Japan Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.96 Billion |

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 4.29 Billion |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

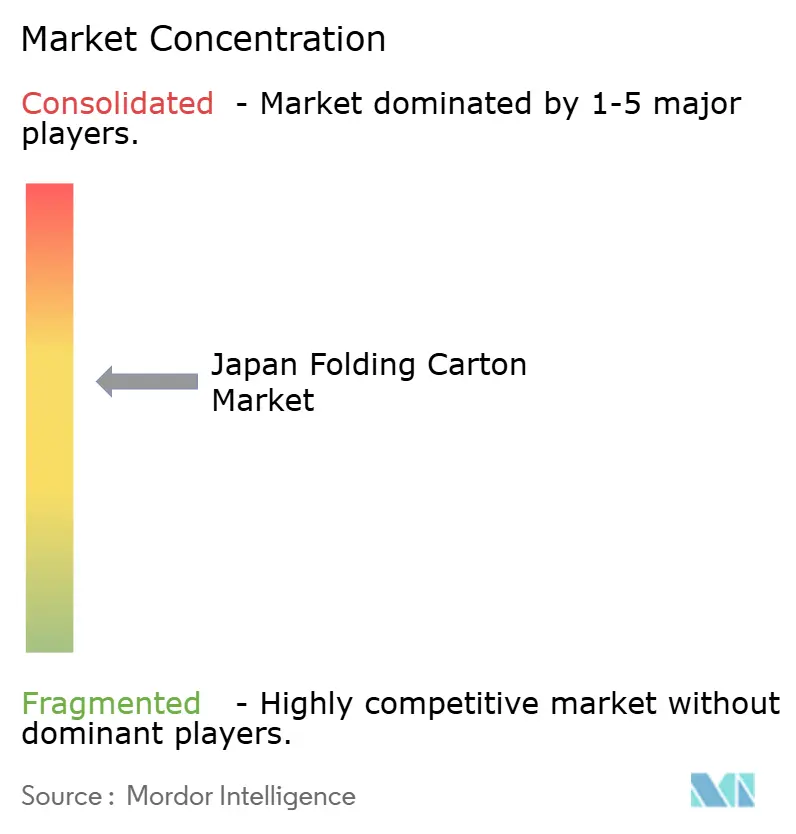

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Folding Carton Market Analysis by Mordor Intelligence

The Japan folding carton market size is expected to increase from USD 2.96 billion in 2025 to USD 3.14 billion in 2026 and reach USD 4.29 billion by 2031, growing at a CAGR of 6.44% over 2026-2031. Structural change in Japan’s fiber-based packaging ecosystem is steering investment away from shrinking graphic paper grades toward higher-margin paperboard that meets retail, e-commerce, and regulatory demands. Domestic mills now allocate 54.6% of output to packaging, while printing-paper volumes are projected to contract by more than 10% through 2030 as digital substitution accelerates. Retailer commitment to lower single-use plastic, an aging consumer base that values easy-open formats, and omnichannel logistics that favor rigid, branded displays are all bolstering demand for folding cartons. Incumbents are answering with barrier-coated substrates that replace aluminum laminates, digital presses that cut make-ready waste, and vertically integrated recycling programs that promise a secure fiber supply. Competitive intensity, however, remains high because imports and flexible pouches are pressuring margins, forcing converters to pursue automation and overseas diversification to protect earnings.

Key Report Takeaways

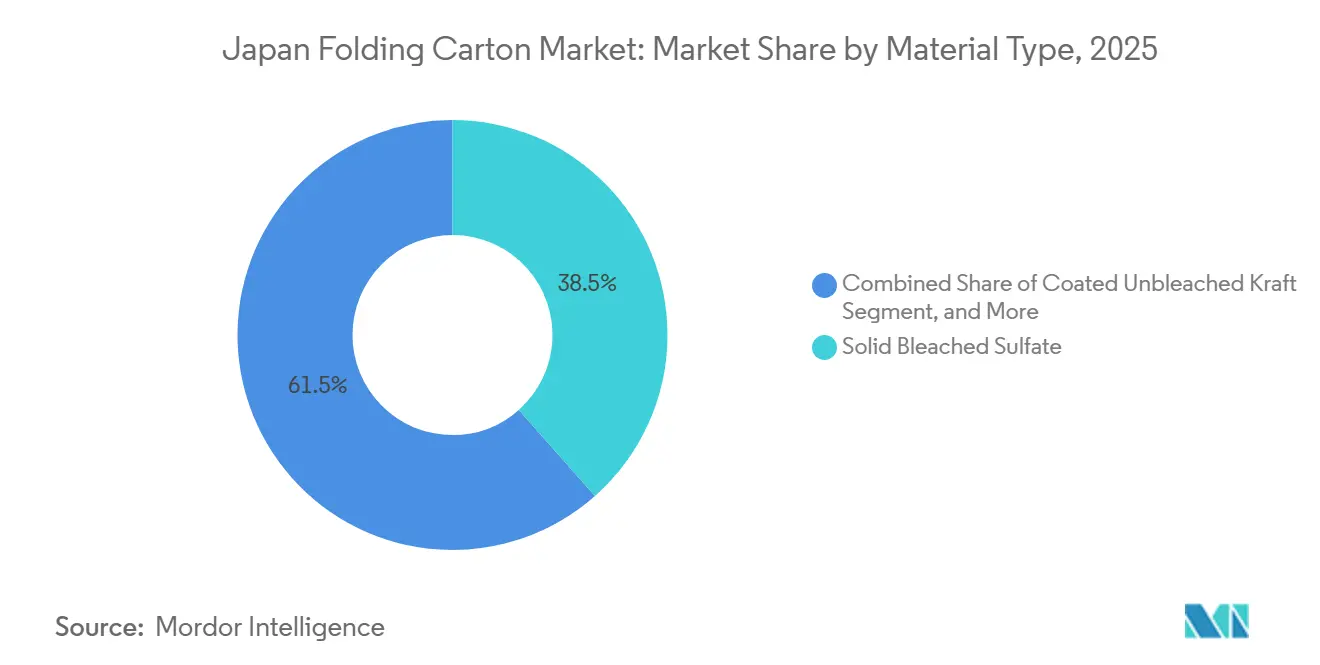

- By material type, solid bleached sulfate captured with 38.47% of the Japan folding carton market share in 2025.

- By printing technology, the Japan folding carton market size for digital platforms is projected to grow at a 7.15% CAGR to 2031.

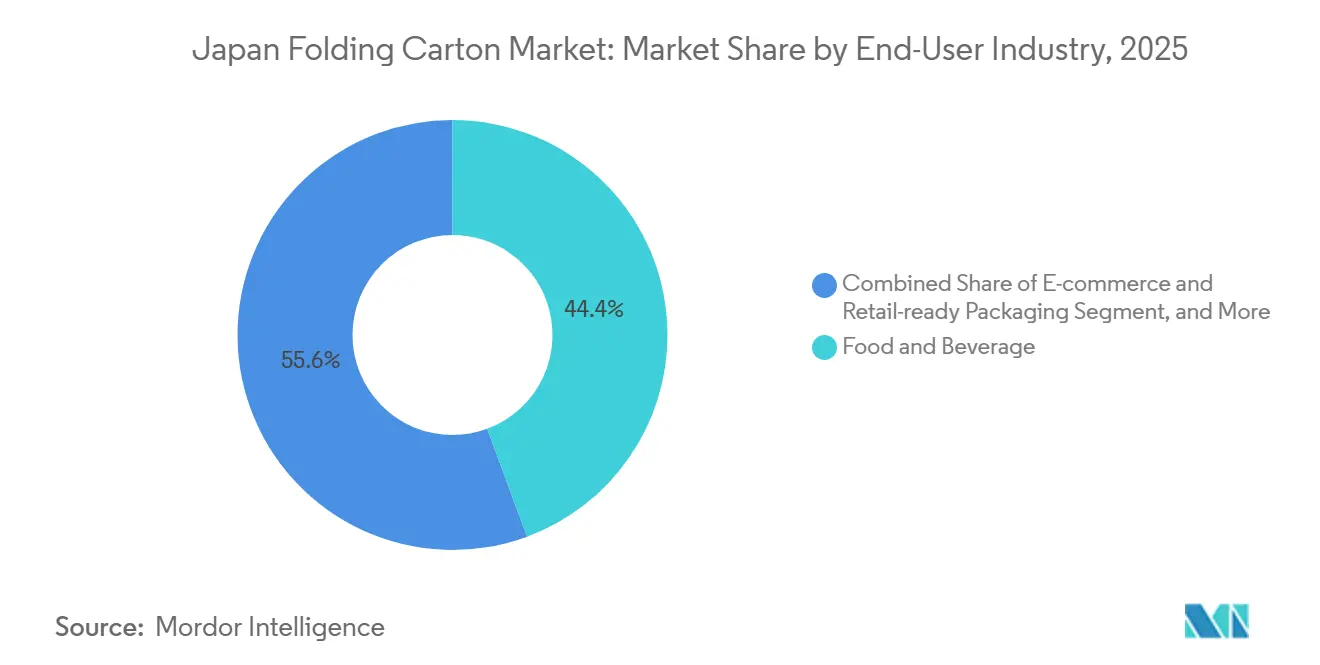

- By end-user industry, the food and beverage industry captured 44.36% of the Japan folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Boom Accelerating Custom Carton Demand | +1.2% | National, focus on Tokyo, Osaka, Nagoya metro areas | Short term (≤ 2 years) |

| Shift Toward Sustainable Packaging Materials | +1.5% | National, aligned with MOE Plastic Resource Circulation Act | Medium term (2-4 years) |

| Premiumization of Ready-to-Eat Meals Requiring High-Graphics Cartons | +0.9% | Urban centers in Kanto and Kansai regions | Medium term (2-4 years) |

| Government Plastic Waste Reduction Targets Boosting Paperboard Use | +1.3% | National, early adoption in strict-sorting municipalities | Long term (≥ 4 years) |

| Retailers’ Private-Label Expansion Driving Short-Run Digital Print Jobs | +0.8% | National, led by Seven-Eleven, Lawson, FamilyMart | Short term (≤ 2 years) |

| Aging Population Increasing Demand for Easy-Open Pharmaceutical Cartons | +0.7% | National, especially rural prefectures with older demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Sustainable Packaging Materials

Japan’s Plastic Resource Circulation Act mandates a 25% cut in single-use plastic by 2030, pushing brand owners to specify FSC-certified or recycled cartons that meet design-for-recycling guidelines. Retailers such as Lawson target 80% eco-friendly packaging, raising demand for paperboard that can displace polystyrene clamshells and polyethylene pouches. Toppan plans to raise sustainable packaging sales to 80% by 2030, reflecting the willingness of cosmetics and personal-care brands to pay premiums for verifiable green claims. Supply, however, is constrained because Japan’s ban on exporting contaminated recovered paper tightened the domestic pool of post-consumer fiber. Converters integrated into collection networks, like Oji Holdings through its Renewa program, thereby gaining a cost and sourcing advantage. The sustainability pivot, therefore, rewards mills able to certify chain-of-custody, formulate water-based inks, and guarantee closed-loop take-back, while penalizing operators limited to virgin-fiber grades.

Government Plastic Waste Reduction Targets Boosting Paperboard Use

National plastic-reduction targets set at 25% by 2030 are steering pharmaceutical, personal-care, and food companies toward paperboard that matches the barrier performance of plastic blister or clamshell packs. Cartons engineered with tear notches and thumb-lift tabs cut opening force by up to 40%, improving medicine adherence among seniors and aligning with ISO 8317 child-resistance requirements. Nippon Paper’s partnership with Elopak to localize Pure-Pak liquid cartons creates a domestic source of non-aluminum, recyclable aseptic packaging, giving brand owners a path to compliance with extended producer responsibility. Municipalities that impose strict waste-sorting accelerate adoption, creating pull-through demand for converters that certify mono-material structures. Over the long term, the policy lock-in ensures baseline growth for fiber-based formats even if commodity pulp costs fluctuate.

E-commerce Boom Accelerating Custom Carton Demand

Parcel volumes have surged as online penetration surpasses 20% across many categories, prompting converters to install high-resolution digital presses that cost-effectively produce runs of fewer than 5,000 impressions. Convenience stores double as micro-fulfillment hubs, pushing shelf-ready cartons with integrated graphics and tamper evidence that shorten replenishment cycles. Ricoh’s thermal media technology enables on-demand printing across thousands of stores, cutting lead times and reducing waste. HP Indigo 35K HD units, now common among large converters, print 1,600 dpi on 150-600 micron board, unlocking mass customization for regional promotions. The e-commerce driver forces lithographic operators to adopt hybrid workflows or risk losing orders to nimble competitors that meet retailer mandates for just-in-time, variable-data packaging.

Premiumization of Ready-To-Eat Meals Requiring High-Graphics Cartons

Convenience chains are upgrading food ranges to preserve ticket size even as foot traffic tails off, demanding visually rich cartons with metallic inks and tactile coatings that elevate perceived quality. Toppan’s GL BARRIER replaces aluminum in mid-barrier applications while maintaining gloss and print fidelity, enabling mono-material recyclability.[1]Toppan Inc., “Sustainability Report FY 2024,” toppan.com Brand owners willingly absorb a 15-25% unit-cost premium because high-graphics packaging boosts sell-through in competitive chilled-food displays. Converters, therefore, must master multi-pass lithography and digital embellishment without compromising fiber recovery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Fiber Pulp Prices | -0.9% | National, higher exposure for converters reliant on imported pulp | Short term (≤ 2 years) |

| Supply Chain Disruptions from Imported Paperboard Feedstock | -0.7% | Port cities such as Yokohama, Osaka, Kobe | Short term (≤ 2 years) |

| Labor Shortages in Converting Facilities Limiting Capacity | -0.5% | National, acute in rural prefectures | Medium term (2-4 years) |

| Rising Popularity of Flexible Pouches in Snacks Segment | -0.4% | National, focused on snack and confectionery shelves | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Fiber Pulp Prices

South American long-fiber bleached kraft pulp reached USD 655 per ton in February 2026, 14% higher than five months earlier, squeezing converters that lack hedging programs. Energy shocks stemming from the Strait of Hormuz closure also added 60% to naphtha input costs, spilling over into secondary packaging consumables. Smaller plants struggle most because they cannot fully pass increases to brand owners or lock in multiyear supply contracts. Dai Nippon Printing warned of margin pressure in its fiscal-year 2025 results, and Nippon Paper trimmed its FY 2026 operating-income outlook by JPY 4 billion (USD 27 million) for similar reasons.[2]Nippon Paper Industries, “Q2 FY 2025 Financial Results,” nipponpapergroup.com Vertically integrated players, notably Oji Holdings with 636,000 hectares of forestry assets, enjoy partial insulation. Nonetheless, prolonged pulp gyrations erode profitability across the value chain and curb capital-expenditure appetite.

Supply Chain Disruptions from Imported Paperboard Feedstock

The February 2026 Strait of Hormuz shutdown forced carriers to reroute around the Cape of Good Hope, adding up to two weeks of transit time and inflating freight by 40-50% for shipments into Yokohama and Kobe. Japan maintains about 20 days of naphtha inventory, leaving converters vulnerable when petrochemical-derived stretch film or adhesives run short. Stretch-film imports account for more than 90% of domestic demand, 70% arriving from Malaysia, amplifying single-source risk. Hokuetsu’s January 2026 creation of an Export Sales Headquarters signals industry attempts to diversify supply lines. Nevertheless, tight shipping capacity and container rollover events can idle converting lines, delay product launches, and reduce revenue, especially for just-in-time private-label programs that lack buffer stock.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Fiber Gains Ground

Solid Bleached Sulfate accounted for 38.47% of the Japan folding carton market share in 2025 because its brightness and stiffness meet the aesthetics demanded by cosmetics and pharmaceutical brands. Yet White Line Chipboard, priced 20-30% below virgin grades, is projected to outpace all others at a 7.26% CAGR through 2031 as grocery retailers and e-commerce shippers accept gray-back board for inner surfaces where appearance matters less. The Japan folding carton market size tied to recycled substrates therefore rises in tandem with corporate plastic-reduction pledges that favor lower-carbon, post-consumer fiber.

Converters are expanding their portfolios to switch rapidly between virgin and recycled recipes as pulp prices swing. Mills equipped with twin-wire formers and multilayer coaters can laminate thin specialty layers over economical core plies, balancing cost against performance. Brand owners increasingly request life-cycle assessment data, prompting suppliers to certify their CO₂ footprints under ISO 14064. As a result, those offering cradle-to-grave metrics gain a sales advantage, particularly in export channels where EU packaging regulations are tightening. The pivot toward recycled fiber aligns with Japan’s goal of a 60% recycling rate for plastic packaging by 2030, anchoring long-term growth for White Line Chipboard and allied recovered-fiber grades.

By Printing Technology: Digital Presses Disrupt Long Runs

Lithographic presses accounted for 41.63% of the Japanese folding carton market in 2025, thanks to low cost per thousand on runs of 10,000+ impressions and unmatched color stability. Yet digital systems are forecast to expand at 7.15% CAGR because convenience-store private labels, loyalty campaigns, and region-specific SKUs need variable data without plate costs. HP Indigo, Landa, and Xeikon machines are now specified in request-for-quote tenders, signaling irreversible demand for mass personalization. Flexographic units are also gaining ground in cartons as high-definition anilox rolls close the quality gap with offset and water-based inks satisfy food-contact rules. Gravure remains dominant only for ultralong tobacco and confectionery runs where cylinder amortization still pays off.

Hybrid workflows that queue litho shells through inline digital overprint modules allow converters to split jobs, maximizing uptime and reducing make-ready waste. Job batching software, color-management automation, and AI-based inspection systems further shrink turnaround times, enabling plants to meet the two-day service-level agreements demanded by e-commerce sellers. Mills that lag in digital adoption risk sliding into commodity status, especially as brand owners consolidate supplier rosters to those offering data-driven versioning and serialization for anti-counterfeit programs.

By End-User Industry: E-commerce Reshapes Demand

Food and Beverage consumed 44.36% of the Japanese folding carton market size in 2025 because more than 55,000 convenience stores restock bentos, sweets, and RTD beverages multiple times a day. Shelf-ready designs that double as mini displays reduce in-store labor and boost impulse purchases, driving carton complexity upward. However, E-commerce and Retail-ready Packaging will post the fastest 6.89% CAGR through 2031, as parcel shippers request branded unboxing experiences that protect goods in transit and reduce void fill. Healthcare and Pharmaceuticals rise steadily on the back of population aging, which hits 35% by 2040. Pharmaceutical cartons must integrate braille, easy-tear features, and ISO 8317 child-resistance, a capability more accessible to converters with laser die-cutters and inline embossing.

Personal Care and Cosmetics remain high-margin niches demanding metallic inks and tactile coatings that convey luxury, aligning with converters’ premiumization strategies. Electrical and Electronics brands transition from foam to molded pulp or rigid board to meet corporate sustainability targets, while Tobacco and Industrial Goods stay flat, reflecting market maturity. Emerging applications, such as toy and automotive aftermarket, provide modest upside as import displacement and e-commerce penetration deepen. Segment diversification therefore cushions converters against cyclical shocks in any single vertical.

Geography Analysis

Production and consumption concentrate along Japan’s Pacific belt. Kanto, dominated by Tokyo and Yokohama, accounts for the largest slice of the Japanese folding carton market thanks to dense population, abundant brand-owner headquarters, and a critical mass of fulfillment centers. Kansai, anchored by Osaka and Kobe, ranks second, benefiting from proximity to food and pharmaceutical plants and an export-oriented industrial base. Chubu, with Nagoya, serves automotive supply chains that prefer heavy-duty cartons. Coastal plants enjoy import logistics advantages for pulp and paperboard, yet face greater exposure to port congestion and shipping reroutes, such as those triggered by the 2026 Strait of Hormuz closure. Inland facilities, by contrast, incur higher inbound freight but are less vulnerable to maritime shocks.

Regional demand also mirrors demographic patterns. Urban prefectures favor high-graphics, short-run cartons for convenience-store restocking and online grocery, whereas rural areas with higher shares of residents over 65 lean toward easy-open pharmaceutical and single-serve food formats. Labor scarcity is most acute outside major metros, pushing mills to automate die-cutting and finishing or consolidate into larger hubs. Nippon Paper’s plan to concentrate graphic-paper output into about three sites to reach 90% utilization exemplifies the drive for scale efficiency.[3]Nippon Paper Industries, “Integrated Report FY 2024,” nipponpapergroup.com

Infrastructure projects further shape competitiveness. Investments in high-speed digital presses and automated gluing lines cluster in Kanto, where converters chase private-label growth. Oji Holdings and Rengo, however, are channeling capital toward Vietnam and India to tap faster-growing ASEAN demand and hedge against Japan’s flat population outlook. Domestic capacity additions therefore remain selective, prioritizing technologies that cut labor reliance or open adjacent services such as design and recycling.

Competitive Landscape

Rengo, Oji Holdings, and Nippon Paper Industries together own more than 60% of domestic capacity, giving the Japan folding carton industry a moderately consolidated profile. Yet price competition is intense because imports, flexible pouches, and smaller niche converters cap pricing power. Rengo’s October 2025 10-yen-per-kilogram price move illustrates attempts to pass on input inflation, but its forecast of only 2.1% corrugated growth signals softening demand. Oji Holdings offsets domestic stagnation through a 40.8% ratio of overseas sales and forest ownership, shielding it from pulp price swings. Nippon Paper is rebalancing toward packaging, aiming to have daily-use products account for more than 50% of revenue by 2030, but has cut its FY 2026 operating income target amid weakness in Australian demand.

White-space opportunities center on sustainable luxury, digital customization, and functional barrier coatings. Toppan’s acquisition of Sonoco's flexibles and paperblister assets adds mono-material solutions to its portfolio, positioning it to win North American eco-friendly mandates.[4]Toppan Inc., “TOPPAN Packaging Acquires Sonoco Flexibles,” toppan.com Smaller firms such as Hokuetsu grew export volume 20% year-over-year to 290,000 tons by serving Southeast Asian buyers who value Japan’s quality. Tomoku’s ECowrap, recognized with a WorldStar Award, shows how protective paperboard cushioning can replace plastic bubble wrap and command premium margins.

Technology adoption is the key differentiator. Converters that deploy AI-enabled inspection, IoT predictive maintenance, and data-linked digital presses can guarantee 24-hour turnaround and lot-level traceability. Capital requirements deter many mid-size plants, creating openings for private-equity roll-ups that aggregate volumes and unlock scale. Over the forecast horizon, the Japan folding carton market will reward companies that marry fiber security, digital agility, and verifiable sustainability credentials.

Japan Folding Carton Industry Leaders

Rengo Co., Ltd.

Oji Holdings Corporation

Nippon Paper Industries Co., Ltd.

Toppan Inc.

Hokuetsu Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Dai Nippon Printing commenced mass production of decorative film for automotive displays, using microfabrication to embed woodgrain patterns within optically clear, scratch-resistant layers for global rollout.

- April 2026: TOPPAN Packaging completed the acquisition of Sonoco’s Flexibles and Thermoformed units, establishing a Charlotte headquarters and adding Paperblister retail packaging to its sustainable lineup.

- January 2026: Hokuetsu reorganized, creating an Export Sales Headquarters to accelerate overseas growth after fiscal-year 2024 export volumes rose 20% to 290,000 tons.

- November 2025: Nippon Paper Industries reported FY 2025 Q2 sales of JPY 274.2 billion (USD 1.83 billion) and negative operating income of JPY 1.5 billion (USD 10.1 million), citing high pulp costs and soft Australian demand.

Japan Folding Carton Market Report Scope

The scope of the study includes an analysis of market trends, growth drivers, challenges, and opportunities within the Japan Folding Carton Market. It covers key segments, including material types, end-user industry, and printing technology, while providing insights into the competitive landscape and market dynamics during the forecast period. These cartons are valued for their lightweight, recyclable, and customizable properties, making them a preferred choice for sustainable packaging solutions.

The Japan Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Market size of the Japanese folding carton market?

The Japan folding carton market size stood at USD 2.96 billion in 2025 and is projected to reach USD 4.29 billion by 2031.

Which material type is growing fastest in Japan’s carton sector?

White Line Chipboard is forecast to grow at a 7.26% CAGR to 2031 as retailers favor cost-effective recycled fiber.

Why are digital presses gaining ground in Japanese folding cartons?

Retailer private-label expansion and e-commerce customization demand short runs and variable data that offset presses cannot deliver economically, prompting converters to install HP Indigo and similar units.

How will plastic-reduction regulations influence carton demand?

National targets for a 25% cut in single-use plastic by 2030 are steering brands toward paperboard formats that satisfy recyclability and extended-producer-responsibility rules.

Which companies lead the Japan folding carton industry consolidation?

Rengo, Oji Holdings, and Nippon Paper Industries together hold more than 60% of domestic capacity, giving them scale advantages in fiber sourcing and technology investment.

What risks could restrain future growth of Japan’s folding carton sector?

Sharp spikes in imported pulp prices and shipping disruptions through key chokepoints such as the Strait of Hormuz can squeeze margins and delay deliveries, especially for mills without vertical integration.

Page last updated on: