Sanitization Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.40 Billion |

| Market Size (2031) | USD 5.57 Billion |

| Growth Rate (2026 - 2031) | 18.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

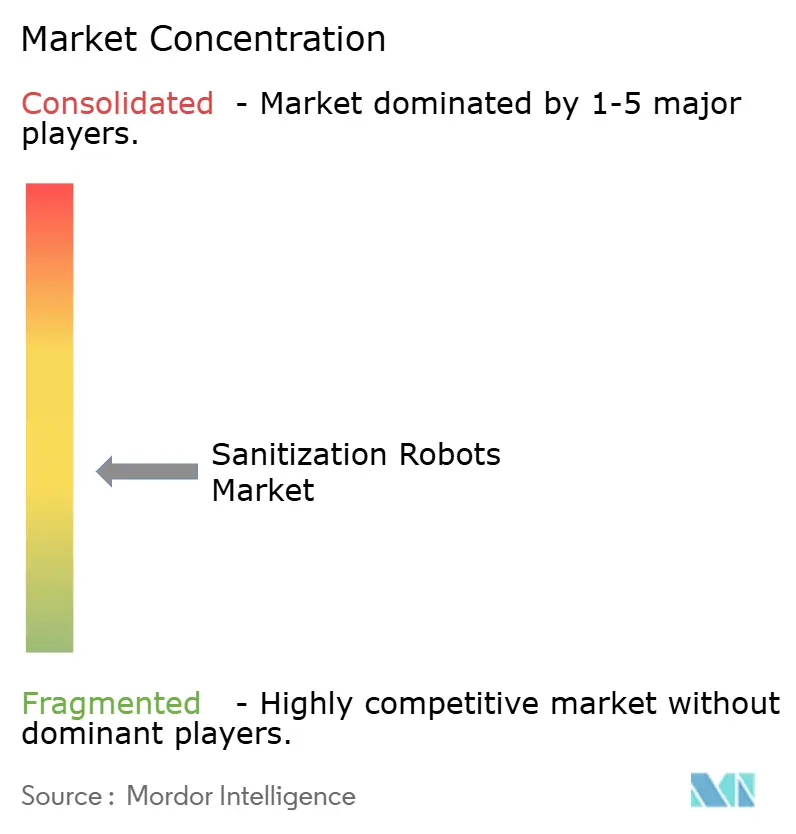

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sanitization Robots Market Analysis by Mordor Intelligence

The Sanitization Robots Market size is expected to grow from USD 2.03 billion in 2025 to USD 2.40 billion in 2026 and is forecast to reach USD 5.57 billion by 2031 at 18.32% CAGR over 2026-2031.

Health systems, airports, and large public venues are automating environmental hygiene as labor pressure, safety expectations, and audit requirements converge. Clinical operations continue to prioritize infection prevention investments because hospital-acquired infections lengthen stays, raise costs, and strain capacity in settings facing persistent staffing shortages. UV-C and vaporized hydrogen peroxide platforms are gaining traction as operators seek consistent, auditable, and technology-neutral approaches that fit within evolving safety standards. North American purchasing remains anchored by regulatory clarity and large buying groups, while Asia-Pacific growth is supported by new-build healthcare and transportation infrastructure. Competitive intensity increases as incumbents secure regulatory and distribution advantages, even as buyers demand stronger real-world evidence and lifecycle cost transparency.

Key Report Takeaways

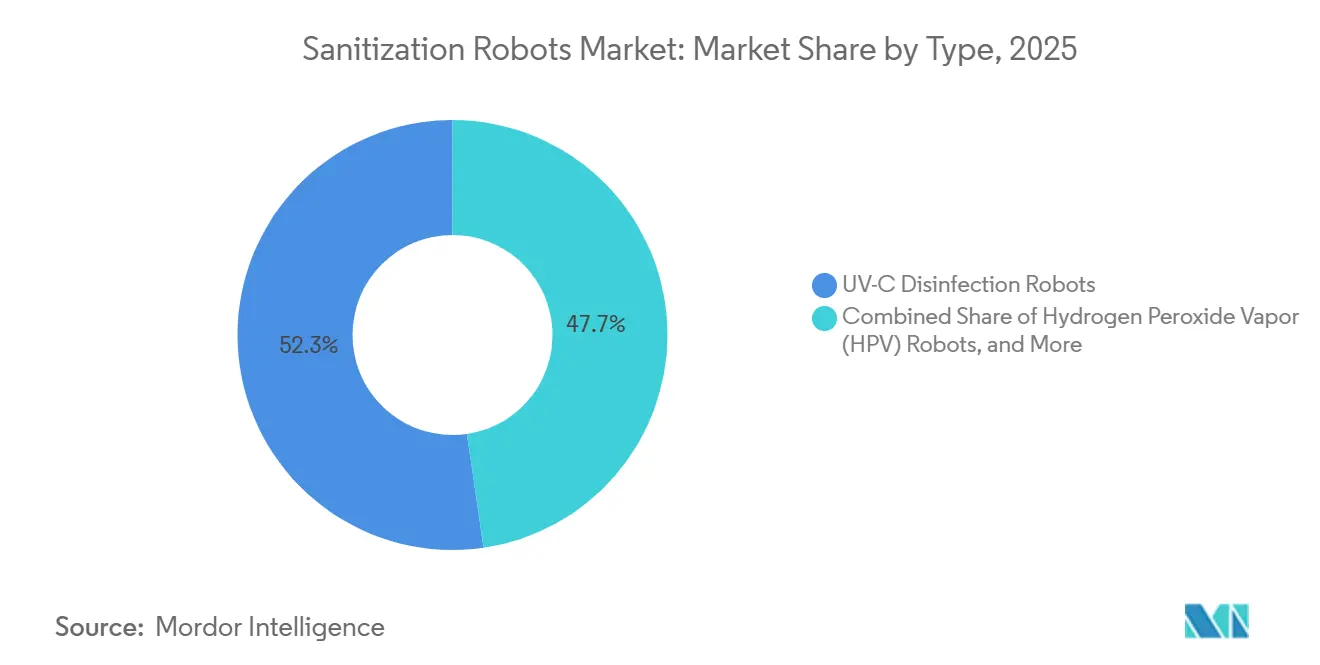

- By type, UV-C disinfection robots led with 52.3% revenue share in 2025, while hydrogen peroxide vapor robots are projected to expand at an 19.34% CAGR through 2031.

- By application, surface disinfection accounted for a 45.8% share in 2025, and air and HVAC disinfection is set to grow at a 22.21% CAGR to 2031.

- By technology, autonomous robots held 49.8% share in 2025, and semi-autonomous robots are projected to record a 20.11% CAGR through 2031.

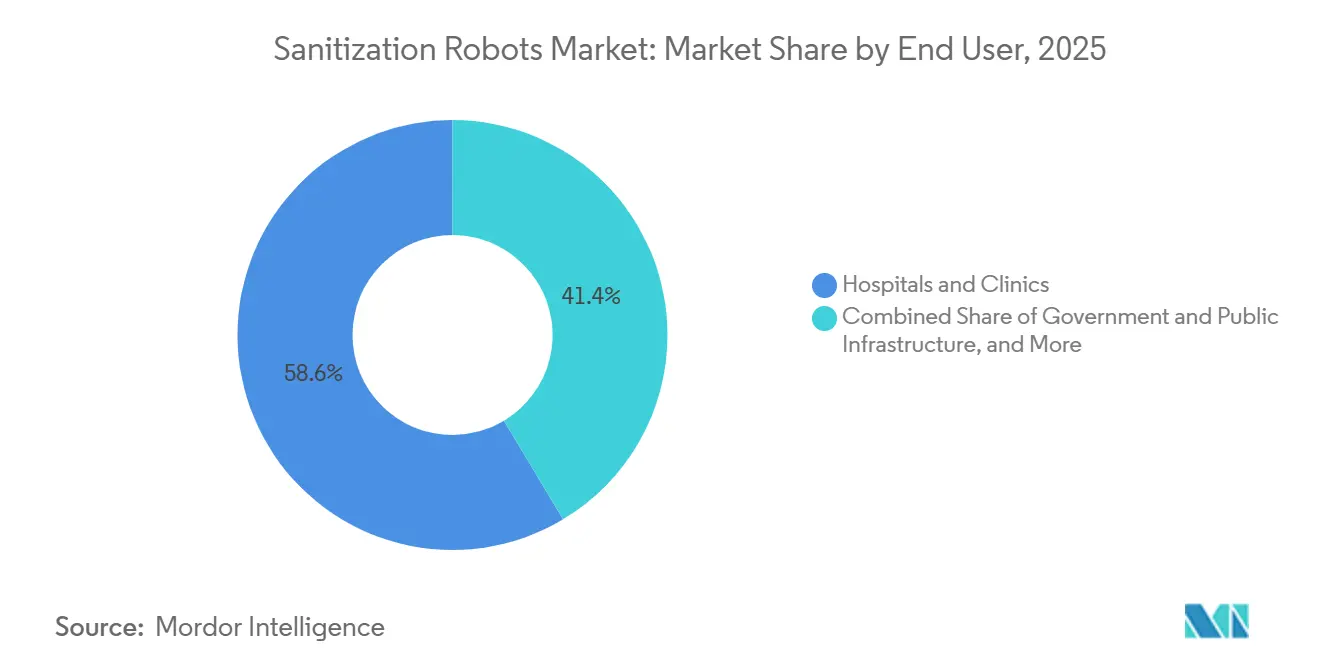

- By end user, hospitals and clinics commanded 58.6% share in 2025, and government and public infrastructure are projected to advance at a 21.30% CAGR to 2031.

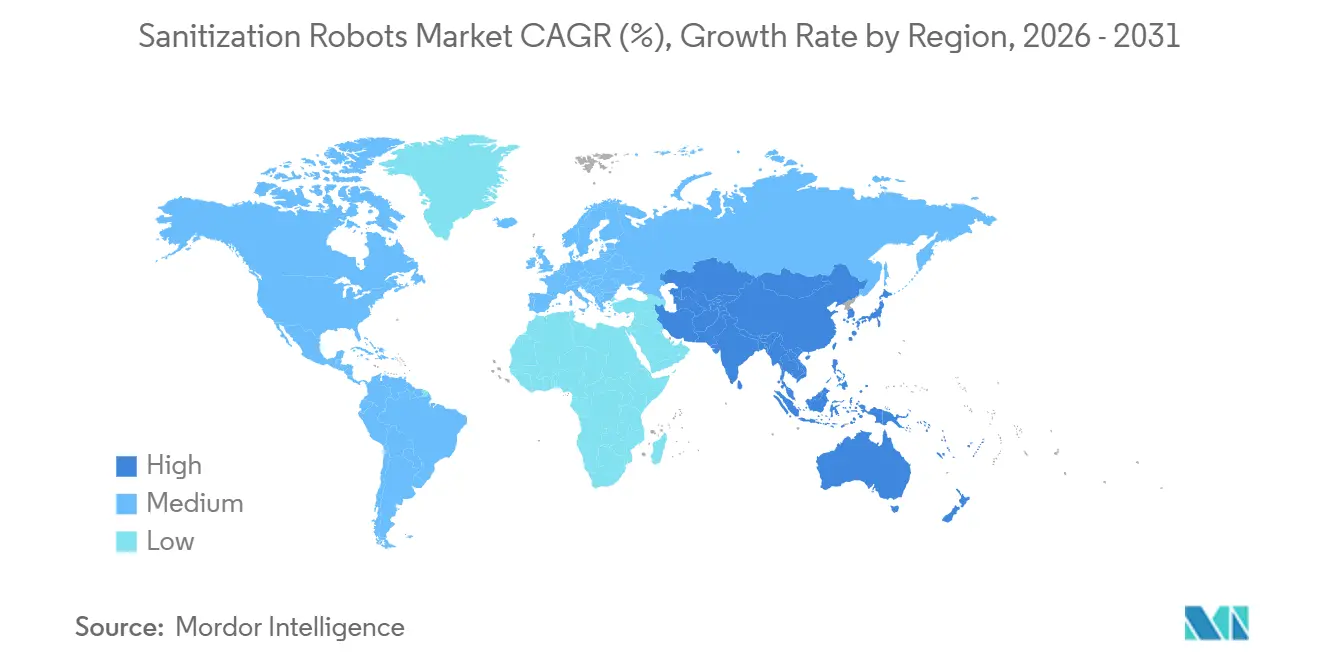

- By geography, North America captured 45.13% share in 2025, and Asia-Pacific is projected to post the fastest growth at a 19.60% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sanitization Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Hospital-Acquired Infections (HAIs) | +2.8% | Global, concentrated in LMICs (15% HAI incidence vs. 7% in HICs) | Short term (≤ 2 years) |

| Growing Adoption of AI, IoT, and Autonomous Navigation Systems | +2.5% | North America, Europe, Asia-Pacific core markets, spill-over to MEA airports | Medium term (2-4 years) |

| Expansion of Smart Hospitals, Airports, and Smart City Infrastructure | +2.1% | Asia-Pacific, North America metro hubs | Medium term (2-4 years) |

| Increasing Regulatory Pressure for Infection Prevention Compliance | +1.7% | North America, Europe, Asia-Pacific emerging standards | Short term (≤ 2 years) |

| EVS Labor Shortages and Wage Inflation Catalyze Automation Adoption | +2.2% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Evolving Far-UVC Exposure Limits Enable in-Occupancy Disinfection Use-Cases | +1.0% | North America, Europe, early APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hospital-Acquired Infections (HAIs)

Evidence continues to show that HAIs elevate mortality risk, lengthen hospital stays, and drive total cost, reinforcing the adoption of automated disinfection that complements manual cleaning. In U.S. data, HAI-associated hospital stays carried higher mortality and longer median length of stay than non-HAI cases, with sharply higher median total cost across select clinical categories, underscoring why decision-makers prioritize solutions that can systematically lower bioburden and standardize terminal cleaning cycles. UV-C devices and vaporized hydrogen peroxide systems demonstrate high levels of inactivation in controlled studies when applied correctly, with spore kill rates and whole-room microbial reduction validated in several research and industry programs[1]The National Institute For Innovation in Manufacturing Biopharmaceuticals.

Hospitals adopt sanitization robots to turn disinfection into a repeatable, auditable workflow, reducing variability from manual-only approaches. The sanitization robots market benefits from the operational need to free skilled staff from low-value tasks while improving environment-of-care metrics that factor into accreditation and payer scrutiny. As standardized reporting and infection control audits scale, platforms that create digital documentation and traceable performance data gain an added advantage in procurement decisions.

Growing Adoption of AI, IoT, and Autonomous Navigation Systems

Advances in autonomy and perception are shifting robots from remote-controlled carts to self-navigating assets that map spaces, schedule workflows, and document outcomes. Large multisite deployments illustrate the maturation of this stack, as robotics platforms integrate LiDAR, vision, and cloud analytics to raise utilization and reduce training time for frontline teams[2]“Frankfurt Airport Case Study: Tennant’s AMRs Powered by BrainOS,” Brain Corp, braincorp.com . Manufacturers report significant installed bases and active fleet growth, supported by modular autonomy software and partnerships with cleaning equipment[3]Brain Corp, “Tennant Company and Brain Corp Agree to Accelerate Robotic Cleaning Innovation,” Brain Corp.

Study data and field evidence also point to targeted UV-C application improving outcomes when it augments manual cleaning, especially on high-touch objects and difficult areas, with AI-driven exposure strategies now a product focus for some vendors[4]Haystack Robotics, “In-Clinic Microbiology Comparative Study of Manual Disinfection and the Addition of UV-C Disinfection with Violet Gen4”. IoT fleet management enables predictive maintenance for UV sources, batteries, and motors, reducing unplanned downtime and tightening cost control on parts and service intervals. The sanitization robots market is therefore supported by a practical path to value that leans on nonclinical automation first, delivering quick operational wins before organizations pursue more complex clinical AI.

Expansion of Smart Hospitals, Airports, and Smart City Infrastructure

New-build healthcare facilities and transportation hubs are being designed for automation from the start, which reduces retrofit friction and helps lock in robotic disinfection within core operations. In hospitals, autonomous platforms now interoperate with room turnover workflows, access control systems, and digital logs, while research collaborations have validated hybrid robots that combine physical wiping with UV-C exposure to address complex geometries in clinical rooms.

Airport operators demonstrate the benefits of autonomous fleets with documented savings and utilization metrics, reinforcing the role of robotics in large, high-traffic environments with strict hygiene standards. As mechanical ventilation upgrades collide with budget constraints, UV solutions deployed in the upper room or in-duct systems support infectious aerosol control targets when integrated with performance standards and safety frameworks. The sanitization robots market expands in parallel with these infrastructure programs because robots convert disinfection into a verifiable process that meets audit expectations. With sustainability targets tightening, electric robotic platforms and water-recovery features align with decarbonization roadmaps that many facility operators now pursue.

Increasing Regulatory Pressure for Infection Prevention Compliance

Regulatory signals guide purchasing and reduce perceived risk for hospital committees. In January 2024, the FDA recognized vaporized hydrogen peroxide as an Established Category A sterilization method, streamlining use cases for VH2O2 systems and encouraging evaluation of alternatives to ethylene oxide where appropriate. Company-level milestones also matter in procurement, including authorizations and registrations that define market access across jurisdictions and build confidence in labeling and clinical use claims.

Harmonized safety standards in Europe, such as IEC 60335-2-65:2023 for air-cleaning appliances that incorporate UV-C, provide common expectations for materials, warnings, and service steps, which help buyers assess risk across brands. Far-UVC exposure research and exposure limit updates have opened the door for in-occupancy use in specific configurations, although ozone formation and secondary chemistry remain considerations that require ventilation and mitigation. The sanitization robots market benefits as device testing methods, emissions requirements, and zero-ozone validations become procurement checkpoints that align engineering controls, labeling, and field use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost and Total Cost of Ownership of Sanitization Robots | -1.8% | Global, most acute in LMICs and rural facilities | Short term (≤ 2 years) |

| Safety Concerns Related to UV-C Exposure and Human Interaction Limits | -0.9% | Global, heightened scrutiny in Europe and North America | Medium term (2-4 years) |

| Mixed Real-World Efficacy Evidence Slows Procurement Decisions | -1.1% | North America and Europe, evidence-led buyers | Medium term (2-4 years) |

| Procurement Complexity (AMRs Vs Towers Vs HPV) Muddies ROI and Compliance | -0.7% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Total Cost of Ownership of Sanitization Robots

Initial capex, maintenance, and downtime risk can slow decisions, especially in facilities under budget pressure. Maintenance analytics show that unplanned downtime and reactive service models erode expected ROI in robotics deployments, highlighting the importance of predictive maintenance, parts planning, and documentation to keep fleets operating at target utilization. Financial constraints are more visible in rural and smaller facilities where capital budgets compete with staffing and clinical equipment, a pattern reflected in hospital labor expenditure studies that imply cautious adoption of additional automation subscriptions or service-heavy models.

State-level reporting has also documented negative reimbursement margins for key payer categories, which compounds capital scarcity and makes payback clarity essential for approval cycles in public and nonprofit hospitals. Buyers therefore emphasize short payback tied to HAI cost avoidance and labor productivity, with whole-room reduction authorizations and high spore kill validation strengthening the business case in certain rooms or workflows. The sanitization robots market continues to evolve its commercial models, but long-term ROI depends on uptime, parts logistics, and alignment with infection control priorities.

Safety Concerns Related to UV-C Exposure and Human Interaction Limits

UV-C exposure risks require engineered safeguards, procedural controls, and training to protect staff and bystanders. European safety standards specify warnings, replacement instructions, and design controls for UV-C components in air-cleaning appliances, which serve as a reference point for buyers and service teams. Research teams have highlighted human-detection system gaps in UV-C platforms and demonstrated dual-redundancy approaches using sensors and AI vision to reduce risk, pointing to the need for robust person-detection under varied conditions.

Far-UVC may enable in-occupancy disinfection within exposure limits, but testing shows potential ozone and secondary pollutants that require ventilation co-design and verification to align with zero-ozone expectations in many building programs. Operators face operational friction in complex rooms because line-of-sight and shadowing reduce irradiance, while soft surfaces often need separate treatment, which together increase process complexity in high-turnover settings. The sanitization robots market addresses these issues through layered safety designs, documented workflows, and hybrid methods that combine contact cleaning with UV-C or vapor cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: HPV Robots Gain Share as FDA Recognition Lowers Sterilization Compliance

UV-C disinfection robots held 52.3% in 2025, while hydrogen peroxide vapor robots are projected to expand at an 19.34% CAGR through 2031, with the FDA’s recognition of vaporized hydrogen peroxide as an Established Category A sterilization method reinforcing adoption in high-sterility settings. In this context, the sanitization robots market continues to see hospitals apply UV-C for speed-sensitive turnover tasks and evaluate VH2O2 for rooms where spore kill validation and residue-free outcomes drive decision criteria. The sanitization robots market size for VH2O2-enabled deployments is supported by multi-room validation that confirms whole-room microbial reduction without manual ventilation steps when integrated catalysts are used. Evidence that high-touch surface coverage improves when autonomous robots augment manual cleaning supports continued UV-C utilization in general-purpose areas like corridors and waiting rooms. Vendors are also shipping multi-technology platforms that blend wiping, UV-C, and vapor capabilities to address geometry, shadowing, and spore tolerance, which lets facilities match method to room needs.

VH2O2 platforms target ambulances, isolation rooms, and labs where standards require consistent spore reductions and traceable digital logs. UV-C platforms focus on autonomy, coverage consistency, and safety interlocks aligned to IEC 60335-2-65:2023, which specifies warnings, materials, and disconnection instructions for components with UV sources. The sanitization robots market also includes electrostatic spray robots, which appeal in budget-constrained settings, although chemical replenishment and residue risks limit use in device-dense rooms. Hospital buyers increasingly evaluate device-level authorizations and registrations when shortlisting vendors, making multi-country approvals and GPO coverage competitive differentiators. Across types, the sanitization robots market benefits from a portfolio approach, with room-class protocols that standardize method selection for each environment of care.

By Application: Air & HVAC Disinfection Accelerates as ASHRAE 241 Drives Equivalence Crediting

Surface disinfection accounted for 45.8% in 2025, while air and HVAC disinfection is projected to grow at a 22.21% CAGR through 2031 as facilities pursue infectious aerosol control targets under technology-neutral standards that credit verified performance. The sanitization robots market aligns to this shift by pairing mobile platforms with in-duct or upper-room solutions that maintain pathogen reduction when rooms are occupied, subject to exposure and emissions safeguards. The sanitization robots market size for air handling use cases benefits from test protocols that benchmark inactivation or irradiance under operating conditions, enabling facility managers to justify allocations within building upgrade programs. In occupied zones, Far-UVC options are under evaluation with attention to ozone formation and secondary chemistry, and facility teams layer ventilation and filtration to satisfy emissions and exposure criteria. Hybrid cleaning schedules that integrate robotic surface disinfection with continuous air treatment support consistent pathogen control in high-footfall areas.

Airport operations offer reference cases on scheduling, fleet coordination, and validated results that help hospitals and public buildings translate playbooks across environments. In clinical spaces, upper-room and in-duct solutions reduce reliance on manual interventions during peak census while robotic surface disinfection standardizes turnover steps for terminal cleaning. Procurement teams weigh device-level measurements, room geometry, and occupant density when allocating budget between surface and air programs, often anchoring decisions to the locations that demonstrate the highest infection risk or patient throughput. The sanitization robots market therefore advances on both surface and air use cases, and new-build facilities are embedding both pathways at design stage to avoid retrofit tradeoffs.

By Technology: Semi-autonomous Bridges Full Automation and Manual Override in Turnover-Intensive Settings

Autonomous robots held 49.8% in 2025, supported by mature navigation stacks, while semi-autonomous robots are projected to grow at 20.11% through 2031 as buyers seek manual override in complex rooms and during sensitive workflows. The sanitization robots market has moved beyond pilot novelty toward fleet operations on autonomy platforms that report thousands of active units and new OEM releases aligned to building systems and voice-enabled operation for easier onboarding. Semi-autonomous configurations remain favored in high-acuity areas where staff judgment is needed to reposition devices or patient belongings, or to extend UV exposure for specific high-touch zones. Remote-controlled platforms persist where autonomy is not feasible due to constraints such as multi-level sites without elevators or temporary structures. Across modalities, safety and documentation are core to procurement, with European standards guiding labeling and component maintenance to reduce risk.

Autonomy’s value centers on uptime, overnight operation, and consistent coverage that minimizes human error in expansive spaces like concourses and corridors, while semi-autonomous systems bridge gaps in irregular or crowded rooms. Vendor roadmaps emphasize multi-robot coordination, occupancy-linked scheduling, and predictive maintenance integrated into fleet dashboards to raise effective utilization. The sanitization robots market benefits as these features push robotics from point solutions into standardized facility services with measurable outcomes. Hospitals and airports are consolidating around platforms that combine autonomy maturity with integration pathways for environmental health, building automation, and compliance reporting.

By End User: Government & Public Infrastructure Expands as Airports and Transit Hubs Address Chronic Labor Gaps

Hospitals and clinics held 58.6% in 2025, as HAI reduction, accreditation checklists, and audit traceability remained central to environmental hygiene programs, while Government & Public Infrastructure are projected to grow at 21.30% through 2031. Procurement is shaped by regulatory authorizations, including device registrations that define where UV-C robots can be promoted for clinical spaces, and by group purchasing agreements that streamline pricing and service. The sanitization robots market size for hospitals increases when buyers pair disinfection with workforce relief for overstretched cleaning teams and clinical staff who should not be diverted to environmental tasks. Airports, convention centers, and transit hubs often become early adopters because scale and footfall justify autonomous fleets.

Large GPO agreements, distributor appointments, and multi-region channel partnerships continue to shape access to public-sector buyers and their integrators. For healthcare-adjacent public facilities, standards that reference emissions limits and safe operation drive procurement to vendors that can demonstrate compliance and provide traceable digital logs. The sanitization robots market therefore scales across end users when solutions integrate with security, facilities, and sustainability programs that public managers already run. In all segments, uptime, serviceability, and evidence that links disinfection steps to outcomes drive renewal and expansion decisions.

Geography Analysis

North America held 45.13% in 2025 and continues to benefit from regulatory clarity, GPO leverage, and hospital capital cycles that emphasize automation for environmental hygiene. The market outlook is influenced by workforce data that show persistent turnover and cost pressure in clinical roles, which intensifies the push to free frontline staff from nonclinical work. Authorizations and registrations support procurement confidence, including platform-level milestones that signal allowable claims and use in clinical rooms across the U.S. and Canada. National GPO agreements improve vendor access to hospital networks and embed robots in multisite service offerings. In parallel, airports and large campuses in the region are expanding autonomous cleaning fleets and integrating robot performance data into building systems to optimize nighttime schedules and cover large floor areas. The sanitization robots market maintains momentum as hospitals and airports adopt common playbooks and prioritize vendors that demonstrate compliance, documentation, and service scale.

Europe remains a significant region supported by harmonized safety standards that simplify multi-country go-to-market work for vendors. Hospitals and airports adopt autonomy at scale with documented ROI and water recovery metrics that align with sustainability targets, with case studies from large airports demonstrating fleet performance and savings. CE marking and IEC-standard alignment help centralize risk assessments, while local reimbursement and capital budgeting rules shape the speed of hospital adoption. Nordic countries often lead on pilot-to-scale transitions due to public innovation funding and aggressive decarbonization timelines, while Eastern Europe’s lower wages elongate ROI for some automation projects. The sanitization robots market advances as vendors pair compliance documentation with energy and water metrics that public buyers need for procurement portals. Cross-border partnerships that target pharmaceutical cleanrooms and GMP-controlled environments further extend addressable markets for UV-C platforms.

Asia-Pacific is projected to post the fastest growth at a 19.60% CAGR during 2026-2031, supported by smart hospital projects, hospital bed expansion, and airport modernizations. Buyer priorities in the region include infection prevention gains and workforce productivity in dense urban hospitals, and consistency and documentation in high-traffic transportation hubs. Research collaborations and new platform introductions within Korea and Japan add momentum around hybrid designs and in-occupancy safety considerations aligned to exposure guidelines. As part of this growth, international vendors are expanding distributor networks and segment-specific offerings, such as pharma-oriented UV-C variants with digital traceability. The sanitization robots market also benefits from public tenders in transport and education that value emissions-safe air treatment and autonomous floor care backed by fleet reporting. Across North America, Europe, and Asia-Pacific, regulatory standards, emissions testing, and exposure science shape engineering and procurement, while lifecycle analytics and serviceability define ROI and renewal in competitive bids.

Competitive Landscape

The sanitization robots market is moderately fragmented, with a mix of UV-C incumbents, VH2O2 solution providers, and autonomy platform partners that supply large fleets to hospitals, airports, and pharma environments. Regulatory and distribution positions create durable advantages; company announcements show cross-border approvals and national GPO contracts that streamline pricing and deployment at scale. Autonomous cleaning platforms with broad installed bases partner with industrial equipment makers to release new models, coordinate fleets, and link to building systems, which strengthens switching costs and increases buyer confidence. Vendors are also customizing UV-C offerings for GMP spaces, adding digital traceability and documentation to meet regulatory expectations in pharma segments.

Product strategies emphasize layered safety, AI-assisted exposure, and integration into fleet dashboards for compliance and maintenance. Evidence generation focuses on room-class protocols and performance traceability that buyers can audit, which addresses hesitancy tied to heterogeneous field results across surfaces and pathogens. Autonomy leaders publish case studies and ROI data from large hubs to prove repeatability and uptime in challenging spaces, which hospitals consider when moving beyond pilots. As fleets expand, lifecycle analytics and predictive maintenance become differentiators that protect realized ROI in year two and beyond. The sanitization robots market therefore rewards vendors that link device performance to measurable outcomes and that can support multi-site service agreements.

Strategic moves include distribution partnerships into new segments, GPO exclusivity in hospital networks, and roadmaps to release multiple models that span footprint and feature options. Some vendors focus on AI-driven object targeting for UV-C exposure, while others extend into pharma cleanrooms with GMP-ready documentation. Large autonomy providers emphasize OEM integrations that convert traditional machines into robotics-enabled systems, expanding reach without building every form factor in-house. Across the competitive set, proof-of-clean, safety alignment, and outcomes reporting remain the common threads that shape awards.

Sanitization Robots Industry Leaders

STERIS

Xenex Disinfection Services Inc.

UVD Robots ApS (Blue Ocean Robotics ApS)

Aethon Inc.

RobotLAB Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Blue Ocean Robotics appointed PSC Biotech Corporation as a new distributor for its UVD Robot Pharma platform across the United States, Australia, and Singapore, targeting pharmaceutical manufacturers and GMP-controlled environments with autonomous UV-C disinfection technology offering full digital documentation and traceability to support contamination control, compliance, and operational efficiency in cleanroom applications.

- March 2026: Blue Ocean Robotics appointed AB Scientific as its UK partner for the pharmaceutical sector, introducing the UVD Robot Pharma to manufacturers and GMP-controlled environments across the United Kingdom to optimize contamination control strategies, reduce costs, save time, optimize labor resources, and advance sustainability objectives, with the partnership showcased at Making Pharmaceuticals.

Global Sanitization Robots Market Report Scope

As per the scope of the report, sanitization robots are autonomous or semi-autonomous machines designed to disinfect surfaces and environments using technologies such as ultraviolet (UV-C) light, hydrogen peroxide vapor, or chemical sprays. They are widely used in healthcare facilities, public spaces, and industrial settings to reduce microbial contamination and prevent the spread of infections. These robots improve cleaning efficiency, ensure consistent disinfection, and minimize human exposure to harmful pathogens.

The sanitization robots market is segmented by type, application, technology, end user, and geography. By type, the market is segmented into UV-C disinfection robots, hydrogen peroxide vapor (HPV) robots, electrostatic spray robots, and hybrid / multi-technology robots. By application, the market is segmented into surface disinfection, air & HVAC disinfection, room / corridor sanitization, and others. By technology, the market is segmented into autonomous robots, semi-autonomous robots, and remote-controlled robots. By end user, the market is segmented into hospitals & clinics, government & public infrastructure, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| UV-C Disinfection Robots |

| Hydrogen Peroxide Vapor (HPV) Robots |

| Electrostatic Spray Robots |

| Hybrid / Multi-technology Robots |

| Surface Disinfection |

| Air & HVAC Disinfection |

| Room / Corridor Sanitization |

| Others |

| Autonomous Robot |

| Semi-autonomous Robots |

| Remote-controlled Robots |

| Hospitals & Clinics |

| Government & Public Infrastructure |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | UV-C Disinfection Robots | |

| Hydrogen Peroxide Vapor (HPV) Robots | ||

| Electrostatic Spray Robots | ||

| Hybrid / Multi-technology Robots | ||

| By Application | Surface Disinfection | |

| Air & HVAC Disinfection | ||

| Room / Corridor Sanitization | ||

| Others | ||

| By Technology | Autonomous Robot | |

| Semi-autonomous Robots | ||

| Remote-controlled Robots | ||

| By End User | Hospitals & Clinics | |

| Government & Public Infrastructure | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and expected CAGR for the sanitization robots market through 2031?

The sanitization robots market size is USD 2.40 billion in 2026 and is projected to reach USD 5.57 billion by 2031 at a 18.32% CAGR during 2026-2031.

Which application areas are growing fastest in sanitization robots?

Air and HVAC disinfection is the fastest-growing application, supported by infectious aerosol control standards and increasing use of safe UV configurations in occupied spaces.

How do regulations influence purchasing of sanitization robots?

FDA recognition of vaporized hydrogen peroxide, European IEC UV-C safety standards, and evolving exposure guidance shape device selection, labeling, and documentation in hospital and public facility procurement.

What technologies dominate deployments across hospitals and public venues?

Autonomous UV-C platforms lead for coverage and consistency, while VH2O2 systems are gaining in rooms where spore reduction and residue-free outcomes are critical, and semi-autonomous modes remain important in complex spaces.

Which regions lead adoption and where is growth fastest?

North America holds the largest share due to regulatory clarity and GPO leverage, while Asia-Pacific is the fastest-growing region driven by smart hospital projects and transportation infrastructure programs.

What evidence do buyers seek when evaluating sanitization robots?

Buyers prioritize validated microbial reduction, documented safety alignment, and traceable performance logs, along with lifecycle support that sustains uptime and ROI.

Page last updated on: