Healthcare Assistive Robot Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

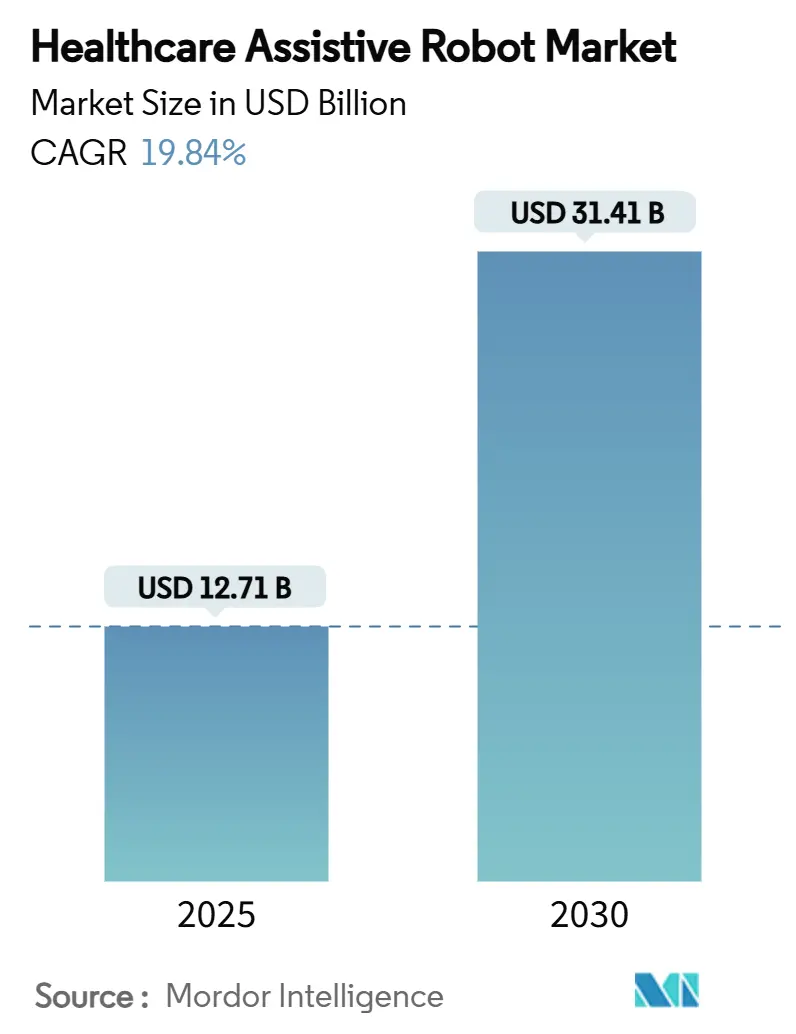

| Market Size (2025) | USD 12.71 Billion |

| Market Size (2030) | USD 31.41 Billion |

| Growth Rate (2025 - 2030) | 19.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Assistive Robot Market Analysis by Mordor Intelligence

The Healthcare assistive robot market size is USD 12.71 billion in 2025 and is forecast to advance to USD 31.41 billion by 2030, reflecting a 19.84% CAGR through the period. A rapid transition from pilot projects to large-scale deployments is underway as demographic change, reimbursement reform and AI-driven precision position robotics as core medical infrastructure. Medicare’s 2024 decision to reimburse at-home exoskeleton therapy and the FDA’s faster review pathway for AI-enabled surgical platforms act as immediate accelerators.[1]Centers for Medicare & Medicaid Services, “CMS Expands Medicare Coverage for Exoskeleton Devices,” cms.gov Device miniaturization, declining battery costs and integration with electronic health records widen practical use cases, while Robot-as-a-Service contracts ease capital constraints and assure continuous software updates. Competitive intensity rises as medical device multinationals acquire start-ups to assemble end-to-end robotic ecosystems, yet smaller innovators still shape niche segments through specialized algorithms and human-robot interface breakthroughs.

Key Report Takeaways

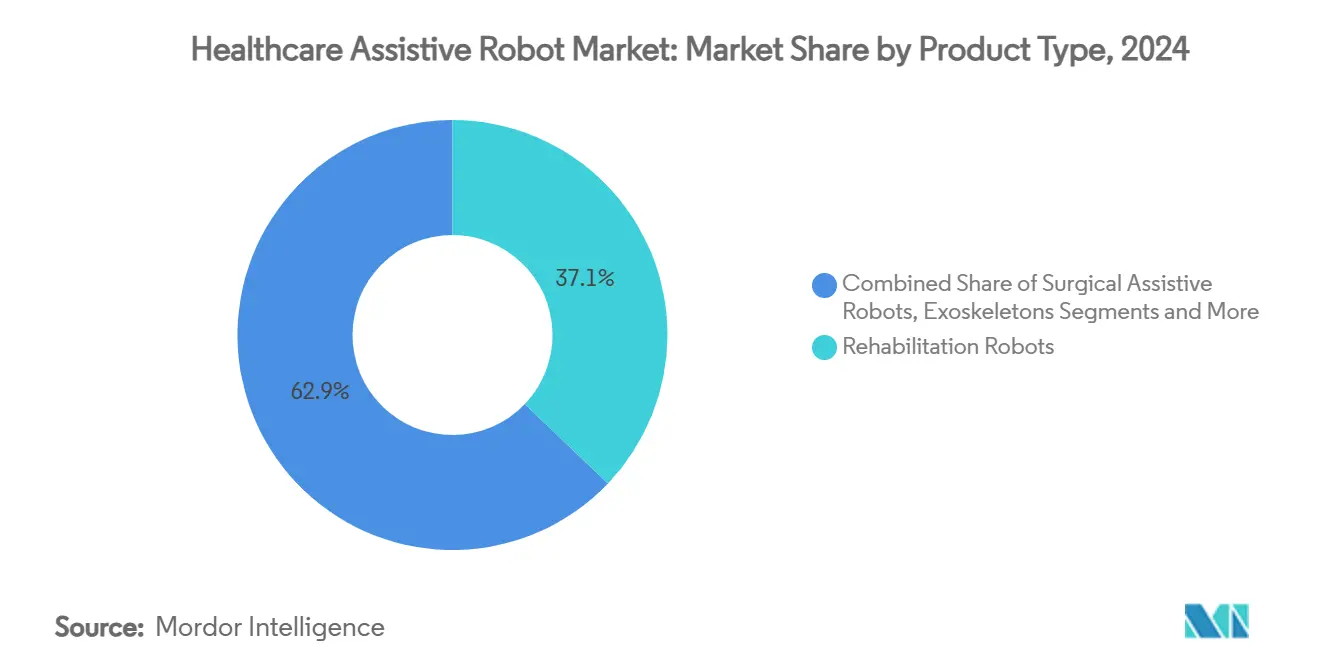

- By product type, rehabilitation robots led with 37.13% of Healthcare assistive robot market share in 2024. Exoskeletons are projected to expand at a 21.57% CAGR through 2030.

- By application, stroke rehabilitation accounted for 32.17% share of the Healthcare assistive robot market size in 2024.Home-based neuro-rehabilitation is set to rise at a 23.28% CAGR to 2030.

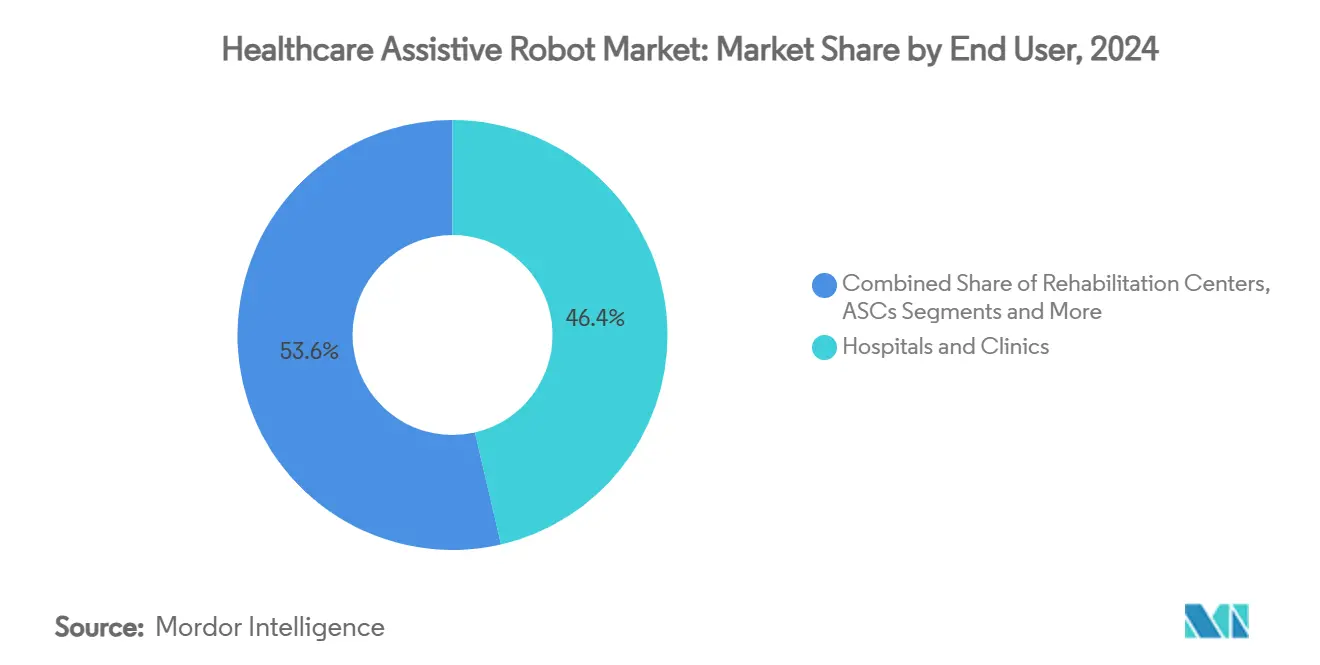

- By end user, hospitals and clinics held 46.38% of Healthcare assistive robot market share in 2024. Homecare settings are advancing at a 23.51% CAGR through 2030.

- By portability, wearable robots and exoskeletons commanded 42.36% share of the Healthcare assistive robot market size in 2024 and will register a 23.89% CAGR to 2030.

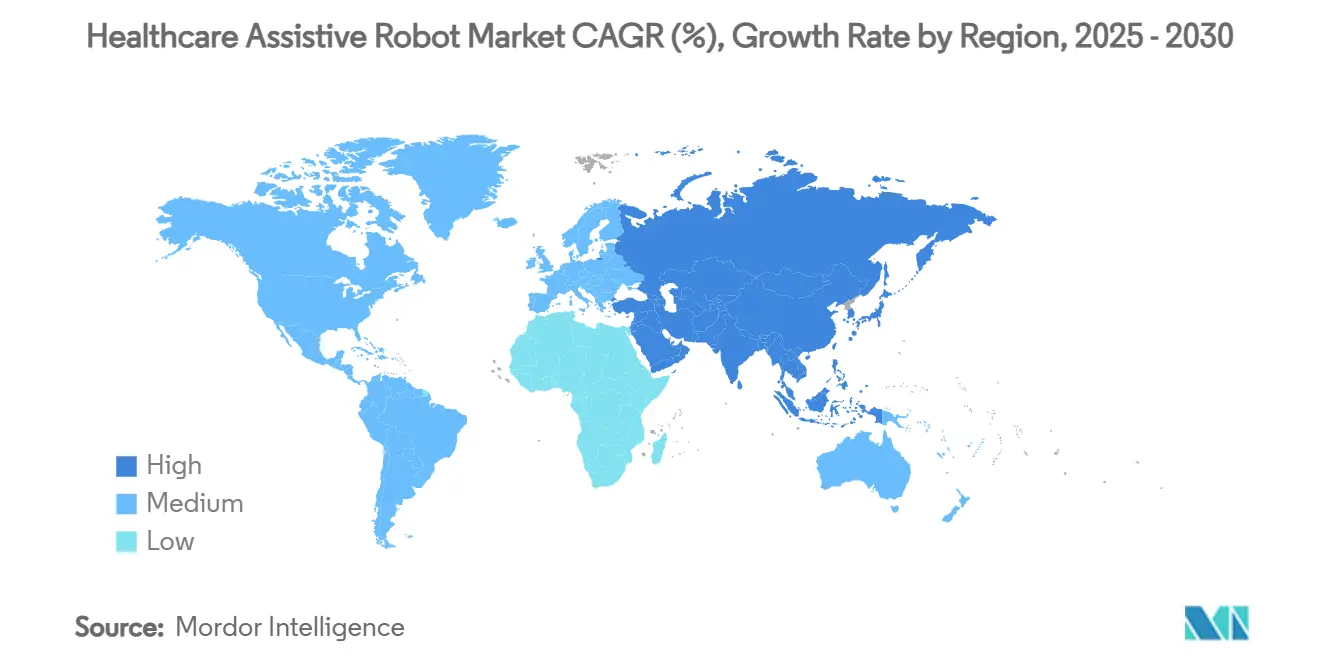

- By geography, North America dominated with 47.66% share in 2024, while Asia-Pacific is tracking a 21.26% CAGR through 2030.

Global Healthcare Assistive Robot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population driving demand for elder-care robots | +4.2% | Japan, Germany, Italy, other aging economies | Long term (≥ 4 years) |

| Rising stroke and spinal-cord injury cases boosting rehabilitation robotics | +3.8% | North America, EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-enabled precision improving surgical assistive robots | +3.1% | North America, Western Europe, global follow-through | Medium term (2-4 years) |

| Reimbursement pilots for at-home exoskeleton therapy | +2.9% | United States, pilot schemes in Canada, United Kingdom | Short term (≤ 2 years) |

| Value-based-care contracts favoring robotic assistive solutions | +2.7% | North America, Western Europe | Medium term (2-4 years) |

| Robot-as-a-Service lowering capital barriers | +2.1% | Early adoption in developed markets worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population Driving Demand For Elder-Care Robots

Global citizens aged 65+ total 771 million in 2024 and will reach 1.6 billion by 2050, creating a care gap that traditional staffing cannot fill. Japan allocated USD 1.2 billion in 2024 for robotic care programs, while China expects to need 50 million additional caregivers by 2040.[2]Ministry of Health, Labour and Welfare Japan, “Policy on Care and Welfare for the Elderly,” mhlw.go.jpElder-care robots cut institutional costs by 30-40% and support aging-in-place goals, which align with EU Horizon Europe funding of EUR 2.4 billion for age-tech through 2027. These demographic and fiscal realities make assistive robotics a necessity rather than a discretionary upgrade.

Rising Stroke & Spinal-Cord Injury Cases Boosting Rehabilitation Robotics

Stroke incidence has climbed 70% since 2000, producing 15 million new global cases each year. In the United States 7 million individuals live with post-stroke disabilities, and annual spinal cord injury cases reach 17,000.[3]American Heart Association, “Heart Disease and Stroke Statistics 2024,” heart.org Robotic therapy delivers 40% superior functional gains over conventional methods, prompting the U.S. Department of Veterans Affairs to invest USD 180 million in 2024 for robotic rehab centers. Insurers have begun reimbursing such systems, reflecting confidence in both clinical outcomes and long-term cost savings.

AI-Enabled Precision Improving Surgical Assistive Robots

FDA clearance of the da Vinci 5 in 2024 introduced machine-learning guidance that reduces complication rates by 23% compared with earlier models. Johnson & Johnson’s USD 3.4 billion acquisition of Auris underscored the strategic value of AI-guided navigation. Natural-language planning and computer-vision feedback now allow surgeons to adjust decisions in real time, lower fatigue and enhance standardization across varying skill levels.

Reimbursement Pilots For At-Home Exoskeleton Therapy

Medicare began covering ReWalk Personal 6.0 and Ekso GT devices for qualified users in 2024, removing the chief economic hurdle for equipment costing more than USD 100,000. Private insurers followed suit, and pilot programs launched in Canada and the United Kingdom. Clinical data show 60% reduction in secondary complications and 45% quality-of-life improvement, giving actuaries evidence needed to broaden coverage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital cost | -2.8% | Global, especially emerging markets | Short term (≤ 2 years) |

| Safety and liability regulatory uncertainties | -2.1% | Global, differing frameworks | Medium term (2-4 years) |

| Shortage of robot-literate allied-health workforce | -1.9% | Rural and underserved regions worldwide | Long term (≥ 4 years) |

| Cyber-security threats to networked robots | -1.6% | Developed markets with dense networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Cost

System prices ranging from USD 150,000 to USD 2.5 million strain hospital budgets still recovering post-pandemic. Emerging market buyers pay 40-60% extra after duties and currency swings, although leasing models spreading payments over seven years now gain momentum.

Safety & Liability Regulatory Uncertainties

AI functions evolve faster than rules. The EU Medical Device Regulation has lengthened approval cycles by up to 18 months and added USD 2-5 million in documentation expense. Liability insurance premiums are 35-50% higher for facilities deploying autonomous systems, reflecting unclear fault attribution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rehabilitation Robots Anchor Clinical Adoption

Rehabilitation platforms hold 37.13% of Healthcare assistive robot market share in 2024, reflecting strong evidence linking robotic therapy to functional gains. Hospitals value outcome data and allocate capital more readily to these systems than to socially assistive or humanoid devices. Exoskeletons, while still 2-digit market proportion, post a 21.57% CAGR through 2030 as lighter batteries, smarter actuators and Medicare coverage expand patient pools. Surgical assistive robots remain staple equipment for tertiary centers pursuing precision and shorter stay metrics. Telepresence and service robots accelerated after pandemic restrictions and are now permanent fixtures in infectious-disease wards. R&D convergence blurs product lines, with firms offering modular units that switch between rehab and mobility functions on a single chassis.

Growing clinical validation underpins payor acceptance, and software updates increasingly determine differentiation. Companies embed predictive analytics and cloud dashboards to monitor therapy adherence, which feeds quality-based reimbursement models. Interoperability with electronic health records further drives purchase decisions as providers avoid siloed data streams. The Healthcare assistive robot market has shifted from hardware-centric innovation toward integrated service ecosystems that include apps, analytics and clinician support.

By Application: Stroke Rehabilitation Dominates While Home-Based Care Surges

Stroke rehabilitation commands 32.17% of current demand, driven by high prevalence and proven therapy algorithms. Doctors quickly justify capital outlay when functional improvement translates to shorter inpatient stays. Home-based neuro-rehabilitation, however, registers the fastest 23.28% CAGR, because wearable systems let patients continue intensive therapy beyond discharge and align with value-based reimbursement. Surgical assistance maintains mid-teen growth as AI guidance improves cut-to-close times. Elderly activities-of-daily-living support grows steadily, backed by policy programs encouraging aging in place.

Telepresence and cognitive interaction applications gained momentum in memory-care facilities where staff shortages undermine resident engagement. Orthopedic rehabilitation integrates wearable sensors that push data to cloud analytics, letting therapists tailor protocols remotely. Application boundaries continue to blur as companies bundle multiple therapy modes into one platform, simplifying facility procurement and maximizing asset utilization. The Healthcare assistive robot market benefits from this convergence because buyers achieve wider clinical coverage from each purchase.

By End User: Hospitals Still Command Spend Yet Homecare Outpaces Growth

Hospitals and clinics control 46.38% share of 2024 revenue, reflecting their established capital budgets and concentration of complex cases. They remain the primary customers for surgical and high-end rehab systems that require specialized staff. Homecare settings, though smaller in base, see 23.51% CAGR as payors reimburse remote therapy and consumers favor treatment at home. Rehabilitation centers hold a stable slice by focusing on intensive multi-week programs. Ambulatory surgery centers adopt compact robotic arms designed for outpatient procedures, helping them boost throughput while meeting strict cost ceilings.

Value-based payment models encourage discharge to home with robotic support, so providers deploy remote dashboards that let clinicians adjust therapy intensity in real time. Partnerships between manufacturers and home-health agencies emerge to bundle device rental with nursing services. The Healthcare assistive robot market finds new demand nodes in these distributed care networks, spreading revenue sources beyond acute facilities.

By Portability: Wearable Solutions Lead Innovation and User Preference

Wearable exoskeletons represent 42.36% of 2024 revenue and post a 23.89% CAGR through 2030, demonstrating user preference for mobility and autonomy. Materials advances cut weight by 30% while extending battery lives to more than eight hours of continuous use, making daily living integration practical. Mobile autonomous robots retain importance inside hospitals for logistics tasks and patient transport, freeing staff for higher-value work. Stationary systems continue to dominate surgical theaters where absolute stability is paramount.

Manufacturers design modular platforms that let a clinic switch from over-ground gait training to seated upper-limb therapy by swapping attachments. The Healthcare assistive robot market benefits because providers reach diverse patient cohorts with single investments, improving return on capital and easing adoption hesitation.

Geography Analysis

North America leads the Healthcare assistive robot market with 47.66% share in 2024, supported by strong reimbursement frameworks and concentrated R&D funding. Hospitals invest in multi-functional robotic suites that reduce variability and help fulfill quality metrics tied to reimbursement. The United States also benefits from a robust venture ecosystem that funnels capital into AI software layers, enriching domestic supply chains.

Europe follows, propelled by coordinated research programs and increased elder-care spending. Horizon Europe grants subsidize pilot installations in Germany, France and the Nordics, accelerating clinical validation and standard-setting. National health systems negotiate volume-based discounts, pushing vendors to adopt agile pricing tiers that mix capital sales with service subscriptions.

Asia-Pacific, recording a 21.26% CAGR, is positioned to close the gap by 2030. Japan’s Society 5.0 earmarks USD 3.2 billion for healthcare robotics, aligning public funding with industry consortia to commercialize elder-care and rehabilitation models. China’s digital-health mandate requires large hospitals to integrate robotic assistance by 2026, stimulated by domestic manufacturers that leverage cost advantages to penetrate rural markets. Singapore’s national robotics road map functions as a regional showcase, attracting multinational trials and talent inflow.

Middle East and Africa remain early-stage but attract attention through sovereign health-care infrastructure projects that seek flagship robotic centers to draw medical tourism. South America sees selective adoption in premium private hospitals constrained by import tariffs and currency swings. Overall, varying policy regimes shape adoption velocity, yet fundamental drivers such as aging, chronic-disease prevalence and clinician shortages remain universal, ensuring long-term expansion of the Healthcare assistive robot market.

Competitive Landscape

The market is moderately fragmented, with the top five suppliers representing an estimated 38% combined share. Intuitive Surgical and Stryker anchor surgical segments through continuous iteration and service bundling. Cyberdyne, ReWalk Robotics and Ekso Bionics specialize in exoskeleton innovation, while multinational device makers pursue acquisitions to accelerate entry; Zimmer Biomet’s July 2025 purchase of Monogram Technologies exemplifies this strategy.

Horizontal integration characterizes 2024-2025 deals, as firms aim to offer cohesive ecosystems rather than isolated products. Vertical moves emerge through Robot-as-a-Service offerings that couple hardware, cloud analytics and maintenance into outcome-based contracts. Intellectual-property filings center on adaptive control algorithms, haptic feedback and safety redundancies, highlighting software as the next competitive battleground.

Smaller start-ups differentiate by focusing on underserved niches such as pediatric mobility or rural tele-rehab, partnering with regional distributors to circumvent high global marketing costs. Market barriers heighten as regulatory clarity and reimbursement norms crystallize, rewarding firms able to document clinical efficacy and sustain manufacturing scale. This environment propels gradual consolidation yet leaves space for specialist entrants who solve specific workflow pain points more nimbly than conglomerates.

Healthcare Assistive Robot Industry Leaders

Intuitive Surgical

Stryker Corp.

Medtronic plc

Cyberdyne Inc.

Ekso Bionics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Zimmer Biomet acquired Monogram Technologies for USD 177 million, expanding its orthopedic surgical robotics capabilities.

- March 2025: AlphaDroid unveiled AI-driven hospital service robots at the International Patient Safety Conference in New Delhi.

- August 2024: KARL STORZ completed the purchase of Asensus Surgical, integrating advanced robotic technology into its endoscopy portfolio.

Global Healthcare Assistive Robot Market Report Scope

| Rehabilitation Robots |

| Surgical Assistive Robots |

| Exoskeletons |

| Socially Assistive Robots |

| Humanoid Care Robots |

| Telepresence & Service Robots |

| Orthopedics & Mobility Rehab |

| Neurological Rehabilitation |

| Surgical Assistance |

| Elderly ADL Support |

| Cognitive & Social Interaction |

| Telepresence & Monitoring |

| Hospitals & Clinics |

| Rehabilitation Centers |

| Homecare Settings |

| Ambulatory Surgery Centers |

| Elderly Care Facilities |

| Mobile Autonomous Robots |

| Wearable Robots & Exoskeletons |

| Stationary / Fixed-base Robots |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Rehabilitation Robots | |

| Surgical Assistive Robots | ||

| Exoskeletons | ||

| Socially Assistive Robots | ||

| Humanoid Care Robots | ||

| Telepresence & Service Robots | ||

| By Application | Orthopedics & Mobility Rehab | |

| Neurological Rehabilitation | ||

| Surgical Assistance | ||

| Elderly ADL Support | ||

| Cognitive & Social Interaction | ||

| Telepresence & Monitoring | ||

| By End User | Hospitals & Clinics | |

| Rehabilitation Centers | ||

| Homecare Settings | ||

| Ambulatory Surgery Centers | ||

| Elderly Care Facilities | ||

| By Portability | Mobile Autonomous Robots | |

| Wearable Robots & Exoskeletons | ||

| Stationary / Fixed-base Robots | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast size of the Healthcare assistive robot market by 2030?

It is projected to reach USD 31.41 billion by 2030, advancing at a 19.84% CAGR.

Which product type currently holds the largest share?

Rehabilitation robots lead with 37.13% of 2024 revenue.

Which geography is growing fastest?

Asia-Pacific is expanding at a 21.26% CAGR through 2030.

Why are exoskeletons gaining attention?

Medicare reimbursement, lighter designs and improved batteries drive a 21.57% CAGR for exoskeletons.

How do Robot-as-a-Service models lower adoption barriers?

Subscription fees replace large upfront purchases and include software updates, maintenance and analytics.

What is the main restraint for emerging markets?

High upfront capital cost, amplified by import duties and currency volatility, slows adoption.

Page last updated on: