Benelux Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.29 Billion |

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 1.64 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benelux Folding Carton Market Analysis by Mordor Intelligence

The Benelux folding carton market size is expected to grow from USD 1.29 billion in 2025 to USD 1.34 billion in 2026 and is forecast to reach USD 1.64 billion by 2031 at 4.12% CAGR over 2026-2031. Dense consumer-goods production clusters, e-commerce saturation, and binding European Union circular-economy mandates are simultaneously lifting volume and reshaping substrate choices. Netherlands logistics dominance around the Port of Rotterdam channels import-export flows into carton converting hubs, while Belgium pharmaceutical and confectionery producers favor premium solid bleached sulfate grades. Luxembourg is emerging as an e-commerce fulfilment springboard for neighboring countries, adding incremental demand despite its small population. Across the Benelux folding carton market, converters that align material light-weighting with recyclability benchmarks are in the strongest competitive position.

Key Report Takeaways

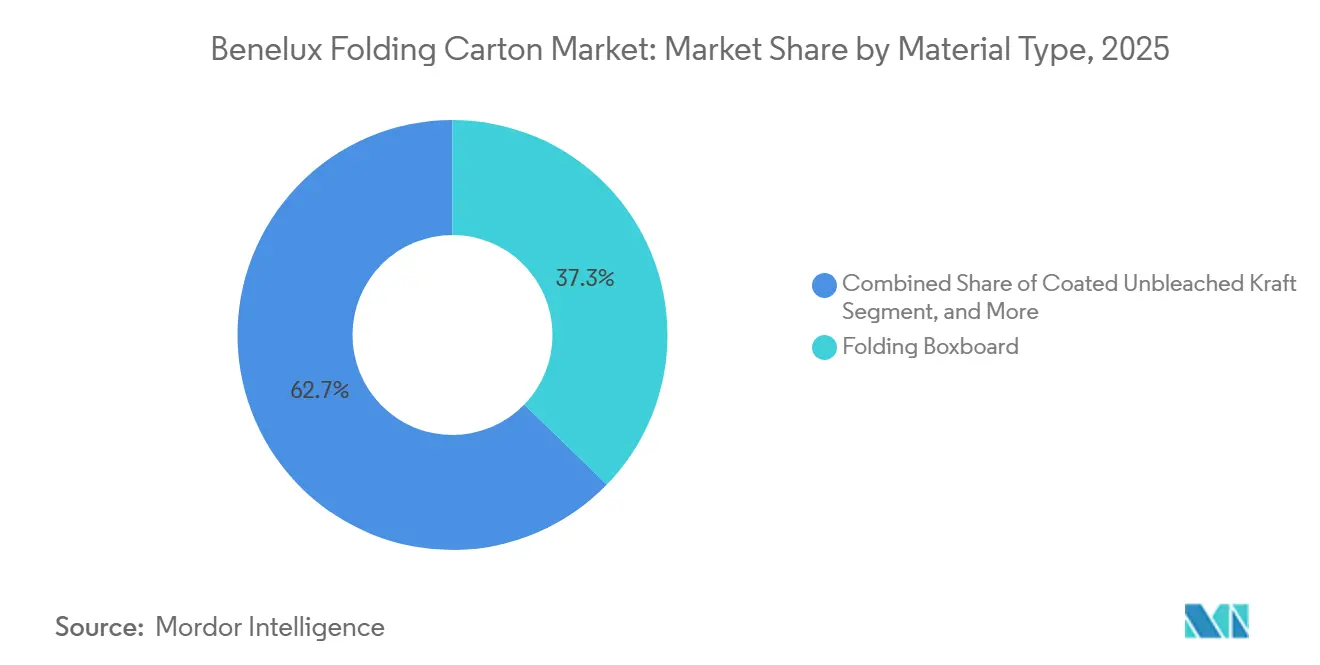

- By material type, folding boxboard captured with 37.25% of the Benelux folding carton market share in 2025.

- By printing technology, the Benelux folding carton market size for digital platforms is projected to grow at a 5.77% CAGR to 2031.

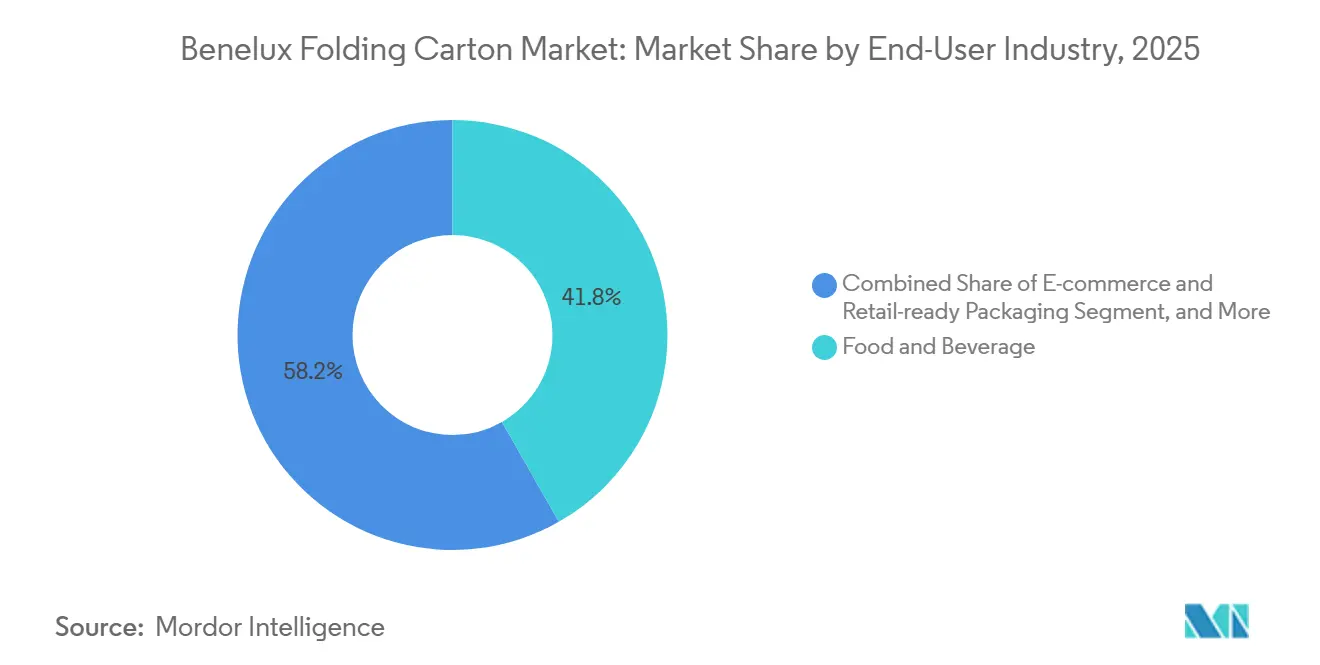

- By end-user industry, the food and beverage industry captured 41.76% of the Benelux folding carton market share in 2025.

- By geography, the Benelux folding carton market size for Luxembourg is projected to grow at a 5.64% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Benelux Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable and Recyclable Packaging | +1.2% | Benelux-wide, strongest in Netherlands and Belgium | Medium term (2-4 years) |

| Rising E-commerce Shipments Driving Retail-ready Formats | +0.9% | Netherlands dominant, Luxembourg emerging | Short term (≤ 2 years) |

| Stringent EU Regulations Phasing Out Single-use Plastics | +0.8% | EU-wide, uniform enforcement across Benelux | Medium term (2-4 years) |

| Advancements in Digital Printing Enabling Short-run Customization | +0.6% | Netherlands and Belgium pharmaceutical hubs | Short term (≤ 2 years) |

| Surging Craft Beer Exports Boosting Premium SBS Cartons | +0.4% | Belgium and Netherlands brewery clusters | Long term (≥ 4 years) |

| Netherlands Tax Incentives for Lightweight Packaging Designs | +0.3% | Netherlands national policy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable and Recyclable Packaging

Consumer preferences and the EU Packaging and Packaging Waste Regulation, effective August 2026, are accelerating a switch from rigid plastics to fiber-based formats in the Benelux folding carton market.[1]European Commission, “Packaging and Packaging Waste Regulation,” EUROPA.EU Beiersdorf cut plastic content in Eucerin refills by 90% in 2025, making the outer folding carton the main brand carrier. Dutch retailer Jumbo adopted Tetra Pak’s Tetra Recart retortable carton, achieving a 43% reduction in carbon dioxide emissions compared with steel cans. SIG’s Terra alu-free aseptic carton reached 81% paper content, with a 90% target by 2030, widening carton demand in dairy and juice. Extended Producer Responsibility fees now reward mono-material fiber designs, sharpening the cost advantage of recyclable cartons.

Rising E-commerce Shipments Driving Retail-ready Formats

Twelve of Europe’s 23 NUTS-2 regions with online ordering penetration above 80% are in the Netherlands, turbo-charging demand for display-ready roll-end tuck-top cartons. Fulfillment centers in Luxembourg ship across borders, pushing carton volumes at a 5.64% CAGR to 2031. Suppliers such as Branded Boxes Europe guarantee two-week delivery for 100-unit minimums, matching the short lead times e-commerce requires. Belgium’s SIXPACK pilot tested reusable beer carriers but confirmed single-use cartons remain cheaper for exports. As a result, the Benelux folding carton market sees parallel growth in protective logistics designs and shelf-presentation functionality.

Stringent EU Regulations Phasing Out Single-use Plastics

The Single-Use Plastics Directive banned polystyrene food containers in 2024, steering foodservice chains toward coated paperboard. The PPWR also prohibits PFAS in food-contact packaging from 2026, prompting mills to switch from grease barriers to starch or dispersion coatings. Metsä Board invested EUR 1 billion (USD 1.06 billion) to scale dispersion barrier grades and achieved 93% fossil-free energy use by 2026. Belgium, already recycling 86% of paper and cardboard, imposes EPR fees that penalize polymer-coated boards, adding urgency to mono-material adoption. These measures are reshaping material selection across the Benelux folding carton market.

Advancements in Digital Printing Enabling Short-run Customization

Pharmaceutical serialization under the Falsified Medicines Directive demands variable QR codes and batch numbers on every carton. Faller Packaging’s Gebesee plant added 650 million digital-ready cartons annually in 2025 to serve Benelux drug makers. Van Genechten invested EUR 10 million (USD 10.6 million) in 2026 in digital embellishment to eliminate tooling costs for luxury confectionery sleeves. Autajon’s 42-site network now offers hybrid print workflows for premium spirits and perfumes. Digital’s flexibility helps brands test regional graphics in runs of 500 units, supporting SKU proliferation across the Benelux folding carton market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Fiber Prices | -0.7% | Benelux-wide, linked to global pulp markets | Short term (≤ 2 years) |

| Competition from Flexible Plastic Pouches | -0.5% | Netherlands and Belgium food segments | Medium term (2-4 years) |

| Labor Shortages in Converting Plants | -0.4% | Netherlands and Belgium industrial clusters | Medium term (2-4 years) |

| Limited Recycling Capacity for Coated Boards | -0.3% | Belgium and Luxembourg infrastructure gaps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Fiber Prices

Eucalyptus pulp producers secured successive hikes in early 2026, while northern bleached softwood kraft talks stalled, injecting cost uncertainty into the Benelux folding carton market. Fastmarkets began monthly spot benchmarks in January 2026, yet transparency has not tamed swings driven by mill outages and energy shocks. Dutch Title Transfer Facility gas prices climbed above EUR 68 per MWh (USD 72.50 per MWh) in 2026, escalating energy costs for recycled board mills. An IPV Netherlands survey found 70% of converters rank raw-material inflation as their top concern, with 40% curbing capital investment. Sonoco responded in April 2026 with a recycled board surcharge of EUR 80 per tonne (USD 85 per tonne), squeezing thin converter margins.

Competition from Flexible Plastic Pouches

Mono-material polyethylene pouches undercut cartons on cost and moisture barrier performance, threatening dry and pet food applications in the Benelux folding carton market. Amcor’s Liquiflex AmPrima pouch cuts carbon emissions by 79% against metal cans and is recyclable in PE streams. Elopak’s LCA showed its D-PAK refill carton beats LDPE pouches on global warming impact by 24%, but still lags on resource scarcity when pouches use high recycled content. Ceresana expects European flexible packaging demand to steady at 19.05 million tonnes by 2031, with stand-up pouches rebounding in food retail. Brand owners now deploy a hybrid mix of cartons for shelf presence and pouches for direct-to-consumer shipments, diluting the growth potential of both formats but posing an immediate substitution threat to the Benelux folding carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium SBS Outpaces Mainstream Grades

Folding boxboard held a 37.25% stake of the Benelux folding carton market size in 2025, serving high-volume food, pharmaceutical, and household staples. Solid bleached sulfate is advancing at a 5.46% CAGR and is winning craft beverage, cosmetics, and luxury confectionery orders that need bright surfaces and moisture resistance. Belgium exported EUR 1.7 billion (USD 1.75 billion) of beer in 2024, while the Netherlands shipped EUR 2.0 billion (USD 2.06 billion) in 2023, pushing breweries toward high-brightness SBS cartons that withstand refrigeration humidity and showcase lithographic graphics. Coated unbleached kraft stays relevant for heavy glass or industrial loads, whereas white line chipboard faces higher EPR fees because polymer coatings hinder recycling.

Regulatory recycled-content targets of 30% by 2030 are nudging converters to blend recycled fiber grades for non-food items while reserving virgin SBS for sensitive products. Converters are qualifying Metsä Board dispersion-barrier boards to replace polyethylene lamination, enabling fully fiber mono-material structures that avoid PFAS restrictions and lower EPR costs.[2]Fost Plus Belgium, “Extended Producer Responsibility,” fostplus.be Market leaders anticipate that solid bleached sulfate will increase its share of the Benelux folding carton market by several points by 2031 as premiumization and sustainability converge.

By Printing Technology: Digital Quality Meets Compliance Needs

Lithographic printing accounted for 47.28% of the Benelux folding carton market in 2025, given its speed and cost efficiency on runs of 50,000 or more impressions. Digital printing, with a 5.77% CAGR, eliminates plate charges and enables serialized data, making it the method of choice for pharmaceutical safety codes under the Falsified Medicines Directive. Faller Packaging’s Gebesee site added 650 million digitally printed cartons annually in 2025 for Benelux drug makers. Van Genechten’s EUR 10 million (USD 10.6 million) Riga upgrade introduced tactile varnish and metallic effects in a single pass, reducing time-to-market for confectionery campaigns.

Hybrid workflows now pair flexographic base colors with digital personalization, giving converters cost leverage on mid-length jobs. Gravure, once the luxury benchmark, is losing share as plain-pack tobacco directives mute elaborate graphics. Through 2031, brand owners that juggle localized language packs, seasonal art, and influencer co-branding will keep steering growth to digital lines inside the Benelux folding carton market.

By End-User Industry: Online Retail Redraws Usage Patterns

Food and beverage accounted for 41.76% of the Benelux folding carton market in 2025, led by dairy multipacks, frozen foods, and beer clusters. Yet e-commerce and retail-ready formats are expanding at a 5.49% CAGR because Dutch consumers rank among Europe’s most avid online grocery shoppers. Shelf-ready roll end tuck top designs improve replenishment velocity at Albert Heijn and Carrefour, while double-thickness bases meet parcel carrier drop tests. Healthcare and pharmaceuticals remain steady, buoyed by serialization mandates and zero-defect tolerances, and cosmetics brands are migrating to refillable jars supported by premium folding cartons that replace rigid plastics.

Subscription pet-food brands use flexible pouches for weight savings but still choose display cartons for brick-and-mortar channels, illustrating hybrid packaging strategies. Over the forecast horizon, omnichannel sales models will continue to reshape volume allocations in the Benelux folding carton market while sustaining growth momentum for converters that master both protective transit designs and high-impact shelf presence.

Geography Analysis

Netherlands generated 57.63% of Benelux folding carton demand in 2025, anchored by Europe’s largest container port at Rotterdam, dense FMCG headquarters in the Randstad, and the continent’s highest online ordering penetration. The Environmental Investment Allowance permits a 45% tax deduction on sustainable packaging machinery, catalyzing upgrades to lightweight carton lines. Dutch recycling rates reached 88% for all packaging in 2024, yet polymer-coated boards remain recovery bottlenecks.

Brewers exporting USD 2.06 billion worth of beer favor moisture-resistant SBS cartons, bolstering demand for premium substrates. Belgium ranks second in volume, supported by pharmaceutical clusters around Antwerp and Wallonia and confectionery majors such as Godiva. A paper and cardboard recycling rate of 86% in 2024 underscores the maturity of the circular economy, although coated liquid cartons still lack domestic separation capacity. Stora Enso and Tetra Pak plan to build a 50,000-tonne beverage carton recycling plant to close this gap by 2027.

Belgium’s EUR 1.75 billion (USD 1.87 billion) beer export trade widens SBS opportunity for specialty six-packs and gift multipacks.[3]Belgian Brewers Association, “Beer Export Statistics 2024,” belgianbrewers.be Luxembourg, while smallest, is poised for a 5.64% CAGR to 2031 as cross-border fulfilment centers leverage low VAT and customs simplicity to serve France, Germany, and Belgium. Converters position short-run digital lines near hub warehouses to cut delivery times. Together, the tri-market integration underpins a resilient and interconnected Benelux folding carton market.

Competitive Landscape

Market concentration is moderate: the top five suppliers, Smurfit WestRock, Mayr-Melnhof, Stora Enso, International Paper, and Mondi, control about 55% to 60% of installed capacity. Smurfit WestRock is allocating USD 2.4 billion to USD 2.5 billion in 2026 capex to retrofit converting lines with inline digital presses, aiming to capture retail-ready volume tied to e-commerce. International Paper’s plan to spin off its EMEA arm and remove USD 250 million to USD 300 million in costs could free capital for niche acquisitions among Benelux specialists.

Regional champions, including Van Genechten Packaging, Edelmann Group, and Autajon Group, win pharmaceutical, cosmetics, and luxury contracts through rapid prototyping and co-development. Van Genechten’s Riga expansion supplies premium confectionery cartons to Benelux boutiques within two days by truck. Autajon’s 42-site network delivers synchronized label and carton programs for cross-channel perfume launches.[4]Autajon Group, “About Us,” autajon.com Technology adoption is the dividing line: converters that deploy automated die-cutting, vision inspection, and hybrid print platforms secure high-margin accounts, while mills reliant on legacy litho-only workflows risk share erosion in the Benelux folding carton market.

White-space growth sits in dispersion-barrier fiber cartons that meet PFAS-free and recyclability criteria. Metsä Board’s EUR 1 billion (USD 1.06 billion) capacity build supports this shift and offers converters substrates that lower EPR fees while preserving grease resistance. Competitive intensity will tighten as premium brand owners lock in partnerships with vertically integrated suppliers that guarantee security of supply, compliance, and design agility.

Benelux Folding Carton Industry Leaders

Smurfit WestRock plc

Mayr-Melnhof Karton AG

Stora Enso Oyj

International Paper Company

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sonoco raised recycled paperboard prices by EUR 80 per tonne (USD 85 per tonne) across EMEA, affecting 19 tube and core plants and five board mills.

- March 2026: Van Genechten Packaging completed a EUR 10 million (USD 10.6 million) capacity upgrade in Riga for digital embellishment on confectionery and beauty cartons.

- March 2026: Metsä Board unveiled its Lead the Pack strategy, targeting more than 4% annual growth in consumer-packaging revenue and a USD 211 million EBITDA uplift by 2028.

- January 2026: International Paper announced plans to separate into North America and EMEA packaging firms, with the EMEA unit to shed up to USD 300 million in costs across 30 plants.

Benelux Folding Carton Market Report Scope

The folding carton market is the industry that produces and distributes paperboard-based packaging solutions, primarily used for consumer goods. These cartons are lightweight, recyclable, and customizable, making them a preferred choice across industries such as food and beverage, personal care, and pharmaceuticals. The study analyzes market trends, growth drivers, challenges, and opportunities in the Benelux region, comprising Belgium, the Netherlands, and Luxembourg. It examines the market dynamics, competitive landscape, and key developments influencing the adoption of folding cartons during the forecast period.

The Benelux Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries), and Geography (Belgium, Netherlands, Luxembourg). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| Belgium |

| Netherlands |

| Luxembourg |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries | |

| By Geography | Belgium |

| Netherlands | |

| Luxembourg |

Key Questions Answered in the Report

What is the current value of the Benelux folding carton market size?

It stood at USD 1.34 billion in 2026 and is forecast to reach USD 1.64 billion by 2031.

Which material segment is growing fastest?

Solid bleached sulfate cartons are projected to post a 5.46% CAGR to 2031, driven by craft beverages and cosmetics.

How are EU regulations influencing substrate selection?

The PPWR and Single-Use Plastics Directive require recyclable, PFAS-free designs, steering converters toward mono-material fiber cartons.

Why is digital printing gaining share?

Pharmaceutical serialization and limited-edition marketing need variable data and small runs that digital presses handle without plates.

Which country leads demand within Benelux?

Netherlands captured 57.63% of folding carton demand in 2025, supported by Rotterdam port logistics and high e-commerce penetration.

What is the key competitive advantage for converters?

Investments in dispersion-barrier board, hybrid digital workflows, and inline quality inspection win high-margin cosmetics and pharma contracts.

Page last updated on: