital from Imker Group to expand serialization capabilities, enhancing compliance in regulated sectors. Meanwhile, Stora Enso introduced Performa Lumi, a lightweight board aimed at sustainability-driven retail demand, and Graphic Packaging International upgraded gravure capacity in Austria to maintain leadership in tobacco carton while also supporting adjacent applications such as textile tagging.

Sustainability and regulatory alignment are increasingly shaping competitive positioning, as producers invest in recyclable barrier solutions and fiber-based alternatives to plastics. Companies are also strengthening supply-chain resilience through nearshoring strategies and long-term pulp sourcing agreements to mitigate input volatility. These combined shifts indicate a market moving toward higher-value, compliance-driven offerings while maintaining cost discipline in core corrugated segments.

Germany Folding Carton Industry Leaders

Smurfit Westrock plc

Mondi plc

Mayr-Melnhof Karton AG

Stora Enso Oyj

Metsä Board Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The European Commission cleared International Paper’s acquisition of DS Smith, with required divestments in France, Portugal, and Spain to safeguard competition.

- February 2026: HP Indigo and ePac signed a USD 50 million deal for ten Indigo 200K presses aimed at short-run pharmaceutical and personalized e-commerce carton.

- January 2026: Faller Packaging welcomed Imker Group as a 25% shareholder, unlocking capital for additional serialization modules in Central Europe.

- January 2026: Stora Enso released Performa Lumi lightweight board, leveraging FiberLight Tec to cut basis weight by up to one-third.

Germany Folding Carton Market Report Scope

The Germany folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into carton for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The Germany Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Germany folding carton market size and its projected growth?

The Germany folding carton market size stands at USD 2.96 billion in 2026 and is forecast to reach USD 4.00 billion by 2031, advancing at a 6.22% CAGR.

Which material type is growing fastest in German folding carton?

Coated Unbleached Kraft is the fastest rising material, expected to expand at a 7.18% CAGR through 2031 on the back of natural-brown aesthetics and lower bleaching costs.

Why are German converters investing in digital printing for carton?

Digital presses enable profitable runs below 5,000 units, meeting demand for pharmaceutical serialization, personalized e-commerce packaging, and limited-edition cosmetics without the plate costs of offset.

How will the 2026 PFAS ban affect folding carton demand?

The ban forces a shift to PFAS-free coatings, eliminating a key advantage of fluorinated flexible films and steering food-service and quick-service-restaurant brands toward compliant fiber-based carton.

Which end-user segment shows the highest growth outlook?

E-commerce and Retail-ready Packaging is forecast to grow at 7.76% through 2031, driven by urban last-mile logistics density and retailer mandates for shelf-ready formats.

What degree of market concentration characterizes folding carton in Germany?

The market scores a 6 on a 1-10 scale, with the top five groups controlling around 62-65% of revenue, signifying moderate concentration and ongoing room for mid-tier digital-first challengers.

Page last updated on: