Europe Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

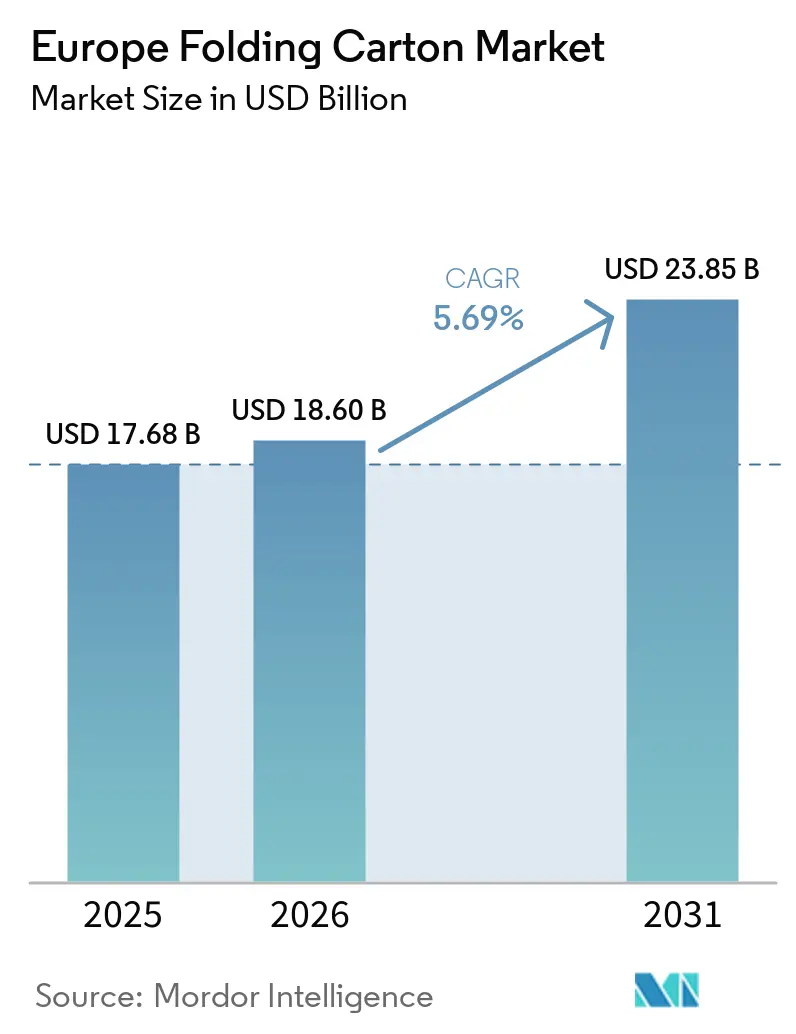

| Base Year Market Size (2025) | USD 17.68 Billion |

| Market Size (2026) | USD 18.60 Billion |

| Market Size (2031) | USD 23.85 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

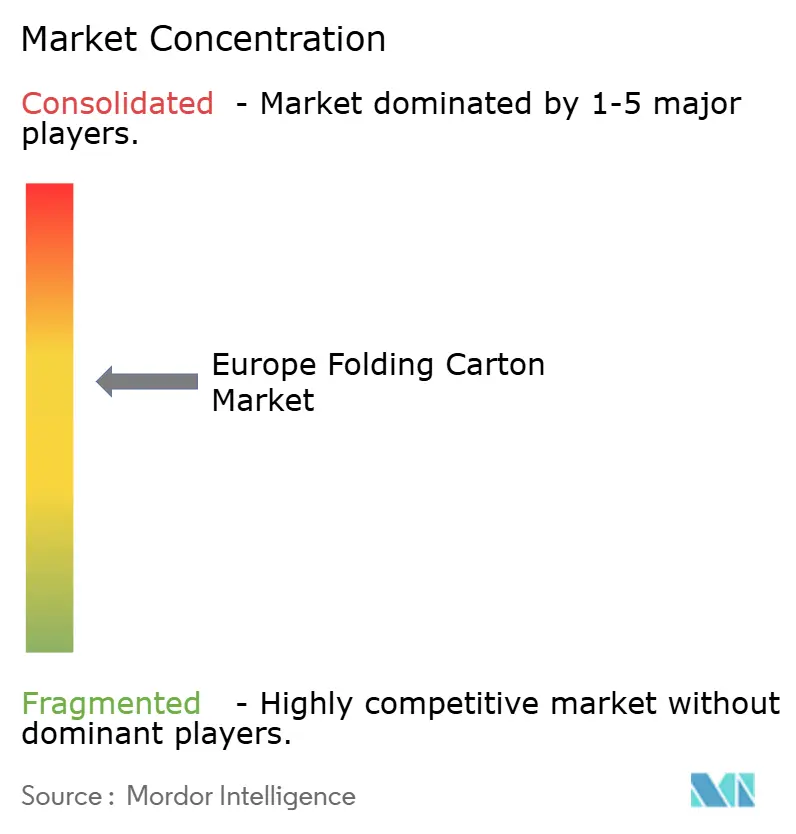

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Folding Carton Market Analysis by Mordor Intelligence

The Europe folding cartons market size is expected to be USD 17.68 billion in 2025, USD 18.60 billion in 2026, and reach USD 23.85 billion by 2031, growing at a CAGR of 5.69% from 2026 to 2031. Demand is rising as consumer-goods brands accelerate recyclable-packaging commitments, e-commerce retailers standardize shelf-ready formats, and converters upgrade printing assets to meet pharmaceutical serialization rules. Heightened Extended Producer Responsibility (EPR) fees are pushing producers toward lightweight, mono-material designs that lower fee modulation, while water-based barrier coatings are opening new high-barrier applications once dominated by plastic laminates. At the same time, pulp-price swings and regional energy-cost gaps are intensifying cost-control efforts, spurring investments in AI-enabled color management and servo-driven converting lines that cut waste and power consumption.

Key Report Takeaways

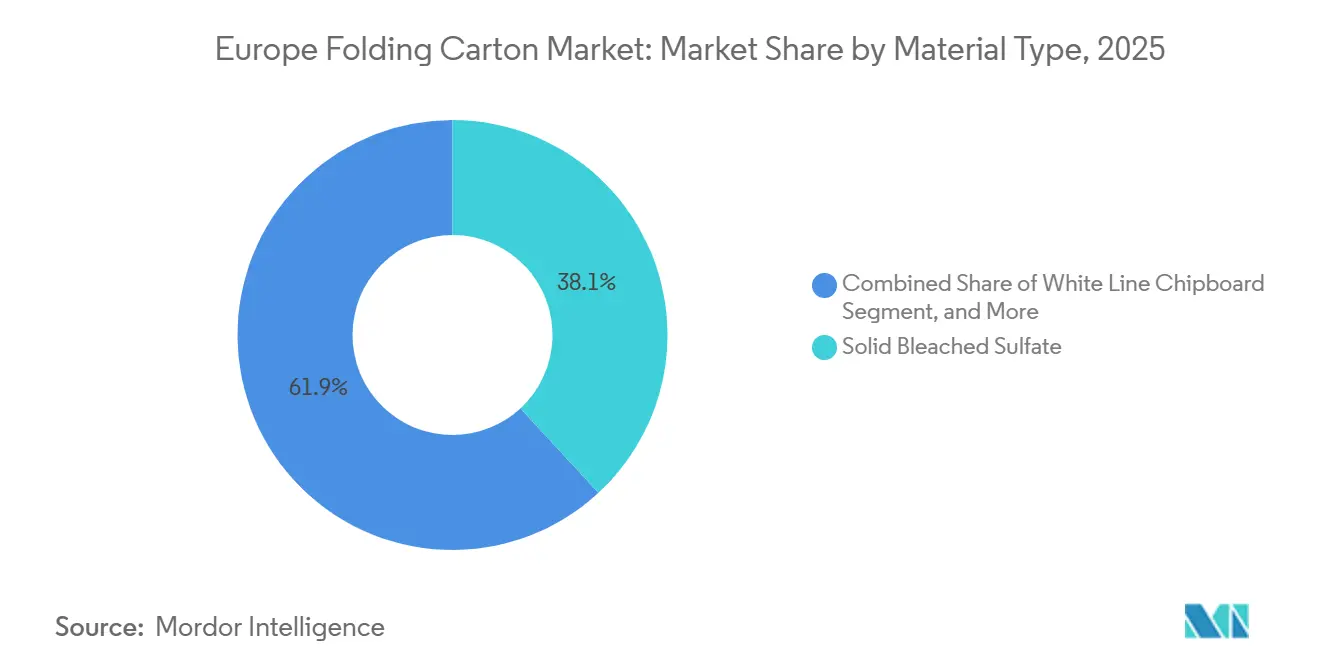

- By material type, folding boxboard captured 38.12% of the Europe folding cartons market share in 2025.

- By printing technology, the Europe folding cartons market size for the digital printing segment is forecast to advance at a 7.68% CAGR through 2031.

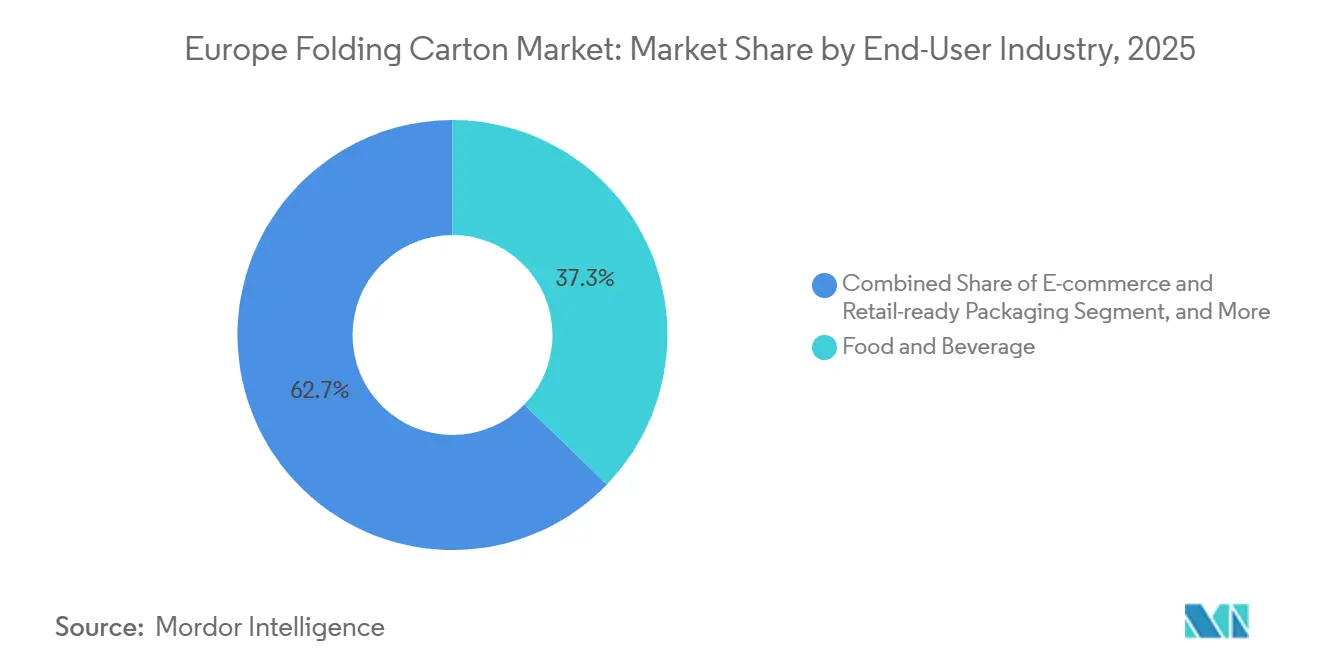

- By end-user industry, food and beverage captured 37.25% of the Europe folding cartons market share in 2025.

- By geography, the Europe folding cartons market size for Spain is forecast to advance at a 6.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Shift Toward Recyclable Packaging Among EU FMCG Brands | +1.80% | Europe-wide, early adoption in Germany, France, Netherlands | Medium term (2-4 years) |

| Mandatory Extended Producer Responsibility Fees Increasing Cost Pressure | +1.20% | Europe-wide, highest fees in France, Netherlands, Belgium | Short term (≤ 2 years) |

| E-commerce Boom Driving Demand for Lightweight Protective Cartons | +1.50% | Western Europe and Iberia, spill-over to Poland, Czech Republic | Medium term (2-4 years) |

| Adoption of High-Barrier Coatings Replacing Plastic Lamination | +1.10% | Germany, France, Italy, Poland | Medium term (2-4 years) |

| Retailer Demand for Shelf-Ready Packaging Optimizing Logistics | +0.70% | UK, Germany, France, Spain | Short term (≤ 2 years) |

| AI-Enabled Color Management Systems Reducing Print Waste | +0.40% | Germany, Netherlands, Italy, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift Toward Recyclable Packaging Among EU FMCG Brands

Major food and personal-care companies are moving faster than regulation to secure fiber supply and cost relief. Groupe Bel committed in 2025 to migrate all cheese-portion packs to folding cartons by 2027, removing 4,200 tonnes of plastic annually. Ferrero met its 2025 goal of sourcing only FSC-certified paperboard, while Mondelez switched to low-migration inks that stay recyclable in standard mills. Early adopters access certified fiber at baseline pricing, whereas late movers could face a 15-25% premium after 2028. National agencies oversee recyclability verification against Joint Research Centre protocols, giving first movers compliance certainty and smoother market access.[1]European Commission, “Proposal for a Regulation on Packaging and Packaging Waste,” europa.eu

E-commerce Boom Driving Demand for Lightweight Protective Cartons

Online retail reached EUR 899 billion (USD 1.01 trillion) in 2025 and is reshaping the design of structures. Cartons between 250-350 gsm now dominate automated fulfillment centers because they reduce shipping weight by 12-18% while resisting crush during last-mile handling. DS Smith upgraded its Grenaa, Denmark, plant in March 2026 with a servo-driven rotary die-cutter that adds 15 million m² of annual capacity, targeting robotics-compatible die-cuts for fashion and electronics shippers. Amazon and Zalando will require frustration-free, glue-free formats by 2027, accelerating uptake of self-locking structures that cut line changeovers and tape usage.[2]Pulp & Paper News, “DS Smith Invests DKK 100 Million in Grenaa,” pulpapernews.com

Mandatory Extended Producer Responsibility Fees Increasing Cost Pressure

France’s CITEO charged EUR 50–80 per tonne (USD 56.43-90.26 per tonne) in 2025 for non-optimized cartons, whereas fully recyclable, lightweight designs earned up to 30% rebates. The Netherlands added EUR 120–150 per tonne (USD 135.44-169.30 per tonne) penalties for plastic windows or metallic inks, prompting converters to adopt wash-off adhesives and pure-fiber barriers. A converter producing 15,000 tons annually can incur EUR 0.6-1.5 million (USD 0.68-1.69 million) in fees, equaling 3-5% of revenue, which pushes redesign toward mono-material boards. Industry associations continue to urge harmonization, but national discretion persists, reinforcing the premium on compliant design expertise.[3]CITEO, “Barème F: Modulated EPR Fees 2025,” citeo.com

Adoption of High-Barrier Coatings Replacing Plastic Lamination

PFAS bans are effective in 2028, and recycled-content mandates have driven dispersion coatings that match plastic performance while remaining pulper-friendly. Mondi’s FunctionalBarrier Paper Ultimate launched in August 2025 with oxygen transmission under 0.5 cubic centimeters per square meter per day. while Stora Enso’s PerformaBARRIER provides grease resistance for frozen foods without foil. Sappi’s Fusion TopScreen cleared CEPI recyclability tests in 2025, opening pharmaceutical and cosmetics uses. Although coatings add EUR 80-150 per tonne (USD 90.26-169.30 per tonne) in material costs, they qualify for EPR rebates that tip net economics in favor of fiber.[4]Mondi, “FunctionalBarrier Paper Ultimate Press Release,” mondigroup.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Hardwood Pulp Prices Compressing Converter Margins | -0.90% | Europe-wide, acute impact in Southern and Eastern Europe | Short term (≤ 2 years) |

| Rising Energy Costs Undermining Small Converters' Profitability | -0.70% | Central and Eastern Europe, UK | Medium term (2-4 years) |

| Plastic Lobby Campaigns Delaying Certain Legislative Bans | -0.30% | Poland, Hungary, Italy | Medium term (2-4 years) |

| Limited Recovery Infrastructure for Multimaterial Cartons | -0.50% | Southern and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Hardwood Pulp Prices Compressing Converter Margins

NBSK pulp bounced between USD 950-1,180 per tonne in 2024-2025, while BEK ranged USD 720-920 per tonne, squeezing converters that operate on 8-12% EBITDA margins. Mayr-Melnhof noted that pulp inflation drove 60% of its COGS hike in 2025, with the pass-through delayed by 3 to 6 months. Smaller converters locked into annual price contracts struggle to recover costs and often accept margin erosion of 200-300 bps. Recycled grades offer only limited relief, as pharmaceutical and cosmetic cartons still require virgin-fiber SBS for migration-safety reasons.

Rising Energy Costs Undermining Small Converters' Profitability

Gas averaged EUR 35-50 per megawatt-hour (USD 39.48-56.43 per megawatt-hour) in 2025, still double pre-2020 norms, while electricity in Poland and Hungary sits 40-60% above France. Folding-carton plants use 400-600 kWh per tonne, so a 20,000 t operation pays EUR 280,000-600,000 (USD 315,91,840-676,95,600) more per year than in 2019. DS Smith’s servo presses recapture braking energy for up to 21% savings, and Germany converters lock in renewable PPAs that cap power at EUR 80-100 per megawatt-hour (USD 90.26-112.83 per megawatt-hour). By contrast, the Czech Republic and Poland independents pay EUR 120-160 per megawatt-hour (USD 135.44-180.58 per megawatt-hour), hastening consolidation into integrated groups with stronger procurement leverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Grades Capture Growth in Pharma and Cosmetics

Solid Bleached Sulfate is projected to outgrow the European folding cartons market average at 6.69% CAGR, reflecting stringent migration limits for medicinal and luxury-cosmetic packs. The European folding cartons market for SBS benefits from Sappi Fusion TopScreen and Stora Enso PerformaBARRIER, both of which cleared CEPI’s recyclability protocol in 2025, enabling barrier performance without plastic film. Folding Boxboard maintains the largest base, with 38.12% of the Europe folding cartons market share in 2025, favored for dry grocery and tobacco applications where moderate stiffness suffices.

Coated Unbleached Kraft expands in organic food lines that leverage its natural brown aesthetic, while White Line Chipboard competes in price-sensitive hardware and household goods. Mondi’s 2025 buyout of Schumacher Packaging deepened its SBS portfolio and added six-color digital capability with white ink on brown substrates, letting cosmetics brands run short, seasonal promotions without litho plate costs. Virgin-fiber dominance persists in pharmaceutical serializations regulated under EU Directive 2011/62/EU, because print uniformity and emboss depth remain critical for anti-tamper integrity.

By Printing Technology: Digital Accelerates for Serialization and SKU Proliferation

Flexographic presses still held 44.61% of the Europe folding cartons market share in 2025 due to high-volume food contracts exceeding 50,000 units. Yet Digital Printing is forecast to grow at a 7.68% CAGR, addressing serialized pharmaceuticals and e-commerce personalization. HP Indigo and Xerox Iridesse platforms enable on-press variable data, embedding QR codes and random alphanumerics that comply with the Falsified Medicines Directive without secondary labeling delays.

Lithography remains entrenched in luxury segments where halftone richness justifies longer changeovers, whereas Gravure declines alongside tobacco plain-pack rules. AI color-management suites from Esko and ColorLoop cut makeready waste by 10-15% and shorten job cycles, giving converters a cost-effective path to shorter runs. Combined with inline die-cutting and foil units, converters can now pivot between flexo and digital in a single shift, a capability that underpins the agility demands of the European folding cartons market.

By End-User Industry: E-Commerce Shapes Shelf-Ready Evolution

Food and Beverage led the European folding cartons market in 2025 at 37.25% of the market, supported by dairy multipacks and frozen entrées that rely on moisture-resistant boards. E-commerce and Retail-ready Packaging is growing 6.17% CAGR, fueled by grocery-delivery expansion and supermarket restocking efficiency mandates. Shelf-ready designs that transition from transit to display in seconds reduce in-store labor 30-40%, a critical gain as retailers battle rising wage costs.

Healthcare and Pharmaceuticals remain a premium niche with high value per tonne, using SBS cartons with leaflet pockets and child-resistant closures that comply with ISO 15378. Personal Care and Cosmetics demand soft-touch coatings and metallic embellishments costing EUR 0.15-0.40 each (USD 0.17-0.45 each), premiums brands readily absorb for differentiation. Electronics accessories migrate to anti-static-coated cartons that withstand parcel networks, while household goods and tobacco shrink or stagnate due to plastic-to-fiber shifts and plain-pack legislation.

Geography Analysis

Germany accounted for 23.41% of Europe's folding carton market revenue in 2025, driven by pharmaceutical exports, automotive aftermarket parts, and a dense FMCG base. Fee rebates under the Zentrale Stelle Verpackungsregister reward converters that cut plastic windows and metallic inks, encouraging rapid adoption of pure-fiber barriers. The country’s well-developed optical-sorting network supports up to 85% carton recovery, reducing EPR liabilities.

Spain is the fastest riser, with a 6.41% CAGR forecast to 2031. Smurfit Kappa’s EUR 12 million (USD 13.6 million) 2025 capacity increase and nearshore North African supply chains bolster Iberian demand. Catalonia and Madrid e-commerce hubs need crush-resistant, lightweight cartons for apparel and fresh produce, and state renewable-energy incentives lower per-unit power costs for converters.

France remains Europe’s second-largest folding-carton consumer, shaped by CITEO’s modulated EPR charges that penalize non-recyclable coatings. Italy’s luxury-cosmetics and fashion sectors sustain SBS demand, while the United Kingdom’s 2024 Plastic Packaging Tax exempts fiber cartons, giving them a 15-20% price advantage over clamshells. Poland and the Czech Republic attract investment for low labor and energy costs, whereas the Netherlands and Belgium lead the continent in circular-economy infrastructure, featuring advanced de-inking systems that enable 65% recycled-content targets by 2030.

Competitive Landscape

The top five suppliers-Stora Enso, Smurfit Kappa, DS Smith, Mayr-Melnhof, and Mondi-held roughly 40-45% of Europe folding cartons market revenue in 2025, signaling moderate concentration. Vertical integration is pivotal: Stora Enso and Mondi own upstream pulp mills, hedging pulp volatility, while AR Packaging and Huhtamäki buy spot pulp, leaving them exposed to margin risk. Capacity expansion in Poland, Spain, and the Czech Republic exploits lower utility rates, and strategic M&A, such as International Paper’s 2025 takeover of DS Smith, underscores the tilt toward region-specific fiber platforms that align with Packaging and Packaging Waste Regulation timetables.

Digital-native platforms like Packhelp serve direct-to-consumer startups with online artwork upload, instant quoting, and minimum orders of 100 units, nibbling share from legacy converters that prioritize five-figure runs. Technology upgrades permeate the European folding cartons industry, with servo-driven die-cutters and AI color-control cutting that reduce waste by up to 15%, a vital offset as EPR fees rise. Certification barriers under ISO 15378 (pharma) and ISO 22000 (food) sustain competitive moats for incumbents that maintain multi-site audit histories.

White-space avenues include turnkey pharmaceutical serialization, where converters manage data aggregation alongside printing, and co-development of automation-ready e-commerce packs that dovetail with robotic pickers. AI-enabled design tools that simulate crush strength and folding behavior reduce prototyping cycles, hastening time-to-market for brand promotions and limited editions across the European folding cartons market.

Europe Folding Carton Industry Leaders

Stora Enso Oyj

Smurfit Westrock plc

Mayr-Melnhof Karton AG

Graphic Packaging Holding Company

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mondi showcased recyclable paper solutions with 15 OEM partners during Interpack 2026, demonstrating kraft-paper shrink-wrap alternatives on Hugo Beck machinery to help converters integrate fiber into existing high-speed lines.

- April 2026: Amcor, Metsä Group, and G. Mondini launched an all-in-one molded-fiber tray system with advanced barrier liners for protein and chilled meals, allowing microwave and oven use while cutting plastic.

- March 2026: Huhtamäki released its 2025 Annual Report, declaring EUR 4.0 billion (USD 4.5 billion) net sales and limited-assurance ESRS sustainability disclosure verified by KPMG.

- November 2025: Mondi broadened its solid-board food portfolio after acquiring Schumacher Packaging, adding six-color digital printing with white ink for seasonal food and beverage campaigns.

Europe Folding Carton Market Report Scope

The Europe folding cartons market refers to the production and commercialization of paperboard-based packaging solutions that are folded into cartons for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The Europe Folding Cartons Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected Europe folding cartons market size by 2031?

The Europe folding cartons market size is forecast to reach USD 23.85 billion by 2031, expanding at a 5.69% CAGR over 2026-2031.

Which material grade is expected to grow fastest in European folding cartons?

Solid Bleached Sulfate is projected to grow at a 6.69% CAGR through 2031, driven by pharmaceutical and cosmetics demand.

How are EPR fees influencing folding-carton design choices?

Modulated EPR schemes reward mono-material, recyclable cartons and penalize plastic windows or metallic inks, prompting converters to adopt pure-fiber barriers and wash-off adhesives.

Why is digital printing gaining traction in the Europe folding cartons industry?

Digital presses enable variable-data serialization and short runs for SKU proliferation, aligning with EU Falsified Medicines Directive and e-commerce personalization needs.

Which European country offers the highest growth outlook for folding cartons?

Spain is expected to post the quickest growth, at a 6.41% CAGR to 2031, due to nearshored supply chains and expanding e-commerce capacity.

What technological upgrades are converters adopting to cut production costs?

Servo-driven die-cutters, AI-powered color-management systems, and inline digital finishing are reducing energy use and print waste, sustaining margins amid rising pulp and power costs.

Page last updated on: