Pharmaceutical Robots Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

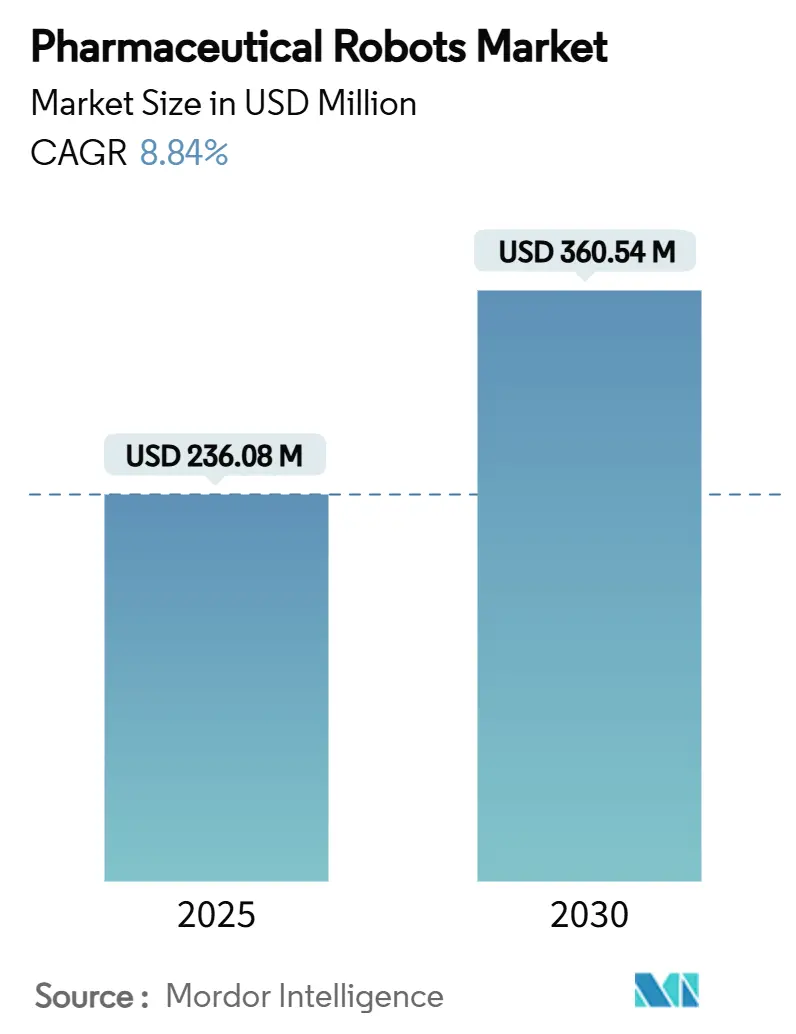

| Market Size (2025) | USD 236.08 Million |

| Market Size (2030) | USD 360.54 Million |

| Growth Rate (2025 - 2030) | 8.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Robots Market Analysis by Mordor Intelligence

The pharmaceutical robots market size stood at USD 236.08 million in 2025 and is forecast to reach USD 360.54 million by 2030, advancing at an 8.84% CAGR through the period. Robust adoption stems from manufacturers reshaping production around smaller, patient-specific batches, where automation guarantees sterility while keeping change-over times short. Early movers also cite faster regulatory reviews because modern robots produce granular audit trails that dovetail with data-integrity rules. Suppliers gain pricing power by bundling robots with validated software, sparing customers lengthy IQ/OQ/PQ cycles. In parallel, venture funding is flowing toward AI-enabled cobots that promise predictive maintenance and round-the-clock uptime, further reinforcing the investment thesis.

Key Report Takeaways

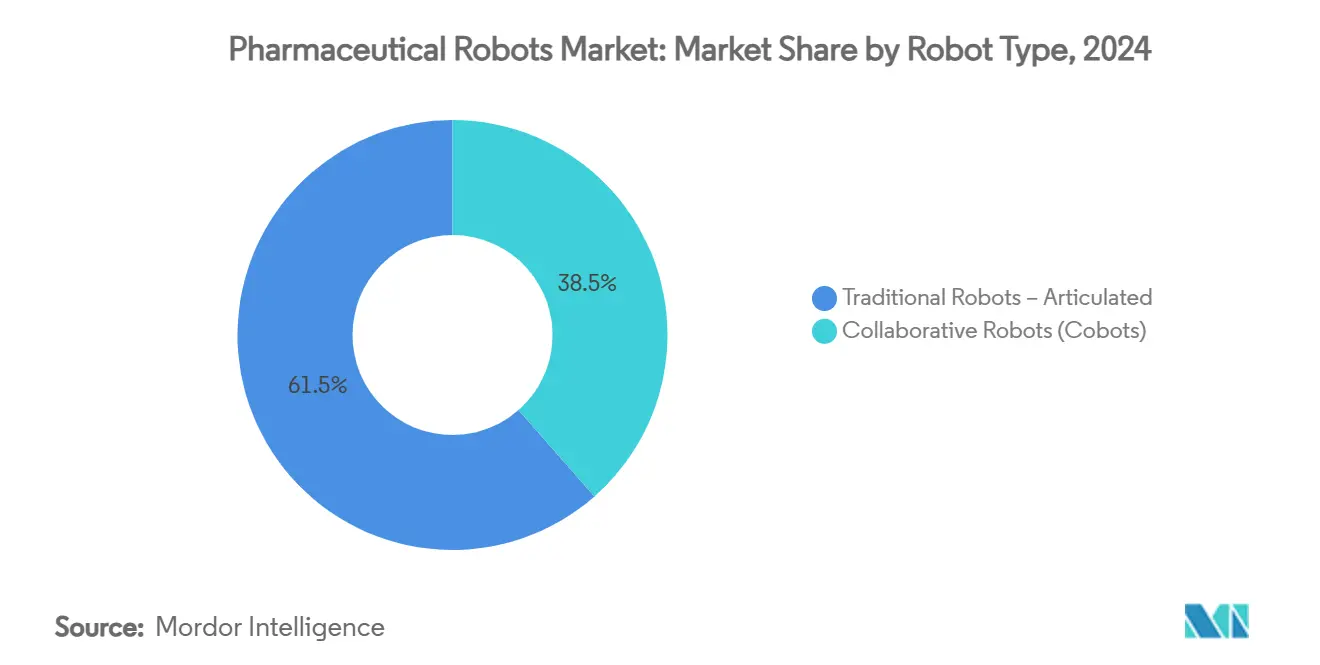

- By robot type, traditional articulated systems led with 61.48% of pharmaceutical robots market share in 2024, while collaborative robots are projected to expand at a 12.48% CAGR to 2030.

- By application, picking and packaging commanded 44.57% of the pharmaceutical robots market size in 2024, whereas aseptic fill-finish is advancing at an 11.63% CAGR through 2030.

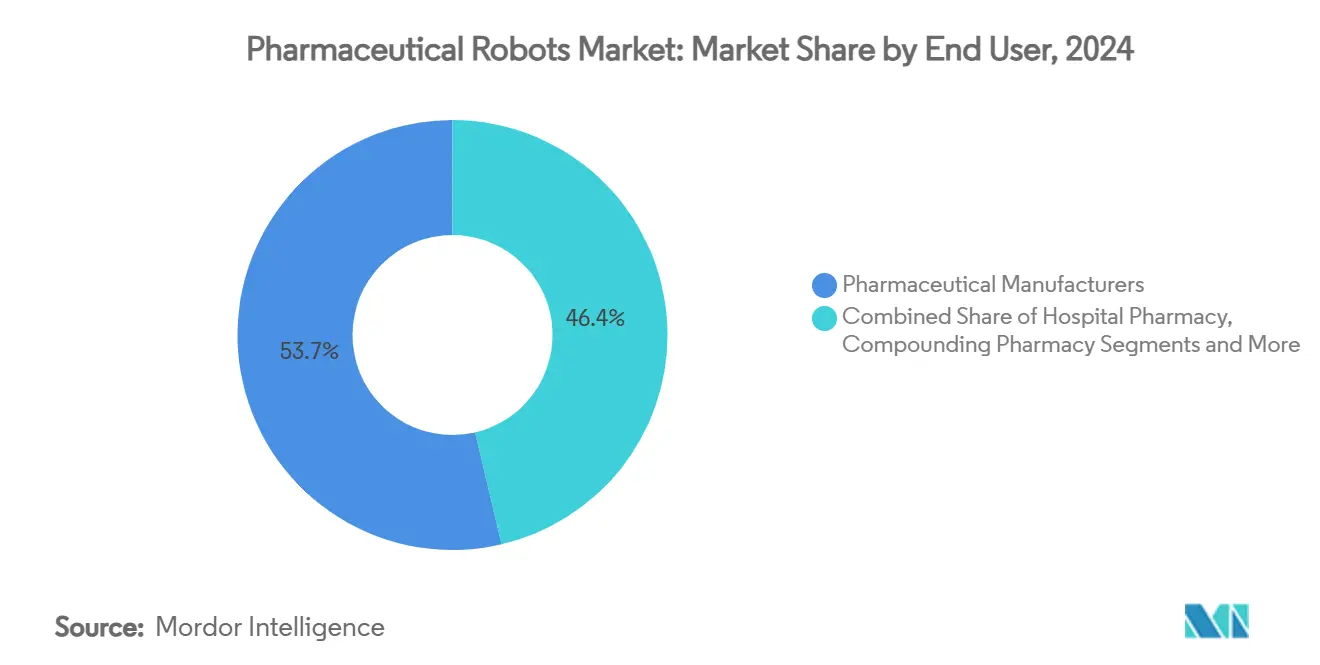

- By end user, pharmaceutical manufacturers held 53.65% share in 2024; contract manufacturing organizations record the fastest growth at a 10.06% CAGR to 2030.

- By payload capacity, the 5-15 kg band captured 34.68% revenue in 2024; the 15-30 kg range is projected to rise at an 11.79% CAGR to 2030.

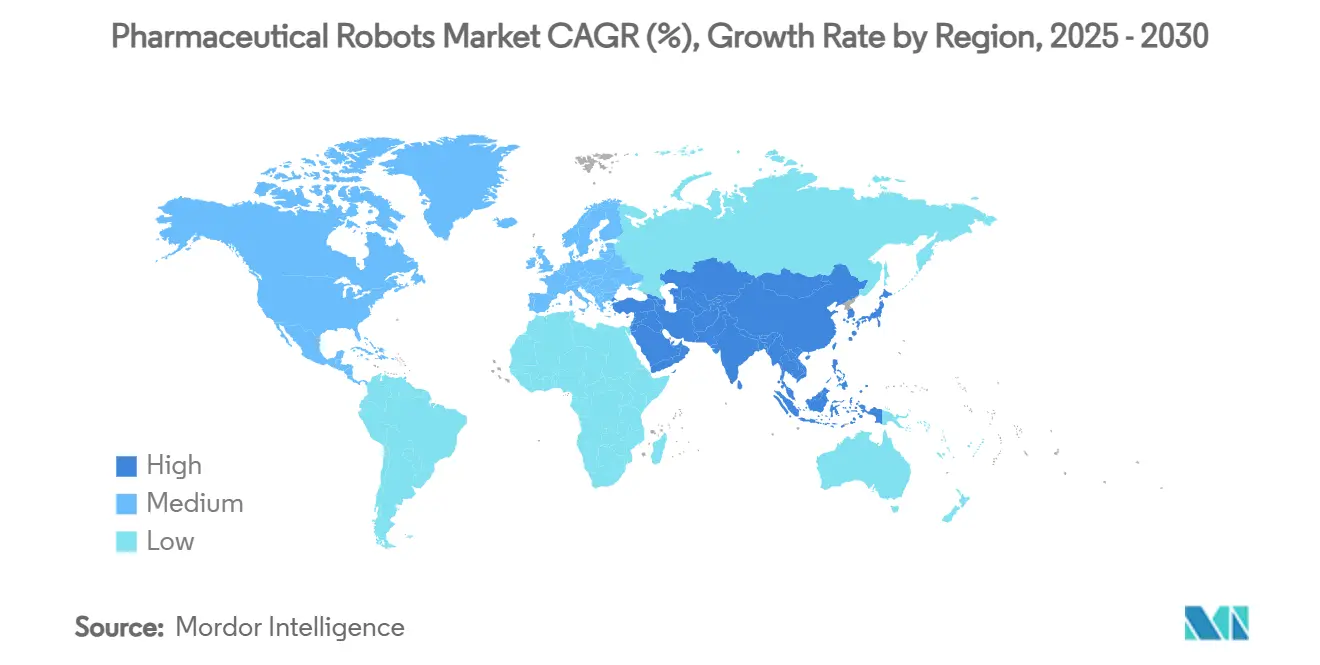

- By geography, North America accounted for 38.57% revenue in 2024, while Asia-Pacific is tracking a 10.74% CAGR through 2030.

Global Pharmaceutical Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift To Personalized, Small-Batch Drug Production | +2.1% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| COVID-19–Accelerated Demand For Contact-Free Fill-Finish Lines | +1.8% | Global, particularly North America & Europe | Short term (≤ 2 years) |

| Shrinking Skilled-Labor Pool In Aseptic Areas | +1.5% | Global, acute in North America & APAC | Long term (≥ 4 years) |

| Regulatory Moves Toward Annex 1 Rev. 12 Sterility Mandates | +1.3% | Europe core, spill-over to global markets | Medium term (2-4 years) |

| AI-Enabled Predictive Maintenance Reducing OEE Downtime | +1.0% | Global, advanced manufacturing regions | Long term (≥ 4 years) |

| Venture Funding Surge For Mobile Clean-Room Cobots | +0.7% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Personalized, Small-Batch Drug Production

Manufacturers pivoting to individualized medicines now require robotics that switch SKUs without hand tools, keeping class A/B cleanrooms sealed. Syntegon’s Versynta FFP line fills micro-vials with wastage under 1%, supporting high-value biologics where every milliliter counts. Bristol Myers Squibb’s collaboration with Cellares illustrates scale-out potential—40,000 automated batches a year versus the legacy 200-batch ceiling. Hospitals pilot point-of-care robots to mix therapies bedside, reducing supply-chain latency. Economic upside includes 60% lower material loss and premium price tags for bespoke treatments. The trend cements a multi-year demand runway for the pharmaceutical robots market.

COVID-19–Accelerated Demand for Contact-Free Fill-Finish Lines

The pandemic exposed contamination risks tied to glove-ports and manual transfer. Cytiva’s SA25 workcell isolates product with single-use flow-paths, satisfying Annex 1 and operating 24/7 without shift breaks. OEE gains near 25% versus hand-loaded lines, while Steriline’s robotic nest fillers cut container change-overs to minutes. As global vaccine programs wind down, pharma plants still prioritize no-touch technologies, embedding lasting demand inside the pharmaceutical robots market.

Shrinking Skilled-Labor Pool in Aseptic Areas

Eighty percent of bioprocess facilities report a skills mismatch, blending microbiology with digital control know-how.[1]ISPE, “Futureproofing US Pharma Manufacturing Jobs,” ispe.org ABB’s IRB 1300, deployed at MVZ Medizinische Labore Dessau Kassel, lifted throughput by 25% while shrinking staffing gaps. With AI projected to discover 30% of new molecules by 2025, demand for data-literate technicians will tighten. Robots become an operational hedge, ensuring capacity when people are scarce. The dynamic injects long-run momentum into the pharmaceutical robots market.

Regulatory Moves Toward Annex 1 Rev 12 Sterility Mandates

The 2023 revision drives a contamination-control mindset rooted in automation. Stäubli’s Sterimove mobile robot meets Grade A/B/D requirements, showcasing how suppliers redesign platforms to slot inside CCS frameworks. PIC/S adoption extends the rulebook beyond Europe, so multinationals align global sites early. Robots offer traceable datasets that inspectors trust, shortening audit cycles. Firms that automate ahead of peers gain reputational lift and smoother market releases, reinforcing the pharmaceutical robots market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Validation & IQ/OQ/PQ Costs For GxP Compliance | -1.9% | Global, particularly regulated markets | Medium term (2-4 years) |

| Cyber-Security Vulnerabilities In Networked Cobots | -1.2% | Global, acute in connected manufacturing | Long term (≥ 4 years) |

| Fragmented Global GMP Standards Prolong Approval Cycles | -0.8% | Global, regional variations | Long term (≥ 4 years) |

| Scarcity Of Open-Source Robot Programming Talent | -0.6% | Global, acute in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Validation & IQ/OQ/PQ Costs for GxP Compliance

Documentation overhead can exceed 40% of total project spend, extending roll-outs by 12-18 months. ARxIUM’s RIVA compounding robot ships with templated protocols, yet buyers still run exhaustive sterility tests to satisfy USP 797. Collaboration-ready platforms face dual scrutiny—safety sensing and aseptic control—multiplying the paperwork. Smaller firms defer purchases, impeding volume expansion for the pharmaceutical robots market.

Cyber-Security Vulnerabilities in Networked Cobots

Manufacturing ranks among top-three breached sectors, and pharma IP magnifies the stakes.[2]World Economic Forum, “Building a Culture of Cyber Resilience in Manufacturing,” weforum.orgLegacy OT links to corporate WANs create soft targets; if malware alters robot paths, batch integrity could fail silently. HMS Networks advises zero-trust segmentation, yet patching forces downtime that sterile suites can ill afford. Security anxiety slows procurement within the pharmaceutical robots market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robot Type: Collaborative Systems Drive Innovation

Traditional articulated models retained 61.48% of pharmaceutical robots market share in 2024 by excelling at payload-intensive palletizing and vial handling. Their long service history and validated enclosures reassure quality teams, sustaining replacement cycles. Yet cobots, projected to grow at 12.48% CAGR, are rewriting production layouts by eliminating hard guarding and shrinking cleanroom footprints.

The collaborative wave gathers pace in labs too, where a UR10e prepares assay plates beside scientists without breaching ISO-7 zoning. Epson’s 6 kg clean-compatible arm, due 2025, signals big-brand commitment to this sub-segment. These gains underpin a wider transition as the pharmaceutical robots market catches up with automotive peers on human-machine synergy.

By Application: Aseptic Processing Captures Premium Growth

Picking & packaging led with 44.57% revenue in 2024, illustrating the quick wins obtainable by replacing repetitive carton loading. However, aseptic fill-finish is set to clock an 11.63% CAGR on the back of Annex 1 sterility clauses that all but mandate enclosed robotics cytivalifesciences.com.

Laboratory automation also climbs as chemists chase cycle-time cuts: ABB and Agilent’s 2025 pact merges sample prep with in-line analysis new.abb.com. These multiple use-cases diversify risk and enlarge the pharmaceutical robots market size for solution vendors who can bundle tools into unified GMP platforms.

By End User: CMOs Accelerate Adoption Curve

Originator firms still commanded 53.65% revenue in 2024, anchoring early tech pilots. Yet CMOs are forecast to outpace the field at a 10.06% CAGR as sponsors off-load capacity spikes. Flexible robots that swap campaigns overnight let service providers serve multiple clients from one line, lifting asset utilization.

Research institutes and hospital pharmacies follow, deploying small-footprint compounding robots such as RIVA to assure dose accuracy in oncology wards. This cascading diffusion widens the pharmaceutical robots market and pressures laggards to automate or lose contracts.

By Payload Capacity: Mid-Range Arms Remain the Workhorse

Units rated 5-15 kg delivered 34.68% of revenue, ideal for vials, syringes and stoppered nests. FANUC’s M-410iB/140H illustrates the upper tier, stacking 140 kg pallets at 1,900 cycles per hour. Growth pivots to the 15-30 kg class, rising 11.79% CAGR as plants automate drum loading and buffer preparation.

Lightweight sub-5 kg delta robots thrive in high-speed blister lines, whereas ≥60 kg giants serve distribution hubs. The balancing act between precision and lift encourages modular platforms able to swap wrists, expanding upsell revenue inside the pharmaceutical robots market.

Geography Analysis

North America held 38.57% of 2024 turnover after regulators pushed real-time release and advanced-manufacturing designations that favor automation.[3]U.S. FDA, “Advanced Manufacturing Technologies Designation Program,” federalregister.gov U.S. firms alone earmarked USD 160 billion for new lines in 2025, with robotics ring-fenced to secure sterility and digital provenance. Canada’s biologics clusters and Mexico’s near-shoring corridors round out the region, creating integrated supply webs that anchor regional demand for the pharmaceutical robots market.

Asia-Pacific follows as the fastest climber, tracking a 10.74% CAGR. China upgrades legacy plants with SCARA pickers, Japan injects robotics know-how into niche cell-therapy workflows, and Singapore grants tax rebates on Industry-4.0 kits. India scales cleanrooms to win regulated-market filings, driving domestic automation buys.

Europe benefits from Annex 1 tailwinds and strong OEM ecosystems in Germany and Switzerland. Stäubli’s Sterimove launch underscores regional innovation that is diffusing across the continent. Meanwhile, Saudi Arabia and the UAE step up investment to diversify from hydrocarbons, revealing white-space potential for the pharmaceutical robots market.

Competitive Landscape

Competition remains moderate, with industrial automation titans and niche pharma specialists jostling for wallet share. ABB, Fanuc, and KUKA adapt proven arms with stainless casings and GMP firmware, leveraging global service fleets. Universal Robots and Stäubli court cleanroom buyers with ISO-5-certified cobots that can be validated faster than legacy guards.

Specialists such as Swisslog Healthcare and BD bundle domain-specific software that logs compounding data to Electronic Batch Records. Partnerships are the norm: ABB’s tie-ups with Mettler-Toledo and Agilent streamline lab flows, while Astellas and Yaskawa co-develop dual-arm cell-therapy platforms. Start-ups bring AI overlays, with Persist AI’s cloud-lab architecture winning early adopters.

Feature wars now orbit around auto-calibration, autonomous navigation, and predictive wear analytics. Suppliers that package these alongside pre-validated documentation ease regulatory burden, tilting tender scores in their favor. The dynamic shapes a pharmaceutical robots market where service, not hardware, drives recurring revenue.

Pharmaceutical Robots Industry Leaders

ABB Ltd.

Fanuc Corp.

Yaskawa Electric

Staubli Robotics

Universal Robots

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Epson unveiled its first collaborative robot aimed at life-science cleanrooms, featuring ISO-5 compliance and Python interfaces.

- May 2025: Persist AI secured USD 12 million Series A funding to expand its AI-driven robotic lab platform.

- March 2025: Astellas Pharma and Yaskawa Electric agreed to launch a cell-therapy manufacturing joint venture leveraging the Maholo dual-arm robot.

- January 2025: ABB Robotics and Agilent Technologies formed a collaboration to create automated laboratory solutions for pharma workflows.

Global Pharmaceutical Robots Market Report Scope

| Traditional Robots | Articulated Robots |

| SCARA Robots | |

| Cartesian Robots | |

| Delta Robots | |

| Collaborative Robots (Cobots) |

| Picking & Packaging |

| Inspection & QA Testing |

| Laboratory Automation |

| Aseptic Fill-Finish |

| Sterile Compounding |

| Material Handling & Palletizing |

| Pharmaceutical Manufacturers |

| Contract Manufacturing Organizations (CMOs) |

| Research & Academic Labs |

| Hospital Pharmacies |

| Compounding Pharmacies |

| Retail & Mail-order Pharmacies |

| Up to 5 kg |

| 5–15 kg |

| 15–30 kg |

| 30–60 kg |

| Above 60 kg |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Robot Type | Traditional Robots | Articulated Robots |

| SCARA Robots | ||

| Cartesian Robots | ||

| Delta Robots | ||

| Collaborative Robots (Cobots) | ||

| By Application | Picking & Packaging | |

| Inspection & QA Testing | ||

| Laboratory Automation | ||

| Aseptic Fill-Finish | ||

| Sterile Compounding | ||

| Material Handling & Palletizing | ||

| By End User | Pharmaceutical Manufacturers | |

| Contract Manufacturing Organizations (CMOs) | ||

| Research & Academic Labs | ||

| Hospital Pharmacies | ||

| Compounding Pharmacies | ||

| Retail & Mail-order Pharmacies | ||

| By Payload Capacity | Up to 5 kg | |

| 5–15 kg | ||

| 15–30 kg | ||

| 30–60 kg | ||

| Above 60 kg | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the pharmaceutical robots market expected to grow?

It is projected to expand from USD 236.08 million in 2025 to USD 360.54 million by 2030 at an 8.84% CAGR.

Which robot type is gaining the most momentum?

Collaborative robots are forecast to post a 12.48% CAGR, outpacing traditional articulated systems.

Why are CMOs investing heavily in automation?

Flexible robots let CMOs switch campaigns quickly, boosting utilization and fueling a 10.06% CAGR for this end-user group.

What geographic region will add the most new revenue?

Asia-Pacific is on track for a 10.74% CAGR, driven by Chinese capacity build-outs and Japanese technology leadership.

What is the main hurdle to faster adoption?

High validation costs—often 40% of project spend—extend deployment timelines by up to 18 months, slowing roll-outs.

Which payload class dominates installations?

Robots rated 5-15 kg captured 34.68% market revenue in 2024, aligning with vial and syringe handling tasks.

Page last updated on: