United States Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

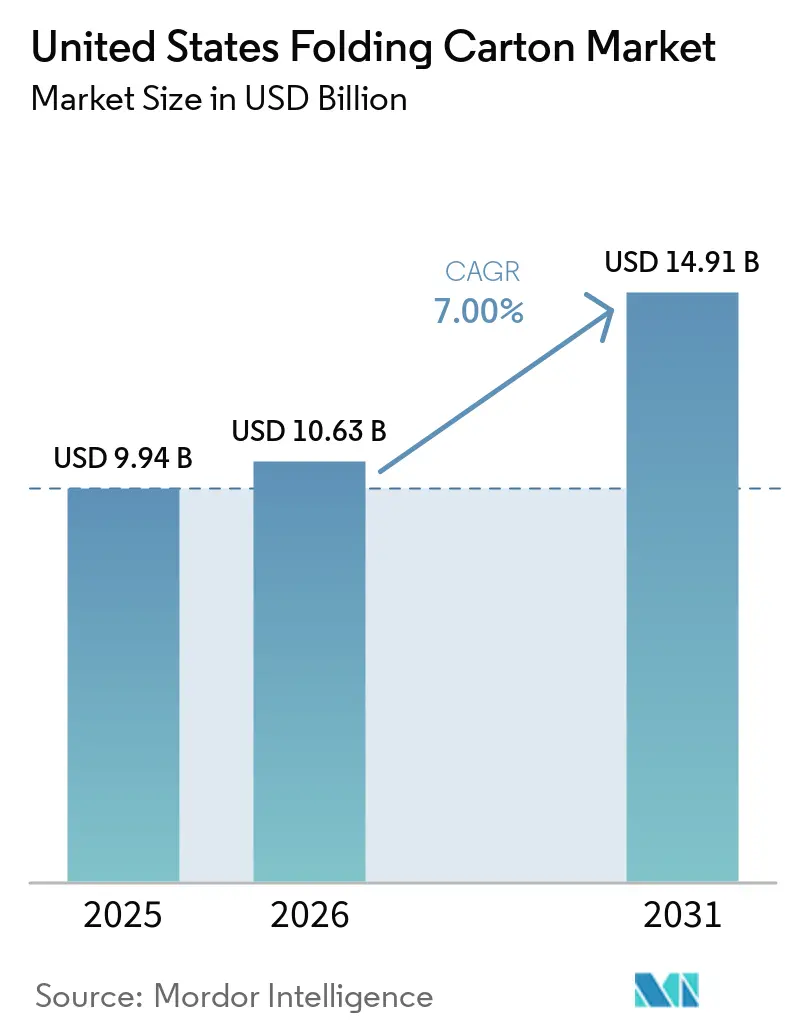

| Base Year Market Size (2025) | USD 9.94 Billion |

| Market Size (2026) | USD 10.63 Billion |

| Market Size (2031) | USD 14.91 Billion |

| Growth Rate (2026 - 2031) | 7.00% CAGR |

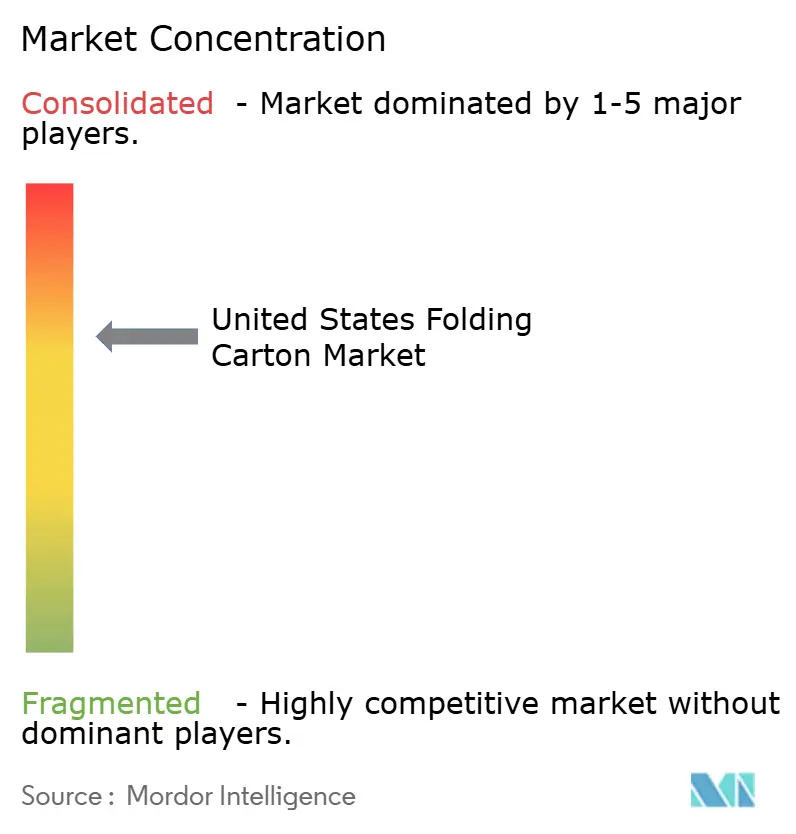

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Folding Carton Market Analysis by Mordor Intelligence

The United States folding carton market size was valued at USD 9.94 billion in 2025 and is estimated to grow from USD 10.63 billion in 2026 to reach USD 14.91 billion by 2031, at a CAGR of 7% during the forecast period (2026-2031). The rebound reflects mandatory extended producer responsibility (EPR) fees that drive carton redesign, strong replenishment of e-commerce safety stock, and the cold-chain medication boom that increases box complexity. Converters are backfilling a 4.8% shipment drop posted in 2023-2024 as food, beverage, and pharmaceutical brands shift from generic corrugated sleeves to premium printed cartons with transit-tested barriers. Material upgrades toward folding boxboard and coated unbleached kraft are accelerating because EPR fee schedules reward higher recycled content, while solid bleached sulfate retains a premium niche where print fidelity and food safety are non-negotiable. At the same time, brand owners are absorbing supply consolidation after Smurfit Westrock’s footprint optimization, which tightened availability of certain bleached grades but expanded recycled paperboard capacity in Texas.

Key Report Takeaways

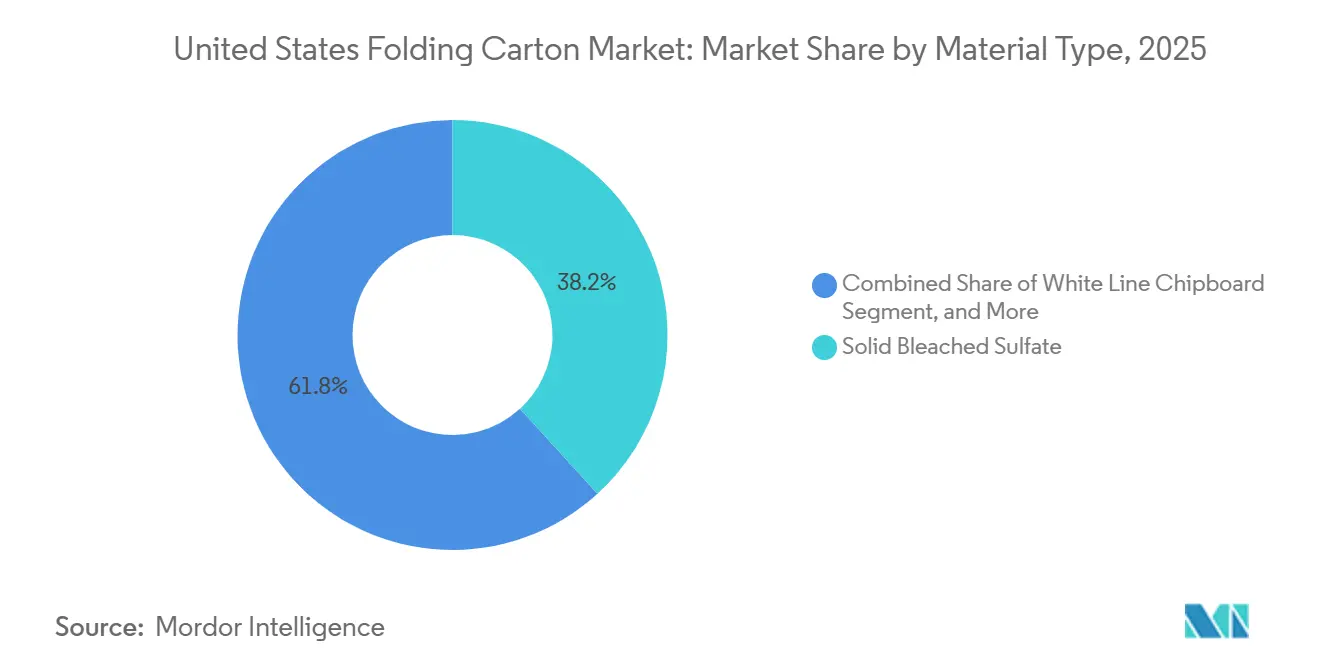

- By material type, solid bleached sulfate captured 38.21% of the United States folding carton market share in 2025.

- By printing technology, the United States folding cartons market size for the digital printing segment is forecast to advance at a 7.81% CAGR through 2031.

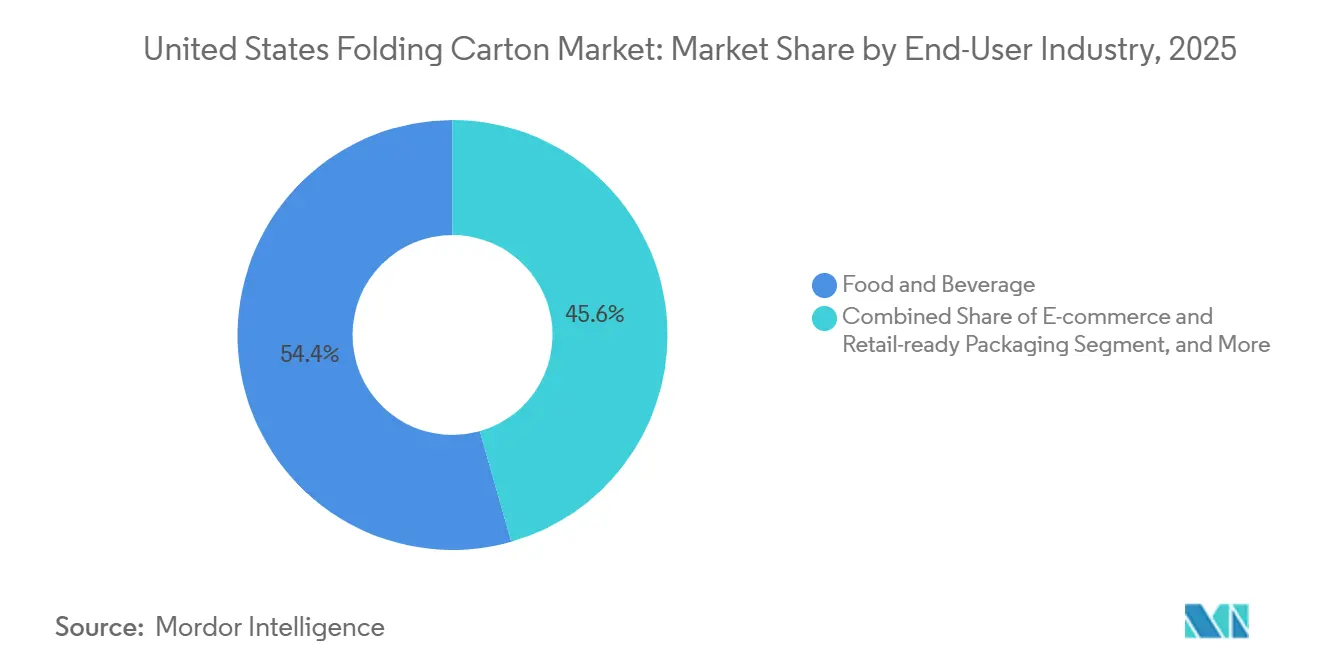

- By end-user industry, food and beverage captured 54.41% of the United States folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Boom Driving Demand for Lightweight Protective Packaging | +1.80% | National, strongest in West Coast and Northeast fulfillment hubs | Medium term (2-4 years) |

| Increasing Demand for Sustainable and Recyclable Packaging Solutions | +2.10% | National, accelerated in California, Minnesota, Washington, Oregon, Maryland, Colorado, Maine | Long term (≥4 years) |

| Premiumization in Food and Beverage Boosting High-Quality Printing | +1.30% | National, pronounced in urban premium retail channels | Medium term (2-4 years) |

| State-Level Extended Producer Responsibility Legislation Accelerating Carton Adoption | +1.50% | California, Minnesota, Washington, Oregon, Maryland, Colorado, Maine | Long term (≥4 years) |

| Rapid Growth of Meal Kit and Ready-to-Eat Delivery Services | +0.90% | National, urban concentration with suburban spillover | Short term (≤2 years) |

| Rise of Pharmaceutical Cold-Chain Shipments Requiring Specialized Folding Cartons | +0.70% | National, clusters in New Jersey, North Carolina, California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Driving Demand for Lightweight Protective Packaging

Boxes and cartons account for 40% of all e-commerce packaging formats, compelling converters to engineer right-sized structures that survive both shelf display and parcel networks.[1]Korpack, “Strategic Packaging Planning, Preparing for 2026 Industry Shifts,” korpack.com Automated systems that trim void space have cut average package weight by 43% in North America and lowered shipping damage by 24%, pushing demand toward folding cartons with ISTA-validated edges and reinforced corner scores. Digital presses now add variable QR codes that link to loyalty sites, meeting the 50% of consumers who scan codes and the retailers who plan universal 2D barcode acceptance by 2027.[2]Printpack, “2026 Packaging Trends, Navigating Change Across Shelf and Digital,” printpack.com This convergence of automation, traceability, and omnichannel aesthetics is steering the United States folding cartons market away from commodity grades toward engineered formats.

Increasing Demand for Sustainable and Recyclable Packaging Solutions

Seven states enacted EPR statutes requiring producers to finance collection and recycling, with Minnesota mandating that all packaging be recyclable, reusable, refillable, or compostable by 2032 and to fund at least 90% of system costs by 2031.[3]Minnesota Pollution Control Agency, “Extended Producer Responsibility for Packaging,” pca.state.mn.us Washington’s program phases in 90% reimbursement by 2032 and earmarks USD 5 million for reuse infrastructure starting in 2029. These laws impose eco-modulated fees that privilege recycled-fiber cartons with verifiable recovery rates, driving brand owners to swap virgin bleached board for folding boxboard containing higher post-consumer fiber. Oregon’s 2026 constitutional challenge over fee transparency has heightened producer scrutiny of cost pass-through strategies, yet the long-term trajectory still favors recyclable-coated barriers and lightweight calipers.[4]JD Supra, “Oregon’s Extended Producer Responsibility Law, A Constitutional Challenge,” jdsupra.com As a result, sustainable substrate selection is now intertwined with finance and compliance, giving recycled paperboard a lasting tailwind in the United States folding cartons market.

Premiumization in Food and Beverage Boosting High-Quality Printing

Premium alcoholic beverage launches grew 7% annually from 2022 to 2025, and the global category is forecast to reach USD 1.686 trillion by 2034, amplifying demand for cartons with tactile coatings, metallic foils, and holographic accents. Ninety-eight percent of consumer-packaged goods brands rate packaging as critical to brand equity, and 99% plan redesigns within three years, primarily to elevate sustainability claims and shelf aesthetics. Digital printing now handles short runs under 5,000 units, enabling regional language variants and personalized gift packs that bolster direct-to-consumer channels. The coupling of premium finishes with rapid SKU turnover positions high-graphic cartons as a value-adding growth pocket for the United States folding carton market.

State-Level Extended Producer Responsibility Legislation Accelerating Carton Adoption

California, Colorado, Maine, Maryland, Minnesota, Oregon, and Washington require producers to join stewardship organizations and file granular packaging data by May 31, 2026, stimulating nationwide carton redesign to avoid multi-state complexity. Eco-modulated fees penalize difficult-to-recycle multilayer laminates and reward mono-material cartons that meet the APR Design Guide. Consequently, brand owners are substituting polyethylene windows with paper-based apertures and adopting water-based barrier coatings that pass repulping tests. Converters that supply compliance documentation are winning multi-year contracts as producers lock in fee-optimized packaging portfolios. The spread of EPR mandates across populous coastal states magnifies their influence on national specifications, raising the regulatory floor for folding carton demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recovered Paper and Virgin Pulp Prices | -1.20% | National, with sharp swings in West Coast and Midwest | Short term (≤2 years) |

| Capacity Expansion of Flexible Packaging Displacing Folding Cartons | -0.90% | National, especially in snack, pet food, personal care | Medium term (2-4 years) |

| Supply Chain Disruptions from Trucker Shortages Increasing Lead Times | -0.50% | National, acute across port-inland corridors | Short term (≤2 years) |

| Labor Shortage in Skilled Press Operators Restricting Output Growth | -0.60% | Midwest and Northeast manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recovered Paper and Virgin Pulp Prices

Old corrugated containers (OCC) averaged USD 44 per ton in November 2025, sinking 41% from the prior year before rebounding USD 1 per ton in January 2026 as mills pre-bought for spring downtime. The Producer Price Index for high-grade recyclable pulp whipsawed from 77.411 in November 2025 to 87.545 in October 2025 and back to 82.723 by February 2026, underscoring monthly cost swings that distort contract budgeting. Chinese policy shifts requiring disclosure of wet versus dry recycled pulp imports cut export pull-through, intensifying domestic price uncertainty. Because folding carton converters typically adjust customer pricing with a 3- to 6-month lag, margin compression surfaces whenever OCC or virgin pulp spikes mid-cycle. Persistent volatility complicates strategic sourcing and discourages long-term price commitments in the United States folding carton industry.

Capacity Expansion of Flexible Packaging Displacing Folding Cartons

The U.S. flexible packaging sector reached USD 64 billion in 2025 and is projected to reach USD 97.5 billion by 2035 at a 4.3% CAGR, outpacing carton growth and capturing share in snacks, pet foods, and personal care through lightweight pouches with high-barrier films. Twenty-one percent of converters already run digital pouch equipment, while 61% of brands have increased SKUs over the past two years, favoring short-run stand-up formats. Major resin players are promoting mono-material films that claim recyclability parity with paperboard, blurring sustainability narratives and siphoning innovation budgets. Folding cartons retain advantages in rigidity, stacking strength, and premium shelf presence, yet the steady scale-up of pouches restrains their addressable volume in several high-turn categories within the United States folding carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Fiber Gains Amid EPR Fee Pressure

The United States folding carton market size for solid bleached sulfate captured 38.21% market share in 2025, underpinned by food, beverage, and pharmaceutical SKUs that require flawless ink laydown and certified food-contact surfaces. Folding boxboard is projected to outpace the overall market at an 8.19% CAGR, buoyed by EPR fee schedules that reward recycled content and by plentiful OCC priced at USD 44 per ton. Coated unbleached kraft serves grease-resistant, natural-aesthetic niches, while white line chipboard competes on cost for non-food secondary packs. Net recycled board capacity rose modestly in 2025 as Graphic Packaging’s Waco mill ramp offset closures in Minnesota and Texas. Minnesota’s EPR eco-modulation rules that favor weight reduction are pushing brands toward lighter caliper folding boxboard, reinforcing momentum away from virgin bleached substrates.

Converters that secure high-quality recycled furnish enjoy price resilience, because EPR fees linked to recycled content narrow the cost gap versus virgin grades. Packaging Corporation of America’s acquisition of Greif’s recycled mills raised its recycled mix from 20% to 30%, highlighting a strategic pivot toward fee-friendly substrates. These fiber-mix adjustments suggest that the United States folding cartons market will continue tilting toward recycled fiber, especially in regulated coastal states where fee structures directly impact total delivered cost.

By Printing Technology: Digital Encroachment Accelerates SKU Proliferation

Flexographic presses controlled 46.91% of output in 2025, leveraging high line speeds and optimized drying tunnels for large-volume SKUs. Yet digital presses are expanding at a 7.81% CAGR because 60% of converters now run inkjet or electrophotographic units that profitably handle runs of fewer than 5,000 sheets. Hybrid lines that marry flexographic spot colors with inkjet variable-data cut makeready waste by 30% and eliminate an entire plate cycle, reducing labor hours when skilled operators are scarce.

Operating cost inflation averaged 4.4% in 2025 for label and package printers, outpacing 3% price hikes, which intensified the search for automation savings. Digital’s ability to queue artworks without plate swaps aligns with the 60% of brand owners expecting further SKU expansion over two years. These economics underpin sustained share gains for digital in the United States folding cartons market, though flexography will likely retain volume leadership for commodity runs above 50,000 impressions.

By End-User Industry: E-Commerce Redefines Carton Specifications

Food and beverage accounted for 54.41% of the United States folding carton market size in 2025, benefiting from shelf-ready displays that lift labor efficiency at mass retailers. E-commerce and retail-ready packaging is projected to grow at an 8.17% CAGR through 2031, as boxes and cartons hold a 40% share of the USD 86.2 billion global e-commerce packaging market. Healthcare and pharmaceuticals rely on cartons validated to ASTM and ISTA cold-chain protocols, while personal care exploits premium coatings to drive unboxing shareability.

Retail standards that require “easily identifiable, easily opened, easily merchandised, easily shopped, and easily disposable” packaging are now default bid specifications at Walmart and Kroger, triggering widespread adoption of tear-strips, resealable features, and How2Recycle PRO labels. Consumer demand for portion control and convenient openings, reinforced by 23% household use of GLP-1 medications, is prompting further functional upgrades. Collectively, these requirements reshape carton design across end-use verticals and fuel sustained growth for engineered formats in the United States folding cartons market.

Geography Analysis

California, Minnesota, Washington, Oregon, Maryland, Colorado, and Maine are dictating national redesign cycles as their EPR statutes require granular data submissions by May 31, 2026, effectively setting a compliance baseline for brands that sell nationally. Coastal states combine high per-capita consumption with access to Asian recycled pulp, yet freight bottlenecks and port congestion have increased inbound lead times, prompting converters to pre-position safety stocks. OCC prices on the West Coast rose USD 5 per ton in January 2026 after local containerboard mills accelerated build-ahead orders.

The Southeast gained manufacturing share as Smurfit WestRock invested USD 19.3 million to expand capacity in Saltillo, Mississippi, while Pratt Industries opened a 496,000-square-foot plant in Georgia, lifting its state workforce above 2,100. Lower labor costs and abundant recycled fiber make the region attractive for new mills and converting lines. In the Midwest, Wisconsin’s location quotient of 2.40 for printing press operators underscores a legacy skill base, yet operators earn below coastal wage scales, keeping production costs competitive.

Northeast converters face higher wages, USD 24.59 hourly in New York, but benefit from dense consumer markets that shorten last-mile delivery. International Paper’s acquisition of North Pacific Paper Company strengthened the supply of lightweight recycled board to Western customers, helping balance geographic production disparities. Together, these dynamics produce a bifurcated map. EPR states accelerate demand for recycled-content cartons, while the Southeast and Midwest absorb capacity additions that feed national distribution, an equilibrium that shapes regional pricing across the United States folding cartons market.

Competitive Landscape

Industry consolidation accelerated when Smurfit Kappa and WestRock merged in July 2024, forming a USD 30.9 billion entity that operates 37 consumer-packaging plants and 3.2 million tons of paperboard capacity, giving it scale in everything from recycled linerboard to litho-laminated cartons. Packaging Corporation of America followed with a USD 1.8 billion pickup of Greif’s mills, lifting its recycled content to 30% and vaulting it to number three in U.S. containerboard supply. Graphic Packaging, with USD 8.807 billion in 2024 net sales, offset mill closures by ramping its Waco recycled board facility in late 2025, reinforcing recycled supply in the Southwest.

Georgia-Pacific deepened its foodservice reach by acquiring Anchor Packaging, adding four plants and 1,250 staff to create GP Foodservice Solutions. Bain and Company’s 2026 analysis notes deal-size growth even as deal count falls, suggesting that strategic buyers are prioritizing scale, vertical integration, and digital capabilities over pure capacity plays. Meanwhile, mid-tier challengers such as PaperWorks Industries and WML Paperboard are expanding in niche value-added segments through targeted acquisitions that shorten lead times and embed design-for-recyclability services.

Antitrust scrutiny looms after a July 2025 class action alleging containerboard price coordination, with motions to dismiss pending in 2026, creating regulatory overhang on future mega-mergers. White-space growth revolves around digital print integration, high-barrier recyclable coatings, and data-driven EPR compliance support. Competitive intensity therefore centers on balancing cost leadership with service differentiation as the United States folding carton market scales toward recycled substrates and omnichannel design demands.

United States Folding Carton Industry Leaders

Smurfit Westrock plc

Graphic Packaging Holding Company

International Paper Company

Sonoco Products Company

Georgia-Pacific LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Packaging Corporation of America reported Q1 2026 net income of USD 171 million on USD 2.368 billion sales, with corrugated shipments up 19.9% year-over-year including Greif volumes.

- February 2026: Smurfit Westrock set a 2030 Adjusted EBITDA goal of USD 7 billion and signaled capacity for share buybacks starting in 2027.

- February 2026: Graphic Packaging confirmed 2026 capex of USD 450 million focused on asset optimization after Waco mill ramp-up.

- October 2025: Georgia-Pacific finalized the Anchor Packaging acquisition, adding four factories and two warehouses to create GP Foodservice Solutions.

United States Folding Carton Market Report Scope

The United States folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into cartons for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The United States Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current United States folding cartons market size and its expected value by 2031?

The market stood at USD 9.94 billion in 2025, should reach USD 10.63 billion in 2026, and is forecast to attain USD 14.91 billion by 2031.

Which material segment is growing fastest within United States folding cartons?

Folding boxboard is projected to grow at an 8.19% CAGR through 2031 as brands seek higher recycled fiber content to minimize EPR fees.

Why are digital printing presses gaining share in folding carton production?

Digital presses cut makeready waste, handle runs below 5,000 units profitably, and support SKU proliferation, leading to a 7.81% CAGR in digital output.

How are state-level EPR laws influencing carton design?

EPR statutes in seven states impose eco-modulated fees that favor recyclable, lightweight cartons with verifiable recycled content, prompting nationwide substrate and barrier conversions.

What competitive moves are reshaping supplier dynamics?

Major consolidation includes the USD 30.9 billion Smurfit Westrock merger and Packaging Corporation of America's USD 1.8 billion purchase of Greif mills, boosting recycled board capacity and vertical integration.

Which end-use segment offers the fastest growth opportunity?

E-commerce and retail-ready packaging is forecast to expand at an 8.17% CAGR through 2031 as online fulfillment demands protective, right-sized cartons.

Page last updated on: