Iran Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

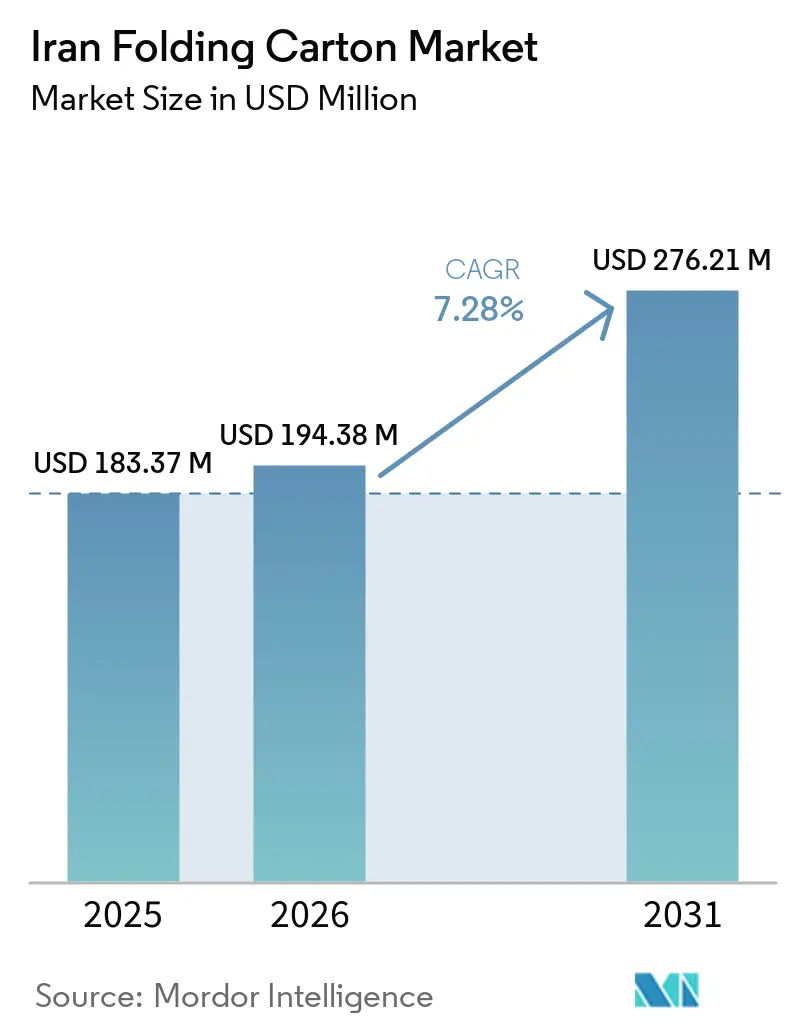

| Base Year Market Size (2025) | USD 183.37 Million |

| Market Size (2026) | USD 194.38 Million |

| Market Size (2031) | USD 276.21 Million |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

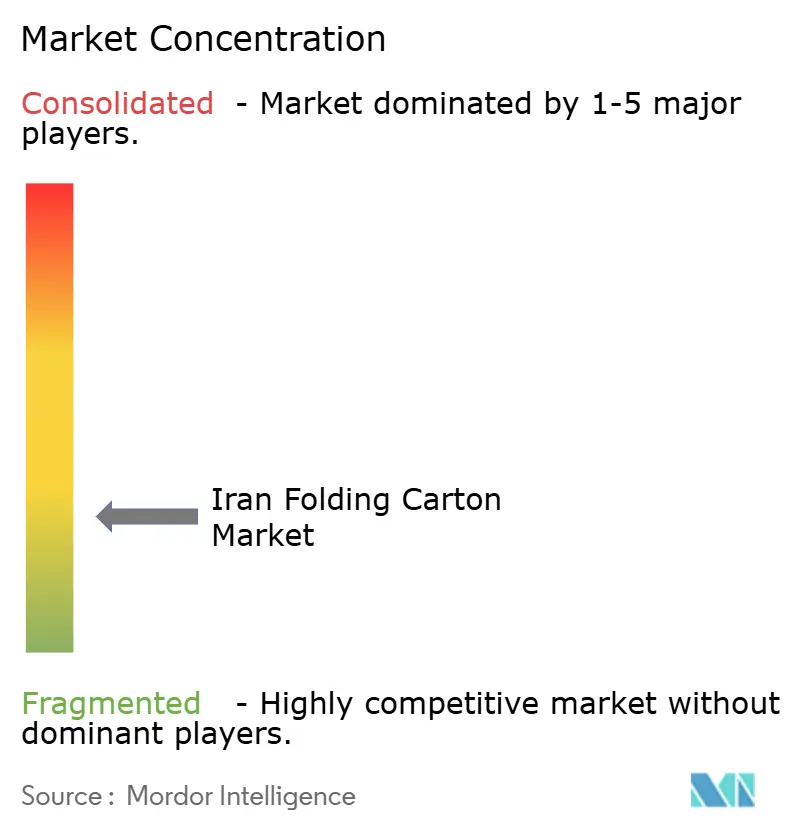

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iran Folding Carton Market Analysis by Mordor Intelligence

The Iran folding carton market size increased from USD 183.37 million in 2025 to USD 194.38 million in 2026 and is expected to reach USD 276.21 million by 2031, growing at a 7.28% CAGR over 2026-2031. Continued surplus in domestic cartonboard production, rapid e-commerce growth, and a resilient food-processing sector support demand even as sanctions limit access to advanced equipment. Rising online sales have shifted order profiles toward short-run, retail-ready cartons, while pharmaceutical cold-chain expansion is moving converters toward high-barrier substrates and serialization capability. Government incentives for agro-based and recycled fibers, combined with bagasse pulp investments, help offset volatility in imported pulp, though energy rationing and foreign-exchange shortages still disrupt production schedules. Competitive pressure remains intense because roughly 1,500 converters operate below optimal scale, forcing firms to differentiate through vertical integration, digital printing, and premium finishing.

Key Report Takeaways

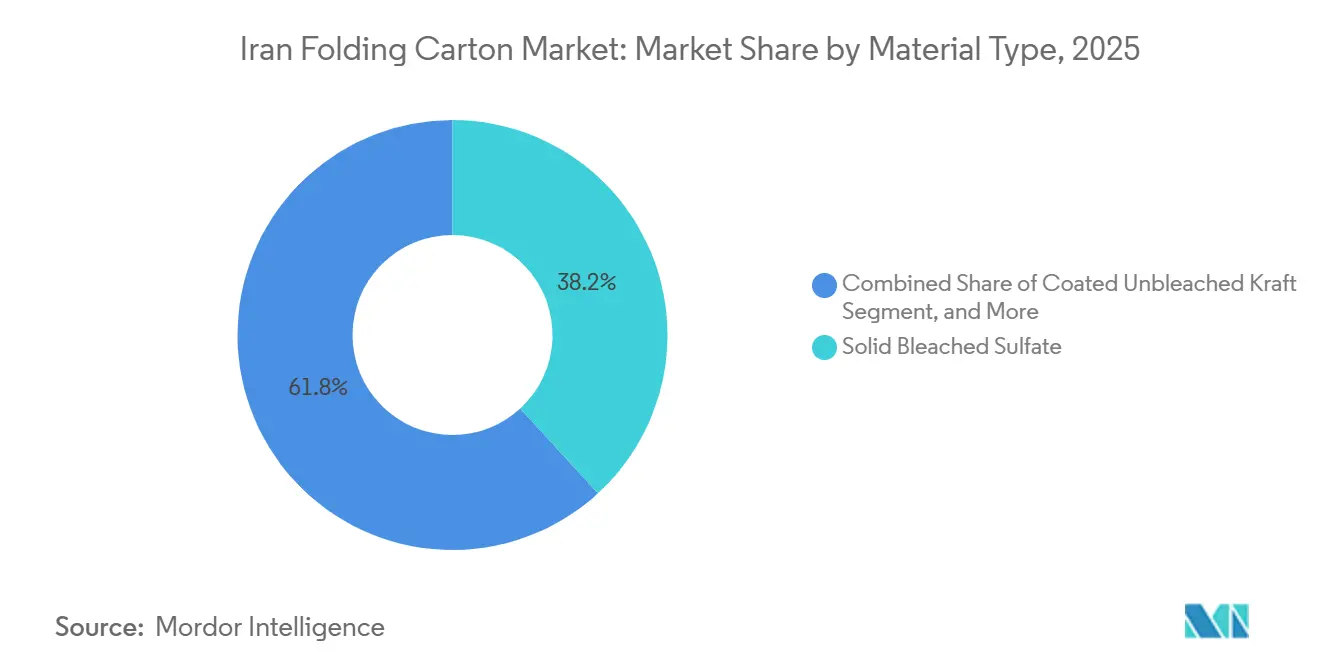

- By material type, solid bleached sulfate captured with 38.16% of the Iran folding carton market share in 2025.

- By printing technology, the Iran folding carton market size for digital printing is projected to grow at a 9.37% CAGR to 2031.

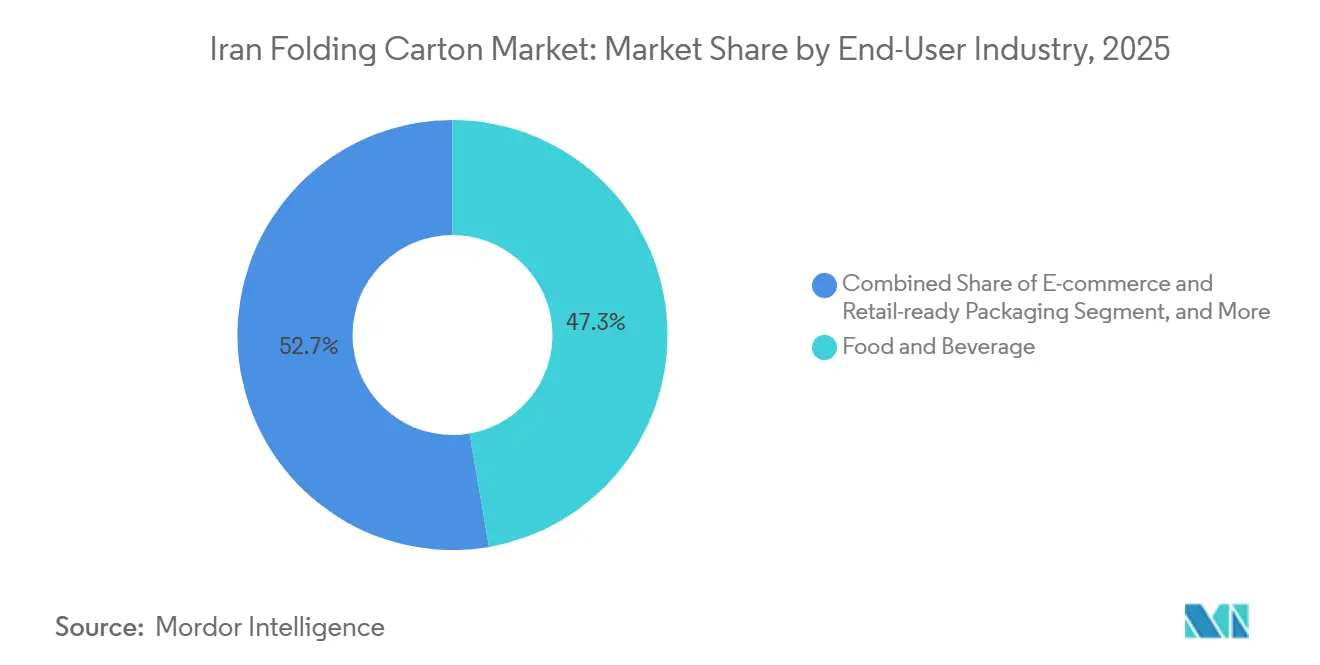

- By end-user industry, the food and beverage industry captured 47.29% of the Iran folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Iran Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand from the Food and Beverage Sector | +2.1% | Tehran, Isfahan, Qazvin industrial clusters | Medium term (2-4 years) |

| Growth of Iran's E-Commerce Sector Driving Retail-Ready Packaging | +1.8% | National, extending into regional and rural markets | Short term (≤ 2 years) |

| Government Incentives for Domestic Pulp Production | +1.2% | Khuzestan, Zanjan, Yazd | Long term (≥ 4 years) |

| Increasing Adoption of Digital Printing for Customization | +0.9% | Tehran, Qazvin, and Isfahan converter hubs | Medium term (2-4 years) |

| Expansion of Pharmaceutical Cold Chain Requiring High-Barrier Cartons | +0.7% | Tehran, Karaj | Medium term (2-4 years) |

| Development of Agro-Based Bagasse Pulp Capacity | +0.6% | Khuzestan, southern Iran | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from the Food and Beverage Sector

Dairy processors handled 8.5 million metric ton of milk annually, generating sustained demand for folding cartons for liquid milk, cheese, and powdered products.[1]Milkypedia Team, “Iran's Dairy Industry Overview,” DAIRYNEWS.TODAY, dairynews.today Cheese and butter exports climbed 32% in value during the quarter ending June 2025, driving demand for export-grade secondary packaging that must comply with EAEU rules. Large processors such as Pegah, Kalleh, and Mihan anchor high-volume contracts requiring grease-resistant Coated Unbleached Kraft. Confectionery shipments, forecast to reach USD 150 million by 2026, underpin premium gift-box orders. Rising freight and energy costs are tightening producer margins, so converters focus on lightweight designs and material efficiency to preserve barrier performance without raising unit costs.

Growth of Iran's E-Commerce Sector Driving Retail-Ready Packaging

Online transaction value jumped 72% to 5.5 quadrillion toman in 2024 on 4.7 billion payments. This surge spreads carton demand beyond Tehran into small cities and villages, favoring short-run, branded boxes that simplify returns and last-mile handling. Courier networks enlarged same-day capacity, motivating lightweight, stackable formats. Converters accelerate digital-press adoption by enabling sellers to offer personalized packs with no minimum order quantity. Anticipated labeling and traceability rules using QR codes further lift variable-data printing.

Government Incentives for Domestic Pulp Production

The February 2024 waste-reduction directive grants tax credits equal to R&D spend and National Development Fund loans for recycling or technology upgrades. Plantation plans targeting 70,000 hectares of poplar and eucalyptus, irrigated with wastewater, aim to close the local wood-fiber gap. Khuzestan’s Pars Paper exemplifies the policy by expanding bagasse- and recycled-fiber lines and trimming foreign-currency outflows tied to virgin pulp. Water scarcity nevertheless limits plantation expansion beyond designated zones.

Increasing Adoption of Digital Printing for Customization

Converters such as Nami Naghsh offer roll and sheet digital printing with nationwide shipment, enabling buyers to run micro-batches for e-commerce, pharma, and start-ups. The 9.37% CAGR outlook reflects advantages in setup waste, turnaround, and variable graphics. Legacy lithographic lines still dominate high-volume food orders, but hybrid workflows that overprint variable data on lithographic bases allow cost control while meeting serialization rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| International Sanctions Hindering Machinery Procurement | -1.4% | All industrial clusters | Long term (≥ 4 years) |

| Volatility In Imported Virgin Pulp Prices | -1.1% | Tehran, Isfahan, Qazvin converter hubs | Short term (≤ 2 years) |

| Water Scarcity Limiting Mill Capacity Expansion | -0.8% | Yazd, Kerman, central and southern provinces | Long term (≥ 4 years) |

| Stringent Ink Effluent Waste Regulations Raising Compliance Costs | -0.5% | Tehran, Qazvin, Isfahan printing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

International Sanctions Hindering Machinery Procurement

Banking restrictions and export-control rules delay access to European presses and finishing lines, forcing many firms to rely on used equipment from Turkey or China. A 2026 study covering 120 managers found that sanctions accounted for 57.6% of the variance in supply-chain performance. The lag curbs automation uptake, widens the technology gap between large integrated plants and small converters, and limits Iranian exporters’ ability to match regional quality benchmarks.

Volatility In Imported Virgin Pulp Prices

Dependence on imported pulp, forecast at 450,000 metric ton in 2021, exposes converters to global price swings and real depreciation. Global pulp costs added 7% between April and July 2025, compressing margins. Oil price spikes during the 2026 Strait of Hormuz crisis raised energy and plastic alternatives, but also inflated paperboard production expenses. Firms with bagasse or recycled-fiber integration, such as Pars Paper, buffer shocks, yet most converters remain price-takers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Grades Gain on Food-Contact Demand

Solid Bleached Sulfate captured the largest 38.16% share of Iran folding carton market in 2025 due to its brightness and printability. Coated Unbleached Kraft, which offers grease resistance, is projected to expand at a 8.67% CAGR, boosting its contribution to the Iran folding carton market through ready-meal and dairy applications. Folding Boxboard balances stiffness and price for household appliances, whereas White Line Chipboard leverages the 1.0-1.2 million-metric-ton wastepaper stream to serve price-sensitive retail packs. The government plans to double fast-growing plantations and expand bagasse capacity to strengthen the local fiber supply, yet arid climates and water stress slow progress.

Domestic mills such as Modern Paper’s 120,000 metric ton kraft liner line in Yazd and Pars Paper’s bagasse operation in Khuzestan illustrate vertical integration that shields converters from currency swings. These mills also position suppliers for Extended Producer Responsibility fees that may favor recycled or agro-based content. Nonetheless, high-barrier imported boards still dominate premium pharma and cosmetics boxes, meaning the Iran folding carton market continues to balance local sustainability goals with performance requirements.

By Printing Technology: Digital Edges Forward Amid Lithographic Dominance

Lithographic presses held 42.75% of the Iran folding carton market share in 2025, underpinned by high-volume food contracts that require consistent multicolor reproduction. Flexography maintains a broad footprint for corrugated and medium-volume cartons, offering eight- to twelve-color versatility across firms like IranZamin Group.[2]IranZamin Group Product Brochure, “Helio and Flexo Printing,” IRANZAMIN GROUP, iranzamingroup.com Digital presses grow at a 9.37% CAGR as converters serve e-commerce brands seeking personalized packs, while gravure remains a niche for ultra-long runs due to cylinder costs.

Events such as the 32nd Tehran Printing and Packaging Exhibition, with 360 exhibitors, also advance technology transfer and joint venture talks. Yet sanctions mean many mid-tiers still import refurbished equipment, limiting productivity gains. Hybrid workflows that overlay variable data onto lithographic bases help balance cost and customization, ensuring competitiveness in the Iran folding carton market without compromising run-length economics.

By End-User Industry: E-Commerce Reshapes Demand Mix

Food and Beverage retained a dominant 47.29% share of the Iran folding carton market in 2025, driven by dairy, confectionery, and beverage filling lines. Iran’s butter exports to Kazakhstan rose 64% in the seven months to July 2025, with demand for export-grade cartons compliant with EAEU codes. E-commerce and Retail-ready Packaging are expected to post the fastest 8.61% CAGR through 2031, driven by rural online shopping penetration.

Folding cartons now combine protective features with shelf appeal, and digital print enables QR-code returns flows. Healthcare and Pharmaceuticals also expand carton adoption as oncology cold-chain and serialization rules proliferate; 114 drug factories rely on high-barrier cartons aligned with ISO 15378. Premium cosmetics, electronics, and tobacco niche packs layer foil, embossing, and spot UV to capture brand value, reflecting bifurcated demand across mass and luxury tiers in the Iran folding carton market.

Geography Analysis

Tehran dominates converter capacity, hosts 55 packaging companies, provides immediate access to food and drug plants, and offers logistics links via Imam Khomeini Port. Qazvin’s Asan Pack runs an 80,000-metric-ton corrugated site supplying multinationals such as Nestlé and Samsung. Isfahan’s Moghadam facility broadens its product line to 40 items, signaling an export orientation toward Russia and Central Asia.

Yazd houses Modern Paper’s linerboard mill and integrated corrugation, while Tabriz’s Zibanaghsh operates 9-color gravure and Nordmeccanica laminators. Khuzestan’s Haft Tappeh hosts Pars Paper, the Middle East’s largest bagasse pulp plant feeding converters nationwide.[3]TradingEconomics Data Team, “Iran Exports of Paper and Paperboard to Afghanistan,” TRADINGECONOMICS, tradingeconomics.com Northern provinces face fiber shortfalls following the natural-forest harvest ban, reinforcing the need for plantation and recycled-fiber strategies.

Export flows rely on land routes to Afghanistan and Armenia; Iran shipped USD 16.05 million in cartons and paperboard articles to Afghanistan in 2022. Sanctions complicate payments, but regional buyers value Iranian board surplus, sustaining cross-border demand even as domestic energy rationing occasionally disrupts supply. The resilience of this demand highlights the strategic importance of Iran's board surplus in the regional market.

Competitive Landscape

Roughly 1,500 folding-carton units and 150,000 small enterprises create a low-concentration arena in which no player dominates the overall folding carton market share in Iran. Large integrated firms pursue three strategic paths: scale and multinational contracts, fiber integration, and technology leadership in digital and flexo. Financial data highlight aggressive leverage; Iran Carton’s debt-to-equity ratio reached 1,756% in Q2 2026, though revenue grew 83.52%.

Iran Packing Industries reported EBITDA growth of 233.45% in Q3 2025, but 16,639% leverage underscores financing challenges.[4]EMIS Analysts, “Iran Carton Company Financials,” EMIS, emis.com Mid-tier converters import used presses via the United Arab Emirates, accepting maintenance burdens. Environmental differentiation emerges: Kavir Moghava Ardestan recycles 95% of process water and irrigates a one-million-sapling plantation, positioning for future Extended Producer Responsibility enforcement.

Competitive intensity will rise as tax-credit programs fund recycling tech, favoring players with closed-loop systems and bagasse or recycled-fiber lines. Digital print specialists serving e-commerce brands capture customization premiums, while legacy lithographic plants seek regional export contracts to fill excess capacity. These contracts help mitigate the challenges posed by declining domestic demand for lithographic printing services.

Iran Folding Carton Industry Leaders

Irani Papel e Embalagem S.A.

Mayr-Melnhof Karton AG

Papyrus Kaveh Paper Company

Asan Pack Company

Ojenili Print & Packaging Complex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Iran Carton Company posted 83.52% revenue growth and 36.26% asset expansion, confirming surging carton demand across food and pharma segments.

- December 2025: The 32nd Tehran International Printing and Packaging Exhibition gathered 360 exhibitors and 40 foreign companies, facilitating machinery and consumable deals.

- June 2025: Kaveh Paper Industries recorded 130.3% sales growth as fluting paper uptake rose across corrugated supply chains.

- February 2025: Government issued waste-reduction directive granting R and D tax credits and National Development Fund loans for recycling upgrades, accelerating domestic fiber substitution.

Iran Folding Carton Market Report Scope

The Iran folding carton market refers to the industry that produces and distributes paperboard-based packaging solutions in Iran. The scope of this study includes an in-depth analysis of the Iran folding carton market, focusing on market dynamics, trends, and growth opportunities. The study also provides insights into market drivers and restraints, as well as forecasts for the defined study period.

The Iran Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and projected size of the Iran folding carton market?

The Iran folding carton market size reached USD 194.38 million in 2026 and is projected at USD 276.21 million by 2031, reflecting a 7.28% CAGR.

Which segment holds the largest Iran folding carton market share by printing technology?

Lithographic Printing led with 42.75% share in 2025, serving long-run food and beverage contracts.

Why is Coated Unbleached Kraft growing faster than other material grades?

It meets grease-resistance demands in dairy and ready-meal packaging, supporting an 8.67% CAGR forecast through 2031.

How are sanctions affecting folding carton converters?

Sanctions restrict access to new presses and banking channels, raising capital expenditure and widening the technology gap among converters.

What drives the surge in e-commerce folding cartons?

A 72% jump in online transaction value in 2024 has accelerated demand for short-run, retail-ready cartons with personalized graphics and easy returns.

Which geographic clusters account for most converter capacity?

Tehran remains the primary hub, followed by Qazvin, Isfahan, Tabriz, Yazd, and Khuzestan, each hosting significant paper or converting facilities.

Page last updated on: