Russia Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.02 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 2.17% CAGR |

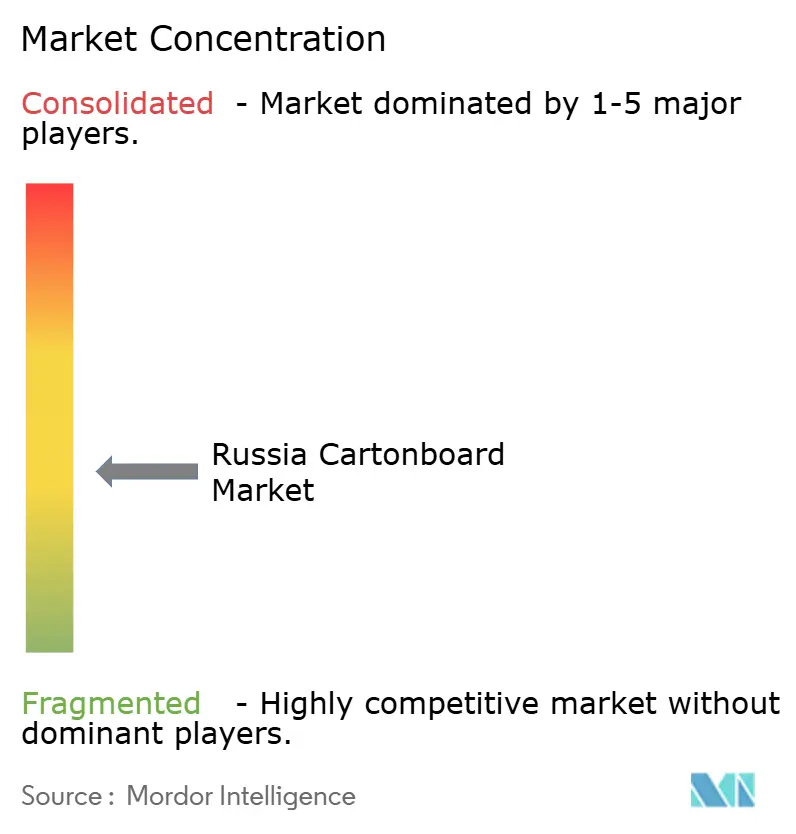

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Cartonboard Market Analysis by Mordor Intelligence

The Russia cartonboard market size is expected to increase from USD 1.02 billion in 2025 to USD 1.06 billion in 2026 and reach USD 1.18 billion by 2031, growing at a CAGR of 2.17% over 2026-2031. Domestic consumption held steady as organized food retail continued to expand and policy support favored locally produced board grades over former imports. Russia's food packaging revenue reached RUB 1.7 trillion (USD 18.5 billion) in 2025, with paper and cardboard accounting for 36% of total packaging revenue, thereby maintaining a broad demand base. The Russia cartonboard market is also being reshaped by capacity additions from local producers, following supply disruptions that forced changes in raw material sourcing between 2022 and 2024. Financing conditions remain tight, so growth is moderate rather than rapid, yet self-sufficiency is improving in coated and specialty grades where import dependence had been high. Demand opportunities are strongest where regulation, localization, and converting upgrades now overlap, especially in food packaging, aseptic formats, and regulated pharmaceutical packs.

Key Report Takeaways

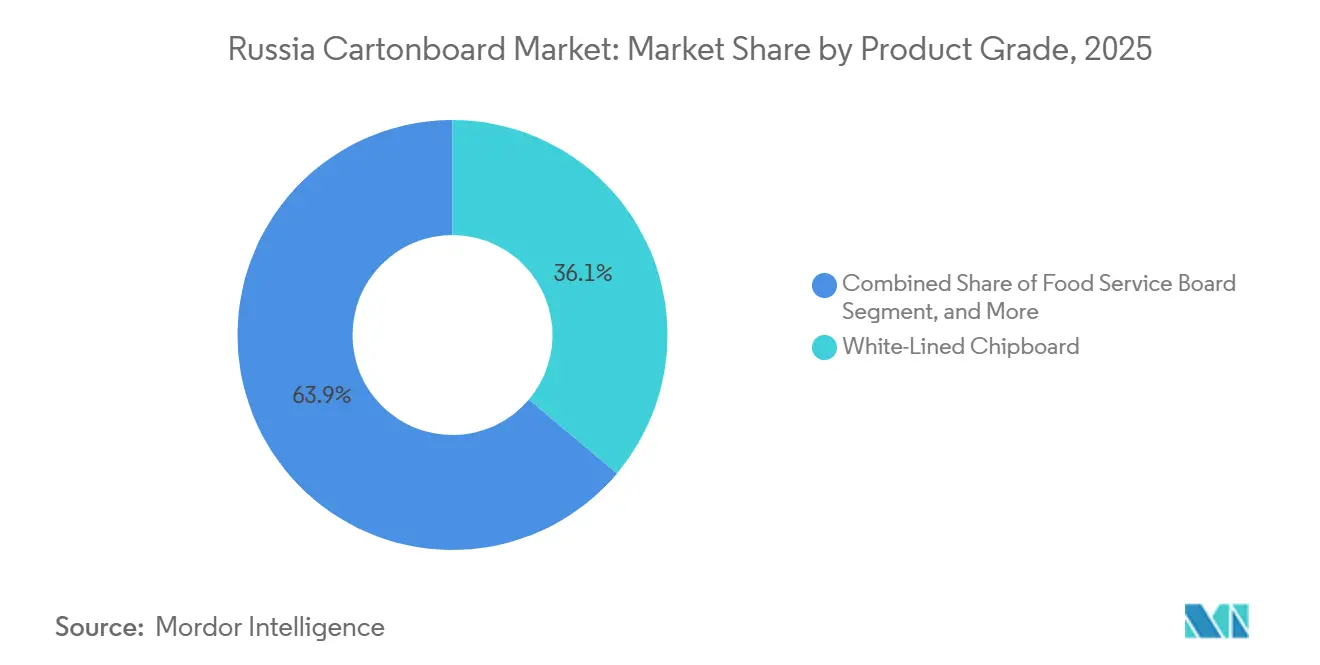

- By product grade, White-Lined Chipboard captured 36.14% of the Russia cartonboard market share in 2025.

- By packaging format, the Russia cartonboard market size for the liquid packaging segment is forecast to advance at a 2.71% CAGR through 2031.

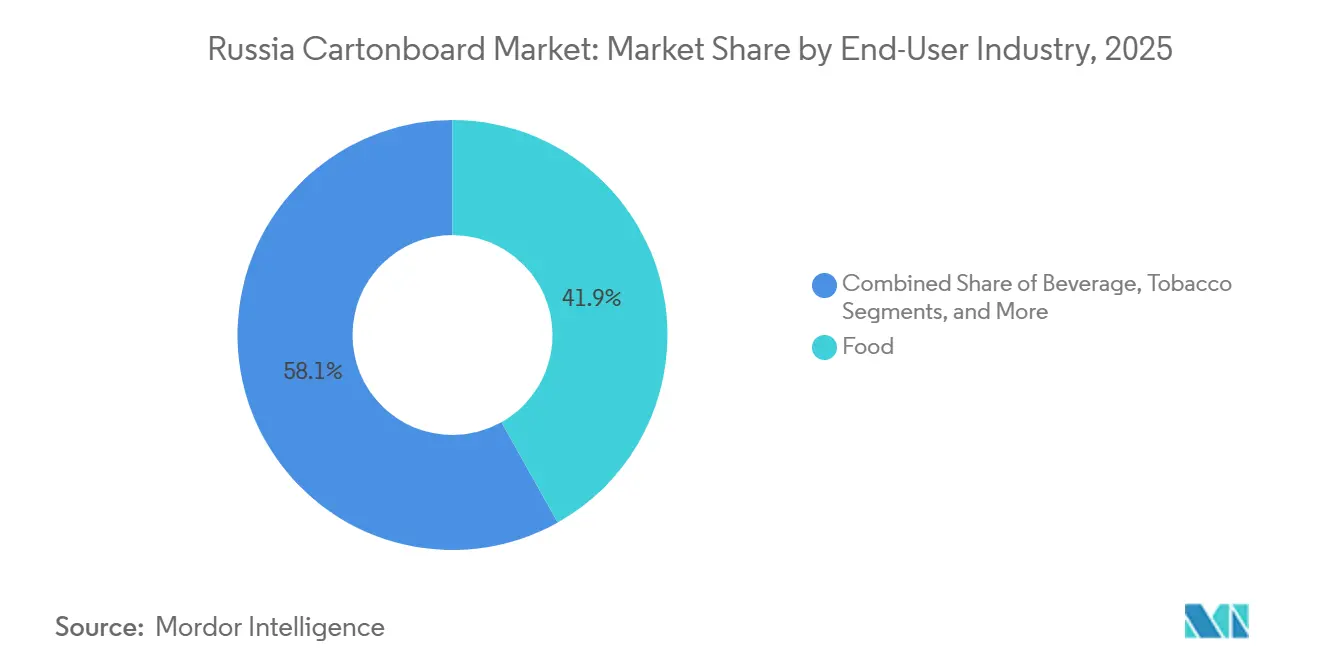

- By end-user industry, food captured 41.86% of the Russia cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food And Beverage Packaging Demand Resilience | +0.65% | National, concentrated in Central Federal District, Volga Federal District, and Southern Federal District food processing hubs | Medium term (2-4 years) |

| Import Substitution In Folding Boxboard And Liquid Cartons | +0.55% | National, with early capacity gains in Perm Krai, Arkhangelsk Oblast, and Moscow Oblast | Long term (≥ 4 years) |

| EPR And Eco-Fee Pressure Supporting Fiber Formats | +0.40% | National, enforced by the Ministry of Natural Resources and Environment and Rospotrebnadzor | Medium term (2-4 years) |

| Pharmaceutical Serialization And Localization | +0.30% | National, with early gains in Moscow, Leningrad, Kaluga, and Yaroslavl pharmaceutical clusters | Medium term (2-4 years) |

| Cupstock And Aseptic Carton Localization | +0.20% | National, concentrated in dairy and juice processing regions across Central Russia and Volga | Long term (≥ 4 years) |

| High-Graphics Digital Conversion For Premium Packs | +0.10% | National, highest intensity in Moscow and St. Petersburg premium consumer goods segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Food And Beverage Packaging Demand Resilience

Russia's food and beverage sector remains the clearest demand anchor for the Russia cartonboard market. Cartonboard demand remained resilient in packaged food as retailers continued to expand shelf-ready and branded secondary packs in modern trade channels. X5 Group and Magnit set internal targets to increase the use of recyclable or compostable packaging materials in private-label ranges to 50-100% during 2025 and 2026, favoring cartonboard over plastic wraps for shelf-ready units.[1]RosUpack Team, “Analysis of the Cardboard and Corrugated Packaging Market in Russia, 2024-2025 and Key Trends,” RosUpack, rosupack.com Smaller households and stronger demand for convenience foods increase the number of packs needed even when underlying food output is not rising quickly. That pattern gives converters in the Russia cartonboard market a steadier order book than suppliers tied more directly to export cycles.

Import Substitution In Folding Boxboard And Liquid Cartons

Import substitution has become the central structural force in the Russia cartonboard market. KAMA LLC, Russia's only domestic FBB producer, invested more than RUB 25 billion (USD 271.7 million) since 2016 and reached 1 million cumulative tons of output in 2026, after starting from no domestic FBB output before April 2021.[2]Editorial Team, “KAMA Produces One Million Tons of Coated Packaging Cardboard Since FBB Line Launch,” Pulp and Paper Chronicle, pulpandpaperchronicle.com The Ministry of Industry and Trade treated KAMA's expansion as a priority project and granted long-term forest lease rights covering 365,000 cubic meters of annual timber, which lowered input uncertainty for the mill. Domestic production now spans five grammage bands from 170 to 380 g/m², which weakens the former quality case for imports. Liquid carton localization is moving more slowly because aseptic barrier technologies still depend partly on imported inputs, but Russian converters are internalizing more production steps than before.

EPR And Eco-Fee Pressure Supporting Fiber Formats

Russia's EPR reform shifted compliance pressure directly onto packaging suppliers, favoring fiber formats in the Russia cartonboard market. From January 2025, recycling responsibility moved from millions of product manufacturers and importers to a much smaller group of packaging producers and importers, which concentrated the cost burden at the packaging stage. The law set packaging recycling obligations at 55% in 2025, 75% in 2026, and 100% from January 2027, which strengthened the commercial case for recyclable paper and board structures.[3]UCEC Quality LLC, “Russia's 2026 Pharma Localization Points System,” UCEC Quality LLC, certru.ru This framework makes hard-to-recycle non-fiber formats less attractive and supports mono-material fiber designs for food, pharmaceutical, and consumer goods packs. The effect is broader than compliance alone, as packaging design decisions now increasingly reflect future fee exposure and reporting obligations across the supply chain.

Pharmaceutical Serialization And Localization

Pharmaceutical demand is becoming a specialized growth pocket within the Russia cartonboard market. Chestny Znak requires each pharmaceutical product to carry a unique 2D Data Matrix code on secondary cartonboard packaging, which makes the carton a functional part of the compliance system. The localization points system under Government Decree No. 719 gives domestic drug makers a procurement advantage when they accumulate qualifying production steps, and locally sourced secondary packaging can contribute to that process. In early 2026, JSC PROMIS said pharmaceutical clients were asking packaging suppliers to support board testing, pack design adaptation, and digital services rather than simple box supply.[4]Editorial Team, “Pharmaceutical Packaging - 2026: Automation, Patient-Centricity, Complex Design, and New Market Requirements,” PharmMedProm, pharmmedprom.ru The 2025 tracking experiment for pharmaceutical substances involved 68 registered companies, suggesting that traceability rules will continue to extend deeper into the packaging chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Virgin Pulp And Financing Cost Volatility | -0.50% | National, with the greatest exposure in mills in Northwest Russia, including Arkhangelsk and Leningrad, that source imported high-grade pulp | Short term (≤ 2 years) |

| Competition From Flexible Packaging | -0.35% | National, most acute in food and personal care segments in Moscow, St. Petersburg, and major retail corridors | Medium term (2-4 years) |

| Barrier-Coating And Lamination Bottlenecks | -0.20% | National, with early impact in liquid packaging and food service board conversion clusters | Long term (≥ 4 years) |

| Skilled Labor And Spare-Parts Constraints | -0.10% | National, concentrated in regions dependent on legacy machinery from European equipment suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Virgin Pulp And Financing Cost Volatility

Cost instability remains the most immediate constraint on profitability in the Russia cartonboard market. In 2025, the Russian pulp and paper sector generated RUB 1.71 trillion in turnover (USD 18.6 billion), yet some companies used 25-30% of profits to service debt, which limited reinvestment capacity. Domestic producers still depend on imported high-grade bleached pulp for premium SBB and FBB grades, so local timber access does not eliminate exposure to world pulp pricing. High interest rates also slow capital spending on board machine upgrades and import-substitution projects. Mills with underused capacity face extra margin pressure because unfavorable export logistics can keep revenue per ton weak.

Competition From Flexible Packaging

Flexible packaging remains the closest substitute in the product categories where cartonboard is most exposed. It is especially competitive in confectionery, snacks, dairy sachets, and personal care formats where low material weight and barrier performance matter most. Some domestic flexible packaging producers now offer barrier-coated mono-material structures that meet recyclability testing requirements, which has weakened the earlier regulatory edge that cartonboard held by default. That leaves cartonboard with a stronger position in packs that need rigidity, strong print surfaces, stacking strength, or child-resistant secondary functions. Converters that have not invested in specialty coatings or value-added finishing remain most exposed to substitution in lower-margin categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: White-Lined Chipboard Anchors Volume, Food Service Board Signals Margin Upside

White-Lined Chipboard held 36.14% of the Russia cartonboard market share in 2025, making it the leading product grade. Its recycled-fiber base and lower cost fit secondary packaging needs in food, FMCG, and household goods, which explains why it remained the volume anchor of the Russia cartonboard market. WLC also aligns well with the shift toward recyclable packaging under EPR rules, so both price and compliance considerations support its value case. Folding Boxboard and Solid Bleached Board serve higher-value uses in pharmaceutical and premium consumer packaging, but their scale stayed more limited because Russia relied heavily on imports for these grades for many years. KAMA's domestic FBB capacity reached 240,000 tons per year by 2025 and is expected to reach 270,000 tons per year by 2027, gradually reducing that dependence.

Solid Unbleached Board and Liquid Packaging Board occupied the middle of the grade mix, with demand for LPB linked closely to dairy and juice packaging needs. Russia packaged 12.8 million tons of dairy products annually as of 2024, and 31% of that volume required multilayer cardboard packaging, which kept a firm base under liquid board demand. The Food Service Board market is projected to grow at a 2.96% CAGR from 2026 to 2031 as quick-service restaurants and food delivery formats increase demand for heat-stable, grease-resistant boards. The Russia cartonboard industry is also shifting product development toward packaging and foodservice uses, indicating where suppliers see better margins than in legacy graphic paper applications.

By Packaging Format: Folding Cartons Dominate, Liquid Packaging Accelerates

Folding cartons accounted for 59.35% of the Russia cartonboard market size in 2025, making them the dominant packaging format. Their lead reflects broad use across pharmaceutical boxes, confectionery packs, cosmetics cartons, and shelf-ready food packaging. This breadth also gives the Russia cartonboard market a strong base in applications that value rigidity, print quality, and retail presentation. Harmens Group operates 4 printing plants across 3 federal districts, with a combined annual cartonboard processing capacity of 44,000 tons, and supplies 46 market segments, demonstrating how widely this format travels across end markets. Sleeve and tray formats remained specialized, serving selected secondary packaging needs for retail and e-commerce.

Liquid packaging is projected to grow at the fastest pace, with a 2.71% CAGR from 2026 to 2031, as domestic dairy and juice producers expand local converting lines. The exit of major foreign suppliers after 2022 created a supply gap that Russian companies such as PJSC Lambumiz are now trying to fill. Multilayer cartonboard accounted for 31% of dairy packaging volume in 2024, underscoring its importance in liquid food packaging. Food-contact certifications such as FSSC 22000 and ISO 9001 are becoming more important procurement filters for large buyers in this part of the Russia cartonboard market.

By End-User Industry: Food Dominates, Pharmaceutical And Healthcare Leads Growth

Food held 41.86% of the Russia cartonboard market in 2025, making it the largest end-user industry. That position rests on the scale of Russia's food processing base and on organized retail demand for shelf-ready and consumer-facing packs. Private-label expansion by large retailers also favors recyclable fiber packaging because it helps manage future compliance and waste-handling costs. Beverage, tobacco, pharmaceutical and healthcare, and cosmetics and toiletries made up the rest of the demand, each with different exposure to regulation and local sourcing. Cosmetics and toiletries packaging have benefited from relocalized supply chains after 2022, as domestic brands and contract manufacturers shifted away from imported folding carton networks.

The pharmaceutical and healthcare sector is projected to grow fastest at a 3.03% CAGR from 2026 to 2031, making it one of the clearest premium niches in the Russia cartonboard market. In 2026, drug makers increasingly asked suppliers to prove stable board geometry, thickness control, and forming behavior for automated packing lines. That requirement favors converters with certified pharmaceutical production and digital service capability, which raises entry barriers in a segment that already depends on compliance precision. The Russia cartonboard industry is therefore seeing pharmaceutical packaging move away from commodity conversion and toward process-controlled, technology-led supply.

Geography Analysis

The Russia cartonboard market was most concentrated in the Central and Volga federal districts, where the country's largest food processing, pharmaceutical, and FMCG clusters are located. Moscow Oblast and nearby regions served as the main conversion hub because they sit close to dense retail distribution networks and major consumer demand centers. JSC GOTEK-Center and Harmens Dubna both operate within this broader corridor, which supports quick delivery to high-volume buyers. The Northwestern Federal District, anchored by producers in Arkhangelsk and Leningrad oblasts, remained Russia's main heartland of pulp and board production. Output in this region has been shifting away from printing and writing paper and toward packaging board, indicating that domestic mills now see more durable demand.

The Siberian and Ural federal districts added resilience to the Russian cartonboard market by reducing transport penalties on long inland routes through regional conversion capacity. Harmens Berdsk near Novosibirsk is described by the company as the largest cartonboard packaging producer beyond the Urals, while converters near Ekaterinburg serve the Ural industrial base. The Perm Pulp and Paper Company also sits in the Ural-Volga corridor and supports food and pharmaceutical customers across surrounding regions. The Southern Federal District remained a smaller demand pocket, but agro-processing and beverage production in Krasnodar kept local carton demand on a growth path.

Trade flows remain a defining feature of the Russia cartonboard market because Russia exports bulk pulp but still relies on imported supply for some high-grade and barrier-coated board. After European suppliers withdrew between 2022 and 2024, converters shifted part of their sourcing toward China and the Middle East for selected coated grades. KAMA has filled the most critical domestic gap in coated virgin-fiber board, yet aseptic-specific and barrier-coated liquid packaging structures still depend partly on foreign inputs. This means import exposure will stay above zero through 2031 even as localization improves. Russian industry participants also warned in 2026 that logistics disruptions could change pulp freight economics and alter the cost balance for imported board grades over the medium term.

Competitive Landscape

The Russia cartonboard market is moderately concentrated at the board production level but remains fragmented at the converting level. KAMA LLC's role as the only domestic FBB producer gives it unusual pricing influence in a grade that matters for pharmaceutical and premium packaging. APPM JSC and Perm Pulp and Paper Company remain important anchors in virgin-fiber and recycled-fiber supply, while converters such as Harmens Group and JSC GOTEK compete across broader format portfolios. This split creates an uneven structure in which upstream control matters more for specification-sensitive grades than for standard folding carton conversion. The Russian cartonboard market, therefore, rewards companies that can secure board supply, maintain stable utilization, and serve national customers across several regions.

Vertical integration is becoming the most important strategic move in the competitive field. JSC GOTEK planned to invest more than RUB 15 billion (USD 164.8 million) in a 265,000-ton-per-year recycled cartonboard plant in Tula Oblast, which would extend its reach from conversion into board production. KAMA also continued modernizing its FBB line and pulp operations in 2025 and 2026, thereby supporting higher domestic availability of coated grades. GOTEK's earlier purchase of 3 former Mondi assets broadened its presence in corrugated and flexible packaging, thereby strengthening scale beyond pure cartonboard conversion.

Technology and certification are becoming as important as scale in the Russia cartonboard market. GOTEK invested in HP Scitex digital printing to secure specialized print runs that standard lines do not handle as efficiently. Harmens Group's FSSC 22000 and ISO 9001 certifications support its access to pharmaceutical and food-grade contracts where compliance operates as an entry barrier. The clearest open space remains in barrier-coated food service boards and recyclable liquid carton substitutes, where domestic capacity remains limited. Russian patent activity in barrier-coating applications remains modest, so that technological progress may depend more on licensing and adaptation than on domestic R&D alone.

Russia Cartonboard Industry Leaders

NPAO Svetogorsk PPM

JSC PROMIS

Harmens Group SC

OOO MoloPak

OOO GA Pack Service

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: KAMA LLC upgraded the pumping fleet of its bleached chemical and thermomechanical pulp, BCTMP No. 2, workshop, increasing productivity by 19% to 470 tons per day. Total investments in this phase exceeded RUB 20 million (USD 0.22 million), with an additional RUB 29 million (USD 0.32 million) planned for subsequent stages, maintaining KAMA's trajectory toward 270,000 tons per year of FBB capacity by 2027.

- April 2026: KAMA LLC published a five-year product development retrospective confirming that its FBB line had produced 1 million cumulative tons since April 2021, supplying 5 grammage bands from 170 to 380 g/m², with total investments in the FBB line exceeding RUB 2.5 billion (USD 27.8 million) since launch. KAMA remained Russia's only domestic FBB and LWC producer.

- February 2026: The L-Pak plant in the Kashira Special Economic Zone officially launched its first production phase, producing 240 million m² of corrugated board and packaging per year, with plans to scale to 1 billion m² annually by 2028. The plant sourced 80% of its raw material from recycled paper, aligning with Russia's EPR recycling targets.

- January 2026: Russia enacted Federal Law No. 495-FZ on December 31, 2025, extending the EPR pilot program for non-EAEU importers by 2 years to January 2028. The law, implemented via Government Decree No. 2228, set packaging recycling obligations at 75% for 2026 and 100% from January 2027, directly affecting cartonboard packaging producers and importers.

Russia Cartonboard Market Report Scope

The Russia Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Russia Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the size of the Russia cartonboard market?

The Russia cartonboard market size was USD 1.02 billion in 2025 and is forecast to reach USD 1.18 billion by 2031, growing at a 2.17% CAGR from 2026 to 2031.

Which product grade leads cartonboard demand in Russia?

White-Lined Chipboard led demand with a 36.14% share in 2025 because it fits cost-sensitive secondary packaging in food, FMCG, and household goods.

Which packaging format is most widely used in Russia cartonboard applications?

Folding cartons were the largest format with 59.35% of market value in 2025 due to their wide use in food, pharmaceuticals, cosmetics, and retail-ready packs.

Which end-user segment is growing fastest in Russia?

Pharmaceutical and healthcare is projected to grow at a 3.03% CAGR through 2031 because serialization and localization rules make cartonboard packaging part of the compliance process.

Why is import substitution important for cartonboard suppliers in Russia?

Import substitution has reduced reliance on foreign coated board grades, especially after KAMA expanded domestic FBB capacity and narrowed the quality gap with imported supply.

What are the main risks for cartonboard producers and converters in Russia?

The main risks are high financing costs, exposure to imported premium pulp, flexible packaging substitution, and slower progress in barrier-coating and aseptic conversion technologies.

Page last updated on: