Italy Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

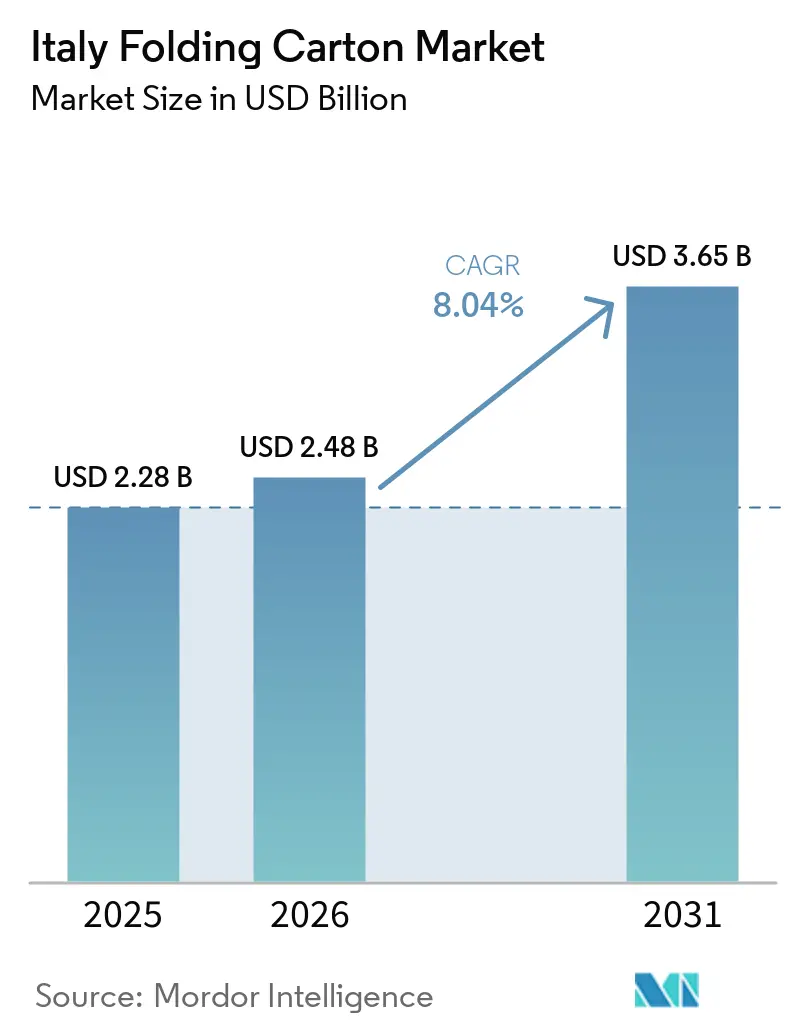

| Base Year Market Size (2025) | USD 2.28 Billion |

| Market Size (2026) | USD 2.48 Billion |

| Market Size (2031) | USD 3.65 Billion |

| Growth Rate (2026 - 2031) | 8.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Folding Carton Market Analysis by Mordor Intelligence

The Italy folding carton market size is expected to increase from USD 2.28 billion in 2025 to USD 2.48 billion in 2026 and reach USD 3.65 billion by 2031, growing at a CAGR of 8.04% over 2026-2031. Structural demand is accelerating as the European Union’s recyclability thresholds converge with brand-owner pledges to phase out non-recyclable plastics, while e-commerce parcel growth amplifies the need for lightweight, protective secondary packs. Converters that combine barrier-coating expertise with rapid digital-press changeovers are widening price-performance gaps against offset-only peers. Brand-owner migration from rigid plastics to fiber substrates, together with retailer mandates for shelf-ready multipacks, is expanding the addressable pool of applications faster than domestic capacity additions. Pulp-price volatility remains the primary cost headwind, yet vertically integrated mills with in-house deinking and R&D facilities are partially insulating margins by locking in long-term supply contracts.

Key Report Takeaways

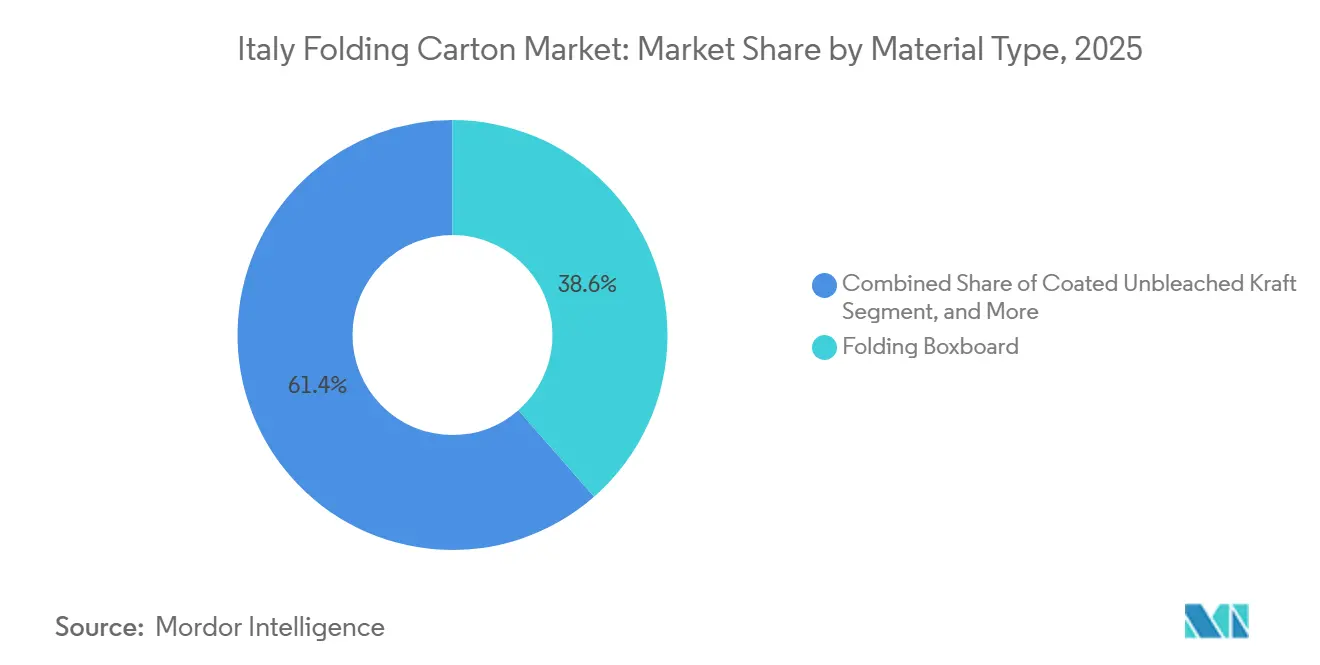

- By material type, folding boxboard captured with 38.56% of the Italy folding carton market share in 2025.

- By printing technology, the Italy folding carton market size for digital platforms is projected to grow at a 9.73% CAGR to 2031.

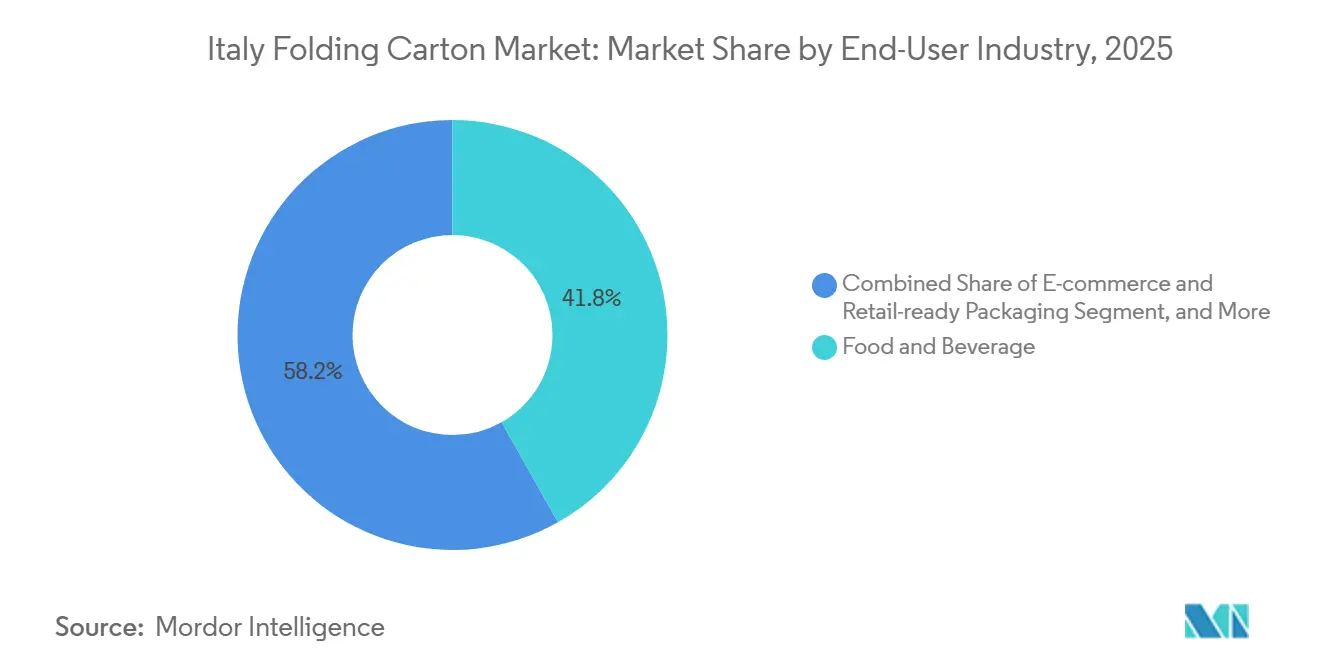

- By end-user industry, the food and beverage industry captured 41.84% of the Italy folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Preference for Recyclable Packaging | +2.1% | National, concentrated in Lombardy, Veneto, Emilia-Romagna | Long term (≥ 4 years) |

| Growth of Premium-Positioned FMCG Products | +1.8% | National, premium clusters in Milan, Rome, Florence | Medium term (2-4 years) |

| E-commerce Boom and Small-Batch Custom Runs | +1.6% | National, hubs in Bologna, Milan, Verona | Short term (≤ 2 years) |

| Brand Owner Migration From Plastics to Paperboard | +1.4% | National, led by multinational FMCG and cosmetics brands | Medium term (2-4 years) |

| Expansion of Italy’s Ready-to-Eat Meal Segment | +0.9% | Urban centers in Northern and Central Italy | Medium term (2-4 years) |

| Retailer Demand for Shelf-Ready Multipacks | +0.7% | National, driven by Coop, Esselunga, Conad | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Preference for Recyclable Packaging

Extended Producer Responsibility fees imposed by CONAI penalize non-recyclable structures, so brand owners are rapidly substituting laminated plastics with mono-material cartons that qualify for lower tariffs.[1]CONAI, “Extended Producer Responsibility and Packaging Contributions,” CONAI.ORG Consumer polling shows that 77% of Italians factor packaging sustainability into their purchase decisions, prompting retailers to favor SKUs with clear disposal labels. Fedrigoni’s 2025 investment in Papkot demonstrates how converters are commercializing PFAS-free coatings that pass recyclability guidelines while retaining grease resistance. The national recovery plan earmarks EUR 1.5 billion (USD 1.70 billion) for reuse centers and digital traceability, which will raise post-consumer fiber availability once projects come online. These factors are expected to underpin above-trend substrate demand through at least 2031.

Growth of Premium-Positioned FMCG Products

Premium food, beverage, and cosmetics lines increasingly specify solid bleached sulfate or metalized boards that tolerate hot-foil stamping, embossing, and soft-touch varnishes. Ready-to-eat meal kits valued at EUR 2.5 billion (USD 2.83 billion) require grease-resistant, microwave-safe cartons that command double-digit price premiums over commodity grades. Retail private-label penetration reached 32% in 2024, yet supermarkets differentiate premium tiers through upgraded pack aesthetics. Converters that add inline spectrophotometers and automated inspection, such as Bobst QualiTronic systems, achieve the tighter color tolerances demanded by luxury brands. As discretionary spending recovers, volumes in high-decor segments are expected to outpace the overall Italy folding carton market.

E-commerce Boom and Small-Batch Custom Runs

Parcel volumes grew 5.7% year-on-year to 572 million in H1-2025, shrinking median order sizes to roughly 8,000 units per SKU. Digital presses such as Bobst DIGITAL MASTER 55 complete job changeovers in 15 minutes, cutting production time by up to 80% for sub-1,000-sheet runs. Variable-data printing enables personalized graphics and QR codes that amplify unboxing experiences, a key driver of repeat e-commerce purchases. Co-located converter-fulfillment sites in Bologna and Milan are reducing lead times and working capital requirements for direct-to-consumer brands. Digital-ready capacity is therefore emerging as a decisive competitive lever within the Italian folding carton market.

Brand Owner Migration from Plastics to Paperboard

Penalties up to EUR 25,000 (USD 28,250) for breaching Italy’s Single-Use Plastics rules have accelerated the phase-out of rigid plastic clamshells. Water-based barrier coatings containing chitosan and carnauba wax now achieve oil- and moisture-resistance levels suitable for refrigerated foods. Folding cartons engineered with micro-flute inserts meet drop-test thresholds once exclusive to plastics, enabling substitution in electronics packaging. The 2024 ban on bisphenol A further narrows compliant plastic options for infant nutrition and beverage packs, so converters offering PFAS-free liners are securing long-term supply agreements. Collectively, these shifts are projected to add 1.4 percentage points to the CAGR of the Italy folding carton market through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Fiber Pulp Prices | -1.2% | National, exposure highest among non-integrated SMEs | Short term (≤ 2 years) |

| Capital-Intensive Nature of High-End Digital Presses | -0.8% | National, hurdle greatest for SMEs in Southern Italy | Medium term (2-4 years) |

| Limited Folding Carton Recycling Infrastructure in the South | -0.5% | Sicily, Calabria, Campania | Long term (≥ 4 years) |

| Stringent Food-Contact Compliance Costs for SMEs | -0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Fiber Pulp Prices

Kraftliner rose more than 20% in 2024, while northern bleached softwood pulp climbed 17.6%, compressing converter margins because pass-through clauses lag spot prices by up to 90 days. Recycled-content mandates intensify competition for recovered paper, which averaged EUR 120-150 (USD 136-170) per tonne in Northern Italy during 2025. Southern regions’ lower collection rates force mills to truck bales north-to-south, adding logistics premiums. Vertically integrated groups like RDM and Burgo hedge volatility through captive pulp and deinking capacity, but most SMEs remain price takers, dampening investment appetite.

Capital-Intensive Nature of High-End Digital Presses

A fully configured DIGITAL MASTER 55 exceeds EUR 3 million (USD 3.39 million), a sum most converters below EUR 10 million (USD 11.14 million), turnover cannot self-finance. Leasing penetration trails Northern Europe, so Italian SMEs typically fund two-thirds of capex from internal cash, stretching payback periods to six years. Skills shortages further delay adoption; ITS Rizzoli graduates fewer than 250 packaging-technician students annually, well below demand. Without targeted subsidies, an estimated 8-12% of converters could exit the Italy folding carton market by 2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Content Drives Specification Shifts

Folding boxboard accounted for 38.56% of the Italian folding carton market size in 2025, favored for balanced stiffness, printability, and cost in mainstream food applications. Solid bleached sulfate is forecast to post a 9.21% CAGR as cosmetics and pharma brands demand high-brightness surfaces compatible with hot-foil, emboss, and barrier coatings. White line chipboard, produced from recycled fibers, is gaining traction in electronics and household goods where surface aesthetics are secondary. RDM’s Vincicoat PLUS, launched in 2026, incorporates 85% recycled fibers yet delivers 15-20% greater strength, illustrating the innovation trajectory toward lightweight, circular substrates.

Producers recasting mills for higher recycled-content output are pre-positioning for the PPWR’s 30% post-consumer target, a shift expected to realign procurement toward mills offering validated closed-loop fibers. Competitive emphasis is moving to coatings that preserve recyclability, with Papkot’s nanostructured liner replacing PFAS while maintaining grease resistance. Substrates with non-cellulosic layers below 5% qualify for CONAI’s lowest fee bracket, nudging buyers toward dispersion-coated or bio-based alternatives. As brand owners publish carbon footprints, mills offering cradle-to-gate emissions data gain sourcing preference, reinforcing a virtuous cycle that favors high-recycled-content grades within the Italy folding carton market.

By Printing Technology: Digital Adoption Redefines Run-Length Economics

Lithographic presses retained 42.76% of the Italian folding carton market share in 2025, unrivaled for runs above 20,000 sheets, where plate amortization outperforms click-charge models. Digital’s forecast 9.73% CAGR stems from configuration agility: the DIGITAL MASTER 55 hits 100 meters per minute and 15-minute changeovers, slashing waste and setup for personalized campaigns.[2]PrintPUB, “Bobst DIGITAL MASTER 55,” PRINTPUB.NET Hybrid workflows emerge, with offset producing base graphics while inkjet heads overprint regional codes or limited-edition visuals.

Flexographic systems, armed with HD photopolymer plates and low-VOC inks, are reclaiming corrugated micro-flute work where water-based inks support food-contact mandates. Pressroom automation is critical; Cartotecnica Garanzini’s Rapida 145 with fully automatic plate change and inline spectrophotometry cuts make-ready waste and meets color delta tolerances demanded by multinationals. As run lengths continue to fragment, converters offering mix-and-match platforms will capture margin, positioning digital capacity as a prerequisite for defending share in the evolving Italian folding carton market.

By End-User Industry: Omnichannel Distribution Shifts Demand Patterns

Food and beverage led 2025 demand at 41.84%, propelled by premium confectionery, organic produce, and microwave-ready meals that need grease barriers and tamper-evident closures. E-commerce and retail-ready formats are projected to outgrow all other verticals at a 10.05% CAGR, reflecting direct-to-consumer models and supermarket mandates for shelf-ready packs that lower labor costs. Pharmaceutical cartons must carry Data Matrix codes and tamper seals ahead of the 2027 Falsified Medicines Directive deadline, pushing converters to install inline vision systems. Cosmetics prioritize solid bleached sulfate with soft-touch coatings to reinforce luxury cues, while electronics buyers request drop-tested structures with micro-flute inserts.

Retailers such as Coop exceeded 80% of private-label packaging being recyclable by 2024, steering suppliers toward FSC-certified substrates. Ready-to-eat meal growth intersects with sustainability, demanding ovenable boards that withstand grease and steam while meeting recyclability standards. As omnichannel strategies fuse store and online channels, converters balancing protective transit functions with shelf charisma will capture the highest-margin growth slices of the Italy folding carton market.

Geography Analysis

Northern Italy’s industrial triangle, Lombardy, Veneto, Emilia-Romagna, hosted 62% of capacity in 2025 thanks to dense FMCG clusters, supplier ecosystems, and vocational institutes. Milan-Bergamo’s packaging district anchors multinationals like Smurfit WestRock, which leverage centralized procurement and multi-plant scheduling. Veneto’s converters benefit from Bobst’s Florence training center, which speeds the deployment of digital fold-and-glue platforms.

Central regions, notably Tuscany and Lazio, specialize in high-brightness specialty boards for cosmetics and pharmaceuticals, leveraging Fedrigoni’s paper mills. Although capacity is lower, profit per tonne is higher due to a premium-grade mix. The South lags; Sicily’s 50.7 kilograms per capita collection rate trails the national average of 65.4 kilograms, limiting recycled-fiber supply and increasing inbound freight costs. SMEs there also face higher borrowing costs, which curb the adoption of digital press.[3]Italian Ministry of Economic Development, “NRRP Funding,” MISE.GOV.IT

Government funds for recycling infrastructure flow disproportionately southward, yet commissioning lags push real gains beyond 2028. As a result, Northern clusters will continue to attract the lion’s share of new investments, consolidating their dominance in the Italian folding carton market. Emilia-Romagna’s logistics corridors integrate carton plants with fulfillment hubs, shortening e-commerce lead times. This regional advantage is expected to drive sustained growth in the northern folding carton industry.

Competitive Landscape

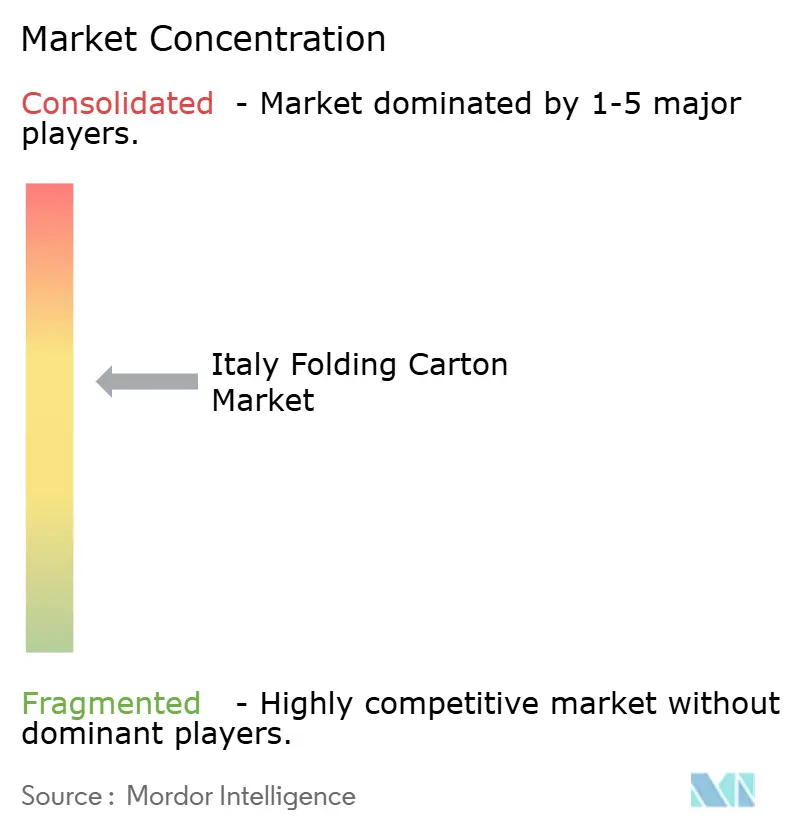

The top 10 producers captured 48% of 2025 revenue, making the field moderately concentrated. Multinationals such as Smurfit WestRock, Mayr-Melnhof Karton, and Graphic Packaging International deploy pan-European networks to balance load and hedge pulp exposure. Mid-tier Italian specialists Lucaprint, Box Marche, Pozzoli, and GPack Group compete on agility, customization, and proximity. The competitive landscape reflects a mix of global players and regional specialists, each employing distinct strategies to maintain market share.

Lucaprint’s twin acquisitions and Packway ERP roll-out exemplify the scale-driven quest to amortize digital-press capex.[4]Lucaprint, “Company Profile,” LUCAPRINT.IT Technology is the new battleground. Bobst’s all-in-one DIGITAL MASTER 55 and upgraded EXPERTFOLD lines, with SPHERE HMI, increase productivity by 25%. Fedrigoni’s minority stake in Papkot positions it to supply PFAS-free liners ahead of upcoming restrictions. These advancements highlight the industry's focus on innovation and regulatory compliance.

BRC food-safety certification, held by under one-third of converters, is fast becoming a gatekeeper for high-margin food deals. Digital-native entrants co-locating with 3PL warehouses threaten incumbents by offering next-day printed cartons at competitive prices. Consolidation momentum is expected to eliminate up to 12% of smaller firms lacking capital for digital transitions, nudging the Italy folding carton market toward higher concentration by 2031.

Italy Folding Carton Industry Leaders

Stora Enso Oyj

International Paper Company

Mayr-Melnhof Karton AG

Graphic Packaging International LLC

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Smurfit WestRock completed the acquisition of CARTOMANABI S.A. to expand South American folding-carton coverage and support global customer footprints.

- February 2026: RDM Group launched Vincicoat PLUS, an 85% recycled-content coating that raises strength 15-20% and trims board weight by up to 20% to meet PPWR targets.

- November 2025: Bobst introduced SPHERE-enabled upgrades for EXPERTFOLD 145 and 165 folder-gluers, boosting SPEEDPACK productivity by 25%.

- October 2025: Fedrigoni announced a restructuring that separates its paper, label, and RFID units into standalone companies to enable sharper capital allocation.

Italy Folding Carton Market Report Scope

The Italy Folding Carton Market encompasses the production, distribution, and use of folding cartons, which are paperboard-based packaging solutions widely used across industries such as food and beverage, personal care, and pharmaceuticals. These cartons are known for their lightweight, recyclability, and versatility, making them a preferred choice for packaging applications.

The Italy Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the projected size of the Italy folding carton market by 2031?

The Italy folding carton market size is forecast to reach USD 3.65 billion by 2031, expanding at an 8.04% CAGR from 2026 to 2031.

Which material type is growing fastest within Italy’s folding carton segment?

Solid bleached sulfate cartons are expected to outpace other substrates with a 9.21% CAGR through 2031, driven by luxury cosmetics and pharmaceutical demand.

How will digital printing affect Italian folding-carton production economics?

Digital presses such as Bobst’s DIGITAL MASTER 55 enable 15-minute job changeovers and cost-effective short runs, positioning converters to capture e-commerce and personalized packaging work.

Why is pulp price volatility a major concern for Italian converters?

Kraft liner and softwood pulp prices rose more than 17% in 2024, eroding margins for non-integrated converters that cannot immediately pass costs to brand owners.

Which Italian regions account for most folding-carton capacity?

Lombardy, Veneto, and Emilia-Romagna collectively house roughly 62% of national capacity due to dense FMCG clusters, skilled labor, and supplier ecosystems.

What regulatory changes are driving material substitution from plastics to cartons?

The EU Single-Use Plastics Directive and the 2024 bisphenol A ban impose penalties on non-compliant plastics, pushing brand owners toward recyclable, PFAS-free folding cartons.

Page last updated on: