Robot Dog Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

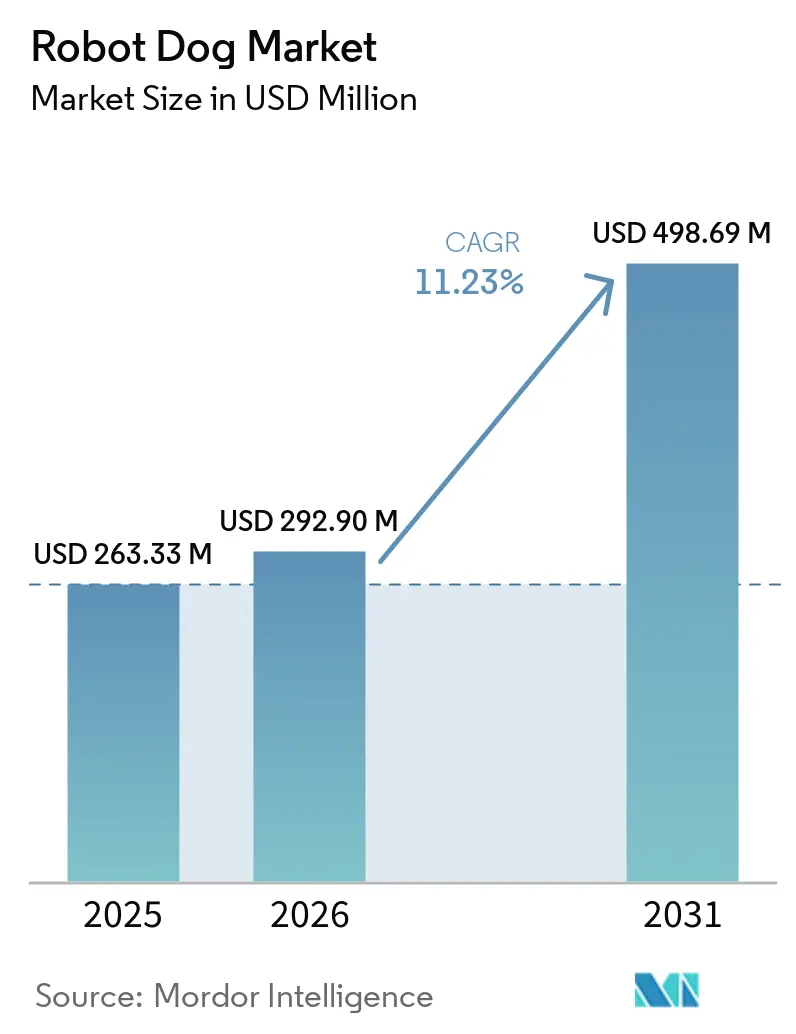

| Market Size (2026) | USD 292.90 Million |

| Market Size (2031) | USD 498.69 Million |

| Growth Rate (2026 - 2031) | 11.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robot Dog Market Analysis by Mordor Intelligence

The Robot Dog Market size is projected to expand from USD 263.33 million in 2025 and USD 292.90 million in 2026 to USD 498.69 million by 2031, registering a CAGR of 11.23% between 2026 to 2031.

Growth now reflects broader movement from pilots to scaled workflows in hospitals where four-legged platforms support inspection, routine security rounds, and patient interaction. The robot dog market is benefiting from staffing gaps that have reshaped how providers allocate time to non-clinical tasks, with automation targeted at logistics, compliance checks, and continuous monitoring rather than bedside care. Commercial traction is strongest where workflows are predictable, and safety-critical risks are low, while regulated use cases move forward as vendors align with established medical QMS and cleanroom standards. The robot dog market also shows a distinct split between high-spec systems sold with full software stacks and lower-cost units tailored by integrators through SDKs and partner ecosystems. Regional momentum continues to diverge as North America scales deployments while Asia Pacific accelerates production, cost optimization, and field trials that expand the range of viable clinical and facilities tasks.

Key Report Takeaways

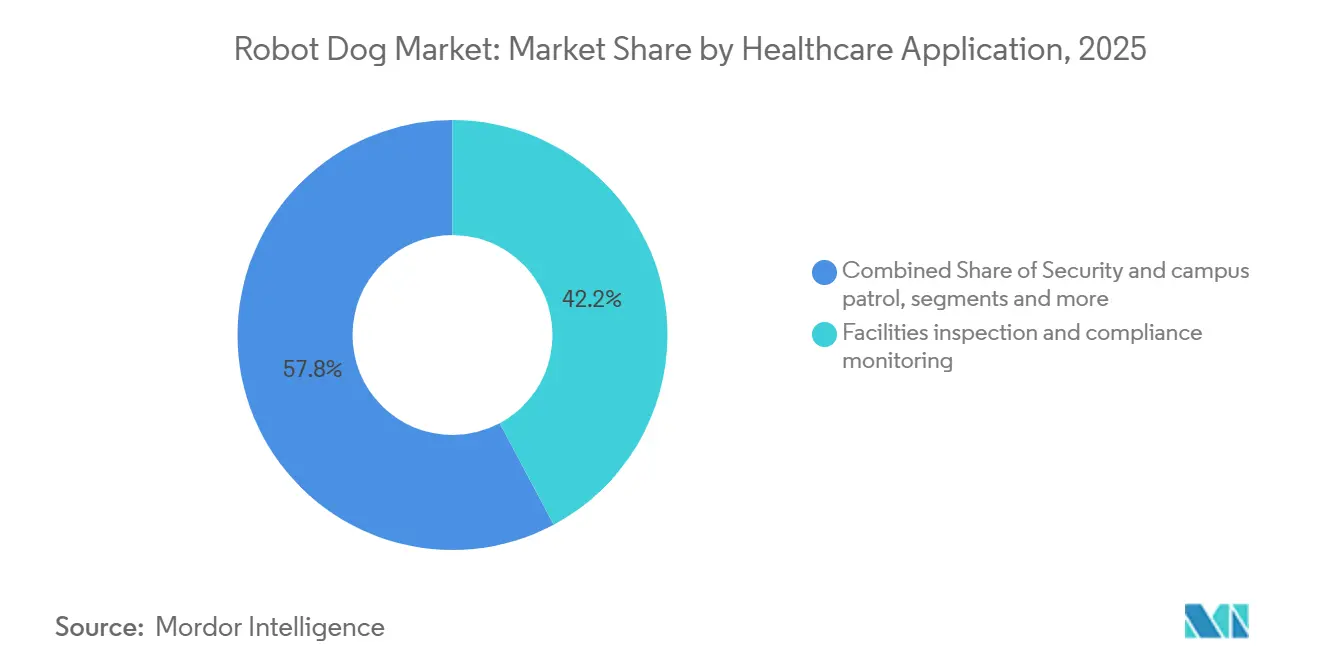

- By healthcare application, facilities inspection led with 42.19% revenue share in 2025, while security and campus patrol is forecast to grow at a 12.89% CAGR through 2031.

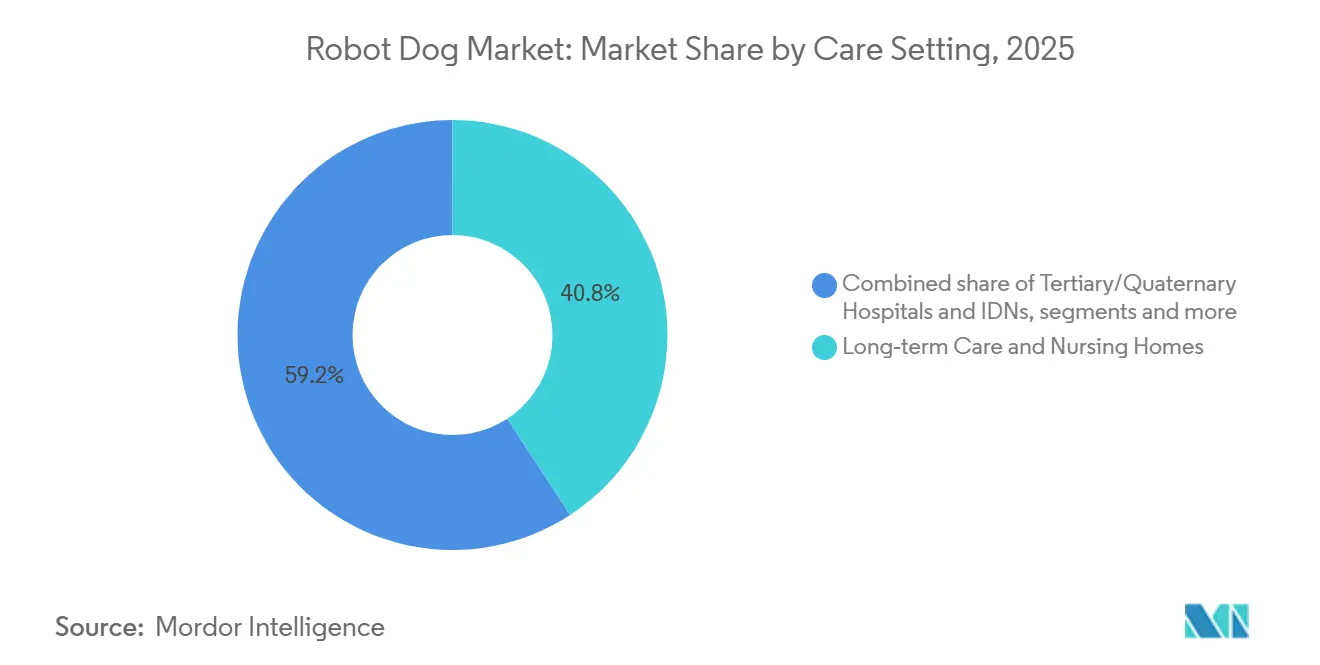

- By care setting, long term care accounted for 40.78% share in 2025, as behavioral health is projected to record the fastest 12.08% CAGR through 2031.

- By autonomy level, remote controlled systems held 51.23% share in 2025, and semi autonomous robots are expected to advance at a 13.21% CAGR through 2031.

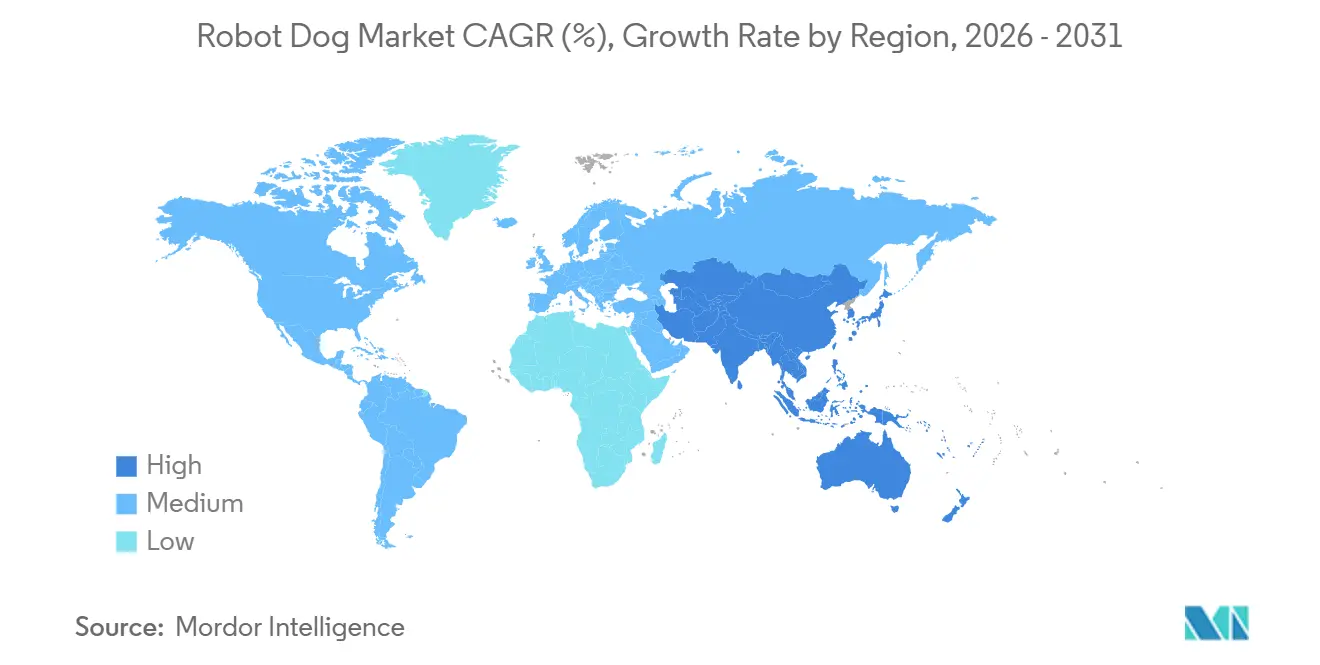

- By geography, North America held 45.44% share in 2025, and Asia Pacific is projected to be the fastest growing region at a 13.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Robot Dog Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Healthcare staffing shortages and rising labor costs push automation for non-clinical tasks | +3.2% | Global, with acute pressure in North America, Japan, Western Europe | Medium term (2-4 years) |

| Infection control and staff safety needs in isolation and critical environments | +2.8% | Global, elevated in urban tertiary hospitals and pandemic-preparedness frameworks | Medium term (2-4 years) |

| Hospital campus security and emergency readiness require 24/7 autonomous patrols | +2.5% | North America and EU core, spill‑over to APAC metro hospitals | Short term (≤ 2 years) |

| AI navigation and sensor fusion enable reliable indoor–outdoor hospital operations | +2.1% | Global, led by facilities with digital infrastructure and Wi‑Fi/5G coverage | Long term (≥ 4 years) |

| Cleanroom/Bio‑safety routines and audit trails for labs and pharmacies | +1.4% | Concentrated in pharmaceutical manufacturing hubs in North America, EU, China | Long term (≥ 4 years) |

| Therapeutic engagement in pediatrics/geriatrics reduces sitter burden | +0.9% | APAC early adopters, North America research institutions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Healthcare Staffing Shortages and Rising Labor Costs Push Automation for Non Clinical Tasks

Hospitals continue to rebalance work across clinical and non clinical roles, which elevates demand for mobile platforms that move specimens, deliver supplies, and perform routine rounds. The robot dog market fits this operational shift because quadrupeds can traverse stairs and uneven surfaces that limit wheeled carts, so coverage extends to basements, ramps, and outdoor connectors. Providers are standardizing on units that deliver 24/7 uptime for repetitive logistics and inspection, so nurses and technicians reclaim time for direct care. Value realization improves when fleets integrate with tasking systems and electronic logs, since this creates auditable trails for compliance teams and measures diverted human hours[1]“Quadruped Robots in Healthcare: Maintenance & Inspection Use Cases 2026,” Oxmaint, oxmaint.com. Subscription and managed service models also reduce upfront spending and smooth budgeting, which speeds adoption in community settings that lack large capital programs. Price transparency for core platforms, such as published list pricing for high end quadrupeds and validated payloads, further lowers evaluation friction for buyers that must build multi year business cases.

Infection Control and Staff Safety Needs in Isolation and Critical Environments

Healthcare facilities maintain stringent infection prevention routines and seek to reduce human exposure in contaminated spaces. Quadrupeds equipped with UV C, thermal sensors, and air quality payloads can support hygiene workflows while limiting staff entries into isolation areas. Trials with autonomous wiping and UV C systems in hospital environments have demonstrated strong microbial load reduction, which aligns with goals to reduce healthcare associated infection risk while maintaining throughput. The robot dog market is also advancing where cleanroom standards and audit requirements apply, since validated decontamination workflows and traceable maintenance logs help satisfy pharmacy and lab governance. When the platform supports consistent environmental monitoring, safety officers gain continuous visibility and fewer blind spots between manual checks. Evolving device quality frameworks and cleanroom guidance have clarified expectations that robots must meet, which aligns vendors and hospitals on documentation, auditability, and quality system integration.

Hospital Campus Security and Emergency Readiness Require 24/7 Autonomous Patrols

Hospitals manage open campuses with constant foot traffic, high value assets, and sensitive patient areas, which creates persistent coverage needs that are hard to staff around the clock. The robot dog market benefits where autonomous patrols reduce the cost of overnight and perimeter coverage, with vendors reporting sizable savings compared to manned posts when robots and human guards work in tandem. Providers also adopt robots that integrate with access control, video management, and incident response platforms, since unified systems reduce dispatcher load and add time stamped evidence. Healthcare networks have expanded security robot contracts as part of multi site modernization, which signals sustained demand for autonomous patrol capabilities that complement human teams. Case studies show hospitals using AI enabled patrols to accelerate escalation on anomalies like loitering or perimeter breaches, and to minimize gaps during shift changes. Vendors that process video on the edge and apply role based control help hospitals meet privacy rules, since sensitive footage stays on premises and access is logged for compliance review.

AI Navigation and Sensor Fusion Enable Reliable Indoor–Outdoor Hospital Operations

Early mobile units struggled with crowded corridors and moving obstacles, while current quadrupeds combine LiDAR, stereo cameras, and IMUs so they localize and avoid people in real time. This advances the robot dog market because platforms can traverse stairs, ramps, and tight spaces that wheeled AMRs avoid or bypass through detours. Trials in 2026 demonstrated autonomous navigation in active hospital areas with pedestrian traffic, which strengthens confidence in shared human robot spaces and reduces the need for continuous teleoperation. High end quadrupeds document reliable foot placement and precision motion, while industrial grade models have proven stair climbing and terrain negotiation across inspection and facilities tasks. The acceptance of robots improves when motion planning is considerate of human behavior, so design teams include social navigation cues and audio prompts to increase comfort among patients and visitors. As mapping and fleet coordination improve, multi robot task allocation can deconflict routes across elevators and junctions, which is important for large academic medical centers with complex layouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TCO, IT/OT integration, and hospital cybersecurity approvals | -2.4% | Global, amplified in regulated markets in the U.S. and EU | Medium term (2-4 years) |

| Clinical workflow fit, infection-control cleaning, and safety validation | -1.9% | Global, particularly community hospitals with limited biomedical engineering staff | Medium term (2-4 years) |

| Patient/visitor acceptance and noise in sensitive wards | -0.7% | Culturally variable, lower resistance in APAC, higher scrutiny in EU patient‑rights frameworks | Short term (≤ 2 years) |

| Legacy buildings limit elevator/door/EMC compatibility near imaging suites | -0.5% | Predominantly older U.S. and European hospital infrastructure built pre‑2000 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High TCO, IT/OT Integration, and Hospital Cybersecurity Approvals

Total ownership costs encompass hardware, payloads, software, connectivity, and change management, which can delay first deployments. Buyers evaluate platform price along with sensors, manipulator arms, safety options, and docking, and then add network upgrades, role based access, and audit logging. High spec quadrupeds with validated payloads command premium pricing, so hospitals weigh single site ROI against multi site scale where service and spare pools lower unit economics over time. Security and privacy reviews extend timelines because robots can capture video in patient areas and must protect sensitive data, which pushes vendors to implement encryption, edge processing, and strict access control. Platforms that keep video on premises and record complete audit trails align better with HIPAA obligations and reduce risk in incident investigations. Interoperability remains a hurdle where fleets mix proprietary stacks and ROS based systems, so providers often lean on certified integrators that expose consistent APIs and workflow handoffs for elevator calls and door access. Compliance teams also look for clear documentation to medical device quality expectations and cleanroom norms when robots operate in pharmacy or lab environments, which favors vendors that publish guidance aligned to hospital governance.

Clinical Workflow Fit, Infection Control Cleaning, and Safety Validation

Hospitals run on dense schedules, so mobile robots must plan around peak traffic, quiet hours, and code events to minimize disruption. Vendors have improved orchestration and exception handling, but teams still tune routes and handoffs to avoid blocking corridors or delaying deliveries. The robot dog market advances where infection control and materials compatibility are well understood, since payloads and housings must tolerate cleaning protocols without sensor damage. Engineering guidance and studies on disinfection robots show the potential for automated routines to reduce bioburden, which supports the case for shared environments with clear, repeatable procedures. Validation requirements for safety interlocks, motion limits, and force thresholds add steps to commissioning and maintenance, and hospitals seek partners that can document conformance with relevant standards. Providers, therefore, favor vendors with robust technical files and audit-ready logs that integrate into biomedical engineering workflows and site quality systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Healthcare Application: Inspection Automation Outpaces Security in Deployment Volume

Facilities inspection and compliance monitoring held the largest share in 2025 deployment base as hospitals prioritized predictable ROI and continuous asset visibility, and this anchor role is expected to persist as orchestration tools mature. Within this context, the robot dog market has aligned to inspection payloads such as thermal imaging, acoustic sensing, and LiDAR that scan HVAC, medical gases, and panels with repeatable quality across frequent rounds. Hospitals use anomaly detection and automated reports to build audit trails for facilities and accreditation teams, which tighten equipment checks that are difficult to complete during manual walkthroughs. A notable inspection reference showed how quadrupeds validated leaks and prevented loss of purified air at a regulated site, which illustrates the performance gains of persistent monitoring over episodic human rounds. Security and campus patrol are currently a smaller share, yet they are set to expand faster as providers reinforce perimeters, parking structures, and lobbies with integrated robot guard workflows. The robot dog market supports these programs with patrols that feed VMS and access control, while trained handlers respond to prioritized alerts that reduce fatigue from constant camera monitoring[2]“AI Security for Healthcare Facilities,” Cobalt AI, cobaltai.com.

Facilities inspection commanded 42.19% of the 2025 application mix, which anchors the deployment base for multi payload use. In contrast, security and campus patrol is the fastest growing application at a 12.89% CAGR through 2031 as autonomous coverage strengthens nighttime readiness and incident documentation. To sustain growth across both use cases, vendors emphasize safer shared operation and human aware navigation, which shortens training and increases acceptance around staff and visitors. The robot dog market size for facilities inspection accounted for significant share in 2025 deployments, reflecting repeatable returns tied to downtime reduction and energy savings, while security adoption follows where hospital networks consolidate procurement across sites. Partnerships that bring together robots, video analytics, and on premises data processing address hospital privacy needs while enabling immediate incident review. As this foundation stabilizes, extensions to emergency drills and disaster assessment leverage the same autonomy and sensing stack, which expands quadruped utility without new hardware classes.

By Care Setting: Long Term Care Dominates Today, Behavioral Health Surges Tomorrow

Long term care and nursing homes represent the largest care setting share in 2025, reflecting aging populations and consistent daily routines that are well suited to structured tasks by mobile platforms. The robot dog market in these environments focuses on mobility assistance roles, simple delivery runs, and guided engagement that can reduce agitation and increase social interaction. Operator feedback highlights that supervised use with clear boundaries around resident care preserves safety and avoids replacing human companionship. Growth in this setting also reflects unit economics that work when robots cover frequent but low complexity activities across wide floorplans. Demand signals extend into assisted living and memory care, where partners explore routines that pair robots with caregivers on scheduled rounds. Shipments of quadrupeds by domestic producers in Asia have also supported pilots in elder care sites, which seed future scale as software improves.

Behavioral health is the fastest growing care setting at a 12.08% CAGR through 2031 as hospitals and specialty centers test structured, supervised engagement that reduces sitter needs in safe contexts. Providers have also trialed pediatric use with friendly interaction models, measured prompts, and staff controlled sessions to support therapeutic goals under clinician oversight. Vendor case studies in children’s care show early signs that supervised social robots can lower procedural distress and improve cooperation during care tasks. The robot dog market share in long term care accounted for 40.78% in 2025, while behavioral settings scale from a smaller base through evidence building programs and aligned governance. Hospitals also evaluate cleanability and durability for behavioral settings, since frequent contact and movement require robust materials that tolerate routine disinfection. As governance frameworks mature, providers expect clearer playbooks on scope of use, staff training, and consent documentation that preserve a high standard of patient rights.

By Autonomy Level: Operators Hedge Liability with Remote Control

Remote controlled and teleoperated systems represented the largest share in 2025 (51.23%), reflecting an emphasis on human supervision in clinical environments where risk tolerance is low. Hospitals prefer a human in the loop for exception handling, sensitive proximity moves, and entry into patient adjacent areas. Published reviews of medical robotics autonomy show that most cleared devices remain at conservative autonomy levels under clinician control, which sets a cautious adoption precedent for mobile robots in shared hospital spaces. The robot dog market also balances oversight with efficiency, with platforms that default to autonomous patrolling and escalation to teleoperation when anomalies are detected. Safety features, observability, and clear handoff paths between autonomy and operator control shape deployment decisions that satisfy both operations and compliance teams.

Semi autonomous systems are the fastest growing autonomy tier at a projected 13.21% CAGR through 2031 as perception, mapping, and planning improve success rates for routine tasks. This mode reduces operator time while retaining human oversight for edge cases and sensitive interactions. The robot dog market size for semi autonomous deployments is expected to increase with software updates that raise completion rates without retraining staff. Vendors support tiered autonomy where route learning, obstacle avoidance, and task execution are autonomous, and escalation to teleoperation occurs when conditions fall outside defined boundaries. Over time, providers will seek consistent logs for autonomy decisions and interventions, which helps quality teams confirm that controls work as intended. Clear documentation against hospital quality systems and privacy rules remains a prerequisite for broader use in patient adjacent zones.

Geography Analysis

North America held 45.44% of robot dog market share in 2025 as early adopters scaled deployments across inspection, logistics, and campus security. Hospitals in the region benefit from mature quality management frameworks and clear documentation pathways, which supports commissioning, change control, and in service audits. Vendors that align device quality practices with recognized standards help hospitals shorten review cycles and sustain compliance through updates. Academic medical centers, integrated delivery networks, and pharma adjacent facilities are key buyers because they manage complex infrastructures where quadrupeds can traverse stairs and varied terrain. Security use cases expand as hospital networks integrate robots with access control and video systems for continuous coverage and faster incident escalation. Providers have also increased contracts for security robots that supplement guard teams, which indicates confidence in hybrid patrol models at scale.

Asia Pacific is projected to be the fastest growing region at a 13.42% CAGR through 2031 as domestic manufacturers and university hospitals advance trials and lower unit costs. Public reporting indicates that domestic shipments of quadrupeds rose in 2025, which supports pilot programs in elder care and facility tasks across multiple cities. Japanese university hospitals ran proofs of concept in 2026 that validated autonomous navigation through active corridors and entry areas, which builds confidence for real world use with staff oversight. This is also supported by integrators and software partners that tailor robots to local workflows and language interfaces. Industrial collaborations involving inspection robots continue to cross over into regulated healthcare infrastructure, which strengthens safety cases and documentation practices. As these examples accumulate, buyers in the region will have clearer playbooks on governance, cleaning protocols, and incident response in shared spaces.

Europe shows steady interest centered on industrial grade inspection that transfers into hospital facilities and pharma manufacturing sites. The robot dog market in the region benefits from vendors with validated inspection references and strong compliance credentials. Partnerships between robot OEMs and service providers in energy and infrastructure are relevant because they stress reliability, safety, and repeatable documentation that hospital environments also require. Hospitals in Europe apply strict patient rights and data protection rules, so platforms that process video at the edge and provide granular access controls align better with procurement needs. Growth is likely to cluster around academic medical centers and large networks with the governance capacity to onboard new technologies under EU medical device quality systems.

Competitive Landscape

The robot dog market remains fragmented with premium incumbents, cost optimized challengers, and specialized solution providers targeting therapeutic and engagement roles. Premium vendors differentiate with integrated autonomy stacks, validated payloads, and full lifecycle software, while cost challengers rely on open SDKs and partner ecosystems to localize features faster. Installed bases in industrial inspection and pharma settings strengthen credibility for hospital facilities, since safety, documentation, and change control expectations are similar across these environments. Strategic moves point to software leverage as a competitive edge, including partnerships that bring foundation model capabilities to perception and manipulation. In January 2026, a leading OEM announced a collaboration to embed advanced AI for dexterous robotics, which positions the stack for continual updates over the air within defined safety bounds.

Challengers emphasize price performance balance and developer access, which accelerates pilots in hospitals that prefer flexible integrations. Documented shipments by a major Chinese producer in 2025 support the view that volume growth will come from cost efficient platforms that integrators tailor to local workflows. Integrators have formalized relationships with these platforms, enabling standardized deployment kits and workflow handoffs that shorten time to value. In parallel, European vendors with deep inspection pedigrees continue to raise capital and add partners in energy and infrastructure, which expands their reach into healthcare facilities that share similar safety and documentation requirements. This combined movement raises competitive intensity as buyers compare premium service depth with faster time to deploy options.

Security use cases highlight another front where ecosystem breadth matters. Hospital networks expanded contracts for autonomous patrol units in 2024 and 2025, confirming interest in hybrid patrol models that mix robots with human responders. Case studies across large hospital campuses show how robots feed real time telemetry into existing VMS and access control stacks, which reduces alert fatigue for human operators. Vendors that document HIPAA aligned logging and provide role based control strengthen their position in clinical spaces, where privacy and auditability are critical. The robot dog market will likely remain a multi tier ecosystem where buyers match price points and software depth to the maturity of their use cases.

Robot Dog Industry Leaders

Boston Dynamics

DEEP Robotics

Kawasaki Heavy Industries (BEX)

Sony (aibo)

Unitree Robotics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Pudu Robotics raised nearly USD 150 million, surpassing USD 1.5 billion in valuation, and reported 100% year over year revenue growth in 2025, with proceeds aimed at embodied AI, portfolio expansion, and global scaling.

- April 2026: Gaode Map's Embodied Intelligence Division unveiled its first quadruped robot integrating the proprietary ABot-M0 manipulation model and opened SDK access to collaborative robot manufacturers including Unitree. The initiative targets cross-border warehousing and logistics integrators, with commercially viable deployment-ready solutions anticipated from the second half of 2026, leveraging Gaode's digital infrastructure to accelerate OEM product differentiation and reduce R&D timelines for perception-manipulation stacks.

Global Robot Dog Market Report Scope

As per the report scope, robot dogs function as socially assistive robots (SARs) or companion robots, designed to replicate the appearance and behavioral traits of real dogs. By integrating artificial intelligence, sensors, and actuators, these robots deliver therapeutic and emotional support, with a particular focus on elderly patients and individuals with dementia.

The robot dogs market is segmented into healthcare applications, care settings, autonomy levels, and geography. By healthcare application, the market is segmented into facilities inspection & compliance monitoring (HVAC, med gas, plant rooms), security and campus patrol, telepresence and virtual rounds in isolation wards, patient engagement and therapy (pediatric, geriatric, behavioral), emergency response and disaster drills, materials couriering & logistics (lab samples, pharmacy), training and simulation for medical education, and environmental and infectious‑disease surveillance. By care setting, the market is segmented into tertiary/quaternary hospitals & IDNS, community hospitals, pediatric hospitals, rehabilitation centers, long‑term care & nursing homes, behavioral health facilities, outpatient clinics & ASCS, hospital‑based laboratories & cleanrooms, university medical centers & teaching hospitals, and field hospitals & public health sites. By autonomy level, the market is segmented into remote‑controlled / teleoperated, semi‑autonomous, and fully autonomous. By geography, the market is segmented as North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Facilities inspection & compliance monitoring (HVAC, med gas, plant rooms) |

| Security and campus patrol |

| Telepresence and virtual rounds in isolation wards |

| Patient engagement and therapy (pediatric, geriatric, behavioral) |

| Emergency response and disaster drills |

| Materials couriering & logistics (lab samples, pharmacy) |

| Training and simulation for medical education |

| Environmental and infectious‑disease surveillance |

| Tertiary/Quaternary Hospitals & IDNs |

| Community Hospitals |

| Pediatric Hospitals |

| Rehabilitation Centers |

| Long‑term Care & Nursing Homes |

| Behavioral Health Facilities |

| Outpatient Clinics & ASCs |

| Hospital‑based Laboratories & Cleanrooms |

| University Medical Centers & Teaching Hospitals |

| Field Hospitals & Public Health Sites |

| Remote‑controlled / Teleoperated |

| Semi‑autonomous |

| Fully autonomous |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Healthcare Application | Facilities inspection & compliance monitoring (HVAC, med gas, plant rooms) | |

| Security and campus patrol | ||

| Telepresence and virtual rounds in isolation wards | ||

| Patient engagement and therapy (pediatric, geriatric, behavioral) | ||

| Emergency response and disaster drills | ||

| Materials couriering & logistics (lab samples, pharmacy) | ||

| Training and simulation for medical education | ||

| Environmental and infectious‑disease surveillance | ||

| By Care Setting | Tertiary/Quaternary Hospitals & IDNs | |

| Community Hospitals | ||

| Pediatric Hospitals | ||

| Rehabilitation Centers | ||

| Long‑term Care & Nursing Homes | ||

| Behavioral Health Facilities | ||

| Outpatient Clinics & ASCs | ||

| Hospital‑based Laboratories & Cleanrooms | ||

| University Medical Centers & Teaching Hospitals | ||

| Field Hospitals & Public Health Sites | ||

| By Autonomy Level | Remote‑controlled / Teleoperated | |

| Semi‑autonomous | ||

| Fully autonomous | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the robot dog market size and growth outlook to 2031?

The robot dog market size is projected to expand from USD 263.33 million in 2025 and USD 292.90 million in 2026 to USD 498.69 million by 2031, registering an 11.23% CAGR between 2026 and 2031.

Which applications are leading and which are growing fastest in hospitals?

Facilities inspection led with 42.19% of 2025 deployments, while security and campus patrol is the fastest growing application at a 12.89% CAGR through 2031.

Which care settings are adopting quadruped robots the most?

Long term care accounted for 40.78% of 2025 deployments, and behavioral health facilities are growing fastest at a 12.08% CAGR through 2031, with supervised engagement and safety first workflows.

What autonomy approach do hospitals prefer today?

Remote controlled systems held 51.23% share in 2025 for liability and exception handling, while semi autonomous robots are projected to advance at a 13.21% CAGR as perception and planning mature.

Which regions are most important for the robot dog market now?

North America held 45.44% share in 2025 due to early adopters and mature governance, while Asia Pacific is projected to be the fastest growing region at a 13.42% CAGR through 2031.

What factors most limit adoption today?

The main constraints are total cost of ownership, IT/OT and cybersecurity approvals, and workflow fit that meets infection control and safety validation requirements, especially in resource constrained hospitals.

Page last updated on: